Accumulation Stage Identifier and Strategy around for TradingIn the psychology of trading at any market condition, there are four stage usually occurs on any tickers.

Stage 1 -> Neglect phase or consolidation phase

It occurs when the company does not produce the expected result and waiting for next result.

It can extend for days, weeks, months and years. Never give entry at this stage though that blue-chip told to be cheaper in price.

Stage 2 -> Accumulation

It occurs when the company's earning and sales consistently grows.

It can extend for days, weeks, months but should not expect the continues increase in price, as there will be potential pull-back which can be considered as opportunity to accumulate.

If the company fundamental is good, just give some space at the time of pullback.

Most of the time, the pullback volume will be low to compare to volume at the time of increase.

Usually, the stock that is going through accumulation stage will definitely trade above 200SMA and short term MA will be greater than long term moving average.

Continues the highest high and highest low along with volume.

Stage 3 -> Distribution

It occurs when the company's earning and sales stagnated due to certain reason.

It can extend for days, weeks while the price and volume highly volatile.

High volume while the price low

Typically, the stock that is going through distribution stage will certainly trade below 200SMA and short term MA will be lesser than long term moving average.

Continues the lowest high and lowest low along with volume.

Stage 4 -> Capitalization

Price reaches the 52W low while volume spikes on big down.

In each stage, the price & volume are perfect indicator to highlight the situation and the trader with proper discipline and patients can certainly reap the fruitful outcome of accumulation stage.

Based on this explanation, here is the strategy that is created with 50,90 & 200 Simple moving average and price volume trends (PVT) indicator applied on MACD to signal whenever the PVT convergence and divergence.

Note:

As the indicator designed to signal on the ticker that trade above 200 moving average, it is good to use this strategy on companies that are fundamental strong.

Whenever, there is pull back happens, the strategy might signal for exit, however, here comes the traders patient based on the conviction on the particular chosen stocks.

White being patient is good, disciplinary in following the strategy also important. Hence, consider the action when the stock goes opposite direction from your expectation.

Hope this strategy would help you find the profit.

Happy investing.

Buscar en scripts para "volume"

DIVI Wunder StrategyAs it is known, divergence is a situation we encounter very often on graphs. Various divergencies may occur according to many indicators. MACD divergence, RSI divergence... In the strategy I use only positive divergence. What is positive divergence I will explain on MACD positive divergence A MACD positive divergence is a situation in which the MACD does not reach a new low, despite the fact that the price of the stock reached a new low. This is seen as a bullish trading signal—hence, the term “positive divergence.” So I thought of these divergencies and came up with a new strategy. Combining the divergencies with the VOLPIN strategy I wrote earlier, a great strategy has emerged. When the divergence signals are came from MACD,RSI,CCI,OBV,Chaikin Money Flow, VWmacd and Money Flow Index all these indicators I sent a buy signal until the 40 times completed. ThenI sent to sell signal when the price come to take profit level. In this strategy, you divide your principal into as many parts as you want. For example, let's say that you have 1000 dollars of money and you make purchases by dividing this money into 40 equal parts in the default settings of the indicator. $25 per purchase. After each purchase is made as 25 dollars, you can adjust your profit rate from the profit taking settings. When you look at the results of the strategy, your profit rate will be very high. I usually use this strategy in one hour periods. Of course you change it whatever you want. Also change all settings from panel to get more profit. Have fun :)

Gemini Wyckoff Trend SystemStrategy Name: Gemini Wyckoff-Trend System

1. Core Design Philosophy

This strategy fuses Wyckoff Theory (specifically the "Law of Effort vs. Result") with classic Trend Following principles. Its primary goal is not to catch every minor fluctuation, but to filter out 80% of market noise and fakeouts, ensuring that you only pull the trigger when "Smart Money" enters the market with genuine volume.

It operates on a strict "3-Dimension Verification" logic:

Trend (Context): Never trade against the macro trend.

Structure (Price Action): Identify accumulation zones and wait for the breakout.

Volume (Effort): Require massive volume confirmation to validate the move.

2. The 3-Filter System

Filter 1: The Trend Filter (EMA 200)

Rule: The strategy only looks for Long setups when the price is ABOVE the 200-period Exponential Moving Average (EMA).

Purpose: To strictly prevent "catching falling knives" or counter-trend trading during a bear market.

Filter 2: The Structure Filter (Donchian Channel)

Rule: The script automatically identifies the highest high of the past 20 bars to define the "Accumulation Box." A signal is only possible if the price closes above this resistance level.

Wyckoff Term: This represents "Jumping the Creek" (JTC)—signaling that price is leaving the trading range.

Filter 3: The Volume Filter (RVOL > 1.5)

Rule: The breakout bar must have a volume that is at least 1.5x higher than the average volume of the past 20 bars.

Purpose: To eliminate "Upthrusts" (Fake Breakouts). If price breaks out on low volume, the system ignores it.

3. Visual Guide

Once loaded, here is how to read the chart:

📉 Orange Line (EMA 200): The Bull/Bear divider. If price is below this line, stay in cash.

🌫️ Grey Zone: The "No-Trade Zone" (Accumulation/Consolidation). Do not trade while price is inside this box.

🟢 Lime Green Bar: The Entry Signal. This indicates a valid breakout confirmed by high volume (Smart Money entry).

🪜 Red Step Line: Your Trailing Stop (ATR-based). As long as you hold a position, watch this line. If price closes below it, exit immediately.

📊 Dashboard (Top Right): Monitors market "Heat." If RVOL is Green, volume is significant.

4. Best Practices

Ideal For: Traders who struggle with over-trading or FOMO. This script enforces patience and discipline.

Timeframe: Recommended for 4-Hour (4H) or Daily (1D) charts to catch major crypto trends (e.g., Bitcoin main waves).

Asset Class: Crypto, Stocks, or any asset with high volume liquidity.

5. Risk Warning

This strategy includes a built-in ATR Volatility Stop. The stop-loss level adjusts dynamically based on market volatility. Please adhere strictly to the stop-loss signals to protect your capital.

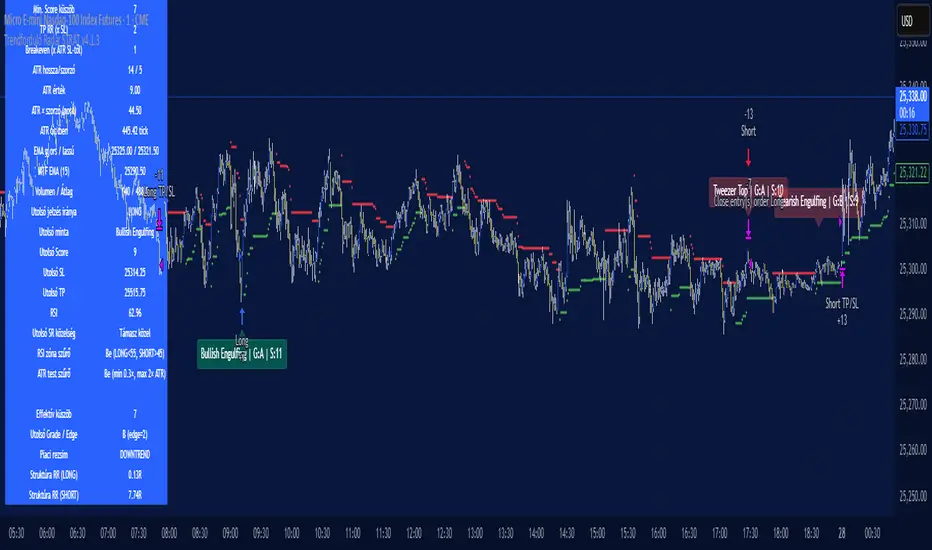

Trendforduló Radar STRAT v4.1.3Trend Reversal Radar is a proprietary indicator that examines potential turning points in market trends. It combines data from multiple time frames, support and resistance levels, and volume movements to provide visual signals to traders. Its purpose is not to provide trading advice, but to complement technical analysis and provide more confident decision support.- A Trendforduló Radar egy saját fejlesztésű indikátor, amely a piaci trendek lehetséges fordulópontjait vizsgálja. Több idősík adatait, támasz–ellenállás szinteket és volumenmozgásokat kombinálva ad vizuális jelzést a kereskedőnek. A célja nem a kereskedési tanácsadás, hanem hogy kiegészítse a technikai elemzést és magabiztosabb döntéstámogatást adjon.

Trendforduló Radar Trend Reversal Radar is a proprietary indicator that examines potential turning points in market trends. It combines data from multiple time frames, support and resistance levels, and volume movements to provide visual signals to traders. Its purpose is not to provide trading advice, but to complement technical analysis and provide more confident decision support.- A Trendforduló Radar egy saját fejlesztésű indikátor, amely a piaci trendek lehetséges fordulópontjait vizsgálja. Több idősík adatait, támasz–ellenállás szinteket és volumenmozgásokat kombinálva ad vizuális jelzést a kereskedőnek. A célja nem a kereskedési tanácsadás, hanem hogy kiegészítse a technikai elemzést és magabiztosabb döntéstámogatást adjon.

Trio Strategy w EMA Timing Gate, Early Flip, Clouds and Cross AlMomentum Trio Strategy w EMA Timing Gate, Early Flip, Clouds and Cross Alerts

Short title: Trio EMA Strategy

Concept and Originality

This strategy merges three momentum systems – StochRSI, RSI EMA, and MACD – into one coordinated Trio.

It triggers possible entries only (no exits) when all three align within user-defined windows, with an EMA timing gate for precision and an optional early flip feature if the EMA crosses first.

Optional cooldown and filters reduce false signals.

It also shows green and purple markers when all three momentum indicators cross together, and provides alert notifications on every individual and trio crossover event.

StochRSI-based clouds highlight overbought and oversold areas for quick visual context.

Each part has a defined role:

Trio alignment ensures multi-indicator confirmation.

EMA gate refines timing and enables early trend flips.

Cooldown reduces overtrading.

Filters check price, trend, and volume quality.

Clouds visualize momentum extremes.

Markers show where the Trio crosses.

Alerts notify on all key momentum events.

How It Works

Trio confirmation (core):

StochRSI – percent K and D cross within stochGroupWindow.

RSI – RSI crossing its EMA.

MACD – line crossing signal within macdGroupWindow.

When all three cross up, a green marker appears.

When all three cross down, a purple marker appears.

These mark potential entry points only. Exits are not included.

EMA timing gate:

EMA(5) and EMA(9) define short-term trend.

Longs: EMA(5) greater than EMA(9).

Shorts: EMA(5) less than EMA(9).

Early Flip: when EMA crosses before the trio, a one-time flip can trigger after the chosen cooldown.

Cooldown prevents multiple entries in choppy markets.

Filters include:

Price Filter – restricts entries relative to EMA.

Trend Filter – aligns trades with a longer EMA.

Volume Filter – checks for rising volume.

Overbought and Oversold Clouds:

Red cloud when StochRSI is greater or equal to 80 (overbought).

Green cloud when StochRSI is less or equal to 20 (oversold).

Clouds are for context only, not trade signals.

Alerts trigger on every Trio signal and each individual crossover for StochRSI, RSI, and MACD.

Inputs You Can Tune

RSI, StochRSI, and MACD periods and windows.

EMA gate lengths.

Early-flip toggle and cooldown.

Trio cooldowns.

Filters for price, trend, and volume.

Marker visibility (green and purple).

Overbought or oversold cloud display.

Alert toggles for all cross types.

How To Use

1. Apply to any liquid market such as stocks, crypto, or forex.

2. Choose timeframe.

3. Keep default settings first, then fine-tune windows or cooldowns.

4. Use clouds and markers for entry guidance only. Exits are manual or from another strategy.

5. Enable alerts for real-time notifications of indicator and Trio crosses.

Default Properties Used for Publication (Backtest Transparency)

Initial capital: 100,000 USD – necessary for stock testing so one percent sizing produces realistic order size.

Order size: one percent of equity per trade to keep risk small.

Commission: 0.10 percent per side, realistic for brokers and exchanges.

Slippage: 0.05 percent, equal to roughly one to two ticks on stocks.

Pyramiding: 0.

Execution: on close.

Sample dataset: at least 100 trades across multiple timeframes and markets.

The higher initial capital ensures valid fills for stock testing, while risk stays proportional since position size is percentage based.

Why These Components Work Together

Trio confluence confirms momentum alignment.

EMA gate refines entry timing and allows early reversals.

Cooldown and filters reduce false triggers.

Markers confirm when all three indicators cross together.

Clouds and alerts improve awareness and reaction speed.

The result is a robust entry-only framework that adapts to many markets.

Notes and Limitations

Focused on entry detection only. Exits are manual or external.

For educational use only, not financial advice.

Always test with realistic slippage, fees, and several symbols.

Past results do not guarantee future performance.

Attribution

All logic and structure are original to this publication.

Common Pine functions follow official Pine documentation.

Reversal Point Dynamics - Machine Learning⇋ Reversal Point Dynamics - Machine Learning

RPD Machine Learning: Self-Adaptive Multi-Armed Bandit Trading System

RPD Machine Learning is an advanced algorithmic trading system that implements genuine machine learning through contextual multi-armed bandits, reinforcement learning, and online adaptation. Unlike traditional indicators that use fixed rules, RPD learns from every trade outcome , automatically discovers which strategies work in current market conditions, and continuously adapts without manual intervention .

Core Innovation: The system deploys six distinct trading policies (ranging from aggressive trend-following to conservative range-bound strategies) and uses LinUCB contextual bandit algorithms with Random Fourier Features to learn which policy performs best in each market regime. After the initial learning phase (50-100 trades), the system achieves autonomous adaptation , automatically shifting between policies as market conditions evolve.

Target Users: Quantitative traders, algorithmic trading developers, systematic traders, and data-driven investors who want a system that adapts over time . Suitable for stocks, futures, forex, and cryptocurrency on any liquid instrument with >100k daily volume.

The Problem This System Solves

Traditional Technical Analysis Limitations

Most trading systems suffer from three fundamental challenges :

Fixed Parameters: Static settings (like "buy when RSI < 30") work well in backtests but may struggle when markets change character. What worked in low-volatility environments may not work in high-volatility regimes.

Strategy Degradation: Manual optimization (curve-fitting) produces systems that perform well on historical data but may underperform in live trading. The system never adapts to new market conditions.

Cognitive Overload: Running multiple strategies simultaneously forces traders to manually decide which one to trust. This leads to hesitation, late entries, and inconsistent execution.

How RPD Machine Learning Addresses These Challenges

Automated Strategy Selection: Instead of requiring you to choose between trend-following and mean-reversion strategies, RPD runs all six policies simultaneously and uses machine learning to automatically select the best one for current conditions. The decision happens algorithmically, removing human hesitation.

Continuous Learning: After every trade, the system updates its understanding of which policies are working. If the market shifts from trending to ranging, RPD automatically detects this through changing performance patterns and adjusts selection accordingly.

Context-Aware Decisions: Unlike simple voting systems that treat all conditions equally, RPD analyzes market context (ADX regime, entropy levels, volatility state, volume patterns, time of day, historical performance) and learns which combinations of context features correlate with policy success.

Machine Learning Architecture: What Makes This "Real" ML

Component 1: Contextual Multi-Armed Bandits (LinUCB)

What Is a Multi-Armed Bandit Problem?

Imagine facing six slot machines, each with unknown payout rates. The exploration-exploitation dilemma asks: Should you keep pulling the machine that's worked well (exploitation) or try others that might be better (exploration)? RPD solves this for trading policies.

Academic Foundation:

RPD implements Linear Upper Confidence Bound (LinUCB) from the research paper "A Contextual-Bandit Approach to Personalized News Article Recommendation" (Li et al., 2010, WWW Conference). This algorithm is used in content recommendation and ad placement systems.

How It Works:

Each policy (AggressiveTrend, ConservativeRange, VolatilityBreakout, etc.) is treated as an "arm." The system maintains:

Reward History: Tracks wins/losses for each policy

Contextual Features: Current market state (8-10 features including ADX, entropy, volatility, volume)

Uncertainty Estimates: Confidence in each policy's performance

UCB Formula: predicted_reward + α × uncertainty

The system selects the policy with highest UCB score , balancing proven performance (predicted_reward) with potential for discovery (uncertainty bonus). Initially, all policies have high uncertainty, so the system explores broadly. After 50-100 trades, uncertainty decreases, and the system focuses on known-performing policies.

Why This Matters:

Traditional systems pick strategies based on historical backtests or user preference. RPD learns from actual outcomes in your specific market, on your timeframe, with your execution characteristics.

Component 2: Random Fourier Features (RFF)

The Non-Linearity Challenge:

Market relationships are often non-linear. High ADX may indicate favorable conditions when volatility is normal, but unfavorable when volatility spikes. Simple linear models struggle to capture these interactions.

Academic Foundation:

RPD implements Random Fourier Features from "Random Features for Large-Scale Kernel Machines" (Rahimi & Recht, 2007, NIPS). This technique approximates kernel methods (like Support Vector Machines) while maintaining computational efficiency for real-time trading.

How It Works:

The system transforms base features (ADX, entropy, volatility, etc.) into a higher-dimensional space using random projections and cosine transformations:

Input: 8 base features

Projection: Through random Gaussian weights

Transformation: cos(W×features + b)

Output: 16 RFF dimensions

This allows the bandit to learn non-linear relationships between market context and policy success. For example: "AggressiveTrend performs well when ADX >25 AND entropy <0.6 AND hour >9" becomes naturally encoded in the RFF space.

Why This Matters:

Without RFF, the system could only learn "this policy has X% historical performance." With RFF, it learns "this policy performs differently in these specific contexts" - enabling more nuanced selection.

Component 3: Reinforcement Learning Stack

Beyond bandits, RPD implements a complete RL framework :

Q-Learning: Value-based RL that learns state-action values. Maps 54 discrete market states (trend×volatility×RSI×volume combinations) to 5 actions (4 policies + no-trade). Updates via Bellman equation after each trade. Converges toward optimal policy after 100-200 trades.

TD(λ) with Eligibility Traces: Extension of Q-Learning that propagates credit backwards through time . When a trade produces an outcome, TD(λ) updates not just the final state-action but all states visited during the trade, weighted by eligibility decay (λ=0.90). This accelerates learning from multi-bar trades.

Policy Gradient (REINFORCE): Learns a stochastic policy directly from 12 continuous market features without discretization. Uses gradient ascent to increase probability of actions that led to positive outcomes. Includes baseline (average reward) for variance reduction.

Meta-Learning: The system learns how to learn by adapting its own learning rates based on feature stability and correlation with outcomes. If a feature (like volume ratio) consistently correlates with success, its learning rate increases. If unstable, rate decreases.

Why This Matters:

Q-Learning provides fast discrete decisions. Policy Gradient handles continuous features. TD(λ) accelerates learning. Meta-learning optimizes the optimization. Together, they create a robust, multi-approach learning system that adapts more quickly than any single algorithm.

Component 4: Policy Momentum Tracking (v2 Feature)

The Recency Challenge:

Standard bandits treat all historical data equally. If a policy performed well historically but struggles in current conditions due to regime shift, the system may be slow to adapt because historical success outweighs recent underperformance.

RPD's Solution:

Each policy maintains a ring buffer of the last 10 outcomes. The system calculates:

Momentum: recent_win_rate - global_win_rate (range: -1 to +1)

Confidence: consistency of recent results (1 - variance)

Policies with positive momentum (recent outperformance) get an exploration bonus. Policies with negative momentum and high confidence (consistent recent underperformance) receive a selection penalty.

Effect: When markets shift, the system detects the shift more quickly through momentum tracking, enabling faster adaptation than standard bandits.

Signal Generation: The Core Algorithm

Multi-Timeframe Fractal Detection

RPD identifies reversal points using three complementary methods :

1. Quantum State Analysis:

Divides price range into discrete states (default: 6 levels)

Peak signals require price in top states (≥ state 5)

Valley signals require price in bottom states (≤ state 1)

Prevents mid-range signals that may struggle in strong trends

2. Fractal Geometry:

Identifies swing highs/lows using configurable fractal strength

Confirms local extremum with neighboring bars

Validates reversal only if price crosses prior extreme

3. Multi-Timeframe Confirmation:

Analyzes higher timeframe (4× default) for alignment

MTF confirmation adds probability bonus

Designed to reduce false signals while preserving valid setups

Probability Scoring System

Each signal receives a dynamic probability score (40-99%) based on:

Base Components:

Trend Strength: EMA(velocity) / ATR × 30 points

Entropy Quality: (1 - entropy) × 10 points

Starting baseline: 40 points

Enhancement Bonuses:

Divergence Detection: +20 points (price/momentum divergence)

RSI Extremes: +8 points (RSI >65 for peaks, <40 for valleys)

Volume Confirmation: +5 points (volume >1.2× average)

Adaptive Momentum: +10 points (strong directional velocity)

MTF Alignment: +12 points (higher timeframe confirms)

Range Factor: (high-low)/ATR × 3 - 1.5 points (volatility adjustment)

Regime Bonus: +8 points (trending ADX >25 with directional agreement)

Penalties:

High Entropy: -5 points (entropy >0.85, chaotic price action)

Consolidation Regime: -10 points (ADX <20, no directional conviction)

Final Score: Clamped to 40-99% range, classified as ELITE (>85%), STRONG (75-85%), GOOD (65-75%), or FAIR (<65%)

Entropy-Based Quality Filter

What Is Entropy?

Entropy measures randomness in price changes . Low entropy indicates orderly, directional moves. High entropy indicates chaotic, unpredictable conditions.

Calculation:

Count up/down price changes over adaptive period

Calculate probability: p = ups / total_changes

Shannon entropy: -p×log(p) - (1-p)×log(1-p)

Normalized to 0-1 range

Application:

Entropy <0.5: Highly ordered (ELITE signals possible)

Entropy 0.5-0.75: Mixed (GOOD signals)

Entropy >0.85: Chaotic (signals blocked or heavily penalized)

Why This Matters:

Prevents trading during choppy, news-driven conditions where technical patterns may be less reliable. Automatically raises quality bar when market is unpredictable.

Regime Detection & Market Microstructure - ADX-Based Regime Classification

RPD uses Wilder's Average Directional Index to classify markets:

Bull Trend: ADX >25, +DI > -DI (directional conviction bullish)

Bear Trend: ADX >25, +DI < -DI (directional conviction bearish)

Consolidation: ADX <20 (no directional conviction)

Transitional: ADX 20-25 (forming direction, ambiguous)

Filter Logic:

Blocks all signals during Transitional regime (avoids trading during uncertain conditions)

Blocks Consolidation signals unless ADX ≥ Min Trend Strength

Adds probability bonus during strong trends (ADX >30)

Effect: Designed to reduce signal frequency while focusing on higher-quality setups.

Divergence Detection

Bearish Divergence:

Price makes higher high

Velocity (price momentum) makes lower high

Indicates weakening upward pressure → SHORT signal quality boost

Bullish Divergence:

Price makes lower low

Velocity makes higher low

Indicates weakening downward pressure → LONG signal quality boost

Bonus: Adds probability points and additional acceleration factor. Divergence signals have historically shown higher success rates in testing.

Hierarchical Policy System - The Six Trading Policies

1. AggressiveTrend (Policy 0):

Probability Threshold: 60% (trades more frequently)

Entropy Threshold: 0.70 (tolerates moderate chaos)

Stop Multiplier: 2.5× ATR (wider stops for trends)

Target Multiplier: 5.0R (larger targets)

Entry Mode: Pyramid (scales into winners)

Best For: Strong trending markets, breakouts, momentum continuation

2. ConservativeRange (Policy 1):

Probability Threshold: 75% (more selective)

Entropy Threshold: 0.60 (requires order)

Stop Multiplier: 1.8× ATR (tighter stops)

Target Multiplier: 3.0R (modest targets)

Entry Mode: Single (one-shot entries)

Best For: Range-bound markets, low volatility, mean reversion

3. VolatilityBreakout (Policy 2):

Probability Threshold: 65% (moderate)

Entropy Threshold: 0.80 (accepts high entropy)

Stop Multiplier: 3.0× ATR (wider stops)

Target Multiplier: 6.0R (larger targets)

Entry Mode: Tiered (splits entry)

Best For: Compression breakouts, post-consolidation moves, gap opens

4. EntropyScalp (Policy 3):

Probability Threshold: 80% (very selective)

Entropy Threshold: 0.40 (requires extreme order)

Stop Multiplier: 1.5× ATR (tightest stops)

Target Multiplier: 2.5R (quick targets)

Entry Mode: Single

Best For: Low-volatility grinding moves, tight ranges, highly predictable patterns

5. DivergenceHunter (Policy 4):

Probability Threshold: 70% (quality-focused)

Entropy Threshold: 0.65 (balanced)

Stop Multiplier: 2.2× ATR (moderate stops)

Target Multiplier: 4.5R (balanced targets)

Entry Mode: Tiered

Best For: Divergence-confirmed reversals, exhaustion moves, trend climax

6. AdaptiveBlend (Policy 5):

Probability Threshold: 68% (balanced)

Entropy Threshold: 0.75 (balanced)

Stop Multiplier: 2.0× ATR (standard)

Target Multiplier: 4.0R (standard)

Entry Mode: Single

Best For: Mixed conditions, general trading, fallback when no clear regime

Policy Clustering (Advanced/Extreme Modes)

Policies are grouped into three clusters based on regime affinity:

Cluster 1 (Trending): AggressiveTrend, DivergenceHunter

High regime affinity (0.8): Performs well when ADX >25

Moderate vol affinity (0.6): Works in various volatility

Cluster 2 (Ranging): ConservativeRange, AdaptiveBlend

Low regime affinity (0.3): Better suited for ADX <20

Low vol affinity (0.4): Optimized for calm markets

Cluster 3 (Breakout): VolatilityBreakout

Moderate regime affinity (0.6): Works in multiple regimes

High vol affinity (0.9): Requires high volatility for optimal characteristics

Hierarchical Selection Process:

Calculate cluster scores based on current regime and volatility

Select best-matching cluster

Run UCB selection within chosen cluster

Apply momentum boost/penalty

This two-stage process reduces learning time - instead of choosing among 6 policies from scratch, system first narrows to 1-2 policies per cluster, then optimizes within cluster.

Risk Management & Position Sizing

Dynamic Kelly Criterion Sizing (Optional)

Traditional Fixed Sizing Challenge:

Using the same position size for all signal probabilities may be suboptimal. Higher-probability signals could justify larger positions, lower-probability signals smaller positions.

Kelly Formula:

f = (p × b - q) / b

Where:

p = win probability (from signal score)

q = loss probability (1 - p)

b = win/loss ratio (average_win / average_loss)

f = fraction of capital to risk

RPD Implementation:

Uses Fractional Kelly (1/4 Kelly default) for safety. Full Kelly is theoretically optimal but can recommend large position sizes. Fractional Kelly reduces volatility while maintaining adaptive sizing benefits.

Enhancements:

Probability Bonus: Normalize(prob, 65, 95) × 0.5 multiplier

Divergence Bonus: Additional sizing on divergence signals

Regime Bonus: Additional sizing during strong trends (ADX >30)

Momentum Adjustment: Hot policies receive sizing boost, cold policies receive reduction

Safety Rails:

Minimum: 1 contract (floor)

Maximum: User-defined cap (default 10 contracts)

Portfolio Heat: Max total risk across all positions (default 4% equity)

Multi-Mode Stop Loss System

ATR Mode (Default):

Stop = entry ± (ATR × base_mult × policy_mult)

Consistent risk sizing

Ignores market structure

Best for: Futures, forex, algorithmic trading

Structural Mode:

Finds swing low (long) or high (short) over last 20 bars

Identifies fractal pivots within lookback

Places stop below/above structure + buffer (0.1× ATR)

Best for: Stocks, instruments that respect structure

Hybrid Mode (Intelligent):

Attempts structural stop first

Falls back to ATR if:

Structural level is invalid (beyond entry)

Structural stop >2× ATR away (too wide)

Best for: Mixed instruments, adaptability

Dynamic Adjustments:

Breakeven: Move stop to entry + 1 tick after 1.0R profit

Trailing: Trail stop 0.8R behind price after 1.5R profit

Timeout: Force close after 30 bars (optional)

Tiered Entry System

Challenge: Equal sizing on all signals may not optimize capital allocation relative to signal quality.

Solution:

Tier 1 (40% of size): Enters immediately on all signals

Tier 2 (60% of size): Enters only if probability ≥ Tier 2 trigger (default 75%)

Example:

Calculated optimal size: 10 contracts

Signal probability: 72%

Tier 2 trigger: 75%

Result: Enter 4 contracts only (Tier 1)

Same signal at 80% probability

Result: Enter 10 contracts (4 Tier 1 + 6 Tier 2)

Effect: Automatically scales size to signal quality, optimizing capital allocation.

Performance Optimization & Learning Curve

Warmup Phase (First 50 Trades)

Purpose: Ensure all policies get tested before system focuses on preferred strategies.

Modifications During Warmup:

Probability thresholds reduced 20% (65% becomes 52%)

Entropy thresholds increased 20% (more permissive)

Exploration rate stays high (30%)

Confidence width (α) doubled (more exploration)

Why This Matters:

Without warmup, system might commit to early-performing policy without testing alternatives. Warmup forces thorough exploration before focusing on best-performing strategies.

Curriculum Learning

Phase 1 (Trades 1-50): Exploration

Warmup active

All policies tested

High exploration (30%)

Learning fundamental patterns

Phase 2 (Trades 50-100): Refinement

Warmup ended, thresholds normalize

Exploration decaying (30% → 15%)

Policy preferences emerging

Meta-learning optimizing

Phase 3 (Trades 100-200): Specialization

Exploration low (15% → 8%)

Clear policy preferences established

Momentum tracking fully active

System focusing on learned patterns

Phase 4 (Trades 200+): Maturity

Exploration minimal (8% → 5%)

Regime-policy relationships learned

Auto-adaptation to market shifts

Stable performance expected

Convergence Indicators

System is learning well when:

Policy switch rate decreasing over time (initially ~50%, should drop to <20%)

Exploration rate decaying smoothly (30% → 5%)

One or two policies emerge with >50% selection frequency

Performance metrics stabilizing over time

Consistent behavior in similar market conditions

System may need adjustment when:

Policy switch rate >40% after 100 trades (excessive exploration)

Exploration rate not decaying (parameter issue)

All policies showing similar selection (not differentiating)

Performance declining despite relaxed thresholds (underlying signal issue)

Highly erratic behavior after learning phase

Advanced Features

Attention Mechanism (Extreme Mode)

Challenge: Not all features are equally important. Trading hour might matter more than price-volume correlation, but standard approaches treat them equally.

Solution:

Each RFF dimension has an importance weight . After each trade:

Calculate correlation: sign(feature - 0.5) × sign(reward)

Update importance: importance += correlation × 0.01

Clamp to range

Effect: Important features get amplified in RFF transformation, less important features get suppressed. System learns which features correlate with successful outcomes.

Temporal Context (Extreme Mode)

Challenge: Current market state alone may be incomplete. Historical context (was volatility rising or falling?) provides additional information.

Solution:

Includes 3-period historical context with exponential decay (0.85):

Current features (weight 1.0)

1 bar ago (weight 0.85)

2 bars ago (weight 0.72)

Effect: Captures momentum and acceleration of market features. System learns patterns like "rising volatility with falling entropy" that may precede significant moves.

Transfer Learning via Episodic Memory

Short-Term Memory (STM):

Last 20 trades

Fast adaptation to immediate regime

High learning rate

Long-Term Memory (LTM):

Condensed historical patterns

Preserved knowledge from past regimes

Low learning rate

Transfer Mechanism:

When STM fills (20 trades), patterns consolidated into LTM . When similar regime recurs later, LTM provides faster adaptation than starting from scratch.

Practical Implementation Guide - Recommended Settings by Instrument

Futures (ES, NQ, CL):

Adaptive Period: 20-25

ML Mode: Advanced

RFF Dimensions: 16

Policies: 6

Base Risk: 1.5%

Stop Mode: ATR or Hybrid

Timeframe: 5-15 min

Forex Majors (EURUSD, GBPUSD):

Adaptive Period: 25-30

ML Mode: Advanced

RFF Dimensions: 16

Policies: 6

Base Risk: 1.0-1.5%

Stop Mode: ATR

Timeframe: 5-30 min

Cryptocurrency (BTC, ETH):

Adaptive Period: 20-25

ML Mode: Extreme (handles non-stationarity)

RFF Dimensions: 32 (captures complexity)

Policies: 6

Base Risk: 1.0% (volatility consideration)

Stop Mode: Hybrid

Timeframe: 15 min - 4 hr

Stocks (Large Cap):

Adaptive Period: 25-30

ML Mode: Advanced

RFF Dimensions: 16

Policies: 5-6

Base Risk: 1.5-2.0%

Stop Mode: Structural or Hybrid

Timeframe: 15 min - Daily

Scaling Strategy

Phase 1 (Testing - First 50 Trades):

Max Contracts: 1-2

Goal: Validate system on your instrument

Monitor: Performance stabilization, learning progress

Phase 2 (Validation - Trades 50-100):

Max Contracts: 2-3

Goal: Confirm learning convergence

Monitor: Policy stability, exploration decay

Phase 3 (Scaling - Trades 100-200):

Max Contracts: 3-5

Enable: Kelly sizing (1/4 Kelly)

Goal: Optimize capital efficiency

Monitor: Risk-adjusted returns

Phase 4 (Full Deployment - Trades 200+):

Max Contracts: 5-10

Enable: Full momentum tracking

Goal: Sustained consistent performance

Monitor: Ongoing adaptation quality

Limitations & Disclaimers

Statistical Limitations

Learning Sample Size: System requires minimum 50-100 trades for basic convergence, 200+ trades for robust learning. Early performance (first 50 trades) may not reflect mature system behavior.

Non-Stationarity Risk: Markets change over time. A system trained on one market regime may need time to adapt when conditions shift (typically 30-50 trades for adjustment).

Overfitting Possibility: With 16-32 RFF dimensions and 6 policies, system has substantial parameter space. Small sample sizes (<200 trades) increase overfitting risk. Mitigated by regularization (λ) and fractional Kelly sizing.

Technical Limitations

Computational Complexity: Extreme mode with 32 RFF dimensions, 6 policies, and full RL stack requires significant computation. May perform slowly on lower-end systems or with many other indicators loaded.

Pine Script Constraints:

No true matrix inversion (uses diagonal approximation for LinUCB)

No cryptographic RNG (uses market data as entropy)

No proper random number generation for RFF (uses deterministic pseudo-random)

These approximations reduce mathematical precision compared to academic implementations but remain functional for trading applications.

Data Requirements: Needs clean OHLCV data. Missing bars, gaps, or low liquidity (<100k daily volume) can degrade signal quality.

Forward-Looking Bias Disclaimer

Reward Calculation Uses Future Data: The RL system evaluates trades using an 8-bar forward-looking window. This means when a position enters at bar 100, the reward calculation considers price movement through bar 108.

Why This is Disclosed:

Entry signals do NOT look ahead - decisions use only data up to entry bar

Forward data used for learning only, not signal generation

In live trading, system learns identically as bars unfold in real-time

Simulates natural learning process (outcomes are only known after trades complete)

Implication: Backtested metrics reflect this 8-bar evaluation window. Live performance may vary if:

- Positions held longer than 8 bars

- Slippage/commissions differ from backtest settings

- Market microstructure changes (wider spreads, different execution quality)

Risk Warnings

No Guarantee of Profit: All trading involves substantial risk of loss. Machine learning systems can fail if market structure fundamentally changes or during unprecedented events.

Maximum Drawdown: With 1.5% base risk and 4% max total risk, expect potential drawdowns. Historical drawdowns do not predict future drawdowns. Extreme market conditions can exceed expectations.

Black Swan Events: System has not been tested under: flash crashes, trading halts, circuit breakers, major geopolitical shocks, or other extreme events. Such events can exceed stop losses and cause significant losses.

Leverage Risk: Futures and forex involve leverage. Adverse moves combined with leverage can result in losses exceeding initial investment. Use appropriate position sizing for your risk tolerance.

System Failures: Code bugs, broker API failures, internet outages, or exchange issues can prevent proper execution. Always monitor automated systems and maintain appropriate safeguards.

Appropriate Use

This System Is:

✅ A machine learning framework for adaptive strategy selection

✅ A signal generation system with probabilistic scoring

✅ A risk management system with dynamic sizing

✅ A learning system designed to adapt over time

This System Is NOT:

❌ A price prediction system (does not forecast exact prices)

❌ A guarantee of profits (can and will experience losses)

❌ A replacement for due diligence (requires monitoring and understanding)

❌ Suitable for complete beginners (requires understanding of ML concepts, risk management, and trading fundamentals)

Recommended Use:

Paper trade for 100 signals before risking capital

Start with minimal position sizing (1-2 contracts) regardless of calculated size

Monitor learning progress via dashboard

Scale gradually over several months only after consistent results

Combine with fundamental analysis and broader market context

Set account-level risk limits (e.g., maximum drawdown threshold)

Never risk more than you can afford to lose

What Makes This System Different

RPD implements academically-derived machine learning algorithms rather than simple mathematical calculations or optimization:

✅ LinUCB Contextual Bandits - Algorithm from WWW 2010 conference (Li et al.)

✅ Random Fourier Features - Kernel approximation from NIPS 2007 (Rahimi & Recht)

✅ Q-Learning, TD(λ), REINFORCE - Standard RL algorithms from Sutton & Barto textbook

✅ Meta-Learning - Learning rate adaptation based on feature correlation

✅ Online Learning - Real-time updates from streaming data

✅ Hierarchical Policies - Two-stage selection with clustering

✅ Momentum Tracking - Recent performance analysis for faster adaptation

✅ Attention Mechanism - Feature importance weighting

✅ Transfer Learning - Episodic memory consolidation

Key Differentiators:

Actually learns from trade outcomes (not just parameter optimization)

Updates model parameters in real-time (true online learning)

Adapts to changing market regimes (not static rules)

Improves over time through reinforcement learning

Implements published ML algorithms with proper citations

Conclusion

RPD Machine Learning represents a different approach from traditional technical analysis to adaptive, self-learning systems . Instead of manually optimizing parameters (which can overfit to historical data), RPD learns behavior patterns from actual trading outcomes in your specific market.

The combination of contextual bandits, reinforcement learning, random fourier features, hierarchical policy selection, and momentum tracking creates a multi-algorithm learning system designed to handle non-stationary markets better than static approaches.

After the initial learning phase (50-100 trades), the system achieves autonomous adaptation - automatically discovering which strategies work in current conditions and shifting allocation without human intervention. This represents an approach where systems adapt over time rather than remaining static.

Use responsibly. Paper trade extensively. Scale gradually. Understand that past performance does not guarantee future results and all trading involves risk of loss.

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

Qullamagi EMA Breakout Autotrade (Crypto Futures L+S)Title: Qullamagi EMA Breakout – Crypto Autotrade

Overview

A crypto-focused, Qullamagi-style EMA breakout strategy built for autotrading on futures and perpetual swaps.

It combines a 5-MA trend stack (EMA 10/20, SMA 50/100/200), volatility contraction boxes, volume spikes and an optional higher-timeframe 200-MA filter. The script supports both long and short trades, partial take profit, trailing MA exits and percent-of-equity position sizing for automated crypto futures trading.

Key Features (Crypto)

Qullamagi MA Breakout Engine – trades only when price is aligned with a strong EMA/SMA trend and breaks out of a tight consolidation range. Longs use: Close > EMA10 > EMA20 > SMA50 > SMA100 > SMA200. Shorts are the mirror condition with all MAs sloping in the trend direction.

Strict vs Loose Modes – Strict (Daily) is designed for cleaner swing trades on 1H–4H (full MA stack, box+ATR and volume filters, optional HTF filter). Loose (Intraday) focuses on 10/20/50 alignment with relaxed filters for more frequent 15m–30m signals.

Volatility & Volume Filters for Crypto – ATR-based box height limit to detect volatility contraction, wide-candle filter to avoid chasing exhausted breakouts, and a volume spike condition requiring current volume to exceed an SMA of volume.

Higher-Timeframe Trend Filter (Optional) – uses a 200-period SMA on a higher timeframe (default: 1D). Longs only when HTF close is above the HTF 200-SMA, shorts only when it is below, helping avoid trading against dominant crypto trends.

Autotrade-Oriented Trade Management – position size as % of equity, initial stop anchored to a chosen MA (EMA10 / EMA20 / SMA50) with optional buffer, partial take profit at a configurable R-multiple, trailing MA exit for the remainder, and an optional cooldown after a full exit.

Markets & Timeframes

Best suited for BTC, ETH and major altcoin futures/perpetuals (Binance, Bybit, OKX, etc.).

Strict preset: 1H–4H charts for classic Qullamagi-style trend structure and fewer fake breakouts.

Loose preset: 15m–30m charts for higher trade frequency and more active intraday trading.

Always retune ATR length, box length, volume multiplier and position size for each symbol and exchange.

Strategy Logic (Quick Summary)

Long (Strict): MA stack in bullish alignment with all MAs sloping up → tight volatility box (ATR-based) → volume spike above SMA(volume) × multiplier → breakout above box high (close or intrabar) → optional HTF close above 200-SMA.

Short: Mirror logic: bearish MA stack, tight box, volume spike and breakdown below box low with optional HTF downtrend.

Best Practices for Crypto

Backtest on each symbol and timeframe you plan to autotrade, including commissions and slippage.

Start on higher timeframes (1H/4H) to learn the behavior, then move to 15m–30m if you want more signals.

Use the higher-timeframe filter when markets are strongly trending to reduce counter-trend trades.

Keep position-size percentage conservative until you fully understand the drawdowns.

Forward-test / paper trade before connecting to live futures accounts.

Webhook / Autotrade Integration

Designed to work with TradingView webhooks and external crypto trading bots.

Alert messages include structured fields such as: EVENT=ENTRY / SCALE_OUT / EXIT, SIDE=LONG / SHORT, STRATEGY=Qullamagi_MA.

Map each EVENT + SIDE combination to your bot logic (open long/short, partial close, full close, etc.) on your preferred exchange.

Important Notes & Disclaimer

Crypto markets are highly volatile and can change regime quickly. Backtest and forward-test thoroughly before using real capital. Higher timeframes generally produce cleaner MA structures and fewer fake breakouts.

This strategy is for educational and informational purposes only and does not constitute financial advice. Trading leveraged crypto products involves substantial risk of loss. Always do your own research, manage risk carefully, and never trade with money you cannot afford to lose.

Intraday Momentum for Volatile Stocks 29.09The strategy targets intraday momentum breakouts in volatile stocks when the broader market (Nifty) is in an uptrend. It enters long positions when stocks move significantly above their daily opening price with sufficient volume confirmation, then manages the trade using dynamic ATR-based stops and profit targets.

Entry Conditions

Price Momentum Filter: The stock must move at least 2.5% above its daily opening price, indicating strong bullish momentum. This percentage threshold is customizable and targets gap-up scenarios or strong intraday breakouts.

Volume Confirmation: Daily cumulative volume must exceed the 20-day average volume, ensuring institutional participation and genuine momentum. This prevents false breakouts on low volume.

Market Regime Filter: The Nifty index must be trading above its 50-day SMA, indicating a favorable market environment for momentum trades. This macro filter helps avoid trades during bearish market conditions.

Money Flow Index: MFI must be above 50, confirming buying pressure and positive money flow into the stock. This adds another layer of momentum confirmation.

Time Restriction: Trades are only initiated before 3:00 PM to ensure sufficient time for position management and avoid end-of-day volatility.

Exit Management

ATR Trailing Stop Loss: Uses a 3x ATR multiplier for dynamic stop-loss placement that trails higher highs, protecting profits while giving trades room to breathe. The trailing mechanism locks in gains as the stock moves favorably.

Profit Target: Set at 4x ATR above the entry price, providing a favorable risk-reward ratio based on the stock's volatility characteristics. This adaptive approach adjusts targets based on individual stock behavior.

Position Reset: Both stops and targets reset when not in a position, ensuring fresh calculations for each new trade.

Key Strengths

Volatility Adaptation: The ATR-based approach automatically adjusts risk parameters to match current market volatility levels. Higher volatility stocks get wider stops, while calmer stocks get tighter management.

Multi-Timeframe Filtering: Combines intraday price action with daily volume patterns and market regime analysis for robust signal generation.

Risk Management Focus: The strategy prioritizes capital preservation through systematic stop-loss placement and position sizing considerations.

Considerations for NSE Trading

This strategy appears well-suited for NSE intraday momentum trading, particularly for mid-cap and small-cap stocks that exhibit high volatility. The Nifty filter helps align trades with broader market sentiment, which is crucial in the Indian market context where sectoral and index movements strongly influence individual stocks.

The 2.5% threshold above open price is appropriate for volatile NSE stocks, though traders might consider adjusting this parameter based on the specific stocks being traded. The strategy's emphasis on volume confirmation is particularly valuable in the NSE environment where retail participation can create misleading price movements without institutional backin

Grand Master's Candlestick Dominance (ATR Enhanced)### Grand Master's Candlestick Dominance (ATR Enhanced)

**Overview**

Unleash the ancient wisdom of Japanese candlestick charting with a modern twist! This comprehensive Pine Script v5 strategy and indicator scans for over 75 classic and advanced candlestick patterns (bullish, bearish, and neutral), assigning dynamic strength scores (1-10) to each for precise signal filtering. Enhanced with Average True Range (ATR) for volatility-aware body size validation, it dominates the markets by combining timeless pattern recognition with robust confirmation layers. Whether used as a backtestable strategy or visual indicator, it empowers traders to spot high-probability reversals, continuations, and indecision setups with surgical accuracy.

Inspired by Steve Nison's *Japanese Candlestick Charting Techniques*, this tool elevates pattern analysis beyond basics—think Hammers, Engulfing patterns, Morning Stars, and rare gems like Abandoned Baby or Concealing Baby Swallow—all consolidated into intelligent arrays for real-time averaging and prioritization.

**Key Features**

- **Extensive Pattern Library**:

- **Bullish (25+ patterns)**: Hammer (8.0), Bullish Engulfing (10.0), Morning Star (7.0), Three White Soldiers (9.0), Dragonfly Doji (8.0), and more (e.g., Rising Three, Unique Three River Bottom).

- **Bearish (25+ patterns)**: Hanging Man (8.0), Bearish Engulfing (10.0), Evening Star (7.0), Three Black Crows (9.0), Gravestone Doji (8.0), and exotics like Upside Gap Two Crows or Stalled Pattern.

- **Neutral/Indecision (34+ patterns)**: Doji variants (Long-Legged, Four Price), Spinning Tops, Harami Crosses, and multi-bar setups like Upside Tasuki Gap or Advancing Block.

Each pattern includes duration tracking (1-5 bars) and ATR-adjusted body/shadow criteria for relevance in volatile conditions.

- **Smart Confirmation Filters** (All Toggleable):

- **Trend Alignment**: 20-period SMA (customizable) ensures entries align with the prevailing trend; optional higher timeframe (e.g., Daily) MA crossover for multi-timeframe confluence.

- **Support/Resistance (S/R)**: Pivot-based levels with 0.01% tolerance to confirm bounces or breaks.

- **Volume Surge**: 20-period volume MA with 1.5x spike multiplier to validate momentum.

- **ATR Body Sizing**: Filters small bodies (<0.3x ATR) and long bodies (>0.8x ATR) for context-aware pattern reliability.

- **Follow-Through**: Ensures post-pattern confirmation via bullish/bearish closes or closes beyond prior bars.

Minimum average strength (default 7.0) and individual pattern thresholds (5.0) prevent weak signals.

- **Entry & Exit Logic**:

- **Long Entry**: Bullish average strength ≥7.0 (outweighing bearish), uptrend, volume spike, near support, follow-through, and HTF alignment.

- **Short Entry**: Mirror for bearish dominance in downtrends near resistance.

- **Exits**: Bearish/neutral shift, or fixed TP (5%) / SL (2%)—pyramiding disabled, 10% equity sizing.

- Backtest range: Jan 1, 2020 – Dec 31, 2025 (editable). Initial capital: $10,000.

- **Interactive Dashboard** (Top-Right Panel):

Real-time insights including:

- Market phase (e.g., "Bullish Phase (Avg Str: 8.2)"), active pattern (e.g., "BULLISH: Bullish Engulfing (Str: 10.0, Bars: 2)"), and trend status.

- Strength breakdowns (Bull/Bear/Neutral counts & averages).

- Filter status (e.g., "Volume: ✔ Spike", "ATR: Enabled (L:0.8, S:0.3)").

- Backtest stats: Total trades, win rate, streak, and last entry/exit details (price & timestamp).

Toggle mode: Strategy (live trades) or Indicator (signals only).

- **Advanced Alerts** (15+ Toggleable Types):

Set up via TradingView's "Any alert() function call" for bar-close triggers:

- Entry/Exit signals with strength & pattern details.

- Strong patterns (≥2 bullish/bearish), neutral indecision, volume spikes.

- S/R breakouts, HTF reversals, high-confidence singles (≥8.0 strength).

- Conflicting signals, MA crossovers, ATR volatility bursts, multi-bar completions.

Example: "STRONG BULLISH PATTERN detected! Strength: 9.5 | Top Pattern: Three White Soldiers | Trend: Up".

**Customization & Usage Tips**

- **Inputs Groups**: Strategy toggles, confirmations, exits, backtest dates, and 15+ alert switches—all intuitively grouped.

- **Optimization**: Tune min strengths for aggressive (lower) or conservative (higher) trading; enable/disable filters to suit your style (e.g., disable S/R for scalping).

- **Best For**: Forex, stocks, crypto on 1H–Daily charts. Test on historical data to refine TP/SL.

- **Limitations**: No external data installs; relies on built-in TA functions. Patterns are probabilistic—combine with your risk management.

Master the candles like a grandmaster. Deploy on TradingView, backtest relentlessly, and let dominance begin! Questions? Drop a comment.

*Version: 1.0 | Updated: September 2025 | Credits: Built on Pine Script v5 with nods to Nison's timeless techniques.*

Dynamic Swing Anchored VWAP STRAT (Zeiierman/PineIndicators)Dynamic Swing Anchored VWAP STRATEGY — Zeiierman × PineIndicators (Pine Script v6)

A pivot-to-pivot Anchored VWAP strategy that adapts to volatility, enters long on bullish structure, and closes on bearish structure. Built for TradingView in Pine Script v6.

Full credits to zeiierman.

Repainting notice: The original indicator logic is repainting. Swing labels (HH/HL/LH/LL) are finalized after enough bars have printed, so labels do not occur in real time. It is not possible to execute at historical label points. Treat results as educational and validate with Bar Replay and paper trading before considering any discretionary use.

Concept

The script identifies swing highs/lows over a user-defined lookback ( Swing Period ). When structure flips (most recent swing low is newer than the most recent swing high, or vice versa), a new regime begins.

At each confirmed pivot, a fresh Anchored VWAP segment is started and updated bar-by-bar using an EWMA-style decay on price×volume and volume.

Responsiveness is controlled by Adaptive Price Tracking (APT) . Optionally, APT auto-adjusts with an ATR ratio so that high volatility accelerates responsiveness and low volatility smooths it.

Longs are opened/held in bullish regimes and closed when the regime turns bearish. No short positions are taken by design.

How it works (under the hood)

Swing detection: Uses ta.highestbars / ta.lowestbars over prd to update swing highs (ph) and lows (pl), plus their bar indices (phL, plL).

Regime logic: If phL > plL → bullish regime; else → bearish regime. A change in this condition triggers a re-anchor of the VWAP at the newest pivot.

Adaptive VWAP math: APT is converted to an exponential decay factor ( alphaFromAPT ), then applied to running sums of price×volume and volume, producing the current VWAP estimate.

Rendering: Each pivot-anchored VWAP segment is drawn as a polyline and color-coded by regime. Optional structure labels (HH/HL/LH/LL) annotate the swing character.

Orders: On bullish flips, strategy.entry("L") opens/maintains a long; on bearish flips, strategy.close("L") exits.

Inputs & controls

Swing Period (prd) — Higher values identify larger, slower swings; lower values catch more frequent pivots but add noise.

Adaptive Price Tracking (APT) — Governs the VWAP’s “half-life.” Smaller APT → faster/closer to price; larger APT → smoother/stabler.

Adapt APT by ATR ratio — When enabled, APT scales with volatility so the VWAP speeds up in turbulent markets and slows down in quiet markets.

Volatility Bias — Tunes the strength of APT’s response to volatility (above 1 = stronger effect; below 1 = milder).

Style settings — Colors for swing labels and VWAP segments, plus line width for visibility.

Trade logic summary

Entry: Long when the swing structure turns bullish (latest swing low is more recent than the last swing high).

Exit: Close the long when structure turns bearish.

Position size: qty = strategy.equity / close × 5 (dynamic sizing; scales with account equity and instrument price). Consider reducing the multiplier for a more conservative profile.

Recommended workflow

Apply to instruments with reliable volume (equities, futures, crypto; FX tick volume can work but varies by broker).

Start on your preferred timeframe. Intraday often benefits from smaller APT (more reactive); higher timeframes may prefer larger APT (smoother).

Begin with defaults ( prd=50, APT=20 ); then toggle “Adapt by ATR” and vary Volatility Bias to observe how segments tighten/loosen.

Use Bar Replay to watch how pivots confirm and how the strategy re-anchors VWAP at those confirmations.

Layer your own risk rules (stops/targets, max position cap, session filters) before any discretionary use.

Practical tips

Context filter: Consider combining with a higher-timeframe bias (e.g., daily trend) and using this strategy as an entry timing layer.

First pivot preference: Some traders prefer only the first bullish pivot after a bearish regime (and vice versa) to reduce whipsaw in choppy ranges.

Deviations: You can add VWAP deviation bands to pre-plan partial exits or re-entries on mean-reversion pulls.

Sessions: Session-based filters (RTH vs. ETH) can materially change behavior on futures and equities.

Extending the script (ideas)

Add stops/targets (e.g., ATR stop below last swing low; partial profits at k×VWAP deviation).

Introduce mirrored short logic for two-sided testing.

Include alert conditions for regime flips or for price-VWAP interactions.

Incorporate HTF confirmation (e.g., only long when daily VWAP slope ≥ 0).

Throttle entries (e.g., once per regime flip) to avoid over-trading in ranges.

Known limitations

Repainting: Swing labels and pivot confirmations depend on future bars; historical labels can look “perfect.” Treat them as annotations, not executable signals.

Execution realism: Strategy includes commission and slippage fields, yet actual fills differ by venue/liquidity.

No guarantees: Past behavior does not imply future results. This publication is for research/education only and not financial advice.

Defaults (backtest environment)

Initial capital: 10,000

Commission value: 0.01

Slippage: 1

Overlay: true

Max bars back: 5000; Max labels/polylines set for deep swing histories

Quick checklist

Add to chart and verify that the instrument has volume.

Use defaults, then tune APT and Volatility Bias with/without ATR adaptation.

Observe how each pivot re-anchors VWAP and how regime flips drive entries/exits.

Paper trade across several symbols/timeframes before any discretionary decisions.

Attribution & license

Original indicator concept and logic: Zeiierman — please credit the author.

Strategy wrapper and publication: PineIndicators .

License: CC BY-NC-SA 4.0 (Attribution-NonCommercial-ShareAlike). Respect the license when forking or publishing derivatives.

Intraday Alpha Pro - ORB + Trend/MomentumOverview

This is a pure intraday trading strategy designed for active traders seeking to capitalize on short-term price movements using two complementary modules: Opening Range Breakout (ORB) and Trend/Momentum. The strategy operates strictly within a user-defined trading session, automatically flattening all positions at session end to avoid overnight carry. It employs a points-based exit system with a trailing stop that activates only after the target is reached, ensuring disciplined risk management. Optional Martingale position sizing is included for users who prefer aggressive scaling after losses.Key Features Pure Intraday, No Carry: Trades are confined to a user-defined session (default: 9:15 AM–3:25 PM, Monday–Sunday). All positions are closed at session end.

Non-Repainting: Entries are evaluated only on confirmed bar closes (barstate.isconfirmed), ensuring no lookahead or repainting.

Dual Signal Modules: Opening Range Breakout (ORB): Captures breakouts above/below the high/low of a user-defined opening range (default: 9:15 AM–9:30 AM).

Trend/Momentum: Combines EMA (9/21) crossovers, RSI filters, volume confirmation, and an optional 200-period MA trend filter for robust trend-following signals.

Points-Based Exits: Uses fixed stop-loss (slPoints, default 16 points) and take-profit (tpPoints, default 32 points) distances. Once the take-profit level is reached, a trailing stop (trailDistPts, default 10 points) activates, ratcheting monotonically to lock in gains.

Martingale Sizing (Optional): Allows position size increases after losses (up to maxQtyInput) with a reset option after wins.

Cooldown Period: Prevents immediate re-entries after exits using a configurable cooldown (cooldownBars).

Flexible Inputs: Toggle long/short entries, enable/disable ORB or Trend/Momentum modules, and customize all parameters (e.g., MA lengths, RSI thresholds, volume multiplier).

Visuals & Alerts: Plots ORB high/low lines and moving averages (9, 21, 200). Includes alerts for long/short entries and end-of-day flattening.

How It Works Session Management: Trades only within the specified tradeSes (default: 9:15 AM–3:25 PM). The ORB module uses a separate orbSes (default: 9:15 AM–9:30 AM) to calculate breakout levels. Positions are closed automatically at session end.

Entry Conditions: ORB: Long when price closes above the ORB high after the ORB session ends; short when price closes below the ORB low.

Trend/Momentum: Long on fast MA (default EMA 9) crossing above slow MA (default EMA 21), with RSI above rsiBuy (default 55), volume exceeding volMult (default 1.5x prior bar), and price above the 200-period MA (if enabled). Shorts use the inverse.

Exit Logic: Stop-loss is set at entry price ± slPoints.

Take-profit is monitored using a running high/low since entry. Once price moves tpPoints in profit, the stop trails at trailDistPts behind the current price, adjusting only in the favorable direction (never loosening).

Exits use strategy.exit with stop only (no limit orders).

Position Sizing: Default size is baseQtyInput (minimum 1 contract). With useMartingale enabled, size increases by martingaleFactor after a loss, capped at maxQtyInput. If resetOnWin is true, size resets to baseQtyInput after a winning trade.

Cooldown: After an exit, no new trades are allowed for cooldownBars to prevent overtrading.

Futures-Safe Volume: Volume filter accommodates markets with missing or zero volume data (e.g., futures), ensuring signals aren’t blocked unnecessarily.

Inputs Trading Session: tradeSes (e.g., "0915-1525:1234567") and orbSes (e.g., "0915-0930:1234567").

Toggles: enableLong, enableShort, useORB, useTrendMom, useTrendFilter (200-MA).

Trend/Momentum: maType (EMA/SMA), fastLen (9), slowLen (21), trendLen (200), rsiLen (14), rsiBuy (55), rsiSell (45), volMult (1.5).

Exits: slPoints (16), tpPoints (32), trailDistPts (10).

Martingale: useMartingale, baseQtyInput, maxQtyInput, martingaleFactor, resetOnWin.

Cooldown: cooldownBars (1).

Legacy (Ignored): tp1RR, tp2RR, tp3RR, tp1Pct, tp2Pct, tp3Pct, stepTrail for backward compatibility.

Usage Notes Best suited for liquid, intraday markets (e.g., futures like ES, NQ, or forex pairs).

Adjust slPoints, tpPoints, and trailDistPts to match instrument volatility.

Use useMartingale cautiously, as it increases risk after losses.

Ensure tradeSes and orbSes align with your market’s trading hours.

Alerts can be set for long/short entries and EOD flattening.

The strategy avoids lookahead and repainting, ensuring reliability in live trading.

Risk Warning

Trading involves significant risk. Backtest thoroughly and use appropriate risk management. The Martingale option can amplify losses if not carefully monitored. Past performance is not indicative of future results.

Auction Market Theory: Value Area & VWAP Fade - DashboardAn "Auction Market Theory" dashboard is a visual summary of the market's state according to the principles of Auction Market Theory. It consolidates key metrics like the Value Area (VA), Point of Control (POC), and Volume-Weighted Average Price (VWAP) into a single, easy-to-read panel on your chart.

What a Dashboard Shows

The purpose of the dashboard is to give traders a quick, real-time snapshot of the market's auction process. It helps you answer critical questions like:

Where is the market's "fair value"? This is shown by the Value Area (VA) range.

Where is the most volume concentrated? This is the Point of Control (POC), the price that acts as a gravitational center.

How are market participants currently positioned? The VWAP provides a measure of the average price paid, weighted by volume. Price trading above VWAP suggests a bullish volume bias, while price below suggests a bearish bias.

Is the market in a state of balance or imbalance? The relationship between the current price and these key levels helps to quickly determine if the market is accepting a price range (balance) or rejecting it (imbalance/trend).

How to Interpret the Dashboard

Value Area (VA) & Point of Control (POC)

These metrics are derived from a volume profile and are the foundation of the auction theory dashboard. The dashboard displays the VA's low and high, as well as the POC. These levels define the market's "accepted" price range for a given period.

VWAP

VWAP acts as a real-time moving average that is more responsive to volume than a standard moving average. It's often used as an intraday anchor. When price is significantly stretched from the VWAP (and its standard deviation bands), it's a signal of a potential over-extension and a target for a mean-reversion trade.

Dashboard's Role in Trading

The dashboard is not an entry signal itself, but a contextual tool. It provides the framework for your trading decisions. For a "fade the edge" strategy, you would use the dashboard to:

Identify the edges: See the exact price levels of the VA and VWAP bands.

Wait for the stretch: Look for price to move beyond those edges.

Confirm the reversal: Only then would you look at other indicators (like RSI or volume spikes) for an entry signal.

Manage the trade: Use the POC as a potential take-profit target, as price has a high probability of returning to this point of volume consensus.

RCI 2 Dashboards ✅ Strategy: RCI 2 Dashboards BY Sonu JAIN

This advanced strategy is built around the Rank Correlation Index (RCI), a unique momentum oscillator, and combines it with a comprehensive suite of powerful indicators to identify high-probability trading opportunities. The strategy’s core strength lies in its ability to filter signals using up to 12 different conditions for both long and short trades.

To make the decision-making process clear and intuitive, the strategy features two dynamic, customizable dashboards right on your chart. The first dashboard gives you a live, detailed breakdown of which conditions are met, while the second provides a real-time overview of the strategy’s performance.

How It Works

The strategy generates entry signals based on RCI crossovers and crossunders. These signals are then filtered by a customizable combination of other indicators to confirm the trade.

Long Entry:

The RCI crosses over its moving average.

All enabled long-side filters are met.

Short Entry:

The RCI crosses under its moving average.

All enabled short-side filters are met.

Key Features

RCI Crossover Logic: The core of the strategy is an RCI crossover/crossunder with a customizable moving average (MA). You can choose from SMA, EMA, SMMA (RMA), WMA, or VWMA.

12 Optional Filters: This strategy goes far beyond a simple RCI signal. You can enable or disable a wide range of filters to refine your entries. These include:

Trend: Supertrend, Parabolic SAR (SAR), and Vortex Indicator.

Volatility: Keltner Channels (KC) and Bollinger Bands (BB).

Momentum: Woodies CCI, Money Flow Index (MFI), and Relative Strength Index (RSI).

Volume: On-Balance Volume (OBV) and simple Volume analysis.

Directional Strength: Average Directional Index (ADX).

Timing: A time-of-day filter to trade only during specific market hours.

Dual Dashboards:

Detailed Condition Dashboard: This dashboard shows you exactly which of the 12 filters are currently met with a simple ✓ or ✗. This provides instant clarity on why a trade is or isn't being considered.

Performance Dashboard: This dashboard displays key performance metrics in real-time, including net profit, win rate, profit factor, max drawdown, and current/max winning and losing streaks. It also provides details on the most recent trade, such as entry, stop-loss, and exit prices.

Customizable Stop Loss: The strategy includes a fixed percentage-based stop loss for both long and short positions, which you can easily configure in the settings.

Trade Direction Control: You can choose to trade "Long Only," "Short Only," or "Long & Short," giving you complete control over your trading bias.

This strategy is a powerful tool for traders who want to build a robust, multi-filtered system. The included dashboards make it an excellent educational tool for understanding how different indicators work together to form a complete trading plan. You can use it to backtest and optimize your own unique combination of indicators to find the perfect setup for your market and timeframe.

DVPOOverview

The DVPO (Dynamic Volume Profile Oscillator) Strategy is a comprehensive and highly customizable trading tool designed for precision and control. It is built around a unique, volume-driven oscillator that identifies potential market entries by analyzing the relationship between price, volume, and volatility.

This strategy is not just another signal generator; it's a complete framework that includes dynamic entry logic, adaptive risk management (ATR Stop Loss and R:R-based Take Profit), and a powerful dashboard of 10+ optional confirmation filters to help you tailor the strategy to your specific instrument, timeframe, and trading style.

The Core Concept: The DVPO Oscillator

The heart of this strategy is the DVPO oscillator. Unlike standard oscillators like RSI or Stochastics, the DVPO's primary goal is to quantify how far the current price has deviated from its recent volume-weighted "fair value."

Here’s how it works conceptually:

Micro Volume Profile: The indicator first analyzes a recent period of bars (defined by Lookback Period) to build a mini-profile of price and volume.

Volume-Weighted Mean: From this profile, it calculates a volume-weighted average price (VWAP) and the average deviation from that mean. This establishes the central point of value for the recent period.

Deviation Measurement: The oscillator's value is derived from how far the current price is from this calculated mean, scaled by the observed price deviation and a user-defined Sensitivity. A value above the midline suggests the price is trading at a premium, while a value below suggests it's at a discount.

Adaptive Volatility Zones: Instead of using fixed overbought/oversold levels (e.g., 70/30), the DVPO calculates dynamic upper and lower zones using the standard deviation of the oscillator itself. These zones expand and contract based on recent market volatility.

An entry signal is triggered not just when the oscillator is "overbought" or "oversold," but when it breaks out of these adaptive volatility zones, signaling that a statistically significant price movement is underway.

📈 Long Entry Condition : The oscillator crosses above the dynamic upper zone.

📉 Short Entry Condition : The oscillator crosses below the dynamic lower zone.

Integrated Risk & Trade Management

A signal is useless without proper risk management. This strategy has professional-grade risk management built directly into its logic.

Stop Loss (ATR-Based): The Stop Loss is not a fixed percentage. It is calculated using the Average True Range (ATR), allowing it to adapt automatically to the market's current volatility. In volatile periods, the stop will be wider; in quiet periods, it will be tighter.

Take Profit (Risk/Reward Ratio): The Take Profit level is calculated based on a user-defined Risk/Reward Ratio. If you set a ratio of 2.0, the Take Profit target will be placed at twice the distance of the Stop Loss from your entry price.

Dynamic Position Sizing: The strategy can automatically calculate the trade quantity for you. It determines the position size based on your specified Capital Size and the % Risk Per Trade you are willing to accept, ensuring disciplined risk control on every trade.

The Filter Dashboard : Enhance Your Signal Quality

To help reduce false signals and adapt to different market conditions, the strategy includes a comprehensive dashboard of optional confirmation filters. An entry signal will only be executed if it aligns with all the filters you have activated.

Trend & Momentum Filters :

T3, VMA, & VWAP Trend Filters: Utilize a suite of advanced moving averages (T3, Variable Moving Average, and a session-based VWAP) to ensure your trades are aligned with the dominant trend.

ADX Filter: Confirms that the market has sufficient directional strength for a trend-following trade, helping to avoid entries during choppy conditions.

Kaufman Efficiency Filter: Uses the Kaufman Efficiency Ratio to measure market noise. It only allows trades when the market is trending efficiently.

Volume & Market State Filters :

Volume Flow (VFI): A sophisticated volume-based filter that confirms whether volume is supporting the price move.

TDFI (Trader's Dynamic Index): A market state indicator designed to identify when the market is primed for a strong, directional move.

Flat Market Detector: A unique filter that identifies and avoids trading in sideways or ranging markets where trend strategies typically underperform.

Trade Condition Filters :

Min TP / Max SL %: Filter out trades where the risk/reward profile doesn't meet your minimum requirements (e.g., ignore a trade if the ATR-based stop loss is more than 10% away from the price).

Session Filters: Allows you to enable or disable trading on specific days of the week and to set a Cooldown Period (a set number of bars to wait after a trade closes before looking for a new entry).

How To Use This Strategy

Start with the Core: Begin by configuring the DVPO Oscillator settings (Lookback Period, Sensitivity, Zone Width) and your Risk Management parameters (ATR Multiplier, RR Ratio, % Risk Per Trade). These form the foundation of the strategy.

Backtest and Observe: Use TradingView's Strategy Tester to see how the core signals perform on your chosen asset and timeframe.

Layer Filters Intelligently: Enable the confirmation filters one by one and re-run your backtest. Observe how each filter impacts performance (e.g., does the T3 filter increase profitability but reduce the number of trades?). The goal is to find the optimal balance between signal quality and frequency.

Visualize and Analyze: Use the Show Risk/Reward Area option to plot your entry, stop loss, and take profit levels directly on the chart for every trade, providing a clear visual representation of your trade plan.