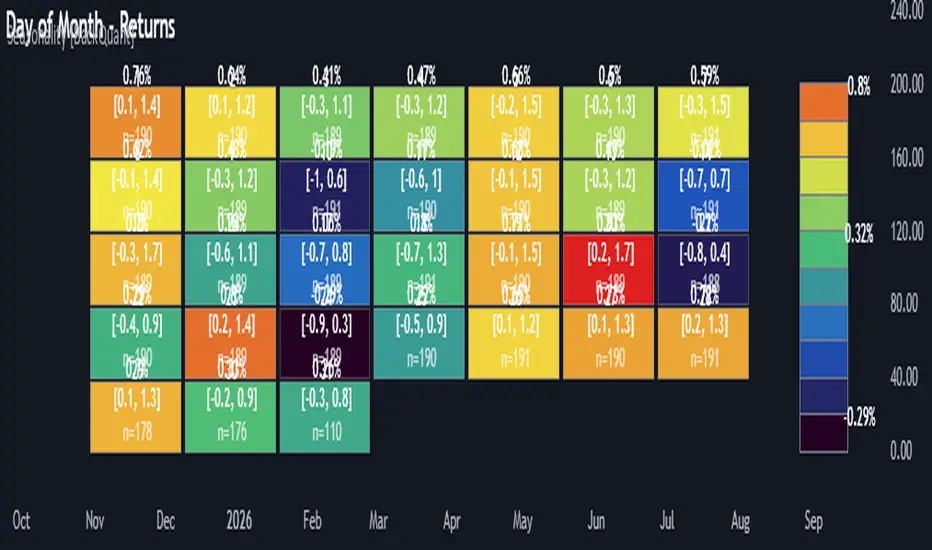

Multi-Mode Seasonality Map [BackQuant]Multi-Mode Seasonality Map

A fast, visual way to expose repeatable calendar patterns in returns, volatility, volume, and range across multiple granularities (Day of Week, Day of Month, Hour of Day, Week of Month). Built for idea generation, regime context, and execution timing.

What is “seasonality” in markets?

Seasonality refers to statistically repeatable patterns tied to the calendar or clock, rather than to price levels. Examples include specific weekdays tending to be stronger, certain hours showing higher realized volatility, or month-end flow boosting volumes. This tool measures those effects directly on your charted symbol.

Why seasonality matters

It’s orthogonal alpha: timing edges independent of price structure that can complement trend, mean reversion, or flow-based setups.

It frames expectations: when a session typically runs hot or cold, you size and pace risk accordingly.

It improves execution: entering during historically favorable windows, avoiding historically noisy windows.

It clarifies context: separating normal “calendar noise” from true anomaly helps avoid overreacting to routine moves.

How traders use seasonality in practice

Timing entries/exits : If Tuesday morning is historically weak for this asset, a mean-reversion buyer may wait for that drift to complete before entering.

Sizing & stops : If 13:00–15:00 shows elevated volatility, widen stops or reduce size to maintain constant risk.

Session playbooks : Build repeatable routines around the hours/days that consistently drive PnL.

Portfolio rotation : Compare seasonal edges across assets to schedule focus and deploy attention where the calendar favors you.

Why Day-of-Week (DOW) can be especially helpful

Flows cluster by weekday (ETF creations/redemptions, options hedging cadence, futures roll patterns, macro data releases), so DOW often encodes a stable micro-structure signal.

Desk behavior and liquidity provision differ by weekday, impacting realized range and slippage.

DOW is simple to operationalize: easy rules like “fade Monday afternoon chop” or “press Thursday trend extension” can be tested and enforced.

What this indicator does

Multi-mode heatmaps : Switch between Day of Week, Day of Month, Hour of Day, Week of Month .

Metric selection : Analyze Returns , Volatility ((high-low)/open), Volume (vs 20-bar average), or Range (vs 20-bar average).

Confidence intervals : Per cell, compute mean, standard deviation, and a z-based CI at your chosen confidence level.

Sample guards : Enforce a minimum sample size so thin data doesn’t mislead.

Readable map : Color palettes, value labels, sample size, and an optional legend for fast interpretation.

Scoreboard : Optional table highlights best/worst DOW and today’s seasonality with CI and a simple “edge” tag.

How it’s calculated (under the hood)

Per bar, compute the chosen metric (return, vol, volume %, or range %) over your lookback window.

Bucket that metric into the active calendar bin (e.g., Tuesday, the 15th, 10:00 hour, or Week-2 of month).

For each bin, accumulate sum , sum of squares , and count , then at render compute mean , std dev , and confidence interval .

Color scale normalizes to the observed min/max of eligible bins (those meeting the minimum sample size).

How to read the heatmap

Color : Greener/warmer typically implies higher mean value for the chosen metric; cooler implies lower.

Value label : The center number is the bin’s mean (e.g., average % return for Tuesdays).

Confidence bracket : Optional “ ” shows the CI for the mean, helping you gauge stability.

n = sample size : More samples = more reliability. Treat small-n bins with skepticism.

Suggested workflows

Pick the lens : Start with Analysis Type = Returns , Heatmap View = Day of Week , lookback ≈ 252 trading days . Note the best/worst weekdays and their CI width.

Sanity-check volatility : Switch to Volatility to see which bins carry the most realized range. Use that to plan stop width and trade pacing.

Check liquidity proxy : Flip to Volume , identify thin vs thick windows. Execute risk in thicker windows to reduce slippage.

Drill to intraday : Use Hour of Day to reveal opening bursts, lunchtime lulls, and closing ramps. Combine with your main strategy to schedule entries.

Calendar nuance : Inspect Week of Month and Day of Month for end-of-month, options-cycle, or data-release effects.

Codify rules : Translate stable edges into rules like “no fresh risk during bottom-quartile hours” or “scale entries during top-quartile hours.”

Parameter guidance

Analysis Period (Days) : 252 for a one-year view. Shorten (100–150) to emphasize the current regime; lengthen (500+) for long-memory effects.

Heatmap View : Start with DOW for robustness, then refine with Hour-of-Day for your execution window.

Confidence Level : 95% is standard; use 90% if you want wider coverage with fewer false “insufficient data” bins.

Min Sample Size : 10–20 helps filter noise. For Hour-of-Day on higher timeframes, consider lowering if your dataset is small.

Color Scheme : Choose a palette with good mid-tone contrast (e.g., Red-Green or Viridis) for quick thresholding.

Interpreting common patterns

Return-positive but low-vol bins : Favorable drift windows for passive adds or tight-stop trend continuation.

Return-flat but high-vol bins : Opportunity for mean reversion or breakout scalping, but manage risk accordingly.

High-volume bins : Better expected execution quality; schedule size here if slippage matters.

Wide CI : Edge is unstable or sample is thin; treat as exploratory until more data accumulates.

Best practices

Revalidate after regime shifts (new macro cycle, liquidity regime change, major exchange microstructure updates).

Use multiple lenses: DOW to find the day, then Hour-of-Day to refine the entry window.

Combine with your core setup signals; treat seasonality as a filter or weight, not a standalone trigger.

Test across assets/timeframes—edges are instrument-specific and may not transfer 1:1.

Limitations & notes

History-dependent: short histories or sparse intraday data reduce reliability.

Not causal: a hot Tuesday doesn’t guarantee future Tuesday strength; treat as probabilistic bias.

Aggregation bias: changing session hours or symbol migrations can distort older samples.

CI is z-approximate: good for fast triage, not a substitute for full hypothesis testing.

Quick setup

Use Returns + Day of Week + 252d to get a clean yearly map of weekday edge.

Flip to Hour of Day on intraday charts to schedule precise entries/exits.

Keep Show Values and Confidence Intervals on while you calibrate; hide later for a clean visual.

The Multi-Mode Seasonality Map helps you convert the calendar from an afterthought into a quantitative edge, surfacing when an asset tends to move, expand, or stay quiet—so you can plan, size, and execute with intent.

Buscar en scripts para "乌德勒支+VS+赫拉克勒斯"

Fixed High Timeframe Moving AveragesFixed High Timeframe Moving Averages (W/D/4H)

Summary

This indicator plots essential, high-timeframe (HTF) Moving Averages onto your chart, **no matter which timeframe you are currently viewing**.

It is designed for traders who need multi-timeframe context at a glance. Stop switching charts to see where the 200-Week or 50-Day MA is—now you can see all critical HTF levels directly on your 5-minute (or any other) chart.

---

Who it’s for

Traders who rely on moving averages but like to work on lower chart timeframes while keeping higher timeframe context in sight. If you scalp on 1–15m yet want Weekly/Daily/4H MAs always visible, this is for you.

---

What it shows

Pinned (“fixed”) moving averages from higher timeframes—Weekly (20/100/200) , Daily (50/100/200/365) and 4H (200) —rendered on any chart timeframe. Your favorite HTF MAs stay on screen no matter what TF you’re currently analyzing.

---

Features

* **MA types:** SMA, EMA, VWMA, Hull.

* **Fully configurable:** toggle each line, set periods, colors, and thickness.

* **Two alert modes (see below):** intrabar vs confirmed HTF close.

* **Works on any symbol & chart TF** using `request.security` to fetch HTF data.

---

Alerts & Modes

This indicator solves the biggest problem with MTF alerts: false signals. You can choose one of two modes:

1. **Intrabar mode** — compares current chart price to the HTF MA. Triggers as soon as price crosses the HTF line; great for early signals but may update until the HTF bar closes.

2. **Confirmed mode** — checks HTF close vs HTF MA. Signals only on the higher-TF bar close; fewer false starts, no intrabar repainting on that TF.

Per-line *Cross Above / Cross Below* conditions are provided for all enabled MAs (e.g., “20W — Cross Above”, “365D — Cross Below”, etc.).

**How to use alerts:** add the script → “Create Alert” → pick any condition from the script’s list.

---

Why this helps

* Keeps Weekly/Daily structure visible while you execute on LTF.

* Classic anchors (e.g., 200D, 20W/100W/200W) are popular for trend bias, dynamic support/resistance, and pullback context.

* Lets you standardize MA references across all your lower-TF playbooks.

---

Notes on confirmation & repainting

* Intrabar signals can change until the higher-TF bar closes (that’s expected with multi-TF data).

* Confirmed mode waits for the HTF close—cleaner, but later. Choose what fits your workflow.

---

Quick setup

1. Pick `MA Type` (SMA/EMA/VWMA/Hull).

2. Enable the HTF lines you want (Weekly 20/100/200; Daily 50/100/200/365; 4H 200).

3. Choose `Alert Mode` (Intrabar vs Confirmed).

4. Style colors/widths to taste and set alerts on the lines you care about.

---

Good practice

* Combine HTF MAs with price action (swings, structure, liquidity grabs) rather than using them in isolation.

* Always validate signals in your execution TF and use a risk plan tailored to volatility.

* Protect your capital: position sizing, stops, and disciplined risk management matter more than any single line on the chart.

---

Disclaimer

For educational/informational purposes only; not financial advice. Trading involves risk—manage it responsibly.

Scissors&Knifes V3.1✂️ The Scissors (PAG Chop V4 Engine)

🧠 Core idea

Scissors measure market compression and breakout readiness.

They use a modified Choppiness Index that looks at the relationship between:

True Range volatility (ATR × period length)

The total high–low range over the same window.

The smaller the ratio (sum of TR vs range), the more directional and impulsive the market is.

The higher the ratio, the more “sideways” the market trades.

This version smooths the result over PAG_SMOOTHLEN bars and applies several color bands that correspond to volatility states.

🎨 Color code meaning

Range State Color Interpretation

≤ 30 Strong Red #8B0000 Momentum exhaustion on downside, sellers dominating — about to reverse or already strong down-trend.

30 – 38 Brick Red #A52A2A Fading downside pressure; often the “bleeding edge” of a bearish climax.

38 – 55 Transparent black (α≈100) Neutral chop zone — indecision, range-building.

55 – 61.8 Yellow (optional) #DAA520 Early compression pocket where volatility starts contracting; the calm before a trend.

61.8 – 70 Bright Green #556B2F Energy release phase: volatility breaking out upward.

≥ 70 Strong Green #355E3B Sustained bullish drive, often continuation leg of a trend.

🪶 Secret nuance:

The transition bands (38–45 and 45–55) are treated as fully transparent to mark “dead zones.”

When PAG Chop sits here, all label activity pauses — the system resets its cluster memory so the next colored print begins a new “cluster”, letting you clearly see where fresh directional momentum starts.

🧩 Cluster logic

Every time a colored (non-transparent) reading appears, it belongs to a “color cluster.”

Grey labels (= count 1) mark the genesis of a new cluster, and following counts 2, 3, 4 … represent the internal continuity of that trend state.

You can optionally hide the first N grey or count 2 labels to reduce clutter on the initial stabilization bars.

✂️ Label meaning

Each label shows:

Emoji ✂️

Current count (e.g. ✂️ = 3 means 3 timeframes are simultaneously firing)

Optional list of the timeframes that contribute.

So a high count (e.g. 8–10) means many lower TFs are synchronizing volatility breakout — a multiframe alignment, often just before an acceleration burst.

🔪 The Knife (Mr Blonde V4 Engine)

🧠 Core idea

Mr Blonde converts the slope of a long EMA into an angle-of-attack metric — literally the “tilt” of market momentum.

It computes the EMA gradient relative to price span and rescales it into degrees (-5 ° to +5 °).

The steeper the angle, the stronger the directional push.

🎨 Color code meaning

Angle range Color Interpretation

≥ +5 ° Transparent (Black 1) Fully over-extended up move — wait for reset.

+3.57 – +5 ° Dark Red Strong upward slope, momentum apex.

+2.14 – +3.57 ° Orange Medium upward slope, trend acceleration zone.

+0.71 – +2.14 ° Light Orange Mild upward bias, pre-momentum phase.

0 to -0.71 ° Yellow Neutral transition.

-0.71 – -2.14 ° Olive Green Soft bearish slope.

-2.14 – -3.57 ° Olive Drab Building bearish momentum.

-3.57 – -5 ° Hunter Green Strong downward angle, aggressive push.

≤ -5 ° Transparent (Black 2) Oversold/over-tilted — likely exhaustion.

🪶 Secret nuance:

Mr Blonde uses a “span normalization” factor that divides EMA slope by the dynamic range of highs and lows.

This lets it compare angles fairly across assets with different volatility profiles (e.g. BTC vs ES) — it’s one of the rare EMA-angle implementations that self-scales properly.

🗡 Label meaning

Emoji 🔪

Count = how many TFs share the same momentum angle bias.

When many TFs show the same slope polarity (e.g. knife = 8), you’re in a deep momentum cascade — a “knife trend.”

💫 Yellow knife

The yellow state marks neutrality or slope flattening.

If you enable yellow visibility (mb_show_yellow), you can see where momentum cools off — often the earliest reversal hint.

⚙️ Shared mechanics between ✂️ and 🔪

Multi-timeframe sweep

The script cycles through 1 m → 10 m by default, running both engines once per TF.

Each returning true adds +1 to the count.

So:

sc_hits = count of timeframes where PAG fires + 1

knife_hits = count of timeframes where MB fires + 1

That “+1 shift” means there’s always at least 1, letting count = 1 represent the local TF itself.

Cluster limiter

If Limit max labels per cluster is on, you cap how many total symbols (both ✂️ & 🔪, including trails) can appear within one color phase — avoiding chart spam during extended trends.

Trails

Each printed label seeds a short-lived “trail” sequence — faded copies extending N bars forward.

Trails visualize the linger effect of the last signal, useful for visually connecting bursts in momentum.

Grey or count = 1 labels can have shorter or longer trails depending on your overrides (*_trail_bars_grey).

They’re purely visual and do not affect alerting.

Alerts

Alerts fire independently of whether you hide labels — unless you enable “respect filters”.

This guarantees you never miss a structural signal even if you suppress visuals for clarity.

🌈 Interpreting Both Together

Scenario Interpretation

✂️ = low (1–2) + 🔪 rising (red/orange) Market just leaving chop, early thrust stage.

✂️ = high (≥ 5) + 🔪 green Fully aligned breakout continuation — trend in progress.

✂️ = yellow cluster + 🔪 yellow Volatility squeeze, energy buildup — next expansion near.

✂️ = green cluster → 🔪 turns red Cross-state conflict; likely transition or correction.

✂️ = grey + 🔪 grey Reset condition — both engines cooling; stand aside.

💡 Hidden edge:

Scissors signal potential, Knife measures kinetic force.

The perfect storm is when ✂️ goes from yellow→green one bar before 🔪 shifts from orange→green — it catches the birth of directional flow while volatility is still tight.

🧭 Reading the labels intuitively

Grey ✂️/🔪 = 1 → embryonic state, may fizzle or bloom.

✂️/🔪 = 2 or 3 → expansion taking hold.

✂️/🔪 ≥ 4 (mid black) → strong synchronized drive across TFs.

Transparent gap → cluster reset; prepare for new phase.

Trail lines → echo of previous cluster strength.

Final secret tip 🗝

Because both engines are mathematically uncorrelated (volatility vs EMA angle), when they agree in color polarity on multiple TFs, you have one of the cleanest probabilistic trend windows possible.

If you ever see ✂️ = 6 + 🔪 = 6 both pointing the same way — that’s a “knife-through-the-scissors” moment: volatility expansion and directional slope synchronized — those are the bars where institutional algorithms tend to add size.

VWAP Composites📊 VWAP Composite - Advanced Multi-Period Volume Weighted Average Price Indicator

═══════════════════════════════════════════════════════════════════

🎯 OVERVIEW

VWAP Composite is an advanced volume-weighted average price (VWAP) indicator that goes beyond traditional single-period VWAP calculations by offering composite multi-period analysis and unprecedented customization. This indicator solves a common problem traders face: traditional VWAP resets at arbitrary intervals (session start, day, week), but significant price action and volume accumulation often spans multiple periods. VWAP Composite allows you to anchor VWAP calculations to any timeframe—or combine multiple periods into a single composite VWAP—giving you a true representation of average price weighted by volume across the exact periods that matter to your analysis.

═══════════════════════════════════════════════════════════════════

⚙️ HOW IT WORKS - CALCULATION METHODOLOGY

📌 CORE VWAP CALCULATION

The indicator calculates VWAP using the standard volume-weighted formula:

• Typical Price = (High + Low + Close) / 3

• VWAP = Σ(Typical Price × Volume) / Σ(Volume)

This calculation is performed across user-defined time periods, ensuring each bar's contribution to the average is proportional to its trading volume.

📌 STANDARD DEVIATION BANDS

The indicator calculates volume-weighted standard deviation to measure price dispersion around the VWAP:

• Variance = Σ / Σ(Volume)

• Standard Deviation = √Variance

• Upper Band = VWAP + (StdDev × Multiplier)

• Lower Band = VWAP - (StdDev × Multiplier)

These bands help identify overbought/oversold conditions relative to the volume-weighted mean, with high-volume price excursions having greater impact on band width than low-volume moves.

📌 COMPOSITE PERIOD METHODOLOGY (Auto Mode)

Unlike traditional VWAP that resets at fixed intervals, Auto Mode creates composite VWAPs by combining the current period with N previous periods:

• Period Span = 1: Current period only (standard VWAP behavior)

• Period Span = 2: Current period + 1 previous period combined

• Period Span = 3: Current period + 2 previous periods combined

• And so on...

Example: A 3-period Weekly composite VWAP calculates from the start of 2 weeks ago through the current week's end, creating a single VWAP that represents 21 days of continuous price and volume data. This provides context about where price stands relative to the volume-weighted average over multiple weeks, not just the current week.

═══════════════════════════════════════════════════════════════════

🔧 KEY FEATURES & ORIGINALITY

✅ DUAL OPERATING MODES

1️⃣ MANUAL MODE (5 Independent VWAPs)

Define up to 5 separate VWAP calculations with custom start/end times:

• Perfect for anchoring VWAP to specific events (earnings, Fed announcements, major reversals)

• Each VWAP has independent color settings for lines and deviation band backgrounds

• Individual control over calculation extension and visual extension (explained below)

• Useful for tracking multiple institutional accumulation/distribution zones simultaneously

2️⃣ AUTO MODE (Composite Period VWAP)

Automatically calculates VWAP across combined time periods:

• Supported periods: Daily, Weekly, Monthly, Quarterly, Yearly

• Configurable period span (1-20 periods)

• Always up-to-date, recalculates on each new bar

• Ideal for systematic analysis across consistent timeframes

✅ DUAL EXTENSION SYSTEM (Manual Mode Innovation)

Most VWAP indicators only offer "on/off" for extending calculations. This indicator provides two distinct extension options:

🔹 EXTEND CALCULATION TO CURRENT BAR

When enabled, continues including new bars in the VWAP calculation after the defined end time. The VWAP value updates dynamically as new volume enters the market.

Use case: You anchored VWAP to a major low 3 weeks ago. You want the VWAP to continue evolving with new volume data to track ongoing institutional positioning.

🔹 EXTEND VISUAL LINE ONLY

When enabled (and calculation extension is disabled), projects the "frozen" VWAP value forward as a reference line. The VWAP value remains fixed at what it was at the end time, but the line and deviation bands visually extend to current price.

Use case: You want to see how price is behaving relative to the VWAP that existed at a specific point in time (e.g., "Where is price now vs. the 5-day VWAP that existed at last Friday's close?").

This dual system gives you unprecedented control over whether you're tracking a "living" VWAP that incorporates new data or using historical VWAP levels as static reference points.

✅ CUSTOMIZABLE STANDARD DEVIATION BANDS

• Adjustable multiplier (0.1 to 5.0)

• Independent background colors with opacity control for each VWAP

• Dashed band lines for easy visual distinction from main VWAP

• Bands extend when visual extension is enabled, maintaining zone visibility

✅ COMPREHENSIVE LABELING SYSTEM

Each VWAP displays:

• Current VWAP value

• Upper deviation band value (High)

• Lower deviation band value (Low)

• Extension status indicator (Calc Extended / Visual Extended)

• Color-coded for quick identification

═══════════════════════════════════════════════════════════════════

📖 HOW TO USE THIS INDICATOR

🎯 SCENARIO 1: EVENT-ANCHORED VWAP (Manual Mode)

Use case: A stock gaps down 15% on earnings and you want to track where institutions are positioning during the recovery.

Setup:

1. Switch to Manual Mode

2. Enable VWAP 1

3. Set Start Time to the earnings gap bar

4. Set End Time to current time (or leave far in future)

5. Enable "Extend Calculation to Current Bar"

6. Watch how price respects the VWAP as a dynamic support/resistance

Interpretation:

• Price above VWAP = buyers in control since the event

• Price testing VWAP from above = potential support

• Volume-weighted standard deviation bands show normal price range

• Price outside bands = potential exhaustion/mean reversion setup

🎯 SCENARIO 2: MULTI-WEEK INSTITUTIONAL ACCUMULATION ZONE (Auto Mode)

Use case: You trade swing setups and want to identify where institutions have been accumulating over the past 3 weeks.

Setup:

1. Switch to Auto Mode

2. Select "Weekly" period type

3. Set Period Span to 3

4. Enable standard deviation bands

Interpretation:

• 3-week composite VWAP shows the true average institutional entry

• Price bouncing off VWAP repeatedly = strong support (institutions defending their average)

• Price breaking below VWAP on high volume = potential distribution

• Deviation bands contracting = consolidation; expanding = volatility increase

🎯 SCENARIO 3: COMPARING MULTIPLE TIME HORIZONS (Manual Mode)

Use case: You want to see short-term vs medium-term vs long-term VWAP alignments.

Setup:

1. Switch to Manual Mode

2. VWAP 1: Last 5 trading days (blue)

3. VWAP 2: Last 10 trading days (orange)

4. VWAP 3: Last 20 trading days (purple)

5. Enable "Extend Calculation" for all

6. Set different background colors for visual separation

Interpretation:

• All VWAPs aligned upward = strong trend across all timeframes

• Price between VWAPs = finding equilibrium between different trader timeframes

• Short-term VWAP crossing long-term VWAP = momentum shift

• Price rejecting at higher-timeframe VWAP = that timeframe's traders defending their average

🎯 SCENARIO 4: HISTORICAL VWAP REFERENCE LEVELS (Manual Mode)

Use case: You want to see where the 1-month VWAP was at each month-end as static reference levels.

Setup:

1. Switch to Manual Mode

2. VWAP 1: Set to last month's start/end dates

3. VWAP 2: Set to 2 months ago start/end dates

4. VWAP 3: Set to 3 months ago start/end dates

5. Disable "Extend Calculation"

6. Enable "Extend Visual Line Only"

Interpretation:

• Each VWAP represents the volume-weighted average for that complete month

• These become static support/resistance levels

• Price returning to old monthly VWAPs = institutional memory/gap fill behavior

• Useful for identifying longer-term value areas

═══════════════════════════════════════════════════════════════════

🎨 CUSTOMIZATION OPTIONS

GENERAL SETTINGS

• Show/hide labels

• Line style: Solid, Dashed, or Dotted

• Standard deviation multiplier (impacts band width)

• Toggle standard deviation bands on/off

MANUAL MODE (Per VWAP)

• Custom start and end times

• Line color picker

• Background color picker (with transparency control)

• Extend calculation option

• Extend visual option

• Show/hide individual VWAPs

AUTO MODE

• Period type selection (Daily/Weekly/Monthly/Quarterly/Yearly)

• Period span (1-20 periods)

• Line color

• Background color (with transparency control)

═══════════════════════════════════════════════════════════════════

💡 TRADING APPLICATIONS

✓ Mean Reversion: Use deviation bands to identify stretched prices likely to return to VWAP

✓ Trend Confirmation: Price sustained above VWAP = bullish bias; below = bearish bias

✓ Support/Resistance: VWAP often acts as dynamic S/R, especially on higher volume periods

✓ Institutional Positioning: Multi-day/week VWAPs show where large players have established positions

✓ Entry Timing: Wait for pullbacks to VWAP in trending markets

✓ Stop Placement: Use VWAP ± standard deviation as volatility-adjusted stop levels

✓ Breakout Confirmation: Breakouts from consolidation with price reclaiming VWAP = stronger signal

✓ Multi-Timeframe Analysis: Compare short vs long-period VWAPs to gauge momentum alignment

═══════════════════════════════════════════════════════════════════

⚠️ IMPORTANT NOTES

• The indicator redraws on each bar to maintain accurate visual representation (uses `barstate.islast`)

• Maximum lookback is limited to 5000 bars for performance optimization

• Time range calculations work across all timeframes but are most effective on intraday to daily charts

• Standard deviation bands assume volume-weighted distribution; extreme events may violate assumptions

• Auto mode always calculates to current bar; use Manual mode for fixed historical periods

═══════════════════════════════════════════════════════════════════

This indicator is open-source. Feel free to examine the code, learn from it, and adapt it to your needs.

ICT HTF Volume Candles (Based on HTF Candles by Fadi)# ICT HTF Volume Candles - Multi-Timeframe Volume Analysis

## Overview

This indicator provides multi-timeframe volume visualization designed to complement price action analysis. It displays volume data from up to 6 higher timeframes simultaneously in a separate panel, allowing traders to identify volume spikes, divergences, and institutional activity without switching between timeframes.

**Original Concept Credits:** This indicator builds upon the HTF Candles framework by Fadi, adapting it specifically for volume analysis with enhanced features including gap-filling for extended hours, multiple scaling methods, and advanced synchronization.

## What Makes This Script Original

### Key Innovations:

1. **Three Volume Scaling Methods:**

- **Per-HTF Auto Scale:** Each timeframe scales independently for detailed comparison

- **Global Auto Scale:** All timeframes use unified scale for relative volume comparison

- **Manual Scale:** User-defined maximum for consistent analysis across sessions

2. **Bullish/Bearish Volume Differentiation:**

- Volume bars colored based on price movement (close vs open)

- Separate styling for bullish (green) and bearish (red) volume periods

- Helps identify whether volume supports price direction

3. **Advanced Time Synchronization:**

- Custom daily candle open times (Midnight, 8:30 AM, 9:30 AM ET)

- Timezone-aware calculations for New York trading hours

- Real-time countdown timers for each timeframe

- **Gap-filling technology** for continuous display during extended hours and weekends

4. **Flexible Display Options:**

- Configurable spacing and positioning

- Label placement (top, bottom, or both)

- Day-of-week or time interval labels on candles

- Works reliably in backtesting and live trading

## How It Works

### Volume Calculation

The indicator uses `request.security()` with optimized parameters to fetch volume data from higher timeframes:

- **Volume Open/High/Low/Close (OHLC):** Tracks volume changes within each HTF candle

- **Color Logic:** Compares HTF close vs open prices to determine bullish/bearish classification

- **Alignment:** All volume bars share a common baseline for easy visual comparison

- **Gap Handling:** Uses `gaps=barmerge.gaps_off` to maintain continuity during non-trading hours

### Technical Implementation

```

1. Monitors HTF timeframe changes using request.security() with lookahead

2. Creates new VolumeCandle object when HTF bar opens

3. Updates current candle's volume H/L/C on each chart bar

4. Applies selected scaling method to normalize display height

5. Repositions all candles and labels on each bar update

6. Fills gaps automatically during extended hours for consistent display

```

### Scaling Methods Explained

**Method 1 - Auto Scale per HTF:**

Each timeframe displays volume relative to its own maximum. Best for identifying patterns within each individual timeframe.

**Method 2 - Global Auto Scale:**

All timeframes share the same scale based on the highest volume across all HTFs. Best for comparing relative volume strength between timeframes.

**Method 3 - Manual Scale:**

User sets maximum volume value. Best for maintaining consistent scale across different trading sessions or instruments.

## How to Use This Indicator

### Setup

1. Add indicator to your chart (it appears in a separate panel below price)

2. Configure up to 6 higher timeframes (default: 5m, 15m, 1H, 4H, 1D, 1W)

3. Set number of candles to display for each timeframe

4. Choose volume scaling method based on your analysis needs

5. Enable "Fix gaps in non-trading hours" for extended hours trading (enabled by default)

### Interpretation

**Volume Spikes:**

- Sudden increase in volume height indicates institutional activity or strong conviction

- Compare volume between timeframes to identify where the real money is moving

- Look for volume spikes that appear across multiple timeframes simultaneously

**Bullish vs Bearish Volume:**

- **Green volume bars:** Price closed higher (buying pressure)

- **Red volume bars:** Price closed lower (selling pressure)

- High green volume during uptrend = confirmation of strength

- High red volume during downtrend = confirmation of weakness

- High volume opposite to trend = potential reversal warning

**Multi-Timeframe Context:**

- **5m/15m:** Scalping and day trading activity

- **1H/4H:** Swing trading and intraday institutional flows

- **Daily/Weekly:** Major position building and long-term trends

**Divergences:**

- Price making new highs but volume declining = weakening trend

- Volume increasing while price consolidates = potential breakout brewing

- Price breaks level but volume doesn't confirm = likely false breakout

### Practical Examples

**Example 1 - Institutional Confirmation:**

Price breaks above resistance. Check volume across timeframes:

- 5m shows spike = retail interest

- 15m + 1H + 4H all show spikes = institutional confirmation

- **Trade confidence: HIGH**

**Example 2 - False Breakout Detection:**

Price breaks resistance with:

- High volume on 5m only

- Normal/low volume on 1H and 4H

- **Interpretation:** Likely retail trap, institutions not participating

- **Action:** Wait for pullback or avoid

**Example 3 - Accumulation Phase:**

Price ranges sideways but:

- Daily volume gradually increasing

- Weekly volume above average

- **Interpretation:** Smart money accumulating

- **Action:** Prepare for breakout in direction of volume

**Example 4 - Volume Divergence:**

Price makes new high:

- Current high has lower volume than previous high across all timeframes

- **Interpretation:** Weakening momentum

- **Action:** Consider profit-taking or reversal trade

## Configuration Parameters

### Timeframe Settings

- **HTF 1-6:** Select timeframes (must be higher than chart timeframe)

- **Max Display:** Number of candles to show per timeframe (1-50)

- **Limit to Next HTFs:** Display only first N enabled timeframes (1-6)

### Styling

- **Bull/Bear Colors:** Separate colors for body, border, and wick

- **Padding from current candles:** Distance offset from live price action

- **Space between candles:** Gap between individual volume bars

- **Space between Higher Timeframes:** Gap between different timeframe groups

- **Candle Width:** Thickness of volume bars (1-4, multiplied by 2)

### Volume Settings

- **Volume Scale Method:** Choose 1, 2, or 3

- 1 = Auto Scale per HTF (each TF independent)

- 2 = Global Auto Scale (all TF unified)

- 3 = Manual Scale (user-defined max)

- **Auto Scale Volume:** Enable/disable automatic scaling

- **Manual Scale Max Volume:** Set maximum when using Method 3

### Label Settings

- **HTF Label:** Show/hide timeframe names with color and size options

- **Label Positions:** Display at Top, Bottom, or Both

- **Label Alignment:** Align centered or Follow Candles

- **Remaining Time:** Show countdown timer until next HTF candle

- **Interval Value:** Display day-of-week or time on each candle

### Custom Daily Candle

- **Enable Custom Daily:** Override default daily candle timing

- **Open Time Options:**

- **Midnight:** Standard 00:00 ET daily open

- **8:30 AM:** Align with economic data releases

- **9:30 AM:** Align with NYSE market open

- Useful for specific trading strategies or market alignment

### Advanced Settings

- **Fix gaps in non-trading hours:** Maintains alignment during extended hours and weekends (recommended: ON)

- Prevents visual gaps during forex weekend closures

- Ensures consistent display during crypto 24/7 trading

- Improves backtesting reliability

## Best Practices

1. **Pair with Price Action:** Use alongside HTF price candles indicator for complete picture

2. **Start Simple:** Enable 2-3 timeframes initially (e.g., 15m, 1H, 4H), add more as needed

3. **Match Settings:** Use same candle width/spacing as companion price indicator for visual alignment

4. **Scale Appropriately:**

- Use **Global scale** (Method 2) when comparing timeframes

- Use **Per-HTF scale** (Method 1) for pattern analysis within each timeframe

- Use **Manual scale** (Method 3) for consistent day-to-day comparison

5. **Watch for Volume Clusters:** High volume appearing simultaneously across multiple HTFs signals significant market events

6. **Confirm Breakouts:** Always check if volume supports the price movement across higher timeframes

7. **Extended Hours:** Keep "Fix gaps" enabled for 24/7 markets (Forex, Crypto) and weekend analysis

## Technical Notes

- **Timezone:** All calculations use America/New_York timezone for consistency

- **Real-time Updates:** Volume and timers update on each tick during market hours

- **Performance:** Optimized with max_bars_back=5000 for extensive historical analysis

- **Compatibility:** Works on all instruments with volume data (Stocks, Forex, Crypto, Futures)

- **Gap Handling:** Uses `barmerge.gaps_off` to fill data gaps during non-trading periods

- **Backtesting:** Uses `lookahead=barmerge.lookahead_on` for stable historical data without repainting

- **Data Continuity:** Automatically handles market closures, weekends, and extended hours

## Updates & Improvements

**Version 2.0 (Current):**

- ✅ Fixed alignment issues during extended hours and weekends

- ✅ Eliminated repainting in backtesting

- ✅ Added gap-filling technology for continuous display

- ✅ Improved data synchronization across all timeframes

- ✅ Enhanced NA value handling for data integrity

- ✅ Added advanced settings group for user control

## Support

For questions, suggestions, or feedback, please comment on the publication or message the author.

---

**Disclaimer:** This indicator is for educational and informational purposes only. It does not constitute financial advice. Past performance is not indicative of future results. Always perform your own analysis and implement proper risk management before making trading decisions.

Adaptive Trend Breaks Adaptive Trend Breaks

## WHAT IT DOES

This script is a modified and enhanced version of "Trendline Breakouts With Targets" concept by ChartPrime.

Adaptive Trend Breaks (ATB) is a trendline breakout system optimized for scalping liquid futures contracts. The indicator automatically draws dynamic support and resistance trendlines based on pivot points, then generates trade signals when price breaks through these levels with confirmation filters. It includes automated target and stop-loss placement with real-time P&L tracking in dollars.

## HOW IT WORKS

**Trendline Detection Method:**

The indicator uses pivot high/low detection to identify significant price turning points. When a new pivot forms, it calculates the slope between consecutive pivots to draw dynamic trendlines. These lines extend forward based on the established trend angle, creating actionable support and resistance zones.

**Band System:**

Around each trendline, the script creates a "band" using a volatility-adjusted calculation: `ATR(14) * 0.2 * bandwidth multiplier / 2`. This adaptive band accounts for current market conditions - wider during volatile periods, tighter during quiet markets.

**Breakout Logic:**

A breakout signal triggers when:

1. Price closes beyond the trendline + band zone

2. Volume exceeds the 20-period moving average by your set multiplier (default 1.2x)

3. Price is within Regular Trading Hours (9:30-16:00 EST) if session filter enabled

4. Current ATR meets minimum volatility threshold (prevents trading dead markets)

**Target & Stop Calculation:**

Upon breakout confirmation:

- **Entry**: Trendline breach point

- **Target**: Entry ± (bandwidth × target multiplier) - default 8x for quick scalps

- **Stop**: Entry ± (bandwidth × stop multiplier) - default 8x for 1:1 risk/reward

- Multipliers adjust automatically to market volatility through the ATR-based band

**P&L Conversion:**

The script converts point movements to dollars using:

```

Dollar P&L = (Price Points × Contract Point Value × Quantity)

```

For example, a 10-point NQ move with 2 contracts = 10 × $20 × 2 = $400

## HOW TO USE IT

**Setup:**

1. Select your instrument (NQ/ES/YM/RTY) - point values auto-configure

2. Set contract quantity for accurate dollar P&L

3. Choose pivot period (lower = more signals but more noise, default 5 for scalping)

4. Adjust bandwidth multiplier if trendlines are too tight/loose (1-5 range)

**Filters Configuration:**

- **Volume Filter**: Requires breakout volume > moving average × multiplier. Increase multiplier (1.5-2.0) for higher conviction trades

- **Session Filter**: Enable to trade only RTH. Disable for 24-hour trading

- **ATR Filter**: Prevents signals during low volatility. Increase minimum % for more active markets only

**Risk Management:**

- Set target/stop multipliers based on your risk tolerance

- 8x bandwidth = approximately 1:1 risk/reward for most liquid futures

- Enable trailing stops for trend-following approach (moves stop to protect profits)

- Adjust line length to see targets further into the future

**Statistics Table:**

- Choose timeframe to analyze: all-time, today, this week, custom days

- Monitor win rate, profit factor, and net P&L in dollars

- Track long vs short performance separately

- See real-time unrealized P&L on active trades

**Reading Signals:**

- **Green triangle below bar** = Long breakout (resistance broken)

- **Red triangle above bar** = Short breakout (support broken)

- **White dashed line** = Entry price

- **Orange line** = Take profit target with dollar value

- **Red line** = Stop loss with dollar value

- **Green checkmark (✓)** = Target hit, winning trade

- **Red X (✗)** = Stop hit, losing trade

## WHAT IT DOES NOT DO

**Limitations to Understand:**

- Does not predict future trendline formations - it reacts to breakouts after they occur

- Historical trendlines disappear after breakout (not kept on chart for clarity)

- Requires sufficient volatility - may not signal in extremely quiet markets

- Volume filter requires exchange volume data (not available on all symbols)

- Statistics are indicator-based simulations, not actual trading results

- Does not account for slippage, commissions, or order fills

## BEST PRACTICES

**Recommended Settings by Market:**

- **NQ (Nasdaq)**: Default settings work well, consider volume multiplier 1.3-1.5

- **ES (S&P 500)**: Slightly slower, try period 7-8, volume 1.2

- **YM (Dow)**: Lower volatility, reduce bandwidth to 1.5-2

- **RTY (Russell)**: Higher volatility, increase bandwidth to 3-4

**Risk Management:**

- Never risk more than 2-3% of account per trade

- Use contract quantity calculator: Max Risk $ ÷ (Stop Distance × Point Value)

- Start with 1 contract while learning the system

- Backtest your specific timeframe and instrument before live trading

**Optimization Tips:**

- Increase pivot period (7-10) for fewer but higher-quality signals

- Raise volume multiplier (1.5-2.0) in choppy markets

- Lower target/stop multipliers (5-6x) for tighter profit taking

- Use trailing stops in strong trending conditions

- Disable session filter for overnight gaps and Asia session moves

## TECHNICAL DETAILS

**Key Calculations:**

- Pivot Detection: `ta.pivothigh(high, period, period/2)` and `ta.pivotlow(low, period, period/2)`

- Slope Calculation: `(newPivot - oldPivot) / (newTime - oldTime)`

- Adaptive Band: `min(ATR(14) * 0.2, close * 0.002) * multiplier / 2`

- Breakout Confirmation: Price crosses trendline + 10% of band threshold

**Data Requirements:**

- Minimum bars in view: 500 for proper pivot calculation

- Volume data required for volume filter accuracy

- Intraday timeframes recommended (1min - 15min) for scalping

- Works on any timeframe but optimized for fast execution

**Performance Metrics:**

All statistics calculate based on indicator signals:

- Tracks every signal as a trade from entry to TP/SL

- P&L in actual contract dollar values

- Win rate = (Winning trades / Total trades) × 100

- Profit factor = Gross profit / Gross loss

- Separates long/short performance for bias analysis

## IDEAL FOR

- Futures scalpers and day traders

- Traders who prefer visual trendline breakouts

- Those wanting automated TP/SL placement

- Traders tracking performance in dollar terms

- Multiple timeframe analysis (compare 1min vs 5min signals)

## NOT SUITABLE FOR

- Swing trading (targets too close)

- Stocks/forex without modifying point values

- Extremely low timeframes (<30 seconds) - too much noise

- Markets without volume data if using volume filter

- Illiquid contracts (signals may not execute at shown prices)

---

**Settings Summary:**

- Core: Period, bandwidth, extension, trendline style

- Filters: Volume, RTH session, ATR volatility

- Risk: R:R ratio, target/stop multipliers, trailing stop

- Display: Stats table position, size, colors

- Stats: Timeframe selection (all-time to custom days)

**License:** This indicator is published open-source under Mozilla Public License 2.0. You may use and modify the code with proper attribution.

**Disclaimer:** This indicator is for educational purposes. Past performance does not guarantee future results. Always practice proper risk management and test thoroughly before live trading.

---

## CREDITS & ATTRIBUTION

This script builds upon the "Trendline Breakouts With Targets" concept by ChartPrime with significant enhancements:

**Major Improvements Added:**

- **Futures-Specific Calculations**: Automated dollar P&L conversion using actual contract point values (NQ=$20, ES=$50, YM=$5, RTY=$50)

- **Advanced Statistics Engine**: Comprehensive performance tracking with customizable timeframe analysis (today, week, month, custom ranges)

- **Multi-Layer Filtering System**: Volume confirmation, RTH session filter, and ATR volatility filter to reduce false signals

- **Professional Trade Management**: Enhanced visual trade tracking with separate TP/SL lines, dollar value labels, and optional trailing stops

- **Optimized for Scalping**: Faster pivot periods (5 vs 10), tighter bands, and reduced extension bars for quick entries

Original trendline detection methodology by ChartPrime - used with modification under Mozilla Public License 2.0.

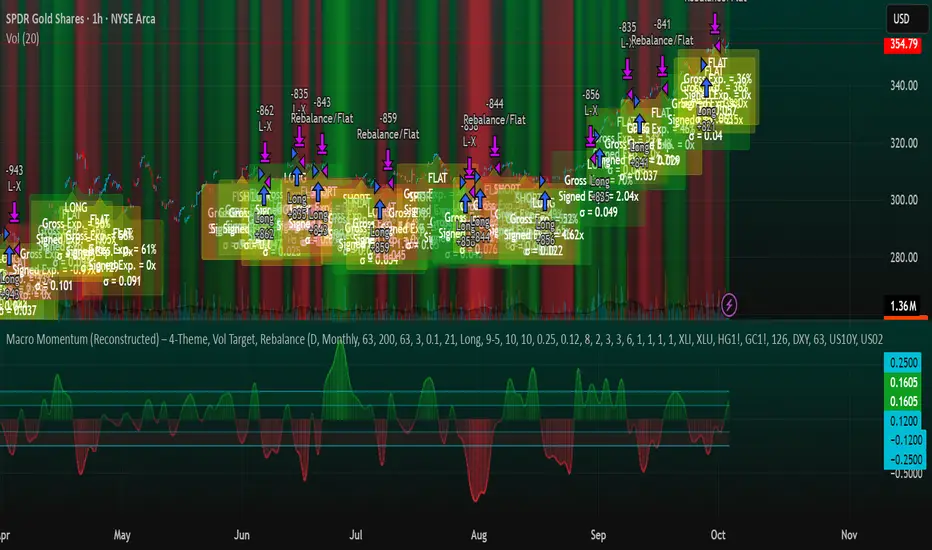

Macro Momentum – 4-Theme, Vol Target, RebalanceMacro Momentum — 4-Theme, Vol Target, Rebalance

Purpose. A macro-aware strategy that blends four economic “themes”—Business Cycle, Trade/USD, Monetary Policy, and Risk Sentiment—into a single, smoothed Composite signal. It then:

gates entries/exits with hysteresis bands,

enforces optional regime filters (200-day bias), and

sizes the position via volatility targeting with caps for long/short exposure.

It’s designed to run on any chart (index, ETF, futures, single stocks) while reading external macro proxies on a chosen Signal Timeframe.

How it works (high level)

Build four theme signals from robust macro proxies:

Business Cycle: XLI/XLU and Copper/Gold momentum, confirmed by the chart’s price vs a long SMA (default 200D).

Trade / USD: DXY momentum (sign-flipped so a rising USD is bearish for risk assets).

Monetary Policy: 10Y–2Y curve slope momentum and 10Y yield trend (steepening & falling 10Y = risk-on; rising 10Y = risk-off).

Risk Sentiment: VIX momentum (bearish if higher) and HYG/IEF momentum (bullish if credit outperforms duration).

Normalize & de-noise.

Optional Winsorization (MAD or stdev) clamps outliers over a lookback window.

Optional Z-score → tanh mapping compresses to ~ for stable weighting.

Theme lines are SMA-smoothed; the final Composite is LSMA-smoothed (linreg).

Decide direction with hysteresis.

Enter/hold long when Composite ≥ Entry Band; enter/hold short when Composite ≤ −Entry Band.

Exit bands are tighter than entry bands to avoid whipsaws.

Apply regime & direction constraints.

Optional Long-only above 200MA (chart symbol) and/or Short-only below 200MA.

Global Direction control (Long / Short / Both) and Invert switch.

Size via volatility targeting.

Realized close-to-close vol is annualized (choose 9-5 or 24/7 market profile).

Target exposure = TargetVol / RealizedVol, capped by Max Long/Max Short multipliers.

Quantity is computed from equity; futures are rounded to whole contracts.

Rebalance cadence & execution.

Trades are placed on Weekly / Monthly / Quarterly rebalance bars or when the sign of exposure flips.

Optional ATR stop/TP for single-stock style risk management.

Inputs you’ll actually tweak

General

Signal Timeframe: Where macro is sampled (e.g., D/W).

Rebalance Frequency: Weekly / Monthly / Quarterly.

ROC & SMA lengths: Defaults for theme momentum and the 200D regime filter.

Normalization: Z-score (tanh) on/off.

Winsorization

Toggle, lookback, multiplier, MAD vs Stdev.

Risk / Sizing

Target Annualized Vol & Realized Vol Lookback.

Direction (Long/Short/Both) and Invert.

Max long/short exposure caps.

Advanced Thresholds

Theme/Composite smoothing lengths.

Entry/Exit bands (hysteresis).

Regime / Execution

Long-only above 200MA, Short-only below 200MA.

Stops/TP (optional)

ATR length and SL/TP multiples.

Theme Weights

Per-theme scalars so you can push/pull emphasis (e.g., overweight Policy during rate cycles).

Macro Proxies

Symbols for each theme (XLI, XLU, HG1!, GC1!, DXY, US10Y, US02Y, VIX, HYG, IEF). Swap to alternatives as needed (e.g., UUP for DXY).

Signals & logic (under the hood)

Business Cycle = ½ ROC(XLI/XLU) + ½ ROC(Copper/Gold), then confirmed by (price > 200SMA ? +1 : −1).

Trade / USD = −ROC(DXY).

Monetary Policy = 0.6·ROC(10Y–2Y) − 0.4·ROC(10Y).

Risk Sentiment = −0.6·ROC(VIX) + 0.4·ROC(HYG/IEF).

Each theme → (optional Winsor) → (robust z or scaled ROC) → tanh → SMA smoothing.

Composite = weighted average → LSMA smoothing → compare to bands → dir ∈ {−1,0,+1}.

Rebalance & flips. Orders fire on your chosen cadence or when the sign of exposure changes.

Position size. exposure = clamp(TargetVol / realizedVol, maxLong/Short) × dir.

Note: The script also exposes Gross Exposure (% equity) and Signed Exposure (× equity) as diagnostics. These can help you audit how vol-targeting and caps translate into sizing over time.

Visuals & alerts

Composite line + columns (color/intensity reflect direction & strength).

Entry/Exit bands with green/red fills for quick polarity reads.

Hidden plots for each Theme if you want to show them.

Optional rebalance labels (direction, gross & signed exposure, σ).

Background heatmap keyed to Composite.

Alerts

Enter/Inc LONG when Composite crosses up (and on rebalance bars).

Enter/Inc SHORT when Composite crosses down (and on rebalance bars).

Exit to FLAT when Composite returns toward neutral (and on rebalance bars).

Practical tips

Start higher timeframes. Daily signals with Monthly rebalance are a good baseline; weekly signals with quarterly rebalances are even cleaner.

Tune Entry/Exit bands before anything else. Wider bands = fewer trades and less noise.

Weights reflect regime. If policy dominates markets, raise Monetary Policy weight; if credit stress drives moves, raise Risk Sentiment.

Proxies are swappable. Use UUP for USD, or futures-continuous symbols that match your data plan.

Futures vs ETFs. Quantity auto-rounds for futures; ETFs accept fractional shares. Check contract multipliers when interpreting exposure.

Caveats

Macro proxies can repaint at the selected signal timeframe as higher-TF bars form; that’s intentional for macro sampling, but test live.

Vol targeting assumes reasonably stationary realized vol over the lookback; if markets regime-shift, revisit volLook and targetVol.

If you disable normalization/winsorization, themes can become spikier; expect more hysteresis band crossings.

What to change first (quick start)

Set Signal Timeframe = D, Rebalance = Monthly, Z-score on, Winsor on (MAD).

Entry/Exit bands: 0.25 / 0.12 (defaults), then nudge until trade count and turnover feel right.

TargetVol: try 10% for diversified indices; lower for single stocks, higher for vol-sell strategies.

Leave weights = 1.0 until you’ve inspected the four theme lines; then tilt deliberately.

Intraday Rising & Reversal ScannerPine Script Description: Intraday Rising & Reversal ScannerThis Pine Script is a TradingView indicator designed to identify stocks with intraday (1-hour timeframe) potential for bullish (rising) or bearish (reversal) movements. It scans for stocks based on user-defined technical criteria, including price change, relative volume, RSI, EMA, ATR, and VWAP. The script plots signals on the chart, displays a summary table, and triggers alerts when conditions are met.FeaturesBullish Signal (Rising Stocks):1H Price Change: > 1% (configurable, e.g., >2% for volatile markets).

Relative Volume: > 2.0 (volume is at least twice the 20-period average).

RSI (14): Between 50 and 70 (strong but not overbought momentum).

Price vs EMA 13: Price above the 13-period EMA (confirms short-term uptrend).

ATR (14): Current ATR above its 20-period average (indicates volatility).

VWAP: Price above VWAP (optional, shown on chart for manual confirmation).

Bearish Signal (Reversal Stocks):1H Price Change: < -1% (configurable, e.g., <-2% for stronger reversals).

Relative Volume: > 2.0 (high volume confirms selling pressure).

RSI (14): > 70 (overbought, increasing reversal likelihood).

Price vs EMA 13: Price below the 13-period EMA (confirms short-term downtrend).

ATR (14): Current ATR above its 20-period average (indicates volatility).

VWAP: Price below VWAP (optional, shown on chart for manual confirmation).

Visualization:Bullish Signal: Green triangle below the bar.

Bearish Signal: Red triangle above the bar.

VWAP: Plotted as a blue line for manual verification.

Table: Displays real-time metrics (Change %, Relative Volume, RSI, Price vs EMA, ATR, VWAP) in the top-right corner, color-coded (green for bullish, red for bearish).

Alerts:Separate alerts for bullish ("Intraday Bullish Signal") and bearish ("Intraday Bearish Signal") conditions.

Customizable alert messages include parameter values for easy tracking.

How It WorksThe script runs on the 1-hour (1H) timeframe, ensuring all calculations are based on hourly data.

Indicators are computed:Change %: Percentage price change over the last hour.

Relative Volume: Current volume divided by the 20-period SMA of volume.

RSI: 14-period Relative Strength Index.

EMA 13: 13-period Exponential Moving Average.

ATR: 14-period Average True Range, compared to its 20-period SMA.

VWAP: Volume Weighted Average Price, plotted for visual confirmation.

Signals are generated when all conditions for either bullish or bearish criteria are met.

A table summarizes key metrics, and alerts can be set up for real-time notifications.

Usage InstructionsApply the Script:Open TradingView’s Pine Editor.

Copy and paste the script.

Click "Add to Chart" and set the chart to the 1-hour (1H) timeframe.

Set Up Alerts:Right-click on the chart > "Add Alert".

Select "Intraday Bullish Signal" or "Intraday Bearish Signal" as the condition.

Configure notifications (e.g., SMS, email, or TradingView alerts).

Manual VWAP Check:VWAP is plotted as a blue line. Verify that the price is above VWAP for bullish signals or below for bearish signals using the table or chart.

To make VWAP a mandatory filter, uncomment the VWAP conditions in the bull_signal and bear_signal definitions.

CMC Macro Regime PanelOverview (what it is):

A macro‑regime gate built entirely from TradingView-native symbols (CRYPTOCAP, FRED, DXY/VIX, HYG/LQD). It aggregates central‑bank liquidity (Fed balance sheet − RRP − Treasury General Account), USD strength, credit conditions, stablecoin flows/dominance, tech beta and BTC–NDX co‑move into one normalized score (CLRC). The panel outputs Risk‑ON/OFF regimes, an Early 3/5 pre‑signal, and an automatic BTC vs ETH vs ALTs preference. It is intentionally scoped to Daily & Weekly reads (no intraday timing). Publish with a clean chart and a clear description as per TradingView rules.

TradingView

Why we also use other TradingView screens (and why that is compliant)

This script pulls data via request.security() from official TV symbols only; users often want to open the raw series on separate charts to sanity‑check:

CRYPTOCAP indices: TOTAL, TOTAL2, TOTAL3 (market cap aggregates) and dominance tickers like BTC.D, USDT.D. Helpful for regime & rotation (ALTs vs BTC). TradingView provides definitions for crypto market cap and dominance symbols.

TradingView

+3

TradingView

+3

TradingView

+3

FRED releases: WALCL (Fed assets, weekly), RRPONTSYD (ON RRP, daily), WTREGEN (TGA, weekly), M2SL (M2, monthly). These are the official macro sources exposed on TV.

FRED

+3

FRED

+3

FRED

+3

Risk proxies: TVC:DXY (USD index), TVC:VIX (implied vol), AMEX:HYG/AMEX:LQD (credit), NASDAQ:NDX (tech beta), BINANCE:ETHBTC. VIX/NDX relationship is well-documented; VIX measures 30‑day expected S&P500 vol.

TradingView

+2

TradingView

+2

Compliance note: Using multiple screens is optional for users, but it explains/justifies how components work together (a requirement for public scripts). Keep publication chart clean; use extra screens only to illustrate in the description.

TradingView

How it works (high level)

Liquidity block (Weekly/Monthly)

Net Liquidity = WALCL − RRPONTSYD − WTREGEN (YoY z‑score). WALCL is weekly (as of Wednesday) via H.4.1; RRP is daily; TGA is a Fed liability series. M2 YoY is monthly.

FRED

+3

FRED

+3

FRED

+3

Risk conditions (Daily)

DXY 3‑month momentum (inverted), VIX level (inverted), Credit (HYG/LQD ratio or HY OAS). VIX is a 30‑day constant‑maturity implied vol index per Cboe methodology.

Cboe

+1

Crypto‑internal (Daily)

Stablecoins (USDT+USDC+DAI 30‑day log change), USDT dominance (20‑day, inverted), TOTAL3 (63‑day momentum). Dominance symbols on TV follow a documented formula.

TradingView

Beta & co‑move (Daily)

NDX 63‑day momentum, BTC↔NDX 90‑day correlation.

All components become z‑scores (optionally clipped), weighted, missing inputs drop and weights renormalize. We never use lookahead; we confirm on bar close to avoid repainting per Pine docs (barstate.isconfirmed, multi‑TF).

TradingView

+2

TradingView

+2

What you see on the chart

White line (CLRC) = macro regime score.

Background: Green = Risk‑ON, Red = Risk‑OFF, Teal = Early 3/5 (pre‑signal).

Table: shows each component’s z‑score and the Preference: BTC / ETH / ALTs / Mixed.

Signals & interpretation

Designed for Daily (1D) and Weekly (1W) only.

Regime gates (default Fast preset):

Enter ON: CLRC ≥ +0.8; Hold ON while ≥ +0.5.

Enter OFF: CLRC ≤ −1.0; Hold OFF while ≤ −0.5.

0 / ±1 reading: CLRC is a standardized composite.

~0 = neutral baseline (no macro edge).

≥ +1 = strong macro tailwind (≈ +1σ).

≤ −1 = strong headwind (≈ −1σ).

Early 3/5 (teal): a fast pre‑signal when at least 3 of 5 daily checks align: USDT.D↓, DXY↓, VIX↓, HYG/LQD↑, ETHBTC↑ or TOTAL3↑. It often precedes a full ON flip—use for pre‑positioning rather than full sizing.

BTC/ETH/ALTs selector (only when ON):

ALTs when BTC.D↓ and (ETHBTC↑ or TOTAL3↑) ⇒ rotate down the risk curve.

BTC when BTC.D↑ and ETHBTC↓ ⇒ keep it concentrated.

ETH when ETHBTC↑ while BTC.D flat/up ⇒ add ETH beta.

(Dominance mechanics are documented by TV.)

TradingView

Dissonance (incompatibility) rules — when to stand down

Use these overrides to avoid false comfort:

CLRC > +1 but USDT.D↑ and/or VIX spikes day‑over‑day → downgrade to Neutral; wait for USDT.D to stabilize and VIX to cool (VIX is a fear gauge of 30‑day expectation).

Cboe Global Markets

CLRC > +1 but DXY↑ sharply (USD squeeze) → size below normal; require DXY momentum to roll over.

CLRC < −1 but Early 3/5 = true two days in a row → start reducing underweights; look for ON flip within a few bars.

NetLiq improving (W) but credit (HYG/LQD) deteriorating (D) → treat as mixed regime; prefer BTC over ALTs.

How to use (step‑by‑step)

A. Read on Daily (1D) — main regime

Open CRYPTOCAP:TOTAL3, 1D (panel applied).

Wait for bar close (use alerts on confirmed bar). Pine docs recommend barstate.isconfirmed to avoid repainting on realtime bars.

TradingView

If ON, check Preference (BTC / ETH / ALTs).

Then drop to 4H on your trading pair for micro entries (this indicator itself is not for intraday timing).

B. Confirm weekly macro (1W) — once per week)

Review WALCL/RRP/TGA after the H.4.1 release on Thursdays ~4:30 pm ET. WALCL is “Weekly, as of Wednesday”; M2 is Monthly—so do not expect daily responsiveness from these.

Federal Reserve

+2

FRED

+2

Recommended check times (practical schedule)

Daily regime read: right after your chart’s daily close (confirmed bar). For consistent timing across crypto, many users set chart timezone to UTC and read ~00:05 UTC; you can change chart timezone in TV’s settings.

TradingView

In‑day monitoring: optional spot checks 16:00 & 20:00 UTC (DXY/VIX move during US hours), but act only after the daily bar confirms.

Weekly macro pass: Thu 21:30–22:30 UTC (after H.4.1 4:30 pm ET) or Fri after daily close, to let weekly FRED series propagate.

Federal Reserve

Limitations & data latency (be explicit)

Higher‑TF data & confirmation: FRED weekly/monthly series will not reflect intraday risk in crypto; we aggregate them for regime, not for entry timing.

Repainting 101: Realtime bars move until close. This script does not use lookahead and follows Pine guidance on multi‑TF series; still, always act on confirmed bars.

TradingView

+1

Public‑library compliance: Title EN‑only; description starts in EN; clean chart; justify component mash‑up; no lookahead; no unrealistic claims.

TradingView

Alerts you can use

“Macro Risk‑ON (entry)” — fires on ON flip (confirmed bar).

“Macro Risk‑OFF (entry)” — fires on OFF flip.

“Early 3/5” — fires when the teal pre‑signal appears (not a regime flip).

“Preference change” — BTC/ETH/ALTs toggles while ON.

Publish note: Alerts are fine; just avoid implying guaranteed accuracy/performance.

TradingView

Background research (why these inputs matter)

Liquidity → Crypto: Fed H.4.1 timing and series definitions (WALCL, RRP, TGA) formalize the “net liquidity” concept used here.

FRED

+3

Federal Reserve

+3

FRED

+3

Stablecoins ↔ Non‑stable crypto: empirical work shows bi‑directional causality between stablecoin market cap and non‑stable crypto cap; stablecoin growth co‑moves with broader crypto activity.

Global liquidity link: world liquidity positively relates to total crypto market cap; lagged effects are observed at monthly horizons.

VIX/Uncertainty effect: fear shocks impair BTC’s “safe haven” behavior; VIX is a meaningful risk‑off read.

BOCS AdaptiveBOCS Adaptive Strategy - Automated Volatility Breakout System

WHAT THIS STRATEGY DOES:

This is an automated trading strategy that detects consolidation patterns through volatility analysis and executes trades when price breaks out of these channels. Take-profit and stop-loss levels are calculated dynamically using Average True Range (ATR) to adapt to current market volatility. The strategy closes positions partially at the first profit target and exits the remainder at the second target or stop loss.

TECHNICAL METHODOLOGY:

Price Normalization Process:

The strategy begins by normalizing price to create a consistent measurement scale. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). The current close price is then normalized using the formula: (close - lowest_low) / (highest_high - lowest_low). This produces values between 0 and 1, allowing volatility analysis to work consistently across different instruments and price levels.

Volatility Detection:

A 14-period standard deviation is applied to the normalized price series. Standard deviation measures how much prices deviate from their average - higher values indicate volatility expansion, lower values indicate consolidation. The strategy uses ta.highestbars() and ta.lowestbars() functions to track when volatility reaches peaks and troughs over the detection length period (default 14 bars).

Channel Formation Logic:

When volatility crosses from a high level to a low level, this signals the beginning of a consolidation phase. The strategy records this moment using ta.crossover(upper, lower) and begins tracking the highest and lowest prices during the consolidation. These become the channel boundaries. The duration between the crossover and current bar must exceed 10 bars minimum to avoid false channels from brief volatility spikes. Channels are drawn using box objects with the recorded high/low boundaries.

Breakout Signal Generation:

Two detection modes are available:

Strong Closes Mode (default): Breakout occurs when the candle body midpoint math.avg(close, open) exceeds the channel boundary. This filters out wick-only breaks.

Any Touch Mode: Breakout occurs when the close price exceeds the boundary.

When price closes above the upper channel boundary, a bullish breakout signal generates. When price closes below the lower boundary, a bearish breakout signal generates. The channel is then removed from the chart.

ATR-Based Risk Management:

The strategy uses request.security() to fetch ATR values from a specified timeframe, which can differ from the chart timeframe. For example, on a 5-minute chart, you can use 1-minute ATR for more responsive calculations. The ATR is calculated using ta.atr(length) with a user-defined period (default 14).

Exit levels are calculated at the moment of breakout:

Long Entry Price = Upper channel boundary

Long TP1 = Entry + (ATR × TP1 Multiplier)

Long TP2 = Entry + (ATR × TP2 Multiplier)

Long SL = Entry - (ATR × SL Multiplier)

For short trades, the calculation inverts:

Short Entry Price = Lower channel boundary

Short TP1 = Entry - (ATR × TP1 Multiplier)

Short TP2 = Entry - (ATR × TP2 Multiplier)

Short SL = Entry + (ATR × SL Multiplier)

Trade Execution Logic:

When a breakout occurs, the strategy checks if trading hours filter is satisfied (if enabled) and if position size equals zero (no existing position). If volume confirmation is enabled, it also verifies that current volume exceeds 1.2 times the 20-period simple moving average.

If all conditions are met:

strategy.entry() opens a position using the user-defined number of contracts

strategy.exit() immediately places a stop loss order

The code monitors price against TP1 and TP2 levels on each bar

When price reaches TP1, strategy.close() closes the specified number of contracts (e.g., if you enter with 3 contracts and set TP1 close to 1, it closes 1 contract). When price reaches TP2, it closes all remaining contracts. If stop loss is hit first, the entire position exits via the strategy.exit() order.

Volume Analysis System:

The strategy uses ta.requestUpAndDownVolume(timeframe) to fetch up volume, down volume, and volume delta from a specified timeframe. Three display modes are available:

Volume Mode: Shows total volume as bars scaled relative to the 20-period average

Comparison Mode: Shows up volume and down volume as separate bars above/below the channel midline

Delta Mode: Shows net volume delta (up volume - down volume) as bars, positive values above midline, negative below

The volume confirmation logic compares breakout bar volume to the 20-period SMA. If volume ÷ average > 1.2, the breakout is classified as "confirmed." When volume confirmation is enabled in settings, only confirmed breakouts generate trades.

INPUT PARAMETERS:

Strategy Settings:

Number of Contracts: Fixed quantity to trade per signal (1-1000)

Require Volume Confirmation: Toggle to only trade signals with volume >120% of average

TP1 Close Contracts: Exact number of contracts to close at first target (1-1000)

Use Trading Hours Filter: Toggle to restrict trading to specified session

Trading Hours: Session input in HHMM-HHMM format (e.g., "0930-1600")

Main Settings:

Normalization Length: Lookback bars for high/low calculation (1-500, default 100)

Box Detection Length: Period for volatility peak/trough detection (1-100, default 14)

Strong Closes Only: Toggle between body midpoint vs close price for breakout detection

Nested Channels: Allow multiple overlapping channels vs single channel at a time

ATR TP/SL Settings:

ATR Timeframe: Source timeframe for ATR calculation (1, 5, 15, 60, etc.)

ATR Length: Smoothing period for ATR (1-100, default 14)

Take Profit 1 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 2.0)

Take Profit 2 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 3.0)

Stop Loss Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 1.0)

Enable Take Profit 2: Toggle second profit target on/off

VISUAL INDICATORS:

Channel boxes with semi-transparent fill showing consolidation zones

Green/red colored zones at channel boundaries indicating breakout areas

Volume bars displayed within channels using selected mode

TP/SL lines with labels showing both price level and distance in points

Entry signals marked with up/down triangles at breakout price

Strategy status table showing position, contracts, P&L, ATR values, and volume confirmation status

HOW TO USE:

For 2-Minute Scalping:

Set ATR Timeframe to "1" (1-minute), ATR Length to 12, TP1 Multiplier to 2.0, TP2 Multiplier to 3.0, SL Multiplier to 1.5. Enable volume confirmation and strong closes only. Use trading hours filter to avoid low-volume periods.

For 5-15 Minute Day Trading:

Set ATR Timeframe to match chart or use 5-minute, ATR Length to 14, TP1 Multiplier to 2.0, TP2 Multiplier to 3.5, SL Multiplier to 1.2. Volume confirmation recommended but optional.

For Hourly+ Swing Trading:

Set ATR Timeframe to 15-30 minute, ATR Length to 14-21, TP1 Multiplier to 2.5, TP2 Multiplier to 4.0, SL Multiplier to 1.5. Volume confirmation optional, nested channels can be enabled for multiple setups.

BACKTEST CONSIDERATIONS:

Strategy performs best during trending or volatility expansion phases

Consolidation-heavy or choppy markets produce more false signals

Shorter timeframes require wider stop loss multipliers due to noise

Commission and slippage significantly impact performance on sub-5-minute charts

Volume confirmation generally improves win rate but reduces trade frequency

ATR multipliers should be optimized for specific instrument characteristics

COMPATIBLE MARKETS:

Works on any instrument with price and volume data including forex pairs, stock indices, individual stocks, cryptocurrency, commodities, and futures contracts. Requires TradingView data feed that includes volume for volume confirmation features to function.

KNOWN LIMITATIONS:

Stop losses execute via strategy.exit() and may not fill at exact levels during gaps or extreme volatility

request.security() on lower timeframes requires higher-tier TradingView subscription

False breakouts inherent to breakout strategies cannot be completely eliminated

Performance varies significantly based on market regime (trending vs ranging)

Partial closing logic requires sufficient position size relative to TP1 close contracts setting

RISK DISCLOSURE:

Trading involves substantial risk of loss. Past performance of this or any strategy does not guarantee future results. This strategy is provided for educational purposes and automated backtesting. Thoroughly test on historical data and paper trade before risking real capital. Market conditions change and strategies that worked historically may fail in the future. Use appropriate position sizing and never risk more than you can afford to lose. Consider consulting a licensed financial advisor before making trading decisions.

ACKNOWLEDGMENT & CREDITS:

This strategy is built upon the channel detection methodology created by AlgoAlpha in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns and sharing this innovative technique with the TradingView community. The enhancements added to the original concept include automated trade execution, multi-timeframe ATR-based risk management, partial position closing by contract count, volume confirmation filtering, and real-time position monitoring.

Opening Range IndicatorComplete Trading Guide: Opening Range Breakout Strategy

What Are Opening Ranges?

Opening ranges capture the high and low prices during the first few minutes of market open. These levels often act as key support and resistance throughout the trading day because:

Heavy volume occurs at market open as overnight orders execute

Institutional activity is concentrated during opening minutes

Price discovery happens as market participants react to overnight news

Psychological levels are established that traders watch all day

Understanding the Three Timeframes

OR5 (5-Minute Range: 9:30-9:35 AM)

Most sensitive - captures immediate market reaction

Quick signals but higher false breakout rate

Best for scalping and momentum trading

Use for early entry when conviction is high

OR15 (15-Minute Range: 9:30-9:45 AM)

Balanced approach - most popular among day traders

Moderate sensitivity with better reliability

Good for swing trades lasting several hours

Primary timeframe for most strategies

OR30 (30-Minute Range: 9:30-10:00 AM)

Most reliable but slower signals

Lower false breakout rate

Best for position trades and trend following

Use when looking for major moves

Core Trading Strategies

Strategy 1: Basic Breakout

Setup:

Wait for price to break above OR15 high or below OR15 low

Enter on the breakout candle close

Stop loss: Opposite side of the range

Target: 2-3x the range size

Example:

OR15 range: $100.00 - $102.00 (Range = $2.00)

Long entry: Break above $102.00

Stop loss: $99.50 (below OR15 low)

Target: $104.00+ (2x range size)

Strategy 2: Multiple Confirmation

Setup:

Wait for OR5 break first (early signal)

Confirm with OR15 break in same direction

Enter on OR15 confirmation

Stop: Below OR30 if available, or OR15 opposite level

Why it works:

Multiple timeframe confirmation reduces false signals and increases probability of sustained moves.

Strategy 3: Failed Breakout Reversal

Setup:

Price breaks OR15 level but fails to hold

Wait for re-entry into the range

Enter reversal trade toward opposite OR level

Stop: Recent breakout high/low

Target: Opposite side of range + extension

Key insight: Failed breakouts often lead to strong moves in the opposite direction.

Advanced Techniques

Range Quality Assessment

High-Quality Ranges (Trade these):

Range size: 0.5% - 2% of stock price

Clean boundaries (not choppy)

Volume spike during range formation

Clear rejection at range levels

Low-Quality Ranges (Avoid these):

Very narrow ranges (<0.3% of stock price)

Extremely wide ranges (>3% of stock price)

Choppy, overlapping candles

Low volume during formation

Volume Confirmation

For Breakouts:

Look for volume spike (2x+ average) on breakout

Declining volume often signals false breakout

Rising volume during range formation shows interest

Market Context Filters

Best Conditions:

Trending market days (SPY/QQQ with clear direction)

Earnings reactions or news-driven moves

High-volume stocks with good liquidity

Volatility above average (VIX considerations)

Avoid Trading When:

Extremely low volume days

Major economic announcements pending

Holidays or half-days

Choppy, sideways market conditions

Risk Management Rules

Position Sizing

Conservative: Risk 0.5% of account per trade

Moderate: Risk 1% of account per trade

Aggressive: Risk 2% maximum per trade

Stop Loss Placement

Inside the range: Quick exit but higher stop-out rate