Boom Hunter + Hull Suite + Volatility Oscillator StrategyTRADE CONDITIONS

Long entry:

Boom Hunter (leading indicator): Trigger line crosses over Quotient 2 line (white cross over red)

Hull Suite (trend confirmation): Price closed above hull suite line and hull suite is green (represented by horizontal line at -10 in strategy pane)

Volatility Oscillator (volatility confirmation): Volatility spike trigger line is above upper band (represented by horizontal line at -30 in strategy pane)

Short entry:

Boom Hunter (leading indicator): Trigger line crosses under Quotient 2 line (white cross under red)

Hull Suite (trend confirmation): Price closed below hull suite line and hull suite is red (represented by horizontal line at -10 in strategy pane)

Volatility Oscillator (volatility confirmation): Volatility spike trigger line is below lower band (represented by horizontal line at -30 in strategy pane)

Risk management:

Each trade risks 3% of account (configurable in settings)

SL size determined by swing low/high of previous X candles (configurable in settings) or 1 ATR if swing is less than 1 ATR

TP is calculated by Risk:Reward ratio (configurable in settings)

TIPS

Timeframe: I have found good results running on BTC/USDT 5M chart

Note: To help visual identification of trade entries and exits you may wish to add the Hull Suite and Volatility Oscillator to the chart separately. It was not possible to display them in a clear way within a single panel for the strategy. Make sure you set the settings of the auxiliary indicators to match what is in the settings of this indicator if you do decide to add them.

CREDITS

Boom Hunter Pro by veryfid

Hull Suite by InSilico

Volatility Oscillator by veryfid

Backtest

Template Trailing Strategy (Backtester)💭 Overview

+ Title: Template Trailing Strategy (Backtester)

+ Author: Iason Nikolas (jason5480)

+ License: CC BY-NC-SA 4.0

💢 What is the "Template Trailing Strategy (Backtester)" ❓

The "Template Trailing Strategy (Backtester)" (TTS) is a back-tester orchestration framework. It supercharges the implementation-test-evaluation lifecycle of new trading strategies, by making it possible to plug in your own trading idea.

While TTS offers a vast number of configuration settings, it primarily allows the trader to:

Test and evaluate your own trading logic that is described in terms of entry, exit, and cancellation conditions.

Define the entry and exit order types as well as their target prices when the limit, stop, or stop-limit order types are used.

Utilize a variety of options regarding the placement of the stop-loss and take-profit target(s) prices and support for well-known techniques like moving to breakeven and trailing.

Provide well-known quantity calculation methods to properly handle risk management and easily evaluate trading strategies and compare them.

Alert on each trading event or any related change through a robust and fully customizable messaging system.

All of the above makes TTS a practical toolkit: once you learn it, many repetitive tasks that strategy authors usually re-implement are eliminated. Using TradingView’s built-in backtesting engine makes testing and comparing ideas straightforward.

By utilizing the TTS one can easily swap "trading logic" by testing, evaluating, and comparing each trading idea and/or individual component of a strategy.

Finally, TTS, through its per-event alert management (and debugging) system, provides an automated solution that supports live trading with brokers via webhooks.

NOTE: The "Template Trailing Strategy (Backtester)" does not dictate how you can combine different indicator types. Thus, it should not be confused as a "Trading System", because it gives its user full flexibility on that end (for better or worse).

💢 What is a "Signal Indicator" ❓

"Signal Indicator" (SI) is an indicator that can output a "signal" that follows a specific convention so that the "Template Trailing Strategy (Backtester)" can "understand" and execute the orders accordingly. The SI realizes the core trading logic signaling to the TTS when to enter, exit, or cancel an order. A SI instructs the TTS "when" to enter or exit, and the TTS determines "how" to enter and exit the position once the Signal Indicator generates a signal.

A very simple example of a Signal Indicator might be a 200-day Simple Moving Average Signal. When the price of the security closes above the 200-day SMA, a SI would provide TTS with a "long entry signal". Once TTS receives the "long entry signal", the TTS will open a long position and send an alert or automated trade message via webhook to a broker, based on the Entry settings defined in TTS. If the TTS Entry settings specify a "Market" order type, then the open long position will be executed by TTS immediately. But if the TTS Entry settings specify a "Stop" order type with a 1% Stop Distance, then when the price of the security rises by 1% after the "long entry signal" occurs, the TTS will open a long position and the Long Entry alert or webhook to the broker will be sent.

🤔 How to Guide

💢 How to connect a "signal" from a "Signal Indicator" ❓

The "Template Trailing Strategy (Backtester)" was designed to receive external signals from a "Signal Indicator". In this way, a "new trading idea" can be developed, configured, and evaluated separately from the TTS. Similarly, the SI can be held constant, and the trading mechanics can change in the TTS settings and back-tested to answer questions such as, "Am I better with a different stop loss placement method, what if I used a limit order instead of a stop order to enter, what if I used 25% margin instead of trading spot market?"

To make that possible by connecting an external signal indicator to TTS, you should:

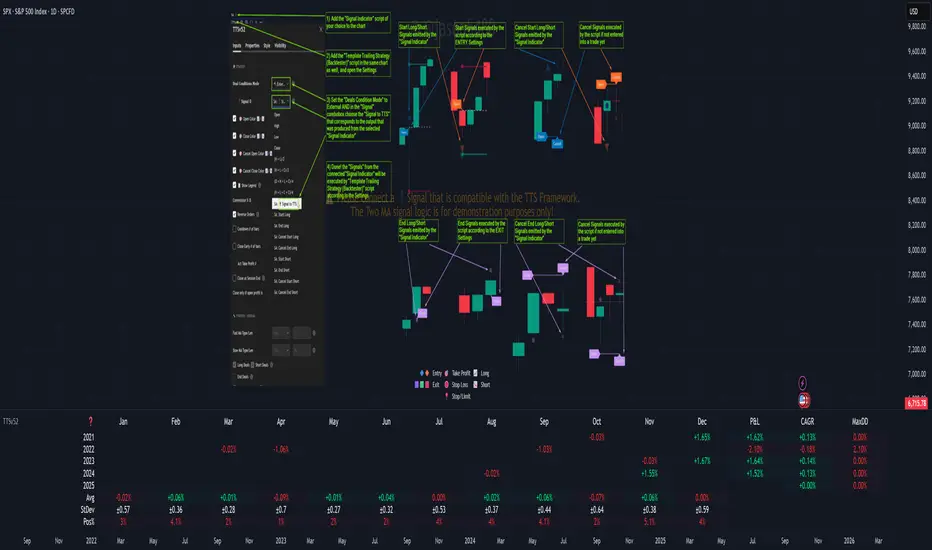

Add both your SI (e.g. "Two MA Signal Indicator" , "Click Signal Indicator" , "Signal Adapter" , "Signal Composer" ) and the TTS script to the same chart.

Open the script's Settings / Inputs dialog for the TTS.

In the 🛠️ STRATEGY group set 𝐃𝐞𝐚𝐥 𝐂𝐨𝐧𝐝𝐢𝐨𝐧𝐬 𝐌𝐨𝐝𝐞 to 🔨External (this makes TTS listen to an external signal source).

Still inside 🛠️ STRATEGY locate the 🔌𝐒𝐢𝐠𝐧𝐚𝐥 🛈 input and choose the plotted output of your SI. The option should look like: "<SI short title>:🔌Signal to TTS" .

Verbose troubleshooting & tips

If the SI does not appear in the 🔌Signal 🛈 selector, confirm both scripts are added to the same chart and the SI exposes a plotted series (title often "🔌Signal to TTS").

When using multiple SIs, pick the SI instance that actually outputs the "🔌Signal to TTS" plotted series.

Validate on the chart: when your SI changes state, the plotted "🔌Signal" series in the TTS (visible in the data window) should change accordingly.

The TTS accepts only signals that follow the tts_convention DealConditions structure. Do not attempt to feed arbitrary scalar series without using conv.getDealConditions / conv.DealConditions.

Make sure your SI composes a DealConditions value following the TTS convention (startLong, endLong, startShort, endShort — optional cancel fields). See the template below.

If the plot is present but TTS does not react, ensure the SI plot is non-repainting (or accept realtime/backtest limitations). Test on historical bars first.

Create alerts on the strategy (see the Alerts section). Use the {{strategy.order.alert_message}} placeholder in the Create Alert dialog to forward TTS messages.

💢 How to create a custom trading logic ❓

The "Template Trailing Strategy (Backtester)" provides two ways to plug in your custom trading logic. Both of them have their advantages and disadvantages.

✍️ Develop your own Customized "Signal Indicator" 💥

The first approach is meant to be used for relatively more complex trading logic. The advantages of this approach are the full control and customization you have over the trading logic and the relatively simple configuration setup by having two scripts only. The downsides are that you have to have some experience with pinescript or you are willing to learn and experiment. You should also know the exact formula for every indicator you will use since you have to write it by yourself. Copy-pasting from existing open-source indicators will get you started quite fast though.

The idea here is either to create a new indicator script from scratch or to copy an existing non-signal indicator and make it a "Signal Indicator". To create a new script, press the "Pine Editor" button below the chart to open the "Pine Editor" and then press the "Open" button to open the drop-down menu with the templates. Select the "New Indicator" option. Add it to your chart to copy an existing indicator and press the source code {} button. Its source code will be shown in the "Pine Editor" with a warning on top stating that this is a read-only script. Press the "create a working copy". Now you can give a descriptive title and a short title to your script, and you can work on (or copy-paste) the (other) indicators of your interest. Once you have the information needed to decide, define a DealConditions object and plot it like this:

import jason5480/tts_convention/ as conv

// Calculate the start, end, cancel start, cancel end conditions

dealConditions = conv.DealConditions.new(

startLongDeal = ,

startShortDeal = ,

endLongDeal = ,

endShortDeal = ,

cnlStartLongDeal = ,

cnlStartShortDeal = ,

cnlEndLongDeal = ,

cnlEndShortDeal = )

// Use this signal in scripts like "Template Trailing Strategy (Backtester)" and "Signal Composer" that can utilize its value

// Emit the current signal value according to the TTS framework convention

plot(series = conv.getSignal(dealConditions), title = '🔌Signal to TTS', color = #808000, editable = false, display = display.data_window + display.status_line, precision = 0)

You should import the latest version of the tts_convention library and write your deal conditions appropriately based on your trading logic and put them in the code section shown above by replacing the "…" part after "=". You can omit the conditions that are not relevant to your logic. For example, if you use only market orders for entering and exiting your positions the cnlStartLongDeal, cnlStartShortDeal, cnlEndLongDeal, and cnlEndShortDeal are irrelevant to your case and can be safely omitted from the DealConditions object. After successfully compiling your new custom SI script add it to the same chart with the TTS by pressing the "Add to chart" button. If all goes well, you will be able to connect your "signal" to the TTS as described in the "How to connect a "signal" from a "Signal Indicator"?" guide.

🧩 Adapt and Combine existing non-signal indicators 💥

The second approach is meant to be used for relatively simple trading logic. The advantages of this approach are the lack of pine script and coding experience needed and the fact that it can be used with closed-source indicators as long as the decision-making part is displayed as a line in the chart. The drawback is that you have to have a subscription that supports the "indicator on indicator" feature so you can connect the output of one indicator as an input to another indicator. Please check if your plan supports that feature here

To plug in your own logic that way you have to add your indicator(s) of preference in the chart and then add the "Signal Adapter" script in the same chart as well. This script is a "Signal Indicator" that can be used as a proxy to define your custom logic in the CONDITIONS group of the "Settings/Inputs" tab after defining your inputs from your preferred indicators in the VARIABLES group. Then a "signal" will be produced, if your logic is simple enough it can be directly connected to the TTS that is also added to the same chart for execution. Check the "How to connect a "signal" from a "Signal Indicator"?" in the "🤔 How to Guide" for more information.

If your logic is slightly more complicated, you can add a second "Signal Adapter" in your chart. Then you should add the "Signal Composer" in the same chart, go to the SIGNALS group of the "Settings/Inputs" tab, and connect the "signals" from the "Signal Adapters". "Signal Composer" is also a SI so its composed "signal" can be connected to the TTS the same way it is described in the "How to connect a "signal" from a "Signal Indicator"?" guide.

At this point, due to the composability of the framework, you can add an arbitrary number (bounded by your subscription of course) of "Signal Adapters" and "Signal Composers" before connecting the final "signal" to the TTS.

💢 How to set up ⏰Alerts ❓

The "Template Trailing Strategy (Backtester)" provides a fully customizable per-event alert mechanism. This means that you may have an entirely different message for entering and exiting into a position, hitting a stop-loss or a take-profit target, changing trailing targets, etc. There are no restrictions, and this gives you great flexibility.

First enable the events you want under the "🔔 ALERT MESSAGES" module. Each enabled event exposes a text area where you can craft the message using placeholders that TTS replaces with actual values when the event occurs.

The placeholder categories (exact names used by the script) are:

Chart & instrument:

{{ticker}}

{{base_currency}}

{{quote_currency}}

Entry / exit / stop / TP prices & offsets:

{{entry_price}}

{{exit_price}}

{{stop_loss_price}}

{{take_profit_price_1}} ... {{take_profit_price_5}}

{{entry+_price}}, {{entry-_price}}, {{exit+_price}}, {{exit-_price}} — Optional offset helpers (computed using "Offset Ticks")

Quantities, percents & derived quantities:

{{entry_base_quantity}} — base units at entry (e.g. BTC)

{{entry_quote_quantity}} — quote amount at entry (e.g. USD)

{{risk_perc}} — % of capital risked for that entry (multiplied by 100 when "Percentage Range " is enabled)

{{remaining_quantity_perc}} — % of the initial position remaining at close/SL

{{remaining_base_quantity}} — remaining base units at close/SL

{{take_profit_quantity_perc_1}} ... {{take_profit_quantity_perc_5}} — % sold/bought at each TP

{{take_profit_base_quantity_1}} ... {{take_profit_base_quantity_5}} — base units closed at each TP

❗ Important: the per-event alert text is injected into the Create Alert dialog using TradingView's strategy placeholder:

{{strategy.order.alert_message}}

During the creation of a strategy alert, make sure the placeholder {{strategy.order.alert_message}} exists in the "Message" box. TradingView will substitute the per-event text you configured and enabled in TTS Settings/Inputs before sending it via webhook/notification.

Tip: For webhook/broker execution, set the proper "Condition" in the Create Alert dialog (for changing-entry/exit/SL notifications use "Order fills and alert() function calls" or "alert() function calls only" as appropriate).

💢 How to execute my orders in a broker ❓

To execute your orders in a broker that supports webhook integration, you should enable the appropriate alerts in the "Template Trailing Strategy (Backtester)" first (see the "How to set up Alerts?" guide above). Then you should go to the "Create Alert/Notifications" tab check the "Webhook URL" and paste the URL provided by your broker. You have to read the documentation of your broker for more information on what messages are expected.

Keep in mind that some brokers have deep integration with TradingView so a per-event alert approach might be overkill.

📑 Definitions

This section tries to give some definitions in terms that appear in the "Settings/Inputs" tab of the "Template Trailing Strategy (Backtester)"

💢 What is Trailing ❓

Trailing is a technique where a price target follows another "barrier" price (usually high or low) by trying to keep a maximum distance from the "barrier" when it moves in only one direction (up or down). When the "barrier" moves in the other direction the price target will not change. There are as many types of trailing as price targets, which means that there are entry trailing, exit trailing, stop-loss trailing, and take-profit trailing techniques.

💢 What is a Moonbag ❓

A Moonbag in a trade is the quantity of the position that is reserved and will not be exited even if all take-profit targets defined in the strategy are hit, the quantity will be exited only if the stop-loss is hit or a close signal is received. This makes the stop-loss trailing technique in a trend-following strategy a good candidate to take advantage of a Moonbag.

💢 What is Distance ❓

Distance is the difference between two prices.

💢 What is Bias ❓

Bias is a psychological phenomenon where you make decisions based on market sentiment. For example, when you want to enter a long position you have a long bias, and when you want to exit from the long position you have a short bias. It is the other way around for the short position.

💢 What is the Bias Distance of a price target ❓

The Bias Distance of a price target is the distance that the target will deviate from its initial price. The direction of this deviation depends on the bias of the market. For example, suppose you are in a long position, and you set a take-profit target to the local highest high. In that case, adding a bias distance of five ticks will place your take-profit target 5 ticks below this local highest high because you have a short bias when exiting a long position. When the bias is long the bias distance will be added resulting in a higher target price and when you have a short bias the bias distance will be subtracted.

⚙️ Settings

In the "Settings/Inputs" tab of the "Template Trailing Strategy (Backtester)", you can find all the customizable settings that are provided by the framework. The variety of those settings is vast; hence we will only scratch the surface here. However, for every setting, there is an information icon 🛈 where you can learn more if you mouse over it. The "Settings/Inputs" tab is divided into ten main groups. Each one of them is responsible for one module of the framework. Every setting is part of a group that is named after the module it represents. So, to spot the module of a setting find the title that appears above it comes with an emoji and uppercase letters. Some settings might have the same name but belong to different modules e.g. "Tgt Dist Mtd" (Target Distance Method). Some settings are indented, which means that they are closely related to the non-indented setting above. Usually, indented settings provide further configuration for one or more options of the non-indented setting above. The groups that correspond to each module of the framework are the following:

🗺️ Quick Module Cross-Reference (use emojis to jump to setting groups)

📆 FILTERS — session, date & weekday filters

🛠️ STRATEGY — internal vs external deal-conditions; pick the signal source

🔧 STRATEGY – INTERNAL — built-in Two MA logic for demonstration purposes

🎢 VOLATILITY — ATR / StDev update modes

🔷 ENTRY — entry order types & trailing

🎯 TAKE PROFIT — multi-step TP and trailing rules

🛑 STOP LOSS — stop placement, move-to-breakeven, trailing

🟪 EXIT — exit order types & cancel logic

💰 QUANTITY/RISK MANAGEMENT — position sizing, moonbag, limits

📊 ANALYTICS — stats, streaks, seasonal tables

🔔 ALERT MESSAGES — per-event alert templates & placeholders

😲 Caveats

💢 Does "Template Trailing Strategy (Backtester)" have repainting behavior? ❓

The answer is that the "Template Trailing Strategy (Backtester)" does not repaint as long as the "Signal Indicator" that is connected also does not repaint. If you developed your own SI make sure that you understand and know how to prevent this behavior. The publication by @PineCoders here will give you a good idea on how to avoid most of the repainting cases.

⚠️ There is an exception though, when the "Enable Trail⚠️💹" checkbox is checked, the Take Profit trailing feature is enabled, and a tick-based approach is used, meaning that after a while, when the TradingView discards all the real-time data, assumptions will be made by the backtesting engine that will cause a form of repainting. To avoid making false assumptions please disable this feature in the early stages and evaluate its usefulness in your strategy later on, after first confirming the success of the logic without this feature. In this case, consider turning on the bar magnifier feature. This way you will get more accurate backtest results when the Take Profit trailing feature is enabled.

💢 Can "Template Trailing Strategy (Backtester)" satisfy all my trading strategies ❓

While this framework can satisfy quite a large number of trading strategies there are cases where it cannot do so. For example, if you have a custom logic for your stop-loss or take-profit placement, or if you want to dollar cost average, then it might be better to start a new strategy script from scratch.

⚠️ It is not recommended to copy the official TTS code and start developing unless you are a Pine wizard! Even in that case, there is a stiff learning curve that might not be worth your time. Last, you must consider that I do not offer support for customized versions of the TTS script and if something goes wrong in the process you are all alone.

💝 Support & Feedback

For feedback, bug reports, or feature requests, contact me via TradingView PM or use the script comments.

Note: The author's personal links and contact are available on the TradingView profile.

🤗 Thanks

Special thanks to the welcoming community members, who regularly gave feedback all those years and helped me to shape the framework as it is today! Thanks everyone who contributed by either filing a "defect report" or asking questions that helped me to understand what improvements were necessary to help traders.

Enjoy!

Jason

WhaleCrew BacktesterBacktesting indicators is easy , just add the following line of code to your script:

plot(longEntry ? 1 : shortEntry ? -1 : longTP ? 0.5 : shortTP ? -0.5 : 0, color=na, editable=false, title='Backtest')

These numbers are defined as constants in the backtester source-code.

After adding this indicator to your chart:

1. Open Settings

2. Select supported indicator to backtest

3. Select if you want to enter Longs and/or Shorts

4. Open the 'Strategy Tester' at the bottom to check the performance

Remember:

past performance is not indicative of future results

repainting indicators will create wrong/unrealistic results

Dual MACD StrategyThis strategy Multi Time Frame Macd Indicator

We take the first long position when we have a buy signal in Weekly Macd (Macd line crosses above Signal line). This open a trading window, showed with green background color

We close the first position when either Weekly or Daily Macd give us a sell signal ((Macd line crosses below Signal line))

Enable Profit and Stop in strategy settings with different percentage to backtest the strategy. Also if it is better to use a Traditional Stop Loss or a Trailing Stop Loss based on a percentage from low prices

Change macd resolution in settings for other time frames to test the strategy

This Strategy was tested on Crypto Market with good results in assets as BTC, ETH, BNB, ADA, LTC, XLM, BCH, among others

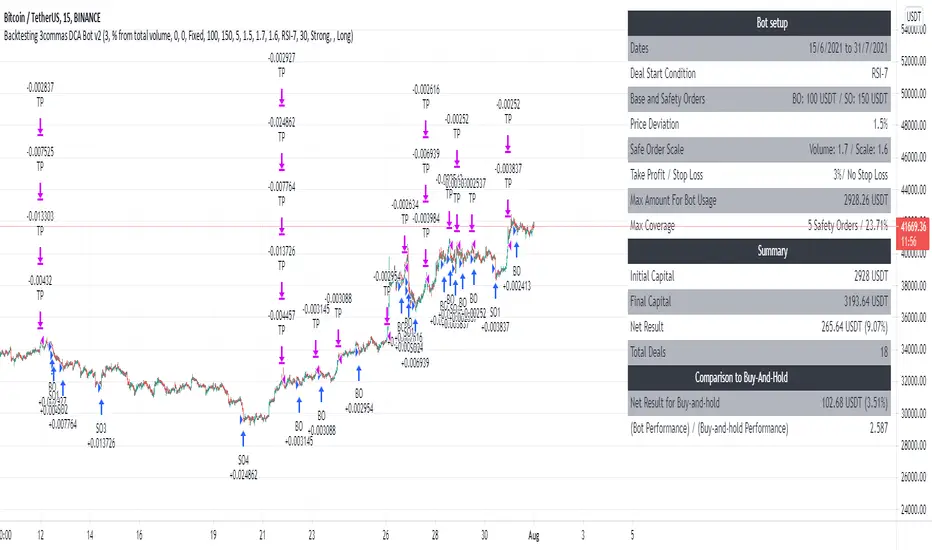

Zendog V2 backtest DCA bot 3commasHi everyone,

After a few iterations and additional implemented features this version of the Backtester is now open source.

The Strategy is a Backtester for 3commas DCA bots. The main usage scenario is to plugin your external indicator, and backtest it using different DCA settings.

Before using this script please make sure you read these explanations and make sure you understand how it works.

Features:

- Because of Tradingview limitations on how orders are grouped into Trades, this Strategy statistics are calculated by the script, so please ignore the Strategy Tester statistics completely

Statistics Table explained:

- Status: either all deals are closed or there is a deal still running, in which case additional info

is provided below, as when the deal started, current PnL, current SO

- Finished deals: Total number of closed deals both Winning and Losing.

A deal is comprised as the Base Order (BO) + all Safety Orders (SO) related to that deal, so this number

will be different than the Strategy Tester List of Trades

- Winning Deals: Deal ended in profit

- Losing deals: Deals ended with loss due to Stop Loss. In the future I might add a Deal Stop condition to

the script, so that will count towards this number as well.

- Total days ( Max / Avg days in Deal ):

Total Days in the Backtest given by either Tradingview limitation on the number of candles or by the

config of the script regarding "Limit Date Range".

Max Days spent in a deal + which period this happened.

Avg days spent in a deal.

- Required capital: This is the total capital required to run the Backtester and it is automatically calculated by

the script taking into consideration BO size, SO size, SO volume scale. This should be the same as 3commas.

This number overwrites strategy.initial_capital and is used to calculate Profit and other stats, so you don't need

to update strategy.initial_capital every time you change BO/SO settings

- Profit after commission

- Buy and Hold return: The PnL that could have been obtained by buying at the close of the first candle of the

backtester and selling at the last.

- Covered deviation: The % of price move from initial BO order covered by SO settings

- Max Deviation: Biggest market % price move vs BO price, in the other direction (for long

is down, for short it is up)

- Max Drawdown: Biggest market % price move vs Avg price of the whole Trade (BO + any SO), in the other

direction (for long price goes down, for short it goes up)

This is calculated for the whole Trade so it is different than List of Trades

- Max / Avg bars in deal

- Total volume / Commission calculated by the strategy. For correct commission please set Commission in the

Inputs Tab and you may ignore Properties Tab

- Close stats for deals: This is a list of how many Trades were closed at each step, including Stop Loss (if

configured), together with covered deviation for that step, the number of deals, and the percentage of this

number from all the deals

TODO: Might add deal avg value for each step

- Settings Table that can be enabled / disabled just to have an overview of your configs on the chart, this is a

drawn on bottom left

- Steps Table similar to 3commas, this is also drawn on bottom left, so please disable Settings table if you want

to see this one

TODO: Might add extra stats here

- Deal start condition: built in RSI-7 or plugin any external indicator and compare with any value the indicator plots

(main purpose of this strategy is to connect your own studies, so using external indicator is recommended)

- Base order and safety orders configs similar to 3commas (order size, percent deviation, safety orders,

percent scale and volume scale)

- Long and Short

- Stop Loss

- Support for Take profit from base order or from Total volume of the deal

- Configs help (besides self explanatory):

- Chart theme: Adjust according to the theme you run on. There is no way to detect theme at the moment.

This adjust different colors

- Deal Start Type: Either a builtin RSI7 or "External indicator"

- Indicator Source an value: If using External Indicator then select source, comparison and value.

For example you could start a deal when Volume is greater than xxxx, or code a custom indicator that plots

different values based on your conditions and test those values

- Visuals / Decimals for display: Adjust according to your symbol

- BO Entry Price for steps table: This is the BO start deal price used to calculate the steps in the table

Hull Crossover Strategy no TP or SLWhat is it?

A simple yet effective strategy ran on the 30m chart.

This is a basic idea that can be expanded on using different indicator to either add signals or filter out certain bad signals!

The strategy consists of 1 fast moving average and 1 slow moving average.

Both of these moving averages are the Hull Moving Average

What is the Hull Moving Average?

The Hull Moving Average ( HMA ) is a directional trend indicator.

It captures the current market conditions and uses recent price action to determine if conditions are bullish or bearish relative to historical data.

The Hull is different from traditional trend indicators like the EMA and the SMA .

It is designed to reduce the lag often associated with other MAs by providing a faster signal on a smoother visual plane.

How it works?

When the fast HMA crosses over the slow HMA , we initiate a long signal, and

when the fast HMA crosses under the slow HMA , we initiate a short signal.

Conclusion

The power of simplicity is what makes this such a great core to use to build onto making something even better!

The results were optimised to suit the most common market conditions seen today.

******** Not financial advice! ********

Rainbow Strategy BacktestingRainbow Strategy Backtesting base on "Rainbow Moving Average" Strategy as below:

1.Rainbow Moving Average setup

- Source: source of 1st MA

- Type: SMA/EMA

- Period: period of 1st MA

- Displacement: period of 2nd MA to 7th MA with source is previous MA

2.Trend Define

- Up Trend: Main MA moving at the top of Rainbow

- Down Trend: Main MA moving at the bottom of Rainbow

- Sideway: Main MA moving between the top and the bottom of Rainbow

3.Signal

- Buy Signal: When Rainbow change to Up Trend.

- Sell Signal: When Rainbow change to Down Trend.

- Exit: When Rainbow change to Sideway.

4.RSI Filter

- "Enable": Only signals have 1st RSI moving between Overbought and Oversold and 2nd RSI moving outside Middle Channel are accepted.

- The filter may help trader avoid bull trap, bear trap and choppy market.

5.Backtesting Infomation

- Ticker: BTCUSDT

- Timeframe: H1

- Rainbow parameter:

+ Source: hlc3

+ Type: SMA

+ Period: 12

+ Displacement: 3

- RSI Filter parameter:

+ Enable

+ 1st RSI filter: period 12, overbought 65, oversold 35

+ 2nd RSI filter: period 9, upper middle 56, lower middle 44

Backtesting 3commas DCA Bot v2Updating previously published simulated 3commas DCA logic with a sexier insert and more meaningful default parameters.

3Commas Bollinger StrategyThis strategy is intended for use as a way of backtesting various parameters available on 3commas.io composite bot using a bollinger band type trading strategy. While it's primary intention is to provide users a way of backtesting bot parameters, it can also be used to trigger a deal start by either using the {{strategy.open.alert_message}} field in your alert and providing the bot details in the configuration screen for the strategy or by including the usual deal start message provided by 3commas. You can find more information about how to do this from help.3commas.io

The primary inputs for the strategy are:

// USER INPUTS

Short MA Window - The length of the Short moving average

Long MA Window - The length of the Long moving average

Upper Band Offset - The offset to use for the upper bollinger offset

Lower Band Offset - The offset to use for the lower bollinger offset

Long Stop Loss % - The stop loss percentage to test

Long Take Profit % - The Take profit percentage to test

Initial SO Deviation % - The price deviation percentage required to place to first safety order

Safety Order Vol Step % - The volume scale to test

3Commas Bot ID - (self explanatory)

Bot Email Token - Found in the deal start message for your bot (see link in previous section for details)

3Commas Bot Trading Pair - The pair to include for composite bot start deals (should match format of 3commas, not TradingView IE. USDT_BTC not BTCUSDT)

Start Date, Month, Year and End Date, Month and Year all apply to the backtesting window. By default it will use as much data as it can given the current period select (there is less historical data available for periods below 1H) back as far as 2016 (there appears to be no historical data on Trading view much before this). If you would like to test a different period of time, just change these values accordingly.

Known Issues

Currently there are a couple of issues with this strategy that you should be aware of. I may fix them at some point in the future but they don't really bug me so this is more for informational purposes than a promise that they may one day be fixed.

Does not test trailing take profit

Number of safety orders and Safety Order Step Scale are currently not user configurable (must edit source code)

Using the user configuration to generate deal start message assumes you are triggering a composite bot, not a simple bot.

Combo Backtest 123 Reversal & MASS Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Mass Index was designed to identify trend reversals by measuring

the narrowing and widening of the range between the high and low prices.

As this range widens, the Mass Index increases; as the range narrows

the Mass Index decreases.

The Mass Index was developed by Donald Dorsey.

WARNING:

- For purpose educate only

- This script to change bars colors.

RSI-VWAP Indicator %█ OVERALL

Simple and effective script that, as you already know, uses vwap as source of the rsi, and with good results as long as the market has no long-term downtrend.

RsiVwap = rsi (vwap (close), Length)

The default settings are for BTC in a 30 minute time frame. For other pairs and time frames you just have to play with the settings.

█ FEATURES

• The option to start trading from a certain date has been added.

• To make the profit more progressive, a percentage of your equity is used for entries and a percentage of your position is used for closings.

• The option to trade in Spot mode has been added, since, for the TradingView backtest, the money is infinite and if you do not limit it somehow,

it would offer you much better profits than the live trading.

QuantityOnLong = Spot ? (EquityPercent / 100) * ((strategy.equity / close) - strategy.position_size) : (EquityPercent / 100) * (strategy.equity / close)

• The option to stop the system when the drawdown exceeds the fixed limit has been added.

Drawdown, as you already know, is a very important measure of risk in trading systems.

The maximum drawdown will tell us what the maximum loss of a trading system has been during a period. This maximum loss is determined by:

strategy.risk.max_drawdown(Risk, strategy.percent_of_equity)

• Leverage plotted on labels added.

█ ALERTS

To enjoy the benefits of automatic trading, TradingView alerts can be used as direct buy-sell orders on spot, or long-close orders with leverage.

Currently there are Chrome extensions that act as a bridge between TradingView and your Exchange or Broker.

This is an example of syntax for this type of extensions. Copy and paste a message like this into the alert window:

{{strategy.order.action}} @ {{strategy.order.price}} | e = {{exchange}} a = account s = {{ticker}} b = {{strategy.order.action}} {{strategy.order.alert_message}}

█ NOTE

Certain Risks of Live Algorithmic Trading You Should Know:

• Backtesting cannot assure actual results.

• The relevant market might fail or behave unexpectedly.

• Your broker may experience failures in its infrastructure, fail to execute your orders in a correct or timely fashion or reject your orders.

• The system you use for generating trading orders, communicating those orders to your broker, and receiving queries and trading results from your broker may fail.

• Time lag at various point in live trading might cause unexpected behavior.

• The systems of third parties in addition to those of the provider from which we obtain various services, your broker, and the applicable securities market may fail or malfunction.

█ THANKS

Thanks to TradingView, its Pine code, its community and especially those Pine wizards who post their ideas that helps us to learn.

If the world is heading toward a equitable new world economic order, let's get rich first ...

Happy trading!

Ultimate Strategy TemplateHello Traders

As most of you know, I'm a member of the PineCoders community and I sometimes take freelance pine coding jobs for TradingView users.

Off the top of my head, users often want to:

- convert an indicator into a strategy, so as to get the backtesting statistics from TradingView

- add alerts to their indicator/strategy

- develop a generic strategy template which can be plugged into (almost) any indicator

My gift for the community today is my Ultimate Strategy Template

Step 1: Create your connector

Adapt your indicator with only 2 lines of code and then connect it to this strategy template.

For doing so:

1) Find in your indicator where are the conditions printing the long/buy and short/sell signals.

2) Create an additional plot as below

I'm giving an example with a Two moving averages cross.

Please replicate the same methodology for your indicator wether it's a MACD, ZigZag, Pivots, higher-highs, lower-lows or whatever indicator with clear buy and sell conditions

//@version=4

study(title='Moving Average Cross', shorttitle='Moving Average Cross', overlay=true, precision=6, max_labels_count=500, max_lines_count=500)

type_ma1 = input(title="MA1 type", defval="SMA", options= )

length_ma1 = input(10, title = " MA1 length", type=input.integer)

type_ma2 = input(title="MA2 type", defval="SMA", options= )

length_ma2 = input(100, title = " MA2 length", type=input.integer)

// MA

f_ma(smoothing, src, length) =>

iff(smoothing == "RMA", rma(src, length),

iff(smoothing == "SMA", sma(src, length),

iff(smoothing == "EMA", ema(src, length), src)))

MA1 = f_ma(type_ma1, close, length_ma1)

MA2 = f_ma(type_ma2, close, length_ma2)

// buy and sell conditions

buy = crossover(MA1, MA2)

sell = crossunder(MA1, MA2)

plot(MA1, color=color_ma1, title="Plot MA1", linewidth=3)

plot(MA2, color=color_ma2, title="Plot MA2", linewidth=3)

plotshape(buy, title='LONG SIGNAL', style=shape.circle, location=location.belowbar, color=color_ma1, size=size.normal)

plotshape(sell, title='SHORT SIGNAL', style=shape.circle, location=location.abovebar, color=color_ma2, size=size.normal)

/////////////////////////// SIGNAL FOR STRATEGY /////////////////////////

Signal = buy ? 1 : sell ? -1 : 0

plot(Signal, title="🔌Connector🔌", transp=100)

Basically, I identified my buy, sell conditions in the code and added this at the bottom of my indicator code

Signal = buy ? 1 : sell ? -1 : 0

plot(Signal, title="🔌Connector🔌", transp=100)

Important Notes

🔥 The Strategy Template expects the value to be exactly 1 for the bullish signal , and -1 for the bearish signal

Now you can connect your indicator to the Strategy Template using the method below or that one

Step 2: Connect the connector

1) Add your updated indicator to a TradingView chart

2) Add the Strategy Template as well to the SAME chart

3) Open the Strategy Template settings and in the Data Source field select your 🔌Connector🔌 (which comes from your indicator)

From then, you should start seeing the signals and plenty of other stuff on your chart

🔥 Note that whenever you'll update your indicator values, the strategy statistics and visual on your chart will update in real-time

Settings

- Color Candles : Color the candles based on the trade state (bullish, bearish, neutral)

- Close positions at market at the end of each session : useful for everything but cryptocurrencies

- Session time ranges : Take the signals from a starting time to an ending time

- Close Direction : Choose to close only the longs, shorts, or both

- Date Filter : Take the signals from a starting date to an ending date

- Set the maximum losing streak length with an input

- Set the maximum winning streak length with an input

- Set the maximum consecutive days with a loss

- Set the maximum drawdown (in % of strategy equity)

- Set the maximum intraday loss in percentage

- Limit the number of trades per day

- Limit the number of trades per week

- Stop-loss: None or Percentage or Trailing Stop Percentage or ATR

- Take-Profit: None or Percentage or ATR

- Risk-Reward based on ATR multiple for the Stop-Loss and Take-Profit

This script is open-source so feel free to use it, and optimize it as you want

Alerts

Maybe you didn't know it but alerts are available on strategy scripts.

I added them in this template - that's cool because:

- if you don't know how to code, now you can connect your indicator and get alerts

- you have now a cool template showing you how to create alerts for strategy scripts

Source: www.tradingview.com

I hope you'll like it, use it, optimize it and most importantly....make some optimizations to your indicators thanks to this Strategy template

Special Thanks

Special thanks to @JosKodify as I borrowed a few risk management snippets from his website: kodify.net

Additional features

I thought of plenty of extra filters that I'll add later on this week on this strategy template

Best

Dave

Combo Backtest 123 Reversal & Line Regression Intercept This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Linear Regression Intercept is one of the indicators calculated by using the

Linear Regression technique. Linear regression indicates the value of the Y

(generally the price) when the value of X (the time series) is 0. Linear

Regression Intercept is used along with the Linear Regression Slope to create

the Linear Regression Line. The Linear Regression Intercept along with the Slope

creates the Regression line.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Laguerre-based RSI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is RSI indicator which is more sesitive to price changes.

It is based upon a modern math tool - Laguerre transform filter.

With help of Laguerre filter one becomes able to create superior

indicators using very short data lengths as well. The use of shorter

data lengths means you can make the indicators more responsive to

changes in the price.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Volume SMA This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Volume and SMA

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Gann Swing Oscillator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Gann Swing Oscillator has been adapted from Robert Krausz's book,

"A W.D. Gann Treasure Discovered". The Gann Swing Oscillator helps

define market swings.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & FX Sniper: T3-CCI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This simple indicator gives you a lot of useful information - when to enter, when to exit

and how to reduce risks by entering a trade on a double confirmed signal.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Volatility Finite Volume ElementsThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is another version of FVE indicator that we have posted earlier

in this forum.

This version has an important enhancement to the previous one that`s

especially useful with intraday minute charts.

Due to the volatility had not been taken into account to avoid the extra

complication in the formula, the previous formula has some drawbacks:

The main drawback is that the constant cutoff coefficient will overestimate

price changes in minute charts and underestimate corresponding changes in

weekly or monthly charts.

And now the indicator uses adaptive cutoff coefficient which will adjust to

all time frames automatically.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & FSK (Fast and Slow Kurtosis) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots the Fast & Slow Kurtosis. The Kurtosis is a market

sentiment indicator. The Kurtosis is constructed from three different parts.

The Kurtosis, the Fast Kurtosis(FK), and the Fast/Slow Kurtosis(FSK).

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Fractal Chaos Oscillator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The value of Fractal Chaos Oscillator is calculated as the difference between

the most subtle movements of the market. In general, its value moves between

-1.000 and 1.000. The higher the value of the Fractal Chaos Oscillator, the

more one can say that it follows a certain trend – an increase in prices trend,

or a decrease in prices trend.

Being an indicator expressed in a numeric value, traders say that this is an

indicator that puts a value on the trendiness of the markets. When the FCO reaches

a high value, they initiate the “buy” operation, contrarily when the FCO reaches a

low value, they signal the “sell” action. This is an excellent indicator to use in

intra-day trading.

WARNING:

- For purpose educate only

- This script to change bars colors.

Simple SMA Strategy Backtest Part 5Simple SMA strategy

In this stream, we will create an intraday trade cap.

WARNING:

- For purpose educate only

- This script to change bars colors

Stream:

www.tradingview.com

Combo Backtest 123 Reversal & Floor Pivot Points This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The name ‘Floor-Trader Pivot,’ came from the fact that Pivot points can

be calculated quickly, on the fly using price data from the previous day

as an input. Although time-frames of less than a day can be used, Pivots are

commonly plotted on the Daily Chart; using price data from the previous day’s

trading activity.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Future Lines of Demarcation This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

An FLD is a line that is plotted on the same scale as the price and is in fact the

price itself displaced to the right (into the future) by (approximately) half the

wavelength of the cycle for which the FLD is plotted. There are three FLD's that can be

plotted for each cycle:

An FLD based on the median price.

An FLD based on the high price.

An FLD based on the low price.

WARNING:

- For purpose educate only

- This script to change bars colors.