Ichimoku Kinko Hyo: ETH 3h Strategy by tobunoIchimoku Kinko Hyo strategy for long term trend trades of Ethereum . Optimized for 3H ticks.

Strategy

Super Z strategy - Thanks to Rafael Zioni//Original script

//https://www.tradingview.com/script/wYknDlLx-super-Z/

This is a test for verifying if this interesting study works well.

The author, thanks to him!!!, advise a possible repaint because the script uses security function.

Refer to tradingview.com for more info on repainting:

www.tradingview.com

QUOTE:

We can see repainting in the following cases:

1- Strategies using calc_on_every_tick=true. A strategy with parameter calc_on_every_tick = false may also be prone to repainting, but to a lesser degree.

(this is not the case, ndr).

2- Using security for requesting data from a resolution higher than the resolution of the chart’s main symbol (i.e. do not use ion weelky chart if you set 1440 (1Day) in inputs)

NOTE: Thanks again to Rafael Zioni. If he requires to delete this strategy, I'll do immediately.

Mean Reversion w/ Bollinger BandsThis is a more advanced version of my original mean reversion script.

It employs the famous Bollinger Bands.

This robot will buy when price falls below the lower Bollinger Band, and sell when price moves above the upper Bollinger Band.

I've only tested it on the S&P 500, though you could try it out on other assets to see the backtest performance.

During the recent COVID-19 bear market drop, it produced several buy signals on the S&P which I followed, and made some nice gains so far.

I still think this would make a better investing strategy (buy undervalued / sell over-valued), rather than a trading strategy.

I use this robot for my long term portfolio.

Strategy Follow Line MTF Any MM AverageThe objective is only to evaluate different configurations of the indicator "Follow Line MTF Any MM Average".

The strategy does not have position management, it's very basic, this indicator should be used to see trend, range zones, evaluate the best areas to enter the market, use higher time frames to confirm a direction can be useful.

I do not recommend using only this indicator to trade, because you can lose all your money if you do not know what you are doing.

I hope you find it useful.

Successes

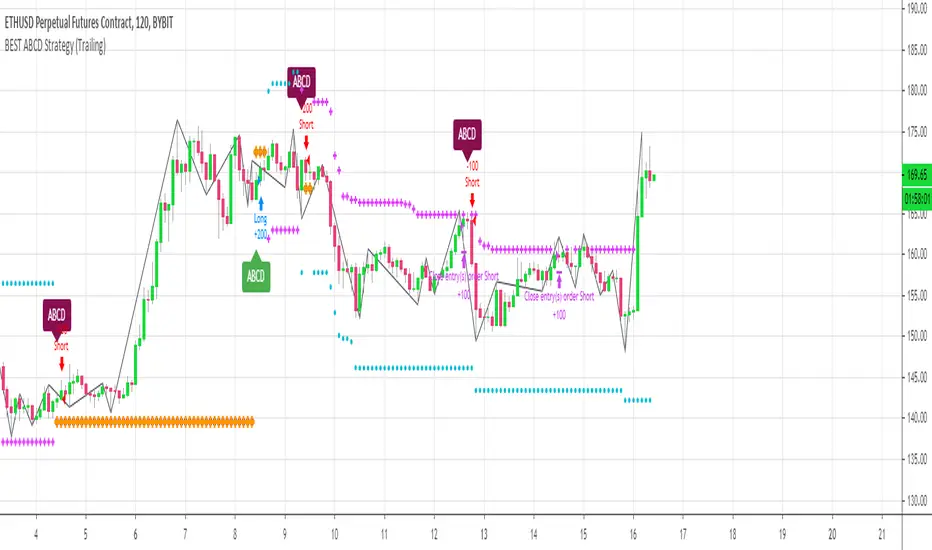

[Daveatt] BEST ABCD Pattern Strategy (Trailing SL + TP)Hello traders

This is the strategy version of my ABCD pattern. I added the Trailing Stop and Trailing Profit upon a follower request

I - Concept

I present to you, ladies and gentlemen, the first screener for harmonic patterns .

Starting with an ACBD pattern screener this time!!

I used the calculations from Ricardo Santo's script

In short, he's using fractals (regular or Bill Williams ) for the pattern calculations. A masterpiece !!!

II - Definitions

The ABCD pattern ( AB=CD ) is one of the classic chart patterns which is repeated over and over again.

The ABCD pattern shows perfect harmony between price and time.

The Williams Fractal is an indicator, developed by Bill Williams , that aims to detect reversal points (highs and lows) and marks them with arrows.

Up fractals and down fractals have specific shapes. The Williams Fractal indicator helps users determine in which direction price will develop

💎Strategy filters💎

I included some cool backtest filters:

- Trailing stop with trigger concept coming from this Trailing Stop Strategy

- Trailing profit with trigger coming from this Trailing Profit Strategy

Last words

It works for all asset classes (Forex, crypto, indices, etc...) and does not repaint

All the BEST

Dave

eha Moving Averages StrategyMoving Average based strategies are very popular ones among both long-term investors and short-term traders as they can be tailored to any time frame. One of the main moving average strategies are crossovers. The very simple type is a price crossover , which is when the price crosses above or below a moving average to signal a potential change in trend.

Another strategy is to apply two moving averages to a chart: one longer (or slow) and one shorter (or fast). When the shorter-term MA crosses above the longer-term MA, it's a buy signal, as it indicates that the trend is shifting up (also known as “ Golden Cross ”). Meanwhile, when the shorter-term MA crosses below the longer-term MA, it's a sell signal, as it indicates that the trend is shifting down (which is also known as “ Dead/Death Cross ”).

This is a study to find a suitable trading strategy for 4-6 hour time frames. As you can see the performance is currently very poor. It has just generated almost 90 trades in a very long period from January 2017 to the time of publishing the study for the first time.

Moving averages work quite well in strong trending conditions but poorly in choppy or ranging conditions. Adjusting the time frame can correct this problem temporarily, although, at some point, these issues are likely to occur regardless of the time frame chosen for the moving average(s).

I am working on this basic strategy to make its performance better and I will update the post in the future. So keep in touch by following the post.

Why have I republished my study?

It sounds like TradingView stores and indexes scripts based on the title of the post rather than the actual title of the scripts and if one chose general terms as the title of the post, the TradingView script search engine may be unable to find it. So I decided to repost the strategy with a more searchable and unique prefix of " eha ".

Please provide me with your precious feedback.

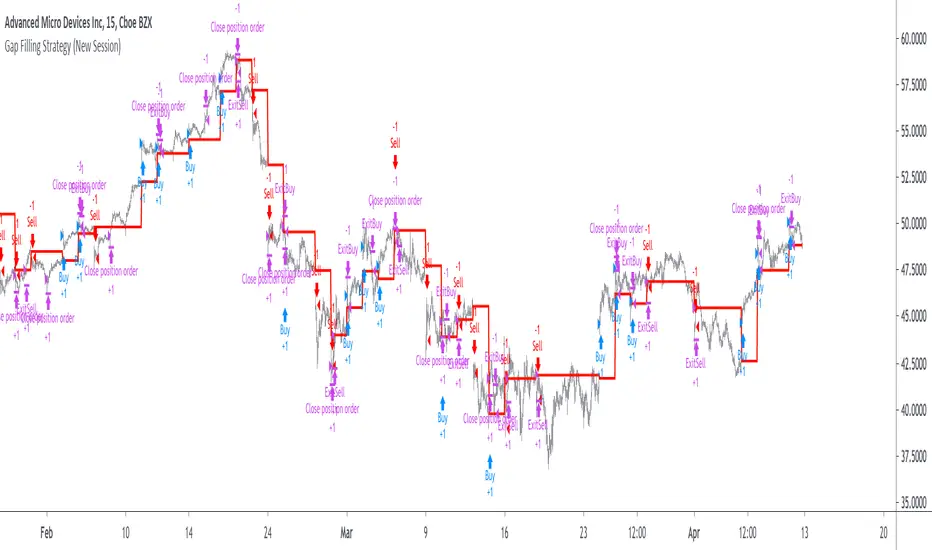

Gap Filling Strategy Gaps are market prices structures that appear frequently in the stock market, and can be detected when the opening price is different from the previous closing price, this is why gaps are also called "opening price jumps". While gaps can occur frequently, some of them are more significant than others, and can be observed when looking at a long term chart.

The following strategy is based on the exploitation of significant gaps occurring during a new session, and posses various options that can return a wide variety of results.

Type Of Gaps And Occurence

I'am not a professional when it comes to gaps, but as you know the stock market close for the day, however it is still possible to place orders, your broker will hold them until the market open back. Once the market reopen the broker execute the pending orders, and when many orders where pending the market register really high volume and the price might differ from the precedent close.

Gaps are generally broken down into four types:

Common : Gaps occurring within a certain price range, mostly occurs during ranging markets.

Break Away : Gaps breaking a support and resistance, making a new higher high/lower low.

Runaway : Gaps occurring within a trend, followed by a continuation of the trend.

Exhaustion : Gaps occurring at the end of a trend, followed by a reversal.

As said before, some gaps are more significant than others, the significance of a gap can be determined by comparing the opening price with the previous high/low price and by looking at volume. Significant up gaps will have an opening price greater than the previous high, while significant down gap will have an opening price lower than the previous low with both high volume accompanying them.

After a gap, when the price go back to the point previous to the gap we say that it has been "filled", this characteristic is what will be exploited in this strategy.

Strategy Rules & Logic

In this strategy, the significance of a gap is determined by the position of the opening price relative to the previous high/low and make sure the bar following the gap don't fill it.

When the setting invert is set to false the strategy interpret the detected gaps as being exhaustion gaps, therefore when an up gap occur a short position is opened, when a down gap occur a long position is opened. When invert is set to true gaps are considered to be runaway or break away gaps, therefore the contrary positions are opened. Positions are exited when the gap has been filled, which in the chart is show'n when the price cross the red level who act as either a take profit (invert = false) or as a stop loss (invert = true).

There are various closing conditions available that the user can select from the "close when" setting.

New Session : This option close all previous positions when the market is in a new session.

New Gap : This option close all previous position when a new gap has been detected.

Reverse Position : This option close all previous position when a contrary position to the current one is opened. This option would reduce the number of trades.

Testing On Some Stocks

The analysis will be tested in different tech stocks with a main TF of 15 minutes with no spread and commissions applied. Default settings will be used. We'll be making our first analysis using AMD, who has recently formed a full reverse HS pattern, where the neckline has been crossed by the price. (by the way i have a bad feeling about it, hey ! feeling filling ! Lame jokes!)

Profit: $ -12.22

Trades: 272

Profitability: 65.07 %

We can see negative results, with an heavily decreasing balance. Using invert would return positive results.

We will now test the strategy on NVDA, the company is one of the biggest when it comes to the Gpu market.

Profit: $ -215.54

Trades: 297

Profitability: 60.27 %

Not better, using invert would of course create better results. Like AMD the balance is heavily decreasing.

Finally we will test the strategy on Seagate technology, a company mostly known for their mechanical hard drives.

Profit: $ -4.32

Trades: 261

Profitability: 65.9 %

Here the balance does not appear so heavily decreasing and even managed to reach back the initial balance before going down again.

Summary

A strategy based on gap filling has been briefly introduced and tested with 3 tech stocks. The results show that using invert option might be better. The advantage of this strategy against ones using technical indicators is that this one does not heavily depend on user settings, which make it way more efficient, this a big advantage of patterns based strategies.

Thx to LucF for helping with the "process_orders_on_close" element, since i had to use closing price i had to remove it tho, was afraid results would differ even more from a more realistic backtest. And thx for those who continuously support me, more cool stuff is coming up.

Thx for reading and i hope you'll have learned something new today !

Strategy Follow Line Indicator The objective is only to evaluate different configurations, I do not recommend using only this indicator to trade, because you can lose all your money if you do not know what you are doing.

I hope you find it useful.

Successes

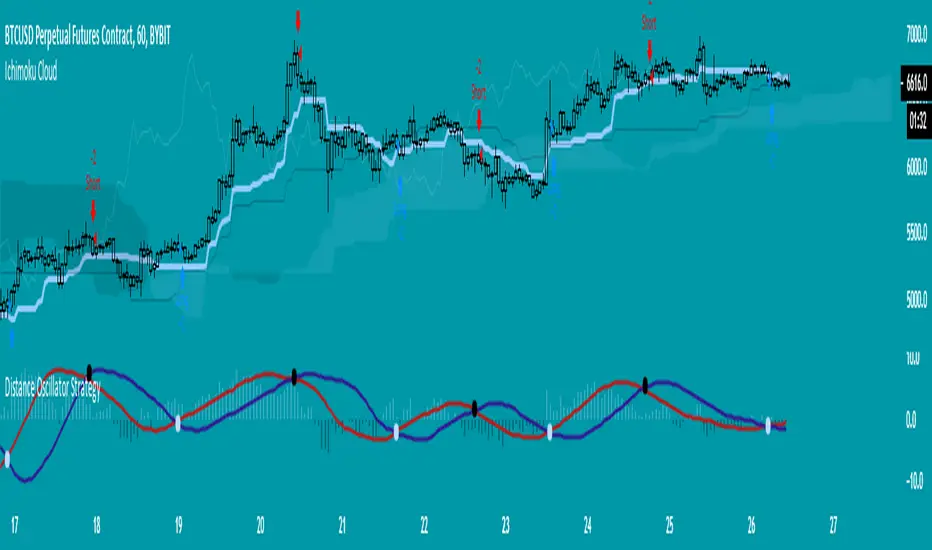

Distance Oscillator Strategy- evoI described the indicator in the link below, this is a strategy version to test settings.

Chaloke System StrategyChaloke System Strategy

This is a trend indicator

Atr and 3 moving averages are used

Short 9-day moving average,Medium 15-day moving average,Calculated with a long 24-day moving average.

Atr period : 5

Sht,Mid,Lng calculation method is different

Buying Strategy

long = crossover(Sht,Mid) and close > Sht

Selling Strategy

short = crossunder(Sht, Lng ) or close < Lng

Buy should be done when the barcolor turns green

Sell should be done when barcolor is red

When the barcolor is black, there may be change.

Laguerre RSI by KivancOzbilgic STRATEGYBacktesting.

" Laguerre RSI is based on John EHLERS' Laguerre Filter to avoid the noise of RSI .

Change alpha coefficient to increase/decrease lag and smoothness.

Buy when Laguerre RSI crosses upwards above 20.

Sell when Laguerre RSI crosses down below 80.

While indicator runs flat above 80 level, it means that an uptrend is strong.

While indicator runs flat below 20 level, it means that a downtrend is strong. "

Developer: John EHLERS

Author: KivancOzbilgic

KPL Swing StrategyThe KPLSwing indicator is a simple trend following mechanical trading system which automates the entry and exit.

The trading system is extremely simple and easy to use and removes emotions from trading.

The trading or investing logic is simple.... buy on close above 20 days high and sell on close below 20 days low.

No targets are given as profits are unknown and is whatever the market gives. Losses are limited via position sizing.

Fractal Breakout StrategyFractal

A type of pattern used in technical analysis to predict a reversal in the current trend. A fractal pattern consists of five bars and is identified when the price meets the following characteristics:

1. A shift from a downtrend to an uptrend occurs when the lowest bar is located in the middle of the pattern and two bars with successively higher lows are positioned around it.

2. A shift from an uptrend to a downtrend occurs when the highest bar is located in the middle of the pattern and two bars with successively lower highs are positioned around it.

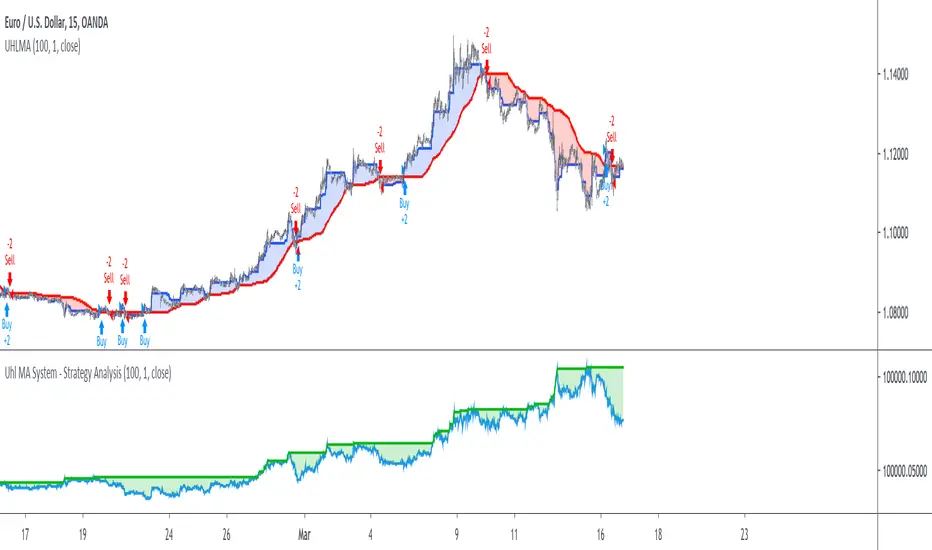

Uhl MA System - Strategy AnalysisThe Uhl MA crossover system was specifically designed to provide an adaptive MA crossover system that didn't committed the same errors of more classical MA systems. This crossover system is based on a fast and a slow moving average, with the slow moving average being the corrected moving average (CMA) originally proposed by Andreas Uhl, and the fast moving average being the corrected trend step (CTS) which is also based on the corrected moving average design.

For more information see :

In this post, the performances of this system are analyzed on various markets.

Setup And Rules

The analysis is solely based on the indicator signals, therefore no spread is applied. Constant position sizing is used. The strategy will be backtested on the 15 minute time-frame. The mult setting is discarded, the default setting used for length is 100.

Here are the rules of our strategy :

long: CTS crossover CMA

short: CTS crossunder CMA

Results And Data

EURUSD:

Net Profit: $ 0.08

Total number of trades: 99

Profitability: 35.35 %

Profit Factor: 1.834

Max Drawdown: $ 0.01

EURUSD behaved pretty well, and was most of time showing long term trends without exhibiting particularly tricky structures, the moving averages still did cross during ranging phases, since march 9 we can see a downtrend with more pronounced cyclical variations (retracements) that could potentially lead to loosing trades.

BTCUSD:

Net Profit: $ 4371.57

Total number of trades: 94

Profitability: 32.98 %

Profit Factor: 1.749

Max Drawdown: $ 1409.96

The strategy didn't started well, producing its largest drawdown after only a few trades, the strategy still managed to recover. BTCUSD exhibited a strong downtrend, the strategy profited from that to recover, signals still occurred on ranging phases, and where mostly caused by a short term volatile move, unfortunately the CMA can converge toward ranging/flat price zones where false signals might occur at higher frequency.

AMD:

Net Profit: $ 16.09

Total number of trades: 95

Profitability: 29.47 %

Profit Factor: 1.288

Max Drawdown: $ 20.11

On AMD the strategy started relatively well with a raising balance, then the balance quickly fallen, this downtrend in the balance lasted quite some time (almost 48 trades), the strategy finally recovered in Nov 2019 and the balance made a new highest high at the end of February. AMD had numerous trends during the backtesting period, yet results are poor.

AAPL:

Net Profit: $ -28.17

Total number of trades: 89

Profitability: 28.09 %

Profit Factor: 0.894

Max Drawdown: $ 63.21

AAPL show the poorest results so far, with a stationary balance around the initial capital (in short the evolution of the balance is not showing any particular trend and oscillate around the initial capital value).

AAPL had some significant retracements in its up-trend, which triggered some trades (of course), and the ranging period from Jan 24 to Feb 13 heavily damaged the strategy performance, generating 6 significant loosing trades. AAPL show the worst results so far, mostly due by ranging phases.

Conclusions

The Uhl MA crossover system strategy has been tested and based on the results don't show particularly interesting performances, and might even be outperformed by simpler MA systems that prove to be more robust against ranging markets. The total number of executed trades are on average 94, and the profitability is on average 31%. The strategy might prove more interesting if we can correct the behavior of the CMA, who sometimes converged toward ranging/flat markets.

FRAMA - Supertrend strategyFRAMA Strategy

I found this strategy on internet, in a well-known forex forum.

I have translated the two indicators mentioned in that strategy (originally in mq4) in pine script.

Thanks to Fractured and Shizaru for the FRAMA snippets, to mejialucas for Supertrend snippet, to JayRogers for trade management snippet and to Trost for backtesting snippet.

I also added some code to have FRAME with a deiiferent timeframe

Indicators set-up:

FRAMA period 24 (it was originally 25 but it's better to use an even number)

FRAMA timefarme lower then chart timeframe (e.g. daily chart and weekly FRAMA)

Supertrend indicator as it is.

Of course, it is better to adapt above setting to traded instrument.

Long/Buy rules:

1 - Enter at crossover between FRAMA and its signal

2 - Option to filter entries based on supertrend signal

3 - Exit when Supertrend change direction;

4 - Exit long when short signal occurs;

Short/Sell rules:

1 - Enter at crossunder between FRAMA and its signal

2 - Option to filter entries based on supertrend signal

3 - Exit when Supertrend change direction;

4 - Exit short when long signal occurs;

VERY IMPORTANT NOTE: this is a trend following strategy, so the target is to stay in the trade as much as possible (drawdown my be high). If your trading style is more focused on scalping and/or pullbaks, this strategy is not for you.

Credits to who developed this startegy (google it).

Thanks to all pinescripters mentined in the code for their snippets.

I have also a study with alerts.

Please use comment section for any feedback or contact me if you need support.

BEST ABCD Pattern StrategyHello traders

This is the strategy version of this script

I - Concept

I present to you, ladies and gentlemen, the first screener for harmonic patterns.

Starting with an ACBD pattern screener this time!!

I used the calculations from Ricardo Santo's script

In short, he's using fractals (regular or Bill Williams ) for the pattern calculations. A masterpiece !!!

II - Definitions

The ABCD pattern ( AB=CD ) is one of the classic chart patterns which is repeated over and over again.

The ABCD pattern shows perfect harmony between price and time.

The Williams Fractal is an indicator, developed by Bill Williams, that aims to detect reversal points (highs and lows) and marks them with arrows.

Up fractals and down fractals have specific shapes. The Williams Fractal indicator helps users determine in which direction price will develop

💎Strategy filters💎

I included some cool backtest filters:

- flexible take profit in USD value (plotted in blue)

- flexible stop loss in USD value (plotted in red)

The take profit and stop loss should work with Forex/FX pairs as well

All the BEST

Dave

BEST Engulfing + Breakout StrategyHello traders

This is a simple algorithm for a Tradingview strategy tracking a convergence of 2 unrelated indicators.

Convergence is the solution to my trading problems.

It's a puzzle with infinite possibilities and only a few working combinations.

Here's one that I like

- Engulfing pattern

- Price vs Moving average for detecting a breakout

Definition

Take out the notebooks :) and some coffee (good for focus). I'm bullish in coffee

The engulfing pattern is a two-candle reversal pattern.

The second candle completely ‘engulfs’ the real body of the first one, without regard to the length of the tail shadows.

The bullish Engulfing pattern appears in a downtrend and is a combination of one red candle followed by a larger green candle

The bearish Engulfing pattern appears in a downtrend and is a combination of one green candle followed by a larger red candle

Example: imgur.com

We're bored sir... what's the point of all this?

In summary, an engulfing is a pattern to track reversals. (the whole TradingView audience stands up now giving a standing ovation)

Adding the Price vs Moving average filters allows to track reversals with momentums (half of the audience collapsed because this is too awesome)

Ok sir... you picked up my interest

I included some cool backtest filters:

- date range filtering

- flexible take profit in USD value (plotted in blue)

- flexible stop loss in USD value (plotted in red)

All the best

Dave

Best Supertrend CCI StrategyHello traders

Someone requested the strategy version of the Supertrend CCI indicator

It's a Supertrend not based on candle close but based on a CCI ( Commodity Channel Index )

How does it work?

Bull event: CCI crossing over the 0 line

Bear event: CCI crossing below the 0 line

When the event is triggered, the script will plot the Supertrend as follow

UP Trend = High + ATR * Factor

DOWN Trend = Low - ATR * Factor

This is an alternative of the classical Supertrend based on candle close being above/beyond the previous Supertrend level.

Hope you'll enjoy it and it will improve your trading making you a better trader

Dave

Slow Heiken Ashi and Exponential Moving average Strategy 2.2Strategy using Slow Heiken Ashi by Glaz and Exponential moving averages. Looking for someone to help me turn the strategy into non-reoccuring alerts as I am having trouble doing so.

[fikira] Fibma/Fibema StrategyMy strategy regarding the Fibma/Fibema lines (also see my Fibma/Fibema study)

You can enable/disable each strategy to see what

works best in what timeframe

Thanks!

NoScoobies Bollinger BandsBollinger Bands strategy that I am trying out, however I can't get my strategy.close to work. Looking for help.

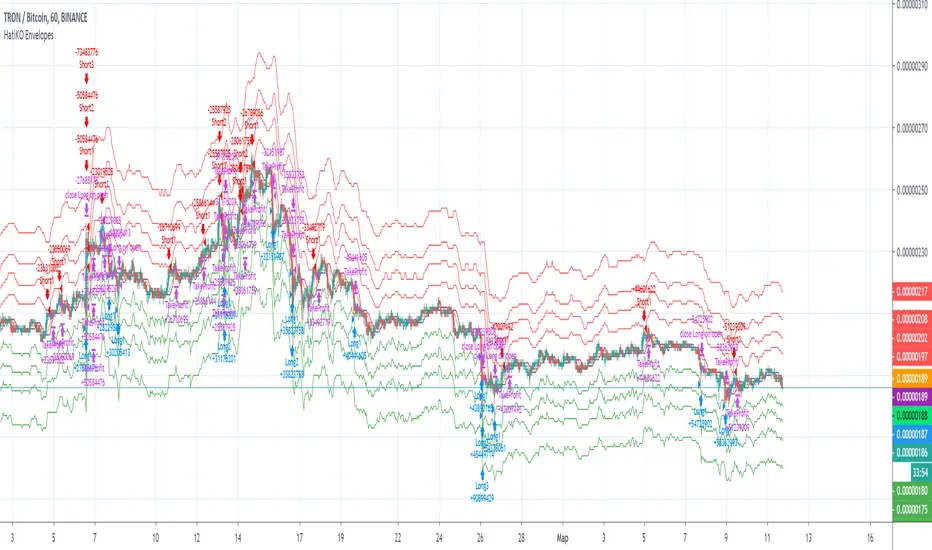

HatiKO EnvelopesPublished source code is subject to the terms of the GNU Affero General Public License v3.0

This script describes and provides backtesting functionality to internal strategy of algorithmic crypto trading software "HatiKO bot".

Suitable for backtesting any Cryptocurrency Pair on any Exchange/Platform, any Timeframe.

Core Mechanics of this strategy are based on theory of price always returning to Moving Average + Envelopes indicator (Moving_average_envelope from Wiki)

Developement of this script and trading software is inspired by:

"Essential Technical Analysis: Tools and Techniques to Spot Market Trends" by Leigh Stevens (published on 12th of April 2002)

"Moving Average Envelopes" by ChartSchool, StockCharts platform (published on 13th of April 2015 or earlier)

"Коля Колеснік" from Crypto Times channel ("Метод сетка", published on 19th of August 2018)

"3 ways to use Moving Average Envelopes" by Rich Fitton, published on Trader's Nest (published on 28st of November 2018 or earlier)

noro's "Robot WhiteBox ShiftMA" strategy v1 script, published on TradingView platform (published on 29th of August 2018)

"Moving Average Envelopes: A Popular Trading Tool" Investopedia article (published 25th of June 2019)

and KROOL1980's blogpost on Argolabs ("Гридерство или Сетка как источник прибыли на форекс", published on 27th of February 2015)

Core Features:

1) Up to 4 Envelopes in each direction (Long/Short)

2) Use any of 6 different basis MAs, optionally use different MAs for Opening and Closure

3) Use different Timeframes for MA calculation, without any repainting and lookahead bias.

4) Fixed order size, not Martingale strategy

5) Close open position earlier by using Deviation parameter

6) PineScript v4 code

Options description:

Lot - % from your initial balance to use for order size calculation

Timeframe Short - Timeframe to use for Short Opening MA calculation, can be chosen from dropdown list, default is Current Graph Timeframe

MA Type Short - Type of MA to use for Short Opening MA calculation, can be chosen from dropdown list, default is SMA

Data Short - Source of Price for Short Opening MA calculation, can be chosen from dropdown list, default is OHLC4

MA Length Short - Period used for Short Opening MA calculation, should be >=1, default is 3

MA offset Short - Offset for MA value used for Short Envelopes calculation, should be >= 0, default is 0

Timeframe Long - Timeframe to use for Long Opening MA calculation, can be chosen from dropdown list, default is Current Graph Timeframe

MA Type Long - Type of MA to use for Long Opening MA calculation, can be chosen from dropdown list, default is SMA

Data Long - Source of Price for Long Opening MA calculation, can be chosen from dropdown list, default is OHLC4

MA Length Long - Period used for Long Opening MA calculation, should be >=1, default is 3

MA offset Long - Offset for MA value used for Long Envelopes calculation, should be >= 0, default is 0

Mode close MA Short - Enable different MA for Short position Closure, default is "false". If false, Closure MA = Opening MA

Timeframe Short Close - Timeframe to use for Short Position Closure MA calculation, can be chosen from dropdown list, default is Current Graph Timeframe

MA Type Close Short - Type of MA to use for Short Position Closure MA calculation, can be chosen from dropdown list, default is SMA

Data Short Close - Source of Price for Short Closure MA calculation, can be chosen from dropdown list, default is OHLC4

MA Length Short Close - Period used for Short Opening MA calculation, should be >=1, default is 3

Short Deviation - % to move from MA value, used to close position above or beyond MA, can be negative, default is 0

MA offset Short Close - Offset for MA value used for Short Position Closure calculation, should be >= 0, default is 0

Mode close MA Long - Enable different MA for Long position Closure, default is "false". If false, Closure MA = Opening MA

Timeframe Long Close - Timeframe to use for Long Position Closure MA calculation, can be chosen from dropdown list, default is Current Graph Timeframe

MA Type Close Long - Type of MA to use for Long Position Closure MA calculation, can be chosen from dropdown list, default is SMA

Data Long Close - Source of Price for Long Closure MA calculation, can be chosen from dropdown list, default is OHLC4

MA Length Long Close - Period used for Long Opening MA calculation, should be >=1, default is 3

Long Deviation - % to move from MA value, used to close position above or beyond MA, can be negative, default is 0

MA offset Long Close - Offset for MA value used for Long Position Closure calculation, should be >= 0, default is 0

Short Shift 1..4 - % from MA value to put Envelopes at, for Shorts numbers should be positive, the higher is number, the higher should be Shift position, example: "Shift 1 = 1, shift 2 = 2, etc."

Long Shift 1..4 - % from MA value to put Envelopes at, for Longs numbers should be negative, the lower is number, the lower should be Shift position, example: "Shift 1 = -1, shift 2 = -2, etc."

From Year 20XX - Backtesting Starting Year number, only 20xx supported as script is cryptocurrency-oriented.

To Year 20XX - Backtesting Final Year number, only 20xx supported as script is cryptocurrency-oriented.

From Month - Years starting Month, optional tweaking, changing not recommended

To Month - Years ending Month, optional tweaking, changing not recommended

From day - Months starting day, optional tweaking, changing not recommended

To day - Months ending day, optional tweaking, changing not recommended

Graph notes:

Green lines - Long Envelopes.

Red lines - Short Envelopes.

Orange line - MA for closing of Short positions.

Lime line - MA for closing of Long positions.

**************************************************************************************************************************************************************************************************************

Опубликованный исходный код регулируется Условиями Стандартной Общественной Лицензии GNU Affero v3.0

Этот скрипт описывает и предоставляет функции бектеста для внутренней стратегии алгоритмического программного обеспечения "HatiKO bot".

Подходит для тестирования любой криптовалютной пары на любой бирже/платформе, на любом таймфрейме.

Кор-механика этой стратегии основана на теории всегда возвращающейся к значению МА цены с использованием индикатора Envelopes (Moving_average_envelope from Wiki)

Разработка этого скрипта и программного обеспечения для торговли вдохновлена следующими источниками:

Книга "Essential Technical Analysis: Tools and Techniques to Spot Market Trends" Ли Стивенса (опубликовано 12 апреля 2002 года)

«Moving Average Envelopes» от ChartSchool, платформа StockCharts (опубликовано 13 апреля 2015 года или раньше)

«Коля Колеснік» с канала Crypto Times («Метод сетка», опубликовано 19 августа 2018 года)

«3 ways to use Moving Average Envelopes» Рича Фиттона, опубликованные в «Trader's Nest» (опубликовано 28 ноября 2018 года или раньше)

Скрипт стратегии noro "Robot WhiteBox ShiftMA" v1, опубликованный на платформе TradingView(опубликовано 29 августа 2018 года)

«Moving Average Envelopes: A Popular Trading Tool», статья Investopedia (опубликовано 25 июня 2019 года)

Блог KROOL1980 из Argolabs («Гридерство или Сетка как источник прибыли на форекс», опубликовано 27 февраля 2015 года)

Основные особенности:

1) До 4-х Ордеров в каждом из направлении (Лонг / Шорт)

2) Выбор из 6-ти разных базовых МА, опционально используйте разные МА для открытия и закрытия.

3) Используйте разные таймфреймы для расчета MA, без перерисовки и "эффекта стеклянного шара".

4) Фиксированный размер ордера, а не стратегия Мартингейла

5) Возможность закрытия открытой позиции заблаговременно, используя параметр Deviation

6) Код реализован на PineScript v4

Описание параметров:

Lot - % от вашего первоначального баланса, используется при расчете размера Ордера

Timeframe Short - таймфрейм, используемый для расчета МА Открытия Шорт позиций, может быть выбран из списка, по умолчанию - таймфрейм текущего графика

MA Type Short - тип MA, используемый для расчета МА Открытия Шорт позиций, может быть выбран из списка, по умолчанию SMA

Data Short - источник цены для расчета МА Открытия Шорт позиций, может быть выбран из списка, по умолчанию OHLC4

MA Length Short - период, используемый для расчета МА Открытия Шорт позиций, должен быть >= 1, по умолчанию 3

MA Offset Short - смещение значения MA, используемого для расчета Шорт Ордеров, должно быть >= 0, по умолчанию 0

Timeframe Long - таймфрейм, используемый для расчета МА Открытия Лонг позиций, может быть выбран из списка, по умолчанию - таймфрейм текущего графика

MA Type Long - тип MA, используемый для расчета МА Открытия Лонг позиций, может быть выбран из списка, по умолчанию SMA

Data Long - источник цены для расчета МА Открытия Лонг позиций, может быть выбран из списка, по умолчанию OHLC4

MA Length Long - период, используемый для расчета МА Открытия Лонг позиций, должен быть >= 1, по умолчанию 3

MA Offset Long - смещение значения MA, используемого для расчета Лонг Ордеров, должно быть >= 0, по умолчанию 0

Mode close MA Short - Включает отдельное MA для закрытия Шорт позиции, по умолчанию «false». Если false, MA Закрытия = MA Открытия

Timeframe Short Close - таймфрейм, используемый для расчета МА Закрытия Шорт позиций, может быть выбран из списка, по умолчанию - таймфрейм текущего графика

MA Type Close Short - тип MA, используемый при расчете МА Закрытия Шорт позиции. Mожно выбрать из списка, по умолчанию SMA

Data Short Close - источник цены для расчета МА Закрытия Шорт позиций, может быть выбран из списка, по умолчанию OHLC4

MA Length Short Close - период, используемый для расчета МА Закрытия Шорт позиции, должен быть >= 1, по умолчанию 3

Short Deviation - % отклонения от значения MA, используется для закрытия позиции выше или ниже рассчитанного значения MA, может быть отрицательным, по умолчанию 0

MA Offset Short Close - смещение значения MA, используемого для расчета закрытия Шорт позиции, должно быть >= 0, по умолчанию 0

Mode close MA Long - Включает разные MA для закрытия Лонг позиции, по умолчанию «false». Если false, MA Закрытия = MA Открытия

Timeframe Long Close - таймфрейм, используемый для расчета МА Закрытия Лонг позиций, может быть выбран из списка, по умолчанию - таймфрейм текущего графика

MA Type Close Long - тип MA, используемый при расчете МА Закрытия Лонг позиции. Mожно выбрать из списка, по умолчанию SMA

Data Long Close - источник цены для расчета МА Закрытия Лонг позиций, может быть выбран из списка, по умолчанию OHLC4

MA Length Long Close - период, используемый для расчета МА Закрытия Лонг позиции, должен быть >= 1, по умолчанию 3

Long Deviation -% для перехода от значения MA, используется для закрытия позиции выше или ниже рассчитанного значения MA, может быть отрицательным, по умолчанию 0

MA Offset Long Close - смещение значения MA, используемого для расчета закрытия Лонг позиции, должно быть >= 0, по умолчанию 0

Short Shift 1..4 - % от значения MA для размещения Ордеров, для Шорт Ордеров должен быть положительным, чем выше номер, тем выше должна располагаться позиция Shift, например: «Shift 1 = 1, Shift 2 = 2 и т.д. "

Long Shift 1..4 - % от значения MA для размещения Ордеров, для Лонг Ордеров должно быть отрицательным, чем ниже число, тем ниже должна располагаться позиция Shift, например: «Shift 1 = -1, Shift 2 = -2, и т.д."

From Year 20XX - Год начала тестирования, из-за ориентированности на криптовалюты поддерживаются только значения формата 20хх.

To Year 20XX - Год окончания тестирования, из-за ориентированности на криптовалюты поддерживаются только значения формата 20хх.

From Month - Начальный месяц, опционально, менять не рекомендуется

To Month - Конечный месяц, опционально, менять не рекомендуется

From day - Начальный день месяца, опционально, менять не рекомендуется

To day - Конечный день месяца, опционально, менять не рекомендуется

Пояснения к графику:

Зеленые линии - Лонг Ордера.

Красные линии - Шорт Ордера.

Оранжевая линия - MA Закрытия Шорт позиций.

Лаймовая линия - MA Закрытия Лонг позиций.

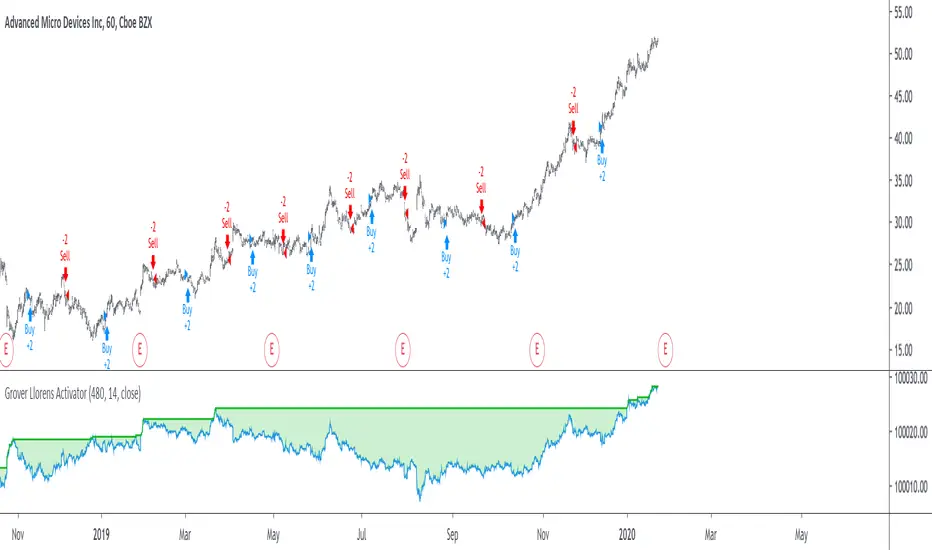

Grover Llorens Activator Strategy AnalysisThe Grover Llorens Activator is a trailing stop indicator deeply inspired by the parabolic SAR indicator, and aim to provide early exit points and reversal detection. The indicator was posted not so long ago, you can find it here :

Today a strategy using the indicator is proposed, and its profitability is analyzed on 3 different markets with the main time frame being 1 hour, remember that lower time frames involve lower absolute price changes, therefore we are way more affected by the spread, and we can require a larger position sizing depending on our investment target, trading higher time-frames is always a good practice and this is why 1 hour is selected. Based on the result we might make various conclusions regarding the indicator accuracy and might have ideas on future improvements of the indicator.

I'am not great when it comes to strategy design, i still hope to share correct and useful information in this post, let me know your thoughts on the post format and if i should make more of these.

Setup And Rules

The analysis is solely based on the indicator signals, money management isn't taken into account, this allow us to have an idea on the indicator robustness and resilience, particularly on extremely volatile markets and ones exhibiting a chaotic structure, altho it is normally good practice to close any position before a market closure in order to avoid any potential major gaps.

The settings used are 480 for length and 14 for mult, this create relatively mid term signals that are suited for a trend indicator such as the Grover Llorens Activator, unfortunately we can't infer the indicator optimal settings, thats how it is with any technical indicator anyway.

Here are the rules of our strategy :

long : closing price cross over the indicator

short : closing price cross under the indicator

We use constant position sizing, once a signal is triggered all the previous positions are closed.

Description Of The Statistics Used

Various statistics are presented in this post, here is a brief description of the main ones :

Percent Profitability (higher = better): Percentage of winning trades, that is : winning trades/total number of trades × 100

Maximum Drawdown (lower = better) : The highest difference between a peak and a valley in the balance, that is : peak - valley , in percentage : (peak - valley)/peak × 100

Profit Factor (higher = better) : Gross profit divided by gross loss, values under 1 represent gross losses superior to the gross profits

Remember that more volatility = more risk, since higher absolute price changes can logically cause larger losses.

EURUSD

The first market analyzed is the Forex market with the EURUSD major pair with a position sizing of 1000 units (1 micro lot). Since October EURUSD is not showing any particular strong trend but posses a discrete rising motion, fortunately cycles can be observed.

The equity was rising until two trades appeared causing a decline in the equity. Before October a bearish market could be observed.

We can see that the equity is rising, the trend still posses various retracements that affect our indicator, however we can see that the indicator totally nail the end of the trend, thats the power of converging toward the price.

In short :

$ 86.63 net profit

340 closed trades

37.65 % profitable (thats a lot of loosing trades)

1.19 profit factor

$ 76.67 max drawdown

Applying a spread would create negative results (in general the average spread is used), not a great start...

BTCUSD

The cryptocurrency market is relatively more volatile than others, which also mean potentially higher returns, we test the indicator using certainly the most traded cryptocurrency, BTCUSD. We will use a position sizing of 1 unit.

In the case of BTCUSD the strategy balance is relatively stationary around the initial capital, with of course high dispersion.

from september to december the market is bearish with various ranging periods, no apparent cycles can be observed, except maybe in the ranging period of october, this ranging period is followed by a non linear trend (relatively parabolic) that the indicator failed to capture in its integrity (this is a recurrent problem and it is starting to piss me off xD).

In short :

$ 2010.64 net profit (aka how i bet the crypto market)

395 closed trades

38.23 % profitable

1.036 profit factor

$ 5738.01 max drawdown (aka how i lost to the crypto market)

AMD

AMD stand for Advanced Micro Devices and is a company focused on the development of computer technology, i love the microprocessor market and i really like AMD who start this year in a pretty great way with a net bullish trend.

The performance of the indicator on AMD is decent (at last !) with the equity producing many new higher highs. The indicator performance still drop in the middle end of 2019 with a large equity drawdown of 17$ caused by the gap of august 8. Unfortunately AMD, like lot of well behaving stocks can only tells us that the indicator has good performances on heavily trending markets with no excess of noise or chaotic structures.

In short :

$ 17.86 net profit (Enough for a consistent lunch)

295 closed trades

36.27 % profitable

1.414 profit factor

$ 10.37 max drawdown.

Conclusion

A strategy using the recently proposed Grover Llorens activator has been presented. We can easily conclude that the indicator can't possibly generate long term returns under chaotic and volatile markets, and could even produce unnecessary trades in trending markets without much parasitic fluctuations such as noise and retracements (think about a simple linear trend) since the indicator converge toward the price and would therefore automatically cross over/under the trend, thus guaranteeing a false signal.

However we have seen its ability to provide accurate early reversal detection shine from time to time, thus over performing lagging indicators in this aspect, however the duration of price fluctuations isn't fixed at a certain period, the rate of convergence should be way faster during volatile fluctuations, of moderate speed during more cyclic fluctuations, and really slow with apparent long term trends, this could be achieved by making the indicator adaptive, but it won't really make it necessarily perform better.

That said i still believe that converging trend indicators are really interesting and aim to capture the non lasting behavior of price fluctuations, they shouldn't receive so much hate (think about the poor p-sar).

Thanks for reading !