MFM - Light Context HUD (Free)Overview

MFM Light Context HUD is the free version of the Market Framework Model. It gives you a fast and clean view of the current market regime and phase without signals or chart noise. The HUD shows whether the asset is in a bullish or bearish environment and whether it is in a volatile, compression, drift, or neutral phase. This helps you read structure at a glance.

Asset availability

The free version works only on a selected list of five assets.

Supported symbols are

SP:SPX

TVC:GOLD

BINANCE:BTCUSD

BINANCE:ETHUSDT

OANDA:EURUSD

All other assets show a context banner only.

How it works

The free version uses fixed settings based on the original MFM model. It calculates the regime using a higher timeframe RSI ratio and identifies the current phase using simplified momentum conditions. The chart stays clean. Only a small HUD appears in the top corner. Full visual phases, ratio logic, signals, and auto tune are part of the paid version.

The free version shows the phase name only. It does not display colored phase zones on the chart.

Phase meaning

The Market Framework Model uses four structural phases to describe how the market behaves. These are not signals but context layers that show the underlying environment.

Volatile (Phase 1)

The market is in a fast, unstable or directional environment. Price can move aggressively with stronger momentum swings.

Compression (Phase 2)

The market is in a contracting state. Momentum slows and volatility decreases. This phase often appears before expansion, but it does not predict direction.

Drift (Phase 3)

The market moves in a more controlled, persistent manner. Trends are cleaner and volatility is lower compared to volatile phases.

No phase

No clear structural condition is active.

These phases describe market structure, not trade entries. They help you understand the conditions you are trading in.

Cross asset context

The Market Framework Model reads markets as a multi layer system. The full version includes cross asset analysis to show whether the asset is acting as a leader or lagger relative to its benchmark. The free version uses the same internal benchmark logic for regime detection but does not display the cross asset layer on the chart.

Cross asset structure is a core part of the MFM model and is fully available in the paid version.

Included in this free version

Higher timeframe regime

Current phase name

Clean chart output

Context only

Works on a selected set of assets

Not included

No forecast signals

No ratio leader or lagger logic

No MRM zones

No MPF timing

No auto tune

The full version contains all features of the complete MFM model.

Full version

You can find the full indicator here:

payhip.com

More information

Model details and documentation:

mfm.inratios.com

Disclaimer

The Market Framework Model (MFM) and all related materials are provided for educational and informational purposes only. Nothing in this publication, the indicator, or any associated charts should be interpreted as financial advice, investment recommendations, or trading signals. All examples, visualizations, and backtests are illustrative and based on historical data. They do not guarantee or imply any future performance. Financial markets involve risk, including the potential loss of capital, and users remain fully responsible for their own decisions. The author and Inratios© make no representations or warranties regarding the accuracy, completeness, or reliability of the information provided. MFM describes structural market context only and should not be used as the sole basis for trading or investment actions.

By using the MFM indicator or any related insights, you agree to these terms.

© 2025 Inratios. Market Framework Model (MFM) is protected via i-Depot (BOIP) – Ref. 155670. No financial advice.

Buscar en scripts para "spx"

$MTF Fractal Echo DetectorMIL:MTVFR FRACTAL ECHO DETECTOR by Timmy741

The first public multi-timeframe fractal convergence system that actually works.

Market makers don’t move price randomly.

They test the same fractal structure on lower timeframes first → then execute the real move on higher timeframes.

This indicator catches the “echo” — when 3–5 timeframes are printing fractals at almost the exact same price level.

That’s not coincidence. That’s preparation.

FEATURES

• 5 simultaneous timeframes (1min → 4H by default)

• Real Williams Fractal detection (configurable period)

• Dynamic echo tolerance & minimum TF alignment

• Visual S/R zones from every timeframe

• Bullish / Bearish echo convergence signals

• Strength meter (3/5, 4/5, 5/5 TF alignment)

• Zero repainting — uses proper lookahead=off

• Fully Pine v6 typed + optimized

USE CASE

When you see a 4/5 or 5/5 echo:

→ That level is being defended or attacked with intent

→ 80%+ chance the next real move comes from there

→ Trade the breakout or reversal at that exact fractal cluster

Works insane on:

• BTC / ETH (all timeframes)

• Nasdaq / SPX futures

• Forex majors (especially GBP & gold)

• 2025 small-cap rotation setups

100% Open Source • MPL 2.0 • Built by Timmy741 • December 2024

If you know about fractal echoes… you already know.

#fractal #mtf #echo #williamsfractal #multitimeframe #smartmoney #ict #smc #orderflow #convergence #timmy741 #snr #structure

Bitcoin vs. S&P 500 Performance Comparison**Full Description:**

**Overview**

This indicator provides an intuitive visual comparison of Bitcoin's performance versus the S&P 500 by shading the chart background based on relative strength over a rolling lookback period.

**How It Works**

- Calculates percentage returns for both Bitcoin and the S&P 500 (ES1! futures) over a specified lookback period (default: 75 bars)

- Compares the returns and shades the background accordingly:

- **Green/Teal Background**: Bitcoin is outperforming the S&P 500

- **Red/Maroon Background**: S&P 500 is outperforming Bitcoin

- Displays a real-time performance difference label showing the exact percentage spread

**Key Features**

✓ Rolling performance comparison using customizable lookback period (default 75 bars)

✓ Clean visual representation with adjustable transparency

✓ Works on any timeframe (optimized for daily charts)

✓ Real-time performance differential display

✓ Uses ES1! (E-mini S&P 500 continuous futures) for accurate comparison

✓ Fine-tuning adjustment factor for precise calibration

**Use Cases**

- Identify market regimes where Bitcoin outperforms or underperforms traditional equities

- Spot trend changes in relative performance

- Assess risk-on vs risk-off periods

- Compare Bitcoin's momentum against broader market conditions

- Time entries/exits based on relative strength shifts

**Settings**

- **S&P 500 Symbol**: Default ES1! (can be changed to SPX or other indices)

- **Lookback Period**: Number of bars for performance calculation (default: 75)

- **Adjustment Factor**: Fine-tune calibration to match specific data feeds

- **Transparency Controls**: Customize background shading intensity

- **Show/Hide Label**: Toggle performance difference display

**Best Practices**

- Use on daily timeframe for swing trading and position analysis

- Combine with other momentum indicators for confirmation

- Watch for color transitions as potential regime change signals

- Consider using multiple timeframes for comprehensive analysis

**Technical Details**

The indicator calculates rolling percentage returns using the formula: ((Current Price / Price ) - 1) × 100, then compares Bitcoin's return to the S&P 500's return over the same period. The background color dynamically updates based on which asset is showing stronger performance.

Gould 10Y + 4Y patternDescription:

Overview This indicator is a comprehensive tool for macro-market analysis, designed to visualize historical market cycles on your chart. It combines Edson Gould’s famous Decennial Pattern with a Customizable 4-Year Cycle (e.g., 2002 base) to help traders identify long-term trends, potential market bottoms, and strong bullish years.

This tool is ideal for long-term investors and analysts looking for cyclical confluence on monthly or yearly timeframes (e.g., SPX, NDX).

Key Concepts

Edson Gould’s Decennial Pattern (10-Year Cycle)

Based on the theory that the stock market follows a psychological cycle determined by the last digit of the year.

5 (Strongest Bull): Historically the strongest performance years.

7 (Panic/Crash): Years often associated with market panic or crashes.

2 (Bottom/Buy): Years that often mark major lows.

Custom 4-Year Cycle (Target Year Strategy)

Identify recurring 4-year opportunities based on a user-defined base year.

Default Setting (Base 2002): Highlights years like 2002, 2006, 2010, 2014, 2018, 2022... which have historically been significant market bottoms or excellent buying opportunities.

When a "Target Year" arrives, the indicator highlights the background and displays a distinct Green "Target Year" Label.

Features

Real-time Dashboard: A table in the top-right corner displays the current year's status for both the 10-Year and 4-Year cycles, including a countdown to the next target year.

Dynamic Labels: Automatically marks every year on the chart with its Decennial status (e.g., "Strong Bull (5)", "Panic (7)").

Visual Highlighting:

Target Years: Distinct green background and labels for easy identification of the 4-year cycle.

Significant Decennial Years: Special small markers for years ending in 5 and 7.

Fully Customizable: You can change the base year for the 4-year cycle, toggle the dashboard, and adjust colors via the settings menu.

How to Use

Apply this indicator to high-timeframe charts (Weekly or Monthly) of major indices like S&P 500 or Nasdaq.

Look for confluence between the 10-Year Pattern (e.g., Year 6 - Bullish) and the 4-Year Cycle (Target Year) to confirm long-term bias.

Disclaimer This tool is for educational and research purposes only based on historical cycle theories. Past performance is not indicative of future results. Always manage your risk.

Global Liquidity Score

Global Liquidity Score – Simple Risk-On / Risk-Off Gauge

This indicator measures overall market liquidity conditions using a single, normalized score.

It takes several macro and crypto variables, standardizes each one (z-score), and combines them into one clear Liquidity Score Line.

You only follow one line (your pink/white line).

The background color shows the current liquidity regime.

⸻

What the indicator measures

The algorithm looks at four major liquidity sources:

1. USD Liquidity (tightening or easing)

• DXY (strong dollar = tighter global liquidity)

• US10Y yield (higher yields = liquidity drain)

2. Risk Sentiment (risk-on vs risk-off)

• VIX index (volatility)

• S&P 500 index (SPX)

3. Credit Market Strength

• High-yield ETFs: HYG, JNK

• Investment-grade corporate credit: LQD

Stronger credit = easier liquidity.

Weaker credit = tightening risk.

4. Internal Crypto Liquidity

• USDT dominance (higher = risk-off in crypto)

• Bitcoin price

• TOTAL2 (crypto market cap excluding BTC)

These are all converted into z-scores and combined into one metric:

Total Liquidity Score =

USD Block + Risk Block − Credit Block − 0.5 × Crypto Block

⸻

How to read the colors

The indicator uses background colors to show the liquidity regime:

Color Meaning

Dark Red Severe liquidity tightening / strong risk-off

Red Mild-to-moderate tightening

Green Liquidity easing / soft risk-on

Dark Green Strong easing, high liquidity / risk-on

Your pink/white line = the final liquidity score.

You only need to follow that single line.

⸻

How to interpret the score

📉 Positive score → Liquidity Tightening (Risk-Off)

• USD stronger

• Yields rising

• Volatility rising

• Credit markets weakening

• Crypto rotating to stablecoins

📈 Negative score → Liquidity Easing (Risk-On)

• USD weakening

• Yields falling

• Stocks rising

• Volatility low

• Credit markets strong

• Crypto beta assets outperform

⸻

What this indicator is NOT

This is not a price predictor.

It does not follow BTC directly.

It tells you liquidity conditions, not immediate price direction.

It answers the macro question:

“Is liquidity flowing INTO the market or OUT of the market?”

If liquidity is tightening (red), crypto rallies are harder to sustain.

If liquidity is easing (green), crypto rallies have more fuel.

CVD [able0.1]# CVD Overlay iOS Style - Complete User Guide

## 📖 Table of Contents

1. (#what-is-cvd)

2. (#installation-guide)

3. (#understanding-the-display)

4. (#reading-the-info-table)

5. (#settings--customization)

6. (#trading-strategies)

7. (#common-mistakes-to-avoid)

---

## 🎯 What is CVD?

**CVD (Cumulative Volume Delta)** tracks the **difference between buying and selling pressure** over time.

### Simple Explanation:

- **Positive CVD** (Orange) = More buying than selling = Bulls winning

- **Negative CVD** (Gray) = More selling than buying = Bears winning

- **Rising CVD** = Increasing buying pressure = Potential uptrend

- **Falling CVD** = Increasing selling pressure = Potential downtrend

### Why It Matters:

CVD helps you see **who's really in control** of the market - not just price movement, but actual buying/selling volume.

---

## 🚀 Installation Guide

### Step 1: Open Pine Editor

1. Go to TradingView

2. Click the **"Pine Editor"** tab at the bottom of the screen

3. Click **"New"** or open an existing script

### Step 2: Copy & Paste the Code

1. Select all existing code (Ctrl+A / Cmd+A)

2. Delete it

3. Copy the entire CVD iOS Style code

4. Paste it into Pine Editor

### Step 3: Add to Chart

1. Click **"Save"** button (or Ctrl+S / Cmd+S)

2. Click **"Add to Chart"** button

3. The indicator will appear on your chart!

### Step 4: Initial Setup

- The indicator appears as an **overlay** on your price chart

- You'll see an **orange/gray line** following price

- An **info table** appears in the top-right corner

---

## 📊 Understanding the Display

### Main Chart Elements:

#### 1. **CVD Line** (Orange/Gray)

- **Orange Line** = Positive CVD (buying pressure)

- **Gray Line** = Negative CVD (selling pressure)

- This line moves with your price chart but shows volume delta

#### 2. **CVD Zone** (Shaded Area)

- Light shaded box around the CVD line

- Shows the "range" of CVD movement

- Helps visualize CVD boundaries

#### 3. **Center Line** (Dotted)

- Gray dotted line in the middle of the zone

- Represents the "neutral" point

- CVD crossing this = shift in market control

#### 4. **Reference Asset Line** (Light Gray)

- Shows Bitcoin (BTC) price movement for comparison

- Helps you see if your asset moves with or against BTC

- Can be changed to any asset you want

#### 5. **CVD Label**

- Shows current CVD value

- Positioned above/below zone to avoid overlap

- Updates in real-time

#### 6. **Reset Background** (Very Light Gray)

- Appears when CVD resets

- Indicates a new calculation period

---

## 📋 Reading the Info Table

The info table (top-right) shows **8 key metrics**:

### Row 1: **Header**

```

╔═ CVD able ═╗ | 15m | ████████ | able

```

- **CVD able** = Indicator name + creator

- **15m** = Current timeframe

- **████████** = Visual decoration

- **able** = Creator signature

### Row 2: **CVD Value**

```

CVD▲ | 7.39K | ████████ | █

█

█

```

- **CVD▲** = CVD with trend arrow

- ▲ = CVD increasing

- ▼ = CVD decreasing

- ► = CVD unchanged

- **7.39K** = Actual CVD number

- **Progress Bar** = Visual strength (darker = stronger)

- **Vertical Bars** = Height shows intensity

### Row 3: **Delta**

```

◆DELTA | -1.274K | ████░░░░ | ░

░

```

- **Delta** = Volume change THIS BAR ONLY

- **Negative** = More selling this bar

- **Positive** = More buying this bar

- Shows **immediate** pressure (not cumulative)

### Row 4: **UP Volume**

```

UP↑ | -1.263K | ████████ | █

█

█

```

- Total **buying volume** this bar

- Higher = Stronger buying pressure

- Green/Orange vertical bars = Bullish strength

### Row 5: **DOWN Volume**

```

DN↓ | 2.643K | ████████ | ░

░

░

```

- Total **selling volume** this bar

- Higher = Stronger selling pressure

- Gray vertical bars = Bearish strength

### Row 6-7: **Reference Asset** (if enabled)

```

══ REF ══ | ══════ | ████████ | █

█

PRICE▲ | 4130.300 | ████████ | █

█

```

- **REF** = Reference asset header

- **PRICE▲** = Reference price with trend

- Shows if BTC (or chosen asset) is rising/falling

- Compare with your chart to see correlation

### Row 8: **Market Status**

```

◄STATUS► | NEUT | ████░░░░ | ▒

▒

```

- **BULL** = CVD positive + Delta positive = Strong buying

- **BEAR** = CVD negative + Delta negative = Strong selling

- **NEUT** = Mixed signals = Wait for clarity

**Status Colors:**

- **Orange background** = Bullish (good for long)

- **Gray background** = Bearish (good for short)

- **White background** = Neutral (no clear signal)

---

## ⚙️ Settings & Customization

### Main Settings (⚙️)

#### **CVD Reset**

- **None** = CVD never resets (from beginning of data)

- **On Higher Timeframe** = Resets when HTF candle closes

- 15m chart → Resets hourly

- 1h chart → Resets daily

- Recommended for most traders

- **On Session Start** = Resets at market open

- **On Visible Chart** = Resets from leftmost visible bar

#### **Precision**

- **Low (Fast)** = Uses 1m data, faster but less accurate

- **Medium** = Uses 5m data, balanced (recommended)

- **High** = Uses 15m data, most accurate but slower

#### **Cumulative**

- ✅ On = CVD accumulates over time (recommended)

- ❌ Off = Shows only current bar delta

#### **Show Labels**

- ✅ On = Shows CVD value label on chart

- ❌ Off = Cleaner chart, no label

#### **Show Info Table**

- ✅ On = Shows info table (recommended for beginners)

- ❌ Off = Hide table for minimalist view

---

### 🎨 iOS Style Colors

You can customize **every color** to match your chart theme:

#### **Primary Colors**

- **Primary (Orange)** = Main bullish color (#FF9500)

- **Secondary (Gray)** = Main bearish color (#8E8E93)

- **Background** = Table background (#FFFFFF)

- **Text** = Text color (#1C1C1E)

#### **Bullish/Bearish**

- **Bullish (Orange)** = Positive CVD color

- **Bearish (Gray)** = Negative CVD color

- **Opacity** = Zone transparency (0-100%)

- **Show Zone** = Enable/disable shaded area

#### **Table Colors** (📋)

- **Header Background** = Top row background

- **Header Text** = Top row text color

- **Cell Background** = Data cells background

- **Cell Text** = Data cells text color

- **Border** = Table border color

- **Accent Background** = Special rows background

- **Alert Background** = Warning/status background

---

### 📊 Reference Asset Settings

#### **Enable**

- ✅ On = Shows reference asset line

- ❌ Off = Hide reference asset

#### **Symbol**

- Default: `BINANCE:BTCUSDT`

- Can change to any asset:

- `BINANCE:ETHUSDT` (Ethereum)

- `SPX` (S&P 500)

- `DXY` (US Dollar Index)

- Any ticker symbol

#### **Color & Width**

- Customize line appearance

- Width: 1-4 (thickness)

---

## 💡 Trading Strategies

### Strategy 1: CVD Divergence (Beginner-Friendly)

**What to Look For:**

- Price making **higher highs** but CVD making **lower highs** = Bearish divergence

- Price making **lower lows** but CVD making **higher lows** = Bullish divergence

**How to Trade:**

1. Wait for divergence to form

2. Look for confirmation (price reversal, candlestick pattern)

3. Enter trade in divergence direction

4. Stop loss beyond recent high/low

**Example:**

```

Price: /\ /\ /\ (higher highs)

CVD: /\ / \/ (lower highs) = Bearish signal

```

### Strategy 2: CVD Trend Following (Intermediate)

**What to Look For:**

- **Strongly rising CVD** + **rising price** = Strong uptrend

- **Strongly falling CVD** + **falling price** = Strong downtrend

**How to Trade:**

1. Wait for CVD and price moving in same direction

2. Enter on pullbacks to support/resistance

3. Stay in trade while CVD trend continues

4. Exit when CVD trend breaks

**Signals:**

- CVD ▲▲▲ + Price ↑ = Go LONG

- CVD ▼▼▼ + Price ↓ = Go SHORT

### Strategy 3: CVD + Reference Asset (Advanced)

**What to Look For:**

- Your asset **rising** but BTC (reference) **falling** = Relative strength

- Your asset **falling** but BTC (reference) **rising** = Relative weakness

**How to Trade:**

1. Compare CVD movement with BTC

2. If your CVD rises faster than BTC = Buy signal

3. If your CVD falls faster than BTC = Sell signal

4. Use for **pair trading** or **asset selection**

### Strategy 4: Volume Delta Confirmation

**What to Look For:**

- **Large positive Delta** = Strong buying this bar

- **Large negative Delta** = Strong selling this bar

**How to Trade:**

1. Price breaks resistance + Large positive Delta = Confirmed breakout

2. Price breaks support + Large negative Delta = Confirmed breakdown

3. Use Delta to **confirm** price moves, not predict them

**Rules:**

- Delta > 2x average = Very strong pressure

- Delta near zero at key level = Weak move, likely false breakout

---

## 🎓 Reading Real Scenarios

### Scenario 1: Strong Buying Pressure

```

Table Shows:

CVD▲ | 12.5K | ████████ | ████ (CVD rising)

◆DELTA | +2.8K | ████████ | ▲ (Positive delta)

UP↑ | 3.1K | ████████ | ████ (High buy volume)

DN↓ | 0.3K | ██░░░░░░ | ░ (Low sell volume)

◄STATUS► | BULL | ████████ | ████ (Orange background)

```

**Interpretation:** Strong buying, good for LONG trades

### Scenario 2: Distribution (Hidden Selling)

```

Table Shows:

CVD► | 8.2K | ████░░░░ | ▒▒ (CVD flat)

◆DELTA | -1.5K | ████████ | ▼ (Negative delta)

UP↑ | 0.8K | ███░░░░░ | ░ (Low buy volume)

DN↓ | 2.3K | ████████ | ████ (High sell volume)

◄STATUS► | BEAR | ████████ | ░░░░ (Gray background)

```

**Interpretation:** Price may look stable, but selling increasing = Prepare for drop

### Scenario 3: Neutral/Choppy Market

```

Table Shows:

CVD► | 5.1K | ████░░░░ | ▒ (CVD sideways)

◆DELTA | +0.2K | ██░░░░░░ | ─ (Small delta)

UP↑ | 1.2K | ████░░░░ | ▒ (Medium buy)

DN↓ | 1.0K | ████░░░░ | ▒ (Medium sell)

◄STATUS► | NEUT | ████░░░░ | ▒▒ (White background)

```

**Interpretation:** No clear direction = Stay out or reduce position size

---

## ⚠️ Common Mistakes to Avoid

### Mistake 1: Trading on CVD Alone

- ❌ **Wrong:** "CVD is rising, I'll buy immediately"

- ✅ **Right:** "CVD is rising, let me check price structure, support/resistance, and wait for confirmation"

### Mistake 2: Ignoring Delta

- ❌ **Wrong:** Looking only at cumulative CVD

- ✅ **Right:** Watch both CVD (trend) and Delta (momentum)

- Delta shows **immediate** pressure changes

### Mistake 3: Wrong Timeframe

- ❌ **Wrong:** Using 1m chart with High Precision (too slow)

- ✅ **Right:** Match precision to timeframe:

- 1m-5m → Low Precision

- 15m-1h → Medium Precision

- 4h+ → High Precision

### Mistake 4: Not Using Reset

- ❌ **Wrong:** Using "None" reset for intraday trading

- ✅ **Right:** Use "On Higher Timeframe" to see fresh CVD each session

### Mistake 5: Overtrading Neutral Status

- ❌ **Wrong:** Forcing trades when STATUS = NEUT

- ✅ **Right:** Only trade clear BULL or BEAR status

### Mistake 6: Ignoring Reference Asset

- ❌ **Wrong:** Trading altcoin without checking BTC

- ✅ **Right:** Always check if BTC CVD agrees with your asset

---

## 🔥 Pro Tips

### Tip 1: Multi-Timeframe Analysis

- Check CVD on **3 timeframes**:

- Lower TF (15m) = Entry timing

- Current TF (1h) = Trade direction

- Higher TF (4h) = Overall trend

### Tip 2: Volume Confirmation

- Big price move + Small Delta = **Weak move** (likely reversal)

- Small price move + Big Delta = **Strong accumulation** (continuation)

### Tip 3: CVD Reset Zones

- Pay attention to **reset backgrounds** (light gray)

- Often marks **session starts** = High volatility periods

### Tip 4: Divergence + Status

- Bearish divergence + STATUS = BEAR = **Strongest short signal**

- Bullish divergence + STATUS = BULL = **Strongest long signal**

### Tip 5: Color Psychology

- **Orange** (Bullish) is **warm** = Buying energy

- **Gray** (Bearish) is **cool** = Selling pressure

- Train your eye to read colors instantly

### Tip 6: Table as Quick Scan

- Glance at table without reading numbers:

- **All orange** = Bullish

- **All gray** = Bearish

- **Mixed** = Wait

---

## 📱 Quick Reference Card

| Signal | CVD | Delta | Status | Action |

|--------|-----|-------|--------|--------|

| **Strong Buy** | ▲▲ High | ++ Positive | BULL | Long Entry |

| **Strong Sell** | ▼▼ Low | -- Negative | BEAR | Short Entry |

| **Divergence Buy** | ▲ Rising | Price ▼ | → BULL | Long Setup |

| **Divergence Sell** | ▼ Falling | Price ▲ | → BEAR | Short Setup |

| **Neutral** | → Flat | ~0 Near Zero | NEUT | Stay Out |

| **Accumulation** | → Flat | ++ Positive | NEUT→BULL | Watch for Breakout |

| **Distribution** | → Flat | -- Negative | NEUT→BEAR | Watch for Breakdown |

---

## 🆘 Troubleshooting

### Issue: "Indicator not showing"

- **Solution:** Make sure overlay=true in code, re-add to chart

### Issue: "Table overlaps with price"

- **Solution:** Change table position in code or use TradingView's "Move" feature

### Issue: "CVD line too far from price"

- **Solution:** This is normal! CVD is volume-based, not price-based. Focus on CVD direction, not position

### Issue: "Too many lines on chart"

- **Solution:** Disable "Show Zone" and "Show Labels" in settings for cleaner view

### Issue: "Calculations too slow"

- **Solution:** Change Precision to "Low (Fast)" or use higher timeframe

### Issue: "Reference asset not showing"

- **Solution:** Check if "Enable" is ON and symbol is valid (e.g., BINANCE:BTCUSDT)

---

## 🎬 Getting Started Checklist

- Install indicator on TradingView

- Set precision to "Medium"

- Set reset to "On Higher Timeframe"

- Enable info table

- Add reference asset (BTC)

- Practice reading the table on demo account

- Test on different timeframes (15m, 1h, 4h)

- Compare CVD with your current strategy

- Paper trade for 1 week before going live

- Keep a trading journal of CVD signals

---

## 📚 Summary

**CVD shows WHO is winning: Buyers or Sellers**

**Key Points:**

1. **Orange/Rising CVD** = Buying pressure = Bullish

2. **Gray/Falling CVD** = Selling pressure = Bearish

3. **Delta** = Immediate momentum THIS BAR

4. **Status** = Overall market condition

5. **Always confirm** with price action & other indicators

**Remember:**

- CVD is a **tool**, not a crystal ball

- Use with proper risk management

- Practice makes perfect

- Stay disciplined!

---

**Created by: able**

**Version:** iOS Style v1.0

**Contact:** For questions, refer to TradingView community

Happy Trading! 🚀📈

200SMA Distance OscillatorThe oscillator measures the percentage deviation of closing price x from SMA200.

The idea behind the oscillator was preceded by an analysis of how often MAs in the index hold/bounce or are broken through.

Basically, the idea was about index analysis, i.e., the macro picture of a market.

Who wants to buy individual stocks when the overall market is plummeting ;-)

Or in other words: How long are you long in a market? When is it time to take profits?

After the analysis of the stability of SMAs in the index was rather modest (ratio of just under 6:4 for bounce to breakout – overall in 20, 50, 100, and 200 frames from 2020 to 2025), it was noticeable that the percentage over- or underperformance was scalable, especially in indices.

And since indices generally move upwards, there were fixed limits for over- and underestimations – especially in the longer term (SMA200) – unlike with individual stocks.

It is therefore more a question of macro trends and less of short-term movements, e.g., in day trading.

It was now interesting to see at what percentage range counter-movements were likely – particularly in the positive range for profit-taking, but of course also in the negative range for entry into sold-off markets.

If, for example, closing prices around +25% above SMA200 were reached in the NDX, the probability is very high that the market has overreacted and an interim correction will follow – so the theory goes.

On the other hand, continuous levels of +5 to +10% are a product of healthy positive development in a bull market and do not necessarily require action.

The oscillator was specifically designed for the NDX, but can also be used for the SPX and others.

The style was based on the RSI, so that the color level rises from 10% to 20% (overbought/oversold principle).

Based on manually examined movements, the criteria were set as follows:

+/-10% = flow / no color background

> +/-10% = border areas / color background

The center line represents the 252 average of the percentage deviations and could also be used as a trigger, provided it has been historically examined and is valid.

The oscillator is very interesting because it behaves completely differently from one financial instrument to another and, as a result, also in the timeframes (4h, D, W).

It would probably make sense to change the flow and border levels in the code when using it outside of indices.

The fact is that the oscillator must be “adjusted” to each instrument in order to achieve its goal of providing the best possible prediction. “Adjusting” refers to the analysis of the levels at which an instrument/asset usually reacts.

As with all indicators and oscillators, it is advisable to take other indicators and, in particular, macro news into account when analyzing this development.

If I find any substantial correlations with other indicators, I will be happy to provide an update.

The idea came from me, the code from Grok.

The code is not 100% perfect, but the data (percentage deviation, color background) is correct according to initial analysis.

In the settings, you can make the lines of the plots invisible. This makes the oscillator clearer. You can also adjust the settings for the average line.

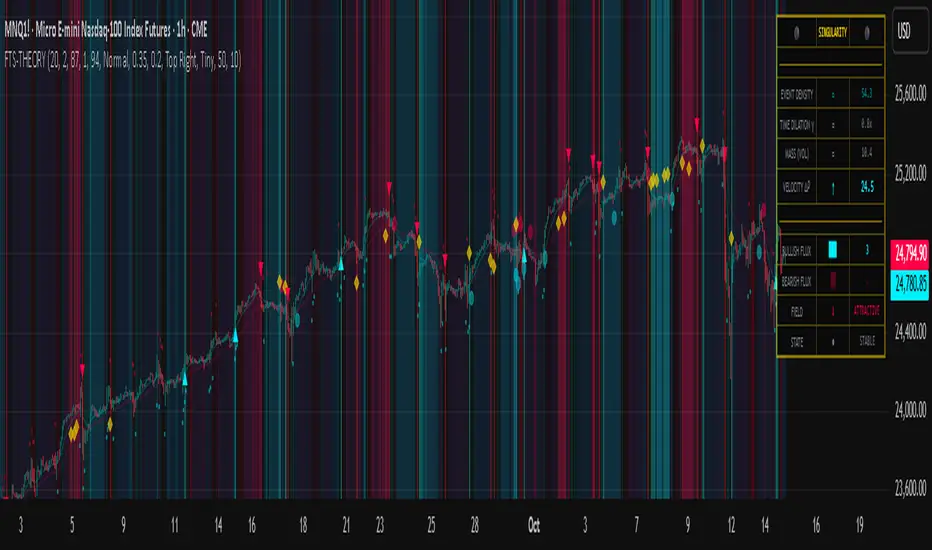

Flux-Tensor Singularity [FTS]Flux-Tensor Singularity - Multi-Factor Market Pressure Indicator

The Flux-Tensor Singularity (FTS) is an advanced multi-factor oscillator that combines volume analysis, momentum tracking, and volatility-weighted normalization to identify critical market inflection points. Unlike traditional single-factor indicators, FTS synthesizes price velocity, volume mass, and volatility context into a unified framework that adapts to changing market regimes.

This indicator identifies extreme market conditions (termed "singularities") where multiple confirming factors converge, then uses a sophisticated scoring system to determine directional bias. It is designed for traders seeking high-probability setups with built-in confluence requirements.

THEORETICAL FOUNDATION

The indicator is built on the premise that market time is not constant - different market conditions contain varying levels of information density. A 1-minute bar during a major news event contains far more actionable information than a 1-minute bar during overnight low-volume trading. Traditional indicators treat all bars equally; FTS does not.

The theoretical framework draws conceptual parallels to physics (purely as a mental model, not literal physics):

Volume as Mass: Large volume represents significant market participation and "weight" behind price moves. Just as massive objects have stronger gravitational effects, high-volume moves carry more significance.

Price Change as Velocity: The rate of price movement through price space represents momentum and directional force.

Volatility as Time Dilation: When volatility is high relative to its historical norm, the "information density" of each bar increases. The indicator weights these periods more heavily, similar to how time dilates near massive objects in physics.

This is a pedagogical metaphor to create a coherent mental model - the underlying mathematics are standard financial calculations combined in a novel way.

MATHEMATICAL FRAMEWORK

The indicator calculates a composite singularity value through four distinct steps:

Step 1: Raw Singularity Calculation

S_raw = (ΔP × V) × γ²

Where:

ΔP = Price Velocity = close - close

V = Volume Mass = log(volume + 1)

γ² = Time Dilation Factor = (ATR_local / ATR_global)²

Volume Transformation: Volume is log-transformed because raw volume can have extreme outliers (10x-100x normal). The logarithm compresses these spikes while preserving their significance. This is standard practice in volume analysis.

Volatility Weighting: The ratio of short-term ATR (5 periods) to long-term ATR (user-defined lookback) is squared to create a volatility amplification factor. When local volatility exceeds global volatility, this ratio increases, amplifying the raw singularity value. This makes the indicator regime-aware.

Step 2: Normalization

The raw singularity values are normalized to a 0-100 scale using a stochastic-style calculation:

S_normalized = ((S_raw - S_min) / (S_max - S_min)) × 100

Where S_min and S_max are the lowest and highest raw singularity values over the lookback period.

Step 3: Epsilon Compression

S_compressed = 50 + ((S_normalized - 50) / ε)

This is the critical innovation that makes the sensitivity control functional. By applying compression AFTER normalization, the epsilon parameter actually affects the final output:

ε < 1.0: Expands range (more signals)

ε = 1.0: No change (default)

ε > 1.0: Compresses toward 50 (fewer, higher-quality signals)

For example, with ε = 2.0, a normalized value of 90 becomes 70, making threshold breaches rarer and more significant.

Step 4: Smoothing

S_final = EMA(S_compressed, smoothing_period)

An exponential moving average removes high-frequency noise while preserving trend.

SIGNAL GENERATION LOGIC

When the tensor crosses above the upper threshold (default 90) or below the lower threshold (default 10), an extreme event is detected. However, the indicator does NOT immediately generate a buy or sell signal. Instead, it analyzes market context through a multi-factor scoring system:

Scoring Components:

Price Structure (+1 point): Current bar bullish/bearish

Momentum (+1 point): Price higher/lower than N bars ago

Trend Context (+2 points): Fast EMA above/below slow EMA (weighted heavier)

Acceleration (+1 point): Rate of change increasing/decreasing

Volume Multiplier (×1.5): If volume > average, multiply score

The highest score (bullish vs bearish) determines signal direction. This prevents the common indicator failure mode of "overbought can stay overbought" by requiring directional confirmation.

Signal Conditions:

A BUY signal requires:

Extreme event detection (tensor crosses threshold)

Bullish score > Bearish score

Price confirmation: Bullish candle (optional, user-controlled)

Volume confirmation: Volume > average (optional, user-controlled)

Momentum confirmation: Positive momentum (optional, user-controlled)

A SELL signal requires the inverse conditions.

INPUTS EXPLAINED - Core Parameters:

Global Horizon (Context): Default 20. Lookback period for normalization and volatility comparison. Higher values = smoother but less responsive. Lower values = more signals but potentially more noise.

Tensor Smoothing: Default 3. EMA period applied to final output. Removes "quantum foam" (high-frequency noise). Range 1-20.

Singularity Threshold: Default 90. Values above this (or below 100-threshold) trigger extreme event detection. Higher = rarer, stronger signals.

Signal Sensitivity (Epsilon): Default 1.0. Post-normalization compression factor. This is the key innovation - it actually works because it's applied AFTER normalization. Range 0.1-5.0.

Signal Interpreter Toggles:

Require Price Confirmation: Default ON. Only generates buy signals on bullish candles, sell signals on bearish candles. Reduces false signals but may delay entry.

Require Volume Confirmation: Default ON. Only signals when volume > average. Critical for stocks/crypto, less important for forex (unreliable volume data).

Use Momentum Filter: Default ON. Requires momentum agreement with signal direction. Prevents counter-trend signals.

Momentum Lookback: Default 5. Number of bars for momentum calculation. Shorter = more responsive, longer = trend-following bias.

Visual Controls:

Colors: Customizable colors for bullish flux, bearish flux, background, and event horizon.

Visual Transparency: Default 85. Master control for all visual elements (accretion disk, field lines, particles, etc.). Range 50-99. Signals and dashboard have separate controls.

Visibility Toggles: Individual on/off switches for:

Gravitational field lines (trend EMAs)

Field reversals (trend crossovers)

Accretion disk (background gradient)

Singularity diamonds (neutral extreme events)

Energy particles (volume bursts)

Event horizon flash (extreme event background)

Signal background flash

Signal Size: Tiny/Small/Normal triangle size

Signal Offsets: Separate controls for buy and sell signal vertical positioning (percentage of price)

Dashboard Settings:

Show Dashboard: Toggle on/off

Position: 9 placement options (all corners, centers, middles)

Text Size: Tiny/Small/Normal/Large

Background Transparency: 0-50, separate from visual transparency

VISUAL ELEMENTS EXPLAINED

1. Accretion Disk (Background Gradient):

A three-layer gradient background that intensifies as the tensor approaches extremes. The outer disk appears at any non-neutral reading, the inner disk activates above 70 or below 30, and the core layer appears above 85 or below 15. Color indicates direction (cyan = bullish, red = bearish). This provides instant visual feedback on market pressure intensity.

2. Gravitational Field Lines (EMAs):

Two trend-following EMAs (10 and 30 period) visualized as colored lines. These represent the "curvature" of market trend - when they diverge, trend is strong; when they converge, trend is weakening. Crossovers mark potential trend reversals.

3. Field Reversals (Circles):

Small circles appear when the fast EMA crosses the slow EMA, indicating a potential trend change. These are distinct from extreme events and appear at normal market structure shifts.

4. Singularity Diamonds:

Small diamond shapes appear when the tensor reaches extreme levels (>90 or <10) but doesn't meet the full signal criteria. These are "watch" events - extreme pressure exists but directional confirmation is lacking.

5. Energy Particles (Dots):

Tiny dots appear when volume exceeds 2× average, indicating significant participation. Color matches bar direction. These highlight genuine high-conviction moves versus low-volume drifts.

6. Event Horizon Flash:

A golden background flash appears the instant any extreme threshold is breached, before directional analysis. This alerts you to pay attention.

7. Signal Background Flash:

When a full buy/sell signal is confirmed, the background flashes cyan (buy) or red (sell). This is your primary alert that all conditions are met.

8. Signal Triangles:

The actual buy (▲) and sell (▼) markers. These only appear when ALL selected confirmation criteria are satisfied. Position is offset from bars to avoid overlap with other indicators.

DASHBOARD METRICS EXPLAINED

The dashboard displays real-time calculated values:

Event Density: Current tensor value (0-100). Above 90 or below 10 = critical. Icon changes: 🔥 (extreme high), ❄️ (extreme low), ○ (neutral).

Time Dilation (γ): Current volatility ratio squared. Values >2.0 indicate extreme volatility environments. >1.5 = elevated, >1.0 = above average. Icon: ⚡ (extreme), ⚠ (elevated), ○ (normal).

Mass (Vol): Log-transformed volume value. Compared to volume ratio (current/average). Icon: ● (>2× avg), ◐ (>1× avg), ○ (below avg).

Velocity (ΔP): Raw price change. Direction arrow indicates momentum direction. Shows the actual price delta value.

Bullish Flux: Current bullish context score. Displayed as both a bar chart (visual) and numeric value. Brighter when bullish score dominates.

Bearish Flux: Current bearish context score. Same visualization as bullish flux. These scores compete - the winner determines signal direction.

Field: Trend direction based on EMA relationship. "Repulsive" (uptrend), "Attractive" (downtrend), "Neutral" (ranging). Icon: ⬆⬇↔

State: Current market condition:

🚀 EJECTION: Buy signal active

💥 COLLAPSE: Sell signal active

⚠ CRITICAL: Extreme event, no directional confirmation

● STABLE: Normal market conditions

HOW TO USE THE INDICATOR

1. Wait for Extreme Events:

The indicator is designed to be selective. Don't trade every fluctuation - wait for tensor to reach >90 or <10. This alone is not a signal.

2. Check Context Scores:

Look at the Bullish Flux vs Bearish Flux in the dashboard. If scores are close (within 1-2 points), the market is indecisive - skip the trade.

3. Confirm with Signals:

Only act when a full triangle signal appears (▲ or ▼). This means ALL your selected confirmation criteria have been met.

4. Use with Price Structure:

Combine with support/resistance levels. A buy signal AT support is higher probability than a buy signal in the middle of nowhere.

5. Respect the Dashboard State:

When State shows "CRITICAL" (⚠), it means extreme pressure exists but direction is unclear. These are the most dangerous moments - wait for resolution.

6. Volume Matters:

Energy particles (dots) and the Mass metric tell you if institutions are participating. Signals without volume confirmation are lower probability.

MARKET AND TIMEFRAME RECOMMENDATIONS

Scalping (1m-5m):

Lookback: 10-14

Smoothing: 5-7

Threshold: 85

Epsilon: 0.5-0.7

Note: Expect more noise. Confirm with Level 2 data. Best on highly liquid instruments.

Intraday (15m-1h):

Lookback: 20-30 (default settings work well)

Smoothing: 3-5

Threshold: 90

Epsilon: 1.0

Note: Sweet spot for the indicator. High win rate on liquid stocks, forex majors, and crypto.

Swing Trading (4h-1D):

Lookback: 30-50

Smoothing: 3

Threshold: 90-95

Epsilon: 1.5-2.0

Note: Signals are rare but high conviction. Combine with higher timeframe trend analysis.

Position Trading (1D-1W):

Lookback: 50-100

Smoothing: 5-7

Threshold: 95

Epsilon: 2.0-3.0

Note: Extremely rare signals. Only trade the most extreme events. Expect massive moves.

Market-Specific Settings:

Forex (EUR/USD, GBP/USD, etc.):

Volume data is unreliable (spot forex has no centralized volume)

Disable "Require Volume Confirmation"

Focus on momentum and trend filters

News events create extreme singularities

Best on 15m-1h timeframes

Stocks (High-Volume Equities):

Volume confirmation is CRITICAL - keep it ON

Works excellently on AAPL, TSLA, SPY, etc.

Morning session (9:30-11:00 ET) shows highest event density

Earnings announcements create guaranteed extreme events

Best on 5m-1h for day trading, 1D for swing trading

Crypto (BTC, ETH, major alts):

Reduce threshold to 85 (crypto has constant high volatility)

Volume spikes are THE primary signal - keep volume confirmation ON

Works exceptionally well due to 24/7 trading and high volatility

Epsilon can be reduced to 0.7-0.8 for more signals

Best on 15m-4h timeframes

Commodities (Gold, Oil, etc.):

Gold responds to macro events (Fed announcements, geopolitical events)

Oil responds to supply shocks

Use daily timeframe minimum

Increase lookback to 50+

These are slow-moving markets - be patient

Indices (SPX, NDX, etc.):

Institutional volume matters - keep volume confirmation ON

Opening hour (9:30-10:30 ET) = highest singularity probability

Strong correlation with VIX - high VIX = more extreme events

Best on 15m-1h for day trading

WHAT MAKES THIS INDICATOR UNIQUE

1. Post-Normalization Sensitivity Control:

Unlike most oscillators where sensitivity controls don't actually work (they're applied before normalization, which then rescales everything), FTS applies epsilon compression AFTER normalization. This means the sensitivity parameter genuinely affects signal frequency. This is a novel implementation not found in standard oscillators.

2. Multi-Factor Confluence Requirement:

The indicator doesn't just detect "overbought" or "oversold" - it detects extreme conditions AND THEN analyzes context through five separate factors (price structure, momentum, trend, acceleration, volume). Most indicators are single-factor; FTS requires confluence.

3. Volatility-Weighted Normalization:

By squaring the ATR ratio (local/global), the indicator adapts to changing market regimes. A 1% move in a low-volatility environment is treated differently than a 1% move in a high-volatility environment. Traditional indicators treat all moves equally regardless of context.

4. Volume Integration at the Core:

Volume isn't an afterthought or optional filter - it's baked into the fundamental equation as "mass." The log transformation handles outliers elegantly while preserving significance. Most price-based indicators completely ignore volume.

5. Adaptive Scoring System:

Rather than fixed buy/sell rules ("RSI >70 = sell"), FTS uses competitive scoring where bullish and bearish evidence compete. The winner determines direction. This solves the classic problem of "overbought markets can stay overbought during strong uptrends."

6. Comprehensive Visual Feedback:

The multi-layer visualization system (accretion disk, field lines, particles, flashes) provides instant intuitive feedback on market state without requiring dashboard reading. You can see pressure building before extreme thresholds are hit.

7. Separate Extreme Detection and Signal Generation:

"Singularity diamonds" show extreme events that don't meet full criteria, while "signal triangles" only appear when ALL conditions are met. This distinction helps traders understand when pressure exists versus when it's actionable.

COMPARISON TO EXISTING INDICATORS

vs. RSI/Stochastic:

These normalize price relative to recent range. FTS normalizes (price change × log volume × volatility ratio) - a composite metric, not just price position.

vs. Chaikin Money Flow:

CMF combines price and volume but lacks volatility context and doesn't use adaptive normalization or post-normalization compression.

vs. Bollinger Bands + Volume:

Bollinger Bands show volatility but don't integrate volume or create a unified oscillator. They're separate components, not synthesized.

vs. MACD:

MACD is pure momentum. FTS combines momentum with volume weighting and volatility context, plus provides a normalized 0-100 scale.

The specific combination of log-volume weighting, squared volatility amplification, post-normalization epsilon compression, and multi-factor directional scoring is unique to this indicator.

LIMITATIONS AND PROPER DISCLOSURE

Not a Holy Grail:

No indicator is perfect. This tool identifies high-probability setups but cannot predict the future. Losses will occur. Use proper risk management.

Requires Confirmation:

Best used in conjunction with price action analysis, support/resistance levels, and higher timeframe trend. Don't trade signals blindly.

Volume Data Dependency:

On forex (spot) and some low-volume instruments, volume data is unreliable or tick-volume only. Disable volume confirmation in these cases.

Lagging Components:

The EMA smoothing and trend filters are inherently lagging. In extremely fast moves, signals may appear after the initial thrust.

Extreme Event Rarity:

With conservative settings (high threshold, high epsilon), signals can be rare. This is by design - quality over quantity. If you need more frequent signals, reduce threshold to 85 and epsilon to 0.7.

Not Financial Advice:

This indicator is an analytical tool. All trading decisions and their consequences are solely your responsibility. Past performance does not guarantee future results.

BEST PRACTICES

Don't trade every singularity - wait for context confirmation

Higher timeframes = higher reliability

Combine with support/resistance for entry refinement

Volume confirmation is CRITICAL for stocks/crypto (toggle off only for forex)

During major news events, singularities are inevitable but direction may be uncertain - use wider stops

When bullish and bearish flux scores are close, skip the trade

Test settings on your specific instrument/timeframe before live trading

Use the dashboard actively - it contains critical diagnostic information

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

TICK & ADD Market Internals SuiteOverview: This is the ultimate Market Internals tool designed for professional SPX/ES and NQ intraday traders.

Traders often monitor both TICK (for short-term timing) and ADD (for daily trend context). However, displaying them on the same chart is usually problematic due to their different scales (TICK ±1000 vs. ADD ±2000), causing chart compression.

Market Internals Suite solves this with a smart "Visual Scaling" algorithm, perfectly fusing TICK Candles and the ADD Line into a single, coherent pane.

Key Features

1.Hybrid Visualization:

· TICK (Foreground): Displayed as OHLC Candles to capture instant liquidity sweeps and wicks.

· ADD (Background): Displayed as a clean Line to show the underlying market breadth trend without clutter.

2.Smart Visual Scaling:

· To prevent chart distortion, the ADD line is visually scaled down (Default Ratio: 1.5).

· This aligns the ADD trend volatility with the TICK range, allowing you to instantly spot divergences or resonance between sentiment and trend.

3.Real-Time Data Dashboard:

· Never lose track of the actual numbers. A dashboard in the top-right corner displays the TRUE values for both TICK and ADD (unscaled).

· Customizable Text Size: You can adjust the dashboard font size (Small/Normal/Large/Huge) in the settings to fit your screen.

4.TICK Extreme Alerts:

· Visual Highlight: The chart background highlights (Green/Red) only when TICK hits the extreme ±1000 levels.

· The ADD line remains clean and alert-free to serve as a stable reference.

Strategy: Context + Timing:

1.Trend Resonance

When the ADD line trends upward and TICK candles consistently maintain levels above zero, it indicates a healthy, strong trend. This is a signal to look for trend-following long setups.

2.Divergence Analysis (The "Holy Grail" Signal)

This combination view makes spotting internal divergences incredibly easy:

· Bearish Divergence: When Price makes a New High, but the ADD line or TICK peaks make a Lower High. This suggests buying exhaustion beneath the surface and often precedes a reversal down.

· Bullish Divergence: When Price makes a New Low, but the ADD line or TICK lows make a Higher Low. This suggests that selling pressure is being absorbed, signaling a potential bounce or reversal up.

TICK Indicator with Extreme AlertsOverview:

This indicator is designed to provide intraday traders (especially those trading SPX, ES, and NQ) with a clearer NYSE TICK analysis tool featuring visual alerts. Unlike traditional TICK line charts, this indicator utilizes OHLC Candlesticks to display data, allowing you to fully view the Open, High, Low, and Close within a specific timeframe, thereby capturing instantaneous liquidity sweeps.

Core Features & Logic:

Candlestick Visualization (OHLC Candles): Uses the USI:TICK.US data source by default. The candlestick patterns allow you to clearly see if the TICK pierced key levels intraday but retraced by the close—vital information that standard line charts often miss.

Dual Key Level System: The indicator is designed with two independent reference tiers for trend observation and reversal detection:

Reference Lines (+/- 800): Marked by gray dashed lines. These represent the standard bull/bear dividing zones. When TICK sustains above +800 or below -800, it typically indicates a strong trending market.

Extreme Alerts (+/- 1000): These thresholds are used to identify extreme market sentiment (overbought/oversold conditions).

Background Highlight Alerts (Visual Alerts): To reduce screen-watching fatigue, the indicator automatically highlights the candlestick background when extreme market sentiment occurs:

Green Background: Triggered when TICK High breaks above +1000. Represents extreme buying sentiment, potentially indicating exhaustion or a short squeeze.

Red Background: Triggered when TICK Low drops below -1000. Represents extreme panic selling (Washout), often serving as a potential signal for an intraday reversal or a short-term bottom.

Custom Settings:

All thresholds (800 reference lines, 1000 alert lines) are fully adjustable in the settings.

All colors (Candles, Reference Lines, Background Alert Colors) can be customized.

Use Cases: This tool is ideal for intraday counter-trend or trend-following trading when combined with Price Action analysis and key Support & Resistance levels.

Percentage Distance from 200-Week SMA200-Week SMA % Distance Oscillator (Clean & Simple)

This lightweight, no-nonsense indicator shows how far the current price is from the classic 200-week Simple Moving Average, expressed as a percentage.

Key features:

• True percentage distance: (Price − 200w SMA) / 200w SMA × 100

• Auto-scaling oscillator (no forced ±100% range → the line actually moves and looks alive)

• Clean zero line

• +10% overbought and −10% oversold levels with subtle background shading

• Real-time table showing the exact current percentage

• Small label on the last bar for instant reading

• Alert conditions when price moves >10% above or below the 200-week SMA

Why 200-week SMA?

Many legendary investors and hedge funds (Stan Druckenmiller, Paul Tudor Jones, etc.) use the 200-week SMA as their ultimate long-term trend anchor. Being +10% or more above it has historically signaled extreme optimism, while −10% or lower has marked deep pessimism and generational buying opportunities.

Perfect for Bitcoin, SPX, gold, individual stocks – works on any timeframe (looks especially good on daily and weekly charts).

Open-source • No repainting • Minimalist & fast

Enjoy and trade well!

Trend-S&R-WiP11-15-2025: This new indicator is my 5/15-Min-ORB-Trend-Finder-WiP indicator simplified to only have:

> Market Open

> 5-Min & 15-Min High/Low

> Support/Resistance lines

> Fair Value Gaps (FVGs)

> a Trend Line

> a Trend table

Recommended to be used with my other indicator: Buy-or-Sell-WiP

Strategy:

> I only trade one ticker, SPX, with ODTE CALL/PUT Credit Spreads

> use Break & Retest with 5-Min High/Low or 15-Min High/Low or FVGs

> 📈 Bullish Trend

Trade: PUT Credit Spread

Trend Confirmations:

Trend Line is green

MACD Histogram is green

Price Condition: Nearest resistance 8-10 points above market price

> 📉 Bearish Trend

Trade: CALL Credit Spread

Trend Confirmations:

Trend Line is purple

MACD Histogram is red

Price Condition: Nearest support 8-10 points below market price

> Fair Value Gaps (FVGs)

- Trade anytime during the day using Break & Retest and all indicator confirmations shown above

🎯 Wyckoff Order Block Entry System🎯 Wyckoff Order Block Entry System

📝 INDICATOR DESCRIPTION

🎯 Wyckoff Order Block Entry System Short Description:

Professional institutional zone trading combined with Wyckoff methodology. Identifies high-probability entries where smart money meets classic price action patterns.

Full Description:

Wyckoff Order Block Entry System is a precision trading tool that combines two powerful concepts:

Order Blocks - Institutional zones where large players place their orders

Wyckoff Method - Classic price action patterns revealing smart money behavior

🎯 What Makes This Different?

Unlike traditional indicators that flood your chart with signals, this system only triggers entries when BOTH conditions are met:

Price enters an institutional Order Block zone (current timeframe OR higher timeframe)

A Wyckoff pattern occurs (Spring, SOS, Upthrust, or SOW)

This dual-confirmation approach ensures you're trading with institutional flow at optimal entry points.

📊 Key Features:

✅ Order Block Detection

Automatically identifies institutional buying/selling zones

Current timeframe order blocks (solid lines)

Higher timeframe order blocks (dashed lines) for stronger zones

Customizable strength and extension settings

✅ 4 Wyckoff Entry Patterns

SPRING (Bullish Reversal): Fake breakdown below support → Quick recovery

SOS (Sign of Strength): Strong bullish candle after accumulation

UPTHRUST (Bearish Reversal): Fake breakout above resistance → Quick rejection

SOW (Sign of Weakness): Strong bearish candle after distribution

✅ Clean Visual Design

Minimalist approach - only essential information

Color-coded zones (Green = Bullish, Red = Bearish, Cyan/Magenta = HTF)

Clear entry signals with pattern type labels

No chart clutter - focus on what matters

✅ Multi-Timeframe Analysis

Integrates higher timeframe order blocks

HTF signals marked with "+HTF" tag for extra confidence

Fully customizable HTF selection (H1, H4, Daily, etc.)

✅ Smart Alerts

Entry signal alerts (Long/Short)

Order block formation alerts

HTF order block alerts

Customizable alert messages

💡 How To Use:

Setup: Add indicator to your chart, configure HTF timeframe (default H1)

Wait: Let order blocks form (green/red boxes appear)

Watch: Price returns to order block zone

Entry: Signal appears when Wyckoff pattern confirms

Trade: Enter with the signal, stop below/above order block

📈 Best For:

Forex pairs (all majors and crosses)

Gold (XAUUSD)

Crypto (BTC, ETH, etc.)

Indices (SPX, NAS100, etc.)

Stocks

Commodities

⏱️ Recommended Timeframes:

M15 for scalping

M30 for day trading

H1 for swing trading

H4 for position trading

🎯 Win Rate Expectations:

Current TF signals: 60-70%

HTF signals (+HTF tag): 70-80%

Spring/Upthrust patterns: Highest probability

Works on ALL liquid markets

⚙️ Customizable Settings:

Order block detection parameters

HTF timeframe selection

Wyckoff sensitivity (swing length, volume threshold)

Zone extension duration

Color schemes

📚 Trading Strategy:

This indicator works best when:

Trading in the direction of higher timeframe trend

Using proper risk management (1-2% per trade)

Placing stops just outside order block zones

Taking profits at opposite order blocks

Focusing on HTF signals for higher quality

🔒 Risk Management:

Always use stop losses! Recommended placement:

LONG: 10-20 pips below order block

SHORT: 10-20 pips above order block

Target: Minimum 1:2 risk/reward ratio

💎 Why Traders Love This System:

"Finally, an indicator that doesn't spam my chart with useless signals!" - The quality-over-quantity approach means you only get high-probability setups.

"The HTF order blocks changed my trading!" - Multi-timeframe analysis built-in removes the need for manual higher timeframe checks.

"Wyckoff + Order Blocks = Perfect combination!" - Two proven concepts working together create powerful confluence.

📊 Universal Application:

This system works on ANY liquid market with sufficient volume:

✅ Forex (EUR/USD, GBP/USD, USD/JPY, etc.)

✅ Commodities (Gold, Silver, Oil, etc.)

✅ Indices (S&P 500, NASDAQ, DAX, etc.)

✅ Cryptocurrencies (Bitcoin, Ethereum, etc.)

✅ Stocks (Large cap with good liquidity)

🎓 Educational Value:

Beyond just signals, this indicator teaches you:

How institutional traders think

Where smart money places orders

Classic Wyckoff accumulation/distribution patterns

Multi-timeframe analysis techniques

⚡ Performance:

Lightning-fast calculations

No repainting

Real-time signal generation

Clean code, optimized for speed

🚀 Get Started:

Add to your favorite chart

Adjust HTF timeframe to match your trading style

Wait for high-quality signals

Trade with confidence

Remember: Quality beats quantity. This system prioritizes precision over frequency. You might see 2-5 signals per day on M30 - and that's exactly the point. Each signal is carefully filtered for maximum probability.

Ready to trade like institutions?

👉 Add this indicator to your chart now

👉 Configure your preferred HTF timeframe

👉 Start catching high-probability setups

👉 Trade smarter, not harder

Questions or feedback? Drop a comment below!

Found this useful? Hit that ⭐ button and share with fellow traders!

Happy Trading! 🚀📈

Volatility-Targeted Momentum Portfolio [BackQuant]Volatility-Targeted Momentum Portfolio

A complete momentum portfolio engine that ranks assets, targets a user-defined volatility, builds long, short, or delta-neutral books, and reports performance with metrics, attribution, Monte Carlo scenarios, allocation pie, and efficiency scatter plots. This description explains the theory and the mechanics so you can configure, validate, and deploy it with intent.

Table of contents

What the script does at a glance

Momentum, what it is, how to know if it is present

Volatility targeting, why and how it is done here

Portfolio construction modes: Long Only, Short Only, Delta Neutral

Regime filter and when the strategy goes to cash

Transaction cost modelling in this script

Backtest metrics and definitions

Performance attribution chart

Monte Carlo simulation

Scatter plot analysis modes

Asset allocation pie chart

Inputs, presets, and deployment checklist

Suggested workflow

1) What the script does at a glance

Pulls a list of up to 15 tickers, computes a simple momentum score on each over a configurable lookback, then volatility-scales their bar-to-bar return stream to a target annualized volatility.

Ranks assets by raw momentum, selects the top 3 and bottom 3, builds positions according to the chosen mode, and gates exposure with a fast regime filter.

Accumulates a portfolio equity curve with risk and performance metrics, optional benchmark buy-and-hold for comparison, and a full alert suite.

Adds visual diagnostics: performance attribution bars, Monte Carlo forward paths, an allocation pie, and scatter plots for risk-return and factor views.

2) Momentum: definition, detection, and validation

Momentum is the tendency of assets that have performed well to continue to perform well, and of underperformers to continue underperforming, over a specific horizon. You operationalize it by selecting a horizon, defining a signal, ranking assets, and trading the leaders versus laggards subject to risk constraints.

Signal choices . Common signals include cumulative return over a lookback window, regression slope on log-price, or normalized rate-of-change. This script uses cumulative return over lookback bars for ranking (variable cr = price/price - 1). It keeps the ranking simple and lets volatility targeting handle risk normalization.

How to know momentum is present .

Leaders and laggards persist across adjacent windows rather than flipping every bar.

Spread between average momentum of leaders and laggards is materially positive in sample.

Cross-sectional dispersion is non-trivial. If everything is flat or highly correlated with no separation, momentum selection will be weak.

Your validation should include a diagnostic that measures whether returns are explained by a momentum regression on the timeseries.

Recommended diagnostic tool . Before running any momentum portfolio, verify that a timeseries exhibits stable directional drift. Use this indicator as a pre-check: It fits a regression to price, exposes slope and goodness-of-fit style context, and helps confirm if there is usable momentum before you force a ranking into a flat regime.

3) Volatility targeting: purpose and implementation here

Purpose . Volatility targeting seeks a more stable risk footprint. High-vol assets get sized down, low-vol assets get sized up, so each contributes more evenly to total risk.

Computation in this script (per asset, rolling):

Return series ret = log(price/price ).

Annualized volatility estimate vol = stdev(ret, lookback) * sqrt(tradingdays).

Leverage multiplier volMult = clamp(targetVol / vol, 0.1, 5.0).

This caps sizing so extremely low-vol assets don’t explode weight and extremely high-vol assets don’t go to zero.

Scaled return stream sr = ret * volMult. This is the per-bar, risk-adjusted building block used in the portfolio combinations.

Interpretation . You are not levering your account on the exchange, you are rescaling the contribution each asset’s daily move has on the modeled equity. In live trading you would reflect this with position sizing or notional exposure.

4) Portfolio construction modes

Cross-sectional ranking . Assets are sorted by cr over the chosen lookback. Top and bottom indices are extracted without ties.

Long Only . Averages the volatility-scaled returns of the top 3 assets: avgRet = mean(sr_top1, sr_top2, sr_top3). Position table shows per-asset leverages and weights proportional to their current volMult.

Short Only . Averages the negative of the volatility-scaled returns of the bottom 3: avgRet = mean(-sr_bot1, -sr_bot2, -sr_bot3). Position table shows short legs.

Delta Neutral . Long the top 3 and short the bottom 3 in equal book sizes. Each side is sized to 50 percent notional internally, with weights within each side proportional to volMult. The return stream mixes the two sides: avgRet = mean(sr_top1,sr_top2,sr_top3, -sr_bot1,-sr_bot2,-sr_bot3).

Notes .

The selection metric is raw momentum, the execution stream is volatility-scaled returns. This separation is deliberate. It avoids letting volatility dominate ranking while still enforcing risk parity at the return contribution stage.

If everything rallies together and dispersion collapses, Long Only may behave like a single beta. Delta Neutral is designed to extract cross-sectional momentum with low net beta.

5) Regime filter

A fast EMA(12) vs EMA(21) filter gates exposure.

Long Only active when EMA12 > EMA21. Otherwise the book is set to cash.

Short Only active when EMA12 < EMA21. Otherwise cash.

Delta Neutral is always active.

This prevents taking long momentum entries during obvious local downtrends and vice versa for shorts. When the filter is false, equity is held flat for that bar.

6) Transaction cost modelling

There are two cost touchpoints in the script.

Per-bar drag . When the regime filter is active, the per-bar return is reduced by fee_rate * avgRet inside netRet = avgRet - (fee_rate * avgRet). This models proportional friction relative to traded impact on that bar.

Turnover-linked fee . The script tracks changes in membership of the top and bottom baskets (top1..top3, bot1..bot3). The intent is to charge fees when composition changes. The template counts changes and scales a fee by change count divided by 6 for the six slots.

Use case: increase fee_rate to reflect taker fees and slippage if you rebalance every bar or trade illiquid assets. Reduce it if you rebalance less often or use maker orders.

Practical advice .

If you rebalance daily, start with 5–20 bps round-trip per switch on liquid futures and adjust per venue.

For crypto perp microcaps, stress higher cost assumptions and add slippage buffers.

If you only rotate on lookback boundaries or at signals, use alert-driven rebalances and lower per-bar drag.

7) Backtest metrics and definitions

The script computes a standard set of portfolio statistics once the start date is reached.

Net Profit percent over the full test.

Max Drawdown percent, tracked from running peaks.

Annualized Mean and Stdev using the chosen trading day count.

Variance is the square of annualized stdev.

Sharpe uses daily mean adjusted by risk-free rate and annualized.

Sortino uses downside stdev only.

Omega ratio of sum of gains to sum of losses.

Gain-to-Pain total gains divided by total losses absolute.

CAGR compounded annual growth from start date to now.

Alpha, Beta versus a user-selected benchmark. Beta from covariance of daily returns, Alpha from CAPM.

Skewness of daily returns.

VaR 95 linear-interpolated 5th percentile of daily returns.

CVaR average of the worst 5 percent of daily returns.

Benchmark Buy-and-Hold equity path for comparison.

8) Performance attribution

Cumulative contribution per asset, adjusted for whether it was held long or short and for its volatility multiplier, aggregated across the backtest. You can filter to winners only or show both sides. The panel is sorted by contribution and includes percent labels.

9) Monte Carlo simulation

The panel draws forward equity paths from either a Normal model parameterized by recent mean and stdev, or non-parametric bootstrap of recent daily returns. You control the sample length, number of simulations, forecast horizon, visibility of individual paths, confidence bands, and a reproducible seed.

Normal uses Box-Muller with your seed. Good for quick, smooth envelopes.

Bootstrap resamples realized returns, preserving fat tails and volatility clustering better than a Gaussian assumption.

Bands show 10th, 25th, 75th, 90th percentiles and the path mean.

10) Scatter plot analysis

Four point-cloud modes, each plotting all assets and a star for the current portfolio position, with quadrant guides and labels.

Risk-Return Efficiency . X is risk proxy from leverage, Y is expected return from annualized momentum. The star shows the current book’s composite.

Momentum vs Volatility . Visualizes whether leaders are also high vol, a cue for turnover and cost expectations.

Beta vs Alpha . X is a beta proxy, Y is risk-adjusted excess return proxy. Useful to see if leaders are just beta.

Leverage vs Momentum . X is volMult, Y is momentum. Shows how volatility targeting is redistributing risk.

11) Asset allocation pie chart

Builds a wheel of current allocations.

Long Only, weights are proportional to each long asset’s current volMult and sum to 100 percent.

Short Only, weights show the short book as positive slices that sum to 100 percent.

Delta Neutral, 50 percent long and 50 percent short books, each side leverage-proportional.

Labels can show asset, percent, and current leverage.

12) Inputs and quick presets

Core

Portfolio Strategy . Long Only, Short Only, Delta Neutral.

Initial Capital . For equity scaling in the panel.

Trading Days/Year . 252 for stocks, 365 for crypto.

Target Volatility . Annualized, drives volMult.

Transaction Fees . Per-bar drag and composition change penalty, see the modelling notes above.

Momentum Lookback . Ranking horizon. Shorter is more reactive, longer is steadier.

Start Date . Ensure every symbol has data back to this date to avoid bias.

Benchmark . Used for alpha, beta, and B&H line.

Diagnostics

Metrics, Equity, B&H, Curve labels, Daily return line, Rolling drawdown fill.

Attribution panel. Toggle winners only to focus on what matters.

Monte Carlo mode with Normal or Bootstrap and confidence bands.

Scatter plot type and styling, labels, and portfolio star.

Pie chart and labels for current allocation.

Presets

Crypto Daily, Long Only . Lookback 25, Target Vol 50 percent, Fees 10 bps, Regime filter on, Metrics and Drawdown on. Monte Carlo Bootstrap with Recent 200 bars for bands.

Crypto Daily, Delta Neutral . Lookback 25, Target Vol 50 percent, Fees 15–25 bps, Regime filter always active for this mode. Use Scatter Risk-Return to monitor efficiency and keep the star near upper left quadrants without drifting rightward.

Equities Daily, Long Only . Lookback 60–120, Target Vol 15–20 percent, Fees 5–10 bps, Regime filter on. Use Benchmark SPX and watch Alpha and Beta to keep the book from becoming index beta.

13) Suggested workflow

Universe sanity check . Pick liquid tickers with stable data. Thin assets distort vol estimates and fees.

Check momentum existence . Run on your timeframe. If slope and fit are weak, widen lookback or avoid that asset or timeframe.

Set risk budget . Choose a target volatility that matches your drawdown tolerance. Higher target increases turnover and cost sensitivity.

Pick mode . Long Only for bull regimes, Short Only for sustained downtrends, Delta Neutral for cross-sectional harvesting when index direction is unclear.

Tune lookback . If leaders rotate too often, lengthen it. If entries lag, shorten it.

Validate cost assumptions . Increase fee_rate and stress Monte Carlo. If the edge vanishes with modest friction, refine selection or lengthen rebalance cadence.

Run attribution . Confirm the strategy’s winners align with intuition and not one unstable outlier.

Use alerts . Enable position change, drawdown, volatility breach, regime, momentum shift, and crash alerts to supervise live runs.

Important implementation details mapped to code

Momentum measure . cr = price / price - 1 per symbol for ranking. Simplicity helps avoid overfitting.

Volatility targeting . vol = stdev(log returns, lookback) * sqrt(tradingdays), volMult = clamp(targetVol / vol, 0.1, 5), sr = ret * volMult.

Selection . Extract indices for top1..top3 and bot1..bot3. The arrays rets, scRets, lev_vals, and ticks_arr track momentum, scaled returns, leverage multipliers, and display tickers respectively.

Regime filter . EMA12 vs EMA21 switch determines if the strategy takes risk for Long or Short modes. Delta Neutral ignores the gate.

Equity update . Equity multiplies by 1 + netRet only when the regime was active in the prior bar. Buy-and-hold benchmark is computed separately for comparison.

Tables . Position tables show current top or bottom assets with leverage and weights. Metric table prints all risk and performance figures.

Visualization panels . Attribution, Monte Carlo, scatter, and pie use the last bars to draw overlays that update as the backtest proceeds.

Final notes

Momentum is a portfolio effect. The edge comes from cross-sectional dispersion, adequate risk normalization, and disciplined turnover control, not from a single best asset call.

Volatility targeting stabilizes path but does not fix selection. Use the momentum regression link above to confirm structure exists before you size into it.

Always test higher lag costs and slippage, then recheck metrics, attribution, and Monte Carlo envelopes. If the edge persists under stress, you have something robust.