DSL Strategy [DailyPanda]

Overview

The DSL Strategy by DailyPanda is a trading strategy that synergistically combines the idea from indicators to create a more robust and reliable trading tool. By integrating these indicators, the strategy enhances signal accuracy and provides traders with a comprehensive view of market trends and momentum shifts. This combination allows for better entry and exit points, improved risk management, and adaptability to various market conditions.

Combining ideas from indicators adds value by:

Enhancing Signal Confirmation : The strategy requires alignment between trend and momentum before generating trade signals, reducing false entries.

Improving Accuracy : By integrating price action with momentum analysis, the strategy captures more reliable trading opportunities.

Providing Comprehensive Market Insight : The combination offers a better perspective on the market, considering both the direction (trend) and the strength (momentum) of price movements.

How the Components Work Together

1. Trend Identification with DSL Indicator

Dynamic Signal Lines : Calculates upper and lower DSL lines based on a moving average (SMA) and dynamic thresholds derived from recent highs and lows with a specified offset. These lines adapt to market conditions, providing real-time trend insights.

ATR-Based Bands : Adds bands around the DSL lines using the Average True Range (ATR) multiplied by a width factor. These bands account for market volatility and help identify potential stop-loss levels.

Trend Confirmation : The relationship between the price, DSL lines, and bands determines the current trend. For example, if the price consistently stays above the upper DSL line, it indicates a bullish trend.

2. Momentum Analysis

RSI Calculation : Computes the RSI over a specified period to measure the speed and change of price movements.

Zero-Lag EMA (ZLEMA) : Applies a ZLEMA to the RSI to minimize lag and produce a more responsive oscillator.

DSL Application on Oscillator : Implements the DSL concept on the oscillator by calculating dynamic upper and lower levels. This helps identify overbought or oversold conditions more accurately.

Signal Generation : Detects crossovers between the oscillator and its DSL lines. A crossover above the lower DSL line signals potential bullish momentum, while a crossover below the upper DSL line signals potential bearish momentum.

3. Integrated Signal Filtering

Confluence Requirement : A trade signal is generated only when both the DSL indicator and oscillator agree. For instance, a long entry requires both an uptrend confirmation from the DSL indicator and a bullish momentum signal from the oscillator.

Risk Management Integration : The strategy uses the DSL indicator's bands for setting stop-loss levels and calculates take-profit levels based on a user-defined risk-reward ratio. This ensures that every trade has a predefined risk management plan.

--------------------------------------------------------------------------------------------

Originality and Value Added to the Community

Unique Synergy : While both indicators are available individually, this strategy is original in how it combines them to enhance their strengths and mitigate their weaknesses, offering a novel approach not present in existing scripts.

Enhanced Reliability : By requiring confirmation from both trend and momentum indicators, the strategy reduces false signals and increases the likelihood of successful trades.

Versatility : The customizable parameters allow traders to adapt the strategy to different instruments, timeframes, and trading styles, making it a valuable tool for a wide range of trading scenarios.

Educational Contribution : The script demonstrates an effective method of combining indicators for improved trading performance, providing insights that other traders can learn from and apply to their own strategies.

--------------------------------------------------------------------------------------------

How to Use the Strategy

Adding the Strategy to Your Chart

Apply the DSL Strategy to your desired trading instrument and timeframe on TradingView.

--------------------------------------------------------------------------------------------

Configuring Parameters

DSL Indicator Settings :

Length (len) : Adjusts the sensitivity of the DSL lines (default is 34).

Offset : Determines the look-back period for threshold calculations (default is 30).

Bands Width (width) : Changes the distance of the ATR-based bands from the DSL lines (default is 1).

DSL-BELUGA Oscillator Settings :

Beluga Length (len_beluga) : Sets the period for the RSI calculation in the oscillator (default is 10).

DSL Lines Mode (dsl_mode) : Chooses between "Fast" (more responsive) and "Slow" (smoother) modes for the oscillator's DSL lines.

Risk Management :

Risk Reward (risk_reward) : Defines your desired risk-reward ratio for calculating take-profit levels (default is 1.5).

--------------------------------------------------------------------------------------------

Interpreting Signals

Long Entry Conditions :

Trend Confirmation : Price is above the upper DSL line and the upper DSL band (dsl_up1 > dsl_dn).

Price Behavior : The last three candles have both their opens and closes above the upper DSL line.

Momentum Signal : The DSL-BELUGA oscillator crosses above its lower DSL line (up_signal), indicating bullish momentum.

Short Entry Conditions :

Trend Confirmation : Price is below the lower DSL line and the lower DSL band (dsl_dn < dsl_up1).

Price Behavior : The last three candles have both their opens and closes below the lower DSL band.

Momentum Signal : The DSL-BELUGA oscillator crosses below its upper DSL line (dn_signal), indicating bearish momentum.

Exit Conditions :

Stop-Loss : Automatically set at the DSL indicator's band level (upper band for longs, lower band for shorts).

Take-Profit : Calculated based on the risk-reward ratio and the initial risk determined by the stop-loss distance.

Visual Aids

Signal Arrows : Upward green arrows for long entries and downward blue arrows for short entries appear on the chart when conditions are met.

Stop-Loss and Take-Profit Lines : Red and green lines display the calculated stop-loss and take-profit levels for active trades.

Background Highlighting : The chart background subtly changes color to indicate when a signal has been generated.

Backtesting and Optimization

Use TradingView's strategy tester to backtest the strategy over historical data.

Adjust parameters to optimize performance for different instruments or market conditions.

Regularly review backtesting results to ensure the strategy remains effective.

Buscar en scripts para "oscillator"

Elder's Force Index Function (with source)TradingView has built in functions for RSI, Momentum, and many other oscillators. Why the source isn't available for Elder's Force Index is beyond me. To me it's one of the Holy Grail indicators. This is EFI indicator with a simple function inside the source code. You're can easily copy this function into any study(indicator) or strategy that uses built-in oscillators, as a replacement.

Example using EFI instead of RSI in built-in Divergence Indicator:

gyazo.com

//Discord: Sheldon#7775

//Server: discord.gg

SynthSAR ConfirmationThis indicator represents confirmation of a trend based on the PSAR indicator and includes signals from the MACD, stochastic oscillator, and awesome oscillator. It displays the points of the parabolic SAR on the chart, which help determine the direction of the trend. Additionally, the indicator allows for tracking signals based on the combined analysis of three other technical indicators: MACD, stochastic oscillator, and awesome oscillator. Furthermore, the indicator includes the ability to display buy/sell labels and signals for changing the trend direction. This is not an investment recommendation.Very effective in higher timeframes.If the MACD "macd line" crosses the "signal line" from above and the Stochastic %K line crosses the %D line from above, and the last column in the Avesome Oscillator is red, then the indicator gives a signal to sell. If the MACD "macd line" crosses the "signal line" from below and the Stochastic %K line crosses the %D line from below, and the last column in the Avesome Oscillator is green, then the indicator gives a signal to buy.

ADX + BB %B + AO + EMA [Luca Massuda]This trading strategy combines different indicators:

1) ADX, Average Directional Movement: to spot the trend

2) BB %B Bollinger Band %B: to spost relative price position to Bollinger Bands

3) AO Awesome Oscillator: to spot momentum

4) ema 5,ema21, ema50, ema200: to decide long or short position

You can configure:

Take profit % : at which % gains to take profit from the entry price

Stop loss % : at which % stop loss from the entry price

BB %B Overbought: At which level you consider Overbought respect to Bollinger Bands (values 0 to 100)

BB %B Oversold: At which level you consider Oversold respect to Bollinger Bands (values 0 to 100)

Awesome Oscillator: AO level to consider a long or short position +/- 2

ADX: ADX value to consider a long or short position

Start Date, Month, Year: Starting point for a backtesting strategy

Lenght , Source , Standard Deviation: Bollinger Bands values

ADX smoothing, DI Lenght: ADX values

Green and purple zones indicate when the strategy can go long or short.

Default Long conditions:

ema5>ema21 and ema50>ema200 and bb>75% and ao>2 and adx>15

Default Short conditions:

ema515

FluxPulse Momentum [JOAT]FluxPulse Momentum - Adaptive Multi-Component Oscillator

FluxPulse Momentum is a composite oscillator that blends three distinct momentum components into a single, smoothed signal line. Rather than relying on a single indicator, it synthesizes adaptive RSI, normalized rate of change, and a Kaufman-style efficiency ratio to provide a multi-dimensional view of momentum.

What This Indicator Does

Combines RSI, Rate of Change (ROC), and Efficiency Ratio into one weighted composite

Applies EMA smoothing to reduce noise while preserving responsiveness

Displays overbought/oversold zones with optional background highlighting

Generates buy/sell signals when the oscillator crosses its signal line in favorable zones

Provides a real-time dashboard showing current state, momentum direction, and efficiency

Core Components

Adaptive RSI (50% weight) — Standard RSI calculation normalized around the 50 level

Normalized ROC (30% weight) — Rate of change scaled relative to its recent maximum range

Efficiency Ratio (20% weight) — Measures directional movement efficiency, inspired by Kaufman's adaptive concepts

The final composite is smoothed twice using EMA to create both a fast line and a signal line.

Signal Logic

// Buy signal: crossover in lower half

buySignal = ta.crossover(qmo, qmoSmooth) and qmo < 50

// Sell signal: crossunder in upper half

sellSignal = ta.crossunder(qmo, qmoSmooth) and qmo > 50

Signals are generated only when the oscillator is positioned favorably—buy signals occur below the 50 midline, sell signals occur above it.

Dashboard Information

The on-chart table displays:

Current oscillator value with gradient coloring

Momentum state (Overbought, Oversold, Bullish, Bearish, Neutral)

Momentum direction and acceleration

Efficiency ratio percentage

Active signal status

Inputs Overview

RSI Length — Period for RSI calculation (default: 14)

ROC Length — Period for rate of change (default: 10)

Smoothing Length — EMA smoothing period (default: 3)

Overbought/Oversold Levels — Threshold levels for zone detection

Await Bar Confirmation — Wait for bar close before triggering alerts

How to Use It

Watch for crossovers between the main line and signal line

Use overbought/oversold zones to identify potential reversal areas

Monitor the histogram for momentum acceleration or deceleration

Combine with price action analysis for confirmation

Alerts

Buy Signal — Bullish crossover in the lower zone

Sell Signal — Bearish crossunder in the upper zone

Overbought/Oversold Crosses — Level threshold crossings

This indicator is provided for educational purposes. It does not constitute financial advice. Always conduct your own analysis before making trading decisions.

— Made with passion by officialjackofalltrades

Moving Average Shift [Quantora]Title: Moving Average Shift

Description:

The Moving Average Shift is a dynamic technical analysis tool designed to help traders better visualize trend strength and direction using a combination of customizable moving averages and a volatility-adjusted oscillator.

🔧 Features:

Multi-Type Moving Average Selection

Choose from SMA, EMA, SMMA (RMA), WMA, and VWMA for your main signal line.

ZLSMA Trio

Three Zero-Lag Smoothed Moving Averages (ZLSMA) with adjustable lengths and colors provide a smoother trend-following structure without the delay of traditional MAs.

EMA Ribbon (50/100/200)

Add clarity to long-term trend direction with layered Exponential Moving Averages in key institutional periods.

Volatility-Adjusted Oscillator

A color-changing oscillator calculated from the normalized deviation between price and the selected MA. This helps identify trend shifts and momentum buildups.

Custom MA Line Widths and Styling

Full control over the width and appearance of all MA lines for visual clarity.

Bar & Candle Coloring

Bars and candles dynamically change color based on the relationship between price and the selected MA — helping you quickly assess bullish/bearish conditions.

📈 How It Helps:

Spot early trend shifts through the oscillator.

Confirm trades using the alignment between ZLSMAs and EMAs.

Quickly assess current trend conditions using color-coded price bars.

Clustering Volatility (ATR-ADR-ChaikinVol) [Sam SDF-Solutions]The Clustering Volatility indicator is designed to evaluate market volatility by combining three widely used measures: Average True Range (ATR), Average Daily Range (ADR), and the Chaikin Oscillator.

Each indicator is normalized using one of the available methods (MinMax, Rank, or Z-score) to create a unified metric called the Score. This Score is further smoothed with an Exponential Moving Average (EMA) to reduce noise and provide a clearer view of market conditions.

Key Features:

Multi-Indicator Integration: Combines ATR, ADR, and the Chaikin Oscillator into a single Score that reflects overall market volatility.

Flexible Normalization: (Supports three normalization methods)

MinMax: Scales values between the observed minimum and maximum.

Rank: Normalizes based on the relative rank within a moving window.

Z-score: Standardizes values using mean and standard deviation.

Dynamic Window Selection: Offers an automatic window selection option based on a specified lookback period, or a fixed window size can be used.

Customizable Weights: Allows the user to assign individual weights to ATR, ADR, and the Chaikin Oscillator. Optionally, weights can be normalized to sum to 1.

Score Smoothing: Applies an EMA to the computed Score to smooth out short-term fluctuations and reduce market noise.

Cluster Visualization: Divides the smoothed Score into a number of clusters, each represented by a distinct color. These colors can be applied to the price bars (if enabled) for an immediate visual indication of the current volatility regime.

How It Works:

Input & Window Setup: Users set parameters for indicator periods, normalization methods, weights, and window size. The indicator can automatically determine the analysis window based on the number of lookback days.

Calculation of Metrics: The indicator computes the ATR, ADR (as the average of bar ranges), and the Chaikin Oscillator (based on the difference between short and long EMAs of the Accumulation/Distribution line).

Normalization & Scoring: Each indicator’s value is normalized and then weighted to form a raw Score. This raw Score is scaled to a range using statistics from the chosen window.

Smoothing & Clustering: The raw Score is smoothed using an EMA. The resulting smoothed Score is then multiplied by the number of clusters to assign a cluster index, which is used to choose a color for visual signals.

Visualization: The smoothed Score is plotted on the chart with a color that changes based on its value (e.g., lime for low, red for high, yellow for intermediate values). Optionally, the price bars are colored according to the assigned cluster.

_____________

This indicator is ideal for traders seeking a quick and clear assessment of market volatility. By integrating multiple volatility measures into one comprehensive Score, it simplifies analysis and aids in making more informed trading decisions.

For more detailed instructions, please refer to the guide here:

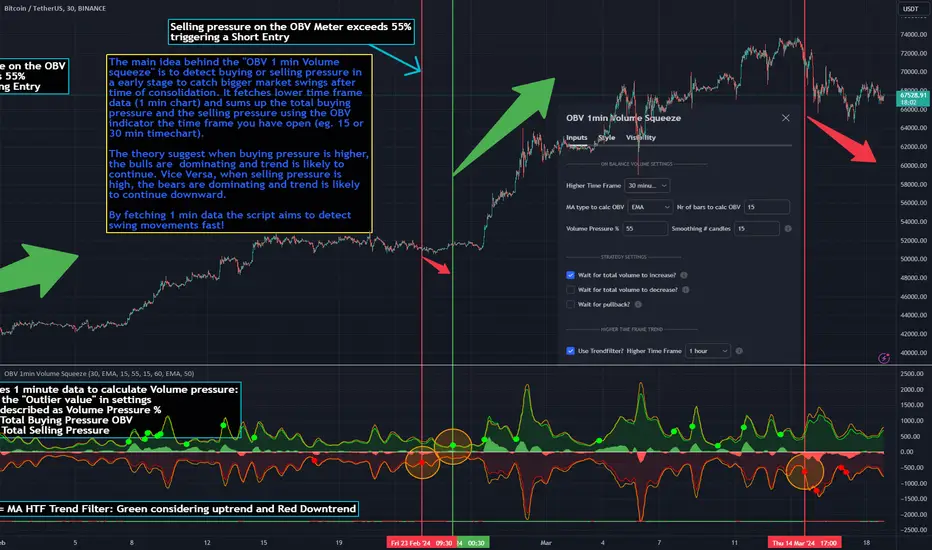

OBV 1min Volume SqueezeIn the vast realm of trading strategies, few terms evoke as much intrigue as the word "squeeze." It conjures images of pent-up energy, ready to burst forth in a sudden and decisive move. In this blog post, we'll delve into a new trading idea titled the "OBV 1-Minute Volume Squeeze" which aims to catch bigger market movements by fetching 1 minute OBV data on higher time charts.

The Essence of Squeeze

In trading parlance, a "squeeze" typically denotes a scenario where volatility contracts, and prices consolidate within a narrow range. Translating this concept to volume dynamics, a "volume squeeze" suggests a period of compressed volume activity. It is unclear if the Bulls or the Bears are at winning hand and price is thus consolidating. The script calculates buying and selling pressure by fetching 1 min data. The total volume presure is the sum of absolute values of the buying and selling pressure added up. By deviding the Buying volume by the total volume we know the Buying Pressure.

The trading theory suggest that when the buying pressure exceeds a certain value eg. 50% (default value in the script is 55%) it is likely the trend will continue to go up for a longer period of time. Vice Versa when selling pressure is higher, the trend is likely to continue down. In the script you can adjust the sensitivity in such way a higher "Volume Pressure %" result in less trading signals.

Fetching 1 min data

The OBV is a wonderful indicator to measure the buying and selling pressure. A disadvantage of the script is that the total volume pressure is presented as a positive (buying) or negative value (selling) value in the Oscillator. It does not offset the Bulls power against the Bears power at given time. The script aims to do measure the directional volume power by defining a volume pressure % (oulier value) by fetching 1 min OBV data on higher time frame charts comparing the Bulls power against the Bears Power. The code is included below:

// Fetch Lower Timeframe Data in an array

// nV = ZeroValue, sV = Selling Volume, bV = Buying Volume, tV = Total Volume

= request.security_lower_tf(syminfo.tickerid, '1', )

sum_bV_Lengthbars = array.sum(bV)

sum_sV_Lengthbars = array.sum(sV)

sum_tV_Lengthbars = sum_bV_Lengthbars + sum_sV_Lengthbars // Combine buying and selling volumes to get total volume

// Calculate buying and selling volume as percentage of the total volume, but ensure the denominator isn't zero.

buying_percentage = sum_tV_Lengthbars != 0 ? sum_bV_Lengthbars / sum_tV_Lengthbars * 100 : na

selling_percentage = sum_tV_Lengthbars != 0 ? -(sum_sV_Lengthbars / sum_tV_Lengthbars * 100) : na

OBV Oscillator Explanation

The On Balance Volume (OBV) indicator is a technical analysis tool used to measure buying and selling pressure in the market. It does this by keeping a running total of volume flows. OBV is typically calculated by adding the volume on a candle when the price closes higher than the previous candle's close and subtracting the volume on candles when the price closes lower than the previous candles close. If the price closes unchanged from the previous candle, the volume is not added to or subtracted from the OBV. The OBV can be presented as an oscillator. Positve value is the buying pressure and negative values is the selling pressure. In the settings the OBV is calculated based on 1 min data and comes with the following input options for visualization on the chart:

Higher Time Frame Settings (make sure the HTF is higher than the chart you have open)

Type of MA being: EMA, DEMA, TEMA, SMA, WMA, HMA, McGinley

Volume Pressure % (outlier value)

Length of number of bars (of the choosen HTF settings)

Smoothing of number candles of hte opened timechart. Note that higher number of bars to smoothen the indicator results in less signals, but lag of the indicator increases.

The Oscilator contains 3 main lines which are used to determin the entry signals:

Orange Line = the Outlier value in settings described as "Volume Pressure %"

Green Line = Total Buying Pressure OBV

Red Line = Total Selling Pressure OBV

If the Green or Red line is in between the zero line and the orange line the volume is squeezed and waiting for a directional break out.

If the Green line crosses over the orange line the buying pressure is > 55% and triggers a long entry position (green dot). If the Red line crosses under the orange line the selling pressure is > 55% and triggers an short entry (red dot). In the strategy settings this option is called: "Wait for total volume to increase?".

Alternative Strategy Options

In order to play around with different settings users can opt for two more strategy entry settings, called:

"Wait for total volume to deacrease?" --> Only gives a signal when total volume is declining, but buying or selling pressure maintains and crosses % threshold.

"Wait for Pull Back?" --> After a pullback occured and opposite buy/sell pressure gets lower than threshold (direction is shifting)

Turning on all options will logically result into more signals. Note these strategy ideas are experimental and can best be used in confirmation with other indicators.

Moving Average Filter (HTF)

The Oscillator has a horizontal line at the bottom. The line is green when the moving average is in a uptrend and red when the moving average is in a downtrend. The MA Filter comes with the following settings:

Higher Time Frame Setting

Type of MA being: EMA, DEMA, TEMA, SMA, WMA, HMA, McGinley

Length of number of bars (of the choosen HTF settings)

At last I hope you like this volume trading idea and if you have any comments let me know!

DVDIQQE [DW]This is an experimental study inspired by the Quantitative Qualitative Estimation indicator designed to identify trend and wave activity.

In this study, rather than using RSI for the calculation, the Dual Volume Divergence Index oscillator is utilized.

First, the DVDI oscillator is calculated by taking the difference between PVI and its EMA, and NVI and its EMA, then taking the difference between the two results.

Optional parameters for DVDI calculation are included within this script:

- An option to use tick volume rather than real volume for the volume source

- An option to use cumulative data, which sums the movements of the oscillator from the beginning to the end of TradingView's maximum window to give a more broad picture of market sentiment

Next, two trailing levels are calculated using the average true range of the oscillator. The levels are then used to determine wave direction.

Lastly, rather than using 0 as the center line, it is instead calculated by taking a cumulative average of the oscillator.

Custom bar colors are included.

Note: For charts that have no real volume component, use tick volume as the volume source.

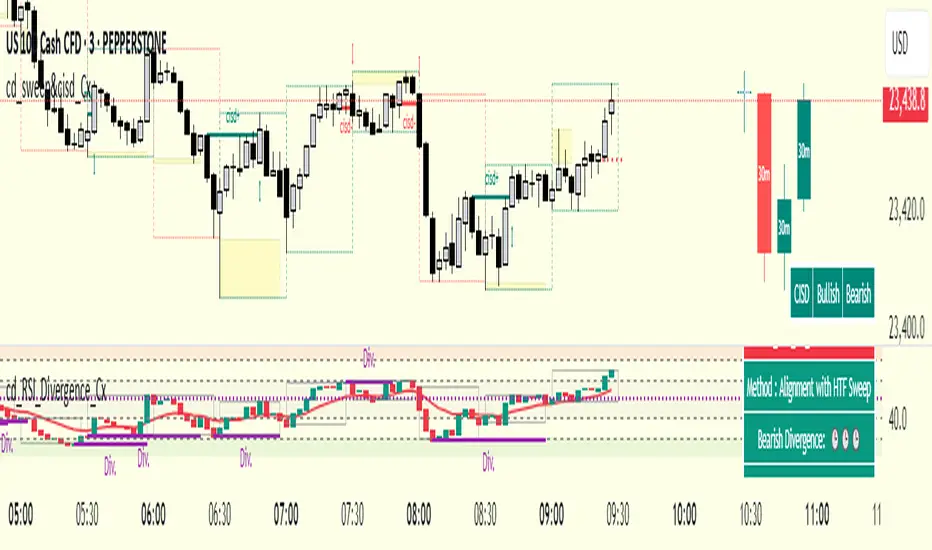

cd_RSI_Divergence_CxGeneral:

The Relative Strength Index (RSI) is a momentum oscillator widely used by traders in price analysis. In addition to showing overbought/oversold zones, divergences between RSI and price are also tracked to identify trading opportunities.

The general consensus is that oscillators alone are not sufficient for entries and should be evaluated together with multiple confirmations.

This oscillator is designed as an additional confirmation/compatible tool for strategies that already use higher time frame (HTF) sweeps and lower time frame (LTF) confirmations such as Change in State Delivery (CISD) or Change of Character (CHOCH).

Features:

While RSI oscillators are commonly displayed in line format (classic), this indicator also offers candlestick-style visualization.

Depending on the selected source, period length, and EMA length, RSI can be displayed as lines and/or candlesticks.

Divergence detection & tracking:

Price and RSI values are monitored on the chosen higher time frame (from the menu) to determine highs and lows. For divergence display, the user can choose between two modes:

1- Alignment with HTF Sweep

2- All

1 - Alignment with HTF Sweep:

First, the price must sweep the previous high/low of the candle on the HTF (i.e., break it) but fail to continue in that direction and return inside (sweep).

If this condition is met, RSI values are checked:

If price makes a high sweep but RSI fails to make a new high → divergence is confirmed.

If price makes a low sweep but RSI fails to make a new low → divergence is confirmed.

Divergence is then displayed on the chart.

2 - All:

In this mode, sweep conditions are ignored. Divergence is confirmed if:

Price makes a new high on HTF but RSI does not.

RSI makes a new high on HTF but price does not.

Price makes a new low on HTF but RSI does not.

RSI makes a new low on HTF but price does not.

Menu & Settings:

RSI visualization (source + period length + EMA period length)

Option to choose classic/candlestick style display

Color customization

Higher time frame selection

Adjustable HTF boxes and table display

Final notes:

This oscillator is designed as an additional confirmation tool for strategies based on HTF sweep + LTF CISD/CHOCH confirmation logic. The chosen HTF in the oscillator should match the time frame where sweeps are expected.

Divergence signals from this oscillator alone will not make you profitable.

For spot trades, monitoring sweeps and divergences on higher time frames is more suitable (e.g., Daily–H1 / Weekly–H4).

My personal usage preferences:

Entry TF: 3m

HTF bias: Daily + H1

Sweep + CISD: 30m / 3m

Market Structure: 3m

RSI divergence: HTF = 30m

If all of them align bullish or bearish ( timeframe alignment ), I try to take the trade.

I’d be glad to hear your feedback and suggestions for improvement.

Happy trading!

Chaikin DivergenceOverview

The Chaikin Divergence is a powerful technical indicator designed to enhance the traditional Chaikin Oscillator by incorporating divergence detection between the oscillator and price action. This advanced tool not only plots the Chaikin Oscillator but also identifies and highlights bullish and bearish divergences, providing traders with valuable insights into potential trend reversals and momentum shifts.

Key Features

Chaikin Oscillator Plotting: Visual representation of the Chaikin Oscillator, aiding in the analysis of market momentum based on volume and price.

Divergence Detection:

Bullish Divergence: Indicates potential upward reversals when price forms lower lows while the oscillator forms higher lows.

Bearish Divergence: Signals possible downward reversals when price creates higher highs while the oscillator forms lower highs.

Customizable Settings:

Fast Length & Slow Length: Adjust the periods for the Exponential Moving Averages (EMA) used in the oscillator calculation.

Pivot Detection Parameters: Define the sensitivity of pivot high and pivot low detection with adjustable left and right bars.

Bars Lookback for Divergence: Set the number of bars to look back for identifying divergences.

Color Customization: Choose distinct colors for bullish and bearish divergence labels to match your trading preferences.

Visual Indicators:

Divergence Labels: Clear and distinct labels (arrows or dots) on the chart indicating the type and location of divergences.

Zero Line: A dashed zero line to reference the oscillator’s crossing points.

Chaikin Oscillator Calculation:

The indicator calculates the Chaikin Oscillator by subtracting the slow EMA of the Accumulation/Distribution Line (ta.accdist) from the fast EMA.

This oscillates around the zero line, indicating buying and selling pressure.

Pivot Detection:

Utilizes ta.pivothigh and ta.pivotlow functions to identify significant pivot points in price action. These pivot points serve as reference points for divergence analysis.

Divergence Identification:

Bullish Divergence: Detected when a recent pivot low in price is lower than the previous pivot low, while the corresponding oscillator value is higher than the previous oscillator pivot.

Bearish Divergence: Identified when a recent pivot high in price is higher than the previous pivot high, but the oscillator value is lower than the previous oscillator pivot.

Label Plotting:

When a divergence is detected, the indicator plots a label (arrow or dot) on the chart at the pivot point, signaling the type of divergence.

Adding the Indicator:

Open TradingView and navigate to the chart where you want to apply the indicator.

Open the Pine Editor, paste the Chaikin Oscillator with Divergences script, and add it to your chart.

Configuring Settings:

Fast Length & Slow Length: Adjust these to modify the sensitivity of the Chaikin Oscillator. Shorter periods make the oscillator more responsive to price changes.

Left Bars for Pivots & Right Bars for Pivots: Define how many bars to the left and right are considered when identifying pivot points. Increasing these values makes pivot detection less sensitive.

Bars Lookback for Divergence: Set how far back the indicator should search for previous pivot points when identifying divergences. A higher value allows detection over a longer timeframe.

Bullish/Bearish Divergence Colors: Choose colors that stand out against your chart background for easy identification of divergence signals.

Interpreting Signals:

Bullish Divergence Labels: Appear when there's a potential upward reversal, signaling a possible buying opportunity.

Bearish Divergence Labels: Show up when a downward reversal might be imminent, indicating a possible selling opportunity.

Oscillator Crosses Zero: Pay attention to when the oscillator crosses the zero line, as this can also signal changes in momentum.

Combining with Other Indicators:

For enhanced trading strategies, combine divergence signals with other technical indicators or chart patterns to confirm potential trade setups.

Crypto Volume/Strength ComparatorHello Traders,

Here is an attempt to perform comparative analysis between top cryptos based on strength (oscillator) and volume. Methodology used here is similar to Magic Number formula described in the post : Enhanced Magic Formula for fundamental analysis . But, instead of using fundamentals, we are making use of few technicals to derive similar outcome. Usage of the available stats will not be same as Magic number since we are using technicals.

⬜ Process

▶ Get crypto exchange based on prefix of instrument being used.

▶ For the given exchange, get data for all the tickers available in input fields.

▶ Calculate Oscillator, Momentum based on price for each tickers.

▶ Calculate Oscillator, Momentum based on volume for each tickers.

▶ Calculate Volatility for each tickers.

▶ Rank Price-Oscillator, Price-Momentum, Volume-Oscillator, Volume-Momentum, Volatility for each tickers.

▶ Calculate combined rank by adding up individual ranks.

▶ Calculate movement of rankings from bar to bar

▶ Sort tickers based on rank and populate them on table. Display direction of rankings.

⬜ Components

Display components are as follows:

⬜ Settings

Settings are pretty simple and straightforward

⬜ Calculations

▶ Oscillators : High values of oscillators are considered as ideal as the process is intended towards finding trend.

▶ Momentum : Momentum is calculated on the basis of Squeeze Momentum Indicator by @LazyBear.

▶ Volatility : Volatility is calculated on the basis of Williams Vix Fix by @ChrisMoody. Here too since we are in trend following mode, lower vix fix is considered ideal.

⬜ Few Notes

Tickers will show data only if selected exchange has them. Some tickers are not available in all exchanges. In that case, it will show NAN. This is kind of unavoidable as we need to have fixed size arrays for any calculations.

Indicator works only on crypto tickers which has valid exchange.

Tickers move through the rankings in real time. Background of all stats are based on gradient from green to red.

Tickers on top may not always have better long opportunity or tickers at bottom may not always be optimal for shorting. We need to consider how long the instrument may stay in the position or how fast it is moving in opposite direction. Hence, directions of the ranking movement are also shown on the table.

Velocity Pressure Index | AlphaNattVelocity Pressure Index (VPI) | AlphaNatt

A sophisticated momentum oscillator that combines price velocity analysis with volume pressure dynamics to identify high-probability trading opportunities.

📊 KEY FEATURES

Dual Analysis System: Merges price velocity measurement with volume pressure analysis for comprehensive market momentum assessment

Dynamic Normalization: Automatically scales values between -100 and +100 for consistent readings across all market conditions

Adaptive Zones: Self-adjusting overbought/oversold levels based on recent price history

Multi-Layer Confirmation: Combines momentum, acceleration, and crossover signals for robust trade identification

Volume-Weighted Pressure: Differentiates between bullish and bearish volume to gauge true market sentiment

📈 HOW IT WORKS

The VPI calculates price velocity using linear regression of price changes, then weights this velocity by the difference between bullish and bearish volume pressure. This creates a momentum reading that accounts for both price movement speed and the volume conviction behind it.

Signal Generation:

Price velocity is measured over the specified period

Volume is separated into bullish (close > open) and bearish (close < open) pressure

Velocity is amplified or dampened based on volume pressure differential

The resulting index is normalized to oscillate between -100 and +100

A signal line smooths the oscillator for crossover detection

🎯 TRADING SIGNALS

Long Signals (Cyan #00F1FF):

Strong Bull: VPI > Signal with positive momentum and acceleration

Crossover Bull: VPI crosses above signal while above oversold zone

Divergence: Price makes lower low while VPI makes higher low

Short Signals (Magenta #FF019A):

Strong Bear: VPI < Signal with negative momentum and deceleration

Crossover Bear: VPI crosses below signal while below overbought zone

Divergence: Price makes higher high while VPI makes lower high

⚙️ CUSTOMIZABLE PARAMETERS

Velocity Settings:

Velocity Period (14): Lookback for price velocity calculation

Pressure Period (21): Volume analysis window

Smoothing Factor (3): Final oscillator smoothing

Signal Configuration:

Signal Type: Choose between SMA, EMA, or DEMA

Signal Length (9): Signal line smoothing period

Normalization Period (50): Range calculation window

Dynamic Zones:

Zone Lookback (100): Period for adaptive overbought/oversold calculation

Percentiles: 80th/20th percentiles for dynamic zones

📐 VISUAL COMPONENTS

Main Oscillator: Color-coded line showing current momentum state

Signal Line: White line for crossover detection

Momentum Histogram: Shows velocity differential at 50% scale

Dynamic Zones: Self-adjusting overbought/oversold bands

Extreme Levels: ±50 dotted lines marking extreme conditions

Background Shading: Subtle highlighting of overbought/oversold regions

💡 USAGE TIPS

Trend Trading: Use strong bull/bear signals in trending markets for continuation entries

Range Trading: Focus on crossovers near extreme zones for reversal trades

Divergence Trading: Watch for price/oscillator divergences at market extremes

Multi-Timeframe: Combine with higher timeframe VPI for directional bias

Volume Confirmation: Stronger signals occur with aligned volume pressure

⚠️ BEST PRACTICES

The VPI works best in liquid markets with reliable volume data. For optimal results, combine with price action analysis and use appropriate risk management. The indicator is most effective during trending conditions but can identify reversals when divergences occur at extremes.

🔔 ALERTS AVAILABLE

VPI Long/Short Signals

Bullish/Bearish Crossovers

Extreme Overbought/Oversold Conditions

Version 6 | Pine Script™ | © AlphaNatt

Divergences + Alerts (ANY Indicator)📊 Divergences + Alerts (ANY Indicator)

This versatile indicator detects four types of divergences between price action and an oscillator:

Buyer Exhaustion

Buyer Absorption

Seller Exhaustion

Seller Absorption

Each divergence type is automatically identified and visually marked on the chart with colored lines. The indicator also includes built-in alert conditions for all four divergence types, allowing traders to receive real-time notifications when potential reversal signals occur.

By default, the oscillator is a candle-style visualization of the Money Flow Index (MFI), enhanced with volatility filtering via a VWMA-based ATR. However, users can replace the default MFI oscillator with any external source using the “Plug External Source” input, enabling full customization and compatibility with other indicators.

Key features:

🔍 Detects both exhaustion and absorption divergences

🔔 Alerts for each divergence type

🕯️ Candle-style oscillator visualization

🔌 Optional input for external indicator sources

⚙️ ATR-based filtering for precision

Ideal for traders seeking to spot early signs of trend reversals or momentum shifts with customizable flexibility.

ADX + DMI (HMA Version)📝 Description (What This Indicator Does)

🚀 ADX + DMI (HMA Version) is a trend strength oscillator that enhances the traditional ADX by using the Hull Moving Average (HMA) instead of EMA.

✅ This results in a much faster and more responsive trend detection while filtering out choppy price action.

🎯 What This Indicator Does:

1️⃣ Measures Trend Strength – ADX shows when a trend is strong or weak.

2️⃣ Identifies Trend Direction – DI+ (Green) shows bullish momentum, DI- (Red) shows bearish momentum.

3️⃣ Uses Hull Moving Average (HMA) for Faster Signals – Removes lag and reacts faster to trend changes.

4️⃣ Reduces False Signals – Traditional ADX lags behind, but this version reacts quickly to reversals.

5️⃣ Good for Scalping & Day Trading – Especially for BTC 5-min and lower timeframes.

⚙ Indicator Inputs (Customization)

Input Name Example Value Purpose

ADX Length 14 Defines the smoothing for the ADX value.

DI Length 14 Defines how DI+ and DI- are calculated.

HMA Length 24 Hull Moving Average smoothing for ADX & DI+.

Trend Threshold 25 The level above which ADX confirms a strong trend.

📌 You can adjust these settings to optimize for different assets and timeframes.

🎯 Trading Rules & How to Use It

✅ How to Identify a Strong Trend:

When ADX (Blue Line) is above 25→ A strong trend is in play.

When ADX is below 25 → The market is choppy or ranging.

✅ How to Use DI+ and DI- for Trend Direction:

If DI+ (Green) is above DI- (Red), the market is in an uptrend.

If DI- (Red) is above DI+ (Green), the market is in a downtrend.

✅ How to Confirm Entries & Exits:

1️⃣ Enter Long when DI+ crosses above DI- while ADX is rising above 25.

2️⃣ Enter Short when DI- crosses above DI+ while ADX is rising above 25.

3️⃣ Avoid trading when ADX is below 25 – the market is in a choppy range.

This should not be used as a stand alone oscillator. Trading takes skill and is risky. Use at your own risk.

This is not advise on how to trade, these are just examples of how I use the oscillator. Trade at your own risk.

You can put this on your chart versus the tradingview adx and you can adjust the settings to see the difference. This was optimized for btc on the 5 min chart. You can adjust for your trading strategy.

Heikin Ashi Processed Generalized Smooth StepDisclaimer : This is my attempt of smoothing and improving @tarasenko_ script. Find the originial author here :

Overview:

The Smooth Step Heikin Ashi Indicator is an enhanced version of the original script developed by tarasenko_. This advanced TradingView tool integrates Heikin Ashi candlestick calculations with a sophisticated smoothing oscillator, offering traders improved trend visualization and dynamic alert capabilities.

Key Enhancements:

Refined Heikin Ashi Calculations: The indicator computes smoothed Open, High, Low, and Close (OHLC) values with adjustable factors, allowing for more precise trend analysis. It also includes an optional second-level modified Heikin Ashi calculation for additional smoothing.

Advanced Smooth Step Oscillator: Utilizing Pascal’s triangle, this oscillator provides a visual representation of price momentum. Traders can configure the lookback period, equation order, and threshold to tailor the oscillator to specific trading strategies.

Enhanced Customization Options: Users can toggle between standard and Heikin Ashi candles, adjust smoothing parameters, and set display preferences to align with their analytical needs.

Noise Reduction: Smoothes out market fluctuations using customizable Heikin Ashi factors. Introduces a second-level smoothing option for even greater noise reduction, allowing traders to focus on the core trend.

Original Indicator :

Heikin Ashi processed version :

Visualization Features:

Heikin Ashi Candles: Displays candles with customizable colors and visibility settings, aiding in clearer trend identification.

Smooth Step Oscillator Line: Plots a line that reflects trend strength and momentum, assisting traders in making informed decisions.

Threshold Line: Provides a visual reference point to facilitate quick assessments of market conditions.

Conclusion:

Building upon tarasenko_'s original work, the Smooth Step Heikin Ashi Indicator delivers a robust tool for traders seeking refined market analysis. Its combination of advanced smoothing techniques and dynamic alert features makes it a valuable addition to any trader's toolkit.

Periodical Trend [BigBeluga]The Periodical Trend indicator is designed to provide a detailed analysis of market trends and volatility. It utilizes a combination of Moving Averages and volatility measures to plot trend line, highlight potential trend reversals, and indicate mean reversion opportunities. The indicator offers customizable display options, allowing traders to adjust for sensitivity, volatility bands, and price deviation visibility.

🔵 KEY FEATURES

● Periodical Trend Analysis

Uses (high + volatility) or (low - volatility) as the foundation for trend analysis with a set period.

// Condition to update the AVG array based on the selected mode

if mode == "Normal"

? bar_index == 122

: bar_index % period == 0

AVG.push(close) // Add the close price to the AVG array

// Update AVG array based on the period and price comparison

if bar_index % period == 0

if close > AVG.last() // If the current close is greater than the last stored value in AVG

AVG.push(low - vlt) // Add the low price minus volatility to the array

if close < AVG.last() // If the current close is lower than the last stored value in AVG

AVG.push(high + vlt) // Add the high price plus volatility to the array

Provides adjustable sensitivity modes ("Normal" and "Sensitive") for different market conditions.

Trend direction is visualized with dynamic color coding based on the relationship between the trend line and price.

● Volatility Bands

Displays upper and lower volatility bands derived from a moving average of price volatility (high-low).

The bands help identify potential breakout zones, overbought, or oversold conditions.

Users can toggle the visibility of the bands to suit their trading style.

● Mean Reversion Signals

Detects mean reversion opportunities when price deviates significantly from the trend line.

Includes both regular and strong mean reversion signals, marked directly on the chart.

Signals are based on oscillator crossovers, offering potential entry and exit points.

● Price Deviation Oscillator

Plots an oscillator that measures the deviation of price from the average trend line.

The oscillator is normalized using standard deviation, highlighting extreme price deviations.

Traders can choose to display the oscillator for in-depth analysis of price behavior relative to the trend.

● Dynamic Trend Coloring

The indicator colors the background on the direction of the trend.

Green indicates bullish trends, while blue indicates bearish trends.

The trend colors adapt dynamically to market conditions, providing clear visual cues for traders.

🔵 HOW TO USE

● Trend Analysis

The trend line represents the current market direction. A green trend line suggests a bullish trend, while a blue trend line indicates a bearish trend.

Use the trend line in conjunction with volatility bands to confirm potential breakouts or areas of consolidation.

● Volatility Bands

Volatility bands offer insight into potential overbought or oversold conditions.

Price exceeding these bands can signal a strong trend continuation or a possible reversal.

● Mean Reversion Strategies

Look for mean reversion signals (regular and strong) when price shows signs of reverting to the trend line after significant deviation.

Regular signals are represented by small dots, while strong signals are represented by larger circles.

These signals can be used as entry or exit points, depending on the market context.

● Price Deviation Analysis

The oscillator provides a detailed view of price deviations from the trend line.

A positive oscillator value indicates that the price is above the trend, while a negative value suggests it is below.

Use the oscillator to identify potential overbought or oversold conditions within the trend.

🔵 USER INPUTS

● Period

Defines the length of the period used for calculating the trend line. A higher period smooths out the trend, while a shorter period makes the trend line more sensitive to price changes.

● Mode

Choose between "Normal" and "Sensitive" modes for trend detection. The "Sensitive" mode responds more quickly to price changes, while the "Normal" mode offers smoother trend lines.

● Volatility Bands

Toggle the display of upper and lower volatility bands. These bands help identify potential areas of price exhaustion or continuation.

● Price Deviation

Toggle the display of the price deviation oscillator. This oscillator shows the deviation of the current price from the trend line and highlights extreme conditions.

● Mean Reversion Signals

Toggle the display of mean reversion signals. These signals highlight potential reversal points when the price deviates significantly from the trend.

● Strong Mean Reversion Signals

Toggle the display of stronger mean reversion signals, which occur at more extreme deviations from the trend.

● Width

Adjust the thickness of the trend line for better visibility on the chart.

🔵 CONCLUSION

The Periodical Trend indicator combines trend analysis, volatility bands, and mean reversion signals to provide traders with a comprehensive tool for market analysis. By offering customizable display options and dynamic trend coloring, this indicator can adapt to different trading styles and market conditions. Whether you are a trend follower or a mean reversion trader, the Periodical Trend indicator helps identify key market opportunities and potential reversals.

For optimal results, it is recommended to use this indicator alongside other technical analysis tools and within the context of a well-structured trading strategy.

Spider VisionSpider Vision is an indicator that I created for trading view, which consists of a spider chart with 7 indicators built into it. This chart provides a visual representation of how these indicators are behaving, allowing traders to quickly assess the current market conditions.

The chart displays the following indicators:

RSI (Relative Strength Index): This is a momentum indicator that measures the strength of a security's price action. When the RSI is above 70, it is considered overbought, and when it is below 30, it is considered oversold.

Stochastic: This is another momentum indicator that compares the closing price of a security to its price range over a given time period. When the stochastic is above 80, it is considered overbought, and when it is below 20, it is considered oversold.

Momentum: This is a simple indicator that measures the change in a security's price over a given time period. When the momentum is positive, it indicates that the price is increasing, and when it is negative, it indicates that the price is decreasing.

BBW (Bollinger Bands Width): This indicator measures the width of the Bollinger Bands, which are a popular technical analysis tool used to identify potential trends and reversals. When the BBW is high, it suggests that the market is volatile, and when it is low, it suggests that the market is quiet.

DTO (Detrended Price Oscillator): This indicator measures the difference between the price of a security and its moving average. When the DTO is positive, it indicates that the price is above its moving average, and when it is negative, it indicates that the price is below its moving average.

Chop Zone: This indicator measures the choppiness of the market by comparing the average true range (ATR) to the difference between the high and low prices over a given time period. When the chop zone is high, it suggests that the market is choppy, and when it is low, it suggests that the market is trending.

Chaikin Oscillator: This is an oscillator that measures the accumulation/distribution of a security. When the Chaikin Oscillator is positive, it indicates that there is buying pressure in the market, and when it is negative, it indicates that there is selling pressure.

To use this indicator, traders can simply add it to their TradingView chart and adjust the input parameters to suit their trading style. The scale parameter can be used to adjust the size of the spider chart, while the color parameters can be used to customize the appearance of the chart. Traders can also adjust the length of each indicator to suit their preference.

Overall, the Spider Vision indicator provides a convenient way for traders to quickly assess the current market conditions and make more informed trading decisions.

Combo Backtest 123 Reversal & D_Three Ten OscThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

TradeStation does not allow the user to make a Multi Data Chart with

a Tick Bar Chart and any other type a chart. This indicator allows the

user to plot a daily 3-10 Oscillator on a Tick Bar Chart or any intraday interval.

Walter Bressert's 3-10 Oscillator is a detrending oscillator derived

from subtracting a 10 day moving average from a 3 day moving average.

The second plot is an 16 day simple moving average of the 3-10 Oscillator.

The 16 period moving average is the slow line and the 3/10 oscillator is

the fast line.

For more information on the 3-10 Oscillator see Walter Bressert's book

"The Power of Oscillator/Cycle Combinations"

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & D_Three Ten Osc This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

TradeStation does not allow the user to make a Multi Data Chart with

a Tick Bar Chart and any other type a chart. This indicator allows the

user to plot a daily 3-10 Oscillator on a Tick Bar Chart or any intraday interval.

Walter Bressert's 3-10 Oscillator is a detrending oscillator derived

from subtracting a 10 day moving average from a 3 day moving average.

The second plot is an 16 day simple moving average of the 3-10 Oscillator.

The 16 period moving average is the slow line and the 3/10 oscillator is

the fast line.

For more information on the 3-10 Oscillator see Walter Bressert's book

"The Power of Oscillator/Cycle Combinations"

WARNING:

- For purpose educate only

- This script to change bars colors.

Stochastic Momentum multi. strategyThe Stochastic Momentum Index (Stoch MTM, SMI) is based on the Stochastic Oscillator. The difference is that the Stochastic Oscillator calculates where the close is relative to the high/low range, while the SMI calculates where the close is relative to the midpoint of the high/low range. The values of the SMI range from +100 to -100. When the close is greater than the midpoint, the SMI is above zero, when the close is less than than the midpoint, the SMI is below zero.

The SMI is interpreted the same way as the Stochastic Oscillator. Extreme high/low SMI values indicate overbought/oversold conditions. A buy signal is generated when the SMI rises above -50, or when it crosses above the signal line. A sell signal is generated when the SMI falls below +50, or when it crosses below the signal line. Also look for divergence with the price to signal the end of a trend or indicate a false trend.

The Stochastic Momentum Index was developed by William Blau and was introduced in his article in the January, 1993 issue of Technical Analysis of Stocks & Commodities magazine.

Stochastic Momentum Index (Stoch MTM, SMI)Stochastic Momentum Index (Stoch MTM, SMI)

The Stochastic Momentum Index (Stoch MTM, SMI) is based on the Stochastic Oscillator. The difference is that the Stochastic Oscillator calculates where the close is relative to the high/low range, while the SMI calculates where the close is relative to the midpoint of the high/low range. The values of the SMI range from +100 to -100. When the close is greater than the midpoint, the SMI is above zero, when the close is less than than the midpoint, the SMI is below zero.

The SMI is interpreted the same way as the Stochastic Oscillator. Extreme high/low SMI values indicate overbought/oversold conditions. A buy signal is generated when the SMI rises above -50, or when it crosses above the signal line. A sell signal is generated when the SMI falls below +50, or when it crosses below the signal line. Also look for divergence with the price to signal the end of a trend or indicate a false trend.

The Stochastic Momentum Index was developed by William Blau and was introduced in his article in the January, 1993 issue of Technical Analysis of Stocks & Commodities magazine.

Money Flow Matrix This comprehensive indicator is a multi-faceted momentum and volume oscillator designed to identify trend strength, potential reversals, and market confluence. It combines a volume-weighted RSI (Money Flow) with a double-smoothed momentum oscillator (Hyper Wave) to filter out noise and provide high-probability signals.

Core Components

1. Money Flow (The Columns) This is the backbone of the indicator. It calculates a normalized RSI and weights it by relative volume.

Green Columns: Positive money flow (Buying pressure).

Red Columns: Negative money flow (Selling pressure).

Neon Colors (Overflow): When the columns turn bright Neon Green or Neon Red, the Money Flow has breached the dynamic Bollinger Band thresholds. This indicates an extreme overbought or oversold condition, suggesting a potential climax in the current move.

2. Hyper Wave (The Line) This is a double-smoothed Exponential Moving Average (EMA) derived from price changes. It acts as the "signal line" for the system. It is smoother than standard RSI or MACD, reducing false signals during choppy markets.

Green Line: Momentum is increasing.

Red Line: Momentum is decreasing.

3. Confluence Zones (Background) The background color changes based on the agreement between Money Flow and Hyper Wave.

Green Background: Both Money Flow and Hyper Wave are bullish. This represents a high-probability long environment.

Red Background: Both Money Flow and Hyper Wave are bearish. This represents a high-probability short environment.

Signal Guide

The Matrix provides three tiers of signals, ranging from early warnings to confirmation entries.

1. Warning Dots (Circles) These appear when the Hyper Wave crosses specific internal levels (-30/30).

Green Dot: Early warning of a bullish rotation.

Red Dot: Early warning of a bearish rotation.

Usage: These are not immediate entry signals but warnings to tighten stop-losses or prepare for a reversal.

2. Major Crosses (Triangles) These occur when Money Flow crosses the zero line, confirmed by momentum direction.

Green Triangle Up: Major Buy Signal (Money Flow crosses above 0).

Red Triangle Down: Major Sell Signal (Money Flow crosses below 0).

Usage: These are the primary trend-following entry signals.

3. Divergences (Labels "R" and "H") The script automatically detects discrepancies between Price action and the Hyper Wave oscillator.

"R" (Regular Divergence): Indicates a potential Reversal.

Bullish R: Price makes a lower low, but Oscillator makes a higher low.

Bearish R: Price makes a higher high, but Oscillator makes a lower high.

"H" (Hidden Divergence): Indicates a potential Trend Continuation.

Bullish H: Price makes a higher low, but Oscillator makes a lower low.

Bearish H: Price makes a lower high, but Oscillator makes a higher high.

Dashboard (Confluence Meter)

Located in the bottom right of the chart, the dashboard provides a snapshot of the current candle's status. It calculates a score based on three factors:

Is Money Flow positive?

Is Hyper Wave positive?

Is Hyper Wave trending up?

Readings:

STRONG BUY: All metrics are bullish.

WEAK BUY: Mixed metrics, but leaning bullish.

NEUTRAL: Metrics are conflicting.

WEAK/STRONG SELL: Bearish equivalents of the buy signals.

Trading Strategies

Strategy A: The Trend Rider

Entry: Wait for a Green Triangle (Major Buy).

Confirmation: Ensure the Background is highlighted Green (Confluence).

Exit: Exit when the background turns off or a Red Warning Dot appears.

Strategy B: The Reversal Catch

Setup: Look for a Neon Red Column (Overflow/Oversold).

Trigger: Wait for a Green "R" Label (Regular Bullish Divergence) or a Green Warning Dot.

Confirmation: Wait for the Hyper Wave line to turn green.

Strategy C: The Pullback (Continuation)

Context: The market is in a strong trend (Green Background).

Trigger: Price pulls back, but a Green "H" Label (Hidden Bullish Divergence) appears.

Action: Enter in the direction of the original trend.

Settings Configuration

The code includes tooltips for all inputs to assist with configuration.

Money Flow Length: Adjusts the sensitivity of the volume calculation. Lower numbers are faster but noisier; higher numbers are smoother.

Threshold Multiplier: Controls the "Neon" overflow bars. Increasing this (e.g., to 2.5 or 3.0) will result in fewer, more extreme signals.

Divergence Lookback: Determines how many candles back the script looks to identify pivots. Increase this number to find larger, macro divergences.

Disclaimer

This source code and the accompanying documentation are for educational and informational purposes only. They do not constitute financial, investment, or trading advice.