Bot Analyzer📌 Script Name: Bot Analyzer

This TradingView Pine Script v5 indicator creates a dashboard table on the chart that helps you analyze any asset for running a martingale grid bot on futures.

🔧 User Inputs

TP % (tpPct): Take Profit percentage.

SO step % (soStepPct): Step size between safety orders.

SO n (soCount): Number of safety orders.

M mult (martMult): Martingale multiplier (how much each next order increases in size).

Lev (leverage): Leverage used in futures.

BB len / BB mult: Bollinger Bands settings for measuring channel width.

ATR len: ATR period for volatility.

HV days: Lookback window (days) for Historical Volatility calculation.

📐 Calculations

ATR % (atrPct): Normalized ATR relative to price.

Bollinger Band width % (bbPct): Market channel width as percentage of basis.

Historical Volatility (hvAnn): Annualized volatility, calculated from daily log returns.

Dynamic Step % (dynStepPct): Step size for safety orders, automatically adjusted from ATR and clamped between 0.3% and 5%.

Covered Move % (coveredPct): Total percentage move the bot can withstand before last safety order.

Martingale Size Factor (sizeFactor): Total position size multiplier after all safety orders, based on martingale multiplier.

Risk Score (riskLabel): Simple risk estimate:

Low if risk < 30

Mid if risk < 60

High if risk ≥ 60

📊 Output (Table on Chart)

At the top-right of the chart, the script draws a table with 9 rows:

Metric Value

BB % Bollinger Band width in %

HV % Historical Volatility (annualized %)

TP % Take profit setting

SO step % Safety order step size

SO n Number of safety orders

M mult Martingale multiplier

Dyn step % Dynamic step based on ATR

Size x Total position size factor (e.g., 4.5x)

Risk Risk label (Low / Mid / High)

⚙️ Use Case

Helps choose coins for a martingale bot:

If BB% is wide and HV% is high → the asset is volatile enough.

If Risk shows "High" → parameters are aggressive, you may need to adjust step size, SO count, or leverage.

The dashboard lets you compare assets quickly without switching between multiple indicators.

Ciclos

Ark FCI OscillatorFinancial Conditions Index Oscillator

This indicator tracks week-over-week changes in the National Financial Conditions Index (NFCI), providing a dynamic view of evolving financial conditions in the United States.

Overview

The National Financial Conditions Index (NFCI) is a comprehensive weekly composite index published by the Federal Reserve Bank of Chicago. It measures financial conditions across U.S. money markets, debt and equity markets, and the traditional and shadow banking systems.

Interpretation

Positive values indicate improving financial conditions

Negative values signal deteriorating financial conditions

Risk assets demonstrate particular sensitivity to changes in financial conditions, making this oscillator valuable for market timing and risk assessment.

Alternative Data Source

Users can modify the source to FRED:NFCIRISK to focus specifically on risk dynamics. The NFCIRISK subindex isolates volatility and funding risk measures within the financial sector, capturing market volatility indicators and liquidity shortage probabilities while excluding broader credit and leverage conditions.

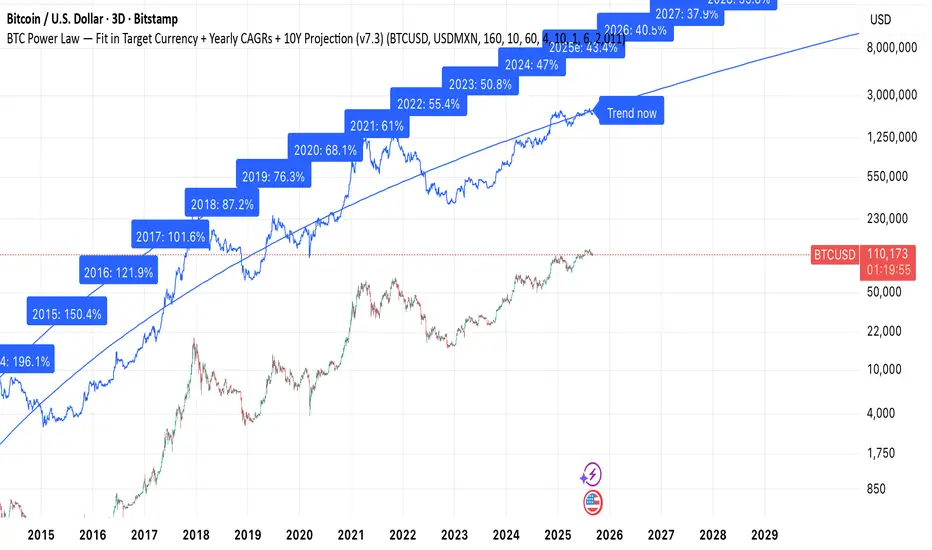

Preston Pysh - BTC Power Law in Any Fiat CurrencyThis tool helps a user understand what the power law suggests the expected annual CAGR is for any currency (can be adjusted in the settings). It also shows the project price (in said fiat currency) for the next ten years.

Niveles Anuales +-5% con PreciosNiveles calculados de % de precios según el precio de apertura anual

Cyclic Reversal Engine [AlgoPoint]Overview

Most indicators focus on price and momentum, but they often ignore a critical third dimension: time. Markets move in rhythmic cycles of expansion and contraction, but these cycles are not fixed; they speed up in trending markets and slow down in choppy conditions.

The Cyclic Reversal Engine is an advanced analytical tool designed to decode this rhythm. Instead of relying on static, lagging formulas, this indicator learns from past market behavior to anticipate when the current trend is statistically likely to reach its exhaustion point, providing high-probability reversal signals.

It achieves this by combining a sophisticated time analysis with a robust price-action confirmation.

How It Works: The Core Logic

The indicator operates on a multi-stage process to identify potential turning points in the market.

1. Market Regime Analysis (The Brain): Before analyzing any cycles, the indicator first diagnoses the current "personality" of the market. Using a combination of the ADX, Choppiness Index, and RSI, it classifies the market into one of three primary regimes:

- Trending: Strong, directional movement.

- Ranging: Sideways, non-directional chop.

- Reversal: An over-extended state (overbought/oversold) where a turn is imminent.

2. Adaptive Cycle Learning (The "Machine Learning" Aspect): This is the indicator's smartest feature. It constantly analyzes past cycles by measuring the bar-count between significant swing highs and swing lows. Crucially, it learns the average cycle duration for each specific market regime. For example, it learns that "in a strong trending market, a new swing low tends to occur every 35 bars," while "in a ranging market, this extends to 60 bars."

3. The Countdown & Timing Signal: The indicator identifies the last major swing high or low and starts a bar-by-bar countdown. Based on the current market regime, it selects the appropriate learned cycle length from its memory. When the bar count approaches this adaptive target, the indicator determines that a reversal is "due" from a timing perspective.

4. Price Confirmation (The Trigger): A signal is never generated based on timing alone. Once the timing condition is met (the cycle is "due"), the indicator waits for a final price-action confirmation. The default confirmation is the RSI entering an extreme overbought or oversold zone, signaling momentum exhaustion. The signal is only triggered when Time + Price Confirmation align.

How to Use This Indicator

- The Dashboard: The panel in the bottom-right corner is your command center.

- Market Regime: Shows the current market personality analyzed by the engine.

- Adaptive Cycle / Bar Count: This is the core of the indicator. It shows the target cycle length for the current regime (e.g., 50) and the current bar count since the last swing point (e.g., 45). The background turns orange when the bar count enters the "due zone," indicating that you should be on high alert for a reversal.

- BUY/SELL Signals: A label appears on the chart only when the two primary conditions are met:

The timing is right (Bar Count has reached the Adaptive Cycle target).

The price confirms exhaustion (RSI is in an extreme zone).

A BUY signal suggests a downtrend cycle is likely complete, and a SELL signal suggests an uptrend cycle is likely complete.

Key Settings

- Pivot Lookback: Controls the sensitivity of the swing point detection. Higher values will identify more significant, longer-term cycles.

- Market Regime Engine: The ADX, Choppiness, and RSI settings can be fine-tuned to adjust how the indicator classifies the market's personality.

- Require Price Confirmation: You can toggle the RSI confirmation on or off. It is highly recommended to keep it enabled for higher-quality signals.

交易区本地时间This is a practical timezone display indicator designed specifically for forex and global market traders, showing real-time current times of three major financial centers in a clear table format at the top-right corner of the chart: Tokyo, New York, and London.

✨ Key Features

🗾 Tokyo Time - Asian trading session reference

🗽 New York Time - American trading session reference

🏛️ London Time - European trading session reference

📅 Complete Date & Time - Display format: MM-DD HH:MM

🔄 Automatic DST - Smart handling of daylight saving time transitions

🎨 Color Coding - Different colors for different timezone identification

⚡ Real-time Updates - Based on current timestamp, accurate with no delay

💼 Use Cases

Forex Traders - Track major financial center opening/closing times

Global Market Analysis - Understand market activity across different timezones

News Trading - Master timing of important economic data releases

Multi-timezone Coordination - Time management tool for international investors

这是一个专为外汇和全球市场交易者设计的实用时区显示指标,在图表右上角以清晰的表格形式实时显示三大主要金融中心的当前时间:东京、纽约和伦敦。

✨ 主要功能

🗾 东京时间 - 亚洲交易时段参考

🗽 纽约时间 - 美洲交易时段参考

🏛️ 伦敦时间 - 欧洲交易时段参考

📅 完整日期时间 - 显示格式:MM-DD HH:MM

🔄 自动夏令时 - 智能处理冬令时/夏令时切换

🎨 色彩区分 - 不同颜色标识不同时区

⚡ 实时更新 - 基于当前时间戳,准确无延迟

💼 适用场景

外汇交易者 - 把握各大金融中心开盘收盘时间

全球市场分析 - 了解不同时区的市场活跃度

新闻交易 - 掌握重要经济数据发布时间

多时区协调 - 国际投资者的时间管理工具

Marubozu Detector with Dynamic SL/TP

Strategy Overview:

This indicator detects a "Marubozu" bullish pattern or a “Marubozu” bearish pattern to suggest potential buy and sell opportunities. It uses dynamic Stop Loss (SL) and Take Profit (TP) management, based on either market volatility (ATR) or liquidity zones.

This tool is intended for educational and informational purposes only.

Key Features:

Entry: Based on detecting Marubozu bullish or bearish candle pattern.

Exit: Targets are managed through ATR multiples or previous liquidity levels (swing highs or swing lows).

Smart Liquidity: Optionally identify deeper liquidity targets.

Full Alerts: Buy and Sell signals supported with customizable alerts.

Visualized Trades: Entry, SL, and TP levels are plotted on the chart.

User Inputs:

ATR Length, ATR Multipliers

Take Profit Mode (Liquidity/ATR)

Swing Lookback and Strength

Toggleable Buy/Sell alerts

All Time Frames

📖 How to Use:

Add the Indicator:

Apply the script to your chart from the TradingView indicators panel.

Look for Buy Signals:

A buy signal is triggered when the script detects a "Marubozu" bullish pattern.

Entry, Stop Loss, and Take Profit levels are plotted automatically.

Look for Sell Signals:

A Sell signal is triggered when the script detects a "Marubozu" bearish pattern.

Entry, Stop Loss, and Take Profit levels are plotted automatically.

Choose Take Profit Mode:

ATR Mode: TP is based on a volatility target.

Liquidity Mode: TP is based on past swing highs.

Set Alerts (Optional):

Enable Buy/Sell alerts in the settings to receive real-time notifications.

Practice First:

Always backtest and paper trade before live use.

📜 Disclaimer:

This script does not offer financial advice.

No guarantees of profit or performance are made.

Use in demo accounts or backtesting first.

Always practice proper risk management and seek advice from licensed professionals if needed.

✅ Script Compliance:

This script is designed in full accordance with TradingView’s House Rules for educational tools.

No financial advice is provided, no performance is guaranteed, and users are encouraged to backtest thoroughly.

Trading Sessions with Holidays & Timer🌍 Trading Sessions Matter

Markets breathe in cycles. When Tokyo, London, or New York steps in, liquidity shifts and price often reacts fast.

Example: New York closed BTC at $110K, and when traders woke up, the price was already $113K. That gap says everything about overnight pressure and the next move.

⚡ Indicator Features

✅ Session boxes (Tokyo, London, NY) with custom colors & time zones

✅ Open/close lines → spot gaps & momentum

✅ Average price per session → see where pressure builds

✅ Tick range → quick volatility check

✅ 🏖 Holiday markers → avoid false quiet markets

✅ Live status table → session OPEN / CLOSED + countdown timer

🚀 How to Use

Works on intraday timeframes (1m–4h)

Watch session opens/closes → liquidity shift points

Compare ranges & averages between Tokyo, London, NY

Use the timer to prep before the next wave

This tool helps you visualize the heartbeat of global markets session by session.

🔖 #BTCUSDT #Forex #TradingSessions #Crypto #DayTrading

4H Candles High and Lows (#1-6) UTC - Last 32h - Colored BlocksThis script creates horizontal rays on the high and low in a 4 Hour period.

Trend Score HTF (Raw Data) Pine Screener📘 Trend Score HTF (Raw Data) Pine Screener — Indicator Guide

This indicator tracks price action using a custom cumulative Trend Score (TS) system. It helps you visualize trend momentum, detect early reversals, confirm direction changes, and screen for entries across large watchlists like SPX500 using TradingView’s Pine Script Screener (beta).

⸻

🔧 What This Indicator Does

• Assigns a +1 or -1 score when price breaks the previous high or low

• Accumulates these scores into a real-time tsScore

• Detects early warnings (primed flips) and trend changes (confirmed flips)

• Supports alerts and labels for visual and automated trading

• Designed to work inside the Pine Screener so you can filter hundreds of tickers live

⸻

⚙️ Recommended Settings (for Beginners)

When adding the indicator to your chart:

Go to the “Inputs” tab at the top of the settings panel.

Then:

• Uncheck “Confirm flips on bar close”

• Check “Accumulate TS Across Flips? (ON = non-reset, OFF = reset)”

This setup allows you to see trend changes immediately without waiting for bar closes and lets the trend score build continuously over time, making it easier to follow long trends.

⸻

🧠 Core Logic

Start Date

Select a meaningful historical start date — for example: 2020-01-01. This provides long-term context for trend score calculation.

Per-Bar Delta (Δ) Calculation

The indicator scores each bar based on breakout behavior:

If the bar breaks only the previous high, Δ = +1

If it breaks only the previous low, Δ = -1

If it breaks both the high and low, Δ = 0

If it breaks neither, Δ = 0

This filters out wide-range or indecisive candles during volatility.

Cumulative Trend Score

Each bar’s delta is added to the running tsScore.

When it rises, bullish pressure is building.

When it falls, bearish pressure is increasing.

Trend Flip Logic

A bullish flip happens when tsScore rises by +3 from the lowest recent point.

A bearish flip happens when tsScore falls by -3 from the highest recent point.

These flips update the active trend direction between bullish and bearish.

⸻

⚠️ What Is a “Primed” Flip?

A primed flip is a signal that the current trend is about to flip — just one point away.

A primed bullish flip means the trend is currently bearish, but the tsScore only needs +1 more to flip. If the next bar breaks the previous high (without breaking the low), it will trigger a bullish flip.

A primed bearish flip means the trend is currently bullish, but the tsScore only needs -1 more to flip. If the next bar breaks the previous low (without breaking the high), it will trigger a bearish flip.

Primed flips are plotted one bar ahead of the current bar. They act like forecasts and give you a head start.

⸻

✅ What Is a “Confirmed” Flip?

A confirmed flip is the first bar of a new trend direction.

A confirmed bullish flip appears when a bearish trend officially flips into a new bullish trend.

A confirmed bearish flip appears when a bullish trend officially flips into a new bearish trend.

These signals are reliable and great for entries, trend filters, or reversals.

⸻

🖼 Visual Cues

The trend score (tsScore) line shows the accumulated trend strength.

A Δ histogram shows the daily price contribution: +1 for breaking highs, -1 for breaking lows, 0 otherwise.

A green background means the chart is in a bullish trend.

A red background means the chart is in a bearish trend.

A ⬆ label signals a primed bullish flip is possible on the next bar.

A ⬇ label signals a primed bearish flip is possible on the next bar.

A ✅ means a bullish flip just confirmed.

A ❌ means a bearish flip just confirmed.

⸻

🔔 Alerts You Can Use

The indicator includes these built-in alerts:

• Primed Bullish Flip — watch for possible bullish reversal tomorrow

• Primed Bearish Flip — watch for possible bearish reversal tomorrow

• Bullish Confirmed — official entry into new uptrend

• Bearish Confirmed — official entry into new downtrend

You can set these alerts in TradingView to monitor across your chart or watchlist.

⸻

📈 How to Use in TradingView Pine Screener

Step 1: Create your own watchlist — for example, SPX500

Step 2: Favorite this indicator so it shows up in the screener

Step 3: Go to TradingView → Products → Screeners → Pine (Beta)

Step 4: Select this indicator and choose a condition, like “Bullish Confirmed”

Step 5: Click Scan

You’ll instantly see stocks that just flipped trends or are close to doing so.

⸻

⏰ When to Use the Screener

Use this screener after market close or before the next open to avoid intraday noise.

During the day, if a candle breaks both the high and low, the delta becomes 0, which may cancel a flip or primed signal.

Results during regular trading hours can change frequently. For best results, scan during stable periods like pre-market or after-hours.

⸻

🧪 Real-World Examples

SWK

NVR

WMT

UNH

Each of these examples shows clean, structured trend transitions detected in advance or confirmed with precision.

PLTR: complicated case primed for bullish (but we don't when it will flip)

⚠️ Risk Disclaimer & Trend Context

A confirmed bullish signal does not guarantee an immediate price increase. Price may continue to consolidate or even pull back after a bullish flip.

Likewise, a primed bullish signal does not always lead to confirmation. It simply means the conditions are close — but if the next bar breaks both the high and low, or breaks only the low, the flip will be canceled.

On the other side, a confirmed bearish signal does not mean the market will crash. If the overall trend is bullish (for example, tsScore has been rising for weeks), then a bearish flip may just represent a short-term pullback — not a trend reversal.

You always need to consider the overall market structure. If the long-term trend is bullish, it’s usually smarter to wait for bullish confirmation signals. Bearish flips in that context are often just dips — not opportunities to short.

This indicator gives you context, not predictions. It’s a tool for alignment — not absolute outcomes. Use it to follow structure, not fight it.

Shade 4H Blocks PSTShades a 4H timeframe intraday. The purpose is to remind me what 4H candle I am operating in without having to manually mark it on the lower-timeframe charts I am watching.

4H Weekly Candle Counter - Increments from Sunday until Friday This script will count the first 4H candle close on Sunday all the way until the final candle of the week on Friday.

4H Weekly Candle Counter (UTC - Dynamic)Counts the 4H Candles on a given trading day. Made specifically for the /ES. (The first 4H Candle opens at 15:00 Sunday-Thursday)

🟥 Synthetic 10Y Real Yield (US10Y - Breakeven)This script calculates and plots a synthetic U.S. 10-Year Real Yield by subtracting the 10-Year Breakeven Inflation Rate (USGGBE10) from the nominal 10-Year Treasury Yield (US10Y).

Real yields are a core macro driver for gold, crypto, growth stocks, and bond pricing, and are closely monitored by institutional traders.

The script includes key reference lines:

0% = Below zero = deeply accommodative regime

1.5% = Common threshold used by macro desks to evaluate gold upside breakout conditions

📈 Use this to monitor macro shifts in real-time and front-run capital flows during major CPI, NFP, and Fed events.

Update Frequency: Daily (based on Treasury market data)

Swing Oracle Stock// (\_/)

// ( •.•)

// (")_(")

📌 Swing Oracle Stock – Professional Cycle & Trend Detection Indicator

The Swing Oracle Stock is an advanced market analysis tool designed to highlight price cycles, trend shifts, and key trading zones with precision. It combines trendline dynamics, normalized oscillators, and multi-timeframe confirmation into a single comprehensive indicator.

🔑 Key Features

NDOS (Normalized Dynamic Oscillator System):

Measures price strength relative to recent highs and lows to detect overbought, neutral, and oversold zones.

Dynamic Trendline (EMA8 or SMA231):

Flexible source selection for adapting to different trading styles (scalping vs. swing).

Multi-Timeframe H1 Confirmation:

Adds higher-timeframe validation to improve signal reliability.

Automated Buy & Sell Signals:

Triggered only on significant crossovers above/below defined levels.

Weekly Cycles (7-day M5 projection):

Tracks recurring time-based market cycles to anticipate reversal points.

Intuitive Visualization:

Colored zones (high, low, neutral) for quick market context.

Optional background and candlestick coloring for better clarity.

Multi-Timeframe Cross Table:

Automatically compares SMA50 vs. EMA200 across multiple timeframes (1m → 4h), showing clear status:

⭐️⬆️ UP = bullish trend confirmation

💀⬇️ Drop = bearish trend confirmation

📊 Built-in Statistical Tools

Normalized difference between short and long EMA.

Projected normalized mean levels plotted directly on the main chart.

Dynamic analysis of price distance from SMA50 to capture market “waves.”

🎯 Use Cases

Spot trend reversals with multi-timeframe confirmation.

Identify powerful breakout and breakdown zones.

Time entries and exits based on trend + cycle confluence.

Enhance market timing for swing trades, scalps, or long-term positions.

⚡ Swing Oracle Stock brings together cycle detection, oscillator normalization, and multi-timeframe confirmation into one streamlined indicator for traders who want a professional edge.

Composite Sentiment Indicator (SPY/QQQ/SOXX + VixFix)# Multi-Index Composite Sentiment Indicator

A comprehensive sentiment indicator that works across SPY, QQQ, SOXX, and custom symbols. Combines volatility, options flow, macro factors, technicals, and seasonality into a single z-score composite.

## What It Does

Takes multiple market sentiment inputs (VIX, put/call ratios, breadth, yields, etc.) and smooshes them into one normalized line. When the composite is high = markets getting spooked. When it's low = markets getting complacent.

## Key Features

- **Multi-Index Support**: Automatically adapts for SPY (uses VIX), QQQ (uses VXN), SOXX (uses VixFix), or custom symbols

- **VixFix Integration**: Larry Williams' VixFix for indices without dedicated VIX measures

- **Signal MA**: Choose from SMA/EMA/WMA/HMA/TEMA/DEMA with color coding (red above MA = risk-on, green below = risk-off)

- **September Focus**: Built-in seasonality weighting for September weakness patterns

- **Comprehensive Components**: Volatility, options sentiment, macro factors, technicals, and sector-specific metrics

## How to Use

**Basic Setup:**

1. Pick your index (SPY/QQQ/SOXX)

2. Choose signal MA type and length (EMA 21 is a good start)

3. Watch for extreme readings and MA crossovers

**Color Signals:**

- Red composite = above signal MA = bearish sentiment

- Green composite = below signal MA = bullish sentiment

- Extreme high readings (red background) = potential tops

- Extreme low readings (green background) = potential bottoms

**For Different Indices:**

- **QQQ**: Uses NASDAQ VIX (VXN) when available, falls back to VixFix

- **SOXX**: Includes semiconductor cycle indicators, uses VixFix for volatility

- **Custom**: Adapts automatically, relies on VixFix and general market metrics

## Components Included

**Volatility**: VIX/VXN/VixFix, term structure, historical vol

**Options**: Put/call ratios, SKEW index

**Macro**: DXY, 10Y yields, yield curve, TIPS spreads

**Technical**: RSI deviation, momentum

**Seasonality**: September effects, quad witching, month-end patterns

**Breadth**: S&P 500 and NASDAQ breadth measures

## Pro Tips

- Works well on Daily Timeframe

- September gets extra weight automatically - watch for August setup signals

- Keltner envelope breaks often mark sentiment exhaustion points

- Use alerts for extreme readings and MA crossovers

Works best when you understand that sentiment extremes often mark turning points, not continuation signals. High readings don't mean "keep shorting" - they mean "start looking for reversal setups."

## Settings Worth Tweaking

- Signal MA type/length for your timeframe

- Component weights based on what matters for your index

- Envelope multipliers for your risk tolerance

- VixFix parameters if default doesn't fit your symbol's volatility

The table shows all current component readings so you can see what's driving the signal. Good for context and debugging weird readings.

Monthly MA Box for S&P 500 or othersThis moving average helps detect when the asset is undervalued or overvalued. Users can adjust the spread between the moving averages.

US Elections Democrate-Republicain (1920-2025)This script shows the different U.S. presidents and indicates whether each was Democratic or Republican. It allows users to analyze the market based on the president in office.

15-Min EMA CrossoverVery useful swing setup indicator that can be used in different styles of trading

Works on any timeframe but calculates EMA and cross signals based on 15-minute candles.

Plots the EMA line.

Shows green triangle for bullish crossover and red triangle for bearish crossunder.

Session Levels [odnac]This indicator plots the high and low levels of the three main trading sessions—Asia, Europe, and New York—along with the previous day’s high, low, and open. Each session’s time range can be customized using a UTC offset, and the indicator automatically tracks session highs and lows as price develops.

Functions:

Plots session highs and lows for Asia, Europe, and New York.

Shows previous day’s high, low, and open as reference levels.

Session times are fully configurable with hour and minute precision, including UTC offset adjustment.

Each session level is marked with both a line and a label for clarity.

Color customization for each session and previous day levels.

Designed for intraday timeframes (1–60 minutes).

Filter Condition:

When the filter option is enabled, the indicator adjusts how levels are drawn:

A session high above the current close is displayed as a solid line with a visible label.

Once price closes above that high, the line becomes dotted and dimmed, and the label also becomes less emphasized.

Similarly, a session low below the current close is displayed as a solid line and label.

If price closes below that low, the line switches to dotted and dimmed, with the label adjusted accordingly.

This behavior highlights only the most relevant levels for the current market position while still keeping breached levels visible in a subdued style, making it easier to spot active breakout or liquidity zones.

Sunset Zones by PDVDescription

Sunset Zones by PDV is an intraday reference indicator that plots key horizontal levels based on selected “root candles” throughout the trading day. At each programmed time, the indicator identifies the high and low of the corresponding candle and projects those levels forward with extended lines, providing traders with a clean visual framework of potential intraday reaction zones.

These zones serve as reference levels for support, resistance, liquidity grabs, and session context, allowing traders to analyze how price reacts around time-specific structures. Unlike lagging indicators, Sunset Zones gives traders real-time, rule-based levels tied directly to the price action of specific moments in the session.

Key Features

Predefined Time Codes

The script comes with a curated list of intraday timestamps (in HHMM format). Each represents a “root candle” from which levels are generated. Examples include 03:12, 06:47, 07:41, 08:51, etc. These time codes can reflect historically important market moments such as session opens, liquidity sweeps, or volatility inflection points.

Automatic Zone Plotting

At each root time, the script captures the candle’s high and low and instantly extends those levels forward across the chart. This provides consistent, objective reference points for intraday trading.

Extended Lines

Levels are projected far into the future (default: 500 bars) so traders can easily track how price interacts with those zones throughout the day.

Color-Coded Levels

Each root time is assigned a distinct color for fast identification. For example:

03:12 → Fuchsia

06:47 → Purple

07:41 → Teal

08:51 → White

09:53 → White

10:20 → Orange

11:10 → Green

11:49 → Red

12:05 → White

13:05 → Teal

14:09 → Aqua

This helps traders quickly recognize which time-of-day level price is interacting with.

Lightweight & Visual

The indicator focuses purely on price and time, avoiding complexity or lagging signals. It can be layered with other analysis tools, order flow charts, or session-based studies.

Practical Use Cases

Intraday Bias:

Observe whether price respects, rejects, or consolidates around these reference levels to form a bias.

Liquidity Zones:

High/low sweeps of the root candle can act as liquidity pools where institutions might trigger stops or reversals.

Support & Resistance:

Extended lines create intraday S/R zones without the need to manually draw levels.

Confluence Finder:

Combine Sunset Zones with VWAP, session ranges, Fibonacci levels, or higher-timeframe structure for layered confluence.

Important Notes

This is a visual reference tool only. It does not generate buy or sell signals.

Default times are provided, but the concept is flexible — traders can adapt it by modifying or expanding the list of time codes.

Works best on intraday timeframes where session structure is most relevant (e.g., 1-minute to 15-minute charts).

✅ In short: Sunset Zones by PDV gives intraday traders a systematic way to anchor their charts to important time-based highs and lows, creating a consistent framework for analyzing price reactions across the day.

Gronk-Style Lunar Cycle Projection (fixed 30m base)Based on the lunar cycle timing provided by Gronko Polo - A Bromance in Finance