Spread ChartThis script lets you chart a spread of a maximum of 3 tickers (one of them being the ticker in the main chart).

Y axis is the currency amount of the spread, that is calculated by this formula:

Y = PnL = quantity * price * handleValue

Y is calculated for each ticker specified, and the sum of Ys obtained is plotted.

this way it is possible to view the PnL of the spread directly.

It is necessary to specify the handle value (point value) in the script inputs (not for the main chart ticker).

A table summarizes the spread configuration, containing all inputs.

Buscar en scripts para "文华财经tick价格"

PlurexSignalLibrary "PlurexSignal"

Provides functions that wrap the built in TradingView strategy functions so you can seemlessly integrate with Plurex Signal automation.

NOTE: Be sure to set your strategy close_entries_rule="ANY" and pyramiding=20 or some other amount appropriate to your strategy in order to have multiple entries.

plurexMarket()

Build a Plurex market string from a base and quote asset symbol.

Returns: A market string that can be used in Plurex Signal messages.

tickerToPlurexMarket()

Builds Plurex market string from the syminfo

Returns: A market string that can be used in Plurex Signal messages.

simpleMessage(secret, action, marketOverride)

Builds Plurex Signal Message json to be sent to a Signal webhook

Parameters:

secret : The secret for your Signal on plurex

action : The action of the message. One of .

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

Returns: A json string message that can be used in alerts to send messages to Plurex.

long(secret, marketOverride, qty)

Open a new long entry. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

qty : Corresponds to strategy.entry qty

short(secret, marketOverride, qty)

Open a new short entry. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

qty : Corresponds to strategy.entry qty

closeAll(secret, marketOverride)

Close all positions. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

closeLongs(secret, marketOverride)

Close all longs. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

closeShorts(secret, marketOverride)

Close all shorts. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

closeLastLong(secret, marketOverride)

Close last long entry. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

closeFirstLong(secret, marketOverride)

Close first long entry. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

closeLastShort(secret, marketOverride)

Close last short entry. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

closeFirstShort(secret, marketOverride)

Close first short entry. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

RaenonX - Manual PnL TrackerChange the "ticker" field in the settings to the ticker to track (for example, "SQQQ") before use.

Manually track the PnL of a single ticker.

The current PnL will be shown at the right bottom of the chart.

switches [experimental / tools]This scripts shows a tool which enables switching between settings without opening the settings

In this case you can switch between a RSI of 3 different tickers, 3 different higher timeframes, and 4 different lengths.

How does it work?

The position of a 'time line' is compared with the position of a box.

Changing the position of the line changes the settings.

The settings need to be set upfront though,

if you want to switch between length 7, 10, 14, 21 they need to be set first.

Example:

One wants to switch between RSI of SOLUSDT, ADAUSDT and FILUSDT

First set your tickers

-> Settings -> Set 1 -> Ticker

Then tap/click and move the line

And there you go!

The same with Timeframe and Length

Important:

It is not possible to automatically set the boxes/line at current time,

so these (settings -> date at Box, Line) need to be set in the beginning

Cheers!

TASC 2022.6 Ehlers' Loops - SectorsInspired by the latest TASC article, the crocker graph is expanded to show 5 tickers.

for commodity also draws a side box with current tickers candles so it can be used as standalone.

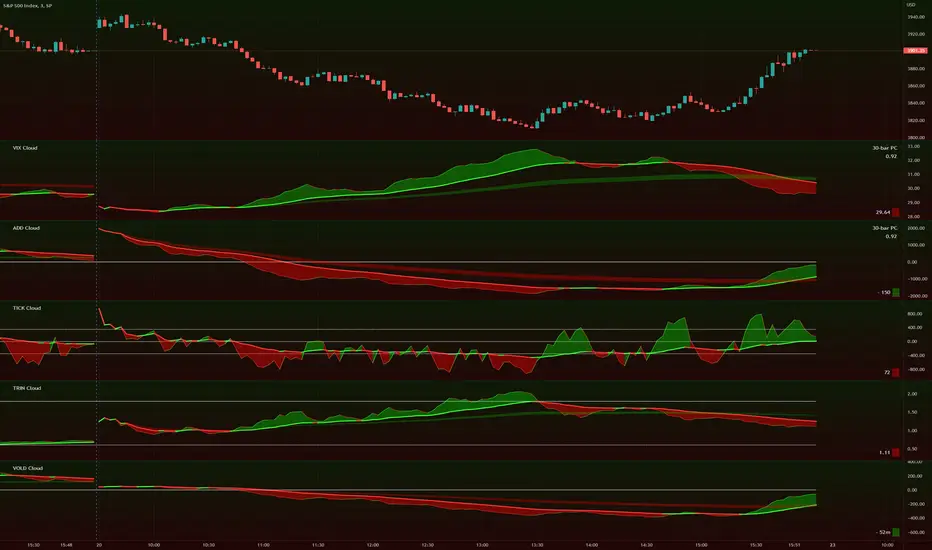

TIG's Market Internals Clouds Indicator v2.0=================================

== GENERAL INTRODUCTION

=================================

If you find market internals inform your intraday trading decisions (SPX, ES futures, SPY or more generally) this may be helpful.

Currently available internals are:

- ADD

- TICK

- TRIN

- VIX

- VOLD

Also, you can display your favorite alternative market internal (or BTC, if you want?!) by entering the relevant ticker in the 'Custom' field

=================================

== NOTES

=================================

The default EMA lengths seem to work reasonably well for 1, 2, 3-minute timeframes (except for TICK - you may wish to apply a bit more smoothing to TICK to reduce the noise)

Of course; you can add this indicator to your chart multiple times, and display a different internal each time.

The default Text Color is set as a mid-grey, which is readable in both TV color schemes. I prefer dark mode, and so I change the text color to white. You can't see the scheme setting from within a script, unfortunately, so this can't be automated.

=================================

== EXPERIMENTAL FEATURE

=================================

As a free bonus, the indicator can display the 30-bar (default) Pearson Correlation Coefficient between the internal, and price action (based on the super-fast EMA, to give a bit of smoothing). This may give a clue as to whether or not the market is aligned with what the internal is doing, or if the market (today) is not correlated with the particular internal.

Very roughly speaking:

- 0.50 means that 50% of the price action can be explained by reference to the internal. This is about the same level of correlation between VIX and Actual Move

- 0.80 suggests pretty strong correlation

I don't know why (yet) but sometimes this works, and sometimes it doesn't display a sensible figure.

=================================

== QUESTIONS AND FEEDBACK

=================================

If you have any general questions about market internals, Google is your friend.

If you have any specific queries, bug reports, feature requests or general feedback about this indicator please leave a comment below, and I'll get back to you ASAP!

Donchian Screener█ OVERVIEW

This is a screener script for the Donchian Channel indicator . It's an excellent indicator for trend following, a trading strategy which tries to take advantage of long, medium or short-term moves that seem to play out in various markets.

█ DESCRIPTION

The screener works by scanning through up to 10 symbols and list down symbols that are currently breaking through the upper or lower band as definied by the Donchian Channels, at which point the market signals the start of a bullish or bearish trend.

█ HOW TO USE

After adding the indicator, open the script settings and type the symbol name and length to be used on the Donchian Channels for each stock.

█ PARAMETERS

- Use High/Low Price Breakouts: check this box if you want to use price high/low instead of price close to identify breakouts

- Panel Position: choose whether you want to position the panel on the top, middle or bottom right side of the graph (default is top)

- Default Timeframe: what timeframe to use on the screener (default is daily)

- Ticker: the ticker name you want to monitor

- Length: length parameter used on Donchian Channel indicator

█ FEATURES

The screener can scan up to 10 symbols each time.

█ LIMITATIONS

The screener will scan the symbols breaking out bands on the current bar, and as such, there maybe some delays depending on the stock/ etf /crypto you choose. Some exchanges require an additional subscription to get realtime data.

Forex Dogs Moving Averages with Distance TableThis is an indicator based on the book【Forex】ForexDog’s Vacuum Zone Trading 2021: Trading Strategy to “not lose” based on Experience and Logic written by Forex Dog (yes, this is his author name on Amazon; he is a trader popular mostly in Japan). It consists of simple moving averages which should somewhat correspond to the higher timeframes moving averages. The original was traded on a 15m chart and the periods are as follows: 5, 20, 40, 50, 80, 100, 200, 400, 640, 1600, 1920, 3200.

Then, there is a big table with a distances overview. This should give you an idea of how far each average is in ticks. The minus in front of the ticks_total signifies direction.

I expect some feedback on this because I don't think the user convenience is very with tables being so bright. My goal is to create a system that limits the number of "noodles" on the chart but still carries the information via the tables on the side.

Moving Average Length is not adjustable by design. The book says to use these quite explicitly, although the logic would work just fine with some other levels, it would not be the original strategy.

Good luck!

Synthetic Price Action GeneratorNOTICE:

First thing you need to know, it "DOES NOT" reflect the price of the ticker you will load it on. THIS IS NOT AN INDICATOR FOR TRADING! It's a developer tool solely generating random values that look exactly like the fractals we observe every single day. This script's generated candles are as fake as the never ending garbage news cycles we are often force fed and expected to believe by using carefully scripted narratives peddled as hypnotic truth to psychologically and emotionally influence you to the point of control by coercion and subjugation. I wanted to make the script's synthetic nature very clear using that analogy, it's dynamically artificial. Do not accidentally become disillusioned by this scripts values, make trading decisions from it, and lastly don't become victim to predatory media magic ministry parrots with pretty, handsome smiles, compelling you to board their ferris wheel of fear. Now, on to the good stuff...

BACKSTORY:

Occasionally I find myself in situations where I have to build analyzers in Pine to actually build novel quantitative analytic indicators and tools worthy of future use. These analyzers certainly don't exist on this platform, but usually are required to engineer and tweak algorithms of the highest quality with the finest computational caliber. I have numerous other synthesizers to publish besides this one.

For many reasons, I needed a synthetic environment to utilize the analyzers I built in Pine, to even pursue building some exotic indicators and algorithms. Pine doesn't allow sourcing of tuples. Not to mention, I required numerous Pine advancements to make long held dreams into tangible realities. Many Pine upgrades have arrived and MANY, MANY more are in need of implementation for all. Now that I have this, intending to use it in the future often when in need, you can now use it too. I do anticipate some skilled Pine poets will employ this intended handy utility to design and/or improved indicators for trading.

ORIGIN:

This was inspired by the brilliance from the world renowned ALGOmist John F. Ehlers, but it's taken on a completely alien form from its original DNA. Browsing on the internet for something else, I came across an article with a small code snippet, and I remembered an old wish of mine. I have long known that by flipping back and forth on specific tickers and timeframes in my Watchlist is not the most efficient way to evaluate indicators in multiple theatres of price action. I realized, I always wanted to possess and use this sort of tool, so... I put it into Pine form, but now have decided to inject it with Pine Script steroids. The outcome is highly mutable candle formations in a reusable mutagenic package, observable above and masquerading as genuine looking price candles.

OVERVIEW:

I guess you could call it a price action synthesizer, but I entitled it "Synthetic Price Action Generator" for those who may be searching for such a thing. You may find this more useful on the All or 5Y charts initially to witness indication from beginning (barstate.isfirst === barindex==0) to end (last_bar_index), but you may also use keyboard shortcuts + + to view the earliest plottable bars on any timeframe. I often use that keyboard shortcut to qualify an indicator through the entirety of it's runtime.

A lot can go wrong unexpectedly with indicator initialization, and you will never know it if you don't inspect it. Many recursively endowed Infinite Impulse Response (IIR) Filters can initialize with unintended results that minutely ring in slightly erroneous fashion for the entire runtime, beginning to end, causing deviations from "what should of been..." values with false signals. Looking closely at spg(), you will recognize that 3 EMAs are employed to manage and maintain randomness of CLOSE, HIGH, and LOW. In fact, any indicator's barindex==0 initialization can be inspected with the keyboard shortcuts above. If you see anything obviously strange in an authors indicator, please contact the developer if possible and respectfully notify them.

PURPOSE:

The primary intended application of this script, is to offer developers from advanced to even novice skill levels assistance with building next generation indicators. Mostly, it's purpose is for testing and troubleshooting indicators AND evaluating how they perform in a "manageable" randomized environment. Some times indicators flake out on rare but problematic price fluctuations, and this may help you with finding your issues/errata sooner than later. While the candles upon initial loading look pristine, by tweaking it to the minval/maxval parameters limits OR beyond with a few code modifications, you can generate unusual volatility, for instance... huge wicks. Limits of minval= and maxval= of are by default set to a comfort zone of operation. Massive wicks or candle bodies will undoubtedly affect your indication and often render them useless on tickers that exhibit that behavior, like WGMCF intraday currently.

Copy/paste boundaries are provided for relevant insertion into another script. Paste placement should happen at the very top of a script. Note that by overwriting the close, open, high, etc... values, your compiler will give you generous warnings of "variable shadowing" in abundance, but this is an expected part of applying it to your novel script, no worries. plotcandle() can be copied over too and enabled/disabled in Settings->Style. Always remember to fully remove this scripts' code and those assignments properly before actual trading use of your script occurs, AND specifically when publishing. The entirety of this provided code should never, never exist in a published indicator.

OTHER INTENTIONS:

Even though these are 100% synthetic generated price points, you will notice ALL of the fractal pseudo-patterns that commonly exist in the markets, are naturally occurring with this generator too. You can also swiftly immerse yourself in pattern recognition exercises with increased efficiency in real time by clicking any SPAG Setting in focus and then using the up/down arrow keys. I hope I explained potential uses adequately...

On a personal note, the existence of fractal symmetry often makes me wonder, do we truly live in a totality chaotic universe or is it ordered mathematically for some outcomes to a certain extent. I think both. My observations, it's a pre-deterministic reality completely influenced by infinitesimal amounts of sentient free will with unimaginable existing and emerging quantities. Some how an unknown mysterious mechanism governing the totality of universal physics and mathematics counts this 100.0% flawlessly and perpetually. Anyways, you can't change the past that long existed before your birth or even yesterday, but you can choose to dream, create, and forge the future into your desires and hopes. As always, shite always happens when your not looking for it. What you choose to do after stepping in it unintentionally... is totally up to you. :) Maybe this tool and tips provided will aid you in not stepping in an algo cachucha up to your ankles somehow.

SCRIPTING LESSONS PORTRAYED IN THIS SCRIPT:

Pine etiquette and code cleanliness

Overwrite capabilities of built-in Pine variables for testing indicators

Various techniques to organize Settings panel while providing ease of adjustment utility

Use of tooltip= to provide users adequate valuable information. Most people want to trade with indicators, not blindly make adjustments to them without any knowledge of their intended operation/effects

When available time provides itself, I will consider your inquiries, thoughts, and concepts presented below in the comments section, should you have any questions or comments regarding this indicator. When my indicators achieve more prevalent use by TV members , I may implement more ideas when they present themselves as worthy additions. Have a profitable future everyone!

Kzx PT mod v1.0 by RX-RAYKzx Position tracker mod v1.0 by RX-RAY

Original script by K-zax

The modification was made for the USDRUB ticker (the number of digits in the values of price, interest, lot volume and profit loss for other tickers may affect the positioning of the inscription, but it is fully operative and it may be used with other tickers )

Typical label view:

74.30 - ENTRY PRICE

+/-0.16% - % of price chang ( range +/-9.99)

20 - position value (range 0-99)

(S) - position type (L) - long (S) - short

+/-0017 - actual profit/loss in cash (range +/- 9999)

(All range value for correct label position,

but script mod can be used out off range)

List of additions and changes:

1. Added display of position value, short / long position type and profit / loss value (including broker commission).

2. Positive interest change now corresponds to profit, negative change in interest to loss in accordance with the type of position ( short/long )

3. The position of the inscription and the digits of the values are fixed and now insignificantly depends on the change in the time interval and the change in the scale of the graph and the change in data values and their signs.

4. Added changing the color of the inscription in the situation positive price change, but profit < commission fee. (critical gain).

Thange VaultLibrary "ThangeVault"

Thange Vault is a collection of utility functions required by the Thange Woodwind Playbook.

debug(msg) Print debug information

Parameters:

msg : message to be logged on console

Returns: nothing

tickFormat() Create a string template to restrict stop-loss, take-profit level precision to ticks.

Returns: A string format template

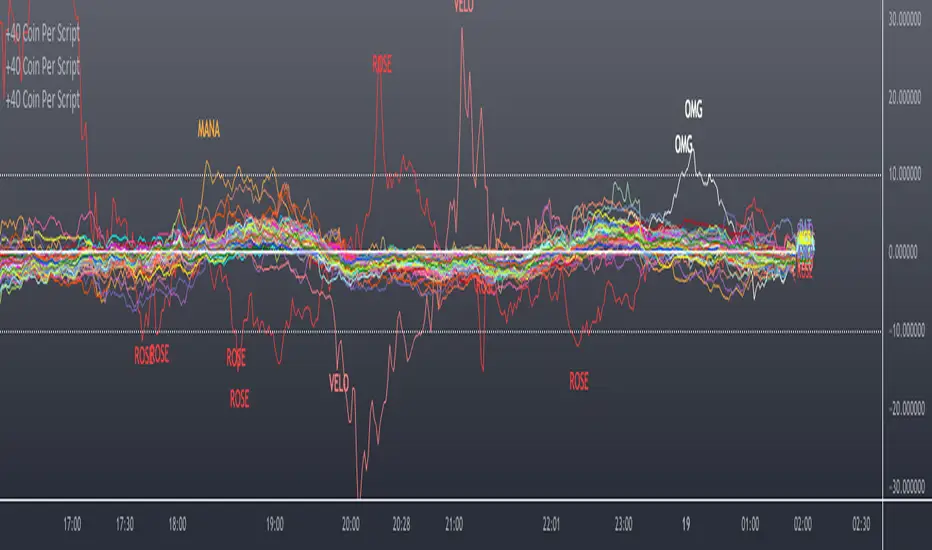

Scanner/Screener of Over 40 Coins Per Script I am very scatter-brained by nature and sporadic in my thought processes but if these benefit the community and ya'll ask for more perhaps I will get better and even out a tad....probably not....but you never know. Firstly, allow me to apologize to all the vet/more sophisticated coders out there whose eyes and brains might just be overly taxed due to my poor coding structure. Im just getting started for the first time in ANY sort of coding...so cut me a little slack. Also, if anyone sees any mistakes or the functionality is not as I proclaimed, PLEASE do let me know. In these past 12mo of me learning my 1st coding language (Pinescript) I would say that I have been intently focused on creating all types/sorts of scanners/screeners. Ive always hoped to be a benefit to the community as I was always SO grateful to those who have come before me that have led me to the little bit of progress I have made with Pinescript. This script is not necessarily something that should be traded with as it is just a thrown together example showing a scanner/screener whose results produce plot outputs (ie, Rate of Change / oscillators as well / etc) and how they can be used in the alert system so that only 1 alert has to be set per iteration of the script but more importantly how to use/scan/screen with over 40 coins per script. My intent is not to trick anyone here. So to be PERFECTLY CLEAR, more than 40 coins CAN in fact be screened/scanned from one script (here I am doing all of KUCOIN's Margin Coins...72 total I look at)...BUT...(heres the catch) it must be added to the chart however many times EQUAL to the amount of "sets" you have in your script. (Heres the limitation by TV) There cannot be more than 40 coins in each "set". The less coins you have per set, the quicker the script will startup and run, thus, the quicker alerts will be received if automating the process. Though, if you only have the free plan and can only have MAX 3 indicators per chart then the MAX you can screen at a time is 120 coins if you use 40 coins per set. So, this is the first one I would like to introduce. For this one your screener/scanner must be using some sort of plots as output that is being screened for. (original inspiration of ALL my variations mainly come from @QuantNomad, @daveatt, and @LonesomeTheBlue (and a few others I may be forgetting at the moment). Thanks for the inspiration through countless publications that ya'll have created for us in the community.

Some of my variations are more complex/elegant than others but there are MANY very different ones that I would like to share with the community. If you leave a comment and wonder why I have not responded but did so to every comment around yours...see if you are one of the individuals in this next few sentences...and if you are then perhaps someone else would like to waste their time responding to your comment...but basically, if you don't want to spend the time helping yourself by reading the title, description section, AND the comments section (at least scanning them) then I am MOST DEFINITELY not going to help you down your path of destruction that is most likely soon to be your blown-up trading account. I was called a "masochist" after asking for guidance on if its worth the headache to publish anything on TV bc there will NO DOUBT be comments that'll make me wish I didn't (ie. someone CLEARLY not reading the description (or seemingly even the title sometimes) bc they make a comment that has been explicitly addressed, or someone asking to rebuild the code compatible for another charting software or whatnot, or how about those asking if it repaints (this one is almost always addressed in the comments section but I can understand this question more than others as Im only 1 yr into learning any sort of coding for the first time in the beginning I saw people ask on EVERY script about if it repainted and it was worrisome at the lest (esp bc I didn't even understand what it was not so long ago, or my favorite...what TF it works best on...these people CLEARLY need not be trading yet if your still asking questions as such...Ill end it there). Point being, Ive got some truly VERY useful scripts that I want to share and as long as these people don't make me regret doing so in the beginning, then whats mine...will soon be yours. Though, I will take a little time between the releases.

YOU GUYS (TV and its community) ARE AWESOME (most of you anyways ;)

MUCH LOVE,

ChasinAlts

(1) INPUTS

Here is where the "sets" come in. I am looking at all of KUCOIN's Margin Coins (72 of them at least) so am splitting them up into 3 sets/iterations and a copy of the script must be added equal to amount of "sets" you have here. This is the ONLY workaround I have found to be able to scan/screen with more than 40 coins per script (due to TV's limitation of 40 Security Calls per script) ***So for everyone saying it's impossible scan more than 40 Coins per scipt...it' MOST DEFINITELY possible....BUT ONLY by adding this script multiple times on the chart and selecting 1 of each of the "sets" in the script settings via the chart window. To save the much needed room you must push each iteration of the script into 1 window and merging the scales of each into 1 scale(ie. "Scale A") within the settings of the script name on the chart(3 horizontal dots)

(2) FUNCTION

(2.1) COLORIDs

This is just to set up all my Colors of plots which are being matched with their respective labels. I have a diff color for each of the 72 coins Im plotting so Im telling the function, "depending on which set of coins I select...give me this color out of the colors I input later into the function"

(2.2) TICKERID CONSTRUCTION

I construct the tickerID this way so that the labels on my plots have only the Coin's name vs the label having the (Exchange Name):(Coin Name)(Base Pair Name). If you are using more than 1 Base pair (ie. XRP/BTC and XRP/USDT and XRP/ETH) OR more than 1 Exchange OR want your plots to show MORE THAN just the Trading Coin's name, then the tickerID MUST BE constructed differently

(2.3) SECURITY CALL & PLOT OUTPUT VARIABLES

If using a Higher Time Frame in Security Call then it MUST BE adjusted to permit or dissallow repainting if you so wish (BEYOND THE SCOPE OF THIS PUBLICATION so Do Your Own Researh). If your MAIN LOGIC is more complex than simply using a TV built-in function), THEN it MUST BE built into its own function outside of this function and called on within the "expression" slot of this Security Call OR can also be built into this function and called on in the "expression" slot of this Security call (BEYOND THE SCOPE OF THIS PUB SO DYOR). FURTHERMORE...when you are using a series(ie high/low/close/open/hl2/etc) / bar_index / time / etc that will be specific to the Coin/tickerID, then they MUST BE explicitly used within the "expression" slot of the Security Function when calling on your Main Logic or else it will pull the series/time/bar_index/etc from the Coin that the Chart is presently on (BEYOND THE SCOPE OF THIS PUB SO DYOR)

(2.4) PLOT LABEL

This is the Plot's Label that will be next to the end of the plot on the LAST bar_index. ***Notice in the "text" slot of the label I have "_coin" (without the quotes obviously)...this is where have JUST the Coin's name comes into effect on the label vs the (Exchange Name):(Coin Name)(Base Pair Name) which looks MUCH cleaner

(2.5) ALERT LOGIC / ALERT LABEL

Your alert logic need not be as complex as this... I just wanted to create a decent enough timing for this system and wanted to simply print the labels displaying which coin produced the alert at the same time the alerts would go off. Alert is set up to Trigger Bullish when the ROC is below the Threshold and _chg > _chg X=length of bars inputted in "Rising/Falling Length" setting and vise versa for Bearish Alerts. If _chg plot only goes past threshold for a VERY few amount of bars NOT providing enough time for initial Alert to trigger, then alert/label triggers on crossing of threshold back towards 0(zero). ONLY 1 alert needs to be set per script to be able to scan ALL 72 of the coins as I have them in this script. Timing of Alert is inline with the name label printed past the thresholds.

(3) VARIABLES FROM MAIN FUNCTION

This is the tuple of the Main Function that outputs the variables from 3 lines up to be able to plot the lines and color them according to the colors on the labels. *** As of now, we CANNOT plot from within the function so MUST BE done this way to produce the variables and colors needed. The plots are the ONLY thing in this script that cannot be executed from within the function

(4) LINE PLOTS

ALL output variables from our Main Function are used here for the line plots

DAYOFWEEK performance1 -Objective

"What is the ''best'' day to trade .. Monday, Tuesday...."

This script aims to determine if there are different results depending on the day of the week.

The way it works is by dividing data by day of the week (Monday, Tuesday, Wednesday ... ) and perform calculations for each day of the week.

1 - Objective

2 - Features

3 - How to use (Examples)

4 - Inputs

5 - Limitations

6 - Notes

7 - Final Tooughs

2 - Features

AVG OPEN-CLOSE

Calculate de Percentage change from day open to close

Green % (O-C)

Percentage of days green (open to close)

Average Change

Absolute day change (O-C)

AVG PrevD. Close-Close

Percentage change from the previous day close to the day of the week close

(Example: Monday (C-C) = Friday Close to Monday close

Tuesday (C-C) = Monday C. to Tuesday C.

Green % (C1-C)

Percentage of days green (open to close)

AVG Volume

Day of the week Average Volume

Notes:

*Mon(Nº) - Nº = Number days is currently calculated

Example: Monday (12) calculation based on the last 12 Mondays. Note: Discrepancies in numbers example Monday (12) - Friday (11) depend on the initial/end date or the market was closed (Holidays).

3 - How to use (Examples)

For the following example, NASDAQ:AAPL from 1 Jan 21 to 1 Jul 21 the results are following.

The highest probability of a Close being higher than the Open is Monday with 52.17 % and the Lowest Tuesday with 38.46 %. Meaning that there's a higher chance (for NASDAQ:AAPL ) of closing at a higher value on Monday while the highest chance of closing is lower is Tuesday. With an average gain on Tuesday of 0.21%

Long - The best day to buy (long) at open (on average) is Monday with a 52.2% probability of closing higher

Short - The best day to sell (short) at open (on average) is Tuesday with a 38.5% probability of closing higher (better chance of closing lower)

Since the values change from ticker to ticker, there is a substantial change in the percentages and days of the week. For example let's compare the previous example ( NASDAQ:AAPL ) to NYSE:GM (same settings)

For the same period, there is a substantial difference where there is a 62.5% probability Friday to close higher than the open, while Tuesday there is only a 28% probability.

With an average gain of 0.59% on Friday and an average loss of -0.34%

Also, the size of the table (number of days ) depends if the ticker is traded or not on that day as an example COINBASE:BTCUSD

4 - Inputs

DATE RANGE

Initial Date - Date from which the script will start the calculation.

End Date - Date to which the script will calculate.

TABLE SETTINGS

Text Color - Color of the displayed text

Cell Color - Background color of table cells

Header Color - Color of the column and row names

Table Location - Change the position where the table is located.

Table Size - Changes text size and by consequence the size of the table

5 - LIMITATIONS

The code determines average values based on the stored data, therefore, the range (Initial data) is limited to the first bar time.

As a consequence the lower the timeframe the shorter the initial date can be and fewer weeks can be calculated. To warn about this limitation there's a warning text that appears in case the initial date exceeds the bar limit.

Example with initial date 1 Jan 2021 and end date 18 Jul 2021 in 5m and 10 m timeframe:

6 - Notes and Disclosers

The script can be moved around to a new pane if need. -> Object Tree > Right Click Script > Move To > New pane

The code has not been tested in higher subscriptions tiers that allow for more bars and as a consequence more data, but as far I can tell, it should work without problems and should be in fact better at lower timeframes since it allows more weeks.

The values displayed represent previous data and at no point is guaranteed future values

7 - Final Tooughs

This script was quite fun to work on since it analysis behavioral patterns (since from an abstract point a Tuesday is no different than a Thursday), but after analyzing multiple tickers there are some days that tend to close higher than the open.

PS: If you find any mistake ex: code/misspelling please comment.

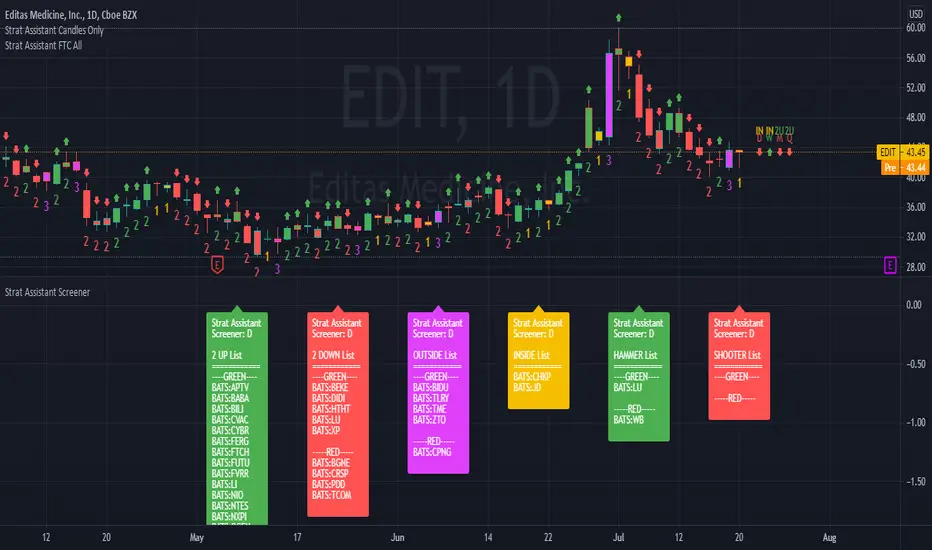

Strat Assistant ScreenerStrat Assistant Screener

----------------------------

█ OVERVIEW

This script is intended to provide screening/scanning functionality for the strat for the time period provided in the input (Day is the default).

When added, the script provides a chart with labels separated for each type of candle (2 up, 2 down, outside, inside) as well as actionable signals (inside already provided, hammer, shooter). Trading view is limited to 40 "security/ticker/symbol" calls so only 40 at a time are available. It's best to run this on higher time frames as it will occasionally push peak trading view memory limits and throw an error. Various inputs are provided a detailed below. It's not FAST so be patient please.

█ DETAIL

Inputs

----------

Security/Screener Time Frame: The screener will only run for one time frame, the time frame selected and this can be changed

Actionable Wick Percentage: The percentage of the WICK to determine a hammer or a shooter. For example, the default is .75 or 75%, which means 75% of the candle must be a WICK (top wick 75% for shooter, bottom wick 75% for hammer). If you wish to be more conservative scale it down or more aggressive scale it up

Label Index Offset Factor: There are 6 separate labels that will appear at the bottom separated by this indicator. If you feel like things are too tight or too narrow you can adjust this to spread things out further, or push them closer together.

Security/SXX: The various securities that can be input to track. If you find this is a pain, you can always copy the source code, put it in the pine editor yourself, and manually modify them there. Trading view limits you to 40 securities/symbols/tickers so I've pushed the limit as far as I can with this script.

Outputs

----------

The screener will provide a second chart at the bottom of the primary chart with labels for the types of candles and actionable signals

Each label will be present even if no results are found.

The label will display the time frame selected toward the end of the header - Strat Assistant Screener:

Each label is colored for quick reference to indicate the various bull/bear/inside/outside "patterns"

Best Practices

----------

It is not fast, so please be patient and let it run.

This screener is best used as a utility a few times a day, not recommended for intraday. I will create a scaled down version of this will only 5 securities/symbols/tickers that can be used intraday.

The screener pushes the limits of training views provided memory, so you may occasionally see errors, please try a higher time frame.

The bottom chart can be scaled and moved just like the top one, play around with it to determine what works best for you. I recommend decreasing the scale and then moving it up so you can see it better.

When the time frame is changed, it will take a minute, you can verify the results by seeing the time frame change in the label - Strat Assistant Screener:

I have not played with this thoroughly intraday yet. So it may be buggy/slower.

Bitfinex Spot PremiumOverview

A tool to display the spot price premium of Bitfinex coins vs the other big 3 exchanges.

Premium is calculated against:

- Coinbase

- Binance

- FTX

The average is calculated through volume weighting. The absolute difference between the Bitfinex spot price and the calculated average is then displayed on the histogram.

Interacting with the tool

Colours: Green bars indicate a positive premium (Bitfinex spot price is greater than the average), Red bars indicate a negative premium. The ability to grey out smaller premiums is also enabled with the "Grey Small Vals" checkbox, this can be used to further emphasise larger premiums.

Ticker: The ticker input allows you to detect the Bitfinex premium for any coin traded within all 4 exchanges (Bitfinex, Coinbase, Binance, FTX). Just input the coins ticker symbol, for example, "BTC", "ETH", "UNI".

Indicator Ideology

Bitfinex is known for being the home of crypto "smart money". Therefore, positive premiums indicate stronger buying from "smart money". Although this premium is a good sign of bullish/ bearish market conditions, for example, consecutive days of a negative Bitfinex premium have been pretty good at indicating short term tops in BTC, this indicator should only be used as a confirmation signal.

Big Move WarningThis script shows plots a warning on the chat when the tick increase is more than the configures value.

It considers the highest and lowest value of each candle.

The following warnings are shown:

"RISE" - the increase is more than the configures value

"BIGRISE" - the increase over the last 3 ticks is more than 2x the configured value

"DIP" - the decrease is more than the configures value

"BIGDIP" - the decrease over the last 3 ticks iscmore than 2x the configured value

CC - Macro Consolidated Interval Display (MCID)Ever wish you didn't have to rapidly flip between 6 different tickers to get the full picture?

Yeah, me too. Do you also wish that you kind of understood how the shift / unshift function works for arrays?

Yeah, I did too. Both of those birds are taken care of with one stone!

The Macro Consolidated Interval Display uses the new Array structure and security to display data for VIX, GLD, TLT, QQQ, SPY and IWM (at a 1D interval) SIMUTANEOUSLY! Regardless of which ticker you're looking at you can get the full picture of macro futures data without flipping around to get it.

This is my first script trying to use arrays. It basically shows the following a 1d interval:

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP for VIX.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP for GLD.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP for TLT.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP for QQQ.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP for SPY.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP for IWM

To make it more or less busy, I've allowed you to toggle off any of the levels you wish. I've also chosen to leave this as open source, as it's nothing too experimental, and I hope that it can gain some traction as an Array example that the public can use! If you don't like the different values that are shown, use this source code example as a spring-board to put values that you do care about onto the labels.

If this code has helped you at all please drop me a like or some constructive criticism if you do not think it's worth a like.

Good luck and happy trading friends. This should be compatible with my CID as well:

If this gets traction, I will post something similar for a dynamic combination of tickers and intervals that you can set yourself.

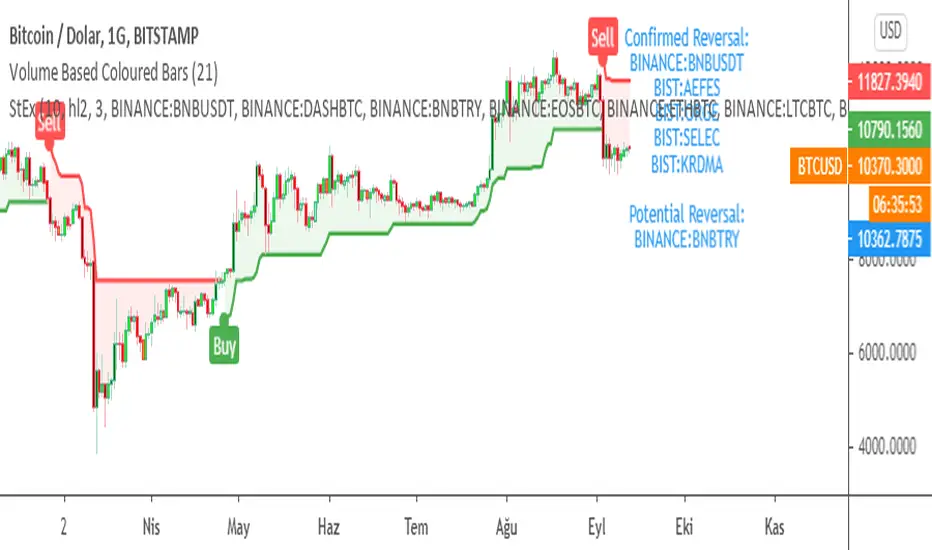

SuperTrend EXPLORER / SCREENERSUPERTREND EXPLORER / SCREENER screens the BUY and SELL signals (trend reversals) for 38 user defined different tickers in Tradingview charts.

Simply input the short name of the ticker in Tradingview that you want to screen.

Script is derived from zzzcrypto123 's work. Thanks for the permission letting me to use his logic.

Terminology explanation:

Confirmed Reversal: Supertrend reversal that happened in the last bar and cannot be repainted.

Potential Reversal: Supertrend reversal that might happen in the current bar but can also not happen depending upon the timeframe closing price.

Screener has also got a built in SuperTrend indicator which users can confirm the reversals on graphs.

Screener explores the 38 tickers in current graph's time frame and also in desired parameters of the SuperTrend indicator.

SUPERTREND INDICATOR:

STRATEGY version of SuperTrend Indicator:

SuperTrend is one of the most common ATR based trailing stop indicators.

In this version you can change the ATR calculation method from the settings. Default method is RMA, when the alternative method is SMA .

The indicator is easy to use and gives an accurate reading about an ongoing trend. It is constructed with two parameters, namely period and multiplier. The default values used while constructing a superindicator are 10 for average true range or trading period and three for its multiplier.

The average true range (ATR) plays an important role in 'Supertrend' as the indicator uses ATR to calculate its value. The ATR indicator signals the degree of price volatility .

The buy and sell signals are generated when the indicator starts plotting either on top of the closing price or below the closing price. A buy signal is generated when the ‘Supertrend’ closes above the price and a sell signal is generated when it closes below the closing price.

It also suggests that the trend is shifting from descending mode to ascending mode. Contrary to this, when a ‘Supertrend’ closes above the price, it generates a sell signal as the colour of the indicator changes into red.

A ‘Supertrend’ indicator can be used on equities, futures or forex, or even crypto markets and also on daily, weekly and hourly charts as well, but generally, it fails in a sideways-moving market.

Source function added to use the indicator as the ATR Trailing Stop indicator.

Just change source type hl2 to close.

different variations might be useful.

Alpha & BetaAlpha & Beta Indicators for Portfolio Performance

β = Σ Correlation (RP, RM) * (σP/σM)

α P = E(RP) –

Where,

RP = Portfolio Return (or Investment Return)

RM = Market Return (or Benchmark Index)

RF = Risk-Free Rate

How to use the Indicator

RM = SPX (Default)

The Market Return for the indicator has the options of $SPX, $NDX, or $DJI (S&P 500, Nasdaq 100, Dow 30)

RF = FRED: DTB3

The Risk-Free Rate in the Indicator is set to the 3-Month Treasury Bill: Secondary Market Rate

The Default Timeframe is 1260 or 5-Years (252 Trading Days in One Year)

RP = The symbol you enter

HOWEVER , you can determine your portfolio value by following the following directions below.

Note: I am currently working on an indicator that will allow you to insert the weights of your positions.

Complete Portfolio Analysis Directions

You will first need...

a) spreadsheet application - Google Sheets is Free, but Microsoft Excel will convert ticker symbols to Stocks and Retrieve Data.

b) your current stock tickers, quantity of shares, and last price information

In the spreadsheet,

In the first column list the stock tickers...

AMZN

AAPL

TSLA

In the second column list the quantity of shares you own...

5

10

0.20

In the third column insert the last price

Excel: Three tickers will automatically give you the option to "Convert to Stocks",

after conversion, click once on cell and click the small tab in the upper right-hand of the highlighted cell.

Click the tab and a menu pops up

Find "Price", "Price Extended-Hours", or "Previous Close"...

$3,284.72

$497.48

$2,049.98

Next, multiply the number of shares by the price (Stock Market Value)

Excel: in fourth column type "=(B1*C1)", "=(B2*C2)", "=(B3*C3)"...

= $16,423.60

= $4,974.80

= $410.00

add the three calculated numbers together or click "ΣAutoSum" (Portfolio Market Value)

= $21,808.40

Last, divide the market value of AMZN ($16,423.60) by the Portfolio Market Value ($21,808.40) for each of the stocks.

= 0.7531

= 0.2281

= 0.0188

These values are the weight of the stock in your portfolio.

Go back to TradingView

Enter into the "search box" the following...

AMZN*0.7531 + AAPL*0.2281 + TSLA*0.0188

and click Enter

Now you can use the "Alpha & Beta" Indicator to analyze your entire portfolio!

Hashem Correlation CoefficientCorrelation Coefficient

Core Code from: www.tradingview.com

This indicator Show Correlation between the Current Ticker & timeframe and a Customizable Ticker. After adding the indicator you can change the second ticker in the settings.

The Correlation Coeff is between -1 to 1 which 1 means 100% correlation and -1 means -100% correlation ( Inverse Correlation ).

The color of the area changes when:

Blue : CC > 0.5

Aqua : CC > 0.75

Purple : CC < -0.5

Red : CC < -0.75

EMA CrossoverEMA Crossover

Input Parameters:

Stop loss (ticks) - define stop loss in unit of ticks (*1 tick = 12.5)

Exit signal - 1: When EMA and price crosses

2: When EMA changes direction

Start year, month, day & Stop year, month, day - define backtest period

You can set Order size, Commission in Settings, Properties tab.

Open Interest:CME e-o-d vs CFTC e-o-wCFTC only publishes total OI on fridays, related to last Tuesday.

But what happened since last Tuesday?

CME Vol & Open Interest data is recorded&exported daily by quandl.com to tradingview

via the che CHRIS/CME datasets

www.quandl.com

Eg. Nat Gas next outstanding cntract n. 20, field n. 7(OI)

@quandl.com:

www.quandl.com

is exported @tradingview:

www.tradingview.com

Every outstanding contract's OI & vol is exported (black column), but not the total (yellow line):

tiny.cc

This script sums up all the existing outstanding contract's OI for the future (the black column), so one can have an idea of the total OI for the day (Yellow line).

As numer of outstanding contracts varies from future to future,Eg:

E-mini (ES) has 4 contracts, Gold(GC) 16 cntrcts, NatGas(NG) has 43, WTI(CL) has 38 etc

the scrips tries to guess how many exist for it and sums them up, to have the total OI for tha day

Number ofoutstanding contracts exported by quandl.com to tradingview is taken from

s3.amazonaws.com

There are 2 params you can enter on the script:

* override the ticket symbol on the chart ,if script cannot guessit or you need a different one

* enter the "preliminary" OI that is published by CME early the next day, butb not yet exported by quandl to tradingview

This script is Open so anyone can copy and modifyit for its use.

Please post comments and ideas if you find it useful

I try to keep a log of my work here:

Multi SMA EMA WMA HMA BB (5x8 MAs Bollinger Bands) MAX MTF - RRBMulti SMA EMA WMA HMA 4x7 Moving Averages with Bollinger Bands MAX MTF by RagingRocketBull 2019

Version 1.0

All available MAX MTF versions are listed below (They are very similar and I don't want to publish them as separate indicators):

ver 1.0: 4x7 = 28 MTF MAs + 28 Levels + 3 BB = 59 < 64

ver 2.0: 5x6 = 30 MTF MAs + 30 Levels + 3 BB = 63 < 64

ver 3.0: 3x10 = 30 MTF MAs + 30 Levels + 3 BB = 63 < 64

ver 4.0: 5(4+1)x8 = 8 CurTF MAs + 32 MTF MAs + 20 Levels + 3 BB = 63 < 64

ver 5.0: 6(5+1)x6 = 6 CurTF MAs + 30 MTF MAs + 24 Levels + 3 BB = 63 < 64

ver 6.0: 4(3+1)x10 = 10 CurTF MAs + 30 MTF MAs + 20 Levels + 3 BB = 63 < 64

Fib numbers: 8, 13, 21, 34, 55, 89, 144, 233, 377

This indicator shows multiple MAs of any type SMA EMA WMA HMA etc with BB and MTF support, can show MAs as dynamically moving levels.

There are 4 MA groups + 1 BB group, a total of 4 TFs * 7 MAs = 28 MAs. You can assign any type/timeframe combo to a group, for example:

- EMAs 9,12,26,50,100,200,400 x H1, H4, D1, W1 (4 TFs x 7 MAs x 1 type)

- EMAs 8,13,21,30,34,50,55,89,100,144,200,233,377,400 x M15, H1 (2 TFs x 14 MAs x 1 type)

- D1 EMAs and SMAs 8,13,21,30,34,50,55,89,100,144,200,233,377,400 (1 TF x 14 MAs x 2 types)

- H1 WMAs 13,21,34,55,89,144,233; H4 HMAs 9,12,26,50,100,200,400; D1 EMAs 12,26,89,144,169,233,377; W1 SMAs 9,12,26,50,100,200,400 (4 TFs x 7 MAs x 4 types)

- +1 extra MA type/timeframe for BB

There are several versions: Simple, MTF, Pro MTF, Advanced MTF, MAX MTF and Ultimate MTF. This is the MAX MTF version. The Differences are listed below. All versions have BB

- Simple: you have 2 groups of MAs that can be assigned any type (5+5)

- MTF: +2 custom Timeframes for each group (2x5 MTF) +1 TF for BB, TF XY smoothing

- Pro MTF: 4 custom Timeframes for each group (4x3 MTF), 1 TF for BB, MA levels and show max bars back options

- Advanced MTF: +4 extra MAs/group (4x7 MTF), custom Ticker/Symbols, Timeframe <>= filter, Remove Duplicates Option

- MAX MTF: +2 subtypes/group, packed to the limit with max possible MAs/TFs: 4x7, 5x6, 3x10, 4(3+1)x10, 5(4+1)x8, 6(5+1)x6

- Ultimate MTF: +individual settings for each MA, custom Ticker/Symbols

MAX MTF version tests the limits of Pinescript trying to squeeze as many MAs/TFs as possible into a single indicator.

It's basically a maxed out Advanced version with subtypes allowing for mixed types within a group (i.e. both emas and smas in a single group/TF)

Pinescript has the following limits:

- max 40 security calls (6 calls are reserved for dupe checks and smoothing, 2 are used for BB, so only 32 calls are available)

- max 64 plot outputs (BB uses 3 outputs, so only 61 plot outputs are available)

- max 50000 (50kb) size of the compiled code

Based on those limits, you can only have the following MAs/TFs combos in a single script:

1. 4x7, 5x6, 3x10 - total number of MTF MAs must always be <= 32, and you can still have BB and Num Levels = total MAs, without any compromises

2. 5(4+1)x8, 6(5+1)x6, 4(3+1)x10 - you can use the Current Symbol/Timeframe as an extra (+1) fixed TF with the same number of MTF MAs

- you don't need to call security to display MAs on the Current Symbol/Timeframe, so the total number of MTF MAs remains the same and is still <= 32

- to fit that many MAs into the max 64 plot outputs limit you need to reduce the number of levels (not every MA Group will have corresponding levels)

Features:

- 4x7 = 28 MAs of any type

- 4x MTF groups with XY step line smoothing

- +1 extra TF/type for BB MAs

- 2 MA subtypes within each group/TF

- 4x7 = 28 MA levels with adjustable group offsets, indents and shift

- supports any existing type of MA: SMA, EMA, WMA, Hull Moving Average (HMA)

- custom tickers/symbols for each group

- show max bars back option

- show/hide both groups of MAs/levels/BB and individual MAs

- timeframe filter: show only MAs/Levels with TFs <>= Current TF

- hide MAs/Levels with duplicate TFs

- support for custom TFs that are not available in free accounts: 2D, 3D etc

- support for timeframes in H: H, 2H, 4H etc

Notes:

- Uses timeframe textbox instead of input resolution dropdown to allow for 240 120 and other custom TFs

- Uses symbol textbox instead of input symbol to avoid establishing multiple dummy security connections to the current ticker - otherwise empty symbols will prevent script from running

- Possible reasons for missing MAs on a chart:

- there may not be enough bars in history to start plotting it. For example, W1 EMA200 needs at least 200 bars on a weekly chart.

- for charts with low/fractional prices i.e. 0.00002 << 0.001 (default Y smoothing step) decrease Y smoothing as needed (set Y = 0.0000001) or disable it completely (set X,Y to 0,0)

- for charts with high price values i.e. 20000 >> 0.001 increase Y smoothing as needed (set Y = 10-20). Higher values exceeding MAs point density will cause it to disappear as there will be no points to plot. Different TFs may require diff adjustments

- TradingView Replay Mode UI and Pinescript security calls are limited to TFs >= D (D,2D,W,MN...) for free accounts

- attempting to plot any TF < D1 in Replay Mode will only result in straight lines, but all TFs will work properly in history and real-time modes. This is not a bug.

- Max Bars Back (num_bars) is limited to 5000 for free accounts (10000 for paid), will show error when exceeded. To plot on all available history set to 0 (default)

- Slow load/redraw times. This indicator becomes slower, its UI less responsive when:

- Pinescript Node.js graphics library is too slow and inefficient at plotting bars/objects in a browser window. Code optimization doesn't help much - the graphics engine is the main reason for general slowness.

- the chart has a long history (10000+ bars) in a browser's cache (you have scrolled back a couple of screens in a max zoom mode).

- Reload the page/Load a fresh chart and then apply the indicator or

- Switch to another Timeframe (old TF history will still remain in cache and that TF will be slow)

- in max possible zoom mode around 4500 bars can fit on 1 screen - this also slows down responsiveness. Reset Zoom level

- initial load and redraw times after a param change in UI also depend on TF. For example: D1/W1 - 2 sec, H1/H4 - 5-6 sec, M30 - 10 sec, M15/M5 - 4 sec, M1 - 5 sec. M30 usually has the longest history (up to 16000 bars) and W1 - the shortest (1000 bars).

- when indicator uses more MAs (plots) and timeframes it will redraw slower. Seems that up to 5 Timeframes is acceptable, but 6+ Timeframes can become very slow.

- show_last=last_bars plot limit doesn't affect load/redraw times, so it was removed from MA plot

- Max Bars Back (num_bars) default/custom set UI value doesn't seem to affect load/redraw times

- In max zoom mode all dynamic levels disappear (they behave like text)

- Dupe check includes symbol: symbol, tf, both subtypes - all must match for a duplicate group

- For the dupe check to work correctly a custom symbol must always include an exchange prefix. BB is not checked for dupes

Good Luck! Feel free to learn from/reuse the code to build your own indicators.