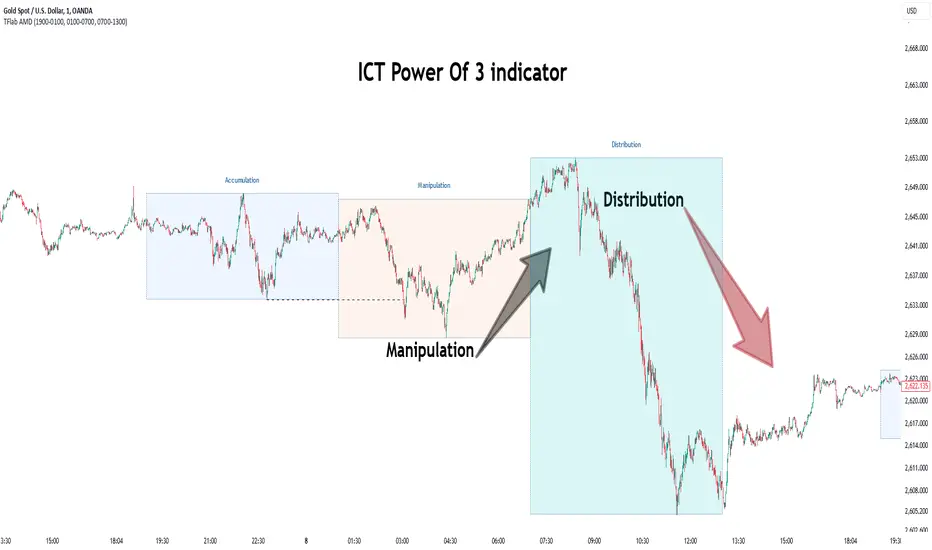

Power Of 3 ICT 01 [TradingFinder] AMD ICT & SMC Accumulations🔵 Introduction

The ICT Power of 3 (PO3) strategy, developed by Michael J. Huddleston, known as the Inner Circle Trader, is a structured approach to analyzing daily market activity. This strategy divides the trading day into three distinct phases: Accumulation, Manipulation, and Distribution.

Each phase represents a unique market behavior influenced by institutional traders, offering a clear framework for retail traders to align their strategies with market movements.

Accumulation (19:00 - 01:00 EST) takes place during low-volatility hours, as institutional traders accumulate orders. Manipulation (01:00 - 07:00 EST) involves false breakouts and liquidity traps designed to mislead retail traders. Finally, Distribution (07:00 - 13:00 EST) represents the active phase where significant market movements occur as institutions distribute their positions in line with the broader trend.

This indicator is built upon the Power of 3 principles to provide traders with a practical and visual tool for identifying these key phases. By using clear color coding and precise time zones, the indicator highlights critical price levels, such as highs and lows, helping traders to better understand market dynamics and make more informed trading decisions.

Incorporating the ICT AMD setup into daily analysis enables traders to anticipate market behavior, spot high-probability trade setups, and gain deeper insights into institutional trading strategies. With its focus on time-based price action, this indicator simplifies complex market structures, offering an effective tool for traders of all levels.

🔵 How to Use

The ICT Power of 3 (PO3) indicator is designed to help traders analyze daily market movements by visually identifying the three key phases: Accumulation, Manipulation, and Distribution.

Here's how traders can effectively use the indicator :

🟣 Accumulation Phase (19:00 - 01:00 EST)

Purpose : Identify the range-bound activity where institutional players accumulate orders.

Trading Insight : Avoid placing trades during this phase, as price movements are typically limited. Instead, use this time to prepare for the potential direction of the market in the next phases.

🟣 Manipulation Phase (01:00 - 07:00 EST)

Purpose : Spot false breakouts and liquidity traps that mislead retail traders.

Trading Insight : Observe the market for price spikes beyond key support or resistance levels. These moves often reverse quickly, offering high-probability entry points in the opposite direction of the initial breakout.

🟣 Distribution Phase (07:00 - 13:00 EST)

Purpose : Detect the main price movement of the day, driven by institutional distribution.

Trading Insight : Enter trades in the direction of the trend established during this phase. Look for confirmations such as breakouts or strong directional moves that align with broader market sentiment

🔵 Settings

Show or Hide Phases :mDecide whether to display Accumulation, Manipulation, or Distribution.

Adjust the session times for each phase :

Accumulation: 1900-0100 EST

Manipulation: 0100-0700 EST

Distribution: 0700-1300 EST

Modify Visualization : Customize how the indicator looks by changing settings like colors and transparency.

🔵 Conclusion

The ICT Power of 3 (PO3) indicator is a powerful tool for traders seeking to understand and leverage market structure based on time and price dynamics. By visually highlighting the three key phases—Accumulation, Manipulation, and Distribution—this indicator simplifies the complex movements of institutional trading strategies.

With its customizable settings and clear representation of market behavior, the indicator is suitable for traders at all levels, helping them anticipate market trends and make more informed decisions.

Whether you're identifying entry points in the Accumulation phase, navigating false moves during Manipulation, or capitalizing on trends in the Distribution phase, this tool provides valuable insights to enhance your trading performance.

By integrating this indicator into your analysis, you can better align your strategies with institutional movements and improve your overall trading outcomes.

Buscar en scripts para "order"

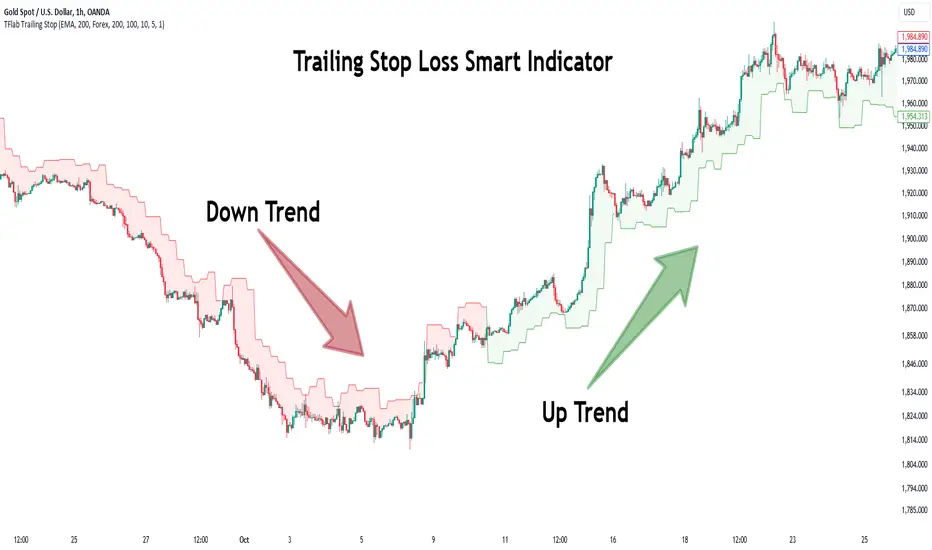

Trailing Stop Loss Smart [TradingFinder] Market Trend + CVD/EMA🔵 Introduction

Trailing Stop Loss (TSL) is one of the most powerful tools available. A Trailing Stop Loss is a modification of a typical stop order that adjusts dynamically based on market price movement. It can be set at a defined percentage or dollar amount away from the security's current market price, making it a flexible tool for locking in profits while minimizing risk. Unlike standard stop-loss orders, a Trailing Stop follows the market in the direction of the trade, protecting gains without requiring constant manual adjustments.

The Trailing Stop Loss Smart (TFlab Trailing Stop) indicator takes this concept even further by incorporating advanced metrics like Cumulative Volume Delta (CVD), volume dynamics, and Average True Range (ATR). This combination not only enhances risk management but also acts as a trend identifier, providing traders with a powerful tool to capitalize on both short-term and long-term price movements.

This indicator also supports various Order Types, allowing for flexible strategies that include a trailing stop/stop-loss combo to maximize winning trades while minimizing losses. The trailing stop limit is particularly useful for traders who want to set their stop at a precise level relative to the current market price, either by a percentage or a dollar amount. The Trailing Stop Loss Smart indicator can help ensure that traders do not exit too early during trends, while the stop-loss feature kicks in during reversals.

The advantages of using a Trailing Stop Loss are its ability to protect profits and reduce the emotional decision-making process in volatile markets. However, like all trading strategies, it has disadvantages, such as the risk of triggering too early during normal market fluctuations. By understanding how the Trailing Stop Loss Smart indicator integrates features like CVD, ATR, and volume analysis, traders can leverage its full potential while navigating these pros and cons.

With its unique ability to track market movements and trends using Cumulative Volume Delta, volume dynamics, and ATR-based trailing stops, this indicator offers a complete solution for traders looking to secure profits while minimizing downside risk. Whether you're employing a simple trailing stop or a trailing stop/stop-loss combo, this tool provides all the flexibility and precision needed to execute winning trades in various markets, including Forex, Crypto, and Stock.

🔵 How to Use

The Trailing Stop Loss Smart indicator integrates multiple advanced components to provide traders with superior risk management and trend identification.

Here’s how each part of the logic works :

🟣 Cumulative Volume Delta (CVD) Logic

The CVD tracks buying and selling pressure by calculating the difference between upward and downward price movements. When there’s more buying pressure, the CVD is positive, indicating a potential bullish trend. Conversely, more selling pressure results in a negative CVD, pointing to a bearish trend.

CVD Trend Detection : The indicator determines whether the market is in a bullish or bearish phase by comparing the CVD to its moving average. A bullish trend is confirmed when the CVD is above its moving average and the price is closing higher.

A bearish trend occurs when the CVD is below its moving average and the price is closing lower. This trend detection is critical for determining whether the trailing stop should be placed below the price (bullish) or above it (bearish).

🟣 Volume Dynamics

Volume is a key factor in identifying market strength. The Trailing Stop Loss Smart indicator pulls volume data based on the market selected (Forex, Crypto, or Stock) and adjusts the trailing stop based on whether the market is experiencing high volume or low volume.

High Volume : When the current volume exceeds the average volume, the market is in a high-volume state. During these conditions, the trailing stop is placed closer to the price, as high volume often indicates strong trends with less chance of reversals.

Low Volume : In low-volume conditions, the trailing stop gives the market more room to breathe by placing the stop further away from the price. This prevents premature stop-outs in periods of reduced market activity.

🟣 ATR-Based Trailing Stop

The Average True Range (ATR) is used to measure market volatility. The Trailing Stop Loss Smart uses the ATR to dynamically adjust the stop-loss distance.

Bullish Market : When a bullish trend is detected, the trailing stop is placed below the lowest price of the recent bars (determined by the Bar Back parameter), and adjusted by the ATR Multiplier. This allows for tighter protection during strong bullish trends.

Bearish Market : When the market is bearish, the trailing stop is placed above the highest price of recent bars, also adjusted by the ATR Multiplier. This ensures that short positions are safeguarded against sudden reversals.

🟣 Dynamic Stop-Loss Updates

The trailing stop is updated every few bars (according to the Refiner parameter), ensuring it remains relevant to the most recent price action and volume changes. This dynamic feature ensures the stop-loss adapts to both trending and volatile market conditions, without requiring manual intervention.

High Volume with Trends : In periods of high volume and a confirmed trend, the stop-loss is positioned tightly to lock in profits while minimizing the risk of reversal.

Low Volume with Trends : In low-volume conditions, the stop-loss is placed further from the price, allowing the market to move freely without triggering premature exits.

🟣 Visual Representation

The indicator visually represents the trailing stop on the chart, with green lines indicating bullish trends and red lines for bearish trends. This visual aid helps traders quickly assess the state of the market and the position of their trailing stop in real-time.

🔵 Settings

The Trailing Stop Loss Smart indicator offers several customizable settings to suit various trading strategies. Understanding these inputs is key to optimizing the tool for your specific trading style.

🟣 General Settings

Cumulative Mode : This controls how the CVD is calculated.

You can choose between :

EMA : Exponential Moving Average smoothing.

Periodic : Sums the delta over a fixed period.

CVD Period : Defines the look-back period for CVD calculation. A longer period smooths the data, making it less sensitive to short-term fluctuations.

Ultra Data : This Boolean input aggregates volume across multiple exchanges for a more comprehensive view of market activity.

Market Ultra Data : Select between Forex, Crypto, and Stock to ensure the indicator pulls accurate volume data for your market.

🟣 Logical Settings

Moving Average CVD Period : Defines the period for the moving average of the CVD. A longer period smooths the trend, reducing noise.

Moving Average Volume Period : Sets the period for the moving average used to distinguish between high and low volume conditions.

Level Finder Bar Back : Determines how many bars to look back when identifying the highest or lowest price for trailing stop placement.

Levels update per candles : Sets how often (in bars) the trailing stop should be updated to remain in sync with market movements.

ATR On : Toggles the use of ATR to adjust the trailing stop based on volatility.

ATR Multiplie r: Defines how far the stop is placed from the price based on the ATR. A larger multiplier increases the stop distance, reducing the likelihood of getting stopped out during market fluctuations.

ATR Multiplier Adjusts the distance of the trailing stop based on the ATR. A higher multiplier places the stop further from the price, providing more breathing room in volatile markets.

🔵 Conclusion

The Trailing Stop Loss Smart indicator is a comprehensive tool for traders looking to manage risk while identifying market trends. By incorporating Cumulative Volume Delta (CVD) to detect buying and selling pressure, volume dynamics to gauge market activity, and ATR to adjust for volatility, this indicator ensures that stop-loss levels are both adaptive and protective.

Whether you’re trading in Forex, Crypto, or Stock markets, the Trailing Stop Loss Smart allows you to capitalize on trends while dynamically adjusting to changing market conditions. Its ability to distinguish between high-volume and low-volume periods ensures that you’re not stopped out prematurely during periods of consolidation or market hesitation.

By providing real-time visual feedback, dynamic adjustments, and trend identification, this indicator serves as a vital tool for traders aiming to maximize profits while minimizing risk. Its versatility and adaptability make it an essential part of any trader’s toolkit, helping you stay ahead in fast-moving markets while safeguarding your positions.

Delta Dashboard with Custom Candle Count "Delta Dashboard with Custom Candle Count," creates a dynamic table on a chart that shows Buying Delta, Selling Delta, and Cumulative Delta for a user-defined number of candles. It is designed to give traders an easy-to-read visual dashboard for analyzing volume-based deltas, potentially helping to identify bullish or bearish trends.

Script Overview:

Custom Timeframe Input: The user has the option to enable a custom lower timeframe (useCustomTimeframeInput). If enabled, the script uses the lowerTimeframeInput (default is 1 minute) to request data from a lower timeframe. If not enabled, the script automatically selects a timeframe based on the chart’s current settings.

Candle Count Input: The script allows the user to specify the number of candles (numCandlesInput) for which they want to track volume deltas. This input determines how many columns are included in the delta dashboard.

Proportional Buy/Sell Volume Calculation: The script calculates the buy and sell volume for each candle. The buy volume is based on how much the price has moved up from the low, while the sell volume is based on how much the price has moved down from the high. The total volume is then split between buyers and sellers for a more accurate volume-based analysis.

Lower Timeframe Volume Data: The script requests volume data from the lower timeframe and uses it to calculate the positive (buying) and negative (selling) volume arrays over the specified number of candles.

Cumulative Delta: The cumulative delta is calculated as the difference between buying volume (positiveVolume) and selling volume (negativeVolume). The delta is accumulated over the day, and it resets at the start of each new day.

Dashboard Creation: The script creates a table (deltaTable) that is displayed on the chart, showing the following for each candle:

Buying Delta: The volume of buy orders.

Selling Delta: The volume of sell orders.

Cumulative Delta: The net difference between buying and selling volumes over the course of the day.

Dynamic Table Updating: The table updates with each new candle. The current candle's data is dynamically added to the table, and older candles shift to the left. When the maximum number of candles (as defined by numCandlesInput) is reached, the table wraps around, continuously updating with the latest data.

Abnormal Volume Detection: The script highlights candles where abnormal volume is detected. If the buying or selling volume for a particular candle is greater than twice the 50-period moving average volume, it highlights the respective cells in the table with shaded background colors:

Green: Indicates abnormal buying volume.

Red: Indicates abnormal selling volume.

Blue: Highlights abnormal cumulative delta spikes.

Daily Reset: The script automatically clears the table at the start of each new day, ensuring that the dashboard only reflects data from the current trading day.

How to Use:

Adding to Chart: To use this script, apply it to your TradingView chart. The dashboard will automatically appear in the upper left corner of the chart, showing volume-based delta data for each candle.

Customizing Timeframe: If you want to use a different timeframe for delta calculation (e.g., 1-second or 1-minute chart data), enable the Use Custom Timeframe option and specify the desired timeframe in the input section.

Adjusting the Number of Candles: You can adjust the number of candles shown in the delta dashboard by changing the Number of Candles input. The script will track the volume deltas for this number of candles, displaying them in the dashboard.

Interpreting the Dashboard:

Buying Delta: A higher positive value indicates stronger buying pressure in that candle.

Selling Delta: A higher negative value indicates stronger selling pressure in that candle.

Cumulative Delta: This value gives the net result of buying versus selling pressure across the trading day. Positive cumulative delta suggests buying dominance, while negative cumulative delta suggests selling dominance.

Abnormal Volume Detection: When abnormal volume spikes occur, pay attention to highlighted rows:

Green cells show that buying volume is unusually high.

Red cells indicate unusually high selling volume.

Blue cells mark large spikes in cumulative delta.

This script can be particularly useful for traders who want to gauge market sentiment based on volume distribution and detect abnormal trading activity, which could precede significant price movements.

ARIMA Indicator with Optional SmoothingOverview

The ARIMA (AutoRegressive Integrated Moving Average) Indicator is a powerful tool used to forecast future price movements by combining differencing, autoregressive, and moving average components. This indicator is designed to help traders identify trends and potential reversal points by analyzing the historical price data.

Key Features

AutoRegressive Component (AR): Utilizes past values to predict future prices.

Moving Average Component (MA): Averages past price differences to smooth out noise.

Differencing: Reduces non-stationarity in the time series data.

Optional Smoothing: Applies EMA to the ARIMA output for a smoother signal.

Customizable Parameters: Allows users to adjust AR and MA orders, differencing periods, and smoothing lengths.

Concepts Underlying the Calculations

Differencing: Subtracts previous prices from current prices to remove trends and seasonality, making the data stationary.

AutoRegressive Component (AR): Predicts future prices based on a linear combination of past values.

Moving Average Component (MA): Uses past forecast errors to refine future predictions.

Exponential Moving Average (EMA): Applies more weight to recent prices, providing a smoother and more responsive signal.

How It Works

The ARIMA Indicator first calculates the differenced series to achieve stationarity. Then, it computes the simple moving average (SMA) of this differenced series. The indicator uses the AR and MA components to adjust the SMA, creating an approximation of the ARIMA model. Finally, an optional smoothing step using EMA can be applied to the ARIMA approximation to produce a smoother signal.

How Traders Can Use It

Traders can use the ARIMA Indicator to:

Identify Trends: Detect emerging trends by observing the direction of the ARIMA line.

Spot Reversals: Look for divergences between the ARIMA line and the price to identify potential reversal points.

Generate Trading Signals: Use crossovers between the ARIMA line and the price to generate buy or sell signals.

Filter Noise: Enable the optional smoothing to filter out market noise and focus on significant price movements.

Example Usage Instructions

Add the ARIMA Indicator to your chart.

Adjust the input parameters to suit your trading strategy:

Set the SMA Length (e.g., 14).

Choose the Differencing Period (e.g., 1).

Define the AR Order (p) and MA Order (q) (e.g., 1).

Configure the Smoothing Length if smoothing is desired (e.g., 5).

Enable or disable smoothing as needed.

Observe the ARIMA line (blue) and compare it to the price chart.

Use the ARIMA line to identify trends and potential reversals.

Implement trading decisions based on the ARIMA line’s behavior relative to the price.

Swing Pivots [UkutaLabs]█ OVERVIEW

The Swing Pivots indicator uses relevant price-action information to identify key levels of Support and Resistance. Traders will be able to use current day Swing Pivots as well as mirror higher time frame Swing Pivots to gain a stronger understanding of overall market strength and key levels.

The aim of this script is to improve the users trading experience by offering a versatile toolkit that can be used in a wide variety of trading strategies to help simplify the complexities of the market.

█ USAGE

Throughout the trading day, the script will automatically identify key High and Low levels in the market based on currently relevant price action information, giving users potentially strong support and resistance levels which serve to guide the trader throughout the complexities in the market.

The script will also Identify powerful Order Blocks which are clusters of orders executed at a specific price level which represent an imbalance between supply and demand. By identifying Order Blocks, the script can indicate valuable supply and demand zones which help signal potential market turning points for the trader.

Furthermore, the script allows the user to mirror higher time frame Swing Pivots onto lower time frame charts to gain a stronger understanding of overall market strength and key levels on multiple time frames from a single chart.

█ SETTINGS

Configuration

Pivot Strength: Determines the sensitivity of the pivot calculation. A higher strength will result in less pivots being drawn, and a lower strength will result in more pivots being drawn.

Current Time frame

• Display: Determines whether or not Swing Pivots from the current time frame will be drawn on the chart.

5 Minute (Higher Time Frame)

• Display: Determines whether or not Swing Pivots from the 5 minute time frame will be drawn on the chart.

15 Minute (Higher Time Frame)

• Display: Determines whether or not Swing Pivots from the 15 minute time frame will be drawn on the chart.

30 Minute (Higher Time Frame)

• Display: Determines whether or not Swing Pivots from the 30 minute time frame will be drawn on the chart.

1 Hour (Higher Time Frame)

• Display: Determines whether or not Swing Pivots from the 1 hour time frame will be drawn on the chart.

4 Hour (Higher Time Frame)

• Display: Determines whether or not Swing Pivots from the 4 hour time frame will be drawn on the chart.

Daily (Higher Time Frame)

• Display: Determines whether or not Swing Pivots from the daily time frame will be drawn on the chart.

[SGM GARCH Volatility]I'm excited to share with you a Pine Script™ that I developed to analyze GARCH (Generalized Autoregressive Conditional Heteroskedasticity) volatility. This script allows you to calculate and plot GARCH volatility on TradingView. Let's see together how it works!

Introduction

Volatility is a key concept in finance that measures the variation in prices of a financial asset. The GARCH model is a statistical method that predicts future volatility based on past volatilities and prediction residuals (errors).

Indicator settings

We define several parameters for our indicator:

length = input.int(20, title="Length")

p = input.int(1, title="Lag order (p)")

q = input.int(1, title="Degree of moving average (q)")

cluster_value = input(0.2,title="cluster value")

length: The period used for the calculations, default 20.

p: The order of the delay for the GARCH model.

q: The degree of the moving average for the GARCH model.

cluster_value: A threshold value used to color the graph.

Calculation of logarithmic returns

We calculate logarithmic returns to capture price changes:

logReturns = math.log(close) - math.log(close )

Initializing arrays

We initialize arrays to store residuals and volatilities:

var float residuals = array.new_float(length, 0)

var float volatilities = array.new_float(length, 0)

We add the new logarithmic returns to the tables and keep their size constant:

array.unshift(residuals, logReturns)

if (array.size(residuals) > length)

array.pop(residuals)

We then calculate the mean and variance of the residuals:

meanResidual = array.avg(residuals)

varianceResidual = array.stdev(residuals, meanResidual)

volatility = math.sqrt(varianceResidual)

We update the volatility table with the new value:

array.unshift(volatilities, volatility)

if (array.size(volatilities) > length)

array.pop(volatilities)

GARCH volatility is calculated from accumulated data:

var float garchVolatility = na

if (array.size(volatilities) >= length and array.size(residuals) >= length)

alpha = 0.1 // Alpha coefficient

beta = 0.85 // Beta coefficient

omega = 0.01 // Omega constant

sumVolatility = 0.0

for i = 0 to p-1

sumVolatility := sumVolatility + beta * math.pow(array.get(volatilities, i), 2)

sumResiduals = 0.0

for j = 0 to q-1

sumResiduals := sumResiduals + alpha * math.pow(array.get(residuals, j), 2)

garchVolatility := math.sqrt(omega + sumVolatility + sumResiduals)

Plot GARCH volatility

We finally plot the GARCH volatility on the chart and add horizontal lines for easier visual analysis:

plt = plot(garchVolatility, title="GARCH Volatility", color=color.rgb(33, 149, 243, 100))

h1 = hline(0.1)

h2 = plot(cluster_value)

h3 = hline(0.3)

colorGarch = garchVolatility > cluster_value ? color.red: color.green

fill(plt, h2, color = colorGarch)

colorGarch: Determines the fill color based on the comparison between garchVolatility and cluster_value.

Using the script in your trading

Incorporating this Pine Script™ into your trading strategy can provide you with a better understanding of market volatility and help you make more informed decisions. Here are some ways to use this script:

Identification of periods of high volatility:

When the GARCH volatility is greater than the cluster value (cluster_value), it indicates a period of high volatility. Traders can use this information to avoid taking large positions or to adjust their risk management strategies.

Anticipation of price movements:

An increase in volatility can often precede significant price movements. By monitoring GARCH volatility spikes, traders can prepare for potential market reversals or accelerations.

Optimization of entry and exit points:

By using GARCH volatility, traders can better identify favorable times to enter or exit a position. For example, entering a position when volatility begins to decrease after a peak can be an effective strategy.

Adjustment of stops and objectives:

Since volatility is an indicator of the magnitude of price fluctuations, traders can adjust their stop-loss and take-profit orders accordingly. Periods of high volatility may require wider stops to avoid being exited from a position prematurely.

That's it for the detailed explanation of this Pine Script™ script. Don’t hesitate to use it, adapt it to your needs and share your feedback! Happy analysis and trading everyone!

Open Interest Profile [Fixed Range] - By LeviathanThis script generates an aggregated Open Interest profile for any user-selected range and provides several other features and tools, such as OI Delta Profile, Positive Delta Levels, OI Heatmap, Range Levels, OIWAP, POC and much more.

The indicator will help you find levels of interest based on where other market participants are opening and closing their positions. This provides a deeper insight into market activity and serves as a foundation for various different trading strategies (trapped traders, supply and demand, support and resistance, liquidity gaps, imbalances,liquidation levels, etc). Additionally, this indicator can be used in conjunction with other tools such as Volume Profile.

Open Interest (OI) is a key metric in derivatives markets that refers to the total number of unsettled or open contracts. A contract is a mutual agreement between two parties to buy or sell an underlying asset at a predetermined price. Each contract consists of a long side and a short side, with one party consenting to buy (long) and the other agreeing to sell (short). The party holding the long position will profit from an increase in the asset's price, while the one holding the short position will profit from the price decline. Every long position opened requires a corresponding short position by another market participant, and vice versa. Although there might be an imbalance in the number of accounts or traders holding long and short contracts, the net value of positions held on each side remains balanced at a 1:1 ratio. For instance, an Open Interest of 100 BTC implies that there are currently 100 BTC worth of longs and 100 BTC worth of shorts open in the market. There might be more traders on one side holding smaller positions, and fewer on the other side with larger positions, but the net value of positions on both sides is equivalent - 100 BTC in longs and 100 BTC in shorts (1:1). Consider a scenario where a trader decides to open a long position for 1 BTC at a price of $30k. For this long order to be executed, a counterparty must take the opposite side of the contract by placing a short order for 1 BTC at the same price of $30k. When both long and short orders are matched and executed, the Open Interest increases by 1 BTC, indicating the introduction of this new contract to the market.

The meaning of fluctuations in Open Interest:

- OI Increase - signifies new positions entering the market (both longs and shorts).

- OI Decrease - indicates positions exiting the market (both longs and shorts).

- OI Flat - represents no change in open positions due to low activity or a large number of contract transfers (contracts changing hands instead of being closed).

Typically, we monitor Open Interest in the form of its running value, either on a chart or through OI Delta histograms that depict the net change in OI for each price bar. This indicator enhances Open Interest analysis by illustrating the distribution of changes in OI on the price axis rather than the time axis (akin to Volume Profiles). While Volume Profile displays the volume that occurred at a given price level, the Open Interest Profile offers insight into where traders were opening and closing their positions.

How to use the indicator?

1. Add the script to your chart

2. A prompt will appear, asking you to select the “Start Time” (start of the range) and the “End Time” (end of the range) by clicking anywhere on your chart.

3. Within a few seconds, a profile will be generated. If you wish to alter the selected range, you can drag the "Start Time" and "End Time" markers accordingly.

4. Enjoy the script and feel free to explore all the settings.

To learn more about each input in indicator settings, please read the provided tooltips. These can be accessed by hovering over or clicking on the ( i ) symbol next to the input.

Net Positions (Net Longs & Net Shorts) - By LeviathanThis script is an experimental indicator that visualizes the entering and exiting of long and short positions in the market. It also includes other useful tools, such as NL/NS Profile, NL/NS Delta, NL/NS Ratio, Volume Heatmap, Divergence finder, Relative Strength Index of Net Longs and Net Shorts, EMAs and VWMAs and more.

To avoid misinterpretation, it's important to understand some basics. The “real” ratio between net long and net short positions in a given market is always 1:1. A futures contract is an agreement between two parties to buy or sell an underlying asset at an agreed-upon price. Each contract has a long side and a short side, with one party agreeing to buy (long) and the other party agreeing to sell (short) the asset at the agreed-upon price. The long position holder anticipates that the asset's price will rise, while the short position holder expects it to fall. Because every futures contract involves both a buyer and a seller, it is impossible to have more net longs than net shorts or vice versa (in terms of the net value). For every long position opened, there must be a corresponding short position taken by another market participant (and vice versa), thus maintaining the 1:1 ratio between longs and shorts. While there can be an imbalance in the number of traders/accounts holding long and short contracts, the net value of positions held on each side remains 1 to 1.

Open Interest (OI) is a metric that tracks the number of open (unsettled) contracts in a given market. For example, Open Interest of 100 BTC means that there are currently 100 BTC worth of longs and 100 BTC worth of shorts open in the market. There may be more traders on one side holding smaller positions, and fewer traders on the other side holding larger positions, but the net value of positions on one side is equal to the net value of positions on the other side → 100 BTC in longs and 100 BTC in shorts (1:1). Consider a scenario in which a trader decides to open a long position for 1 BTC at a price of HKEX:30 ,000. For this long order to be executed, a counterparty must take the opposite side of the contract by placing an order to short 1 BTC at the same price of HKEX:30 ,000. When both the long and short orders are matched and executed, the open interest increases by 1 BTC, reflecting the addition of this new contract to the market.

Changes in Open Interest essentially tell us 3 things:

- OI Increase - new positions entered the market (both longs and shorts!)

- OI Decrease - positions exited the market (both longs and shorts!)

- OI Flat - no change in open positions due to low activity or simply lots of transfers of contracts

However, different concepts can be used to analyze sentiment, aggressiveness, and activity in the market by analyzing data such as Open Interest, price, volume, etc. This indicator combines Open Interest data and price action to simplify the visualization of positions entering and exiting the market. It is based on the following concept:

Increase in Open Interest + Increase in price = Longs Opening

Decrease in Open Interest + Decrease in price = Longs Closing

Increase in Open Interest + Decrease in price = Shorts Opening

Decrease in Open Interest + Increase in price = Shorts Closing

When "Longs Opening" occurs, the OI Delta value is added to the running total of Net Longs, and when "Longs Closing" occurs, the OI Delta value is subtracted from the running total of Net Longs.

When "Shorts Opening" occurs, the OI Delta value is added to the running total of Net Shorts, and when "Shorts Closing" occurs, the OI Delta value is subtracted from the running total of Net Shorts.

To summarize:

Net Longs: Cumulative value of Longs Opening and Longs Closing (LO - LC)

Net Shorts: Cumulative value of Shorts Opening and Shorts Closing (SO - SC)

Net Delta: Net Longs - Net Shorts

Net Ratio: Net Longs / Net Shorts

This is the fundamental logic of how this script functions, but it also includes several other tools and options. Here is an overview of the settings:

Type:

- Net Positions (display values of Net Longs, Net Shorts, Net Delta, Net Ratio as described above)

- Relative Strength (display Net Longs, Net Shorts, Net Delta, Net Ratio in the form of a momentum oscillator that measures the speed and change of movements. Same logic as RSI for price)

Display as:

- Candles (display the data in the form of candlesticks)

- Lines (display the data in the form of candlesticks)

- Columns (display the data in the form of columns)

Cumulation:

- Visible Range (data is cumulated from the first visible bar on your chart)

- Full Data (data is cumulated from the beginning)

Quoted in:

- Base Currency (all data is presented in the pair’s base currency eg. BTC)

- Quote Currency (all data is presented in the pair’s quote currency eg USDT)

OI Sources

- Pick the sources from where the data is collected (if available).

Net Positions:

- NET LONGS (show/hide Net Longs plot, choose candle colors, choose line color)

- NET SHORTS (show/hide Net Shorts plot, choose candle colors, choose line color)

- NET DELTA (show/hide Net Delta plot, choose candle colors, choose line color)

- NET RATIO (show/hide Net Ratio plot, choose candle colors, choose line color)

Moving Averages:

- Type (choose between EMA and Volume Weighted Moving Average)

- NET LONGS (show/hide NL moving average plot, choose length, choose color)

- NET SHORTS (show/hide NS moving average plot, choose length, choose color)

- NET DELTA (show/hide ND moving average plot, choose length, choose color)

- NET RATIO (show/hide NR moving average plot, choose length, choose color)

Profile:

- Profile Data (choose the source data of the profile)

- Value Area % (set the percentage width of profile’s value area)

- Positions (set the position of the profile to left or right of the visible range)

- Node Size (set the relative size of nodes to make them appear smaller or larger)

- Rows (select the amount of rows displayed by the profile to control granularity)

- POC (show/hide POC- Point Of Control and select its color)

- VA (show/hide VA- Value Area and select its color)

Divergence finder

- Source (choose the source data used by the script to compare it with price pivot points)

- Maximum distance (the maximum distance between two divergent pivot points)

- Lookback Bars Left (the number of bars to the left of the current bar that the function will consider when looking for a pivot point)

- Lookback Bars Right (the number of bars to the right of the current bar that the function will consider when looking for a pivot point)

Stats:

- Show/Hide the Stats table

- Bars Back (choose the length of data analyzed for stats in number of bars)

- Position (choose the position of the Stats table)

- Select Data you want to display in the Stats table

Additional Settings:

- Volume Heatmap (show/hide volume heatmap and select its color)

- Label Offset (select how much the plot label is shifted to the right

- Position Relative Strength Length (select the length used in the calculation)

- Value Label (show/hide OI Delta values when candles are displayed)

- Plot Labels (show/hide the labels next to the plot)

- Wicks (show/hide wick when candles are displayed)

Code used for generating profiles is taken from @KioseffTrading's "Profile Any Indicator" script (used with author's permission)

S&P500 Sectors Relative Overviewdear fellows,

this indicator is yet another representation of S&P 500 industry sectors.

it is inspired by mr. stanley drukenmiller who in an interview mentioned that he knows no better market forecaster than the inside of the sp500 itself, which are its industry sectors.

thus, we have been for a while thinking on how to represent the performance of these sectors such that one could visually estimated the current stage of the cycle, and grasp the next one.

unfortunatelly, we believe this cannot be achieved by solely looking into SP500 industry sectors. perhaps coupled with a broad market indicator like our MRI, for instance, one can have greater odds of success.

what does it show

it displays colorfully through out time how each sector travels through its 200 period high and lows.

note that an alternative view of the sectors relatively to SPX could be considered, but by now we focused on the relative performance against its recent past (200 period, regardless the timeframe).

over the colored columns we've plotted in white the SPX under the same logic.

how is it calculated

each sector price is converged into a percentage of how near it is to its 200 period low.

so, when the price of the sector index equals the 200 period min, it is valued as 0.

when it equals the 200 period max, it is valued as 100.

same for the white plot of SPX above the colored columns.

thus a flat reading at 100 makes it indistinguishable a continued ATH extension from a pause at the ATH.

how is it colored

when the converted price results in a value lesser or equal 33, its respective bar is colored in red.

when it is between 33 and 66, the bar is colored in yellow.

and when it lies above 66, in green.

on how is it grouped

the specific ordering of the sectors is not yet settled.

we've grouped it visually based on likelihood.

on how to use this indicator

although we believe that it does not suffice for any conclusion on the market, we do not believe that an above chart can improve the resulting insight. so, at least by the time being, we recommend it to be stared alone, although not exclusively, by trader.

we are open to suggestions of any sort.

your feedback is much appreciated.

this is a work we'd have been looking for a while to put it out.

enjoy.

best regards.

[XRP][1h] Chanu Delta inspired — Breakeven StrategyHello, this is my first TV contribution. I usually don't publish anything but the script is a quick review of an other contributor (Chanu Delta V3 script )

I reverse engineered this indicator today as I wanted to test it on other contracts. The original version (which aims to be traded on BTC) has been ported to XRP (as btc and xrp prices are narrowly correlated) then modified with a couple of what I believe are improvements:

- No backtest bias even with `security` function.

- Extra backtest bias validation, always trading on next bar as Crossover/under bias is confirmed

- Backtest with 2 ajustable TP, ajustable equity and breakeven option

- The current version is not design to use pyramiding as it would require extra logic to monitor the lifecycle of the position in the context of a study.

- Commented alerts examples with variables available in script scope so you can use them in alerts (just replace strategy with indicator and remove backtest related code block).

- Trade filling assumption set to 10, fees to 0.02 as the are default bybit maker fees and I advice to enter with trailing orders using a max of 2 ticks as offset to lower fees rather than a market order!

- Backtest and Alerts happen on barclose.

- No repaint guaranteed.

There are a thousand ways to improve it (adx/bb based dynamic TP/SL, order lifecycle, pyramiding...) but it seems to be a cool starting point.

Don't forget to have fun!

SUPPORT RESISTANCE STRATEGY [5MIN TF]A SUPPORT RESISTANCE BREAKOUT STRATEGY for 5 minute Time-Frame , that has the time condition for Indian Markets

The Timing can be changed to fit other markets, scroll down to "TIME CONDITION" to know more.

The commission is also included in the strategy .

The basic idea is when ,

1) Price crosses above Resistance Level ,indicated by Red Line, is a Long condition.

2) Price crosses below Support Level ,indicated by Green Line , is a Short condition.

3) Candle high crosses above ema1, is a part of the Long condition .

4) Candle low crosses below ema1, is a part of the Short condition .

5) Volume Threshold is an added confirmation for long/short positions.

6) Maximum Risk per trade for the intraday trade can be changed .

7) Default qty size is set to 50 contracts , which can be changed under settings → properties → order size.

8) ATR is used for trailing after entry, as mentioned in the inputs below.

// ═════════════════════════//

// ————————> INPUTS <————————— //

// ═════════════════════════//

→ L_Bars ———————————> Length of Resistance / Support Levels.

→ R_Bars ———————————> Length of Resistance / Support Levels.

→ Volume Break ———————> Volume Breakout from range to confirm Long/Short position.

→ Price Cross Ema —————> Added condition as explained above (3) and (4).

→ ATR LONG —————————> ATR stoploss trail for Long positions.

→ ATR SHORT ————————> ATR stoploss trail for Short positions.

→ RISK ————————————> Maximum Risk per trade intraday.

The strategy was back-tested on TCS ,the input values and the results are mentioned under "BACKTEST RESULTS" below.

// ═════════════════════════ //

// ————————> PROPERTIES<——————— //

// ═════════════════════════ //

Default_qty_size ————> 50 contracts , which can be changed under

Settings

↓

Properties

↓

Order size

// ═══════════════════════════════//

// ————————> TIME CONDITION <————————— //

// ═══════════════════════════════//

The time can be changed in the script , Add it → click on ' { } ' → Pine editor→ making it a copy [right top corner} → Edit the line 27.

The Indian Markets open at 9:15am and closes at 3:30pm.

The 'time_cond' specifies the time at which Entries should happen .

"Close All" function closes all the trades at 3pm , at the open of the next candle.

To change the time to close all trades , Go to Pine Editor → Edit the line 92 .

All open trades get closed at 3pm , because some brokers don't allow you to place fresh intraday orders after 3pm .

// ═══════════════════════════════════════════════ //

// ————————> BACKTEST RESULTS ( 100 CLOSED TRADES )<————————— //

// ═══════════════════════════════════════════════ //

INPUTS can be changed for better Back-Test results.

The strategy applied to NSE:TCS ( 5 min Time-Frame and contract size 50) gives us 60% profitability , as shown below

It was tested for a period a 6 months with a Profit Factor of 1.8 ,net Profit of 30,000 Rs profit .

Sharpe Ratio : 0.49

Sortino Ratio : 1.4

The graph has a Linear Curve with Consistent Profits.

The INPUTS are as follows,

1) L_Bars —————————> 4

2) R_Bars —————————> 4

3) Volume Break ————> 5

4) Price Cross Ema ——> 100

5) ATR LONG ——————> 2.4

6) ATR SHORT —————> 2.6

7) RISK —————————> 2000

8) Default qty size ——> 50

NSE:TCS

Save it to favorites.

Apply it to your charts Now !!

Thank You ☺ NSE:TCS

PIVOT STRATEGY [INDIAN MARKET TIMING]

A Back-tested Profitable Strategy for Free!!

A PIVOT INTRADAY STRATEGY for 5 minute Time-Frame , that also explains the time condition for Indian Markets

The Timing can be changed to fit other markets, scroll down to "TIME CONDITION" to know more.

The commission is also included in the strategy .

The basic idea is when ,

1) Price crosses above ema1 ,indicated by pivot highest line in green color .

2) Price crosses below ema1 ,indicated by pivot lowest line in red color .

3) Candle high crosses above pivot highest , is the Long condition .

4) Candle low crosses below pivot lowest , is the Short condition .

5) Maximum Risk per trade for the intraday trade can be changed .

6) Default_qty_size is set to 60 contracts , which can be changed under settings → properties → order size .

7) ATR is used for trailing after entry, as mentioned in the inputs below.

// ═════════════════════════//

// ————————> INPUTS <————————— //

// ═════════════════════════//

Leftbars —————> Length of pivot highs and lows

Rightbars —————> Length of pivot highs and lows

Price Cross Ema —————> Added condition

ATR LONG —————> ATR stoploss trail for Long positions

ATR SHORT —————> ATR stoploss trail for Short positions

RISK —————> Maximum Risk per trade for the day

The strategy was back-tested on RELIANCE ,the input values and the results are mentioned under "BACKTEST RESULTS" below .

// ═════════════════════════ //

// ————————> PROPERTIES<——————— //

// ═════════════════════════ //

Default_qty_size ————> 60 contracts , which can be changed under settings

↓

properties

↓

order size

// ═══════════════════════════════//

// ————————> TIME CONDITION <————————— //

// ═══════════════════════════════//

The time can be changed in the script , Add it → click on ' { } ' → Pine editor→ making it a copy [right top corner} → Edit the line 25 .

The Indian Markets open at 9:15am and closes at 3:30pm .

The 'time_cond' specifies the time at which Entries should happen .

"Close All" function closes all the trades at 3pm, at the open of the next candle.

To change the time to close all trades , Go to Pine Editor → Edit the line 103 .

All open trades get closed at 3pm , because some brokers don't allow you to place fresh intraday orders after 3pm .

NSE:RELIANCE

// ═══════════════════════════════════════════════ //

// ————————> BACKTEST RESULTS ( 128 CLOSED TRADES )<————————— //

// ═══════════════════════════════════════════════ //

INPUTS can be changed for better back-test results.

The strategy applied to NIFTY ( 5 min Time-Frame and contract size 60 ) gives us 60% profitability y , as shown below

It was tested for a period a 6 months with a Profit Factor of 1.45 ,net Profit of 21,500Rs profit .

Sharpe Ratio : 0.311

Sortino Ratio : 0.727

The graph has a Linear Curve with consistent profits .

The INPUTS are as follows,

1) Leftbars ————————> 3

2) Rightbars ————————> 5

3) Price Cross Ema ——————> 150

4) ATR LONG ————————> 2.7

5) ATR SHORT ———————> 2.9

6) RISK —————————> 2500

7) Default qty size ——————> 60

NSE:RELIANCE

Save it to favorites.

Apply it to your charts Now !!

↓

FOLLOW US FOR MORE !

Thank me later ;)

STD-Filtered, N-Pole Gaussian Filter [Loxx]This is a Gaussian Filter with Standard Deviation Filtering that works for orders (poles) higher than the usual 4 poles that was originally available in Ehlers Gaussian Filter formulas. Because of that, it is a sort of generalized Gaussian filter that can calculate arbitrary (order) pole Gaussian Filter and which makes it a sort of a unique indicator. For this implementation, the practical mathematical maximum is 15 poles after which the precision of calculation is useless--the coefficients for levels above 15 poles are so high that the precision loss actually means very little. Despite this maximal precision utility, I've left the upper bound of poles open-ended so you can try poles of order 15 and above yourself. The default is set to 5 poles which is 1 pole greater than the normal maximum of 4 poles.

The purpose of the standard deviation filter is to filter out noise by and by default it will filter 1 standard deviation. Adjust this number and the filter selections (price, both, GMA, none) to reduce the signal noise.

What is Ehlers Gaussian filter?

This filter can be used for smoothing. It rejects high frequencies (fast movements) better than an EMA and has lower lag. published by John F. Ehlers in "Rocket Science For Traders".

A Gaussian filter is one whose transfer response is described by the familiar Gaussian bell-shaped curve. In the case of low-pass filters, only the upper half of the curve describes the filter. The use of gaussian filters is a move toward achieving the dual goal of reducing lag and reducing the lag of high-frequency components relative to the lag of lower-frequency components.

A gaussian filter with...

One Pole: f = alpha*g + (1-alpha)f

Two Poles: f = alpha*2g + 2(1-alpha)f - (1-alpha)2f

Three Poles: f = alpha*3g + 3(1-alpha)f - 3(1-alpha)2f + (1-alpha)3f

Four Poles: f = alpha*4g + 4(1-alpha)f - 6(1-alpha)2f + 4(1-alpha)3f - (1-alpha)4f

and so on...

For an equivalent number of poles the lag of a Gaussian is about half the lag of a Butterworth filters: Lag = N*P / pi^2, where,

N is the number of poles, and

P is the critical period

Special initialization of filter stages ensures proper working in scans with as few bars as possible.

From Ehlers Book: "The first objective of using smoothers is to eliminate or reduce the undesired high-frequency components in the eprice data. Therefore these smoothers are called low-pass filters, and they all work by some form of averaging. Butterworth low-pass filters can do this job, but nothing comes for free. A higher degree of filtering is necessarily accompanied by a larger amount of lag. We have come to see that is a fact of life."

References John F. Ehlers: "Rocket Science For Traders, Digital Signal Processing Applications", Chapter 15: "Infinite Impulse Response Filters"

Included

Loxx's Expanded Source Types

Signals

Alerts

Bar coloring

Related indicators

STD-Filtered, Gaussian Moving Average (GMA)

STD-Filtered, Gaussian-Kernel-Weighted Moving Average

One-Sided Gaussian Filter w/ Channels

Fisher Transform w/ Dynamic Zones

R-sqrd Adapt. Fisher Transform w/ D. Zones & Divs .

VXD SupercycleVXD is a brand new indicator and still developing. to minimize stop losses and overcome sideways market conditions, Higher Timeframe are recommended

Trend lines

-using Rolling VWAP as trend line to determined if Volume related to a certain price.

-you can switch RVWAP to EMA in the setting

ATR

-trailing 12*ATR and 2.4 Mutiplier

Pivot point and Rejected Block

Pivot show last High and low of a price in past bars

Rejected Block show when that High or Low price are important level to determined if it's Hidden Divergence or Divergence

Symbols on chart show Premium and Discount Prices

X-Cross - show potential reversal trend with weak volume .

O-circle - show potential reversal trend with strong volume .

Setting

Momentum: RSI = 25 , RSI MA = 14

Trend: Rolling VWAP and ATR and Subhag

Trailing STOP: ATR 12 x 2.4

Highlight Bars color when volume is above SMA 6

SMA200 act as TP Line

Risk:Reward Calculation

if Buy your Stoploss will be previous Pivot low

if Sell your Stoploss will be previous Pivot high and will be calculated form there, then show TP in Orange color line

VXD เป็นระบบเทรดที่ผมทดลองเอาหลาย ๆ ไอเดีย ทั้งจาก Youtube facebook และกลุ่มคนต่าง ๆ มารวบรวมไว้ แล้วตกผลึกขึ้นมาเป็นระบบนี้ ใน Timeframe ใหญ่ ๆ สามารถลากได้ทั้ง Cycle กันเลย

Trend lines

-ใช้ Rolling VWAP ของแอพ Tradingview (สามารถตั้งแค่าเป็น EMA ได้)

ATR

-ใช้ค่า ATR 12 Mutiplier 2.4

Pivot point and Rejected Block

Pivot โชว์เส้น High low และมีผลกับออเดอร์ หากแท่งเทียนปิดทะลุเส้นนี้

Rejected Block วาดแนวรับ-ต้าน อัตโนมัติ ใช้ประกอบ RSI ว่ามี Divergence หรือไม่

สัญลักษณ์ต่าง ๆ

X-Cross - แท่งกลืนกิน วอลุ่มน้อย

O-circle - แท่งกลืนกิน มีวอลุ่ม

Setting

Momentum: RSI = 25 , RSI MA = 14

Trend: Rolling VWAP and ATR and Subhag

Trailing STOP: ATR 12 x 2.4

Highlight Bars color when volume is above SMA 6

SMA200 act as TP Line

Risk:Reward Calculation

หาก Buy จุด SL จะอยู่ที่ Pivot low

หาก Sell จุด SL จะอยู่ที่ Pivot high และระบบจะคำนวณจากตรงนั้น จากนั้นแสดงเป็นเส้น TP สีส้ม

This Strategy Combined the following indicators and conditioning by me

ATR , RSI , EMA , SMA

Rolling VWAP - /script/ZU2UUu9T-Rolling-VWAP/

Regression Lines - Subhag form Subhag Ghosh /script/LHHBVpQu-Subhag-Ghosh-Algo-Version-for-banknifty/

Rejection Block , Pivots , High Volume Bars and PPDD form Super OrderBlock / FVG / BoS Tools by makuchaku & eFe /script/aZACDmTC-Super-OrderBlock-FVG-BoS-Tools-by-makuchaku-eFe/

ขอให้รวยครับ.

SuperJump Turn Back Bollinger BandThis is a simple indicator using bolinger band return.

After the candle's bolinger band broke out,

Turn back inside BB is the entry point.

Usually there are more than two triangles, so you can wait after ordering a better price.

As you already know about it, it is very dangerous for the bolinger band to enter in the reverse direction when a strong trend is created.

That's why I made the Red Line. It is calculated by ATR and will suggest you an appropriate StopLoss value.

[JL] EMA Trading ZoneI want to make a script to help catch pullback on a strong trend.

This script display colors based on EMAs' slope.

The trading zone is calculated from EMA short + - ATR

if 2 EMA lines' slope both are more than an angle, then the trading zone is green color, it can be considered to place long orders.

if 2 EMA lines' slope both are less than a negative angle, then the trading zone is red color, it can be considered to place short orders.

Otherwise the zone is blue color.

DCA Bot Long/Short Thanks to @TheTradingParrot for the inspiration and knowledge shared.

Thanks to @ericlin0122 for the original DCA Bot Emulator which is the backbone of this strategy.

The script simulates DCA strategy with parameters used in 3commas DCA bots for futures trading. Experiment with parameters

to find your trading setup.

Beware how large your total leveraged position is and how far can market go before you get liquidated!

Do that with the help of futures liquidation calculators you can find online!

I`ve added:

1) an internal average price and profit calculating, instead of TV`s native one, which is subject to severe slippage.

2) I`ve built a graphic interface, so levels are clearly visible and back-test analyzing made easier.

3) now both Long & Short direction of the strategy exist.

4) trailing TP which was featured in the initial script has been removed because TV`s execution model makes

it impossible to know how the real world trailing would have unfolded.

5) the table is self explanatory, and it is there to help you discover what happened and where.

6) vertical colored lines appear when the new maximum deviation from the original price has

been reached

All the trading happens with total account capital, and all order sizes inputs are expressed in percent.

Known issues:

When deviation is small, and the same candle triggers safety AND the close order, the initial orders are closed, but a

new one opens on the next candle. This is "resolved" by closing the unwanted trade forcefully on the next candle, affecting

profit calculating minimally and guaranteeing that what should be closed has been closed.

The code could be improved through use of arrays, making the table flexible so the number of rows should be dynamic depending

on the number of SOs.

!!!!! IMPORTANT!!!!!

This strategy script is made to receive a signal from an exterior study script, which should plot +100 for long or -100 for short

entry (that is by default - values can be changed in the strategy settings menu). That plot should be found in "Enter Trigger" input

dropdown menu at the bottom of strategy settings menu. Removing the "and trigger == long/short_trigger" condition from strategy entry

conditions makes the strategy open trades ASAP.

Cheers!

Price ActionFirst, you have to know price action, RTM price action Handbook could help you

this indicator shows you base and momentum candles

base candles could be zones of trade that show you fighting of bulls and bears, and momentum candles could show the power of those zones.

Base candles are white in the chart, and you can place your order at the good zone.

Rally candles and drop candles are momentum candles, and bold rally and bold drop show that it is more powerful than its before candle.

Zigzag compression is one way that shows the compression in trend.

it looks like the Wedges pattern at classic technical that shows pending orders are closed, so the target zone could be powerful to reverse the trend.

Black background of candle means that candle doesn't reach its before candle and so it is poor candle, I named it domination.

It is better to do not trade at poor candles.

At the end, I find Price action the best way to trade, and it makes you free of other indicator, even volume indicator.

This indicator is good for those who use price action strategy to trade and those who want to learn the price action.

It could be so helpful and reliable way to find the zones, and place buy or sell order and the target, specially for scalping.

[blackcat] L1 New TRIX ScalperNOTE: Because the originally released script failed to comply with the House Rule in the description, it was banned. After revising and reviewing the description, it is republished again. Please forgive the inconvenience caused.

Level: 1

Background

The Triple Exponential Moving Average (TRIX) indicator is a strong technical analysis tool. It can help investors determine the price momentum and identify oversold and overbought signals in a financial asset. Jack Hutson is the creator of the TRIX indicator . He created it in the early 1980s to show the rate of change in a triple exponentially smoothed moving average.

When used as an oscillator, it shows a potential peak and trough price zones. A positive value tells traders that there is an overbought market while a negative value means an oversold market. When traders use TRIX as a momentum indicator, it filters spikes in the price that are vital to the general dominant trend.

A positive value means momentum is rising while a negative value means that momentum is reducing. A lot of analysts believe that when the TRIX crosses above the zero line it produces a buy signal, and when it closes below the zero line, it produces a sell signal.The indicator has three major components:

Zero line

TRIX line (or histograms)

Percentage Scale

Function

The TRIX indicator determines overbought and oversold markets, and it can also be a momentum indicator. Just as it is with most oscillators, TRIX oscillates around a zero line. Additionally, divergences between price and TRIX can mean great turning points in the market. TRIX calculates a triple exponential moving average of the log of the price input. It calculates this based on the time specified by the length input for the current bar.

Trading TRIX indicator signals

Zero line cross

TRIX can help determine the impulse of the market. With the 0 value acting as a centerline, if it crosses from below, it will be mean that the impulse is growing in the market.Traders can, therefore, look for opportunities to place buy orders in the market. Similarly, a cross of the centerline from above will mean a shrinking impulse in the market. Traders can, therefore, look for opportunities to sell in the market.

Signal line cross

To select the best entry points, investors add a signal line on the TRIX indicator. The signal line is a moving average of the TRIX indicator, and due to this, it will lag behind the TRIX.A signal to place a buy order will occur when the TRIX crosses the signal line from below. In the same way, a signal to place a sell order will come up when the TRIX crosses the signal line from above. This is applicable in both trending and ranging markets.In trending markets, a signal line cross will indicate an end of the price retracement, and the main trend will resume. In ranging markets, a signal line confirms that resistance and support zones have been upheld in the market.

Divergences

Traders can use the Triple Exponential Average can to identify when important turning points can happen in the market. They can achieve this by looking at divergences. Divergences happen when the price is moving in the opposite direction as the TRIX indicator.When price makes higher highs but the TRIX makes lower highs, it means that the up-trend is weakening, and a bearish reversal is about to form. When the price makes lower lows, but the TRIX makes higher lows, it means that a bullish reversal is about to happen. Bullish and bearish divergences happen when the security and the indicator do not confirm themselves. A bullish divergence can happen when the security makes a lower low, but the indicator forms a higher low. This higher low means less downside momentum that may foreshadow a bullish reversal. A bearish divergence happens when the commodity makes a higher low, but the indicator forms a lower high. This lower high indicates weak upside momentum that can foreshadow a bearish reversal sometimes. Bearish divergences do not work well in strong uptrends. Even though momentum appears to be weakening due to the indicator is making lower highs, momentum still has a bullish bias as long as it is above its centerline.When bullish and bearish divergences work, they work very well. The secret is to separate the bad signals from the good signals.

Key Signal

RXval --> new TRIX indicator.

AvgTRX --> linear regression average of new TRIX indicator.

Remarks

This is a Level 1 free and open source indicator.

Feedbacks are appreciated.

Trend Surfers - Premium Breakout + AlertsTrend Surfers - Premium Breakout Strategy with Alerts

I am happy today to release the first free Trend Surfers complete Breakout Strategy!

The strategy includes:

Entry for Long and Short

Stoploss

Position Size

Exit Signal

Risk Management Feature

How the strategy works

This is a Trend Following strategy. The strategy will have drawdowns, but they will be way smaller than what you would go through with buy and old.

As a Trend Following strategy, we will buy on strength, when a breakout occurs. And sell on weakness.

The strategy includes a FIX Stoploss determined by an ATR multiple and a trailing Stoploss/Takeprofit also determined by an ATR multiple.

You can also manage your risk by entering the maximum % you are willing to risk on every trade. Additionally, there is an option to enter how many pairs you will be trading with the strategy. This will change your position size in order to make sure that you have enough funds to trade all your favorite pairs.

Use the strategy with alerts

This strategy is alert-ready. All you have to do is:

Go on a pair you would like to trade

Create an alert

Select the strategy as a Trigger

Wait for new orders to be sent to you

Every Entry (Long/Short) will include:

Market Entry (Enter position NOW!)

Stoploss price

Position Size

Leverage

* If you do not wish to use leverage, you can multiply the Position Size by the Leverage. But doing that, you might end up with a position greater than your equity. Trading on Futures is better in order to have accurate risk management.

Exit signals:

When you receive an exit signal, you need to close the position ASAP. If you want to keep your results as close as possible to the backtest results, you need to execute quickly and follow what the strategy is telling you.

Do not try to outsmart the strategy

Leave your emotion out of trading! If you trust the strategy, you will have way better returns than if you try to outsmart it. Follow each signal you receive even if it doesn't seem logical at the moment.

Become a machine that executes. Don't look at fundamentals. Follow the trend! Trust the strategy!

I hope you enjoy it!

Cvwap-Pvwap 2.0A simple vwap based Intraday trend indicator.

Volume-Weighted Average Price (VWAP) - the average price weighted by volume, starts when trading opens and ends when it closes. This can help institutions buy or sell in large orders, without disturbing the market.

After buying or selling, institutions compare instrument price to closing VWAP values at end of the day.

For big financial institutions;

A buy order executed below the VWAP value, considered a good fill because the security was bought at a below average price.

A sell order executed above the VWAP would be deemed a good fill because it was sold at an above average price.

Simple price based moving average is not helpful for them; = as it doesn't incorporates volume traded. Hence - VWAP :)

So how it helps us in decoding the IntraDay-trend? - Through a 2 day vwap co-relation.

So, Closing value of previous day vwap = Pvwap

Today's running vwap = Cvwap

Defining the IntraDay Trend:

Moderately Bullish = candle closing price above Pvwap but below Cvwap

Super Bullish = Closing price is above both (Cvwap and Pvwap)

Moderately Bearish = Closing price is above Cvwap but below Pvwap

Super Bearish = Closing Price is below both (Cvwap and Pvwap)

A big gap between the Cvwap and the candle closing price defines the strong participation from institutions in that direction. (Strong Trend)

Moving with the smart money, in the overall trend is a wise decision for any intraday trader and this helps at its best.

Arbitrage Sniper (POC)Good Morning Traders!

Today I want to share with you the proof-of-concept of how you would be able to do arbitrage with crypto pairs.

THE INDICATOR MUST BE PLACED ON THE TRADING PAIR OF THE TWO CURRENCIES (i.e. ETH/BTC, EOS/ETH etc.)

This arbitrage method is based on the transitional decorrelation between the crypto treding pair and the price ratio of the involved currencies, of course computing commissions as well.

Whenever the non-arbitrage condition is not respected, there is an arbitrage oportunity.

This indicator won't consider the chance of shorting, so if the arbitrage oportunity occurs the indicator will suggest you just the chance of buying the relative-undervalued currency (but inside the code you will know how to do the alternative method as well, by shorting the relative-overvalued currency)

Let's take the trading pair ETH/BTC (as in the graph) → if we assume commissions for the 0.075% of the order, the non-arbitrage condition will be presented like this

This arbitrage method will need three orders, so n=3

So let's assume that P(ETH)/(P(BTC)*P(ETH/BTC))>(1-0.075)^(-3) → it means that the price of Ethereum is currently overreated enough (relatively to the trading pair) for doing arbitrage.

We have two alternatives:

• Buy BTC, change it into ETH (by "buying" ETH in the trading pair ETH/BTC) and then sell ETH

• Sell ETH, buy BTC, change it into ETH (by "buying" ETH in the trading pair ETH/BTC)

On the other hand, if P(ETH)/(P(BTC)*P(ETH/BTC))<(1-0.075)^(-3) → it means that the price of Ethereum is currently underrared enough (relatively to the trading pair) for doing arbitrage.

We have two alternatives:

• Buy ETH, change it into BTC (by "selling" ETH in the trading pair ETH/BTC) and then sell BTC

• Sell BTC, buy ETH, change it into BTC (by "selling" ETH in the trading pair ETH/BTC)

I'm saying that is nothing more than a proof-of-concept since:

- Arbitrage Oportunities will emerge frequently just nearly zero commissions

- Data of prices are retrieved using security() function and there can be some delay (so the arbitrage oportunity will be already extinguished by the time the signal is retrieved)

- In order to have the freshest data, repiainting will occurr

KD compare strategy (交易策略對照組)This is a base and easy trading strategy for comparing my other strategy.

The strategy consider K >= 80 is strong target in the last high period,

and consider K <=20 is the weak target in the last low period.

In the strong target, the strategy may increase long at the first day when K < 50, until 2/3 max order limitation or strong target become to weak.

In the weak target, the strategy may increase short at the first day when K > 50, until 2/3 max order limitation or strong target become to strong.

there are three orders for this strategy.

when the strong become to weak, it may use the remain 1/3 to save itself, and change the direction at the next k > 50

when the weak become to weak, it may use the remain 1/3 to save itself, and change the direction at the next k < 50

這是一個簡單的雙向交易策略,用來對照我其他的策略。

當 K>=80 它會認為目前是強勢股,偏多操作

當 K<=20 它會認為目前是強勢股,偏空操作

當標的為強勢股時,當第一次 K<50 會加碼多單,最多買進2/3的持股,直到轉弱

當標的為弱勢股時,當第一次 K>50 會加碼空單,最多買進2/3的持股,直到轉強

當強勢轉弱勢時,會使用剩下的1/3來拯救持股,在下次 k > 50 出清持股

當弱勢轉強勢時,會使用剩下的1/3來拯救持股,在下次 k < 50 出清持股