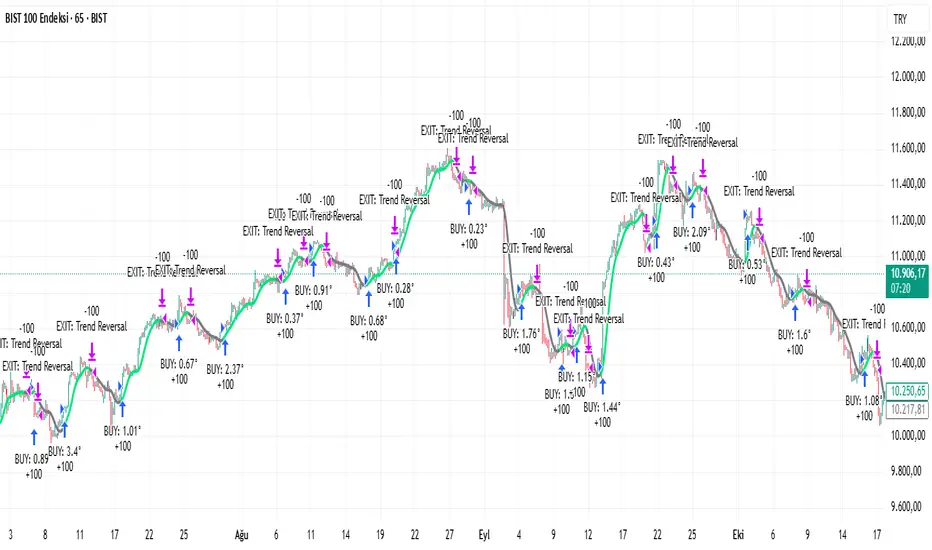

Double MOST with Pivot and EMAMOST Long Strategy with Multi-Filter Confirmation (Pivot + VAR Trend Filter)

This strategy combines a custom MOST stop-line structure with a moving average trend filter (EMA / VAR / ZLMA), daily pivot levels, and a 9-period VAR filter to generate clean long-only entries.

It aims to capture early trend continuations while avoiding reversals and false breakouts.

✔ Buy Conditions

A long position is opened only if all of the conditions below occur simultaneously:

MA (ort) > MOST Line (s2)

– Confirms that momentum is on the long side.

Price > Daily Pivot (pvt_gun)

– Ensures the market is trading above the day’s fair-value level.

Price > VAR(9)

– Short-term VAR filter to confirm trend strength and reduce noise.

Only the first bar where all conditions turn true generates a position.

✔ Sell Condition

A long position is closed when:

MOST Line (s2) crosses above MA (ort)

– Indicates a momentum shift against the long position.

✔ Execution Style (MetaStock-like)

Strategy operates long-only

Orders are filled on the next bar open, not on the signal bar

Commission: 0.03% (3 bps / on-binde 3)

Position size: 100% of equity per trade

This makes the behavior comparable to classical MetaStock backtesting logic.

✔ Chart Markers

Only actual trade entries and exits are drawn

No repeated signals or overlapping markers

Clean visual trade history

Purpose

This strategy is ideal for traders who want:

A structured long-only trend model

A multi-layer confirmation filter

Clean execution without repaint

High-quality entries above market structure levels

Estrategia Pine Script®