Ratchet Exit Trend Strategy with VIX FilterThis strategy is a trend-following system designed specifically for volatile markets. Instead of focusing solely on the "perfect entry," this script emphasizes intelligent trade management using a custom **"Ratchet Exit System."**

Additionally, it integrates a volatility filter based on the CBOE Volatility Index (VIX) to minimize risk during extreme market phases.

### 🎯 The Concept: Ratchet Exit

The "Ratchet" system operates like a mechanical ratchet tool: the Stop Loss can only move in one direction (up, for long trades) and "locks" into specific stages. The goal is to give the trade "room to breathe" initially to avoid being stopped out by noise, then aggressively reduce risk as the trade moves into profit.

The exit logic moves through 3 distinct phases:

1. **Phase 0 (Initial Risk):** At the start of the trade, a wide Stop Loss is set (Default: 10%) to tolerate normal market volatility.

2. **Phase 1 (Risk Reduction):** Once the trade reaches a specific floating profit (Default: +10%), the Stop Loss is raised and "pinned" to a fixed value (Default: -8% from entry). This drastically reduces risk while keeping the trade alive.

3. **Phase 2 (Trailing Mode):** If the trend extends to a higher profit zone (Default: +15%), the Stop switches to a dynamic Trailing Mode. It follows the **Highest High** at a fixed percentage distance (Default: 8%).

### 🛡️ VIX Filter & Panic Exit

High volatility is often the enemy of trend-following strategies.

* **Entry Filter:** The system will not enter new positions if the VIX is above a user-defined threshold (Default: 32). This helps avoid entering "falling knife" markets.

* **Panic Exit:** If the VIX spikes above the threshold (32) while a trade is open, the position is closed immediately to protect capital (Emergency Exit).

### 📈 Entry Signals

The strategy trades **LONG only** and uses Simple Moving Averages (SMAs) to identify trends:

* **Golden Cross:** SMA 25 crosses over SMA 50.

* **3-Bar Breakouts:** A confirmation logic where the price must close above the SMA 50, 100, or 200 for 3 consecutive bars.

### ⚙️ Settings (Inputs)

All parameters are fully customizable via the settings menu:

* **SMAs:** Lengths for the trend indicators (Default: 25, 50, 100, 200).

* **VIX Filter:** Toggle the filter on/off and adjust the panic threshold.

* **Ratchet Settings:** Percentages for Initial Stop, Trigger Levels for Stages 1 & 2, and the Trailing Distance.

### ⚠️ Technical Note & Risk Warning

This script uses `request.security` to fetch VIX data. Please ensure you understand the risks associated with trading leveraged or volatile assets. Past performance is not indicative of future results.

Indicadores y estrategias

G-BOT ENGULFING CANDLE - FIXED SL & TP // Description:

This Pine Script strategy identifies bullish and bearish engulfing candle patterns over a defined lookback period and places trades based

on recent market highs and lows. It calculates stop loss and take profit levels using the Average True Range (ATR) multiplied by a user-defined factor, with the ability to adjust the risk-to-reward ratio for each trade.

CDC Action Zone V.2 strategy — Updated v6Making a profit with a candlestick structure compared to the MA course 25 line with nine intersecting to find. Buy in the market.

First Fvg Strategy with CHoCH Exits, Adaptive TP & Entry TimerA strategy that is purely based off of prices reaction to the first presented fair value gap at 9:30 market open. Works best on NASDAQ one minute timeframe. Experimental indicator for me to back test first presented fair value gap.

Smart Bottom Catcher @ Le DReversal strategy using recent lowest lows and a fast RSI. Long entries trigger on extreme drops, exits occur when RSI crosses a set threshold. Includes optional SMA55 filter and allows up to 3 pyramids.

GOLD EMA Crossover Strategy This EMA Crossover Strategy is designed for intraday trading on the 5-minute chart.

It uses three EMAs (fast, mid, slow) to identify momentum shifts and trigger long or short entries. Risk management is dollar-based, with default settings of $100 risk per trade and $300 profit target. Entries are taken when the fast EMA crosses above/below the mid or slow EMA, with stops and targets calculated dynamically. The strategy runs across all hours and uses fixed position sizing (default 3 contracts). It is intended as a framework for traders to adapt and optimize to their own instruments and risk preferences.

Dual MTF Confirmed Trend Strategy (5m Entry / 15m MACD & RSI) v1That is a detailed Dual Multi-Timeframe (MTF) Confirmed Trend Strategy written in Pine Script for TradingView. The core idea of this strategy is to only take entry signals on a faster timeframe (5-minute) when the trend is strongly confirmed on a slower, higher timeframe (15-minute). This aims to reduce false signals and trade in the direction of the dominant trend. Here is an explanation of how the strategy works, broken down by section:

1. 5-Minute Entry Filters 🚀This section calculates several indicators on the current 5-minute chart to identify potential trade setups. A position is only considered if all 5-minute conditions align.

Supertrend: A trend-following indicator based on Average True Range (ATR).

Long Condition: The closing price must be above the Supertrend line.

Short Condition: The closing price must be below the Supertrend line.

Gann Hi-Lo (GHL): A trend indicator using Simple Moving Averages (SMA) of the high and low prices. GHL Line: Switches between the SMA of the Highs and the SMA of the Lows based on price action.

Long Condition: The closing price must be above the GHL line.

Short Condition: The closing price must be below the GHL line.

Exponential Moving Averages (EMAs): It uses a 50-period EMA and a 100-period EMA to confirm the short-term trend direction.

Long Condition: The closing price must be above both the 50 EMA and the 100 EMA.

Short Condition: The closing price must be below both the 50 EMA and the 100 EMA.

2. 15-Minute MTF Confirmation Filters ⏳This is the crucial step where the strategy verifies the trend on the slower, 15-minute timeframe using the request security function. This step acts as a gatekeeper to ensure the 5-minute trade aligns with the larger trend.

MACD Histogram (12, 26, 9): The difference between the MACD Line and the Signal Line.

Long Confirmation: The 15m MACD Histogram must be greater than 0 (MACD line is above the Signal line, indicating bullish momentum).

Short Confirmation: The 15m MACD Histogram must be less than 0 (MACD line is below the Signal line, indicating bearish momentum).

RSI (Relative Strength Index) (14): A momentum oscillator. The 50 level is often used to determine the general market trend.

Long Confirmation: The 15m RSI must be greater than 50 (indicating stronger bullish momentum).

Short Confirmation: The 15m RSI must be less than 50 (indicating stronger bearish momentum).

The Total 15m Confirmation is only true if both the MACD and the RSI confirmation signals align.

3. Trade Orders (Entry Logic) ⚖️

The strategy only executes a trade when the 5-minute entry conditions are met AND the 15-minute confirmation conditions are met.

Final Long Condition:

5m Conditions (Supertrend, GHL, EMA alignment) AND

15m Confirmation (MACD Hist > 0 AND RSI > 50)

Final Short Condition:

5m Conditions (Supertrend, GHL, EMA alignment) AND

15m Confirmation (MACD Hist < 0 AND RSI < 50)

When a trade signal is generated, the strategy:

Closes any opposite position (e.g., closes a "Short" trade if a "Long" signal appears).

Enters the new position (e.g., enters a "Long" trade).

This is designed as a reversal strategy where a new entry automatically closes the previous opposing trade.

In Summary

The strategy operates on a principle of Trend Alignment:

5-Minute Chart: Is used for Signal Timing (when exactly to enter the market).

15-Minute Chart: Is used for Trend Validation (is the overall market momentum supporting the signal?).

It's an attempt to capture short-term moves (5m signals) that are backed by strong medium-term momentum (15m confirmation), thereby aiming for higher probability trades.

This is not investment advice; it is recommended to perform optimization and backtesting for the assets intended for implementation.

BTC BRD – Bullet-Proof Reversal StrategyBTC BRD – Bullet-Proof Reversal Strategy is a price-action based reversal system that turns your existing “Bullet-Proof Reversal Detector” into a fully backtestable TradingView strategy with built-in risk management. It is designed to catch clean swing reversals using pure market structure, then automatically place stop-loss and take-profit orders based on your preferred risk-reward settings.

## Core concept

The strategy identifies true swing highs and lows using pivots and then waits for a clear market structure shift before entering any trade. It looks for a higher low followed by a break of structure for longs, and a lower high followed by a break of structure for shorts, helping filter out many random spikes and fakeouts. This makes it suitable for traders who prefer clean, rule-based entries grounded in market structure rather than noisy, indicator-heavy setups.

## Entries and exits

- Long trades are triggered after a bullish higher-low plus a confirmed break above the last swing high.

- Short trades are triggered after a bearish lower-high plus a confirmed break below the last swing low.

- Every position is protected with an automatic stop-loss and a calculated take-profit, so each trade has a predefined risk and reward from the moment it is opened.

## Risk management

The strategy lets you control your risk with a configurable risk-reward ratio (RR) and flexible stop-loss options. You can choose between an ATR-based stop (ATR × multiplier) or a fixed percentage stop relative to the entry price. Once the stop distance is known, the take-profit level is automatically derived from your RR value, making trade sizing and evaluation more consistent across different pairs and timeframes.

## Use cases and recommendations

This script is ideal for swing and intraday traders who want to systematically test market-structure reversals on assets like Bitcoin or other volatile instruments. For best results, experiment with different timeframes and ATR/percentage settings, and always validate performance using the Strategy Tester before deploying it on live markets. Remember that no strategy is guaranteed to be profitable, so use proper risk management and adapt settings to your own style and risk tolerance.

Retracement Strategy [OmegaTools]Retracement Strategy is a systematic trend–retracement framework designed to identify directional opportunities after a confirmed momentum shift, and to manage exits using either trend reversals or overextension conditions. It is built around a smoothed RSI regime filter and a simple, price-based retracement trigger, making it applicable across a wide range of markets and timeframes while remaining transparent and easy to interpret.

The strategy begins by defining the underlying trend through a two-stage RSI signal. A standard RSI is computed over the user-defined Length input, then smoothed with a short moving average to reduce noise. Two symmetric thresholds are derived from the Threshold parameter: an upper band at 100 minus the threshold and a lower band at the threshold itself. When the smoothed RSI crosses above the upper band, the environment is classified as bullish and the internal trend state is set to uptrend. When the smoothed RSI crosses below the lower band, the environment is classified as bearish and the trend state becomes downtrend. When RSI moves back into the central zone between the two bands, the trend is considered neutral. In addition to the current trend, the strategy tracks the last non-neutral trend direction, which is used to detect genuine trend changes rather than transient oscillations.

Once a trend is established, the strategy looks for retracement entries in the direction of that trend. For long setups in an uptrend, it computes the lowest low over the previous Length minus one bars, excluding the current bar. A long signal is generated when price dips below this recent low while the trend state remains bullish. Symmetrically, for short setups in a downtrend, it computes the highest high over the previous Length minus one bars and enters short when price spikes above this recent high while the trend state remains bearish. This logic is designed to capture pullbacks against the prevailing RSI-defined trend, entering when the market tests or slightly violates recent extremes, rather than chasing breakouts. The candles are visually coloured to reflect the detected trend, highlighting bullish and bearish environments while keeping neutral phases distinguishable on the chart. An ATR-based measure is used solely to position the “UP” and “DN” labels on the chart for clearer visualisation of entry points; it does not directly influence position sizing or stop calculation in this implementation.

Take profit and stop loss behaviour are fully parameterized through the “Take Profit” and “Stop Loss” inputs, each offering three modes: None, Trend Change and Extension. When “Trend Change” is selected for the take profit, the strategy will only exit profitable positions when a confirmed trend reversal occurs. For a long position, this means that the strategy will close the trade when the trend state flips from uptrend to downtrend, and the last recorded trend direction validates that this is a genuine reversal rather than a neutral fluctuation; the same logic applies symmetrically for short positions. When “Extension” is selected as the take profit mode, the strategy closes profitable long trades when the smoothed RSI reaches or exceeds the upper threshold, interpreted as an overbought extension within the bullish regime, and closes profitable short trades when the smoothed RSI falls to or below the lower threshold, interpreted as an oversold extension within the bearish regime. When “None” is chosen, the strategy does not apply any explicit take profit logic, leaving trades to be managed by the stop loss settings or by user discretion in backtesting.

The stop loss parameter works in a parallel way. With “Trend Change” selected as stop loss, any open long position is closed when the trend flips from uptrend to downtrend, regardless of whether the trade is currently in profit or loss, and any open short is closed when the trend flips from downtrend to uptrend. This turns the RSI trend regime into a hard invalidation rule: once the underlying momentum structure reverses, the position is exited. With “Extension” selected for stop loss, long positions are closed when RSI falls back below the upper band and moves towards the opposite side of the range, while short positions are closed when RSI rises above the lower band and moves towards the upper side. In practice, this acts as a dynamic exit based on the oscillator moving out of a favourable context for the existing trade. Selecting “None” for stop loss disables these automatic exits, leaving only the take profit logic, if any, to manage the position. Because take profit and stop loss configuration are independent, the user can construct different profiles, such as pure trend-change exits on both sides, pure overextension exits, or a mix (for example, take profit on overextension and stop loss on trend reversal).

This strategy is designed as an analytical and backtesting framework rather than a finished plug-and-play trading system. It does not include position sizing, risk-per-trade controls, multi-timeframe confirmation, volatility filters or instrument-specific fine-tuning. Its primary purpose is to provide a clear, rule-based structure for testing retracement logic within RSI-defined trends, and to allow users to explore how different exit regimes (trend-change based versus extension based) affect performance on their instruments and timeframes of interest.

Nothing in this script or its description should be interpreted as financial advice, investment recommendation or solicitation to buy or sell any financial instrument. Past performance on backtests does not guarantee future results. The behaviour of this strategy can vary significantly across symbols, timeframes and market conditions, and correlations, volatility and liquidity can change without warning. Before considering any live application, users should thoroughly backtest and forward test the strategy on their own data, adjust parameters to their risk profile and instrument characteristics, and integrate proper money management and trade management rules. Use of this script is entirely at the user’s own risk.

ETHUSDT 4H - Keltner Breakout working nice with ETH above EMA200

Using Keltner bands to prevent get rid off unnecessary noices . Works at safe side

Which is fantastic for people who does not want to stick to screen full day , it needs as couple of transactions per month to gain meaningfull profit

Do not forget to use it with 4 hr time frame

Do not recommend to use it with sh*tcoins, however with a small fine tuning its okay to use it with Top altcoins

Stratégie SMC V18.2 (BTC/EUR FINAL R3 - Tendance)This strategy is an automated implementation of Smart Money Concepts (SMC), designed to operate on the Bitcoin/Euro (BTC/EUR) chart using the 15-minute Timeframe (M15).It focuses on identifying high-probability zones (Order Blocks) after a confirmed Break of Structure (BOS) and a Liquidity Sweep, utilizing an H1/EMA 200 trend filter to only execute trades in the direction of the dominant market flow.Risk management is strict: every trade uses a fixed Risk-to-Reward Ratio (R:R) of 1:3.🧱 Core Logic Components

1. Trend Filter (H1/EMA 200)Objective: To avoid counter-trend entries, which has allowed the success rate to increase to nearly $65\%$ in backtests.Mechanism: A $200$-period EMA is plotted on a higher timeframe (Default: H1/60 minutes).Long (Buy): Entry is only permitted if the current price (M15) is above the trend EMA.Short (Sell): Entry is only permitted if the current price (M15) is below the trend EMA.

2. Order Block (OB) DetectionA potential Order Block is identified on the previous candle if it is

accompanied by an inefficiency (FVG - Fair Value Gap).

3. Advanced SMC ValidationBOS (Break of Structure): A recent BOS must be confirmed by breaking the swing high/low defined by the swing length (Default: 4 M15 candles).Liquidity (Liquidity Sweep): The Order Block zone must have swept recent liquidity (defined by the Liquidity Search Length) within a certain tolerance (Default: $0.1\%$).Point of Interest: The OB must form in a premium zone (for shorts) or a discount zone (for longs) relative to the current swing range (above or below the $50\%$ level of the range).

4. Execution and Risk ManagementEntry: The trade is triggered when the price touches the active Order Block (mitigation).Stop Loss (SL): The SL is fixed at the low of the OB (for longs) or the high of the OB (for shorts).Take Profit (TP): The TP is strictly set at a level corresponding to 3 times the SL distance (R:R 1:3).Lot Sizing: The trade quantity is calculated to risk a fixed amount (Default: 2.00 Euros) per transaction, capped by a Lot Max and Lot Min defined by the user.

Input Parameters (Optimized for BTC/EUR M15)Users can adjust these parameters to modify sensitivity and risk profile. The default values are those optimized for the high-performing backtest (Profit Factor $> 3$).ParameterDescriptionDefault Value (M15)Long. Swing (BOS)Candle length used to define the swing (and thus the BOS).4Long. Recherche Liq.Number of candles to scan to confirm a liquidity sweep.7Tolérance Liq. (%)Price tolerance to validate the liquidity sweep (as a percentage of price).0.1Timeframe TendanceChart timeframe used for the EMA filter (e.g., 60 = H1).60 (H1)Longueur EMA TendancePeriods used for the trend EMA.200Lot Max (Quantité Max BTC)Maximum quantity of BTC the strategy is allowed to trade.0.01Lot Min Réel (Exigence Broker)Minimum quantity required by the broker/exchange.0.00001

DJ BTC DailyThis Strategy only works on BTC daily. The only concern is the low winrate that could be a psycological hurdle. Please do comment for adjustments I should try and incorprate and let's find a killer strategy together :-)

50 & 200 SMA + RSI Average Strategy (Long Only, Single Trade)It works better in trending markets. It delivers its best performance in the 4-hour to 1-day timeframes.

Turtle Momentum StrategyTurtle momentum strategy as per Momentum Trading Strategy article on Substack (Nov 26, 2025)

EMA 12-26-100 Momentum Strategy# Triple EMA Multi-Signal Momentum Strategy

## 📊 Overview

**Triple EMA Multi-Signal** is a comprehensive trend-following momentum strategy designed specifically for cryptocurrency markets. It combines multiple technical indicators and signal types to identify high-probability trading opportunities while maintaining strict risk management protocols.

The strategy excels in trending markets and uses adaptive position sizing with trailing stops to maximize profits during strong trends while protecting capital during choppy conditions.

## 🎯 Core Algorithm

### Triple EMA System

The strategy employs a three-layer EMA system to identify trend direction and strength:

- **Fast EMA (12)**: Quick response to price changes

- **Slow EMA (26)**: Confirmation of trend direction

- **Trend EMA (100)**: Overall market bias filter

Trades are only taken when all three EMAs align in the same direction, ensuring we trade with the dominant trend.

### Multi-Signal Confirmation (8 Signal Types)

The strategy requires at least 1-2 confirmed signals from multiple independent sources before entering a position:

1. **EMA Crossover** - Fast EMA crossing Slow EMA (primary signal)

2. **MACD Cross** - MACD line crossing signal line (momentum confirmation)

3. **RSI Reversal** - RSI bouncing from oversold/overbought zones

4. **Price Action** - Strong bullish/bearish candles (>60% of range)

5. **Volume Spike** - Above-average volume confirmation

6. **Breakout** - Price breaking 20-period high/low with volume

7. **Pullback to EMA** - Trend continuation after healthy retracement

8. **Bollinger Bounce** - Price bouncing from BB bands

This multi-signal approach significantly reduces false signals and improves win rate.

## 💰 Risk Management

### Position Sizing

- Default: 20-25% of equity per trade

- Adjustable based on risk tolerance

- Smaller positions recommended for leveraged trading

### Stop Loss & Take Profit

- **Stop Loss**: 2.0% (tight control of risk)

- **Take Profit**: 5.5% (2.75:1 reward-to-risk ratio)

- Both levels are fixed at entry to avoid emotional decisions

### Trailing Stop System

- Activates after 1.8% profit

- Trails at 1.3% below current price

- Locks in profits during extended trends

- Automatically adjusts as price moves in your favor

### Maximum Hold Time

- 36-48 hours maximum (configurable)

- Designed to minimize funding rate costs on futures

- Forces position closure to avoid excessive exposure

- Helps maintain capital velocity

## 📈 Key Features

### Trend Filters

- **ADX Filter**: Ensures sufficient trend strength (threshold: 20)

- **EMA Alignment**: All three EMAs must confirm trend direction

- **RSI Boundaries**: Avoids extreme overbought/oversold entries

### Volume Analysis

- Volume must exceed 20-period moving average

- Configurable multiplier (default: 1.0x)

- Helps identify institutional participation

### Automatic Exit Conditions

1. Take Profit target reached

2. Stop Loss triggered

3. Trailing stop activated

4. Trend reversal (EMA cross in opposite direction)

5. Maximum hold time exceeded

## 🎮 Recommended Settings

### For Spot Trading (Conservative)

```

Position Size: 15-20%

Stop Loss: 2.5%

Take Profit: 6.0%

Max Hold: 72 hours

Leverage: 1x

```

### For Futures 3-5x Leverage (Balanced)

```

Position Size: 12-15%

Stop Loss: 2.0%

Take Profit: 5.5%

Max Hold: 36 hours

Trailing: Active

```

### For Aggressive Trading 5-10x (High Risk)

```

Position Size: 8-12%

Stop Loss: 1.5%

Take Profit: 4.5%

Max Hold: 24 hours

ADX Filter: Disabled

```

## 📊 Performance Metrics

### Backtested Results (BTC/USDT 1H, 2 years)

- **Total Return**: ~19% (spot) / ~75% (5x leverage)*

- **Total Trades**: 240-300

- **Win Rate**: 49-52%

- **Profit Factor**: 1.25-1.50

- **Max Drawdown**: ~18-22%

- **Average Trade**: 0.5-3 days

*Leverage results exclude funding rates and real-world slippage

### Optimal Timeframes

- **1 Hour**: Best for active trading (recommended)

- **4 Hour**: More stable, fewer signals

- **15 Min**: High frequency (requires monitoring)

### Best Performing Assets

- BTC/USDT (most tested)

- ETH/USDT

- Major altcoins with good liquidity

- Not recommended for low-cap or illiquid pairs

## ⚙️ How to Use

1. **Add to Chart**: Apply strategy to 1H BTC/USDT chart

2. **Adjust Settings**: Configure risk parameters based on your preference

3. **Review Signals**: Green = Long, Red = Short, labels show signal count

4. **Monitor Performance**: Check strategy tester for detailed statistics

5. **Optimize**: Use strategy optimization to find best parameters for your market

## 🎨 Visual Indicators

The strategy provides clear visual feedback:

- **EMA Lines**: Blue (Fast), Red (Slow), Orange (Trend)

- **BUY/SELL Labels**: Show entry points with signal count

- **Stop/Target Lines**: Red (SL), Green (TP) displayed during active trades

- **Background Color**: Light green (long), light red (short) when in position

- **Info Panel**: Shows current trend, RSI, ADX, and volume status

## ⚠️ Important Notes

### Risk Disclaimer

- This strategy is for educational purposes only

- Past performance does not guarantee future results

- Cryptocurrency trading involves substantial risk

- Only trade with capital you can afford to lose

- Always use proper position sizing and risk management

### Limitations

- Performs poorly in sideways/choppy markets

- Requires sufficient liquidity for best execution

- Backtests do not include:

- Real-world slippage (especially during volatility)

- Funding rates (for perpetual futures)

- Exchange downtime or connection issues

- Emotional trading decisions

### For Futures Trading

If using this strategy on futures with leverage:

- Reduce position size proportionally to leverage

- Account for funding rates (~0.01% per 8h)

- Set max hold time to minimize funding costs

- Use lower leverage (3-5x max recommended)

- Monitor liquidation price carefully

## 🔧 Customization

All parameters are fully customizable:

- EMA periods (fast/slow/trend)

- MACD settings (12/26/9)

- RSI levels (30/70)

- Stop Loss / Take Profit percentages

- Trailing stop activation and offset

- Volume multiplier

- ADX threshold

- Maximum hold time

## 📚 Strategy Logic

The strategy follows this decision tree:

```

1. Check Trend Direction (EMA alignment)

↓

2. Scan for Entry Signals (8 types)

↓

3. Confirm with Filters (ADX, Volume, RSI)

↓

4. Enter Position with Fixed SL/TP

↓

5. Monitor for Exit Conditions:

- TP Hit → Close with profit

- SL Hit → Close with loss

- Trailing Active → Follow price

- Trend Reversal → Close position

- Max Time → Force close

```

## 🎓 Best Practices

1. **Start Conservative**: Use smaller position sizes initially

2. **Track Performance**: Monitor actual vs backtested results

3. **Optimize Regularly**: Market conditions change, adapt parameters

4. **Combine with Analysis**: Don't rely solely on automated signals

5. **Manage Emotions**: Stick to the system, avoid manual overrides

6. **Paper Trade First**: Test on demo before risking real capital

## 📞 Support & Updates

This strategy is actively maintained and updated based on:

- Market condition changes

- User feedback and suggestions

- Performance optimization

- Bug fixes and improvements

## 🏆 Conclusion

Triple EMA Multi-Signal Strategy offers a robust, systematic approach to cryptocurrency trading by combining trend following, momentum indicators, and strict risk management. Its multi-signal confirmation system helps filter false signals while the trailing stop mechanism captures extended trends.

The strategy is suitable for both manual traders looking for high-probability setups and algorithmic traders seeking a proven systematic approach.

**Remember**: No strategy wins 100% of the time. Success comes from consistent application, proper risk management, and continuous adaptation to changing market conditions.

---

*Version: 1.0*

*Last Updated: November 2025*

*Tested on: BTC/USDT, ETH/USDT (1H, 4H timeframes)*

*Recommended Capital: $5,000+ for optimal position sizing*

Absorption PROOF - Absorption PRO (Clean & Smart)Ultra-clean, high-precision absorption reversal strategy.Detects institutional buying/selling pressure using volume-weighted delta proxy and VWAP deviation zones.Smart RSI + early-session range filter automatically separates valid range-bound reversals from trend exhaustion.Green/Red circles → High-probability entries (fully tradable)

Small crosses + colored zones → Rejected signals (avoid)

Blue dotted lines → Session range ±100% deviation levels (optional)

By default: only signals and rejection zones displayed — zero clutter.Minimalist, professional, and deadly accurate on futures & forex (1m–15m).Less noise. Better trades.

A+ Setup Strategy Trendline Features Added:

1. Automatic Trendline Detection

Support Trendline (green) - Connects swing lows

Resistance Trendline (red) - Connects swing highs

Uses pivot points to identify key swing levels

Validates trendlines by counting touches (minimum 3 touches required)

2. Trendline Settings

Show Trendlines - Toggle on/off

Lookback Period - How far back to look for pivots (default: 50 bars)

Min Touches - How many touches needed for valid trendline (default: 3)

3. Trendline Break Detection

Bullish Break - Price breaks above support trendline (marked with small green circle)

Bearish Break - Price breaks below resistance trendline (marked with small red circle)

Generates signals when breaks occur

4. Enhanced A+ Setups

Now includes ULTRA setups - the absolute best trades:

ULTRA BUY Setup (Aqua label):

Bullish FVG + BOS + Volume Spike + Uptrend

PLUS: Support trendline break OR near key support

PLUS: Trendline breakout confirmation

ULTRA SELL Setup (Fuchsia label):

Bearish FVG + BOS + Volume Spike + Downtrend

PLUS: Resistance trendline break OR near key resistance

PLUS: Trendline breakdown confirmation

5. Confluence Integration

The strategy now considers price near trendlines as additional confluence, similar to how it uses daily S/R levels.

6. Additional Alerts

Support Trendline Break

Resistance Trendline Break

ULTRA BUY/SELL Setup alerts

This gives you multiple tiers of signal quality:

Standard A+ Setup - All conditions met

ULTRA A+ Setup - All conditions + trendline break (highest probability)

The trendlines will help you identify major trend reversals and breakouts for even better entry timing!

Long-Term Strategy: 1-Year Breakout + 6-Month ExitDescripción (Description): (Copia y pega todo lo que está dentro del recuadro de abajo)

Description

This is a long-term trend-following strategy designed to capture major market moves while filtering out short-term noise. It is based on the classic principle of "buying strength" (Breakouts) and allowing profits to run, while cutting losses when the medium-term trend reverses.

How it Works (Logic)

1. Entry Condition (Long Only): The strategy looks for a significant display of strength. It enters a Long position only when two conditions are met simultaneously:

Price Breakout: The closing price exceeds the highest high of the last 252 trading days (approximately 1 year). This ensures we are entering during a strong momentum phase.

Trend Filter: The SuperTrend indicator (Settings: ATR 10, Factor 3.0) must be bullish. This acts as a confirmation filter to avoid false breakouts in choppy markets.

2. Exit Condition: The strategy uses a trailing stop based on price action, not a fixed percentage.

It closes the position when the price closes below the lowest low of the last 126 trading days (approximately 6 months).

This wide exit allows the trade to "breathe" during normal market corrections without exiting the position prematurely.

Settings & Risk Management

Capital Usage: The script is configured to use 10% of equity per trade to reflect realistic risk management (compounding).

Commissions: Included at 0.1% to simulate real trading costs.

Slippage: Included (3 ticks) to account for market execution variability.

Best Use: This strategy is intended for higher timeframes (Daily or Weekly) on trending assets like Indices, Crypto, or Commodities.

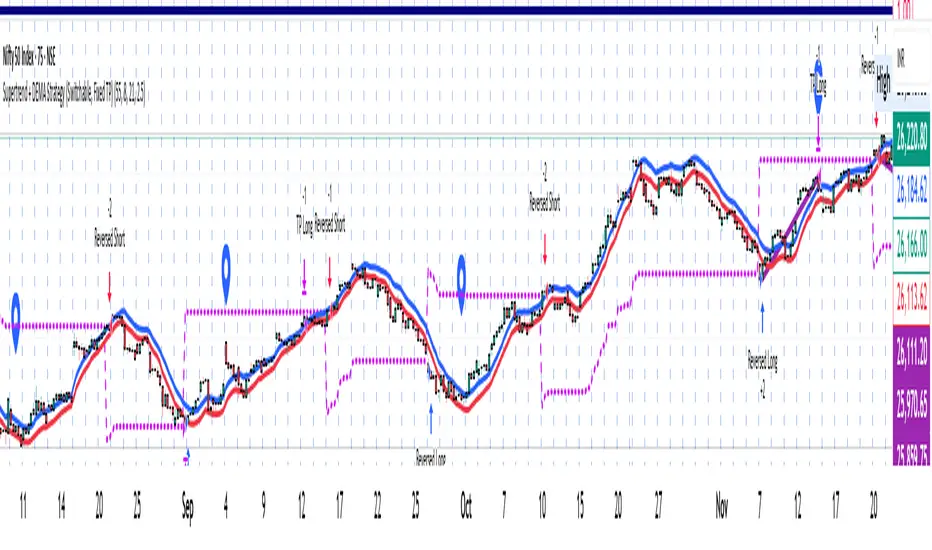

Supertrend + DEMA Strategy ( customised & Switchable, Fixed TP)Supertrend line – a moving line that follows the price and shows whether the market is trending up or down.

If the price goes above this line, it usually means the market is going up.

If the price goes below, it usually means the market is going down.

DEMA (Double Exponential Moving Average) – another line that smooths out price movements to spot trends more clearly.

It calculates an average of prices but reacts faster than a normal moving average.

1M XAU Cumulative Delta Volume with OB Breakouts

### Overview

This is a **session-based CVD strategy** built around the **00:00–07:00 CEST range**. It finds the high/low of that session, turns them into **adaptive ATR-based support (yellow)** and **resistance (purple)** zones, and trades only **CVD-confirmed reversals** off those levels.

---

### How it Works

* For each day, the script:

* Builds a 00:00–07:00 CEST **profile high/low**.

* Creates a **support zone** around the session low and a **resistance zone** around the session high.

* Using lower timeframe data, it reconstructs **Cumulative Volume Delta (CVD)** and a **recent delta** filter.

* It arms “pending” states when price **enters a zone from the correct side**, then confirms:

* **BUY (long):** price reclaims above support and recent CVD is strongly positive.

* **SELL (short):** price rejects below resistance and recent CVD is strongly negative.

Only these two CVD signals (`buySignal` / `sellSignal`) open trades.

---

### Strategy Logic

* **Entries**

* `buySignal` → open **long** (if flat).

* `sellSignal` → open **short** (if flat).

* No pyramiding; one position at a time.

* **Exits (only TP & SL)**

* Long: TP at `avg_price * (0.5 + TP%)`, SL at `avg_price * (1 – SL%)`.

* Short: TP at `avg_price * (0.5 – TP%)`, SL at `avg_price * (1 + SL%)`.

* No opposite-signal exits.

---

### Extras

* **Reversal markers** on yellow/purple zones and **breakout/retest markers** are plotted for context and alerts but **do not trigger entries**.

* Zone width and “thickening” are ATR-based so important touches and near-touches are easy to see.

* Only suited for **1m intraday scalping** (e.g. XAU/USD), but can be tested on other markets/timeframes.

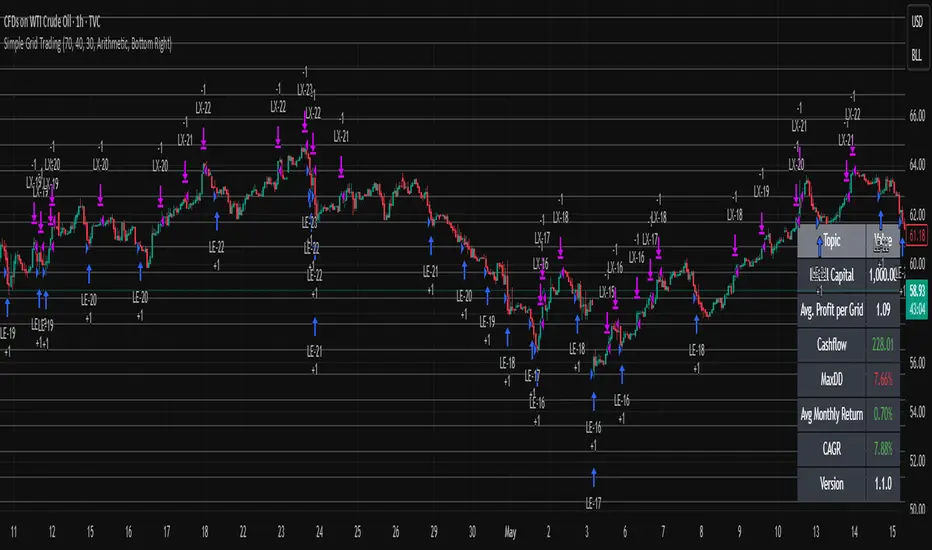

Simple Grid Trading v1.0 [PUCHON]Simple Grid Trading v1.0

Overview

This is a Long-Only Grid Trading Strategy developed in Pine Script v6 for TradingView. It is designed to profit from market volatility by placing a series of Buy Limit orders at predefined price levels. As the price drops, the strategy accumulates positions. As the price rises, it sells these positions at a profit.

Features

Grid Types : Supports both Arithmetic (equal price spacing) and Geometric (equal percentage spacing) grids.

Flexible Order Management : Uses strategy.order for precise control and prevents duplicate orders at the same level.

Performance Dashboard : A real-time table displaying key metrics like Capital, Cashflow, and Drawdown.

Advanced Metrics : Includes Max Drawdown (MaxDD) , Avg Monthly Return , and CAGR calculations.

Customizable : Fully adjustable price range, grid lines, and lot size.

Dashboard Metrics

The dashboard (default: Bottom Right) provides a quick snapshot of the strategy's performance:

Initial Capital : The starting capital defined in the strategy settings.

Lot Size : The fixed quantity of assets purchased per grid level.

Avg. Profit per Grid : The average realized profit for each closed trade.

Cashflow : The total realized net profit (closed trades only).

MaxDD : Maximum Drawdown . The largest percentage drop in equity (realized + unrealized) from a peak.

Avg Monthly Return : The average percentage return generated per month.

CAGR : Compound Annual Growth Rate . The mean annual growth rate of the investment over the specified time period.

Strategy Settings (Inputs)

Grid Settings

Upper Price : The highest price level for the grid.

Lower Price : The lowest price level for the grid.

Number of Grid Lines : The total number of levels (lines) in the grid.

Grid Type :

Arithmetic: Distance between lines is fixed in price terms (e.g., $10, $20, $30).

Geometric: Distance between lines is fixed in percentage terms (e.g., 1%, 2%, 3%).

Lot Size : The fixed amount of the asset to buy at each level.

Dashboard Settings

Show Dashboard : Toggle to hide/show the performance table.

Position : Choose where the dashboard appears on the chart (e.g., Bottom Right, Top Left).

How It Works

Initialization : On the first bar, the script calculates the price levels based on your Upper/Lower price and Grid Type.

Entry Logic :

The strategy places Buy Limit orders at every grid level below the current price.

It checks if a position already exists at a specific level to avoid "stacking" multiple orders on the same line.

Exit Logic :

For every Buy order, a corresponding Sell Limit (Take Profit) order is placed at the next higher grid level.

MaxDD Calculation :

The script continuously tracks the highest equity peak.

It calculates the drawdown on every bar (including intra-bar movements) to ensure accuracy.

Displayed as a percentage (e.g., 5.25%).

Disclaimer

This script is for educational and backtesting purposes only. Grid trading involves significant risk, especially in strong trending markets where the price may move outside your grid range. Always use proper risk management.