TRADING VIEW INDICATOR - PINE TUTORIAL 5After a long gap, I have written the 5th tutorial for the pine script. You can find the others below, if you read through all of these you should be good to do your own writing.

This script mimics the Trading View Indicator . For example this one below.

www.tradingview.com

It shows the net result of the 28 indicator, either as buy or sell. I have worked hard to make sure it matches the trading view results but I am not in hundred percent agreement with tradingView on SMA, EMA and Ichimoku indicator.

There are many commented plots because I needed to check separately if each indicator is working correctly.

Someone else wrote this code but they did not make it public. It took me about 3 weeks to write this and to be honest it could be cleaner and better commented.

If you find any mistake please let me know. I hope it will be useful in your learning.

Buscar en scripts para "technical"

Indicators: MMA and 3 oscillatorsGuppy Multiple Moving Averages

---------------------------------

Developed by Daryl Guppy, the basic idea of Multiple moving average(MMA) is to view the trend as two band of moving averages – short term band and long term band.

Shortterm averages capture the inferred behaviour of traders and long term represents the investors. Uses fractal repetition to identify points of agreement and disagreement which precede significant trend changes.

Short intro on interpreting the signals:

drive.google.com

More info:

www.guppytraders.com

Guppy Oscillator

---------------------------------

The Guppy MMA Oscillator, developed by Leon Wilson, is an oscillator representation of difference between GMMA ribbons. Look for signal crosses for the triggers.

Linda Raschke (3/10) Oscillator

---------------------------------

This oscillator is similar to having a MACD of (3,10,16), the nuances are explained by Linda Raschke in her manual "Professional Trading Techniques":

www.lbrgroup.com

Ian Oscillator

---------------------------------

Simple EMA difference converted to an oscillator. Use the signal crosses as triggers.

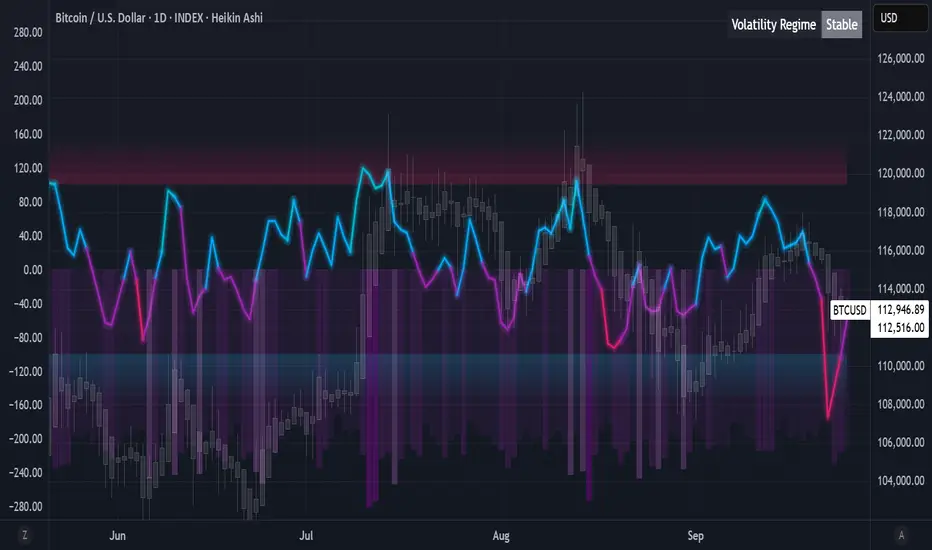

Algorithmic Value Oscillator [CRYPTIK1]Algorithmic Value Oscillator

Introduction: What is the AVO? Welcome to the Algorithmic Value Oscillator (AVO), a powerful, modern momentum indicator that reframes the classic "overbought" and "oversold" concept. Instead of relying on a fixed lookback period like a standard RSI, the AVO measures the current price relative to a significant, higher-timeframe Value Zone .

This gives you a more contextual and structural understanding of price. The core question it answers is not just "Is the price moving up or down quickly?" but rather, " Where is the current price in relation to its recently established area of value? "

This allows traders to identify true "premium" (overbought) and "discount" (oversold) levels with greater accuracy, all presented with a clean, futuristic aesthetic designed for the modern trader.

The Core Concept: Price vs. Value The market is constantly trying to find equilibrium. The AVO is built on the principle that the high and low of a significant prior period (like the previous day or week) create a powerful area of perceived value.

The Value Zone: The range between the high and low of the selected higher timeframe.

Premium Territory (Distribution Zone): When the oscillator moves into the glowing pink/purple zone above +100, it is trading at a premium.

Discount Territory (Accumulation Zone): When the oscillator moves into the glowing teal/blue zone below -100, it is trading at a discount.

Key Features

1. Glowing Gradient Oscillator: The main oscillator line is a dynamic visual guide to momentum.

The line changes color smoothly from light blue to neon teal as bullish momentum increases.

It shifts from hot pink to bright purple as bearish momentum increases.

Multiple transparent layers create a professional "glow" effect, making the trend easy to see at a glance.

2. Dynamic Volatility Histogram: This histogram at the bottom of the indicator is a custom volatility meter. It has been engineered to be adaptive, ensuring that the visual differences between high and low volatility are always clear and dramatic, no matter your zoom level. It uses a multi-color gradient to visualize the intensity of market volatility.

3. Volatility Regime Dashboard: This simple on-screen table analyzes the histogram and provides a clear, one-word summary of the current market state: Compressing, Stable, or Expanding.

How to Use the AVO: Trading Strategies

1. Reversion Trading This is the most direct way to use the indicator.

Look for Buys: When the AVO line drops into the teal "Accumulation Zone" (below -100), the price is trading at a discount. Watch for the oscillator to form a bottom and start turning up as a signal that buying pressure is returning.

Look for Sells: When the AVO line moves into the pink "Distribution Zone" (above +100), the price is trading at a premium. Watch for the oscillator to form a peak and start turning down as a signal that selling pressure is increasing.

2. Best Practices & Settings

Timeframe Synergy: The AVO is most effective when your chart timeframe is lower than your selected "Value Zone Source." For example, if you trade on the 1-hour chart, set your Value Zone to "Previous Day."

Confirmation is Key: This indicator provides powerful context, but it should not be used in isolation. Always combine its readings with your primary analysis, such as market structure and support/resistance levels.

Smart Money Precision Structure [BullByte]Smart Money Precision Structure

Advanced Market Structure Analysis Using Institutional Order Flow Concepts

---

OVERVIEW

Smart Money Precision Structure (SMPS) is a comprehensive market analysis indicator that combines six analytical frameworks to identify high-probability market structure patterns. The indicator uses multi-dimensional scoring algorithms to evaluate market conditions through institutional order flow concepts, providing traders with professional-grade market analysis.

---

PURPOSE AND ORIGINALITY

Why This Indicator Was Developed

• Addresses the gap between retail and institutional analysis methods

• Consolidates multiple analysis techniques that professionals use separately

• Automates complex market structure evaluation into actionable insights

• Eliminates the need for multiple indicators by providing comprehensive analysis

What Makes SMPS Original

• Six-Layer Confluence System - Unique combination of market regime, structure, volume flow, momentum, price action, and adaptive filtering

• Institutional Pattern Recognition - Identifies smart money accumulation and distribution patterns

• Adaptive Intelligence - Parameters automatically adjust based on detected market conditions

• Real-Time Market Scoring - Proprietary algorithm rates market quality from 0-100%

• Structure Break Detection - Advanced pivot analysis identifies trend reversals early

---

HOW IT WORKS - TECHNICAL METHODOLOGY

1. Market Regime Analysis Engine

The indicator evaluates five core market dimensions:

• Volatility Score - Measures current volatility against 50-period historical baseline

• Trend Score - Analyzes alignment between 8, 21, and 50-period EMAs

• Momentum Score - Combines RSI divergence with MACD signal alignment

• Structure Score - Evaluates pivot point formation clarity

• Efficiency Score - Calculates directional movement efficiency ratio

These scores combine to classify markets into five regimes:

• TRENDING - Strong directional movement with aligned indicators

• RANGING - Sideways movement with mixed directional signals

• VOLATILE - Elevated volatility with unpredictable price swings

• QUIET - Low volatility consolidation periods

• TRANSITIONAL - Market shifting between different regimes

2. Market Structure Analysis

Advanced pivot point analysis identifies:

• Higher Highs and Higher Lows for bullish structure

• Lower Highs and Lower Lows for bearish structure

• Structure breaks when established patterns fail

• Dynamic support and resistance from recent pivot points

• Key level proximity detection using ATR-based buffers

3. Volume Flow Decoding

Institutional activity detection through:

• Volume surge identification when volume exceeds 2x average

• Buy versus sell pressure analysis using price-volume correlation

• Flow strength measurement through directional volume consistency

• Divergence detection between volume and price movements

• Institutional threshold alerts when unusual volume patterns emerge

4. Multi-Period Momentum Synthesis

Weighted momentum calculation across four timeframes:

• 1-period momentum weighted at 40%

• 3-period momentum weighted at 30%

• 5-period momentum weighted at 20%

• 8-period momentum weighted at 10%

Result smoothed with 6-period EMA for noise reduction.

5. Price Action Quality Assessment

Each bar evaluated for:

• Range quality relative to 20-period average

• Body-to-range ratio for directional conviction

• Wick analysis for rejection pattern identification

• Pattern recognition including engulfing and hammer formations

• Sequential price movement analysis

6. Adaptive Parameter System

Parameters automatically adjust based on detected regime:

• Trending markets reduce sensitivity and confirmation requirements

• Volatile markets increase filtering and require additional confirmations

• Ranging markets maintain neutral settings

• Transitional markets use moderate adjustments

---

COMPLETE SETTINGS GUIDE

Section 1: Core Analysis Settings

Analysis Sensitivity (0.3-2.0)

• Default: 1.0

• Lower values require stronger price movements

• Higher values detect more subtle patterns

• Scalpers use 0.8-1.2, swing traders use 1.5-2.0

Noise Reduction Level (2-7)

• Default: 4

• Controls filtering of false patterns

• Higher values reduce pattern frequency

• Increase in volatile markets

Minimum Move % (0.05-0.50)

• Default: 0.15%

• Sets minimum price movement threshold

• Adjust based on instrument volatility

• Forex: 0.05-0.10%, Stocks: 0.15-0.25%, Crypto: 0.20-0.50%

High Confirmation Mode

• Default: True (Enabled)

• Requires all technical conditions to align

• Reduces frequency but increases reliability

• Disable for more aggressive pattern detection

Section 2: Market Regime Detection

Enable Regime Analysis

• Default: True (Enabled)

• Activates market environment evaluation

• Essential for adaptive features

• Keep enabled for best results

Regime Analysis Period (20-100)

• Default: 50 bars

• Determines regime calculation lookback

• Shorter for responsive, longer for stable

• Scalping: 20-30, Swing: 75-100

Minimum Market Clarity (0.2-0.8)

• Default: 0.4

• Quality threshold for pattern generation

• Higher values require clearer conditions

• Lower for more patterns, higher for quality

Adaptive Parameter Adjustment

• Default: True (Enabled)

• Enables automatic parameter optimization

• Adjusts based on market regime

• Highly recommended to keep enabled

Section 3: Market Structure Analysis

Enable Structure Validation

• Default: True (Enabled)

• Validates patterns against support/resistance

• Confirms trend structure alignment

• Essential for reliability

Structure Analysis Period (15-50)

• Default: 30 bars

• Period for structure pattern analysis

• Affects support/resistance calculation

• Match to your trading timeframe

Minimum Structure Alignment (0.3-0.8)

• Default: 0.5

• Required structure score for valid patterns

• Higher values need stronger structure

• Balance with desired frequency

Section 4: Analysis Configuration

Minimum Strength Level (3-5)

• Default: 4

• Minimum confirmations for pattern display

• 5 = Maximum reliability, 3 = More patterns

• Beginners should use 4-5

Required Technical Confirmations (4-6)

• Default: 5

• Number of aligned technical factors

• Higher = fewer but better patterns

• Works with High Confirmation Mode

Pattern Separation (3-20 bars)

• Default: 8 bars

• Minimum bars between patterns

• Prevents clustering and overtrading

• Increase for cleaner charts

Section 5: Technical Filters

Momentum Validation

• Default: True (Enabled)

• Requires momentum alignment

• Filters counter-trend patterns

• Essential for trend following

Volume Confluence Analysis

• Default: True (Enabled)

• Requires volume confirmation

• Identifies institutional participation

• Critical for reliability

Trend Direction Filter

• Default: True (Enabled)

• Only shows patterns with trend

• Reduces counter-trend signals

• Disable for reversal hunting

Section 6: Volume Flow Analysis

Institutional Activity Threshold (1.2-3.5)

• Default: 2.0

• Multiplier for unusual volume detection

• Lower finds more institutional activity

• Stock: 2.0-2.5, Forex: 1.5-2.0, Crypto: 2.5-3.5

Volume Surge Multiplier (1.8-4.5)

• Default: 2.5

• Defines significant volume increases

• Adjust per instrument characteristics

• Higher for stocks, lower for forex

Volume Flow Period (12-35)

• Default: 18 bars

• Smoothing for volume analysis

• Shorter = responsive, longer = smooth

• Match to timeframe used

Section 7: Analysis Frequency Control

Maximum Analysis Points Per Hour (1-5)

• Default: 3

• Limits pattern frequency

• Prevents overtrading

• Scalpers: 4-5, Swing traders: 1-2

Section 8: Target Level Configuration

Target Calculation Method

• Default: Market Adaptive

• Three modes available:

- Fixed: Uses set point distances

- Dynamic: ATR-based calculations

- Market Adaptive: Structure-based levels

Minimum Target/Risk Ratio (1.0-3.0)

• Default: 1.5

• Minimum acceptable reward vs risk

• Higher filters lower probability setups

• Professional standard: 1.5-2.0

Fixed Mode Settings:

• Fixed Target Distance: 50 points default

• Fixed Invalidation Distance: 30 points default

• Use for consistent instruments

Dynamic Mode Settings:

• Dynamic Target Multiplier: 1.8x ATR default

• Dynamic Invalidation Multiplier: 1.0x ATR default

• Adapts to volatility automatically

Market Adaptive Settings:

• Use Structure Levels: True (default)

• Structure Level Buffer: 0.1% default

• Places levels at actual support/resistance

Section 9: Visual Display Settings

Color Theme Options

• Professional (Teal/Red)

- Bullish: Teal (#26a69a)

- Bearish: Red (#ef5350)

- Neutral: Gray (#78909c)

- Best for: Traditional traders, clean appearance

• Dark (Neon Green/Pink)

- Bullish: Neon Green (#00ff88)

- Bearish: Hot Pink (#ff0044)

- Neutral: Dark Gray (#333333)

- Best for: Dark theme users, high contrast

• Light (Green/Red Classic)

- Bullish: Green (#4caf50)

- Bearish: Red (#f44336)

- Neutral: Light Gray (#9e9e9e)

- Best for: Light backgrounds, traditional colors

• Vibrant (Cyan/Magenta)

- Bullish: Cyan (#00ffff)

- Bearish: Magenta (#ff00ff)

- Neutral: Medium Gray (#888888)

- Best for: High visibility, modern appearance

Dashboard Position

• Options: Top Left, Top Right, Bottom Left, Bottom Right, Middle Left, Middle Right

• Default: Top Right

• Choose based on chart layout preference

Dashboard Size

• Full: Complete information display (desktop)

• Mobile: Compact view for small screens

• Default: Full

Analysis Display Style

• Arrows : Simple directional markers

• Labels : Detailed text information

• Zones : Colored areas showing pattern regions

• Default: Labels (most informative)

Display Options:

• Display Analysis Strength: Shows star rating

• Display Target Levels: Shows target/invalidation lines

• Display Market Regime: Shows regime in pattern labels

---

HOW TO USE SMPS - DETAILED GUIDE

Understanding the Dashboard

Top Row - Header

• SMPS Dashboard title

• VALUE column: Current readings

• STATUS column: Condition assessments

Market Regime Row

• Shows: TRENDING, RANGING, VOLATILE, QUIET, or TRANSITIONAL

• Color coding: Green = Favorable, Red = Caution

• Status: FAVORABLE or CAUTION trading conditions

Market Score Row

• Percentage from 0-100%

• Above 60% = Strong conditions

• 40-60% = Moderate conditions

• Below 40% = Weak conditions

Structure Row

• Direction: BULLISH, BEARISH, or NEUTRAL

• Status: INTACT or BREAK

• Orange BREAK indicates structure failure

Volume Flow Row

• Direction: BUYING or SELLING

• Intensity: STRONG or WEAK

• Color indicates dominant pressure

Momentum Row

• Numerical momentum value

• Positive = Upward pressure

• Negative = Downward pressure

Volume Status Row

• INST = Institutional activity detected

• HIGH = Above average volume

• NORM = Normal volume levels

Adaptive Mode Row

• ACTIVE = Parameters adjusting

• STATIC = Fixed parameters

• Shows required confirmations

Analysis Level Row

• Minimum strength level setting

• Pattern separation in bars

Market State Row

• Current analysis: BULLISH, BEARISH, NEUTRAL

• Shows analysis price level when active

T:R Ratio Row

• Current target to risk ratio

• GOOD = Meets minimum requirement

• LOW = Below minimum threshold

Strength Row

• BULL or BEAR dominance

• Numerical strength value 0-100

Price Row

• Current price

• Percentage change

Last Analysis Row

• Previous pattern direction

• Bars since last pattern

Reading Pattern Signals

Bullish Structure Pattern

• Upward triangle or "Bullish Structure" label

• Star rating shows strength (★★★★★ = strongest)

• Green line = potential target level

• Red dashed line = invalidation level

• Appears below price bars

Bearish Structure Pattern

• Downward triangle or "Bearish Structure" label

• Star rating indicates reliability

• Green line = potential target level

• Red dashed line = invalidation level

• Appears above price bars

Pattern Strength Interpretation

• ★★★★★ = 6 confirmations (exceptional)

• ★★★★☆ = 5 confirmations (strong)

• ★★★☆☆ = 4 confirmations (moderate)

• ★★☆☆☆ = 3 confirmations (minimum)

• Below minimum = filtered out

Visual Elements on Chart

Lines and Levels:

• Gray Line = 21 EMA trend reference

• Green Stepline = Dynamic support level

• Red Stepline = Dynamic resistance level

• Green Solid Line = Active target level

• Red Dashed Line = Active invalidation level

Pattern Markers:

• Triangles = Arrow display mode

• Text Labels = Label display mode

• Colored Boxes = Zone display mode

Target Completion Labels:

• "Target" = Price reached target level

• "Invalid" = Pattern invalidated by price

---

RECOMMENDED USAGE BY TIMEFRAME

1-Minute Charts (Scalping)

• Sensitivity: 0.8-1.2

• Noise Reduction: 3-4

• Pattern Separation: 3-5 bars

• High Confirmation: Optional

• Best for: Quick intraday moves

5-Minute Charts (Precision Intraday)

• Sensitivity: 1.0 (default)

• Noise Reduction: 4 (default)

• Pattern Separation: 8 bars

• High Confirmation: Enabled

• Best for: Day trading

15-Minute Charts (Short Swing)

• Sensitivity: 1.0-1.5

• Noise Reduction: 4-5

• Pattern Separation: 10-12 bars

• High Confirmation: Enabled

• Best for: Intraday swings

30-Minute to 1-Hour (Position Trading)

• Sensitivity: 1.5-2.0

• Noise Reduction: 5-7

• Pattern Separation: 15-20 bars

• Regime Period: 75-100

• Best for: Multi-day positions

Daily Charts (Swing Trading)

• Sensitivity: 1.8-2.0

• Noise Reduction: 6-7

• Pattern Separation: 20 bars

• All filters enabled

• Best for: Long-term analysis

---

MARKET-SPECIFIC SETTINGS

Forex Pairs

• Minimum Move: 0.05-0.10%

• Institutional Threshold: 1.5-2.0

• Volume Surge: 1.8-2.2

• Target Mode: Dynamic or Market Adaptive

Stock Indices (ES, NQ, YM)

• Minimum Move: 0.10-0.15%

• Institutional Threshold: 2.0-2.5

• Volume Surge: 2.5-3.0

• Target Mode: Market Adaptive

Individual Stocks

• Minimum Move: 0.15-0.25%

• Institutional Threshold: 2.0-2.5

• Volume Surge: 2.5-3.5

• Target Mode: Dynamic

Cryptocurrency

• Minimum Move: 0.20-0.50%

• Institutional Threshold: 2.5-3.5

• Volume Surge: 3.0-4.5

• Target Mode: Dynamic

• Increase noise reduction

---

PRACTICAL APPLICATION EXAMPLES

Example 1: Strong Trending Market

Dashboard Reading:

• Market Regime: TRENDING

• Market Score: 75%

• Structure: BULLISH, INTACT

• Volume Flow: BUYING, STRONG

• Momentum: +0.45

Interpretation:

• Strong uptrend environment

• Institutional buying present

• Look for bullish patterns as continuation

• Higher probability of success

• Consider using lower sensitivity

Example 2: Range-Bound Conditions

Dashboard Reading:

• Market Regime: RANGING

• Market Score: 35%

• Structure: NEUTRAL

• Volume Flow: SELLING, WEAK

• Momentum: -0.05

Interpretation:

• No clear direction

• Low opportunity environment

• Patterns are less reliable

• Consider waiting for regime change

• Or switch to a range-trading approach

Example 3: Structure Break Alert

Dashboard Reading:

• Previous: BULLISH structure

• Current: Structure BREAK

• Volume: INST flag active

• Momentum: Shifting negative

Interpretation:

• Trend reversal potentially beginning

• Institutional participation detected

• Watch for bearish pattern confirmation

• Adjust bias accordingly

• Increase caution on long positions

Example 4: Volatile Market

Dashboard Reading:

• Market Regime: VOLATILE

• Market Score: 45%

• Adaptive Mode: ACTIVE

• Confirmations: Increased to 6

Interpretation:

• Choppy conditions

• Parameters auto-adjusted

• Fewer but higher quality patterns

• Wider stops may be needed

• Consider reducing position size

Below are a few chart examples of the Smart Money Precision Structure (SMPS) indicator in action.

• Example 1 – Bullish Structure Detection on SOLUSD 5m

• Example 2 – Bearish Structure Detected with Strong Confluence on SOLUSD 5m

---

TROUBLESHOOTING GUIDE

No Patterns Appearing

Check these settings:

• High Confirmation Mode may be too restrictive

• Minimum Strength Level may be too high

• Market Clarity threshold may be too high

• Regime filter may be blocking patterns

• Try increasing sensitivity

Too Many Patterns

Adjust these settings:

• Enable High Confirmation Mode

• Increase Minimum Strength Level to 5

• Increase Pattern Separation

• Reduce Sensitivity below 1.0

• Enable all technical filters

Dashboard Shows "CAUTION"

This indicates:

• Market conditions are unfavorable

• Regime is RANGING or QUIET

• Market score is low

• Consider waiting for better conditions

• Or adjust expectations accordingly

Patterns Not Reaching Targets

Consider:

• Market may be choppy

• Volatility may have changed

• Try Dynamic target mode

• Reduce target/risk ratio requirement

• Check if regime is VOLATILE

---

ALERTS CONFIGURATION

Alert Message Format

Alerts include:

• Pattern type (Bullish/Bearish)

• Strength rating

• Market regime

• Analysis price level

• Target and invalidation levels

• Strength percentage

• Target/Risk ratio

• Educational disclaimer

Setting Up Alerts

• Click Alert button on TradingView

• Select SMPS indicator

• Choose alert frequency

• Customize message if desired

• Alerts fire on pattern detection

---

DATA WINDOW INFORMATION

The Data Window displays:

• Market Regime Score (0-100)

• Market Structure Bias (-1 to +1)

• Bullish Strength (0-100)

• Bearish Strength (0-100)

• Bull Target/Risk Ratio

• Bear Target/Risk Ratio

• Relative Volume

• Momentum Value

• Volume Flow Strength

• Bull Confirmations Count

• Bear Confirmations Count

---

BEST PRACTICES AND TIPS

For Beginners

• Start with default settings

• Use High Confirmation Mode

• Focus on TRENDING regime only

• Paper trade first

• Learn one timeframe thoroughly

For Intermediate Users

• Experiment with sensitivity settings

• Try different target modes

• Use multiple timeframes

• Combine with price action analysis

• Track pattern success rate

For Advanced Users

• Customize per instrument

• Create setting templates

• Use regime information for bias

• Combine with other indicators

• Develop systematic rules

---

IMPORTANT DISCLAIMERS

• This indicator is for educational and informational purposes only

• Not financial advice or a trading system

• Past performance does not guarantee future results

• Trading involves substantial risk of loss

• Always use appropriate risk management

• Verify patterns with additional analysis

• The author is not a registered investment advisor

• No liability accepted for trading losses

---

VERSION NOTES

Version 1.0.0 - Initial Release

• Six-layer confluence system

• Adaptive parameter technology

• Institutional volume detection

• Market regime classification

• Structure break identification

• Real-time dashboard

• Multiple display modes

• Comprehensive settings

## My Final Thoughts

Smart Money Precision Structure represents an advanced approach to market analysis, bringing institutional-grade techniques to retail traders through intelligent automation and multi-dimensional evaluation. By combining six analytical frameworks with adaptive parameter adjustment, SMPS provides comprehensive market intelligence that single indicators cannot achieve.

The indicator serves as an educational tool for understanding how professional traders analyze markets, while providing practical pattern detection for those seeking to improve their technical analysis. Remember that all trading involves risk, and this tool should be used as part of a complete analysis approach, not as a standalone trading system.

- BullByte

Pasrsifal.RegressionTrendStateSummary

The Parsifal.Regression.Trend.State Indicator analyzes the leading coefficients of linear and quadratic regressions of price (against time). It also considers their first- and second-order changes. These features are aggregated into a Trend-State background, shown as a gradient color. In addition, the indicator generates fast and slow signals that can be used as potential entry- or exit triggers.

This tool is designed for advanced trend-following strategies, leveraging information from multiple trendline features.

Background

Trendlines provide insight into the state of a trend or the “trendiness” of a price process. While moving averages or pivot-based lines can serve as envelopes and breakout levels, they are often too lagging for swing traders, who need tools that adapt more closely to price swings, ideally using trendlines, around which the price process swings continuously.

Regression lines address this by cutting directly through the data, making them a natural anchor for observing how price winds around a central trendline within a chosen lookback period.

Regression Trendlines

• Linear Regression:

o Minimizes distance to all closing values over the lookback period.

o The slope represents the short-term linear trend.

o The change of slope indicates trend acceleration or deceleration.

o Linear regression lags during phases of rapid market shifts.

• Quadratic Regression:

o Fits a second-degree polynomial to minimize deviation from closing prices.

o The convexity term (leading coefficient) reflects curvature:

Positive convexity → accelerating uptrend or fading downtrend.

Negative convexity → accelerating downtrend or fading uptrend.

o The change of convexity detects early shifts in momentum and often reacts faster than slope features.

Features Extracted

The indicator evaluates six features:

• Linear features: slope, first derivative of slope, second derivative of slope.

• Quadratic features: convexity term, first derivative of the convexity term, second derivative of the convexity term.

• Linear features: capture broad, background trend behavior.

• Quadratic features: detect deviations, accelerations, and smaller-scale dynamics.

Quadratic terms generally react first to market changes, while linear terms provide stability and context.

Dynamics of Market Moves as seen by linear and quadratic regressions

• At the start of a rapid move:

The change of convexity reacts first, capturing the shift in dynamics before other features. The convexity term then follows, while linear slope features lag further behind. Because convexity measures deviation from linearity, it reflects accelerating momentum more effectively than slope.

• At the end of a rapid move:

Again, the change of convexity responds first to fading momentum, signaling the transition from above-linear to below-linear dynamics. Even while a strong trend persists, the change of convexity may flip sign early, offering a warning of weakening strength. The convexity term itself adjusts more slowly but may still turn before the price process does. Linear features lag the most, typically only flipping after price has already reversed, thereby smoothing out the rapid, more sensitive reactions of quadratic terms.

________________________________________

Parsifal Regression.Trend.State Method

1. Feature Mapping:

Each feature is mapped to a range between -1 and 1, preserving zero-crossings (critical for sign interpretation).

2. Aggregation:

A heuristic linear combination*) produces a background information value, visualized as a gradient color scale:

o Deep green → strong positive trend.

o Deep red → strong negative trend.

o Yellow → neutral or transitional states.

3. Signals:

o Fast signal (oscillator): ranges from -1 to 1, reflecting short-term trend state.

o Slow signal (smoothed): moving average of the fast signal.

o Their interactions (crossovers, zero-crossings) provide actionable trading triggers.

How to Use

The Trend-State background gradient provides intuitive visual feedback on the aggregated regression features (slope, convexity, and their changes). Because these features reflect not only current trend strength but also their acceleration or deceleration, the color transitions help anticipate evolving market states:

• Solid Green: All features near their highs. Indicates a strong, accelerating uptrend. May also reflect explosive or hyperbolic upside moves (including gaps).

• Fading Solid Green: A recently strong uptrend is losing momentum. Price may shift into a slower uptrend, consolidation, or even a reversal.

• Fading Green → Yellow: Often appears as a dirty yellow or a rapidly mixing pattern of green and red. Signals that the uptrend is weakening toward neutrality or beginning to turn negative.

• Yellow → Deepening Red: Two possible scenarios:

o Coming from a strong uptrend → suggests a sharp fade, though the trend may still technically be up.

o Coming from a weaker uptrend or sideways market → suggests the start of an accelerating downtrend.

• Solid Red: All features near their lows. Indicates a strong, accelerating downtrend. May also reflect crash-type conditions or downside gaps.

• Fading Solid Red: A recently strong downtrend is losing strength. Market may move into a slower decline, consolidation, or early reversal upward.

• Fading Red → Yellow : The downtrend is weakening toward neutral, with potential for a bullish shift.

• Yellow → Increasing Green: Two possible scenarios:

o Coming from a strong downtrend, it reflects a sharp fade of bearish momentum, though the market may still technically be trending down.

o Coming from a weaker downtrend or sideways movement, it suggests the start of an accelerating uptrend.

Note: Market evolution does not always follow this neat “color cycle.” It may jump between states, skip stages, or reverse abruptly depending on market conditions. This makes the background coloring particularly valuable as a contextual map of current and evolving price dynamics.

Signal Crossovers:

Although the fast signal is very similar (but not identical) to the background coloring, it provides a numerical representation indicating a bullish interpretation for rising values and bearish for falling.

o High-confidence entries:

Fast signal rising from < -0.7 and crossing above the slow signal → potential long entry.

Fast signal falling from > +0.7 and crossing below the slow signal → potential short entry.

o Low-confidence entries:

Crossovers near zero may still provide a valid trigger but may be noisy and should be confirmed with other signals.

o Zero-crossings:

Indicate broader state changes, useful for conservative positioning or option strategies. For confirmation of a Fast signal 0-crossing, wait for the Slow signal to cross as well.

________________________________________

*) Note on Aggregation

While the indicator currently uses a heuristic linear combination of features, alternatives such as Principal Component Analysis (PCA) could provide a more formal aggregation. However, while in the absence of matrix algebra, the required eigenvalue decomposition can be approximated, its computational expense does not justify the marginal higher insight in this case. The current heuristic approach offers a practical balance of clarity, speed, and accuracy.

Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.

Hidden Markov Model: The actual regimes are unobservable ("hidden") and must be inferred from market output or indicator "emissions" using statistical learning algorithms. HMMs are more complex, can capture more subtle structure, but are harder to visualize and require additional machine learning steps for training.

A standard Markov Chain models transitions between observable states using a simple transition matrix, while a Hidden Markov Model assumes the true states are hidden (latent) and must be inferred from observable “emissions” like price or volume data. In practical terms, a Markov Chain is transparent and easier to implement and interpret; an HMM is more expressive but requires statistical inference to estimate hidden states from data.

Markov Chain: states are observable; you directly count or estimate transition probabilities between visible states. This makes it simpler, faster, and easier to validate and tune.

HMM: states are hidden; you only observe emissions generated by those latent states. Learning involves machine learning/statistical algorithms (commonly Baum–Welch/EM for training and Viterbi for decoding) to infer both the transition dynamics and the most likely hidden state sequence from data.

How does the indicator avoid “repainting” or look-ahead bias?

All regime changes and matrix updates happen only on confirmed (closed) bars, so no future data is leaked, ensuring reliable real-time operation.

Are there practical tuning tips?

Tune the Lookback Period for your asset/timeframe: shorter for fast markets, longer for stability.

Use custom indicators if your asset has unique regime drivers.

Watch for rapid changes in transition probabilities as early warning of a possible regime shift.

Who is this indicator for?

Quants and quantitative researchers exploring probabilistic market modeling, especially those interested in regime-switching dynamics and Markov models.

Programmers and system developers who need a probabilistic regime filter for systematic and algorithmic backtesting:

The Markov Chain indicator is ideally suited for programmatic integration via its bias output (1 = Bull, 0 = Neutral, -1 = Bear).

Although the visualization is engaging, the core output is designed for automated, rules-based workflows—not for discretionary/manual trading decisions.

Developers can connect the indicator’s output directly to their Pine Script logic (using input.source()), allowing rapid and robust backtesting of regime-based strategies.

It acts as a plug-and-play regime filter: simply plug the bias output into your entry/exit logic, and you have a scientifically robust, probabilistically-derived signal for filtering, timing, position sizing, or risk regimes.

The MC's output is intentionally "trinary" (1/0/-1), focusing on clear regime states for unambiguous decision-making in code. If you require nuanced, multi-probability or soft-label state vectors, consider expanding the indicator or stacking it with a probability-weighted logic layer in your scripting.

Because it avoids subjectivity, this approach is optimal for systematic quants, algo developers building backtested, repeatable strategies based on probabilistic regime analysis.

What's the mathematical foundation behind this?

The mathematical foundation behind this Markov Chain indicator—and probabilistic regime detection in finance—draws from two principal models: the (standard) Markov Chain and the Hidden Markov Model (HMM).

How to use this indicator programmatically?

The Markov Chain indicator automatically exports a bias value (+1 for Bullish, -1 for Bearish, 0 for Neutral) as a plot visible in the Data Window. This allows you to integrate its regime signal into your own scripts and strategies for backtesting, automation, or live trading.

Step-by-Step Integration with Pine Script (input.source)

Add the Markov Chain indicator to your chart.

This must be done first, since your custom script will "pull" the bias signal from the indicator's plot.

In your strategy, create an input using input.source()

Example:

//@version=5

strategy("MC Bias Strategy Example")

mcBias = input.source(close, "MC Bias Source")

After saving, go to your script’s settings. For the “MC Bias Source” input, select the plot/output of the Markov Chain indicator (typically its bias plot).

Use the bias in your trading logic

Example (long only on Bull, flat otherwise):

if mcBias == 1

strategy.entry("Long", strategy.long)

else

strategy.close("Long")

For more advanced workflows, combine mcBias with additional filters or trailing stops.

How does this work behind-the-scenes?

TradingView’s input.source() lets you use any plot from another indicator as a real-time, “live” data feed in your own script (source).

The selected bias signal is available to your Pine code as a variable, enabling logical decisions based on regime (trend-following, mean-reversion, etc.).

This enables powerful strategy modularity : decouple regime detection from entry/exit logic, allowing fast experimentation without rewriting core signal code.

Integrating 45+ Indicators with Your Markov Chain — How & Why

The Enhanced Custom Indicators Export script exports a massive suite of over 45 technical indicators—ranging from classic momentum (RSI, MACD, Stochastic, etc.) to trend, volume, volatility, and oscillator tools—all pre-calculated, centered/scaled, and available as plots.

// Enhanced Custom Indicators Export - 45 Technical Indicators

// Comprehensive technical analysis suite for advanced market regime detection

//@version=6

indicator('Enhanced Custom Indicators Export | Fractalyst', shorttitle='Enhanced CI Export', overlay=false, scale=scale.right, max_labels_count=500, max_lines_count=500)

// |----- Input Parameters -----| //

momentum_group = "Momentum Indicators"

trend_group = "Trend Indicators"

volume_group = "Volume Indicators"

volatility_group = "Volatility Indicators"

oscillator_group = "Oscillator Indicators"

display_group = "Display Settings"

// Common lengths

length_14 = input.int(14, "Standard Length (14)", minval=1, maxval=100, group=momentum_group)

length_20 = input.int(20, "Medium Length (20)", minval=1, maxval=200, group=trend_group)

length_50 = input.int(50, "Long Length (50)", minval=1, maxval=200, group=trend_group)

// Display options

show_table = input.bool(true, "Show Values Table", group=display_group)

table_size = input.string("Small", "Table Size", options= , group=display_group)

// |----- MOMENTUM INDICATORS (15 indicators) -----| //

// 1. RSI (Relative Strength Index)

rsi_14 = ta.rsi(close, length_14)

rsi_centered = rsi_14 - 50

// 2. Stochastic Oscillator

stoch_k = ta.stoch(close, high, low, length_14)

stoch_d = ta.sma(stoch_k, 3)

stoch_centered = stoch_k - 50

// 3. Williams %R

williams_r = ta.stoch(close, high, low, length_14) - 100

// 4. MACD (Moving Average Convergence Divergence)

= ta.macd(close, 12, 26, 9)

// 5. Momentum (Rate of Change)

momentum = ta.mom(close, length_14)

momentum_pct = (momentum / close ) * 100

// 6. Rate of Change (ROC)

roc = ta.roc(close, length_14)

// 7. Commodity Channel Index (CCI)

cci = ta.cci(close, length_20)

// 8. Money Flow Index (MFI)

mfi = ta.mfi(close, length_14)

mfi_centered = mfi - 50

// 9. Awesome Oscillator (AO)

ao = ta.sma(hl2, 5) - ta.sma(hl2, 34)

// 10. Accelerator Oscillator (AC)

ac = ao - ta.sma(ao, 5)

// 11. Chande Momentum Oscillator (CMO)

cmo = ta.cmo(close, length_14)

// 12. Detrended Price Oscillator (DPO)

dpo = close - ta.sma(close, length_20)

// 13. Price Oscillator (PPO)

ppo = ta.sma(close, 12) - ta.sma(close, 26)

ppo_pct = (ppo / ta.sma(close, 26)) * 100

// 14. TRIX

trix_ema1 = ta.ema(close, length_14)

trix_ema2 = ta.ema(trix_ema1, length_14)

trix_ema3 = ta.ema(trix_ema2, length_14)

trix = ta.roc(trix_ema3, 1) * 10000

// 15. Klinger Oscillator

klinger = ta.ema(volume * (high + low + close) / 3, 34) - ta.ema(volume * (high + low + close) / 3, 55)

// 16. Fisher Transform

fisher_hl2 = 0.5 * (hl2 - ta.lowest(hl2, 10)) / (ta.highest(hl2, 10) - ta.lowest(hl2, 10)) - 0.25

fisher = 0.5 * math.log((1 + fisher_hl2) / (1 - fisher_hl2))

// 17. Stochastic RSI

stoch_rsi = ta.stoch(rsi_14, rsi_14, rsi_14, length_14)

stoch_rsi_centered = stoch_rsi - 50

// 18. Relative Vigor Index (RVI)

rvi_num = ta.swma(close - open)

rvi_den = ta.swma(high - low)

rvi = rvi_den != 0 ? rvi_num / rvi_den : 0

// 19. Balance of Power (BOP)

bop = (close - open) / (high - low)

// |----- TREND INDICATORS (10 indicators) -----| //

// 20. Simple Moving Average Momentum

sma_20 = ta.sma(close, length_20)

sma_momentum = ((close - sma_20) / sma_20) * 100

// 21. Exponential Moving Average Momentum

ema_20 = ta.ema(close, length_20)

ema_momentum = ((close - ema_20) / ema_20) * 100

// 22. Parabolic SAR

sar = ta.sar(0.02, 0.02, 0.2)

sar_trend = close > sar ? 1 : -1

// 23. Linear Regression Slope

lr_slope = ta.linreg(close, length_20, 0) - ta.linreg(close, length_20, 1)

// 24. Moving Average Convergence (MAC)

mac = ta.sma(close, 10) - ta.sma(close, 30)

// 25. Trend Intensity Index (TII)

tii_sum = 0.0

for i = 1 to length_20

tii_sum += close > close ? 1 : 0

tii = (tii_sum / length_20) * 100

// 26. Ichimoku Cloud Components

ichimoku_tenkan = (ta.highest(high, 9) + ta.lowest(low, 9)) / 2

ichimoku_kijun = (ta.highest(high, 26) + ta.lowest(low, 26)) / 2

ichimoku_signal = ichimoku_tenkan > ichimoku_kijun ? 1 : -1

// 27. MESA Adaptive Moving Average (MAMA)

mama_alpha = 2.0 / (length_20 + 1)

mama = ta.ema(close, length_20)

mama_momentum = ((close - mama) / mama) * 100

// 28. Zero Lag Exponential Moving Average (ZLEMA)

zlema_lag = math.round((length_20 - 1) / 2)

zlema_data = close + (close - close )

zlema = ta.ema(zlema_data, length_20)

zlema_momentum = ((close - zlema) / zlema) * 100

// |----- VOLUME INDICATORS (6 indicators) -----| //

// 29. On-Balance Volume (OBV)

obv = ta.obv

// 30. Volume Rate of Change (VROC)

vroc = ta.roc(volume, length_14)

// 31. Price Volume Trend (PVT)

pvt = ta.pvt

// 32. Negative Volume Index (NVI)

nvi = 0.0

nvi := volume < volume ? nvi + ((close - close ) / close ) * nvi : nvi

// 33. Positive Volume Index (PVI)

pvi = 0.0

pvi := volume > volume ? pvi + ((close - close ) / close ) * pvi : pvi

// 34. Volume Oscillator

vol_osc = ta.sma(volume, 5) - ta.sma(volume, 10)

// 35. Ease of Movement (EOM)

eom_distance = high - low

eom_box_height = volume / 1000000

eom = eom_box_height != 0 ? eom_distance / eom_box_height : 0

eom_sma = ta.sma(eom, length_14)

// 36. Force Index

force_index = volume * (close - close )

force_index_sma = ta.sma(force_index, length_14)

// |----- VOLATILITY INDICATORS (10 indicators) -----| //

// 37. Average True Range (ATR)

atr = ta.atr(length_14)

atr_pct = (atr / close) * 100

// 38. Bollinger Bands Position

bb_basis = ta.sma(close, length_20)

bb_dev = 2.0 * ta.stdev(close, length_20)

bb_upper = bb_basis + bb_dev

bb_lower = bb_basis - bb_dev

bb_position = bb_dev != 0 ? (close - bb_basis) / bb_dev : 0

bb_width = bb_dev != 0 ? (bb_upper - bb_lower) / bb_basis * 100 : 0

// 39. Keltner Channels Position

kc_basis = ta.ema(close, length_20)

kc_range = ta.ema(ta.tr, length_20)

kc_upper = kc_basis + (2.0 * kc_range)

kc_lower = kc_basis - (2.0 * kc_range)

kc_position = kc_range != 0 ? (close - kc_basis) / kc_range : 0

// 40. Donchian Channels Position

dc_upper = ta.highest(high, length_20)

dc_lower = ta.lowest(low, length_20)

dc_basis = (dc_upper + dc_lower) / 2

dc_position = (dc_upper - dc_lower) != 0 ? (close - dc_basis) / (dc_upper - dc_lower) : 0

// 41. Standard Deviation

std_dev = ta.stdev(close, length_20)

std_dev_pct = (std_dev / close) * 100

// 42. Relative Volatility Index (RVI)

rvi_up = ta.stdev(close > close ? close : 0, length_14)

rvi_down = ta.stdev(close < close ? close : 0, length_14)

rvi_total = rvi_up + rvi_down

rvi_volatility = rvi_total != 0 ? (rvi_up / rvi_total) * 100 : 50

// 43. Historical Volatility

hv_returns = math.log(close / close )

hv = ta.stdev(hv_returns, length_20) * math.sqrt(252) * 100

// 44. Garman-Klass Volatility

gk_vol = math.log(high/low) * math.log(high/low) - (2*math.log(2)-1) * math.log(close/open) * math.log(close/open)

gk_volatility = math.sqrt(ta.sma(gk_vol, length_20)) * 100

// 45. Parkinson Volatility

park_vol = math.log(high/low) * math.log(high/low)

parkinson = math.sqrt(ta.sma(park_vol, length_20) / (4 * math.log(2))) * 100

// 46. Rogers-Satchell Volatility

rs_vol = math.log(high/close) * math.log(high/open) + math.log(low/close) * math.log(low/open)

rogers_satchell = math.sqrt(ta.sma(rs_vol, length_20)) * 100

// |----- OSCILLATOR INDICATORS (5 indicators) -----| //

// 47. Elder Ray Index

elder_bull = high - ta.ema(close, 13)

elder_bear = low - ta.ema(close, 13)

elder_power = elder_bull + elder_bear

// 48. Schaff Trend Cycle (STC)

stc_macd = ta.ema(close, 23) - ta.ema(close, 50)

stc_k = ta.stoch(stc_macd, stc_macd, stc_macd, 10)

stc_d = ta.ema(stc_k, 3)

stc = ta.stoch(stc_d, stc_d, stc_d, 10)

// 49. Coppock Curve

coppock_roc1 = ta.roc(close, 14)

coppock_roc2 = ta.roc(close, 11)

coppock = ta.wma(coppock_roc1 + coppock_roc2, 10)

// 50. Know Sure Thing (KST)

kst_roc1 = ta.roc(close, 10)

kst_roc2 = ta.roc(close, 15)

kst_roc3 = ta.roc(close, 20)

kst_roc4 = ta.roc(close, 30)

kst = ta.sma(kst_roc1, 10) + 2*ta.sma(kst_roc2, 10) + 3*ta.sma(kst_roc3, 10) + 4*ta.sma(kst_roc4, 15)

// 51. Percentage Price Oscillator (PPO)

ppo_line = ((ta.ema(close, 12) - ta.ema(close, 26)) / ta.ema(close, 26)) * 100

ppo_signal = ta.ema(ppo_line, 9)

ppo_histogram = ppo_line - ppo_signal

// |----- PLOT MAIN INDICATORS -----| //

// Plot key momentum indicators

plot(rsi_centered, title="01_RSI_Centered", color=color.purple, linewidth=1)

plot(stoch_centered, title="02_Stoch_Centered", color=color.blue, linewidth=1)

plot(williams_r, title="03_Williams_R", color=color.red, linewidth=1)

plot(macd_histogram, title="04_MACD_Histogram", color=color.orange, linewidth=1)

plot(cci, title="05_CCI", color=color.green, linewidth=1)

// Plot trend indicators

plot(sma_momentum, title="06_SMA_Momentum", color=color.navy, linewidth=1)

plot(ema_momentum, title="07_EMA_Momentum", color=color.maroon, linewidth=1)

plot(sar_trend, title="08_SAR_Trend", color=color.teal, linewidth=1)

plot(lr_slope, title="09_LR_Slope", color=color.lime, linewidth=1)

plot(mac, title="10_MAC", color=color.fuchsia, linewidth=1)

// Plot volatility indicators

plot(atr_pct, title="11_ATR_Pct", color=color.yellow, linewidth=1)

plot(bb_position, title="12_BB_Position", color=color.aqua, linewidth=1)

plot(kc_position, title="13_KC_Position", color=color.olive, linewidth=1)

plot(std_dev_pct, title="14_StdDev_Pct", color=color.silver, linewidth=1)

plot(bb_width, title="15_BB_Width", color=color.gray, linewidth=1)

// Plot volume indicators

plot(vroc, title="16_VROC", color=color.blue, linewidth=1)

plot(eom_sma, title="17_EOM", color=color.red, linewidth=1)

plot(vol_osc, title="18_Vol_Osc", color=color.green, linewidth=1)

plot(force_index_sma, title="19_Force_Index", color=color.orange, linewidth=1)

plot(obv, title="20_OBV", color=color.purple, linewidth=1)

// Plot additional oscillators

plot(ao, title="21_Awesome_Osc", color=color.navy, linewidth=1)

plot(cmo, title="22_CMO", color=color.maroon, linewidth=1)

plot(dpo, title="23_DPO", color=color.teal, linewidth=1)

plot(trix, title="24_TRIX", color=color.lime, linewidth=1)

plot(fisher, title="25_Fisher", color=color.fuchsia, linewidth=1)

// Plot more momentum indicators

plot(mfi_centered, title="26_MFI_Centered", color=color.yellow, linewidth=1)

plot(ac, title="27_AC", color=color.aqua, linewidth=1)

plot(ppo_pct, title="28_PPO_Pct", color=color.olive, linewidth=1)

plot(stoch_rsi_centered, title="29_StochRSI_Centered", color=color.silver, linewidth=1)

plot(klinger, title="30_Klinger", color=color.gray, linewidth=1)

// Plot trend continuation

plot(tii, title="31_TII", color=color.blue, linewidth=1)

plot(ichimoku_signal, title="32_Ichimoku_Signal", color=color.red, linewidth=1)

plot(mama_momentum, title="33_MAMA_Momentum", color=color.green, linewidth=1)

plot(zlema_momentum, title="34_ZLEMA_Momentum", color=color.orange, linewidth=1)

plot(bop, title="35_BOP", color=color.purple, linewidth=1)

// Plot volume continuation

plot(nvi, title="36_NVI", color=color.navy, linewidth=1)

plot(pvi, title="37_PVI", color=color.maroon, linewidth=1)

plot(momentum_pct, title="38_Momentum_Pct", color=color.teal, linewidth=1)

plot(roc, title="39_ROC", color=color.lime, linewidth=1)

plot(rvi, title="40_RVI", color=color.fuchsia, linewidth=1)

// Plot volatility continuation

plot(dc_position, title="41_DC_Position", color=color.yellow, linewidth=1)

plot(rvi_volatility, title="42_RVI_Volatility", color=color.aqua, linewidth=1)

plot(hv, title="43_Historical_Vol", color=color.olive, linewidth=1)

plot(gk_volatility, title="44_GK_Volatility", color=color.silver, linewidth=1)

plot(parkinson, title="45_Parkinson_Vol", color=color.gray, linewidth=1)

// Plot final oscillators

plot(rogers_satchell, title="46_RS_Volatility", color=color.blue, linewidth=1)

plot(elder_power, title="47_Elder_Power", color=color.red, linewidth=1)

plot(stc, title="48_STC", color=color.green, linewidth=1)

plot(coppock, title="49_Coppock", color=color.orange, linewidth=1)

plot(kst, title="50_KST", color=color.purple, linewidth=1)

// Plot final indicators

plot(ppo_histogram, title="51_PPO_Histogram", color=color.navy, linewidth=1)

plot(pvt, title="52_PVT", color=color.maroon, linewidth=1)

// |----- Reference Lines -----| //

hline(0, "Zero Line", color=color.gray, linestyle=hline.style_dashed, linewidth=1)

hline(50, "Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-50, "Lower Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(25, "Upper Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-25, "Lower Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

// |----- Enhanced Information Table -----| //

if show_table and barstate.islast

table_position = position.top_right

table_text_size = table_size == "Tiny" ? size.tiny : table_size == "Small" ? size.small : size.normal

var table info_table = table.new(table_position, 3, 18, bgcolor=color.new(color.white, 85), border_width=1, border_color=color.gray)

// Headers

table.cell(info_table, 0, 0, 'Category', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 1, 0, 'Indicator', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 2, 0, 'Value', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

// Key Momentum Indicators

table.cell(info_table, 0, 1, 'MOMENTUM', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 1, 'RSI Centered', text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 2, 1, str.tostring(rsi_centered, '0.00'), text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 0, 2, '', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 1, 2, 'Stoch Centered', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 2, str.tostring(stoch_centered, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 3, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 3, 'Williams %R', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 3, str.tostring(williams_r, '0.00'), text_color=color.red, text_size=table_text_size)

table.cell(info_table, 0, 4, '', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 1, 4, 'MACD Histogram', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 2, 4, str.tostring(macd_histogram, '0.000'), text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 0, 5, '', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 1, 5, 'CCI', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 2, 5, str.tostring(cci, '0.00'), text_color=color.green, text_size=table_text_size)

// Key Trend Indicators

table.cell(info_table, 0, 6, 'TREND', text_color=color.navy, text_size=table_text_size, bgcolor=color.new(color.navy, 90))

table.cell(info_table, 1, 6, 'SMA Momentum %', text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 2, 6, str.tostring(sma_momentum, '0.00'), text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 0, 7, '', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 1, 7, 'EMA Momentum %', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 2, 7, str.tostring(ema_momentum, '0.00'), text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 0, 8, '', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 1, 8, 'SAR Trend', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 2, 8, str.tostring(sar_trend, '0'), text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 0, 9, '', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 1, 9, 'Linear Regression', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 2, 9, str.tostring(lr_slope, '0.000'), text_color=color.lime, text_size=table_text_size)

// Key Volatility Indicators

table.cell(info_table, 0, 10, 'VOLATILITY', text_color=color.yellow, text_size=table_text_size, bgcolor=color.new(color.yellow, 90))

table.cell(info_table, 1, 10, 'ATR %', text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 2, 10, str.tostring(atr_pct, '0.00'), text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 0, 11, '', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 1, 11, 'BB Position', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 2, 11, str.tostring(bb_position, '0.00'), text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 0, 12, '', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 1, 12, 'KC Position', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 2, 12, str.tostring(kc_position, '0.00'), text_color=color.olive, text_size=table_text_size)

// Key Volume Indicators

table.cell(info_table, 0, 13, 'VOLUME', text_color=color.blue, text_size=table_text_size, bgcolor=color.new(color.blue, 90))

table.cell(info_table, 1, 13, 'Volume ROC', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 13, str.tostring(vroc, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 14, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 14, 'EOM', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 14, str.tostring(eom_sma, '0.000'), text_color=color.red, text_size=table_text_size)

// Key Oscillators

table.cell(info_table, 0, 15, 'OSCILLATORS', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 15, 'Awesome Osc', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 15, str.tostring(ao, '0.000'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 16, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 16, 'Fisher Transform', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 16, str.tostring(fisher, '0.000'), text_color=color.red, text_size=table_text_size)

// Summary Statistics

table.cell(info_table, 0, 17, 'SUMMARY', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.gray, 70))

table.cell(info_table, 1, 17, 'Total Indicators: 52', text_color=color.black, text_size=table_text_size)

regime_color = rsi_centered > 10 ? color.green : rsi_centered < -10 ? color.red : color.gray

regime_text = rsi_centered > 10 ? "BULLISH" : rsi_centered < -10 ? "BEARISH" : "NEUTRAL"

table.cell(info_table, 2, 17, regime_text, text_color=regime_color, text_size=table_text_size)

This makes it the perfect “indicator backbone” for quantitative and systematic traders who want to prototype, combine, and test new regime detection models—especially in combination with the Markov Chain indicator.

How to use this script with the Markov Chain for research and backtesting:

Add the Enhanced Indicator Export to your chart.

Every calculated indicator is available as an individual data stream.

Connect the indicator(s) you want as custom input(s) to the Markov Chain’s “Custom Indicators” option.

In the Markov Chain indicator’s settings, turn ON the custom indicator mode.

For each of the three custom indicator inputs, select the exported plot from the Enhanced Export script—the menu lists all 45+ signals by name.

This creates a powerful, modular regime-detection engine where you can mix-and-match momentum, trend, volume, or custom combinations for advanced filtering.

Backtest regime logic directly.

Once you’ve connected your chosen indicators, the Markov Chain script performs regime detection (Bull/Neutral/Bear) based on your selected features—not just price returns.

The regime detection is robust, automatically normalized (using Z-score), and outputs bias (1, -1, 0) for plug-and-play integration.

Export the regime bias for programmatic use.

As described above, use input.source() in your Pine Script strategy or system and link the bias output.

You can now filter signals, control trade direction/size, or design pairs-trading that respect true, indicator-driven market regimes.

With this framework, you’re not limited to static or simplistic regime filters. You can rigorously define, test, and refine what “market regime” means for your strategies—using the technical features that matter most to you.

Optimize your signal generation by backtesting across a universe of meaningful indicator blends.

Enhance risk management with objective, real-time regime boundaries.

Accelerate your research: iterate quickly, swap indicator components, and see results with minimal code changes.

Automate multi-asset or pairs-trading by integrating regime context directly into strategy logic.

Add both scripts to your chart, connect your preferred features, and start investigating your best regime-based trades—entirely within the TradingView ecosystem.

References & Further Reading

Ang, A., & Bekaert, G. (2002). “Regime Switches in Interest Rates.” Journal of Business & Economic Statistics, 20(2), 163–182.

Hamilton, J. D. (1989). “A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle.” Econometrica, 57(2), 357–384.

Markov, A. A. (1906). "Extension of the Limit Theorems of Probability Theory to a Sum of Variables Connected in a Chain." The Notes of the Imperial Academy of Sciences of St. Petersburg.

Guidolin, M., & Timmermann, A. (2007). “Asset Allocation under Multivariate Regime Switching.” Journal of Economic Dynamics and Control, 31(11), 3503–3544.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets. New York Institute of Finance.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). “Simple Technical Trading Rules and the Stochastic Properties of Stock Returns.” Journal of Finance, 47(5), 1731–1764.

Zucchini, W., MacDonald, I. L., & Langrock, R. (2017). Hidden Markov Models for Time Series: An Introduction Using R (2nd ed.). Chapman and Hall/CRC.

On Quantitative Finance and Markov Models:

Lo, A. W., & Hasanhodzic, J. (2009). The Heretics of Finance: Conversations with Leading Practitioners of Technical Analysis. Bloomberg Press.

Patterson, S. (2016). The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution. Penguin Press.

TradingView Pine Script Documentation: www.tradingview.com

TradingView Blog: “Use an Input From Another Indicator With Your Strategy” www.tradingview.com

GeeksforGeeks: “What is the Difference Between Markov Chains and Hidden Markov Models?” www.geeksforgeeks.org

What makes this indicator original and unique?

- On‑chart, real‑time Markov. The chain is drawn directly on your chart. You see the current regime, its tendency to stay (self‑loop), and the usual next step (arrows) as bars confirm.

- Source‑agnostic by design. The engine runs on any series you select via input.source() — price, your own oscillator, a composite score, anything you compute in the script.

- Automatic normalization + regime mapping. Different inputs live on different scales. The script standardizes your chosen source and maps it into clear regimes (e.g., Bull / Bear / Neutral) without you micromanaging thresholds each time.

- Rolling, bar‑by‑bar learning. Transition tendencies are computed from a rolling window of confirmed bars. What you see is exactly what the market did in that window.

- Fast experimentation. Switch the source, adjust the window, and the Markov view updates instantly. It’s a rapid way to test ideas and feel regime persistence/switch behavior.

Integrate your own signals (using input.source())

- In settings, choose the Source . This is powered by input.source() .

- Feed it price, an indicator you compute inside the script, or a custom composite series.

- The script will automatically normalize that series and process it through the Markov engine, mapping it to regimes and updating the on‑chart spheres/arrows in real time.

Credits:

Deep gratitude to @RicardoSantos for both the foundational Markov chain processing engine and inspiring open-source contributions, which made advanced probabilistic market modeling accessible to the TradingView community.

Special thanks to @Alien_Algorithms for the innovative and visually stunning 3D sphere logic that powers the indicator’s animated, regime-based visualization.

Disclaimer

This tool summarizes recent behavior. It is not financial advice and not a guarantee of future results.

IU Indicators DashboardDESCRIPTION

The IU Indicators Dashboard is a comprehensive multi-stock monitoring tool that provides real-time technical analysis for up to 10 different stocks simultaneously. This powerful indicator creates a customizable table overlay that displays the trend status of multiple technical indicators across your selected stocks, giving you an instant overview of market conditions without switching between charts.

Perfect for portfolio monitoring, sector analysis, and quick market screening, this dashboard consolidates critical technical data into one easy-to-read interface with color-coded trend signals.

USER INPUTS

Stock Selection (10 Configurable Stocks):

- Stock 1-10: Customize any symbols (Default: NSE:CDSL, NSE:RELIANCE, NSE:VEDL, NSE:TCS, NSE:BEL, NSE:BHEL, NSE:TATAPOWER, NSE:TATASTEEL, NSE:ITC, NSE:LT)

Technical Indicator Parameters:

- EMA 1 Length: First Exponential Moving Average period (Default: 20)

- EMA 2 Length: Second Exponential Moving Average period (Default: 50)

- EMA 3 Length: Third Exponential Moving Average period (Default: 200)

- RSI Length: Relative Strength Index calculation period (Default: 14)

- SuperTrend Length: SuperTrend indicator period (Default: 10)

- SuperTrend Factor: SuperTrend multiplier factor (Default: 3.0)

Visual Customization:

- Table Size: Choose from Normal, Tiny, Small, or Large

- Table Background Color: Customize dashboard background

- Table Frame Color: Set frame border color

- Table Border Color: Configure border styling

- Text Color: Set text display color

- Bullish Color: Color for positive/bullish signals (Default: Green)

- Bearish Color: Color for negative/bearish signals (Default: Red)

LOGIC OF THE INDICATOR

The dashboard employs a multi-timeframe analysis approach using five key technical indicators:

1. Triple EMA Analysis

- Compares current price against three different EMA periods (20, 50, 200)

- Bullish Signal: Price above EMA level

- Bearish Signal: Price below EMA level

- Provides short-term, medium-term, and long-term trend perspective

2. RSI Momentum Analysis

- Uses 14-period RSI with 50-level threshold

- Bullish Signal: RSI > 50 (upward momentum)

- Bearish Signal: RSI < 50 (downward momentum)

- Identifies momentum strength and potential reversals

3. SuperTrend Direction

- Utilizes SuperTrend with configurable length and factor

- Bullish Signal: SuperTrend direction = -1 (uptrend)

- Bearish Signal: SuperTrend direction = 1 (downtrend)

- Provides clear trend direction with volatility-adjusted signals

4. MACD Histogram Analysis

- Uses standard MACD (12, 26, 9) histogram values

- Bullish Signal: Histogram > 0 (bullish momentum)

- Bearish Signal: Histogram < 0 (bearish momentum)

- Identifies momentum shifts and trend confirmations

5. Real-time Data Processing

- Implements request.security() for multi-symbol data retrieval

- Uses barstate.isrealtime logic for accurate live data

- Processes data only on the last bar for optimal performance

WHY IT IS UNIQUE

Multi-Stock Monitoring

- Monitor up to 10 different stocks simultaneously on a single chart

- No need to switch between multiple charts or timeframes

Highly Customizable Interface

- Full color customization for personalized visual experience

- Adjustable table size and positioning

- Clean, professional dashboard design

Real-time Analysis

- Live data processing with proper real-time handling

- Instant visual feedback through color-coded signals

- Optimized performance with smart data retrieval

Comprehensive Technical Coverage

- Combines trend-following, momentum, and volatility indicators

- Multiple timeframe perspective through different EMA periods

- Balanced approach using both lagging and leading indicators

Flexible Configuration

- Easy symbol switching for different markets (NSE, BSE, NYSE, NASDAQ)

- Adjustable indicator parameters for different trading styles

- Suitable for both swing trading and position trading

HOW USERS CAN BENEFIT FROM IT

Portfolio Management

- Quick Portfolio Health Check: Instantly assess the technical status of your entire stock portfolio

- Diversification Analysis: Monitor stocks across different sectors to ensure balanced exposure

- Risk Management: Identify which positions are showing bearish signals for potential exit strategies

- Rebalancing Decisions: Spot strongest performers for potential position increases

Market Screening and Analysis

- Sector Rotation: Compare different sector stocks to identify rotation opportunities

- Relative Strength Analysis: Quickly identify which stocks are outperforming or underperforming

- Market Breadth Assessment: Gauge overall market sentiment by monitoring diverse stock selections

- Trend Confirmation: Validate market trends by observing multiple stock behaviors

Time-Efficient Trading

- Single-Glance Analysis: Get complete technical overview without chart-hopping

- Pre-Market Preparation: Quickly assess overnight changes across multiple positions

- Intraday Monitoring: Track multiple opportunities simultaneously during trading hours

- End-of-Day Review: Efficiently review all watched stocks for next-day planning

Strategic Decision Making

- Entry Point Identification: Spot stocks showing bullish alignment across multiple indicators

- Exit Signal Recognition: Identify positions showing deteriorating technical conditions

- Swing Trading Opportunities: Find stocks with favorable technical setups for swing trades

- Long-term Investment Guidance: Use 200 EMA signals for long-term position decisions

Educational Benefits

- Pattern Recognition: Learn how different indicators behave across various market conditions

- Correlation Analysis: Understand how stocks move relative to each other

- Technical Analysis Learning: Observe multiple indicator interactions in real-time

- Market Sentiment Understanding: Develop better market timing skills through multi-stock observation

Workflow Optimization

- Reduced Chart Clutter: Keep your main chart clean while monitoring multiple stocks

- Faster Analysis: Complete technical analysis of 10 stocks in seconds instead of minutes

- Consistent Methodology: Apply the same technical criteria across all monitored stocks

- Alert Integration: Easy visual identification of stocks requiring immediate attention