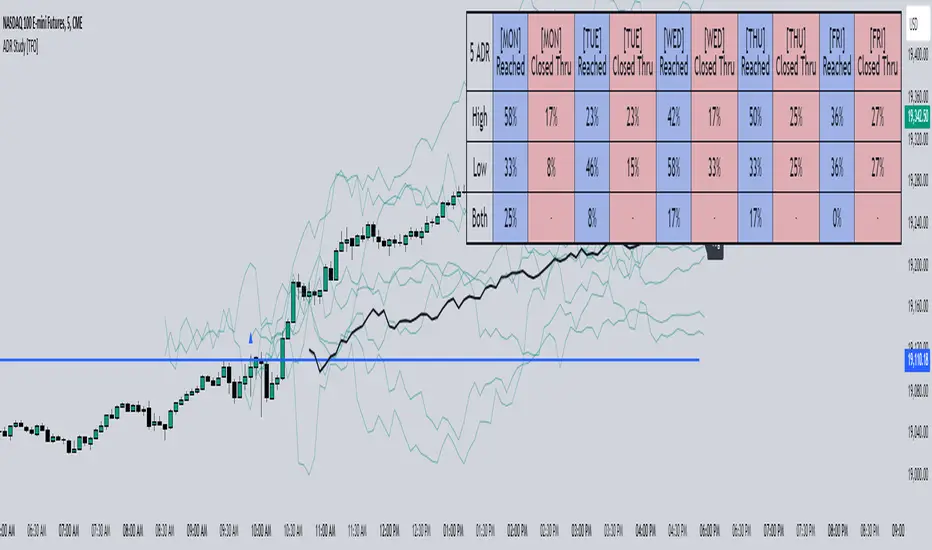

ADR Study [TFO]This indicator is focused on the Average Daily Range (ADR), with the goal of collecting data to show how often price reaches/closes through these levels, as well as a look at historical moves that reached ADR and at similar times of day to study how price moved for the remainder of the session.

The ADR here (blue line) is calculated using the difference between a day's highest and lowest points. If our ADR length is 5, then we are taking this difference from the last 5 days and averaging them together. At the following day's open, we take half of this average and plot it above and below the daily opening price to place theoretical limits on how far price may move according to the lookback period. The triangles indicate when price has reached ADR (either +ADR or -ADR), and alerts can be created for these events.

The Scale Factor is an optional parameter to scale the ADR by a certain amount. If set to 2 for example, then the ADR would be 2x the average daily range. This value will be reflected in the statistics options so that users can see how different values affect the outcomes.

Show Table will display data collected on how often price reaches these levels, and how often price closes through them, for each day of the week. By default, these are colored as blue and red, respectively. From the following chart of NQ1!, we can see for example that on Mondays, price reached +ADR 38% of the time and closed through it 23% of the time. Note that the statistics for closing through the ADR levels are derived from all instances, not just those that reached ADR.

Show Sample Sizes will display how many instances were collected for all given sets of data. Referring to the same example of NQ1!, we can see that this particular chart has collected data from 109 Mondays. From those Mondays, 41 reached +ADR (38%, verifying our initial claim) and 25 closed through it (23%). This is important to understand the scope of the data that we're working with, as percentages can be misleading for smaller sample sizes.

Show Histogram will plot the same exact data as the table, just in a histogram form to visually emphasize the differences on a day-by-day basis. On this chart of RTY1!, we can see for example from the top histogram that on Wednesdays, 40% reached +ADR and only 22% closed through it. Similarly if we look at the bottom histogram, we can see that Wednesdays reached -ADR 46% of the time and closed through it only 28% of the time.

We can also use Show Sample Sizes to display the same information that would be in the table, showing how many instances were collected for each event. In this case we can see that we observed 175 Fridays, where 76 reached +ADR (43%) and 44 closed above it (25%).

Show Historical Moves is an interesting feature of this script. When enabled, if price has reached +/- ADR in the current session, the indicator will plot the evolution of the close prices from all past sessions that reached +/- ADR to see how they traded for the remainder of the session. These calculations are made with respect to the ADR range at the time that price traded through these levels.

Historical Proximity (Bars) allows the user to observe historical moves where price reached ADR within this many bars of the current session (assuming price has reached an ADR level in the current session). In the above chart, this is set to 1000 so that we can observe each and every instance where price reached an ADR level. However, we can refine this a bit more.

By limiting the Historical Proximity to something like 20, we are only considering historical moves that reached ADR within 20 bars of todays +ADR reach (9:50 am EST, noted by the blue triangle up). We can enable Show Average Move to display the average move by the filtered dataset, and Match +/-ADR to only observe moves inline with the current day's price action (in this case, only moves that reached +ADR, since price has not reached -ADR).

We can add one more filter to this data with the setting Only Show Days That: closed through ADR; closed within ADR; or either. The option either is what you see above, as we are considering both days that closed through ADR and days that closed within it (note that in this case, closing within ADR simply means that price reached +ADR and closed the day below it, and vice versa for -ADR; this does not mean that price must have closed in between +ADR and -ADR). If we set this to only show instances that closed within ADR, we see the following data.

Alternatively, we can choose to Only Show Days That closed through ADR, where we would see the following data. In this case, the average move very much resembles the price action that occurred on this particular day. This is in no way guaranteed, but it makes an interesting case for how we could use this data in our analysis by observing similar, historical price action.

Please note that this data will change over time on a rolling basis due to TradingView's bar lookback, and that for this same reason, lower timeframes will yield less data than larger timeframes.

Buscar en scripts para "ha溢价率"

Intellect_city - World Cycle - Ath - Timeframe 1D and 1WIndicator Overview

The Pi Cycle Top Indicator has historically been effective in picking out the timing of market cycle highs within 3 days.

It uses the 111 day moving average (111DMA) and a newly created multiple of the 350 day moving average, the 350DMA x 2.

Note: The multiple is of the price values of the 350DMA, not the number of days.

For the past three market cycles, when the 111DMA moves up and crosses the 350DMA x 2 we see that it coincides with the price of Bitcoin peaking.

It is also interesting to note that 350 / 111 is 3.153, which is very close to Pi = 3.142. In fact, it is the closest we can get to Pi when dividing 350 by another whole number.

It once again demonstrates the cyclical nature of Bitcoin price action over long time frames. However, in this instance, it does so with a high degree of accuracy over Bitcoin's adoption phase of growth.

Bitcoin Price Prediction Using This Tool

The Pi Cycle Top Indicator forecasts the cycle top of Bitcoin’s market cycles. It attempts to predict the point where Bitcoin price will peak before pulling back. It does this on major high time frames and has picked the absolute tops of Bitcoin’s major price moves throughout most of its history.

How It Can Be Used

Pi Cycle Top is useful to indicate when the market is very overheated. So overheated that the shorter-term moving average, which is the 111-day moving average, has reached an x2 multiple of the 350-day moving average. Historically, it has proved advantageous to sell Bitcoin around this time in Bitcoin's price cycles.

It is also worth noting that this indicator has worked during Bitcoin's adoption growth phase, the first 15 years or so of Bitcoin's life. With the launch of Bitcoin ETF's and Bitcoin's increased integration into the global financial system, this indicator may cease to be relevant at some point in this new market structure.

Momentum Alligator 4h Bitcoin StrategyOverview

The Momentum Alligator 4h Bitcoin Strategy is a trend-following trading system that operates on dual time frames. It utilizes the 1D Williams Alligator indicator to identify the prevailing major price trend and seeks trading opportunities on the 4-hour (4h) time frame when the momentum is turning up. The strategy is designed to close trades if the trend fails to develop or holding position if price continues increasing without any significant correction. Note that this strategy is specifically tailored for the 4-hour time frame.

Unique Features

2-layers market noise filtering system: Trades are only initiated in the direction of the 1D trend, determined by the Williams Alligator indicator. This higher time frame confirmation filters out minor trade signals, focusing on more substantial opportunities. At the same time, strategy has additional filter on 4h time frame with Awesome Oscillator which is showing the current price momentum.

Flexible Risk Management: The strategy exclusively opens long positions, resulting in fewer trades during bear markets. It incorporates a dynamic stop-loss mechanism, which can either follow the jaw line of the 4h Alligator or a user-defined fixed stop-loss. This flexibility helps manage risk and avoid non-trending markets.

Methodology

The strategy initiates a long position when the d-line of Stochastic RSI crosses up it's k-line. It means that there is a high probability that price momentum reversed from down to up. To avoid overtrading in potentially choppy markets, it skips the next two trades following a winning trade, anticipating sideways movement after a significant price surge.

This strategy has two layers trades filtering system: 4h and 1D time frames. The first one is awesome oscillator. It shall be increasing and value has to be higher than it's 5-period SMA. This is an additional confirmation that long trade is opened in the direction of the current momentum. As it was mentioned above, all entry signals are validated against the 1D Williams Alligator indicator. A trade is only opened if the price is above all three lines of the 1D Alligator, ensuring alignment with the major trend.

A trade is closed if the price hits the 4h jaw line of the Alligator or reaches the user-defined stop-loss level.

Risk Management

The strategy employs a combined approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined stop-loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 2% drop from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Stochastic RSI on 4h time frame to open long trade when momentum started reversing to the upside. On the one hand, Stochastic RSI is one of the most sensitive indicator, which allows to react fast on the potential trend reversal. On the other hand, this indicator can be too sensitive and provide a lot of false trend changing signals. To eliminate this weakness we use two-layers trades filtering system.

The first layer is the 4h Awesome oscillator. This is less sensitive momentum indicator. Usually it starts increasing when price has already passed significant distance from the actual reversal point. The strategy opens long trade only is Awesome oscillator is increasing and above it's 5-period SMA. This approach increases the probability to filter the false signals during the choppy market or if the reversal is false.

The second layer filter is the Williams Alligator indicator on 1D time frame. The 1D Alligator serves as a filter for identifying the primary trend and increases probability to avoid the trades with low potential because trading against major trend usually is more risky. It's much better to catch the trend continuation than local bounce.

Last but not least feature of this strategy is close trades condition. It uses the flexible approach. First of all, user can set up the fixed stop-loss according to his own risk-tolerance, by default this value is 2% of price movement. It restricts the potential loss at the moment when trade has just been opened. Moreover strategy utilizes the 4h Williams Alligator's jaw line to exit the trade. If price fell below it trade is closed. This approach helps to not keep open trade if trend is not developing and hold it if price continues going up.

Backtest Results:

Operating window: Date range of backtests is 2021.01.01 - 2024.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -3.04%

Maximum Single Profit: +29.67%

Net Profit: +6228.01 USDT (+62.28%)

Total Trades: 118 (24.58% win rate)

Profit Factor: 1.71

Maximum Accumulated Loss: 1527.69 USDT (-11.52%)

Average Profit per Trade: 52.78 USDT (+0.89%)

Average Trade Duration: 60 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use:

Add the script to favorites for easy access.

Apply to the 4h timeframe desired chart (optimal performance observed on the BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Bitcoin Momentum StrategyThis is a very simple long-only strategy I've used since December 2022 to manage my Bitcoin position.

I'm sharing it as an open-source script for other traders to learn from the code and adapt it to their liking if they find the system concept interesting.

General Overview

Always do your own research and backtesting - this script is not intended to be traded blindly (no script should be) and I've done limited testing on other markets beyond Ethereum and BTC, it's just a template to tweak and play with and make into one's own.

The results shown in the strategy tester are from Bitcoin's inception so as to get a large sample size of trades, and potential returns have diminished significantly as BTC has grown to become a mega cap asset, but the script includes a date filter for backtesting and it has still performed solidly in recent years (speaking from personal experience using it myself - DYOR with the date filter).

The main advantage of this system in my opinion is in limiting the max drawdown significantly versus buy & hodl. Theoretically much better returns can be made by just holding, but that's also a good way to lose 70%+ of your capital in the inevitable bear markets (also speaking from experience).

In saying all of that, the future is fundamentally unknowable and past results in no way guarantee future performance.

System Concept:

Capture as much Bitcoin upside volatility as possible while side-stepping downside volatility as quickly as possible.

The system uses a simple but clever momentum-style trailing stop technique I learned from one of my trading mentors who uses this approach on momentum/trend-following stock market systems.

Basically, the system "ratchets" up the stop-loss to be much tighter during high bearish volatility to protect open profits from downside moves, but loosens the stop loss during sustained bullish momentum to let the position ride.

It is invested most of the time, unless BTC is trading below its 20-week EMA in which case it stays in cash/USDT to avoid holding through bear markets. It only trades one position (no pyramiding) and does not trade short, but can easily be tweaked to do whatever you like if you know what you're doing in Pine.

Default parameters:

HTF: Weekly Chart

EMA: 20-Period

ATR: 5-period

Bar Lookback: 7

Entry Rule #1:

Bitcoin's current price must be trading above its higher-timeframe EMA (Weekly 20 EMA).

Entry Rule #2:

Bitcoin must not be in 'caution' condition (no large bearish volatility swings recently).

Enter at next bar's open if conditions are met and we are not already involved in a trade.

"Caution" Condition:

Defined as true if BTC's recent 7-bar swing high minus current bar's low is > 1.5x ATR, or Daily close < Daily 20-EMA.

Trailing Stop:

Stop is trailed 1 ATR from recent swing high, or 20% of ATR if in caution condition (ie. 0.2 ATR).

Exit on next bar open upon a close below stop loss.

I typically use a limit order to open & exit trades as close to the open price as possible to reduce slippage, but the strategy script uses market orders.

I've never had any issues getting filled on limit orders close to the market price with BTC on the Daily timeframe, but if the exchange has relatively low slippage I've found market orders work fine too without much impact on the results particularly since BTC has consistently remained above $20k and highly liquid.

Cost of Trading:

The script uses no leverage and a default total round-trip commission of 0.3% which is what I pay on my exchange based on their tier structure, but this can vary widely from exchange to exchange and higher commission fees will have a significantly negative impact on realized gains so make sure to always input the correct theoretical commission cost when backtesting any script.

Static slippage is difficult to estimate in the strategy tester given the wide range of prices & liquidity BTC has experienced over the years and it largely depends on position size, I set it to 150 points per buy or sell as BTC is currently very liquid on the exchange I trade and I use limit orders where possible to enter/exit positions as close as possible to the market's open price as it significantly limits my slippage.

But again, this can vary a lot from exchange to exchange (for better or worse) and if BTC volatility is high at the time of execution this can have a negative impact on slippage and therefore real performance, so make sure to adjust it according to your exchange's tendencies.

Tax considerations should also be made based on short-term trade frequency if crypto profits are treated as a CGT event in your region.

Summary:

A simple, but effective and fairly robust system that achieves the goals I set for it.

From my preliminary testing it appears it may also work on altcoins but it might need a bit of tweaking/loosening with the trailing stop distance as the default parameters are designed to work with Bitcoin which obviously behaves very differently to smaller cap assets.

Good luck out there!

Support and Resistance ZoneSupport and Resistance Zone Indicator :

Introduction :

The purpose of this indicator is to identify the chart symbol's main supports and resistances. It displays these key zones, which are very important psychological points for traders. Since support and resistance are not very precise levels, the indicator displays them as zones.

Pivots :

Pivots are a key concept in identifying support and resistance. The indicator uses two types of pivot:

Pivot high : This is a high point that has not been reached by a user-defined number of candles on either the left and right of this candle. The " left pivot leg " is the number of candles before this pivot point that have not reached the realized high, and the " right pivot leg " is the number of candles after this pivot point that have not reached this high. If these two conditions are met, the pivot point is considered a turning point, and resistance is probably the cause.

Pivot low : This is a low point that has not been reached by a user-defined number of candles on either the left or right. The " left pivot leg " is the number of candles before this pivot point that have not reached the candle low, and the " right pivot leg " is the number of candles after this pivot point that have not reached this low. If these two conditions are met, the pivot point is considered a turning point, and support is probably the cause.

Support/Resistance area :

If a pivot point has been identified, the indicator considers it a resistance if it's a pivot high, or a support if it's a pivot low. To define the support or resistance zone, we'll use the ATR (Average True Range), an indicator that measures asset volatility. We'll take the ATR of the candle for which the pivot was spotted, and use it as the width of the support or resistance zone. Thus the upper line of support/resistance is at pivot+atr/2 and the lower line is at pivot-atr/2 . The greater the volatility, the larger the zone.

New Support/Resistance :

If a new pivot has been identified, but the level of this pivot lies between the lower line and the upper line of the previous support or resistance, the indicator considers this to be the same support or resistance as before. In this case, no new support or resistance is created. The pivot must be outside the area of the previous support or resistance to be validated.

Anticipated Support/Resistance :

This indicator also allows early detection of support or resistance. To do this, the value of the right pivot legs will be shortened in order to find these areas more quickly. The support or resistance will then be considered anticipated and may disappear at any time if the high/low is reached. On the other hand, if the high/low is not reached, and a number of candles equal to the " Right Pivot Legs" parameter has elapsed since the detection of this anticipated support/resistance, it will be considered validated and will integrate the other supports/resistances of the chart.

Extended supports/resistances :

For a more optimal view, the indicator allows the user to choose the number of last support or resistance levels to be extended to the last candle. This must be specified in the indicator parameters.

Parameters :

Pivot Legs : Determine the left and right legs of the pivot i.e the number of candle before and after the pivot that doesn’t reach pivot point. The pivot is validated only if this two conditions are verified.

Extend Last Supports : Number of supports to extend to the last bar

Extend Last Resistances : Number of resistances to extend to the last bar

Show Support/Resistance Anticipated : If yes, will find anticipated support and resistance

Right Pivot Legs for Anticipation : Determine the right legs of pivots to find faster a support or a resistance.

Conclusion :

This indicator plot support and resistance zones based on pivot. The width of support and resistance zones are calculated with ATR. Possibility to find anticipated support and resistance in order to have more timeliness informations.

Enjoy the indicator and don’t forget to take the trade ;)

Relative Strength Scoring SystemRelative Strength Scoring System :

Important prerequisite :

This indicator can be loaded on any forex chart, i.e. a currency pair, but must not be loaded on any other asset due to certain market closures.

The chart timeframe must be less than or equal to the trading timeframe, which is the indicator's first parameter. A timeframe equal to that of the "Trading Timeframe" parameter is preferable.

Introduction :

This indicator measures the relative strength of a currency against all other currencies using spread formulas. It gives an indication of which currencies are bullish, neutral or bearish. The ultimate aim of this indicator is to find out which pair will generate a higher probability of gain than the others by pairing the most bullish pair with the most bearish pair.

Spread formulas :

To find the relative strength of a currency compared with others, we use the following spreads formulas :

USD = (FX:USDJPY/100+SAXO:USDEUR+FX:USDCHF+SAXO:USDGBP+FX:USDCAD+SAXO:USDAUD+FX_IDC:USDNZD)/7

JPY = (SAXO:JPYUSD/100+FX_IDC:JPYAUD/100+FX_IDC:JPYCAD/100+FX_IDC:JPYNZD/100+FX_IDC:JPYCHF/100+SAXO:JPYEUR/100+FX_IDC:JPYGBP/100)/7

CHF = (FX:CHFJPY/100+SAXO:CHFUSD+SAXO:CHFEUR+FX_IDC:CHFGBP+FX_IDC:CHFCAD+SAXO:CHFAUD+FX_IDC:CHFNZD)/7

EUR = (FX:EURJPY/100+FX:EURUSD+FX:EURCHF+FX:EURGBP+FX:EURCAD+FX:EURAUD+FX:EURNZD)/7

GBP = (FX:GBPJPY/100+FX:GBPUSD+FX:GBPCHF+SAXO:GBPEUR+FX:GBPCAD+FX:GBPAUD+FX:GBPNZD)/7

CAD = (FX:CADJPY/100+SAXO:CADUSD+FX:CADCHF+FX_IDC:CADGBP+SAXO:CADEUR+FX_IDC:CADAUD+FX_IDC:CADNZD)/7

AUD = (FX:AUDJPY/100+FX:AUDUSD+FX:AUDCHF+SAXO:AUDGBP+FX:AUDCAD+SAXO:AUDEUR+FX:AUDNZD)/7

NZD = (FX:NZDJPY/100+FX:NZDUSD+FX:NZDCHF+SAXO:NZDGBP+FX:NZDCAD+SAXO:NZDAUD+SAXO:NZDEUR)/7

CRYPTO = (BITSTAMP:BTCUSD+BITSTAMP:ETHUSD+BITSTAMP:LTCUSD+BITSTAMP:BCHUSD)/4

Timeframes :

As mentioned in the prerequisites, the chart timeframe must not be greater than the trading timeframe. The latter corresponds to the timeframe chosen by the trader to enter a position, and is the indicator's first parameter. Once this has been chosen, the algorithm selects the timeframes of the "Trend" and "Velocity" charts. Here's how it allocates them :

Trading TF => ("Velocity TF", "Trend TF")

"5min" => ("15min ", "60min")

"15min" => ("60min ", "4h")

"30min" => ("2h ", "8h")

"60min" => ("4h ", "12h")

"4h" => ("12h", "1D")

"6h" => ("1D", "3D")

"8h" => ("1D", "4D")

"12h" => ("2D", "1W")

"1D" => ("3D", "1W")

Trend Scoring System :

When the timeframe of the trend graph has been allocated, the algorithm will establish this graph's score using three criteria :

Trend chart pivot points: if the last two pivots, high and low, are increasing, the score is 1; if they are decreasing, the score is -1; else the score is 0.

SMA: if its slope is increasing with a candle strictly above the SMA value, the score is 1; if its slope is decreasing with a candle strictly below it, the score is -1; otherwise, it is 0.

MACD: if the MACD is positive, the score is 1, if it is negative, the score is -1; else it's 0.

We then sum the scores of these three criteria to find the trend score.

Velocity Scoring System :

In the same way, we analyze the score of the "velocity" graph with its corresponding timeframe using three criteria :

The EMA: if its slope is increasing with a candle strictly above the EMA value, the score is 1; if its slope is decreasing with a candle strictly below it, the score is -1; otherwise, it is 0.

The RSI: if the RSI's EMA has an increasing slope with an RSI strictly greater than the value of this EMA, the score is 1; and if the RSI's EMA has a decreasing slope with an RSI strictly less than this EMA, the score is -1; otherwise it is 0.

SAR parabolic: if the SAR is below the price, the score is 1; if it is above the price, the score is -1.

We then sum the scores of these three criteria to find the velocity score.

Relative Strength Scoring System :

Once the trend score and velocity score have been calculated, we determine the relative strength score of each currency using the following algorithm :

If trend score >=2 and velocity score >=2, the currency is bullish.

If trend score <=2 and velocity score <=2, currency is bearish

If (trendScore>=2 or velocityScore>=2) and (trendScore=1 or velocityScore=1) the currency is not yet bullish

If (trendScore<=2 or velocityScore<=2) and (trendScore=-1 or velocityScore=-1) the currency is not yet bearish.

Otherwise the currency is neutral

Parameters :

Trading Timeframe: the trading timeframe chosen by the trader for which he makes his position entry and exit decisions. Default is 1h

Pivot Legs: Parameter used for the chart "Trend" setting the pivot strength to the right and left of high/low. Default is 2

SMA Length: SMA length of the chart "Trend". Default is 20

MACD Fast Length: Length of the MACD fast SMA calculated on the chart "Trend". Default is 12

MACD Slow Length: Length of the MACD slow SMA calculated on the chart "Trend". Default is 26

MACD Signal Length: Length of the MACD signal SMA calculated on the chart "Trend". Default is 9

EMA Length: EMA length of the "Velocity" graph. Default is 13

RSI Length: RSI length of the "Velocity" graph. Default is 14

RSI EMA Length: Length of the RSI EMA. Default is 9

Parabolic SAR Start: Start of the SAR parabola in the "Velocity" graph. Default is 0.02

Parabolic SAR Increment: Increment of the SAR parabola in the "Velocity" graph. Default is 0.02

Parabolic SAR Max: Maximum of the SAR parabola in the "Velocity" graph. Default is 0.2

Conclusion :

This indicator has been designed to determine the relative strength of the major currencies against each other. The aim is to know which pair to trade at the right time in order to maximize the probability of a successful trade. For example, if the USD is bullish and the NZD bearish, we'll short the NZDUSD pair.

Enjoy this indicator and don't forget to take the trade ;)

MACD_RSI_trend_followingINFO:

This indicator can be used to build-up a strategy for trading of assets which are currently in trending phase.

My preference is to use it on slowly moving assets like GOLD and on higher timeframes, but practice may show that we find more usefull cases.

This script uses two indicators - MACD and RSI, as the timeframe that those are extracted for is configurable (defaults with the Chart TF, but can be any other selected by the user).

The strategy has the following simple idea - buy if any if the conditions below is true:

The selected TF MACD line crosses above the signal line and the TF RSI is above the user selected trigger value

The selected TF MACD line is above the signal line and the TF RSI crosses above the user selected trigger value

Once we're in position we wait for the selected TF MACD line to cross below the signal line, and then we set a SL at the low of that bar

DETAILS and USAGE:

In the current implementation I find two possible use cases for the indicator:

as a stand-alone indicator on the chart which can also fire alerts that can help to determine if we want to manually enter/exit trades based on them

can be used to connect to the Signal input of the TTS (TempalteTradingStrategy) by jason5480 in order to backtest it, thus effectively turning it into a strategy (instructions below in TTS CONNECTIVITY section)

In the example below we see a position opened at the bar after the buy indicator from the script has been triggered, and then later after the SL indicator from the script has been triggered a SL has been set on the lower wick of the closing candle, and the position eventually got closed once the price hit that level. Note that most of the drawing on the example snapshot below are from the TTS indicator following the buy/sell/SL conditions themseves:

Trading period can be selected from the indicator itself to limit to more interesting periods.

Arrow indications are drawn on the chart to indicate the trading conditions met in the script - green arrow for a buy signal indication and orange for LTF crossunder to indicate setting of SL.

SETTINGS:

Leaving all of the settings as in vanilla use case, as both the MACD and RSI indicator's settings follow the default ones for the stand-alone indicators themselves.

The start-end date is a time filter that can be extermely usefull when backtesting different time periods.

Pesonal preference is using the script on a D/W timeframe, while the indicator is configured to use Monthly chart.

The default value of the RSI filter is left to 50, which can be changed. I.e. if the RSI is above 50 we have a regime filter based on the MACD criteria.

EXTERNAL LIBRARIES:

The script uses a couple of external libraries:

HeWhoMustNotBeNamed/enhanced_ta/14 - collection of TA indicators

jason5480/tts_convention/3 - more details about the Template Trading Strategy below

I would like to highly appreciate and credit the work of both HeWhoMustNotBeNamed and jason5480 for providing them to the community.

TTS SETTINGS (NEEDED IF USED TO BACKTEST WITH TTS):

The TempalteTradingStrategy is a strategy script developed in Pine by jason5480, which I recommend for quick turn-around of testing different ideas on a proven and tested framework

I cannot give enough credit to the developer for the efforts put in building of the infrastructure, so I advice everyone that wants to use it first to get familiar with the concept and by checking

by checking jason5480's profile www.tradingview.com

The TTS itself is extremely functional and have a lot of properties, so its functionality is beyond the scope of the current script -

Again, I strongly recommend to be thoroughly epxlored by everyone that plans on using it.

In the nutshell it is a script that can be feed with buy/sell signals from an external indicator script and based on many configuration options it can determine how to execute the trades.

The TTS has many settings that can be applied, so below I will cover only the ones that differ from the default ones, at least according to my testing - do your own research, you may find something even better :)

The current/latest version that I've been using as of writing and testing this script is TTSv48

Settings which differ from the default ones:

from - False (time filter is from the indicator script itself)

Deal Conditions Mode - External (take enter/exit conditions from an external script)

🔌Signal 🛈➡ - MACD_RSI_trend_following: 🔌Signal to TTSv48 (this is the output from the indicator script, according to the TTS convention)

Sat/Sun - true (for crypto, in order to trade 24/7)

Order Type - STOP (perform stop order)

Distance Method - HHLL (HigherHighLowerLow - in order to set the SL according to the strategy definition from above)

The next are just personal preferenes, you can feel free to experiment according to your trading style

Take Profit Targets - 0 (either 100% in or out, no incremental stepping in or out of positions)

Dist Mul|Len Long/Short- 10 (make sure that we don't close on profitable trades by any reason)

Quantity Method - EQUITY (personal backtesting preference is to consider each backtest as a separate portfolio, so determine the position size by 100% of the allocated equity size)

Equity % - 100 (note above)

The Ultimate Buy and Sell IndicatorThis indicator should be used in conjunction with a solid risk management strategy that does not over-leverage positions and uses stop-losses. You can not rely 100% on the signals provided by this indicator (or any other for that matter).

With that said, this indicator can provide some excellent signals.

It has been designed with a large number of customization options intended for advanced traders, but you do not HAVE to be an advanced user to simply use the indicator. I have tried to make it easy to understand, and this section will provide you with a better understanding of how to use it.

NOTE:

While NOT REQUIRED, I would recommend also finding my indicator called, "Ultimate RSI", which is designed to work together with this indicator (visually). They both contain the same settings and allow you to visualize changes made in this indicator that can not be displayed on the main chart.

This indicator creates it's own candles(bars), so you have to go into your main settings and turn off the "body, border and wick" color settings. Using a dark background is also recommended.

How does it work?

The indicator mainly relies on the RSI indicator with Bollinger Bands for signals. (Though not entirely)

First, there are something that I call "Watch Signals", which are various Bollinger Band crossing events. This could be the price crossing Bollinger Bands or the RSI crossing Bollinger Bands.

There are separate watch signals for buys and sells. Buy watch signals are colored orange to match the BUY signal candle color and Fuchsia (kind of a bright purple) to match SELL signal candles.

In order for most buy or sell signals to be created, there must first be a watch signal. There is a lookback period (or length) for watch signals to be used, and after that many candles (bars) have passed, they will be ignored. You can set a length to look back as well as a time to wait before creating any.

What this means is that if there has previously been (for instance) a sell signal. You can tell it to wait 10 bars before creating any buy watch signals. You can then also tell it that it should look back 10 bars from the current one in order to find any buy watch signals. This means that if you had it set up that way 10 to wait and 10 to validate, it would start allowing buy watch signals 11 bars after a sell, and then once you hit 20 bars, it will start leaving a gap (invisible to you) as the 10 bar lookback period starts moving forward with each new bar. This is useful in order to keep signals more spaced apart as some bad signals come quickly after another one.

Example: You may get a sell signal where the Bollinger bands are tight, then the price easily drops down into the lower band creating a buy watch signal, then you get a "fake" or short pump up and it says buy, but then drops dramatically afterwards. The wait period can ensure that the sell stays in effect longer before a buy is considered by blocking any buy watch signals for a period of time.

After you get a watch signal, the system then looks for various other things to happen to create buy or sell signals. This could be the RSI crossing the (slow) RSI Basis line (from its Bollinger bands), it could be the price crossing its basis line, it could be MACD crosses, it could even be RSI crossing certain levels. All of these are options. If you like the MACD strategy and want it to give you buy and sell signals from just MACD crosses, simply select that option for signals.

It is also able to use the first of any of the options that takes place.

I included an option to force alternating buy and sell signals, rather than showing groups of, or subsequent buy, buy, buy signals, for instance.

Moving on....

You can change the moving average that is used to calculate the RSI. The standard moving average for RSI is the RMA (aka SWMA). Changes to this can dramatically change your signals. You also have the option to change the moving average type used in the Bollinger bands calculation. You can change the length of these as well. The same goes for the Bollinger bands over the Price chart. I added an ATR option for the RSI Bollinger bands to play with, as well. You are able to adjust the standard deviation (multiplier) of the bands as well, which will of course affect the signals.

The ways you can play with signals are nearly infinite, so have fun figuring it out.

The indicator allows for moving averages to be shown as well, with a variety of types to choose from. The standard numbers are 5, 10, 20, 50, 100 and 200, with the addition of a custom moving average of your choice. You can also change the color of this one. You can choose to show them all or any of them you want to show, in any combination, although the TYPE of moving average (SMA, EMA, WMA, etc.) will apply to all of them.

You may also notice the Bollinger Bands over the Price are colored, and become more or less transparent.

The color is derived from the trend of the RSI or the RSI basis (your choice). It looks back at the value however many bars you want and compares the values and that's how it determines if it is trending up or down. Since RSI is a directional momentum indicator, this can be quite useful. If you see the bands are getting darker, this will explain why.

The indicator has a lookback period for determining the widest the bands (which measure volatility) have been over that period of time. This is the baseline. It then will make the bands disappear (by making them more transparent) if the volatility is low. This indicates that a change in volatility is coming and that price isn't really changing much compared to the past (default 500) bars. If they become bright, this is because price has started trending in a direction and volatility is increasing.

I should also note that the candles are colored based on RSI levels.

If you use the Ultimate Companion indicator, you will be able to see the RSI levels (zones) that the colors are based on. As RSI moves into a new range, the candle color will change.

I have created a yellow zone where the candles turn yellow. This is when RSI is between (default) 45 and 55, indicating there is basically no momentum and price is going sideways. This is a good place to get trapped in bad trades, and there is a Yellow RSI Filter to block signals in this area to keep you from entering bad trades.

Green candles indicate values over 55 (getting brighter as RSI rises) and red candles are RSI values under 45 (getting brighter as RSI values get lower). If you see white, this means RSI is either over 80 or under 20. A sharp reversal is almost always imminent at this stage.

When we talk about Buy and Sell Signals, they draw a green or red triangle and it literally says BUY or SELL. There is an option to color the background for added visibility. These signals do not "repaint", what this means is that they can be late. To account for this, I have included a background color that will flash as a warning that a buy or sell could be imminent, although it may fail to break through and set a buy or sell signal. This is simply an advanced warning. The reason is that sometimes a candle may be very large and you won't be told to buy or sell during the candle until the move is completely over and now you're getting in on the next one. That's not a great feeling, so I made it repaint the background color and not repaint the completed signal. You get the best of both worlds.

This indicator also uses complex logic to handle things.

When there is a buy signal, it enters into a state of having been bought, or a "bought state". The same for sells. If Force alternating signals is off, you could have more than one buy in a bought state, or more than one sell in a sell state. There is an option to color the background green during the full duration of a bought state, or red during the full duration of a sold state.

I have added divergence.

This shows that the lows or highs of RSI and PRICE are different. If RSI is making higher highs but the price is not, then the price is likely to follow this bullish divergence, if the opposite happens, it's bearish. It will draw a line on the chart connecting the highs and lows and call it bearish or bullish. You can adjust this as well.

I have an RSI High/Low filter. If the RSI basis (or average) is very high or low, you can block signal from this area since the price is likely to continue in that direction before actually reversing.

You can change the settings of the MACD if you choose to use it for signals, and if you want to see it, you'll have to run that indicator below the chart and match the settings to see what is going on, just like the RSI.

Going back to Watch Signals. You can also choose to require more than one watch signal if you choose. You can skip watch signals, so it will ignore the first or second one, whatever you want to do. You can color the background to show you where watch signals have been skipped.

Regarding the wait period for creating watch signals after a sell or after a buy, you can also color the background to see where these were blocked by the wait period.

Lastly you can choose which type of watch signals to use, or keep them from being shown on the chart. This allows you to study the history of how the asset you are trading behaves and customize the behavior of signals based on your study of it.

Everything in the settings area has tooltips, which will explain what that thing does to help you along this journey.

I hope this indicator (and perhaps Ultimate RSI alongside this) will help you take your trading to the next level.

Renko StrategyRENKO STRATEGY

CAUTION : This strategy must be applied to a candlestick chart (not a Renko chart).

INTRODUCTION :

The Traditional Renko chart has been reproduced and is plotted according to the evolution of the price. It will enable us to receive buy or sell signals and follow major trends. This is a medium/long term strategy and depends a lot on the box size chosen in the parameters. There's also a money management method allowing us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

RENKO CHART :

Renko chart construction methodology :

The user must first choose the box size. The minimum is 0.00001 and there is no maximum. The default is 10. The user must then choose the source that will define the data on which the calculations will be based (high, low, open, close). By default, close is selected. The first candle on the chart is used to draw the first box with its high and low.

Each time the price changes by the amount of the box size relative to the high or low of the last box, a new box is added above or below the previous one. If price variations are less than the box size, the same box is added next to the previous one. If price variations are N (integer number) times greater than box size, N boxes are added above or below the previous one. Each box added above the previous one is a green box, while each box added below the previous one is a red box.

Conditions for drawing a green box above the previous one :

(source - high_of_the_last_box) / box_size > 1

Condition for drawing a red box below the previous one :

(low_of_the_last_box - source) / box_size > 1

If neither condition is triggered, the same box is drawn next to the previous one.

Example :

The last candle has drawn a box with low 12 and high 14. The box size is therefore 2. The strategy will look at the value of the close each time a candle ends. The current candle closes with a close equal to 15.5. As the variation from the previous high is only 1.5 (which is less than the box size), the same box is added next to the previous one. The next candle closes at 16.2. The price variation is therefore 2.2 compared with the previous high. We can now add a new green box just above the previous one, with a low of 14 and a high of 16. The same process applies if the candle's close is at least one box size below the low of the last box. In this case, a new red box is placed below the previous one.

PARAMETERS :

Source : Allows you to specify which data will be taken into account by the strategy when performing calculations. The default is close.

Box size : Size of Renko graph boxes. This is a very important parameter to choose carefully, as it has a strong impact on the strategy's performance. Defaults to 10.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. The default is 400, meaning that for each $400 gain or loss, the order size is increased or decreased by a user-selected amount.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test all possible box sizes to find out which one generates the highest return on BITSTAMP:LTCUSD while limiting the drawdown. This strategy is the most optimal with a box size equal to 5.08 in 8h timeframe.

BUY AND SHORT SIGNALS :

As the aim of this strategy is to follow major trends based on price movements, we need to be on the right side of price fluctuation. We trade every box reversal, i.e. we are LONG when the boxes are green indicating an uptrend and SHORT when they are red indicating a downtrend.

RISK MANAGEMENT :

This strategy can incur losses. The size of the box is decisive, as it is used to plot the RENKO chart and thus trigger buy or sell signals. It's also what allows us to manage risk. For every trade, we risk a maximum amount equal to 2 times the size of the box, i.e. :(5.08*2*nb_contract)/trade_value.

MONEY MANAGEMENT :

The fixed ratio method has been used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy not only increases our performance, but also our drawdown.

Enjoy the strategy and don't forget to take the trade :)

Statistical Package for the Trading Sciences [SS]

This is SPTS.

It stands for Statistical Package for the Trading Sciences.

Its a play on SPSS (Statistical Package for the Social Sciences) by IBM (software that, prior to Pinescript, I would use on a daily basis for trading).

Let's preface this indicator first:

This isn't so much an indicator as it is a project. A passion project really.

This has been in the works for months and I still feel like its incomplete. But the plan here is to continue to add functionality to it and actually have the Pinecoding and Tradingview community contribute to it.

As a math based trader, I relied on Excel, SPSS and R constantly to plan my trades. Since learning a functional amount of Pinescript and coding a lot of what I do and what I relied on SPSS, Excel and R for, I use it perhaps maybe a few times a week.

This indicator, or package, has some of the key things I used Excel and SPSS for on a daily and weekly basis. This also adds a lot of, I would say, fairly complex math functionality to Pinescript. Because this is adding functionality not necessarily native to Pinescript, I have placed most, if not all, of the functionality into actual exportable functions. I have also set it up as a kind of library, with explanations and tips on how other coders can take these functions and implement them into other scripts.

The hope here is that other coders will take it, build upon it, improve it and hopefully share additional functionality that can be added into this package. Hence why I call it a project. Okay, let's get into an overview:

Current Functions of SPTS:

SPTS currently has the following functionality (further explanations will be offered below):

Ability to Perform a One-Tailed, Two-Tailed and Paired Sample T-Test, with corresponding P value.

Standard Pearson Correlation (with functionality to be able to calculate the Pearson Correlation between 2 arrays).

Quadratic (or Curvlinear) correlation assessments.

R squared Assessments.

Standard Linear Regression.

Multiple Regression of 2 independent variables.

Tests of Normality (with Kurtosis and Skewness) and recognition of up to 7 Different Distributions.

ARIMA Modeller (Sort of, more details below)

Okay, so let's go over each of them!

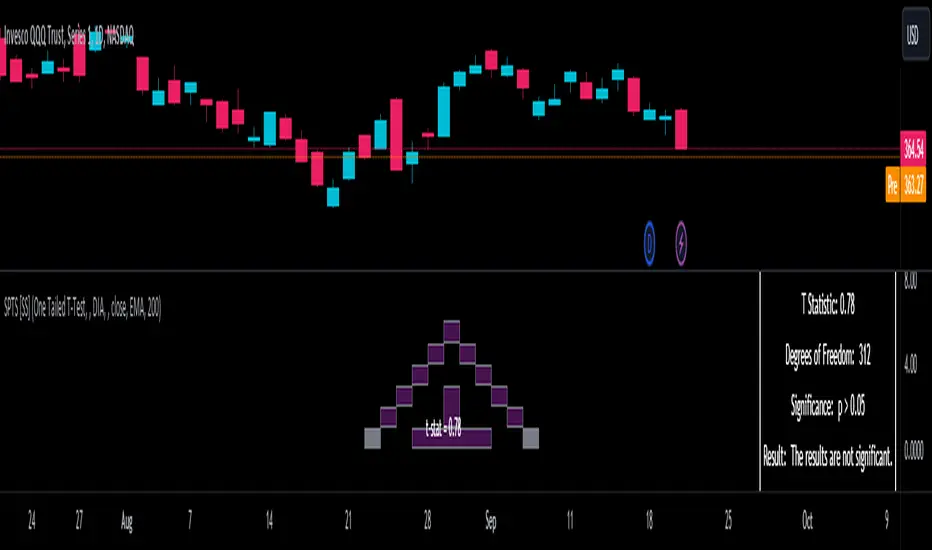

T-Tests

So traditionally, most correlation assessments on Pinescript are done with a generic Pearson Correlation using the "ta.correlation" argument. However, this is not always the best test to be used for correlations and determine effects. One approach to correlation assessments used frequently in economics is the T-Test assessment.

The t-test is a statistical hypothesis test used to determine if there is a significant difference between the means of two groups. It assesses whether the sample means are likely to have come from populations with the same mean. The test produces a t-statistic, which is then compared to a critical value from the t-distribution to determine statistical significance. Lower p-values indicate stronger evidence against the null hypothesis of equal means.

A significant t-test result, indicating the rejection of the null hypothesis, suggests that there is statistical evidence to support that there is a significant difference between the means of the two groups being compared. In practical terms, it means that the observed difference in sample means is unlikely to have occurred by random chance alone. Researchers typically interpret this as evidence that there is a real, meaningful difference between the groups being studied.

Some uses of the T-Test in finance include:

Risk Assessment: The t-test can be used to compare the risk profiles of different financial assets or portfolios. It helps investors assess whether the differences in returns or volatility are statistically significant.

Pairs Trading: Traders often apply the t-test when engaging in pairs trading, a strategy that involves trading two correlated securities. It helps determine when the price spread between the two assets is statistically significant and may revert to the mean.

Volatility Analysis: Traders and risk managers use t-tests to compare the volatility of different assets or portfolios, assessing whether one is significantly more or less volatile than another.

Market Efficiency Tests: Financial researchers use t-tests to test the Efficient Market Hypothesis by assessing whether stock price movements follow a random walk or if there are statistically significant deviations from it.

Value at Risk (VaR) Calculation: Risk managers use t-tests to calculate VaR, a measure of potential losses in a portfolio. It helps assess whether a portfolio's value is likely to fall below a certain threshold.

There are many other applications, but these are a few of the highlights. SPTS permits 3 different types of T-Test analyses, these being the One Tailed T-Test (if you want to test a single direction), two tailed T-Test (if you are unsure of which direction is significant) and a paired sample t-test.

Which T is the Right T?

Generally, a one-tailed t-test is used to determine if a sample mean is significantly greater than or less than a specified population mean, whereas a two-tailed t-test assesses if the sample mean is significantly different (either greater or less) from the population mean. In contrast, a paired sample t-test compares two sets of paired observations (e.g., before and after treatment) to assess if there's a significant difference in their means, typically used when the data points in each pair are related or dependent.

So which do you use? Well, it depends on what you want to know. As a general rule a one tailed t-test is sufficient and will help you pinpoint directionality of the relationship (that one ticker or economic indicator has a significant affect on another in a linear way).

A two tailed is more broad and looks for significance in either direction.

A paired sample t-test usually looks at identical groups to see if one group has a statistically different outcome. This is usually used in clinical trials to compare treatment interventions in identical groups. It's use in finance is somewhat limited, but it is invaluable when you want to compare equities that track the same thing (for example SPX vs SPY vs ES1!) or you want to test a hypothesis about an index and a leveraged share (for example, the relationship between FNGU and, say, MSFT or NVDA).

Statistical Significance

In general, with a t-test you would need to reference a T-Table to determine the statistical significance of the degree of Freedom and the T-Statistic.

However, because I wanted Pinescript to full fledge replace SPSS and Excel, I went ahead and threw the T-Table into an array, so that Pinescript can make the determination itself of the actual P value for a t-test, no cross referencing required :-).

Left tail (Significant):

Both tails (Significant):

Distributed throughout (insignificant):

As you can see in the images above, the t-test will also display a bell-curve analysis of where the significance falls (left tail, both tails or insignificant, distributed throughout).

That said, I have not included this function for the paired sample t-test because that is a bit more nuanced. But for the one and two tailed assessments, the indicator will provide you the P value.

Pearson Correlation Assessment

I don't think I need to go into too much detail on this one.

I have put in functionality to quickly calculate the Pearson Correlation of two array's, which is not currently possible with the "ta.correlation" function.

Quadratic (Curvlinear) Correlation

Not everything in life is linear, sometimes things are curved!

The Pearson Correlation is great for linear assessments, but tends to under-estimate the degree of the relationship in curved relationships. There currently is no native function to t-test for quadratic/curvlinear relationships, so I went ahead and created one.

You can see an example of how Quadratic and Pearson Correlations vary when you look at CME_MINI:ES1! against AMEX:DIA for the past 10 ish months:

Pearson Correlation:

Quadratic Correlation:

One or the other is not always the best, so it is important to check both!

R-Squared Assessments:

The R-squared value, or the square of the Pearson correlation coefficient (r), is used to measure the proportion of variance in one variable that can be explained by the linear relationship with another variable. It represents the goodness-of-fit of a linear regression model with a single predictor variable.

R-Squared is offered in 3 separate forms within this indicator. First, there is the generic R squared which is taking the square root of a Pearson Correlation assessment to assess the variance.

The next is the R-Squared which is calculated from an actual linear regression model done within the indicator.

The first is the R-Squared which is calculated from a multiple regression model done within the indicator.

Regardless of which R-Squared value you are using, the meaning is the same. R-Square assesses the variance between the variables under assessment and can offer an insight into the goodness of fit and the ability of the model to account for the degree of variance.

Here is the R Squared assessment of the SPX against the US Money Supply:

Standard Linear Regression

The indicator contains the ability to do a standard linear regression model. You can convert one ticker or economic indicator into a stock, ticker or other economic indicator. The indicator will provide you with all of the expected information from a linear regression model, including the coefficients, intercept, error assessments, correlation and R2 value.

Here is AAPL and MSFT as an example:

Multiple Regression

Oh man, this was something I really wanted in Pinescript, and now we have it!

I have created a function for multiple regression, which, if you export the function, will permit you to perform multiple regression on any variables available in Pinescript!

Using this functionality in the indicator, you will need to select 2, dependent variables and a single independent variable.

Here is an example of multiple regression for NASDAQ:AAPL using NASDAQ:MSFT and NASDAQ:NVDA :

And an example of SPX using the US Money Supply (M2) and AMEX:GLD :

Tests of Normality:

Many indicators perform a lot of functions on the assumption of normality, yet there are no indicators that actually test that assumption!

So, I have inputted a function to assess for normality. It uses the Kurtosis and Skewness to determine up to 7 different distribution types and it will explain the implication of the distribution. Here is an example of SP:SPX on the Monthly Perspective since 2010:

And NYSE:BA since the 60s:

And NVDA since 2015:

ARIMA Modeller

Okay, so let me disclose, this isn't a full fledge ARIMA modeller. I took some shortcuts.

True ARIMA modelling would involve decomposing the seasonality from the trend. I omitted this step for simplicity sake. Instead, you can select between using an EMA or SMA based approach, and it will perform an autogressive type analysis on the EMA or SMA.

I have tested it on lookback with results provided by SPSS and this actually works better than SPSS' ARIMA function. So I am actually kind of impressed.

You will need to input your parameters for the ARIMA model, I usually would do a 14, 21 and 50 day EMA of the close price, and it will forecast out that range over the length of the EMA.

So for example, if you select the EMA 50 on the daily, it will plot out the forecast for the next 50 days based on an autoregressive model created on the EMA 50. Here is how it looks on AMEX:SPY :

You can also elect to plot the upper and lower confidence bands:

Closing Remarks

So that is the indicator/package.

I do hope to continue expanding its functionality, but as of now, it does already have quite a lot of functionality.

I really hope you enjoy it and find it helpful. This. Has. Taken. AGES! No joke. Between referencing my old statistics textbooks, trying to remember how to calculate some of these things, and wanting to throw my computer against the wall because of errors in the code, this was a task, that's for sure. So I really hope you find some usefulness in it all and enjoy the ability to be able to do functions that previously could really only be done in external software.

As always, leave your comments, suggestions and feedback below!

Take care!

CNTLibraryLibrary "CNTLibrary"

Custom Functions To Help Code In Pinescript V5

Coded By Christian Nataliano

First Coded In 10/06/2023

Last Edited In 22/06/2023

Huge Shout Out To © ZenAndTheArtOfTrading and his ZenLibrary V5, Some Of The Custom Functions Were Heavily Inspired By Matt's Work & His Pine Script Mastery Course

Another Shout Out To The TradingView's Team Library ta V5

//====================================================================================================================================================

// Custom Indicator Functions

//====================================================================================================================================================

GetKAMA(KAMA_lenght, Fast_KAMA, Slow_KAMA)

Calculates An Adaptive Moving Average Based On Perry J Kaufman's Calculations

Parameters:

KAMA_lenght (int) : Is The KAMA Lenght

Fast_KAMA (int) : Is The KAMA's Fastes Moving Average

Slow_KAMA (int) : Is The KAMA's Slowest Moving Average

Returns: Float Of The KAMA's Current Calculations

GetMovingAverage(Source, Lenght, Type)

Get Custom Moving Averages Values

Parameters:

Source (float) : Of The Moving Average, Defval = close

Lenght (simple int) : Of The Moving Average, Defval = 50

Type (string) : Of The Moving Average, Defval = Exponential Moving Average

Returns: The Moving Average Calculation Based On Its Given Source, Lenght & Calculation Type (Please Call Function On Global Scope)

GetDecimals()

Calculates how many decimals are on the quote price of the current market © ZenAndTheArtOfTrading

Returns: The current decimal places on the market quote price

Truncate(number, decimalPlaces)

Truncates (cuts) excess decimal places © ZenAndTheArtOfTrading

Parameters:

number (float)

decimalPlaces (simple float)

Returns: The given number truncated to the given decimalPlaces

ToWhole(number)

Converts pips into whole numbers © ZenAndTheArtOfTrading

Parameters:

number (float)

Returns: The converted number

ToPips(number)

Converts whole numbers back into pips © ZenAndTheArtOfTrading

Parameters:

number (float)

Returns: The converted number

GetPctChange(value1, value2, lookback)

Gets the percentage change between 2 float values over a given lookback period © ZenAndTheArtOfTrading

Parameters:

value1 (float)

value2 (float)

lookback (int)

BarsAboveMA(lookback, ma)

Counts how many candles are above the MA © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are above the MA

BarsBelowMA(lookback, ma)

Counts how many candles are below the MA © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are below the EMA

BarsCrossedMA(lookback, ma)

Counts how many times the EMA was crossed recently © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many times price recently crossed the EMA

GetPullbackBarCount(lookback, direction)

Counts how many green & red bars have printed recently (ie. pullback count) © ZenAndTheArtOfTrading

Parameters:

lookback (int)

direction (int)

Returns: The bar count of how many candles have retraced over the given lookback & direction

GetSwingHigh(Lookback, SwingType)

Check If Price Has Made A Recent Swing High

Parameters:

Lookback (int) : Is For The Swing High Lookback Period, Defval = 7

SwingType (int) : Is For The Swing High Type Of Identification, Defval = 1

Returns: A Bool - True If Price Has Made A Recent Swing High

GetSwingLow(Lookback, SwingType)

Check If Price Has Made A Recent Swing Low

Parameters:

Lookback (int) : Is For The Swing Low Lookback Period, Defval = 7

SwingType (int) : Is For The Swing Low Type Of Identification, Defval = 1

Returns: A Bool - True If Price Has Made A Recent Swing Low

//====================================================================================================================================================

// Custom Risk Management Functions

//====================================================================================================================================================

CalculateStopLossLevel(OrderType, Entry, StopLoss)

Calculate StopLoss Level

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, Defval = na

StopLoss (float) : Is The Custom StopLoss Distance, Defval = 2x ATR Below Close

Returns: Float - The StopLoss Level In Actual Price As A

CalculateStopLossDistance(OrderType, Entry, StopLoss)

Calculate StopLoss Distance In Pips

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, NEED TO INPUT PARAM

StopLoss (float) : Level Based On Previous Calculation, NEED TO INPUT PARAM

Returns: Float - The StopLoss Value In Pips

CalculateTakeProfitLevel(OrderType, Entry, StopLossDistance, RiskReward)

Calculate TakeProfit Level

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, Defval = na

StopLossDistance (float)

RiskReward (float)

Returns: Float - The TakeProfit Level In Actual Price

CalculateTakeProfitDistance(OrderType, Entry, TakeProfit)

Get TakeProfit Distance In Pips

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, NEED TO INPUT PARAM

TakeProfit (float) : Level Based On Previous Calculation, NEED TO INPUT PARAM

Returns: Float - The TakeProfit Value In Pips

CalculateConversionCurrency(AccountCurrency, SymbolCurrency, BaseCurrency)

Get The Conversion Currecny Between Current Account Currency & Current Pair's Quoted Currency (FOR FOREX ONLY)

Parameters:

AccountCurrency (simple string) : Is For The Account Currency Used

SymbolCurrency (simple string) : Is For The Current Symbol Currency (Front Symbol)

BaseCurrency (simple string) : Is For The Current Symbol Base Currency (Back Symbol)

Returns: Tuple Of A Bollean (Convert The Currency ?) And A String (Converted Currency)

CalculateConversionRate(ConvertCurrency, ConversionRate)

Get The Conversion Rate Between Current Account Currency & Current Pair's Quoted Currency (FOR FOREX ONLY)

Parameters:

ConvertCurrency (bool) : Is To Check If The Current Symbol Needs To Be Converted Or Not

ConversionRate (float) : Is The Quoted Price Of The Conversion Currency (Input The request.security Function Here)

Returns: Float Price Of Conversion Rate (If In The Same Currency Than Return Value Will Be 1.0)

LotSize(LotSizeSimple, Balance, Risk, SLDistance, ConversionRate)

Get Current Lot Size

Parameters:

LotSizeSimple (bool) : Is To Toggle Lot Sizing Calculation (Simple Is Good Enough For Stocks & Crypto, Whilst Complex Is For Forex)

Balance (float) : Is For The Current Account Balance To Calculate The Lot Sizing Based Off

Risk (float) : Is For The Current Risk Per Trade To Calculate The Lot Sizing Based Off

SLDistance (float) : Is The Current Position StopLoss Distance From Its Entry Price

ConversionRate (float) : Is The Currency Conversion Rate (Used For Complex Lot Sizing Only)

Returns: Float - Position Size In Units

ToLots(Units)

Converts Units To Lots

Parameters:

Units (float) : Is For How Many Units Need To Be Converted Into Lots (Minimun 1000 Units)

Returns: Float - Position Size In Lots

ToUnits(Lots)

Converts Lots To Units

Parameters:

Lots (float) : Is For How Many Lots Need To Be Converted Into Units (Minimun 0.01 Units)

Returns: Int - Position Size In Units

ToLotsInUnits(Units)

Converts Units To Lots Than Back To Units

Parameters:

Units (float) : Is For How Many Units Need To Be Converted Into Lots (Minimun 1000 Units)

Returns: Float - Position Size In Lots That Were Rounded To Units

ATRTrail(OrderType, SourceType, ATRPeriod, ATRMultiplyer, SwingLookback)

Calculate ATR Trailing Stop

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

SourceType (int) : Is To Determine Where To Calculate The ATR Trailing From, Defval = close

ATRPeriod (simple int) : Is To Change Its ATR Period, Defval = 20

ATRMultiplyer (float) : Is To Change Its ATR Trailing Distance, Defval = 1

SwingLookback (int) : Is To Change Its Swing HiLo Lookback (Only From Source Type 5), Defval = 7

Returns: Float - Number Of The Current ATR Trailing

DangerZone(WinRate, AvgRRR, Filter)

Calculate Danger Zone Of A Given Strategy

Parameters:

WinRate (float) : Is The Strategy WinRate

AvgRRR (float) : Is The Strategy Avg RRR

Filter (float) : Is The Minimum Profit It Needs To Be Out Of BE Zone, Defval = 3

Returns: Int - Value, 1 If Out Of Danger Zone, 0 If BE, -1 If In Danger Zone

IsQuestionableTrades(TradeTP, TradeSL)

Checks For Questionable Trades (Which Are Trades That Its TP & SL Level Got Hit At The Same Candle)

Parameters:

TradeTP (float) : Is The Trade In Question Take Profit Level

TradeSL (float) : Is The Trade In Question Stop Loss Level

Returns: Bool - True If The Last Trade Was A "Questionable Trade"

//====================================================================================================================================================

// Custom Strategy Functions

//====================================================================================================================================================

OpenLong(EntryID, LotSize, LimitPrice, StopPrice, Comment, CommentValue)

Open A Long Order Based On The Given Params

Parameters:

EntryID (string) : Is The Trade Entry ID, Defval = "Long"

LotSize (float) : Is The Lot Size Of The Trade, Defval = 1

LimitPrice (float) : Is The Limit Order Price To Set The Order At, Defval = Na / Market Order Execution

StopPrice (float) : Is The Stop Order Price To Set The Order At, Defval = Na / Market Order Execution

Comment (string) : Is The Order Comment, Defval = Long Entry Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

OpenShort(EntryID, LotSize, LimitPrice, StopPrice, Comment, CommentValue)

Open A Short Order Based On The Given Params

Parameters:

EntryID (string) : Is The Trade Entry ID, Defval = "Short"

LotSize (float) : Is The Lot Size Of The Trade, Defval = 1

LimitPrice (float) : Is The Limit Order Price To Set The Order At, Defval = Na / Market Order Execution

StopPrice (float) : Is The Stop Order Price To Set The Order At, Defval = Na / Market Order Execution

Comment (string) : Is The Order Comment, Defval = Short Entry Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

TP_SLExit(FromID, TPLevel, SLLevel, PercentageClose, Comment, CommentValue)

Exits Based On Predetermined TP & SL Levels

Parameters:

FromID (string) : Is The Trade ID That The TP & SL Levels Be Palced

TPLevel (float) : Is The Take Profit Level

SLLevel (float) : Is The StopLoss Level

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

CloseLong(ExitID, PercentageClose, Comment, CommentValue, Instant)

Exits A Long Order Based On A Specified Condition

Parameters:

ExitID (string) : Is The Trade ID That Will Be Closed, Defval = "Long"

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Instant (bool) : Is For Exit Execution Type, Defval = false

Returns: Void

CloseShort(ExitID, PercentageClose, Comment, CommentValue, Instant)

Exits A Short Order Based On A Specified Condition

Parameters:

ExitID (string) : Is The Trade ID That Will Be Closed, Defval = "Short"

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Instant (bool) : Is For Exit Execution Type, Defval = false

Returns: Void

BrokerCheck(Broker)

Checks Traded Broker With Current Loaded Chart Broker

Parameters:

Broker (string) : Is The Current Broker That Is Traded

Returns: Bool - True If Current Traded Broker Is Same As Loaded Chart Broker

OpenPC(LicenseID, OrderType, UseLimit, LimitPrice, SymbolPrefix, Symbol, SymbolSuffix, Risk, SL, TP, OrderComment, Spread)

Compiles Given Parameters Into An Alert String Format To Open Trades Using Pine Connector

Parameters:

LicenseID (string) : Is The Users PineConnector LicenseID

OrderType (int) : Is The Desired OrderType To Open

UseLimit (bool) : Is If We Want To Enter The Position At Exactly The Previous Closing Price

LimitPrice (float) : Is The Limit Price Of The Trade (Only For Pending Orders)

SymbolPrefix (string) : Is The Current Symbol Prefix (If Any)

Symbol (string) : Is The Traded Symbol

SymbolSuffix (string) : Is The Current Symbol Suffix (If Any)

Risk (float) : Is The Trade Risk Per Trade / Fixed Lot Sizing

SL (float) : Is The Trade SL In Price / In Pips

TP (float) : Is The Trade TP In Price / In Pips

OrderComment (string) : Is The Executed Trade Comment

Spread (float) : is The Maximum Spread For Execution

Returns: String - Pine Connector Order Syntax Alert Message

ClosePC(LicenseID, OrderType, SymbolPrefix, Symbol, SymbolSuffix)

Compiles Given Parameters Into An Alert String Format To Close Trades Using Pine Connector

Parameters:

LicenseID (string) : Is The Users PineConnector LicenseID

OrderType (int) : Is The Desired OrderType To Close

SymbolPrefix (string) : Is The Current Symbol Prefix (If Any)

Symbol (string) : Is The Traded Symbol

SymbolSuffix (string) : Is The Current Symbol Suffix (If Any)

Returns: String - Pine Connector Order Syntax Alert Message

//====================================================================================================================================================

// Custom Backtesting Calculation Functions

//====================================================================================================================================================

CalculatePNL(EntryPrice, ExitPrice, LotSize, ConversionRate)

Calculates Trade PNL Based On Entry, Eixt & Lot Size

Parameters:

EntryPrice (float) : Is The Trade Entry

ExitPrice (float) : Is The Trade Exit

LotSize (float) : Is The Trade Sizing

ConversionRate (float) : Is The Currency Conversion Rate (Used For Complex Lot Sizing Only)

Returns: Float - The Current Trade PNL

UpdateBalance(PrevBalance, PNL)

Updates The Previous Ginve Balance To The Next PNL

Parameters:

PrevBalance (float) : Is The Previous Balance To Be Updated

PNL (float) : Is The Current Trade PNL To Be Added

Returns: Float - The Current Updated PNL

CalculateSlpComm(PNL, MaxRate)

Calculates Random Slippage & Commisions Fees Based On The Parameters

Parameters:

PNL (float) : Is The Current Trade PNL

MaxRate (float) : Is The Upper Limit (In Percentage) Of The Randomized Fee

Returns: Float - A Percentage Fee Of The Current Trade PNL

UpdateDD(MaxBalance, Balance)

Calculates & Updates The DD Based On Its Given Parameters

Parameters:

MaxBalance (float) : Is The Maximum Balance Ever Recorded

Balance (float) : Is The Current Account Balance

Returns: Float - The Current Strategy DD

CalculateWR(TotalTrades, LongID, ShortID)

Calculate The Total, Long & Short Trades Win Rate

Parameters:

TotalTrades (int) : Are The Current Total Trades That The Strategy Has Taken

LongID (string) : Is The Order ID Of The Long Trades Of The Strategy

ShortID (string) : Is The Order ID Of The Short Trades Of The Strategy

Returns: Tuple Of Long WR%, Short WR%, Total WR%, Total Winning Trades, Total Losing Trades, Total Long Trades & Total Short Trades

CalculateAvgRRR(WinTrades, LossTrades)

Calculates The Overall Strategy Avg Risk Reward Ratio

Parameters: