Multi Indicators v1 - 20 50 200 EMA/SMA, Bollinger Bands, VWAPMulti Indicators v1

20 50 200 EMA/SMA, Bollinger Bands, VWAP

These can be turned on and off

I'll be adding to this multi indicator in future updates

Buscar en scripts para "黄金近20年走势"

Multiple Ema 20/50/100Multiple Ema 20/50/100 and you can add more EMA Plot easily by changing the codes.

EMA Cross 20/50/200Added a 20 EMA cross to the avaiable 50/200 EMA Cross script in the public library

EMA 20/50/100/200Script that publishes the EMA for 20, 50, 100, and 200.

Follow me on Twitter at @PotatoMcGruff

EMA 20/50/100/200Plots exponential moving average on four timeframes at once for rapid indication of momentum shift as well as slower-moving confirmations.

Displays EMA 20, 50, 100, and 200... default colors are hotter for faster timeframes, cooler for slower ones

B3 20/50 MeanSimple MA's 20 and 50 are averaged to produce a mean MA line. I like the smoothness of it, and it can help you stay in a trade in the slow moving trends. Also if you start to see a large cloud in your favor, it could be a great time take the profits.

ShareGenius Swing Trading (SST) 20 days low

20 days high

target to set

special thanks to Shri Mahesh Chander Kaushik and Shri Krishan

Bullish & Bearish Reversal Pattern with Sequential Bars20 Bollinger Bands and custom Stochasti_MTM Setup

Both long and short reversal signals.

EMA/SMA + Multi-Timeframe Dashboard (Vertical)20/50 ema and 200 sma

The EMA SMA Trading Indicator combines the power of Exponential Moving Averages (EMA) and Simple Moving Averages (SMA) to help traders identify trends, reversals, and key entry/exit points.

Features:

Dual Moving Averages: Tracks both EMA and SMA to provide a balanced view of short-term and long-term market trends.

Customizable Periods: Allows users to set unique periods for EMA and SMA to suit their trading style and timeframe (e.g., day trading, swing trading, or investing).

Cross Alerts: Highlights EMA and SMA crossover points, which often indicate potential buy or sell signals.

Color-Coded Lines: Visual differentiation between EMA (dynamic and responsive) and SMA (smooth and lagging) for better readability.

Multi-Timeframe Compatibility: Suitable for scalping, intraday trading, and long-term analysis.

Usage:

Trend Confirmation: When the EMA is above the SMA, it signals a bullish trend; when it is below the SMA, it signals a bearish trend.

Crossover Strategy: Use crossovers as potential buy (EMA crosses above SMA) or sell (EMA crosses below SMA) signals.

Dynamic Support/Resistance: EMA can act as short-term support/resistance, while SMA represents long-term levels.

This indicator is perfect for traders who want to combine EMA's speed with SMA's stability for improved decision-making in volatile markets. Customizable alerts and visual cues make it user-friendly for beginners and experienced traders.

Make informed decisions and take your trading to the next level with the EMA SMA Trading Indicator!

6 Bollinger Bands (1.5 thru 4)20 period SMA Bollinger Bands with the following standard deviations: 1.5 2 2.5 3 3.5 4

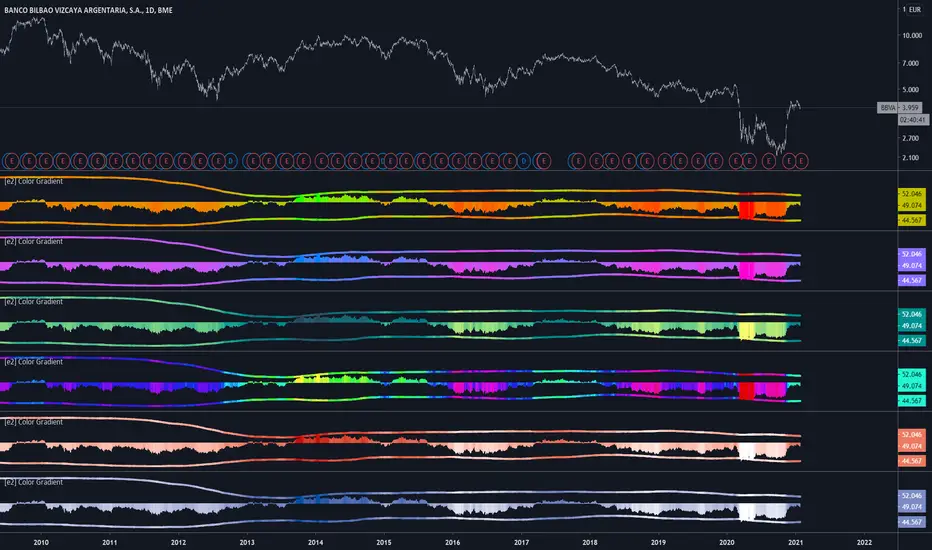

[e2] Color Gradient Function20 step red/green gradient function

The color gradient function allow colorize any source in 5% steps.

Define the source, minimum and maximum value (constant or , for example, bb (or any other channel)).

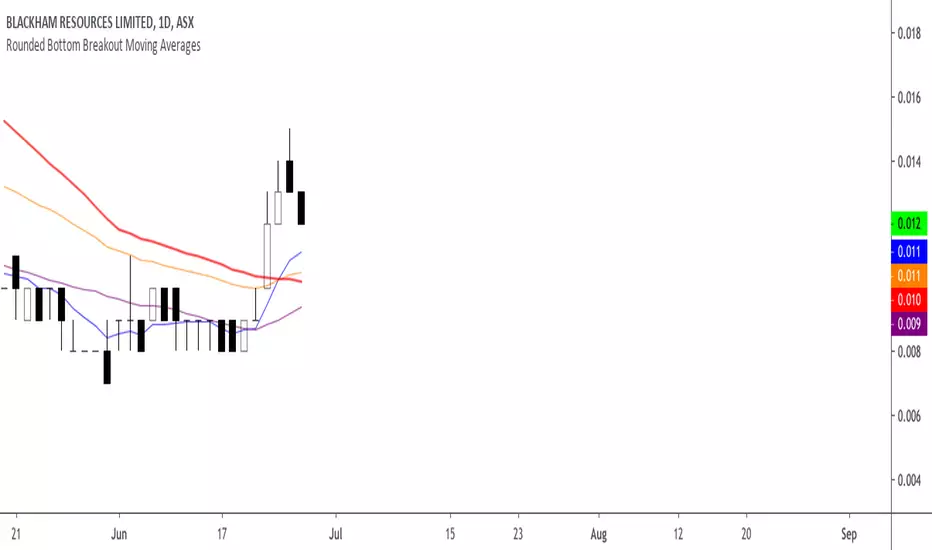

Rounded Bottom Breakout Strategy Moving Averages20-day SMA , 34-day EMA , 50-day SMA and 200-day SMA moving average indicator based on Rick Saddler's Rounded Bottom Reversal Breakout Strategy

Noro's Fishnet Strategy20 lines are JMA. Green color - a uptrend. Red color - a downtrend.

Color filter

If this checkbox is chosen, then long positions will be open only if a red candle. Short positions will open if a green candle.

If this checkbox is not chosen, then positions will open at change of a trend. Color of a candle will not matter.