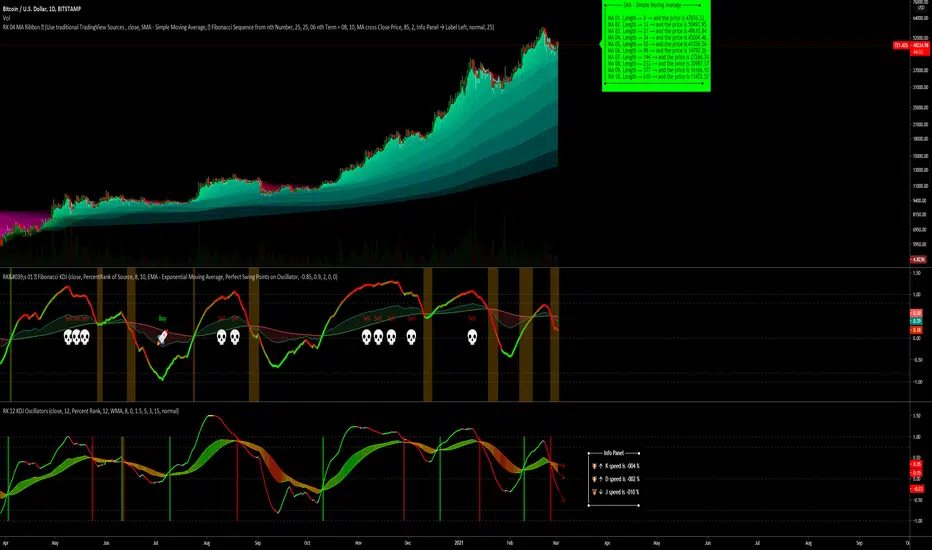

RK's 04 - Lots of MA Types RibbonHello again,

I made this script to test what is the better Moving Average type to predict the market direction, so I put a function with All the MA I know.

To go beyond, this script have an option to increase the MA length as a Fibonacci Number or any other simple number to step.

If the drawing is too slow, just reduce the amount of MA lines in the input option ("Number of MA to Plot:") to 10 or less and it will be faster.

Hope you like, and if you know other Moving Average type, just tell me how can I get the formula and (if its good, not copyrighted and I have time) I can add here and update for all of us.

Obs: To avoid errors, the Maximum Nth Fibonacci Term to use in MA Length is 19 (4181)

Indicador Pine Script®