20 Day Range High/Low (Turtle Soup)This indicator identifies the Highest High and Lowest Low of the last 20 periods (customizable) and projects horizontal support/resistance lines to the right.

Unlike standard Donchian Channels or other High/Low indicators that clutter the chart with historical "steps" or extend lines infinitely to the left, this script focuses on chart cleanliness.

Key Features:

Pivot-Point Start: The lines do not span the whole chart. They start exactly at the candle where the High or Low occurred.

Right Extension: Lines extend only to the future, providing a clear visual for potential breakouts or support levels.

No Historical Clutter: It does not draw the past movement of the High/Low, keeping your chart clean for price action analysis.

Dynamic: As new Highs or Lows are made, the lines instantly update to the new positions.

How to Use:

Trend Identification: Use the High line as a resistance/breakout level (similar to Turtle Trading strategies).

Stop Loss Placement: The Low line of the last 20 days often acts as a trailing stop location for long-term trends.

Timeframes: While designed for the classic "20-Day" lookback on the Daily chart, this script works on any timeframe (e.g., finding the 20-hour range on a 1H chart).

Settings:

Length: Default is 20 bars. You can change this in the settings to any lookback period you prefer (e.g., 50, 100).

Volumen

Smoothed VWAP Bands + EMAsSmoothed VWAP bands

With my script, you take the raw standard deviation and apply an EMA (exponential moving

Advantages:

1. Less noise:

* The bands don’t jump around with every tiny price spike.

* Makes it easier to judge real price extremes.

2. Better zone visualization:

* Inner and outer bands are smoother and more visually “stable.”

* Easier to see meaningful trends, support/resistance, and breakout zones.

3. Fewer fakeouts:

* Traders can filter out small false signals because smoothed bands only move when volatility actually changes.

4. Dynamic to volatility:

* EMA smoothing keeps the bands adaptive:

* In quiet periods, bands tighten.

* In volatile periods, bands expand.

* But it avoids extreme jitter caused by every micro-move.

Safe Zone Rules

1. Long entries (green zone):

* Price above VWAP (trend bullish).

* Price inside inner band ±1σ (not touching outer extremes).

* Optional: candle close confirmation (price fully above inner band).

2. Short entries (red zone):

* Price below VWAP (trend bearish).

* Price inside inner band ±1σ.

* Optional: candle close confirmation.

3. Outer bands (±2σ):

* Considered overextended zones → avoid entries to reduce fakeouts.

4. Visual cues:

* Safe zones shaded lightly green/red inside inner band.

* Outer bands remain unshaded (for context).

Here’s a cheat sheet for trading the Smoothed VWAP Bands + EMAs that shows safe entry zones and trend alignment clearly.

Smoothed VWAP Bands + EMAs Cheat Sheet

Price Action Relative to Bands & EMAs

+2σ (Outer Upper Band)

----------------

Extreme volatility zone

Avoid entries here

+1σ (Inner Upper Band)

----------------

Safe zone limit for longs

Consider profit taking here

VWAP Line (Green = Bullish, Red = Bearish)

==================

Core trend indicator

Only trade in VWAP trend direction

-1σ (Inner Lower Band)

----------------

Safe zone limit for shorts

Good for entries in trend direction

-2σ (Outer Lower Band)

----------------

Extreme volatility zone

Avoid entries here

1️⃣ Trend Direction with VWAP & EMAs

* VWAP → shows the overall session trend.

* Price above VWAP → bullish

* Price below VWAP → bearish

* EMA 5 (blue) → short-term momentum

* EMA 20 (orange) → medium-term trend

Rule: Only take trades in the direction of the trend:

* Long trades → price > VWAP and EMA 5 > EMA 20

* Short trades → price < VWAP and EMA 5 < EMA 20

This prevents chasing trades against the trend and reduces fakeouts.

2️⃣ Entry Zones Using Smoothed VWAP Bands

* Inner band (±1σ) → “safe entry zone”

* Outer band (±2σ) → volatility extremes → avoid entries here

Rule: Enter longs inside the inner band above VWAP and shorts inside the inner band below VWAP.

Best used on intraday timeframes.

15, 5, 2, 1 min charts.

Normalised Volume Oscillator [BackQuant]Normalised Volume Oscillator

A refined evolution of the Klinger Volume Oscillator, rebuilt for clarity, precision, and adaptability. This tool normalizes volume-driven momentum into a bounded scale so you can easily identify shifts in accumulation and distribution across any asset or timeframe, while keeping readings comparable between markets.

What this indicator does

The Normalised Volume Oscillator quantifies the balance between buying and selling pressure using the Klinger Volume Oscillator (KVO) as its base, then rescales it dynamically into a normalized range between -0.5 and +0.5. This normalization allows traders to interpret relative strength and exhaustion in volume flow, rather than dealing with raw unbounded values that differ across symbols.

It is a momentum-volume hybrid that reveals the strength of trend participation: when buyers dominate, normalized readings rise toward +0.5; when sellers dominate, they fall toward -0.5. The midline (0) acts as an equilibrium between accumulation and distribution.

Core components

Klinger Volume Oscillator: The foundation of this indicator, combining volume with price trend direction to measure long-term money flow relative to short-term movement.

Normalization process: The raw KVO is scaled over a user-defined Normalisation Period , computing `(KVO - lowest) / (highest - lowest) - 0.5`. This centers all readings around zero, allowing overbought/oversold detection independent of asset volatility or volume magnitude.

Signal moving average: The normalized KVO is smoothed with a user-selectable moving average type—SMA, EMA, DEMA, TEMA, HMA, ALMA, and others. This becomes the signal line for confirmation of trend direction or mean-reversion setups.

How it works conceptually

1. The KVO detects when volume supports price movement (bullish) or diverges from it (bearish).

2. The script normalizes the raw KVO so that relative magnitude is consistent—what is “strong buying pressure” looks the same on BTCUSD as it does on AAPL.

3. Overbought and oversold regions are derived statistically, rather than from arbitrary values, based on percentile zones around ±0.4 and ±0.5.

4. The oscillator is optionally combined with a moving average to help identify crossovers, momentum shifts, and divergence confirmation.

How to interpret it

Above 0: Indicates dominant buying pressure and likely continuation of upward momentum.

Below 0: Suggests dominant selling pressure and potential continuation of downward movement.

Crosses of 0: Often mark transitions between accumulation and distribution phases.

+0.4 to +0.5 zone: Overbought region where buying intensity is stretched; watch for deceleration or divergence.

[-0.4 to -0.5 zone: Oversold region indicating panic or exhaustion in selling.

Signal-line crossover: A traditional momentum confirmation method; when the normalized KVO crosses above its moving average, buyers regain control, and vice versa.

Why normalization matters

Typical volume oscillators are asset-specific—what is considered “high” volume for one symbol is not the same for another. By dynamically normalizing KVO values within a rolling lookback, this version transforms raw amplitude into a standardized scale. This means you can:

Compare multiple assets objectively.

Set consistent alert thresholds for overbought/oversold regions.

Avoid misleading interpretations from absolute oscillator values.

Customization and UI

Moving Average Type & Period: Select your preferred smoothing method (SMA, EMA, TEMA, etc.) and adjust its period to tune sensitivity.

Normalisation Period: Defines how many bars the KVO range is measured over; shorter periods adapt faster, longer ones smooth more.

Visual Toggles:

* Show Oscillator : enables or hides the core histogram.

* Show Moving Average : adds a smoothed overlay for signal confirmation.

* Paint Candles : optional color overlay for chart candles based on oscillator direction.

* Show Static Levels : displays ±0.4 and ±0.5 zones for overbought/oversold boundaries.

How to use it

Trend confirmation: Use midline (0) crossovers as confirmation of emerging trend shifts—cross above 0 suggests a new bullish phase, cross below 0 a bearish one.

Reversal spotting: Look for normalized readings reaching ±0.5 and flattening, or diverging against price extremes.

Divergence analysis: When price makes a new high but the normalized oscillator fails to, it signals waning buying conviction (and vice versa for lows).

Multi-timeframe integration: Works best alongside higher timeframe trend filters or moving averages; normalization makes this consistent.

Alerts

Prebuilt alert conditions allow quick automation:

Midline crossovers (0): transition between accumulation and distribution.

Overbought (+0.4) and Oversold (-0.4) triggers for potential exhaustion.

Signal moving-average crosses for confirmation entries.

Tips for use

Combine with price structure—don’t fade every overbought/oversold reading; confirm with break of structure or candle patterns.

Use longer normalization periods for position trading, shorter for intraday analysis.

In choppy markets, treat 0-line oscillations as noise filters, not trade triggers.

Summary

The Normalised Volume Oscillator modernizes the classic Klinger Volume Oscillator by normalizing its readings into a standardized range. This makes it more adaptive across assets and timeframes, improves interpretability, and provides intuitive, data-driven overbought/oversold levels. Whether used standalone or as a confirmation layer, it offers a clearer view of volume dynamics—revealing when markets are truly being accumulated, distributed, or stretched beyond their sustainable extremes.

My script//@version=5

indicator("200-Day Volume MACD Oscillator", overlay=false)

length = 200

vol_avg = ta.sma(volume, length)

oscillator = volume - vol_avg

plot(oscillator, style=plot.style_histogram, color=oscillator >= 0 ? color.green : color.red, title="Volume MACD Oscillator")

Smart RSI Money Flow - Core Bands V1.01SMART RSI – Money Flow Bands (Technical Overview)

1. Background: RSI and Its Behavior on Lower Timeframes

The Relative Strength Index (RSI) originally is a momentum oscillator calculated from average gains and losses over a selected period. In its standard form, RSI is derived solely from price changes; it does not incorporate volume data or order-flow information in its formula.

Because RSI is price-based, its interpretation depends strongly on the timeframe:

• On higher timeframes, each bar aggregates more trading activity, and RSI tends to behave more smoothly.

• On lower timeframes (1-hour down to intraday scalping intervals), price fluctuations are quicker, and RSI becomes more sensitive to short-term noise.

This does not imply that RSI becomes invalid, but that its signals on fast charts can be more reactive and may benefit from additional context such as volume behavior or structural information.

2. Purpose of This Indicator

This indicator extends the classical RSI by adding information that RSI does not include:

• Mapping RSI values into price-based bands instead of the 0–100 oscillator space.

• Retrieving lower timeframe volume data and separating it into buy and sell components.

• Comparing the slope (angle) of price movement with the slope of buy and sell volume.

The goal is to provide a structural interpretation of where price sits relative to RSI conditions and how volume is behaving on a lower timeframe.

3. Technical Differences Compared to Classical RSI

A) Classical RSI

• Input: price only (usually close).

• Output: normalized oscillator between 0 and 100.

• Does not incorporate intra-bar volume distribution.

• Does not separate buy/sell volume.

B) SMART RSI – Money Flow Bands

1) RSI-to-Price Mapping

Converts RSI values into upper/lower price bands using recent price extremes.

2) Lower Timeframe Volume Decomposition

Retrieves LTF data and splits each bar’s volume into buy (close>open) and sell (close

Smoothed VWAP Bands🎯 Best Smoothing Setting for Scalping (What You Should Use)

Style σ Smoothing Result

Fast scalping (1min) EMA 14 Very responsive, still filters noise

Balanced intraday (1–5min) EMA 20 Best overall reliability

Slow confirmation (5–15min) EMA 30 Eliminates nearly all fakeouts

✅ What We Are Actually Smoothing

You are NOT smoothing VWAP itself.

You are smoothing the standard deviation (σ) that creates the VWAP bands:

✔ What this does:

* Computes the raw standard deviation (σ) of price relative to VWAP

* Smooths that σ using EMA smoothing

* Builds ±1 and ±2 bands using the smoothed σ

* You get clean, stable bands that filter fakeouts

✔ Result:

* Bands do NOT twitch in chop

* Fakeouts are filtered

* Real breakouts show obvious expansion

RED-E Market Structure (Pro V2)RED-E Market Structure - Comprehensive Technical Analysis System

⚠️ EDUCATIONAL TOOL - NO GUARANTEES

This indicator is designed for educational purposes to help traders learn technical analysis concepts. It does not predict future price movements or guarantee profitable trades. Trading involves substantial risk of loss.

═══════════════════════════════════════════════════════════════

📊 WHAT THIS INDICATOR DOES

This indicator combines multiple standard technical analysis methods into a unified system for analyzing market structure, momentum, volume dynamics, and key price levels. Rather than adding 10 separate indicators to your chart, this consolidates related information into one cohesive interface where each component informs the others.

═══════════════════════════════════════════════════════════════

🔧 TECHNICAL METHODOLOGY - HOW IT WORKS

1️⃣ MOMENTUM CANDLE COLORING (6 Levels)

Calculation Method:

- Compares close vs EMA(9) and EMA(21)

- Applies RSI(14) thresholds for strength

- Color codes: Royal Blue (strongest bull) → Cyan → Green → Yellow → Orange → Red (strongest bear) → White (neutral)

Formula Logic:

IF close > EMA(9) AND close > EMA(21) AND close > open:

RSI > 70 = Level 3 Bull (Royal Blue)

RSI 60-70 = Level 2 Bull (Cyan)

RSI < 60 = Level 1 Bull (Green)

Purpose: Visualizes momentum strength by combining trend (EMAs), candle direction, and overbought/oversold conditions (RSI).

2️⃣ ENTRY SIGNAL LABELS

Calculation Method:

- Uses EMA alignment: EMA(9) > EMA(21) > EMA(50) for bullish

- Filters RSI to avoid extremes

- Requires confirming candle

BUY Signal Logic:

IF close > EMA(9) AND RSI between 40-70 AND EMA(9) > EMA(21) > EMA(50) AND close > open

THEN: Display "BUY" label

Purpose: Identifies potential entries when multiple trend and momentum conditions align. This is standard multi-confirmation technical analysis.

3️⃣ VOLUME DELTA PERCENTAGE

Calculation Method:

FOR each bar in lookback period (default 20):

IF close > open: add volume to bullish_volume

IF close < open: add volume to bearish_volume

bullish_percent = (bullish_volume / total_volume) × 100

Purpose: Quantifies buying vs selling pressure as percentages. Shows if volume supports the current trend.

Display: "🟢65.3% | 🔴34.7%" in dashboard

4️⃣ PRE-MARKET HIGH/LOW TRACKING

Calculation Method:

1. Detect pre-market session (4:00-9:30 AM ET)

2. Track highest high during pre-market

3. Track lowest low during pre-market

4. Draw horizontal lines when market opens

Purpose: Pre-market levels often act as support/resistance during regular hours. This automates their tracking and visualization.

5️⃣ OPENING RANGE BREAKOUT (ORB)

Calculation Method:

1. User sets start time (default 9:30 AM) and duration (default 15 min)

2. Track highest high and lowest low during this period

3. Draw box and extend lines

Purpose: The opening range breakout is a well-documented day trading strategy. First X minutes establish a range, and breakouts often signal directional moves.

6️⃣ SUPPORT/RESISTANCE TRENDLINES

Calculation Method:

1. Identify pivot highs: ta.pivothigh(high, 5, 5)

2. Identify pivot lows: ta.pivotlow(low, 5, 5)

3. Connect last two pivot highs = Resistance (red)

4. Connect last two pivot lows = Support (blue)

Purpose: Automatically connects significant pivot points. Based on standard pivot analysis where price respects these levels.

7️⃣ GAMMA ZONE DETECTION

Calculation Method:

1. Calculate 30-min range: (high - low)

2. Calculate 10-period SMA of range

3. Calculate ratio: current_range / average_range

IF ratio < (1.0 / sensitivity): HIGH GAMMA = Low volatility

IF ratio > (1.0 × sensitivity): LOW GAMMA = High volatility

Purpose: Approximates options gamma effects. High gamma = dealers hedge more = suppressed volatility. Low gamma = less hedging = potential explosive moves.

8️⃣ TAKE PROFIT LEVELS (5 Levels + ATR Stop Loss)

Calculation Method:

LONG: TP = entry_price × (1 + percentage/100)

SHORT: TP = entry_price × (1 - percentage/100)

Stop Loss (ATR): entry ± (ATR(14) × multiplier)

Purpose: Automatically calculates percentage-based targets and volatility-adjusted stops. ATR adapts stop to current market conditions.

9️⃣ THE STRAT PATTERN RECOGNITION

Calculation Method:

Compare current bar to previous:

- Strat 3 (outside bar): high > high AND low < low

- Strat 1 (inside bar): high ≤ high AND low ≥ low

- Strat 2 (directional): All others

Purpose: The Strat is a price action system categorizing bars by relationship to previous bars. This automates classification.

🔟 FIBONACCI RETRACEMENTS

Calculation Method:

1. Find highest high in lookback (default 30 bars)

2. Find lowest low in lookback

3. Calculate: 0.0, 0.382, 0.5, 0.618, 1.0 levels

Purpose: Standard Fibonacci tool. These ratios are commonly used support/resistance in technical analysis.

1️⃣1️⃣ MULTI-TIMEFRAME ANALYSIS

Calculation Method:

FOR each timeframe (default 15m, 1H, 4H):

Check if close > EMA(9) on that timeframe

IF true: "BULLISH", else: "BEARISH"

Purpose: Shows trend alignment across timeframes using Pine's request.security(). Common confirmation technique.

═══════════════════════════════════════════════════════════════

💡 WHY THESE COMPONENTS WORK TOGETHER

This indicator's originality lies in its unified system approach:

1. TREND IDENTIFICATION (EMAs, MTF) - Shows direction

2. MOMENTUM MEASUREMENT (RSI, candles) - Shows strength

3. VOLUME CONFIRMATION (Volume Delta) - Shows conviction

4. KEY LEVELS (PM, ORB, Fib, S/R) - Shows decision points

5. RISK MANAGEMENT (TP levels, ATR stops) - Shows exits

VALUE OF INTEGRATION:

Rather than 10 separate indicators creating chart clutter, this consolidates related concepts where each component provides different information that, when viewed together, gives a more complete market picture.

Example Integration:

- Entry signal appears (EMA + RSI aligned)

- Volume Delta confirms (more buying than selling)

- MTF shows higher timeframes agree

- TP levels auto-calculate with good risk:reward

- Support trendline nearby provides stop reference

═══════════════════════════════════════════════════════════════

⚙️ CUSTOMIZATION OPTIONS

All features independently toggleable:

- EMAs: Adjust lengths (9, 21, 50, 200), colors, widths

- RSI: Change overbought/oversold levels (70/30)

- Volume Delta: Adjust lookback period (20)

- ORB: Set custom start time, duration, timezone

- Gamma: Adjust sensitivity (1-10)

- TP Levels: Customize all 5 percentages

- Dashboard: Reposition, resize, recolor

═══════════════════════════════════════════════════════════════

📖 HOW TO USE

Step 1 - Assess Context:

- Check MTF Dashboard for alignment

- Check EMA indicator for trend

- Check Gamma Zone for volatility expectation

Step 2 - Identify Setups:

- Wait for BUY/SELL signal

- Check Volume Delta matches direction

- Verify RSI not extreme (30-70)

- Look for support/resistance confluence

Step 3 - Evaluate Risk:Reward:

- Review TP3 R:R ratio (target 2:1+)

- Check stop loss placement

- Ensure risk acceptable

Step 4 - Monitor:

- Track P&L % in real-time

- Use TP levels as potential exits

- Adjust stops based on S/R

═══════════════════════════════════════════════════════════════

⚠️ LIMITATIONS & REALISTIC EXPECTATIONS

This indicator does NOT:

- Predict future price movements

- Guarantee profitable trades

- Work in all market conditions

- Replace proper education and practice

This indicator CAN:

- Display standard technical indicators in organized way

- Automate common calculations

- Visualize multiple analysis methods simultaneously

- Help learn how different indicators relate

Key Understanding:

All technical indicators use historical data. They help identify patterns and conditions but cannot predict the future. Successful trading requires risk management, psychology, and experience—not just indicators.

═══════════════════════════════════════════════════════════════

📚 EDUCATIONAL CONCEPTS TAUGHT

- How EMAs show trend direction and alignment

- How RSI identifies momentum extremes

- How volume confirms or diverges from price

- How support/resistance levels form

- How multiple timeframes provide context

- How ATR adapts stops to volatility

- How risk:reward ratios work

═══════════════════════════════════════════════════════════════

📊 BEST SUITED FOR

- Scalping: 1m-5m charts with quick entries/exits

- Day Trading: 15m-1H focusing on ORB and PM levels

- Swing Trading: 4H-D following major trends

═══════════════════════════════════════════════════════════════

⚠️ RISK DISCLAIMER

Trading involves substantial risk of loss. This educational tool:

- Does NOT guarantee profits

- Cannot predict future performance

- Requires proper risk management

- Should be practiced on demo accounts first

Always use stop losses, risk only 1-2% per trade, and consult licensed financial professionals before trading with real capital.

═══════════════════════════════════════════════════════════════

Educational tool for learning technical analysis. Not financial advice. Past results do not indicate future performance.

NEW PRICE ACTION ALGO (v2)Updated price action indicator for day trading QQQ,SPY & IWM on the 5-6min chart

One Minute AI scalper keep extended trading hours on# One Minute AI Scalper - Trading Indicator

## Overview

The One Minute AI Scalper is a precision-engineered trading indicator designed specifically for short-term scalping strategies on 1-minute timeframes. This indicator combines multiple technical analysis methods to identify high-probability entry points for both long and short positions, making it ideal for active traders seeking quick, momentum-based opportunities.

## Key Features

### Visual Signals

- **Long Entry Arrows**: Clear green triangle markers appear below price bars when bullish conditions align

- **Short Entry Arrows**: Clear red triangle markers appear above price bars when bearish conditions align

- Clean, uncluttered chart interface focusing on actionable signals

### Advanced Signal Generation

The indicator utilizes a sophisticated multi-factor approach to generate trading signals:

1. **Trend Analysis**: Employs moving average crossover methodology to identify the prevailing market direction

2. **Momentum Confirmation**: Analyzes candlestick patterns and price behavior to confirm momentum strength

3. **Volume Validation**: Incorporates volume analysis to distinguish between high-conviction and standard signals

4. **Reversal Detection**: Identifies potential trend reversals by examining recent price action patterns

5. **Precision Entry Filtering**: Uses specific candlestick characteristics to minimize false signals

### Alert System

Comprehensive alert functionality for all signal types:

- Long Entry alerts

- Short Entry alerts

## How It Works

### Long Position Signals

The indicator generates long entry signals when multiple bullish conditions simultaneously align, including:

- Confirmation of upward momentum through price action

- Specific candlestick structure indicating strong buying pressure

- Price position relative to key moving averages

- Recent price behavior suggesting reversal potential

- Volume characteristics supporting the move

### Short Position Signals

Short entry signals are generated when multiple bearish conditions converge, including:

- Confirmation of downward momentum through price action

- Specific candlestick structure indicating strong selling pressure

- Price position relative to key moving averages

- Recent price behavior suggesting reversal potential

- Volume characteristics supporting the move

### Position Management

The indicator includes intelligent position state tracking to:

- Prevent duplicate signals while in an active position

- Generate exit signals based on opposing price action

- Maintain clear status of whether you're in a long or short position

## Best Practices

### Recommended Usage

- **Timeframe**: Optimized for 1-minute charts

- **Extended Hours**: Keep extended trading hours enabled for full market coverage

- **Markets**: Works on stocks, forex, crypto, and futures

- **Strategy**: Best suited for scalping and day trading strategies

### Risk Management

- Always use proper stop-loss orders

- Consider position sizing based on account risk tolerance

- Pay attention to volume-indicated signals for higher conviction trades

- Avoid trading during low-liquidity periods

- Combine with your own risk management rules

### Trading Tips

- Higher volume signals generally indicate stronger conviction

- Wait for clear arrow signals rather than trying to anticipate them

- Monitor overall market conditions and major support/resistance levels

- Be aware of news events that may cause unusual volatility

- Practice in a paper trading account before using real capital

## Important Notes

### What This Indicator Does

✅ Provides clear visual entry signals for long and short positions

✅ Incorporates multiple technical factors for signal generation

✅ Includes volume analysis for conviction assessment

✅ Offers comprehensive alert options for all signal types

✅ Maintains position state awareness

### What This Indicator Doesn't Do

❌ Does not guarantee profitable trades

❌ Does not provide specific price targets or stop-loss levels

❌ Does not replace the need for proper risk management

❌ Does not account for fundamental analysis or news events

❌ Does not adapt settings automatically to market conditions

## Disclaimer

This indicator is provided for educational and informational purposes only. It is not financial advice, and past performance does not guarantee future results. Trading involves substantial risk of loss, and you should only trade with capital you can afford to lose. Always conduct your own research and consider consulting with a qualified financial advisor before making trading decisions.

## Configuration

This indicator uses fixed, optimized parameters that have been carefully calibrated for 1-minute scalping. No user configuration is required - simply add it to your chart and monitor for signals.

## Support

For questions, suggestions, or feedback about this indicator, please use the comments section or contact the author directly through TradingView.

---

**Version**: 6.0

**Category**: Momentum/Scalping

**Overlay**: Yes

**Timeframe**: 1 minute (optimized)

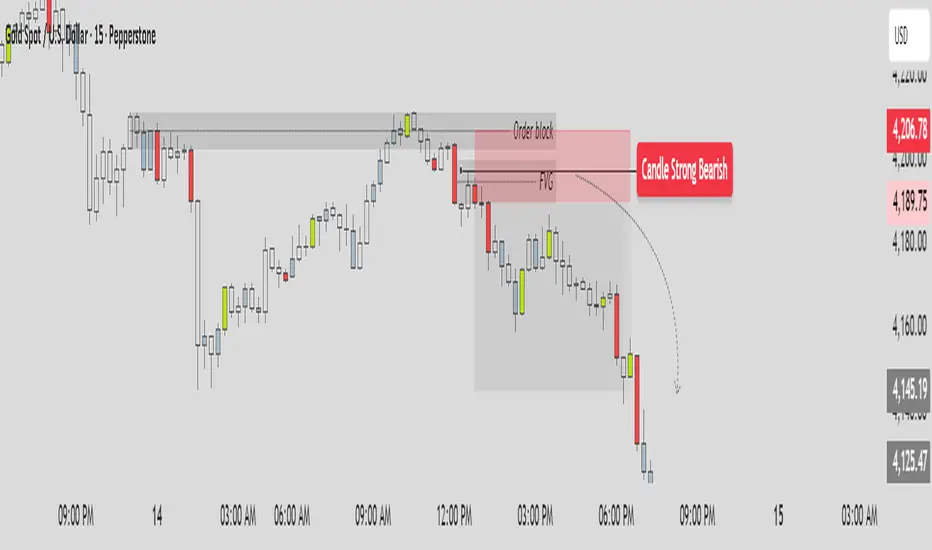

Fair Value Gaps - Cucaracha📘 Fair Value Gaps (FVG) – Clean, Automatic Detection & Real-Time Tracking

The Fair Value Gaps (FVG) indicator automatically detects and visualizes Bullish and Bearish Fair Value Gaps directly on your chart. Built with precision, it highlights imbalance zones, continuously extends them in real time, and removes them the moment they’re mitigated — giving you a clean and accurate market structure view.

✅ Key Features

Automatic FVG Detection

Identifies bullish and bearish FVGs using a strict 3-candle imbalance model.

Dynamic Boxes

Each detected FVG is drawn as a shaded box and extends forward until price fills or mitigates the zone.

Auto-Cleanup (Mitigation Logic)

When price returns to the gap and fills it, the zone is instantly removed, keeping your chart clean and focused.

Custom Colors

Choose your own colors for bullish and bearish FVG boxes.

🎯 Why Traders Use This

Fair Value Gaps are widely used in:

Smart Money Concepts (SMC)

ICT-style trading

Market imbalance analysis

They highlight areas where price moved aggressively and may later return to rebalance.

This indicator helps you:

Spot institutional imbalances instantly

Track unmitigated FVGs without manually drawing boxes

Stay focused on key reaction zones

Improve entries based on premium/discount and liquidity concepts

🧠 How It Works

Bullish FVG:

Occurs when price leaves a gap where low > high , creating an upward imbalance zone.

Bearish FVG:

Occurs when high < low , indicating a downward imbalance zone.

Detected gaps are plotted as forward-extending boxes until price mitigates them.

Once mitigated (price fills the gap), the zone is automatically removed.

🟦🟥 Visuals

Blue (or your chosen color): Bullish FVG

Red (or your chosen color): Bearish FVG

150% Volume Surge1M charts show 150% volume surge to confirm scalping oppos in the direction of the general trend.

Cumulative Volume Delta Divergence [TradingFinder] Periodic EMACVD Divergence with Alerts.

Cumulative Volume Delta Divergence Periodic EMA with some alerts added

TSI.LTA | Base BTC 1DTSI.LTA | Base BTC 1D is a closed‑source trend‑following strategy designed for BTC on the 1D timeframe .

It focuses on participating in the main directional moves of the market while avoiding as much short‑term noise as possible.

📊 The script:

Uses a combination of moving‑average–based filters and volatility bands to define the active trend.

Applies optional volume filters to avoid low‑participation or exhausted moves.

Includes risk‑management controls (Stop Loss, Take Profit, Trailing Stop) that work on a per‑trade basis.

All entries and exits are confirmed at bar close and the script does not repaint .

This makes it suitable for backtesting, alerts and external automation.

█ 💡 CONCEPTS

This strategy is built around a few simple ideas:

1 — Trend first.

Positions are only taken when a group of smoothed trend filters agree on direction.

The goal is to ride larger swings, not to scalp each fluctuation.

2 — Volatility awareness.

Standard‑deviation–based bands help avoid entries in abnormal spikes or during very compressed ranges.

3 — Participation filter.

Optional volume‑based conditions (VWMA, OBV slope, MFI, volume Z‑score) try to ensure that entries occur when the market shows enough activity, not during dead phases.

4 — Risk defined in advance.

Stop‑loss and trailing‑stop inputs are expressed as percentages relative to entry price, so users can align them with their own risk tolerance.

The logic is purposely conservative: it is expected to stay flat during parts of the market where the trend is unclear or participation is weak.

█ ⚙️ FEATURES & INPUTS

This section follows approximately the order of the script’s inputs, so users can read here and then match what they see in the “Inputs” tab.

1 — 📐 Trend filters

These inputs control how the strategy detects the underlying trend:

DEMA / Gaussian / SMMA lengths

Control how fast or slow the trend reacts to price changes.

Shorter lengths → more responsive, more trades, more noise.

Longer lengths → slower reaction, fewer trades, more filtering.

Volatility Bands (SD length & multipliers)

Standard‑deviation bands around the smoothed price series.

They are used to avoid entries during extreme moves or very narrow ranges where a breakout is not yet confirmed.

In practice, these settings let the user choose between a more “aggressive” trend follower (shorter lengths, smaller bands) or a more “patient” one.

2 — 📊 Volume filters (optional)

These filters are meant to restrict trades to periods where the market shows meaningful participation:

VWMA filter

Requires price to be aligned with a Volume‑Weighted Moving Average, which de‑emphasizes moves on very low volume.

OBV slope filter

Uses the slope of On‑Balance Volume to check that net volume flow supports the direction of the trade.

MFI band filter

Uses the Money Flow Index to avoid taking new entries in zones that often correspond to exhaustion (extreme values defined by the user).

Volume Z‑Score

Compares current volume to its recent history. Trades can be restricted when volume is unusually low or out of character for that period.

When any of these filters are turned off, the strategy relies only on price‑based trend and volatility logic.

When they are on, trades are more selective and may be fewer.

3 — 🛡️ Risk management

These inputs define how individual trades are managed once entered.

They do not change the trend logic itself:

Stop Loss (%)

A percentage move against the entry price that will close the position.

Typical values on BTC 1D remain in the single‑digit range so that no single trade risks an unrealistic portion of equity.

Take Profit (%)

An optional fixed target that closes the trade when price has moved a chosen percentage in favor.

This can be disabled if the user prefers to let the trend filters perform the exit.

Trailing Stop (%)

A stop that follows the most favorable price reached since entry.

When the “use lower timeframe peak” option is enabled, peaks can be detected on a lower timeframe for more granular trailing, while decisions still occur at the close of the 1D bar.

Fixed SL/TP Price and Activation Date

Allow defining absolute price levels and a date from which they start applying.

This is useful when the user wants structural protection around known price zones.

The combination of these controls determines how deep a pullback the user is willing to tolerate and how much profit they are prepared to give back in order to stay in trends.

4 — 🚫 Filter failure & cooldown

To avoid over‑trading in difficult environments, the script can:

Automatically exit when filters remain unfavorable for a configurable number of bars.

Enter a cooldown period, during which no new trades are taken, even if some conditions improve.

These mechanisms are intended to protect capital during choppy or low‑quality phases rather than force constant exposure.

█ 📚 HOW TO USE

A suggested process for using this strategy as a study tool:

1 — Start on BTC 1D.

Apply the script to BTCUSD or BTC/USDT on the 1D timeframe, with default inputs.

2 — Open the Strategy Tester.

Choose a time window (for example a full halving cycle, a crash + recovery period, or just the most recent bull leg).

3 — Compare with Buy & Hold.

For the same window, look at:

Net profit of the strategy vs Buy & Hold.

Max drawdown of the strategy vs Buy & Hold.

The goal is not to hit a particular number, but to see whether, in that window, the strategy manages to:

Provide a smoother equity curve (lower drawdown),

While still performing at least as well as, or better than, simply holding the asset.

4 — Experiment with risk inputs.

Vary Stop Loss, Trailing Stop and the volume filters.

After each change, re‑check the same two questions above. This should make clear how each input affects the trade‑off between participation and risk.

5 — Forward‑test.

Before using any configuration with real capital, let it run for a while in paper‑trading or demo conditions.

█ 🚧 LIMITATIONS

The strategy is built and tuned primarily for BTC on 1D.

It can be used on other symbols and timeframes, but behavior may differ and requires new testing.

In very tight ranges or during event‑driven gaps, trend logic may enter later than discretionary trading would. This is expected for a conservative trend‑following approach.

Results from historical backtests depend on data quality, broker settings, fees and slippage configured in the Strategy Tester.

█ 📝 NOTES

Signals are generated on bar close.

The script is closed‑source, but the description explains the main ideas so users and moderators can understand what it does and how to use it.

The HUD on the chart is meant as a compact summary of the same statistics available in the Strategy Tester; it simply makes comparisons quicker.

█ ⚠️ DISCLAIMER

This strategy is provided for educational and research purposes only .

It is not financial advice and does not recommend any specific trades, assets, position sizes, or risk levels.

Users are fully responsible for:

Choosing their own risk parameters (Stop Loss, Take Profit, Trailing Stop, position sizing, etc.).

Testing the script on the markets and timeframes they intend to trade.

Verifying that any configuration is appropriate for their capital, risk tolerance and jurisdiction.

Past performance in backtests or examples does not guarantee future results.

Always test carefully before considering any live deployment.

Frequency Momentum Oscillator [QuantAlgo]🟢 Overview

The Frequency Momentum Oscillator applies Fourier-based spectral analysis principles to price action to identify regime shifts and directional momentum. It calculates Fourier coefficients for selected harmonic frequencies on detrended price data, then measures the distribution of power across low, mid, and high frequency bands to distinguish between persistent directional trends and transient market noise. This approach provides traders with a quantitative framework for assessing whether current price action represents meaningful momentum or merely random fluctuations, enabling more informed entry and exit decisions across various asset classes and timeframes.

🟢 How It Works

The calculation process removes the dominant trend from price data by subtracting a simple moving average, isolating cyclical components for frequency analysis:

detrendedPrice = close - ta.sma(close , frequencyPeriod)

The detrended price series undergoes frequency decomposition through Fourier coefficient calculation across the first 8 harmonics. For each harmonic frequency, the algorithm computes sine and cosine components across the lookback window, then derives power as the sum of squared coefficients:

for k = 1 to 8

cosSum = 0.0

sinSum = 0.0

for n = 0 to frequencyPeriod - 1

angle = 2 * math.pi * k * n / frequencyPeriod

cosSum := cosSum + detrendedPrice * math.cos(angle)

sinSum := sinSum + detrendedPrice * math.sin(angle)

power = (cosSum * cosSum + sinSum * sinSum) / frequencyPeriod

Power measurements are aggregated into three frequency bands: low frequencies (harmonics 1-2) capturing persistent cycles, mid frequencies (harmonics 3-4), and high frequencies (harmonics 5-8) representing noise. Each band's power normalizes against total spectral power to create percentage distributions:

lowFreqNorm = totalPower > 0 ? (lowFreqPower / totalPower) * 100 : 33.33

highFreqNorm = totalPower > 0 ? (highFreqPower / totalPower) * 100 : 33.33

The normalized frequency components undergo exponential smoothing before calculating spectral balance as the difference between low and high frequency power:

smoothLow = ta.ema(lowFreqNorm, smoothingPeriod)

smoothHigh = ta.ema(highFreqNorm, smoothingPeriod)

spectralBalance = smoothLow - smoothHigh

Spectral balance combines with price momentum through directional multiplication, producing a composite signal that integrates frequency characteristics with price direction:

momentum = ta.change(close , frequencyPeriod/2)

compositeSignal = spectralBalance * math.sign(momentum)

finalSignal = ta.ema(compositeSignal, smoothingPeriod)

The final signal oscillates around zero, with positive values indicating low-frequency dominance coupled with upward momentum (trending up), and negative values indicating either high-frequency dominance (choppy market) or downward momentum (trending down).

🟢 How to Use This Indicator

→ Long/Short Signals: the indicator generates long signals when the smoothed composite signal crosses above zero (indicating low-frequency directional strength dominates) and short signals when it crosses below zero (indicating bearish momentum persistence).

→ Upper and Lower Reference Lines: the +25 and -25 reference lines serve as threshold markers for momentum strength. Readings beyond these levels indicate strong directional conviction, while oscillations between them suggest consolidation or weakening momentum. These references help traders distinguish between strong trending regimes and choppy transitional periods.

→ Preconfigured Presets: three optimized configurations are available with Default (32, 3) offering balanced responsiveness, Fast Response (24, 2) designed for scalping and intraday trading, and Smooth Trend (40, 5) calibrated for swing trading and position trading with enhanced noise filtration.

→ Built-in Alerts: the indicator includes three alert conditions for automated monitoring - Long Signal (momentum shifts bullish), Short Signal (momentum shifts bearish), and Signal Change (any directional transition). These alerts enable traders to receive real-time notifications without continuous chart monitoring.

→ Color Customization: four visual themes (Classic green/red, Aqua blue/orange, Cosmic aqua/purple, Custom) allow chart customization for different display environments and personal preferences.

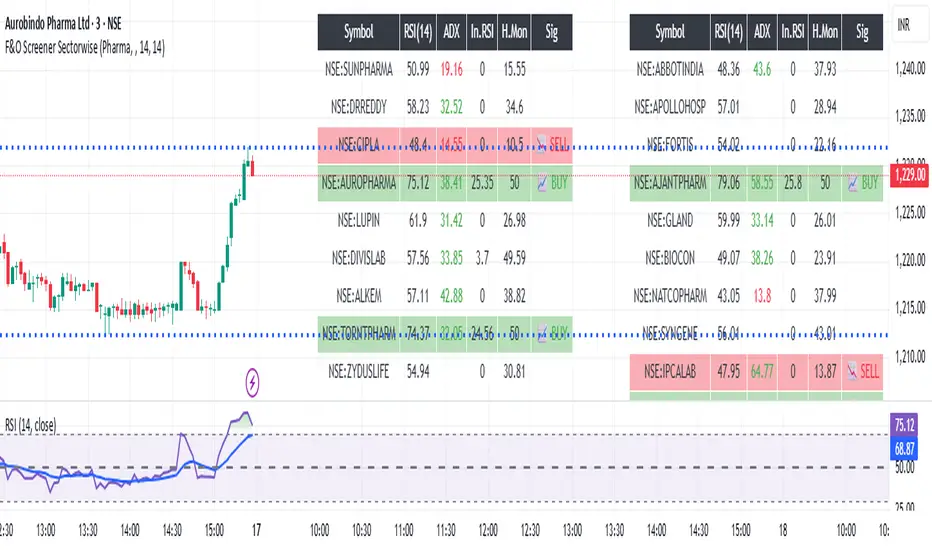

NIFTY FNO STOCK (UPDATED)New latest FNO stock Shown at top of the table in indicator for buy and sell signal in sectorwise stock selection

NIFTY FNO Stock Screener Sector-wiseNSE FNO STOCK SCREENER SECTOR WISE. Open indicator and select sector. find which sector is moving upward or downward today. select specific sector and you will see all stock list in selected sector. you will show buy and sell signal in particular sector. open stock which show buy or sell signal and check your requirement for buy or sell . you can also used for options also to buy as per required signal

Vol——BcnkVol-Bcnk Volume Indicator Introduction

Overview

Vol-Bcnk is an advanced volume analysis indicator built on Pine Script 6 that helps traders identify abnormal trading volume activity through statistical analysis and heatmap visualization. This indicator not only displays basic volume data but also classifies volume strength through a multi-level threshold system with color coding.

Core Features

1. Intelligent Volume Analysis

· Moving Average Baseline: Uses configurable moving average length (default 610 periods) as volume baseline

· Standard Deviation Measurement: Calculates how many standard deviations current volume is from historical average

· Dynamic Thresholds: Automatically adjusts sensitivity based on market volatility

2. Multi-Level Heatmap System

The indicator provides five clear volume strength levels:

Extra High - More than 4.0 standard deviations (Red) - Extreme abnormality, may indicate major events

High - 2.5 to 4.0 standard deviations (Orange) - Significant abnormality, strong signals

Medium - 1.0 to 2.5 standard deviations (Yellow) - Moderate abnormality, worth attention

Normal - -0.5 to 1.0 standard deviations (Light Blue) - Normal fluctuation range

Low - Less than -0.5 standard deviations (Dark Blue) - Below average volume

3. Dual Color Mode System

Heatmap Mode

· Colors based solely on volume strength

· Unified color scheme focused on pure volume analysis

Up/Down Mode

· Combines price direction with volume strength

· Green shades for up moves, red shades for down moves

· Provides richer market context information

4. Multiple Visualization Options

· Colored Volume Bars: Visual display of each strength level

· Heatmap Zone Backgrounds: Background colors for each threshold range

· Threshold Level Lines: Mark key threshold positions

· Moving Average Line: Optional volume baseline display

Parameter Configuration

Main Settings

· MA Length: Moving average period, controls baseline smoothness

· Standard Deviation Length: Standard deviation calculation period, affects volatility sensitivity

Threshold Adjustment

Users can customize standard deviation multipliers for each strength level to adapt to different market characteristics:

· Smaller values: More sensitive, suitable for short-term trading

· Larger values: More conservative, suitable for long-term analysis

Alert System

The indicator includes a comprehensive alert mechanism for:

· Volume anomalies at each strength level

· Abnormal volume differentiated by upward and downward direction

· Real-time trading opportunity notifications

Application Scenarios

1. Breakout Confirmation

Identifies abnormal volume accompanying price breakouts to verify authenticity

2. Reversal Signals

Extreme volume combined with price reversal patterns provides high-probability reversal signals

3. Trend Strength Assessment

Evaluates current trend sustainability through volume strength distribution

4. Institutional Activity Detection

Abnormally high volume may reveal institutional large orders entering or exiting

Usage Recommendations

Short-Term Trading

· Use shorter MA and standard deviation periods (like 50-100)

· Focus on High and Extra High level signals

· Confirm with price action

Long-Term Investing

· Use longer periods (like default 610)

· Mainly focus on Extra High level significant anomalies

· Combine with fundamental analysis

Vol-Bcnk provides traders with a powerful volume analysis tool through scientific statistical methods and intuitive visualization, helping identify truly important volume activities in the market while avoiding distraction from normal market noise in decision-making.

Nifty FNO Stock Screener Sector wise (Protected)NSE FNO STOCK SCREENER SECTOR WISE. Open indicator and select sector. find which sector is moving upward or downward today. select specific sector and you will see all stock list in selected sector. you will show buy and sell signal in particular sector. open stock which show buy or sell signal and check your requirement for buy or sell . you can also used for options also to buy as per required signal

SHA CandleFlow ProSHA CandleFlow Pro v1.0.0 ✨🚀

SHA CandleFlow Pro is a next-generation price-action tool designed to detect high-probability candlestick rejection signals with extreme clarity and precision.

Built for traders who rely on reversal confirmation, wick rejection, momentum shifts, and candle behavior, this indicator helps you instantly visualize where price is likely to reverse, react, or continue with reduced strength.

Whether you trade scalping, intraday, swing, or ICT/SMC concepts, SHA CandleFlow Pro enhances your entries and timing with accurate rejection detection

Core Features ⚙️🔰

- Strong Bullish -> Green color

- Strong Bearish -> Red color

- Medium Bullish/Bearish -> Blue gray color

- Normal Bullish/Bearish -> N/A color

1. Strong Bullish Rejection — Green

Identifies powerful bullish rejection candles with strong wick dominance and momentum absorption.

Green highlights show areas where buyers aggressively step in, signaling high-probability bullish reactions or reversals.

2. Strong Bearish Rejection — Red

Detects strong bearish rejection candles with clear selling pressure.

Red highlights mark zones where sellers strongly reject price, indicating potential downside continuation or reversal points.

3. Medium Bullish / Bearish Rejection — Blue-Gray

For moderate rejection strength, the indicator displays blue-gray highlights.

These candles show noticeable but not extreme rejection, often signaling:

Early reversal signs

Weakening trend

Reaction zones

Potential continuation entries

They act as secondary confirmation.

4. Normal Candles — No Color

If a candle shows no meaningful rejection, no highlight is applied.

This keeps the chart clean and ensures you only focus on:

High-quality rejection

Clear price reaction levels

Relevant market behavior

Normal candles are intentionally ignored to avoid noise and over-signal conditions.

How to Use SHA CandleFlow Pro📘

SHA CandleFlow Pro is designed to help you confirm market reversals, rejections, and price reactions with high precision.

The best way to use it effectively is combine with your strategy to trade.

This is sample how to use it :

⚠️ Disclaimer

The information and tools provided in this script are for educational and informational purposes only.

Trading in the financial markets involves risk of loss and is not suitable for every investor. You are solely responsible for your trading decisions. Always do your own research, use proper risk management, and consult a licensed financial advisor before making any financial decisions.

Ross Cameron 5 Pillars FilterFirst, I am not Ross Cameron. This indicator is based on his five pillars of stock selection.

ROSS CAMERON 5 PILLARS MOMENTUM FILTER

🎯 OVERVIEW

This indicator automatically checks if the current symbol meets Ross Cameron's famous "5 Pillars" stock selection criteria from Warrior Trading - a proven methodology for identifying high-probability momentum day trading setups.

📊 ROSS CAMERON'S 5 PILLARS

1️⃣ RELATIVE VOLUME ≥5x (Automated ✅)

• Compares current volume to 30-day average

• Minimum 5x confirms institutional/retail interest

• High RVol = high liquidity and momentum potential

2️⃣ DAILY % CHANGE ≥10% (Automated ✅)

• Stock must already be showing momentum

• Default threshold: 10% up from previous close

• Confirms demand is already present

3️⃣ NEWS CATALYST (Manual Check ⚠️)

• Breaking news justifies the price movement

• Look for: earnings, FDA approvals, partnerships, contracts

• 🔥 icon flags stocks with ≥15% momentum (likely news-driven)

4️⃣ PRICE RANGE $1-$20 (Automated ✅)

• Sweet spot for retail trader momentum

• Highly volatile small-cap stocks

• Accessible price range for position building

5️⃣ FLOAT <10 MILLION SHARES (Automated ✅)

• Low float creates supply/demand imbalances

• Enables explosive 50-100%+ intraday moves

• Automatically checked when data available

• Shows actual float with ✅/❌ indicator

🚀 KEY FEATURES

✅ GREEN BACKGROUND HIGHLIGHT

• Visual alert when ALL automated criteria are met

• Instantly identify potential setups while scanning watchlist

📋 DETAILED BREAKDOWN TABLE

• Shows pass/fail status for each pillar

• Displays actual values (RVol, %, Float, etc.)

• Color-coded for quick interpretation

🔥 STRONG MOMENTUM INDICATOR

• Highlights stocks ≥15% (likely have news catalyst)

• Helps prioritize which stocks to research first

🔔 BUILT-IN ALERTS

• "Ross Cameron Criteria Met" - All automated criteria pass

• "Strong Momentum Alert" - Stock showing explosive movement

⚙️ FULLY CUSTOMIZABLE

• Adjust all thresholds to your trading style

• Configurable table position and display

• Toggle volume spike filter on/off

💡 HOW TO USE

BEST WORKFLOW:

1. Build a watchlist of small-cap stocks using TradingView's Stock Screener

2. Add this indicator to your charts

3. Flip through your watchlist - look for GREEN BACKGROUNDS

4. Check the table for detailed breakdown of each pillar

5. VERIFY NEWS CATALYST (required for Pillar 3)

6. If float shows N/A, verify manually on Finviz

7. Execute your trading plan with proper risk management

OPTIMAL TIMING:

• Pre-Market (8:00-9:30 AM ET) - Identify gap-up candidates

• Morning Session (9:30 AM-12:00 PM ET) - Prime momentum window

• Avoid lunch hour (12:00-2:00 PM ET) - Low volume, choppy

ALERT SETUP:

1. Click "Create Alert" on your chart

2. Select "Ross Cameron Criteria Met" condition

3. Get notified when new setups appear real-time

⚙️ CUSTOMIZABLE SETTINGS

PILLAR 1 - RELATIVE VOLUME:

• Min RVol: 5.0x (Ross's minimum, increase for more selective)

• RVol Period: 30 days (industry standard)

PILLAR 2 - MOMENTUM:

• Min Daily %: 10% (increase to 15% for stronger setups)

PILLAR 3 - CATALYST:

• Strong Momentum %: 15% (threshold for 🔥 indicator)

PILLAR 4 - PRICE RANGE:

• Min Price: $1.00 (adjust based on account size)

• Max Price: $20.00 (Ross's sweet spot)

PILLAR 5 - FLOAT:

• Max Float: 10M shares (ultra-aggressive traders use 5M)

ADDITIONAL FILTERS:

• Volume Spike: 2x (Warrior Trading standard)

• Confirms intraday momentum continuation

📈 INTERPRETATION GUIDE

✅ GREEN BACKGROUND = GO!

• All automated criteria are met

• Check news catalyst before trading

• Verify setup on chart (not overextended)

• Follow your risk management plan

❌ NO GREEN BACKGROUND = WAIT

• At least one criterion failed

• Check table to see which pillar(s) failed

• May become valid later if momentum increases

🔥 FLAME ICON = HIGH PRIORITY

• Stock showing very strong momentum (≥15%)

• Likely has significant news catalyst

• Research news IMMEDIATELY

• Often the best setups of the day

⚠️ N/A FOR FLOAT = MANUAL CHECK

• TradingView doesn't have float data for this symbol

• Verify on Finviz.com or similar

• If float >10M, setup is invalid per Ross's criteria

📚 RECOMMENDED STRATEGIES

GAP AND GO:

• Stock gaps up 10%+ on news

• Enters above gap high with volume

• Targets: 20-50% gains

VWAP BOUNCE:

• Pullback to VWAP support

• Enters on bounce with volume confirmation

• Tight stop below VWAP

HIGH OF DAY BREAKOUT:

• New HOD with volume surge

• Momentum continuation play

• Trail stop as it runs

ABCD PATTERN:

• Classic reversal pattern

• Enters on D-point breakout

• Target: A-B distance from C

⚠️ RISK WARNINGS

• DAY TRADING IS HIGHLY RISKY - Most day traders lose money

• This indicator finds setups - YOUR EXECUTION determines success

• Always use proper risk management (1-2% risk per trade)

• Never trade without stop losses

• Paper trade extensively before using real money

• Past performance does not guarantee future results

🔧 TECHNICAL DETAILS

• Pine Script v6

• Works on any timeframe (calculates daily metrics automatically)

• Compatible with TradingView Free, Pro, Premium

• No repainting - all calculations based on confirmed data

• Efficient code - minimal lag

📊 DATA SOURCES

• Relative Volume: Calculated from 30-day volume average

• Daily %: Previous day's close vs current price

• Float: TradingView's shares_outstanding_float data

• Volume Spike: 20-period volume moving average

🎯 WHO THIS IS FOR

IDEAL FOR:

✅ Day traders focused on momentum strategies

✅ Traders who follow Ross Cameron/Warrior Trading methodology

✅ Small-cap stock traders ($1-$20 range)

✅ Scalpers and swing traders seeking high-volatility setups

NOT IDEAL FOR:

❌ Long-term investors

❌ Large-cap stock traders

❌ Options-only traders

❌ Traders who don't monitor news catalysts

💬 USAGE TIPS

1. COMBINE WITH OTHER TOOLS

• Use alongside your charting/technical analysis

• Verify pattern setups (bull flags, ABCD, etc.)

• Check Level 2 / Time & Sales for confirmation

2. MAINTAIN A WATCHLIST

• Update daily with fresh small-cap movers

• Use Finviz Gap Scanner as starting point

• Focus on sectors with momentum

3. RISK MANAGEMENT IS KEY

• Never risk more than 1-2% per trade

• Use 2:1 minimum profit/loss ratio

• Cut losses quickly, let winners run

• Position size based on volatility (ATR)

4. TRACK YOUR RESULTS

• Keep a trading journal

• Note which setups work best for you

• Refine criteria based on your data

• Continuous improvement mindset

📝 DISCLAIMER

This indicator is for EDUCATIONAL PURPOSES ONLY. It is not investment advice, a recommendation to buy/sell securities, or a guarantee of profits. Trading involves substantial risk of loss. Always:

• Conduct your own research and due diligence

• Consult with a licensed financial advisor

• Never risk money you cannot afford to lose

• Understand that most day traders lose money

• Practice in a simulator before trading real money

The creator of this indicator is not affiliated with Ross Cameron or Warrior Trading. This is an independent implementation of publicly available trading methodology.

📈 SUPPORT & FEEDBACK

If you find this indicator helpful, please:

• Give it a thumbs up 👍

• Leave a comment with your experience

• Share with other momentum traders

• Follow for updates and new indicators

For questions or suggestions, leave a comment below!

---

🏆 HAPPY TRADING! Remember: The indicator finds opportunities, but YOUR discipline, risk management, and execution determine your success.

#DayTrading #Momentum #RossCameron #WarriorTrading #SmallCaps #GapAndGo #Scalping #StockScreener

DMV Volume Volume Radar SIMPLEThis indicator helps identify early signs of accumulation, breakout, and distribution by analyzing relative volume and price action within defined ranges.

It detects:

🔵 ACCUM: High relative volume with buying pressure near support (early accumulation)

🟢 BRK: High relative volume near range high with bullish price action (potential breakout)

🔴 DIST: High relative volume with selling pressure near range high (distribution / potential reversal)

How it works:

Measures relative volume vs. a moving average

Builds a dynamic price range using recent swing highs/lows

Looks for wick behavior + location in range to validate signals

Color-codes candles and adds labels for quick visualization

Optional alert conditions are baked in for automated notifications

Perfect for:

Pre-breakout positioning

Spotting smart-money accumulation

Identifying distribution zones for exits or reversals

Works best on 15m–4h timeframes for crypto and alts

Adaptive Window Volume ProfileThe indicator builds a rolling volume profile over a chosen time window (1, 3, 12 months or lower), finds POC, VAH/VAL, RH/RL, HVN/LVN, and then overlays volume-driven bar colors (climax, initiative, absorption) filtered by a 30-day RVWAP trend, so you can see where big volume traded and who is winning there right now.

Example Use Case:

How to use it on 4H with 3-month and 12-month rolling profiles:

On a 4H chart, you run two copies of the indicator, both in Rolling Lookback mode, both using the Full (Overlap) engine:

Instance A – 12-month rolling profile (macro map):

-Rolling Unit: Months

-Rolling Length: 12

This gives you the 1-year composite:

-12M RH / RL → outer range of where almost all yearly volume traded (macro high/low “rails”).

-12M VAH / VAL → yearly value area: where the market has been comfortable doing business over the last year.

-12M POC → the single most traded price of the last 12 months (macro gravity).

-12M HVNs/LVNs → long-term shelves (acceptance) and gaps (knife-edges).

Use this instance to answer:

Where are we in the last year’s distribution, and are we approaching macro extremes or living in fair value?

-Combine it with the 30-day RVWAP regime the script computes:

-Above RVWAP and RVWAP rising → macro bull tilt.

-Below RVWAP and RVWAP falling → macro bear tilt.

For example:

-Price near 12M RL with RVWAP bull → potential deep-discount accumulation zone.

-Price near 12M RH with RVWAP bear → potential exhaustion / distribution zone.

Instance B – 3-month rolling profile (tactical map)

-Rolling Unit: Months

-Rolling Length: 3

This builds a 3-month composite on top of your 4H chart:

-3M RH / RL → extremes of the current quarter’s trading.

-3M VAH / VAL → current “fair value box” for the last 90-ish days.

-3M POC → where recent volume concentrates most heavily.

-3M HVNs/LVNs → fresh shelves and gaps inside the bigger yearly structure.

You use this instance for actual trade locations and management:

-Pullbacks into 3M VAL / RL that still sit inside the 12M value and in a bull RVWAP regime → high-probability dip-buy zones; you then look for bull initiative/absorption bar colors to confirm entry.

-Rallies into 3M VAH / RH that line up near 12M VAH / RH in a bear RVWAP regime → good areas to look for shorts, especially when you see bear climax/initiative bars there.

-3M LVNs that coincide with 12M LVNs or VA edges act as sharp decision points: acceptance through often means expansion; rejection often means reversal.

How it all fits together

On your 4H chart, with both instances active:

-12M profile = macro context and big terrain (where the yearly battlefield is).

-3M profile = tactical zones (where to actually trade inside that terrain).

-Bar colors (climax / initiative / absorption) filtered by 30-day RVWAP = timing + confirmation at those levels, favoring the side that has trend and effort behind it.

So the indicator, used this way, becomes:

-one instance to tell you where the big war is being fought (12M)

-one instance to tell you where the current campaign inside that war is concentrated (3M)

-bar colors to tell you whether the team you want to back is actually showing up with size when price hits those levels.