Conditional Value at Risk (CVaR)This Pine Script implements the Conditional Value at Risk (CVaR), a risk metric that evaluates the potential losses in a financial portfolio beyond a certain confidence level, incorporating both the Value at Risk (VaR) and the expected loss given that the VaR threshold has been breached.

Key Features:

Input Parameters:

length: Defines the observation period in days (default is 252, typically used to represent the number of trading days in a year).

confidence: Specifies the confidence interval for calculating VaR and CVaR, with values between 0.5 and 0.99 (default is 0.95, indicating a 95% confidence level).

Logarithmic Returns Calculation: The script computes the logarithmic returns based on the daily closing prices, a common method to measure financial asset returns, given by:

Log Return=ln(PtPt−1)

Log Return=ln(Pt−1Pt)

where PtPt is the price at time tt, and Pt−1Pt−1 is the price at the previous time point.

VaR Calculation: Value at Risk (VaR) is estimated as the percentile of the returns array corresponding to the given confidence interval. This represents the maximum loss expected over a given time horizon under normal market conditions at the specified confidence level.

CVaR Calculation: The Conditional VaR (CVaR) is calculated as the average of the returns that fall below the VaR threshold. This represents the expected loss given that the loss has exceeded the VaR threshold.

Visualization: The script plots two key risk measures:

VaR: The maximum potential loss at the specified confidence level.

CVaR: The average of the losses beyond the VaR threshold.

The script also includes a neutral line at zero to help visualize the losses and their magnitude.

Source and Scientific Background:

The concept of Value at Risk (VaR) was popularized by J.P. Morgan in the 1990s, and it has since become a widely-used tool for risk management (Jorion, 2007). Conditional Value at Risk (CVaR), also known as Expected Shortfall, addresses the limitation of VaR by considering the severity of losses beyond the VaR threshold (Rockafellar & Uryasev, 2002). CVaR provides a more comprehensive risk measure, especially in extreme tail risk scenarios.

References:

Jorion, P. (2007). Value at Risk: The New Benchmark for Managing Financial Risk. McGraw-Hill Education.

Rockafellar, R.T., & Uryasev, S. (2002). Conditional Value-at-Risk for General Loss Distributions. Journal of Banking & Finance, 26(7), 1443–1471.

Buscar en scripts para "ha溢价率"

Systematic Investment Tracker by Ceyhun Gonul### English Description

**Systematic Investment Tracker with Enhanced Features**

This script, titled **Systematic Investment Tracker with Enhanced Features**, is a TradingView tool designed to support systematic investments across different market conditions. It provides traders with two customizable investment strategies — **Continuous Buying** and **Declining Buying** — and includes advanced dynamic investment adjustment features for each.

#### Detailed Explanation of Script Features and Originality

1. **Two Investment Strategies**:

- **Continuous Buying**: This strategy performs purchases consistently at each interval, as set by the user, regardless of market price changes. It follows the principle of dollar-cost averaging, allowing users to build an investment position over time.

- **Declining Buying**: Unlike Continuous Buying, this strategy triggers purchases only when the asset's price has declined from the previous interval's closing price. This approach helps users capitalize on lower price points, potentially improving average costs during downward trends.

2. **Dynamic Investment Adjustment**:

- For both strategies, the script includes a **Dynamic Investment Adjustment** feature. If enabled, this feature increases the purchasing amount by 50% if the current price has fallen by a specific user-defined percentage relative to the previous price. This allows users to accumulate a larger position when the asset is declining, which may benefit long-term cost-averaging strategies.

3. **Customizable Time Frames**:

- Users can specify a **start and end date** for investment, allowing them to restrict or backtest strategies within a specific timeframe. This feature is valuable for evaluating strategy performance over specific market cycles or historical periods.

4. **Graphical Indicators and Labels**:

- The script provides graphical labels on the chart that display purchase points. These indicators help users visualize their investment entries based on the strategy selected.

- A summary **performance label** is also displayed, providing real-time updates on the total amount spent, accumulated quantity, average cost, portfolio value, and profit percentage for each strategy.

5. **Language Support**:

- The script includes English and Turkish language options. Users can toggle between these languages, allowing the summary label text and descriptions to be displayed in their preferred language.

6. **Performance Comparison Table**:

- An optional **Performance Comparison Table** is available, offering a side-by-side analysis of net profit, total investment, and profit percentage for both strategies. This comparison table helps users assess which strategy has yielded better returns, providing clarity on each approach's effectiveness under the chosen parameters.

#### How the Script Works and Its Uniqueness

This closed-source script brings together two established investment strategies in a single, dynamic tool. By integrating continuous and declining purchase strategies with advanced settings for dynamic investment adjustment, the script offers a powerful, flexible tool for both passive and active investors. The design of this script provides unique benefits:

- Enables automated, systematic investment tracking, allowing users to build positions gradually.

- Empowers users to leverage declines through dynamic adjustments to optimize average cost over time.

- Presents an easy-to-read performance label and table, enabling an efficient and transparent performance comparison for informed decision-making.

---

### Türkçe Açıklama

**Gelişmiş Özellikli Sistematik Yatırım Takipçisi**

**Gelişmiş Özellikli Sistematik Yatırım Takipçisi** adlı bu TradingView scripti, çeşitli piyasa koşullarında sistematik yatırım stratejilerini desteklemek üzere tasarlanmış bir araçtır. Script, kullanıcıya iki özelleştirilebilir yatırım stratejisi — **Sürekli Alım** ve **Düşen Alım** — ve her strateji için gelişmiş dinamik yatırım ayarlama seçenekleri sunar.

#### Script Özelliklerinin Detaylı Açıklaması ve Özgünlük

1. **İki Yatırım Stratejisi**:

- **Sürekli Alım**: Bu strateji, fiyat değişimlerine bakılmaksızın kullanıcının belirlediği her aralıkta sabit bir miktar yatırım yapar. Bu yaklaşım, uzun vadede pozisyonu kademeli olarak oluşturmak isteyenler için idealdir.

- **Düşen Alım**: Sürekli Alım’ın aksine, bu strateji yalnızca fiyat bir önceki aralığın kapanış fiyatına göre düştüğünde alım yapar. Bu yöntem, yatırımcıların daha düşük fiyatlardan alım yaparak ortalama maliyeti potansiyel olarak iyileştirmelerine yardımcı olur.

2. **Dinamik Yatırım Ayarlaması**:

- Her iki strateji için de **Dinamik Yatırım Ayarlaması** özelliği bulunmaktadır. Bu özellik aktif edildiğinde, mevcut fiyatın bir önceki fiyata göre kullanıcı tarafından belirlenen bir yüzde oranında düşmesi durumunda alım miktarını %50 artırır. Bu durum, uzun vadede maliyet ortalaması stratejilerine katkıda bulunur.

3. **Özelleştirilebilir Tarih Aralığı**:

- Kullanıcılar, yatırımı belirli bir tarih aralığında sınırlandırmak veya test etmek için bir **başlangıç ve bitiş tarihi** belirleyebilir. Bu özellik, strateji performansını geçmiş piyasa döngüleri veya belirli dönemlerde değerlendirmek için kullanışlıdır.

4. **Grafiksel İşaretleyiciler ve Etiketler**:

- Script, grafik üzerinde alım noktalarını gösteren işaretleyiciler sağlar. Bu görsel göstergeler, kullanıcıların seçilen stratejiye göre yatırım girişlerini görselleştirmesine yardımcı olur.

- Ayrıca, her strateji için harcanan toplam tutar, biriken miktar, ortalama maliyet, portföy değeri ve kâr yüzdesi gibi bilgileri gerçek zamanlı olarak gösteren bir **performans etiketi** sunar.

5. **Dil Desteği**:

- Script, İngilizce ve Türkçe dillerini desteklemektedir. Kullanıcılar, performans etiketi metninin ve açıklamalarının tercih ettikleri dilde görüntülenmesi için dil seçimini yapabilir.

6. **Performans Karşılaştırma Tablosu**:

- İsteğe bağlı olarak kullanılabilen bir **Performans Karşılaştırma Tablosu**, her iki strateji için net kâr, toplam yatırım ve kâr yüzdesi gibi bilgileri yan yana analiz eder. Bu tablo, kullanıcıların hangi stratejinin daha yüksek getiri sağladığını değerlendirmesine yardımcı olur.

#### Scriptin Çalışma Prensibi ve Özgünlüğü

Bu script, iki yatırım stratejisini gelişmiş bir araçta birleştirir. Sürekli ve düşen fiyatlara dayalı alım stratejilerini dinamik yatırım ayarlama özelliğiyle entegre ederek yatırımcılar için güçlü ve esnek bir çözüm sunar. Script’in tasarımı aşağıdaki benzersiz faydaları sağlamaktadır:

- Otomatik, sistematik yatırım takibi yaparak kullanıcıların pozisyonlarını kademeli olarak oluşturmalarına olanak tanır.

- Dinamik ayarlama ile düşüşlerden yararlanarak zaman içinde ortalama maliyeti optimize etme olanağı sağlar.

- Her iki stratejinin performansını basit ve anlaşılır bir şekilde karşılaştıran etiket ve tablo ile verimli bir performans değerlendirmesi sunar.

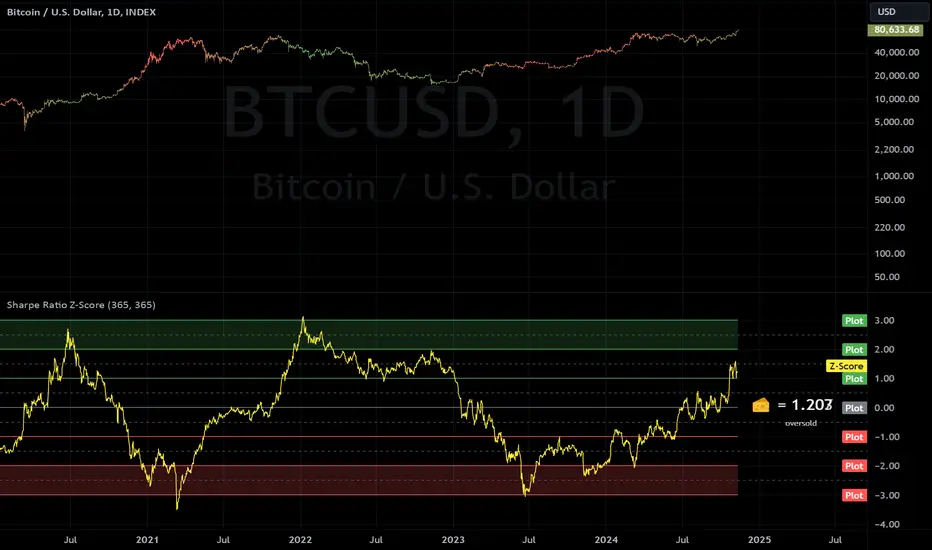

Sharpe Ratio Z-ScoreThis indicator calculates the Sharpe Ratio and its Z-Score , which are used to evaluate the risk-adjusted return of an asset over a given period. The Sharpe Ratio is computed using the average return and the standard deviation of returns, while the Z-Score standardizes this ratio to assess how far the current Sharpe Ratio deviates from its historical average.

The Sharpe Ratio is a measure of how much return an investment has generated relative to the risk it has taken. In the context of this script, the risk-free rate is assumed to be 0, but in real applications, it would typically be the return on a safe investment, like a Treasury bond. A higher Sharpe Ratio indicates that the investment's returns are higher compared to its risk, making it a more favorable investment. Conversely, a lower Sharpe Ratio suggests that the investment may not be worth the risk.

Calculation:

Daily Returns Calculation: The script calculates the daily return of the asset. This measures the percentage change in the asset’s closing price from one period to the next.

Sharpe Ratio Calculation: The Sharpe Ratio is calculated by taking the average daily return and dividing it by the standard deviation of the returns, then multiplying by the square root of the period length.

Usage:

Traders and Investors can use the Sharpe Ratio to evaluate how well the asset is compensating for risk. A high Sharpe Ratio indicates a high return per unit of risk, whereas a low or negative Sharpe Ratio suggests poor risk-adjusted returns. In overbought times, an asset would have high/positive returns per unit of risk. In oversold times, an asset would have low/negative returns per unit of risk.

The Z-Score provides a way to compare the current Sharpe Ratio to its historical distribution, offering a more standardized view of how extreme or typical the current ratio is.

Positive Z-score: Indicates that the asset's return is significantly lower than its risk, suggesting potential oversold conditions.

Negative Z-score: Indicates that the asset's return is significantly higher than its risk, suggesting potential overbought conditions.

Red Zone (-3 to -2): Strong overbought conditions.

Green Zone (2 to 3): Strong oversold conditions.

Sharpe Ratio Limitations:

While the Sharpe Ratio is widely used to evaluate risk-adjusted returns, it has its limitations.

Fat Tails: It assumes that returns are normally distributed and does not account for extreme events or "fat tails" in the return distribution. This can be problematic for assets like cryptocurrencies, which may experience large, sudden price swings that skew the return distribution.

Single Risk Factor: The Sharpe Ratio only considers standard deviation (total volatility) as a measure of risk, ignoring other types of risks like skewness or kurtosis, which may also impact an asset’s performance.

Time Frame Sensitivity: The accuracy of the Sharpe Ratio and its Z-Score is heavily influenced by the time frame chosen for the calculation. A longer period may smooth out short-term fluctuations, while a shorter period might be more sensitive to recent volatility.

Overbought and Oversold Zones: The script marks overbought and oversold conditions based on the Z-Score, but this is not a guarantee of market reversal. It’s important to combine this tool with other technical indicators and fundamental analysis for a more comprehensive market evaluation.

Volatility: The Sharpe Ratio and Z-Score depend on the volatility (standard deviation) of the asset’s returns. For highly volatile assets, such as cryptocurrencies, the Sharpe Ratio may not fully capture the true risk or may be misleading if the volatility is transient.

Doesn't Account for Downside Risk: The Sharpe Ratio treats upside and downside volatility equally, which may not reflect how investors perceive risk. Some investors may be more concerned with downside risk, which the Sharpe Ratio does not distinguish from upside fluctuations.

Important Considerations:

The Sharpe Ratio should not be used in isolation. While it provides valuable insights into risk-adjusted returns, it is important to combine it with other performance and risk indicators to form a more comprehensive market evaluation. Relying solely on the Sharpe Ratio may lead to misleading conclusions, particularly in volatile or non-normally distributed markets.

When integrated into a broader investment strategy, the Sharpe Ratio can help traders and investors better assess the risk-return profile of an asset, identifying periods of potential overperformance or underperformance. However, it should be used alongside other tools to ensure more informed decision-making, especially in highly fluctuating markets.

Enhanced Buy/Sell Pressure, Volume, and Trend Bar analysisEnhanced Buy/Sell Pressure, Volume, and Trend Bar Analysis Indicator

Overview

This indicator is designed to help traders identify buy and sell pressure, volume changes, and overall trend direction in the market. It combines multiple concepts like price action, volume, and trend analysis, candlestick anaysis to provide a comprehensive view of market dynamics. The visual elements are intuitive, making it suitable for traders at different levels. This indicator works together with Enhanced Pressure MTF Screener which is a screener based of this indicator to make it easier to see Bullish/Bearish pressures and trend across multiple timeframes.

Image below: is the Enhanced Buy/Sell Pressure, Volume, and Trend Bar Analysis with the Enhanced Pressure MTF Screener indicator both active together.

Key Features

1.Buy/Sell Pressure Identification

Buy Pressure: Calculated based on price movement where the close price is higher than the opening price.

Sell Pressure: Calculated when the closing price is equal to or lower than the opening price.These pressures help you understand whether buyers or sellers are more dominant for each bar.

2.Volume Analysis

Normalized Volume: Volume data is normalized, making it easier to compare volume levels over different periods.

Volume Histogram: The volume is also presented as a histogram for easy visualization, showing whether the current volume is higher or lower compared to the average.

3.Simplified Coloring Option

You can choose to simplify the coloring of bars to reflect the dominant pressure: green for bullish pressure and red for bearish pressure. This makes it visually easier to identify who is in control. When simplified coloring is disabled, the bars' colors will represent the combined effect of buy and sell pressure.

4.Heikin-Ashi Candles for Pressure Calculation

The indicator includes an option to use Heikin-Ashi candles instead of traditional candles to calculate buy and sell pressure. Heikin-Ashi candles are known for smoothing out price action and providing a clearer trend representation.

5.Trend Background Coloring

This feature uses exponential moving averages (EMAs) to determine the trend:

Short-Term EMA vs. Long-Term EMA: When the short-term EMA is above the long-term EMA, the trend is considered bullish, and vice versa.

The background color changes based on the identified trend: green for an uptrend and red for a downtrend. This feature helps visualize the overall market direction at a glance.

6.Signals for Key Price Actions

The indicator plots various symbols to signal important price movements:

Bullish Close (▲): Indicates a strong upward movement where the close price crosses above the open.

Bearish Close (▼): Indicates a downward movement where the close price falls below the open.

Higher High (•): Highlights new highs compared to previous bars, useful for confirming an uptrend.

Lower Low (•): Highlights lower lows compared to previous bars, which can indicate a downtrend or bearish pressure.

Calculations Explained

1.Buy and Sell Pressure Calculation

The buy pressure is determined by the price range (high - low) if the closing price is above the opening price, indicating an increase in value.

The sell pressure is similarly calculated when the closing price is equal to or below the opening price.

The indicator uses the Average True Range (ATR) for normalization. Normalizing helps you compare pressure across different periods, regardless of market volatility.

2.Volume Normalization

Volume Normalization: To make volume comparable across different periods, the indicator normalizes it using the Simple Moving Average (SMA) of volume over a user-defined length.

Volume Histogram: The histogram provides a clear representation of volume changes compared to the average, making it easier to spot unusual activity that may indicate market shifts.

3.Combined Pressure Calculation

The indicator calculates a combined pressure value by subtracting sell pressure from buy pressure.

When combined pressure is positive, buying is dominant, and when negative, selling is dominant. This helps in visually understanding the ongoing momentum.

4.Trend Calculation

The indicator uses two EMAs to determine the trend:

Short-Term EMA (default 14-period) to capture recent price movements.

Long-Term EMA (default 50-period) to provide a broader trend perspective.

By comparing these EMAs on a higher timeframe, the indicator can identify whether the trend is up or down, making it easier for traders to align their trades with the larger market movement.

Inputs and Customization

The indicator provides several options for customization, allowing you to adjust it to your preferences:

SMA Length: Determines the lookback period for moving averages and volume normalization. A longer length provides more smoothing, whereas a shorter length makes the indicator more responsive.

Buy/Sell/Volume Colors: Customize the colors used to represent buying, selling, and volume to suit your preferences.

Heikin Ashi Option: Toggle between using Heikin Ashi or traditional OHLC (Open-High-Low-Close) candles for pressure calculations.

Trend Timeframe and EMA Periods: You can choose different timeframes and EMA periods for trend analysis to suit your trading strategy.

How to Use This Indicator

Identifying Market Momentum: Use the buy/sell pressure columns to see which side (buyers or sellers) is in control. Positive pressure combined with green color indicates strong buying, while red indicates selling.

Volume Confirmation: Check the volume area plot and histogram. High volume coupled with strong pressure is a sign of conviction, meaning the current move has backing from market participants.

Trend Identification: The trend background color helps identify the overall trend direction. Trade in the direction of the trend (e.g., take long positions during a green background).

Signal Indicators: The plotted symbols like "Bullish Close" and "Bearish Close" provide visual signals of key price actions, useful for timing entry or exit points.

Practical use Example

Scenario: The market is consolidating, and you see alternating green and red bars.

Action: Wait for a consistent sequence of green bars (buy pressure) along with a green background (uptrend) to consider going long, although you can go long without having a green background, the background adds confirmation layer.

Scenario: The market has several bearish closes (red ▼ symbols) accompanied by increasing volume.

Action: This could indicate strong selling pressure. If the background also turns red, it might be a good time to exit long positions or consider shorting.

Higher timeframe pressure and volume: Another way to use the indicator is to check buy/sell volume and pressure of the higher timeframe say weekly or daily or any timeframe you consider higher, once you’ve identified or feel confident in which direction the bar is going along with the full picture of trend, you can go to the lower timeframe and wait for it to sync with the higher timeframe to consider a long or a short. It is also easier to see when markets sync up by also applying the Enhanced Pressure MTF Screener which works in companion to this indicator.

Visual Cues and Interpretation

Combined Pressure Plot: The green and red column plot at the bottom of the chart represents the dominance between buying and selling. Tall green bars signify strong buying, while tall red bars indicate selling dominance.

Trend Background: Helps visualize the overall direction without manually drawing trend lines. When the background turns green, it generally indicates that the shorter-term moving average has crossed above the longer-term average—a sign of a bullish trend.

To Summarize shortly

The Enhanced Buy/Sell Pressure, Volume, and Trend Bar Analysis Indicator is an advanced but simple tool designed to help traders visually understand market dynamics. It combines different aspects of market analysis of candle pressure from buyers and sellers, volume confirmation, and trend identification into a single view, which can assist both new and experienced traders in making informed trading decisions.

This indicator:

Saves time by simplifying market analysis.

Provides clear visual cues for buy/sell pressure, volume, and trend.

Offers customizable settings to suit individual trading styles.

Always, I am happy to share my creations with you all for free. If you guys have cool ideas you would like to share, or suggestions for improvements the comment is below and I hope this overview gave an idea of how to use the indicator :D

Target Trend [BigBeluga]The Target Trend indicator is a trend-following tool designed to assist traders in capturing directional moves while managing entry, stop loss, and profit targets visually on the chart. Using adaptive SMA bands as the core trend detection method, this indicator dynamically identifies shifts in trend direction and provides structured exit points through customizable target levels.

SP500:

🔵 IDEA

The Target Trend indicator’s concept is to simplify trade management by providing automated visual cues for entries, stops, and targets directly on the chart. When a trend change is detected, the indicator prints an up or down triangle to signal entry direction, plots three customizable target levels for potential exits, and calculates a stop-loss level below or above the entry point. The indicator continuously adapts as price moves, making it easier for traders to follow and manage trades in real time.

When price crosses a target level, the label changes to a check mark, confirming that the target has been achieved. Similarly, if the stop-loss level is hit, the label changes to an "X," and the line becomes dashed, indicating that the stop loss has been activated. This feature provides traders with a clear visual trail of whether their targets or stop loss have been hit, allowing for easier trade tracking and exit strategy management.

🔵 KEY FEATURES & USAGE

SMA Bands for Trend Detection: The indicator uses adaptive SMA bands to identify the trend direction. When price crosses above or below these bands, a new trend is detected, triggering entry signals. The entry point is marked on the chart with a triangle symbol, which updates with each new trend change.

Automated Targets and Stop Loss Management: Upon a new trend signal, the indicator automatically plots three price targets and a stop loss level. These levels provide traders with structured exit points for potential gains and a clear risk limit. The stop loss is placed below or above the entry point, depending on the trend direction, to manage downside risk effectively.

Visual Target and Stop Loss Validation: As price hits each target, the label beside the level updates to a check mark, indicating that the target has been reached. Similarly, if the stop loss is activated, the stop loss label changes to an "X," and the line becomes dashed. This feature visually confirms whether targets or stop losses are hit, simplifying trade management.

The indicator also marks the entry price at each trend change with a label on the chart, allowing traders to quickly see their initial entry point relative to current price and target levels.

🔵 CUSTOMIZATION

Trend Length: Set the lookback period for the trend-detection SMA bands to adjust the sensitivity to trend changes.

Targets Setting: Customize the number and spacing of the targets to fit your trading style and market conditions.

Visual Styles: Adjust the appearance of labels, lines, and symbols on the chart for a clearer view and personalized layout.

🔵 CONCLUSION

The Target Trend indicator offers a streamlined approach to trend trading by integrating entry, target, and stop loss management into a single visual tool. With automatic tracking of target levels and stop loss hits, it helps traders stay focused on the current trend while keeping track of risk and reward with minimal effort.

Price Action StrategyThe **Price Action Strategy** is a tool designed to capture potential market reversals by utilizing classic reversal candlestick patterns such as Hammer, Shooting Star, Doji, and Pin Bar near dinamic support and resistance levels.

***Note to moderators

- The moving average was removed from the strategy because it was not suitable for the strategy and not participating in the entry or exit criteria.

- The moving average length has been replaced/renamed by the support/resistance lenght.

- The bullish engulfing and bearish engulfing patterns were also removed because in practice they were not working as entry criteria, since the candle price invariably closes far from the support/resistance level even considering the sensitivity range. There was no change in the backtest results after removing these patterns.

### Key Elements of the Strategy

1. Support and Resistance Levels

- Support and resistance are pivotal price levels where the asset has previously struggled to move lower (support) or higher (resistance). These levels act as psychological barriers where buying interest (at support) or selling interest (at resistance) often increases, potentially causing price reversals.

- In this strategy, support is calculated as the lowest low and resistance as the highest high over a 16-period length. When the price nears these levels, it indicates possible zones for a reversal, and the strategy looks for specific candlestick patterns to confirm an entry.

2. Candlestick Patterns

- This strategy uses classic reversal patterns, including:

- **Hammer**: Indicates a buy signal, suggesting rejection of lower prices.

- **Shooting Star**: Suggests a sell signal, showing rejection of higher prices.

- **Doji**: Reflects indecision and potential reversal.

- **Pin Bar**: Represents price rejection with a long shadow, often signaling a reversal.

By combining these reversal patterns with the proximity to dinamic support or resistance levels, the strategy aims to capture potential reversal movements.

3. Sensitivity Level

- The sensitivity parameter adjusts the acceptable range (Default 0.018 = 1.8%) around support and resistance levels within which reversal patterns can trigger trades (i.e. the closing price of the candle must occur within the specified range defined by the sensitivity parameter). A higher sensitivity value expands this range, potentially leading to less accurate signals, as it may allow for more false positives.

4. Entry Criteria

- **Buy (Long)**: A Hammer, Doji, or Pin Bar pattern near support.

- **Sell (Short)**: A Shooting Star, Doji, or Pin Bar near resistance.

5. Exit criteria

- Take profit = 9.5%

- Stop loss = 16%

6. No Repainting

- The Price Action Strategy is not subject to repainting.

7. Position Sizing by Equity and risk management

- This strategy has a default configuration to operate with 35% of the equity. The stop loss is set to 16% from the entry price. This way, the strategy is putting at risk about 16% of 35% of equity, that is, around 5.6% of equity for each trade. The percentage of equity and stop loss can be adjusted by the user according to their risk management.

8. Backtest results

- This strategy was subjected to deep backtest and operations in replay mode on **1000000MOGUSDT.P**, with the inclusion of transaction fees at 0.12% and slipagge of 5 ticks, and the past results have shown consistent profitability. Past results are no guarantee of future results. The strategy's backtest results may even be due to overfitting with past data.

9. Chart Visualization

- Support and resistance levels are displayed as green (support) and red (resistance) lines.

- Only the candlestick pattern that generated the entry signal to triger the trade is identified and labeled on the chart. During the operation, the occurrence of new Doji, Pin Bar, Hammer and Shooting Star patterns will not be demonstrated on the chart, since the exit criteria are based on percentage take profit and stop loss.

Doji:

Pin Bar and Doji

Shooting Star and Doji

Hammer

10. Default settings

Chart timeframe: 20 min

Moving average lenght: 16

Sensitivity: 0.018

Stop loss (%): 16

Take Profit (%): 9.5

BYBIT:1000000MOGUSDT.P

ICT Panther (By Obicrypto) V1 ICT Panther Indicator: Full and Detailed Description

The ICT Panther Indicator, created by Obicrypto, is an advanced technical analysis tool designed specifically for traders looking to identify key price action events based on institutional trading techniques, particularly in the context of the Inner Circle Trader (ICT) methodology. This indicator helps traders spot market structure breaks, order blocks, and potential trade opportunities driven by institutional behaviors in the market. Here's a detailed breakdown of its features and how it works:

What Does the ICT Panther Indicator Do?

1. Market Structure Breaks (MSB) Identification:

The ICT Panther identifies critical points where the market changes direction, commonly referred to as a break of structure (BoS). When the price breaks above or below certain key levels (based on highs and lows or opens and closes), it signals a potential shift in market sentiment. These break-of-structure points are essential for traders to determine whether the market is likely to continue its trend or reverse.

2. Order Blocks Visualization:

The indicator plots demand (bullish) and supply (bearish) boxes, which represent areas where institutional traders might place significant buy or sell orders. These zones, known as order blocks, are areas where the price tends to pause or reverse, giving traders key insights into potential entry and exit points. The indicator shows these areas graphically as colored boxes on the chart, which can be used to plan trades based on market structure and price action.

3. Pivot Point Detection:

The ICT Panther identifies important pivot points by tracking higher highs and lower lows. These pivot points are critical in determining the strength of a trend and can help traders confirm the direction of the market. The indicator uses a unique algorithm to detect two levels of pivot points:

- First-Order Pivots: Major pivot points where the price makes notable highs and lows.

- Second-Order Pivots: Smaller pivot points, useful for detecting microtrends within the larger market structure.

4. Bullish and Bearish Break of Structure Lines:

When a significant market structure break (BoS) occurs, the indicator will automatically draw red lines (for bearish break of structure) and green lines (for bullish break of structure) at key price levels. These lines help traders quickly see where institutional moves have occurred in the past and where potential future price moves could originate from.

5. Tested and Filled Boxes:

The ICT Panther also has a built-in mechanism to dim previously tested order blocks. When the price tests an order block (returns to a previous demand or supply zone), the box's color dims to indicate that the area has already been tested, reducing its significance. If the price fully fills an order block, the box stops plotting, providing a clear and clutter-free chart.

Key Features

1. Market Structure Break (MSB) Trigger:

- The indicator allows users to select between highs/lows or opens/closes as the trigger for market structure breaks. This flexibility lets traders adjust the indicator to suit their personal trading style or the behavior of specific assets.

2. Order Block Detection and Visualization:

- The tool automatically plots bullish and bearish demand and supply boxes, representing institutional order blocks on the chart. These boxes provide visual cues for areas of potential price action, where institutional traders might be active.

3. Second-Order Pivot Highlighting:

- The ICT Panther offers an option to plot second-order pivots, highlighting smaller pivot points within the larger market structure. These pivots can be helpful for short-term traders who need to react to smaller price movements while still keeping the larger trend in mind.

4. Box Test and Fill Delays:

- Users can configure delays for box tests and box fills, meaning the indicator will only mark a box as tested or filled after a certain number of bars. This prevents false signals and helps confirm that a zone is truly significant in the market.

5. Customization and Visual Clarity:

- The indicator is highly customizable, allowing users to turn on or off various features like:

- Displaying second-order pivots.

- Highlighting candles that broke structure.

- Plotting market structure broke lines.

- Showing or hiding tested and filled demand boxes.

- Setting custom delays for box testing and filling to suit different market conditions.

6. Tested and Filled Order Block Visualization:

- The indicator visually adjusts the tested and filled order blocks, dimming tested zones and removing filled zones to avoid clutter on the chart. This ensures that traders can focus on active trading opportunities without distractions from historical data.

How Does It Work?

1. Detecting Market Structure Breaks (BoS):

- The indicator continuously tracks the market for key price action signals. When the price breaks through previous highs or lows (or opens and closes, depending on your selection), the indicator marks this as a break of structure. This is a critical signal used by institutional traders and retail traders alike to determine potential future price movements.

2. Order Block Identification:

- Whenever a bullish break of structure occurs, the indicator plots a green demand box to show the area where institutional buyers might have placed significant orders. Similarly, for a bearish break of structure, it plots a red supply box representing areas where institutional sellers are active.

3. Pivot Analysis and Tracking:

- As the market moves, the indicator continuously updates first-order and second-order pivot points based on highs and lows. These points help traders identify whether the market is trending or consolidating. Traders can use these pivot points in combination with the order blocks to make informed trading decisions.

4. Box Testing and Filling:

- When the price retests an existing order block, the box dims to show it has been tested. If the price fully fills the box, it is no longer shown, which helps traders focus on the most relevant, untested order blocks.

Benefits for Traders

- Improved Decision-Making: With clear visuals and advanced logic based on institutional trading strategies, this indicator provides a deeper understanding of market structure and price action.

- Reduced Clutter: The indicator intelligently manages the display of order blocks and pivot points, ensuring that traders focus only on the most relevant information.

- Adaptability: Whether you are a swing trader or a day trader, the ICT Panther can be adjusted to fit your trading style, offering robust and flexible tools for tracking market structure and order blocks.

- Institutional Edge: By identifying institutional-level order blocks and market structure breaks, traders using this indicator can trade in line with the strategies of large market participants.

Who Should Use the ICT Panther Indicator?

This indicator is ideal for:

- Crypto, Forex, and Stock Traders who want to incorporate institutional trading concepts into their strategies.

- Technical Analysts looking for precise tools to measure the market structure and price action.

- ICT Traders who follow the Inner Circle Trader methodology and want an advanced tool to automate and enhance their analysis.

- Price Action Traders seeking a reliable indicator to track pivot points, order blocks, and market structure breaks.

The ICT Panther Indicator is a powerful, versatile tool that brings institutional trading techniques to the fingertips of retail traders. Whether you are looking to identify key market structure breaks, order blocks, or crucial pivot points, this indicator offers detailed visualizations and customizable options to help you make more informed trading decisions. With its ability to track the activities of institutional traders, the ICT Panther Indicator equips traders with the insights needed to stay ahead of the market and trade with confidence.

With the ICT Panther Indicator, traders can follow the movements of institutional money, making it easier to predict market direction and capitalize on high-probability trading opportunities.

Enjoy it and share it with your friends!

SMT Divergences [OutOfOptions]Smart Money Technique (SMT) Divergence is designed to identify discrepancies between correlated assets within the same timeframe. It occurs when two related assets exhibit opposing signals, such as one forming a higher low while the other forms a lower low. This technique is particularly useful for anticipating market shifts or reversals before they become evident through other Premium Discount (PD) Arrays.

This indicator works by identifying the highs and lows that have formed for an asset on the current chart and the correlated symbol defined in the settings. Once a pivot on either asset is formed, it checks if the pivot has taken liquidity as identified by the previous pivot in the same direction (i.e., a new high taking out a previous high). If this is the case and the corresponding asset has not taken a similar pivot, the condition is determined to be a potential valid divergence. The indicator will then filter out SMTs formed by adjacent candles, requiring at least one candle difference between the candles forming the SMT.

If the “Candle Direction Validation” setting is enabled, the indicator will further check both assets to ensure that for bullish SMTs, the last high on both assets was formed by down candle, and for bearish SMTs, the low was formed by an up candle. This check can often eliminate low-probability SMTs that are frequently broken.

The referenced chart shows divergence between Nasdaq (NQ) and S&P 500 (ES) futures, which are normally closely correlated assets that move in the same direction. The lines shown represent bullish and bearish divergences between the two when they are formed. As you can see from the chart, SMT Divergences may not always indicate a reversal, or a reversal might be just a short-term retrace. Therefore, SMT Divergences should not be used independently. However, in conjunction with other PD arrays, they can provide strong confirmation of a change in market direction.

Configurability:

Pivot strength - Indicates how many bars to the left/right of a high for pivot to be considered, recommended to keep at 1 for maximum detection speed

Candle Direction Validation - Additional SMT validation to filter out weak/low-probability SMTs be examining candle direction

Line Styling for Bullish/Bearish SMTs - Ability to customize line style, color & width for bullish/bearish SMTs

Label Control - Whether or not to show SMT label and if shown what font size & color should be used

What makes this indicator different:

Unlike other SMT indicators, this indicators has additional built-in controls to remove low-probability SMTs

Liquidity Pools [LuxAlgo]The Liquidity Pools indicator identifies and displays estimated liquidity pools on the chart by analyzing high and low wicked price areas, along with the amount, and frequency of visits to each zone.

🔶 USAGE

Liquidity Pools are areas where smaller participants are likely to place stop-limit orders to manage risks at reasonable swing points. These zones attract institutional traders who use the pending orders as liquidity to enter larger positions, aiming to influence price movements. By monitoring these zones, traders can anticipate market movements and potentially benefit from these dynamics.

Beyond general liquidity theory, identifying zones consistently visited by price aids in using them as support and resistance zones. By analyzing these areas, we can assess how effectively participants enter or exit these zones, helping to gauge their importance.

In the screenshots below, we will explore both sides of the same chart in more detail to display how each zone could be viewed from a bullish and bearish perspective.

Bullish Zones Example:

Bearish Zones Example:

🔶 DETAILS

The method behind this indicator focuses on identifying a swing point and tracking future interactions with it. It adaptively identifies high and low "potential zones". These zones are monitored over time; if a zone meets the user-defined criteria, the script marks and displays these zones on the chart.

🔹 Identification

The method to identify Liquidity Pools in this indicator revolves around 3 main parameters. By utilizing these settings, the indicator can be tailored to produce zones that fit the specific strategic needs of each trader.

Zone Identification Parameters

Zone Contact Amount: This setting determines the number of times each zone must be in contact with the price (and bought or sold out of) before being identified by the indicator as a Liquidity Pool.

For example: When a zone is first displayed, it is considered as having been reached 1 time. When the zone is re-tested for the first time, this is considered the 2nd contact, since the price has seen the zone a total of 2 times.

Bars Required Between Each Contact: This is used to rule out (or in) consecutive candles reaching each zone from the calculation, adding a separation length between zone contact points to refine the zones produced.

For example: When set to "2", the first contact point (first re-test) will be ignored by the script if it is not at least 2 bars away from the initial zone proposal point.

Confirmation Bars: After a zone has reached the desired Contact Amount, this setting will cause the script to wait a specified number of bars before identifying a zone. While this might initially seem counterintuitive, by waiting, we are able to watch the market's reaction to the proposed zone and respond accordingly. If the price were to continue through the potential liquidity zone Immediately, it would not be logical to consider this area as a valid Liquidity Pool.

Displayed in this screenshot, you will see the specific points we are looking for in order to identify these zones.

🔹 Display

After a Liquidity Pool is identified, its boundary line is extended to the current price to keep it in view for reference. This extension will continue until the zone is mitigated (price has closed above or below the zone), after which it will stop extending.

Candles can optionally be colored when returning to the most recent Liquidity Pool if it is still unmitigated, and will only color after the zone is displayed on the chart. Because of this, if a candle is colored within a zone, then its color comes from being inside a previously unmitigated zone.

🔹 Volume

Each time a candle overlaps an Unmitigated Zone, a percentage of its volume will be accumulated to the total for each specific zone. The volume total is displayed on the right end of the extended boundary lines.

This volume data could help to determine the importance of specific zones based on the amount of volume traded within.

Note: This volume is fractional to the percentage of candles that are contained within the zone. If a candle is 50% within a zone, The zone will receive 50% of the candle's volume added to its current total.

🔶 SETTINGS

See above for a more detailed explanation of the "Zone Identification" parameters.

Zone Contact Amount: The number of times the price must bounce from this zone before considering it as a liquidity pool.

Bars Required Between Each Contact: The number of bars to wait before checking for another zone contact.

Confirmation Bars: The number of bars to wait before identifying a zone to confirm validity.

Display Volume Labels: Toggles the display for the volume readout for each Liquidity Pool.

Fill Candles Inside Zones: Toggles the display of colored candles within Liquidity Pools.

HTF LQ SweepThe following script recognises QL sweeps in the desired time frame with alarm function!

Theory:

There is liquidity above highs and below lows. If this is tapped and the market reacts strongly immediately, the probability of a reversal is greatly increased! In the chart, this is defined in such a way that a candle has its wicks BELOW the old low, but the close is ABOVE the old low. the same applies to the high, of course!

In such a case we have an "LQ Sweep"

How does the script work?

Williams 3 fractals are used as a basis. These are meaningful as lows or highs. Whenever a fractal is created, the price level is saved.

This means that not only the last fractal is relevant, but all historical fractals as long as they have not been reached!

If a candle reaches the level, but shows a rejection and closes within the level again, we have our "LQ Sweep" setup.

In the script you can select the timeframe in which the market has to be analysed. When the QL sweep occurs, an alert is triggered. This saves a lot of time because you can analyse different markets in different timeframes at the same time!

Each QL Sweep is marked in the chart when we are in the selected timeframe. These can also be deactivated so that only the last sweep is displayed.

Benefits for the trader:

An LQ sweep is a nice confirmation for a reversal.

If we have such an LQ sweep, we can wait in the lower timeframe for further confirmation, such as a structural break, to position our entries there.

The alarm function saves us a lot of time and we only go to the chart when a potential setup has been created.

You can set different time frames in the script: The selected time frame is then scanned and sends a signal when the event occurs.

Universal Ratio Trend Matrix [InvestorUnknown]The Universal Ratio Trend Matrix is designed for trend analysis on asset/asset ratios, supporting up to 40 different assets. Its primary purpose is to help identify which assets are outperforming others within a selection, providing a broad overview of market trends through a matrix of ratios. The indicator automatically expands the matrix based on the number of assets chosen, simplifying the process of comparing multiple assets in terms of performance.

Key features include the ability to choose from a narrow selection of indicators to perform the ratio trend analysis, allowing users to apply well-defined metrics to their comparison.

Drawback: Due to the computational intensity involved in calculating ratios across many assets, the indicator has a limitation related to loading speed. TradingView has time limits for calculations, and for users on the basic (free) plan, this could result in frequent errors due to exceeded time limits. To use the indicator effectively, users with any paid plans should run it on timeframes higher than 8h (the lowest timeframe on which it managed to load with 40 assets), as lower timeframes may not reliably load.

Indicators:

RSI_raw: Simple function to calculate the Relative Strength Index (RSI) of a source (asset price).

RSI_sma: Calculates RSI followed by a Simple Moving Average (SMA).

RSI_ema: Calculates RSI followed by an Exponential Moving Average (EMA).

CCI: Calculates the Commodity Channel Index (CCI).

Fisher: Implements the Fisher Transform to normalize prices.

Utility Functions:

f_remove_exchange_name: Strips the exchange name from asset tickers (e.g., "INDEX:BTCUSD" to "BTCUSD").

f_remove_exchange_name(simple string name) =>

string parts = str.split(name, ":")

string result = array.size(parts) > 1 ? array.get(parts, 1) : name

result

f_get_price: Retrieves the closing price of a given asset ticker using request.security().

f_constant_src: Checks if the source data is constant by comparing multiple consecutive values.

Inputs:

General settings allow users to select the number of tickers for analysis (used_assets) and choose the trend indicator (RSI, CCI, Fisher, etc.).

Table settings customize how trend scores are displayed in terms of text size, header visibility, highlighting options, and top-performing asset identification.

The script includes inputs for up to 40 assets, allowing the user to select various cryptocurrencies (e.g., BTCUSD, ETHUSD, SOLUSD) or other assets for trend analysis.

Price Arrays:

Price values for each asset are stored in variables (price_a1 to price_a40) initialized as na. These prices are updated only for the number of assets specified by the user (used_assets).

Trend scores for each asset are stored in separate arrays

// declare price variables as "na"

var float price_a1 = na, var float price_a2 = na, var float price_a3 = na, var float price_a4 = na, var float price_a5 = na

var float price_a6 = na, var float price_a7 = na, var float price_a8 = na, var float price_a9 = na, var float price_a10 = na

var float price_a11 = na, var float price_a12 = na, var float price_a13 = na, var float price_a14 = na, var float price_a15 = na

var float price_a16 = na, var float price_a17 = na, var float price_a18 = na, var float price_a19 = na, var float price_a20 = na

var float price_a21 = na, var float price_a22 = na, var float price_a23 = na, var float price_a24 = na, var float price_a25 = na

var float price_a26 = na, var float price_a27 = na, var float price_a28 = na, var float price_a29 = na, var float price_a30 = na

var float price_a31 = na, var float price_a32 = na, var float price_a33 = na, var float price_a34 = na, var float price_a35 = na

var float price_a36 = na, var float price_a37 = na, var float price_a38 = na, var float price_a39 = na, var float price_a40 = na

// create "empty" arrays to store trend scores

var a1_array = array.new_int(40, 0), var a2_array = array.new_int(40, 0), var a3_array = array.new_int(40, 0), var a4_array = array.new_int(40, 0)

var a5_array = array.new_int(40, 0), var a6_array = array.new_int(40, 0), var a7_array = array.new_int(40, 0), var a8_array = array.new_int(40, 0)

var a9_array = array.new_int(40, 0), var a10_array = array.new_int(40, 0), var a11_array = array.new_int(40, 0), var a12_array = array.new_int(40, 0)

var a13_array = array.new_int(40, 0), var a14_array = array.new_int(40, 0), var a15_array = array.new_int(40, 0), var a16_array = array.new_int(40, 0)

var a17_array = array.new_int(40, 0), var a18_array = array.new_int(40, 0), var a19_array = array.new_int(40, 0), var a20_array = array.new_int(40, 0)

var a21_array = array.new_int(40, 0), var a22_array = array.new_int(40, 0), var a23_array = array.new_int(40, 0), var a24_array = array.new_int(40, 0)

var a25_array = array.new_int(40, 0), var a26_array = array.new_int(40, 0), var a27_array = array.new_int(40, 0), var a28_array = array.new_int(40, 0)

var a29_array = array.new_int(40, 0), var a30_array = array.new_int(40, 0), var a31_array = array.new_int(40, 0), var a32_array = array.new_int(40, 0)

var a33_array = array.new_int(40, 0), var a34_array = array.new_int(40, 0), var a35_array = array.new_int(40, 0), var a36_array = array.new_int(40, 0)

var a37_array = array.new_int(40, 0), var a38_array = array.new_int(40, 0), var a39_array = array.new_int(40, 0), var a40_array = array.new_int(40, 0)

f_get_price(simple string ticker) =>

request.security(ticker, "", close)

// Prices for each USED asset

f_get_asset_price(asset_number, ticker) =>

if (used_assets >= asset_number)

f_get_price(ticker)

else

na

// overwrite empty variables with the prices if "used_assets" is greater or equal to the asset number

if barstate.isconfirmed // use barstate.isconfirmed to avoid "na prices" and calculation errors that result in empty cells in the table

price_a1 := f_get_asset_price(1, asset1), price_a2 := f_get_asset_price(2, asset2), price_a3 := f_get_asset_price(3, asset3), price_a4 := f_get_asset_price(4, asset4)

price_a5 := f_get_asset_price(5, asset5), price_a6 := f_get_asset_price(6, asset6), price_a7 := f_get_asset_price(7, asset7), price_a8 := f_get_asset_price(8, asset8)

price_a9 := f_get_asset_price(9, asset9), price_a10 := f_get_asset_price(10, asset10), price_a11 := f_get_asset_price(11, asset11), price_a12 := f_get_asset_price(12, asset12)

price_a13 := f_get_asset_price(13, asset13), price_a14 := f_get_asset_price(14, asset14), price_a15 := f_get_asset_price(15, asset15), price_a16 := f_get_asset_price(16, asset16)

price_a17 := f_get_asset_price(17, asset17), price_a18 := f_get_asset_price(18, asset18), price_a19 := f_get_asset_price(19, asset19), price_a20 := f_get_asset_price(20, asset20)

price_a21 := f_get_asset_price(21, asset21), price_a22 := f_get_asset_price(22, asset22), price_a23 := f_get_asset_price(23, asset23), price_a24 := f_get_asset_price(24, asset24)

price_a25 := f_get_asset_price(25, asset25), price_a26 := f_get_asset_price(26, asset26), price_a27 := f_get_asset_price(27, asset27), price_a28 := f_get_asset_price(28, asset28)

price_a29 := f_get_asset_price(29, asset29), price_a30 := f_get_asset_price(30, asset30), price_a31 := f_get_asset_price(31, asset31), price_a32 := f_get_asset_price(32, asset32)

price_a33 := f_get_asset_price(33, asset33), price_a34 := f_get_asset_price(34, asset34), price_a35 := f_get_asset_price(35, asset35), price_a36 := f_get_asset_price(36, asset36)

price_a37 := f_get_asset_price(37, asset37), price_a38 := f_get_asset_price(38, asset38), price_a39 := f_get_asset_price(39, asset39), price_a40 := f_get_asset_price(40, asset40)

Universal Indicator Calculation (f_calc_score):

This function allows switching between different trend indicators (RSI, CCI, Fisher) for flexibility.

It uses a switch-case structure to calculate the indicator score, where a positive trend is denoted by 1 and a negative trend by 0. Each indicator has its own logic to determine whether the asset is trending up or down.

// use switch to allow "universality" in indicator selection

f_calc_score(source, trend_indicator, int_1, int_2) =>

int score = na

if (not f_constant_src(source)) and source > 0.0 // Skip if you are using the same assets for ratio (for example BTC/BTC)

x = switch trend_indicator

"RSI (Raw)" => RSI_raw(source, int_1)

"RSI (SMA)" => RSI_sma(source, int_1, int_2)

"RSI (EMA)" => RSI_ema(source, int_1, int_2)

"CCI" => CCI(source, int_1)

"Fisher" => Fisher(source, int_1)

y = switch trend_indicator

"RSI (Raw)" => x > 50 ? 1 : 0

"RSI (SMA)" => x > 50 ? 1 : 0

"RSI (EMA)" => x > 50 ? 1 : 0

"CCI" => x > 0 ? 1 : 0

"Fisher" => x > x ? 1 : 0

score := y

else

score := 0

score

Array Setting Function (f_array_set):

This function populates an array with scores calculated for each asset based on a base price (p_base) divided by the prices of the individual assets.

It processes multiple assets (up to 40), calling the f_calc_score function for each.

// function to set values into the arrays

f_array_set(a_array, p_base) =>

array.set(a_array, 0, f_calc_score(p_base / price_a1, trend_indicator, int_1, int_2))

array.set(a_array, 1, f_calc_score(p_base / price_a2, trend_indicator, int_1, int_2))

array.set(a_array, 2, f_calc_score(p_base / price_a3, trend_indicator, int_1, int_2))

array.set(a_array, 3, f_calc_score(p_base / price_a4, trend_indicator, int_1, int_2))

array.set(a_array, 4, f_calc_score(p_base / price_a5, trend_indicator, int_1, int_2))

array.set(a_array, 5, f_calc_score(p_base / price_a6, trend_indicator, int_1, int_2))

array.set(a_array, 6, f_calc_score(p_base / price_a7, trend_indicator, int_1, int_2))

array.set(a_array, 7, f_calc_score(p_base / price_a8, trend_indicator, int_1, int_2))

array.set(a_array, 8, f_calc_score(p_base / price_a9, trend_indicator, int_1, int_2))

array.set(a_array, 9, f_calc_score(p_base / price_a10, trend_indicator, int_1, int_2))

array.set(a_array, 10, f_calc_score(p_base / price_a11, trend_indicator, int_1, int_2))

array.set(a_array, 11, f_calc_score(p_base / price_a12, trend_indicator, int_1, int_2))

array.set(a_array, 12, f_calc_score(p_base / price_a13, trend_indicator, int_1, int_2))

array.set(a_array, 13, f_calc_score(p_base / price_a14, trend_indicator, int_1, int_2))

array.set(a_array, 14, f_calc_score(p_base / price_a15, trend_indicator, int_1, int_2))

array.set(a_array, 15, f_calc_score(p_base / price_a16, trend_indicator, int_1, int_2))

array.set(a_array, 16, f_calc_score(p_base / price_a17, trend_indicator, int_1, int_2))

array.set(a_array, 17, f_calc_score(p_base / price_a18, trend_indicator, int_1, int_2))

array.set(a_array, 18, f_calc_score(p_base / price_a19, trend_indicator, int_1, int_2))

array.set(a_array, 19, f_calc_score(p_base / price_a20, trend_indicator, int_1, int_2))

array.set(a_array, 20, f_calc_score(p_base / price_a21, trend_indicator, int_1, int_2))

array.set(a_array, 21, f_calc_score(p_base / price_a22, trend_indicator, int_1, int_2))

array.set(a_array, 22, f_calc_score(p_base / price_a23, trend_indicator, int_1, int_2))

array.set(a_array, 23, f_calc_score(p_base / price_a24, trend_indicator, int_1, int_2))

array.set(a_array, 24, f_calc_score(p_base / price_a25, trend_indicator, int_1, int_2))

array.set(a_array, 25, f_calc_score(p_base / price_a26, trend_indicator, int_1, int_2))

array.set(a_array, 26, f_calc_score(p_base / price_a27, trend_indicator, int_1, int_2))

array.set(a_array, 27, f_calc_score(p_base / price_a28, trend_indicator, int_1, int_2))

array.set(a_array, 28, f_calc_score(p_base / price_a29, trend_indicator, int_1, int_2))

array.set(a_array, 29, f_calc_score(p_base / price_a30, trend_indicator, int_1, int_2))

array.set(a_array, 30, f_calc_score(p_base / price_a31, trend_indicator, int_1, int_2))

array.set(a_array, 31, f_calc_score(p_base / price_a32, trend_indicator, int_1, int_2))

array.set(a_array, 32, f_calc_score(p_base / price_a33, trend_indicator, int_1, int_2))

array.set(a_array, 33, f_calc_score(p_base / price_a34, trend_indicator, int_1, int_2))

array.set(a_array, 34, f_calc_score(p_base / price_a35, trend_indicator, int_1, int_2))

array.set(a_array, 35, f_calc_score(p_base / price_a36, trend_indicator, int_1, int_2))

array.set(a_array, 36, f_calc_score(p_base / price_a37, trend_indicator, int_1, int_2))

array.set(a_array, 37, f_calc_score(p_base / price_a38, trend_indicator, int_1, int_2))

array.set(a_array, 38, f_calc_score(p_base / price_a39, trend_indicator, int_1, int_2))

array.set(a_array, 39, f_calc_score(p_base / price_a40, trend_indicator, int_1, int_2))

a_array

Conditional Array Setting (f_arrayset):

This function checks if the number of used assets is greater than or equal to a specified number before populating the arrays.

// only set values into arrays for USED assets

f_arrayset(asset_number, a_array, p_base) =>

if (used_assets >= asset_number)

f_array_set(a_array, p_base)

else

na

Main Logic

The main logic initializes arrays to store scores for each asset. Each array corresponds to one asset's performance score.

Setting Trend Values: The code calls f_arrayset for each asset, populating the respective arrays with calculated scores based on the asset prices.

Combining Arrays: A combined_array is created to hold all the scores from individual asset arrays. This array facilitates further analysis, allowing for an overview of the performance scores of all assets at once.

// create a combined array (work-around since pinescript doesn't support having array of arrays)

var combined_array = array.new_int(40 * 40, 0)

if barstate.islast

for i = 0 to 39

array.set(combined_array, i, array.get(a1_array, i))

array.set(combined_array, i + (40 * 1), array.get(a2_array, i))

array.set(combined_array, i + (40 * 2), array.get(a3_array, i))

array.set(combined_array, i + (40 * 3), array.get(a4_array, i))

array.set(combined_array, i + (40 * 4), array.get(a5_array, i))

array.set(combined_array, i + (40 * 5), array.get(a6_array, i))

array.set(combined_array, i + (40 * 6), array.get(a7_array, i))

array.set(combined_array, i + (40 * 7), array.get(a8_array, i))

array.set(combined_array, i + (40 * 8), array.get(a9_array, i))

array.set(combined_array, i + (40 * 9), array.get(a10_array, i))

array.set(combined_array, i + (40 * 10), array.get(a11_array, i))

array.set(combined_array, i + (40 * 11), array.get(a12_array, i))

array.set(combined_array, i + (40 * 12), array.get(a13_array, i))

array.set(combined_array, i + (40 * 13), array.get(a14_array, i))

array.set(combined_array, i + (40 * 14), array.get(a15_array, i))

array.set(combined_array, i + (40 * 15), array.get(a16_array, i))

array.set(combined_array, i + (40 * 16), array.get(a17_array, i))

array.set(combined_array, i + (40 * 17), array.get(a18_array, i))

array.set(combined_array, i + (40 * 18), array.get(a19_array, i))

array.set(combined_array, i + (40 * 19), array.get(a20_array, i))

array.set(combined_array, i + (40 * 20), array.get(a21_array, i))

array.set(combined_array, i + (40 * 21), array.get(a22_array, i))

array.set(combined_array, i + (40 * 22), array.get(a23_array, i))

array.set(combined_array, i + (40 * 23), array.get(a24_array, i))

array.set(combined_array, i + (40 * 24), array.get(a25_array, i))

array.set(combined_array, i + (40 * 25), array.get(a26_array, i))

array.set(combined_array, i + (40 * 26), array.get(a27_array, i))

array.set(combined_array, i + (40 * 27), array.get(a28_array, i))

array.set(combined_array, i + (40 * 28), array.get(a29_array, i))

array.set(combined_array, i + (40 * 29), array.get(a30_array, i))

array.set(combined_array, i + (40 * 30), array.get(a31_array, i))

array.set(combined_array, i + (40 * 31), array.get(a32_array, i))

array.set(combined_array, i + (40 * 32), array.get(a33_array, i))

array.set(combined_array, i + (40 * 33), array.get(a34_array, i))

array.set(combined_array, i + (40 * 34), array.get(a35_array, i))

array.set(combined_array, i + (40 * 35), array.get(a36_array, i))

array.set(combined_array, i + (40 * 36), array.get(a37_array, i))

array.set(combined_array, i + (40 * 37), array.get(a38_array, i))

array.set(combined_array, i + (40 * 38), array.get(a39_array, i))

array.set(combined_array, i + (40 * 39), array.get(a40_array, i))

Calculating Sums: A separate array_sums is created to store the total score for each asset by summing the values of their respective score arrays. This allows for easy comparison of overall performance.

Ranking Assets: The final part of the code ranks the assets based on their total scores stored in array_sums. It assigns a rank to each asset, where the asset with the highest score receives the highest rank.

// create array for asset RANK based on array.sum

var ranks = array.new_int(used_assets, 0)

// for loop that calculates the rank of each asset

if barstate.islast

for i = 0 to (used_assets - 1)

int rank = 1

for x = 0 to (used_assets - 1)

if i != x

if array.get(array_sums, i) < array.get(array_sums, x)

rank := rank + 1

array.set(ranks, i, rank)

Dynamic Table Creation

Initialization: The table is initialized with a base structure that includes headers for asset names, scores, and ranks. The headers are set to remain constant, ensuring clarity for users as they interpret the displayed data.

Data Population: As scores are calculated for each asset, the corresponding values are dynamically inserted into the table. This is achieved through a loop that iterates over the scores and ranks stored in the combined_array and array_sums, respectively.

Automatic Extending Mechanism

Variable Asset Count: The code checks the number of assets defined by the user. Instead of hardcoding the number of rows in the table, it uses a variable to determine the extent of the data that needs to be displayed. This allows the table to expand or contract based on the number of assets being analyzed.

Dynamic Row Generation: Within the loop that populates the table, the code appends new rows for each asset based on the current asset count. The structure of each row includes the asset name, its score, and its rank, ensuring that the table remains consistent regardless of how many assets are involved.

// Automatically extending table based on the number of used assets

var table table = table.new(position.bottom_center, 50, 50, color.new(color.black, 100), color.white, 3, color.white, 1)

if barstate.islast

if not hide_head

table.cell(table, 0, 0, "Universal Ratio Trend Matrix", text_color = color.white, bgcolor = #010c3b, text_size = fontSize)

table.merge_cells(table, 0, 0, used_assets + 3, 0)

if not hide_inps

table.cell(table, 0, 1,

text = "Inputs: You are using " + str.tostring(trend_indicator) + ", which takes: " + str.tostring(f_get_input(trend_indicator)),

text_color = color.white, text_size = fontSize), table.merge_cells(table, 0, 1, used_assets + 3, 1)

table.cell(table, 0, 2, "Assets", text_color = color.white, text_size = fontSize, bgcolor = #010c3b)

for x = 0 to (used_assets - 1)

table.cell(table, x + 1, 2, text = str.tostring(array.get(assets, x)), text_color = color.white, bgcolor = #010c3b, text_size = fontSize)

table.cell(table, 0, x + 3, text = str.tostring(array.get(assets, x)), text_color = color.white, bgcolor = f_asset_col(array.get(ranks, x)), text_size = fontSize)

for r = 0 to (used_assets - 1)

for c = 0 to (used_assets - 1)

table.cell(table, c + 1, r + 3, text = str.tostring(array.get(combined_array, c + (r * 40))),

text_color = hl_type == "Text" ? f_get_col(array.get(combined_array, c + (r * 40))) : color.white, text_size = fontSize,

bgcolor = hl_type == "Background" ? f_get_col(array.get(combined_array, c + (r * 40))) : na)

for x = 0 to (used_assets - 1)

table.cell(table, x + 1, x + 3, "", bgcolor = #010c3b)

table.cell(table, used_assets + 1, 2, "", bgcolor = #010c3b)

for x = 0 to (used_assets - 1)

table.cell(table, used_assets + 1, x + 3, "==>", text_color = color.white)

table.cell(table, used_assets + 2, 2, "SUM", text_color = color.white, text_size = fontSize, bgcolor = #010c3b)

table.cell(table, used_assets + 3, 2, "RANK", text_color = color.white, text_size = fontSize, bgcolor = #010c3b)

for x = 0 to (used_assets - 1)

table.cell(table, used_assets + 2, x + 3,

text = str.tostring(array.get(array_sums, x)),

text_color = color.white, text_size = fontSize,

bgcolor = f_highlight_sum(array.get(array_sums, x), array.get(ranks, x)))

table.cell(table, used_assets + 3, x + 3,

text = str.tostring(array.get(ranks, x)),

text_color = color.white, text_size = fontSize,

bgcolor = f_highlight_rank(array.get(ranks, x)))

Multiple ATR Lines with Current Price PercentageThis indicator plots multiple lines based on the Average True Range (ATR) on the chart, helping traders identify potential support and resistance levels. Specifically, it draws three lines above the price and three lines below the price at different multiples of the ATR. Additionally, it plots a dynamic line at the current price level, which shows how much percentage of the ATR the current price has traveled from a specific point.

How it works:

ATR-Based Lines: The indicator calculates three upper and three lower levels based on the ATR of the selected period. These levels represent 1x, 2x, and 3x ATR above and below the current price.

Current Price Line: A dotted line follows the current price, displaying the percentage of the ATR that the price has moved.

Labels: Each line is labeled with its respective ATR multiple (1x ATR, 2x ATR, 3x ATR), and the current price line shows the percentage of the ATR traveled.

Use Cases:

Identifying Market Volatility: Traders can use this indicator to see how far the price has moved relative to its average volatility.

Support and Resistance Levels: The ATR lines can be treated as potential support and resistance zones, providing insight into price targets or stop-loss placement.

Dynamic Tracking: The percentage of ATR traveled helps traders understand the market momentum relative to its historical volatility.

Settings:

ATR Length: The user can adjust the length of the ATR calculation period.

ATR Multiplier: A multiplier to adjust the distance of the lines relative to the ATR.

Advantages:

Clear visualization of market volatility through ATR-based levels.

Real-time tracking of the price’s movement relative to ATR, giving traders a better understanding of price action.

Customizable settings for different trading styles.

Autotable█ OVERVIEW

The library allows to automatically draw a table based on a string or float matrix (or both) controlling all of the parameters of the table (including merging cells) with parameter matrices (like, e.g. matrix of cell colors).

All things you would normally do with table.new() and table.cell() are now possible using respective parameters of library's main function, autotable() (as explained further below).

Headers can be supplied as arrays.

Merging of the cells is controlled with a special matrix of "L" and "U" values which instruct a cell to merged with the cell to the left or upwards (please see examples in the script and in this description).

█ USAGE EXAMPLES

The simplest and most straightforward:

mxF = matrix.new(3,3, 3.14)

mxF.autotable(bgcolor = color.rgb(249, 209, 29)) // displays float matrix as a table in the top right corner with defalult settings

mxS = matrix.new(3,3,"PI")

// displays string matrix as a table in the top right corner with defalult settings

mxS.autotable(Ypos = "bottom", Xpos = "right", bgcolor = #b4d400)

// displays matrix displaying a string value over a float value in each cell

mxS.autotable(mxF, Ypos = "middle", Xpos = "center", bgcolor = color.gray, text_color = #86f62a)

Draws this:

Tables with headers:

if barstate.islast

mxF = matrix.new(3,3, 3.14)

mxS = matrix.new(3,3,"PI")

arColHeaders = array.from("Col1", "Col2", "Col3")

arRowHeaders = array.from("Row1", "Row2", "Row3")

// float matrix with col headers

mxF.autotable(

bgcolor = #fdfd6b

, arColHeaders = arColHeaders

)

// string matrix with row headers

mxS.autotable(arRowHeaders = arRowHeaders, Ypos = "bottom", Xpos = "right", bgcolor = #b4d400)

// string/float matrix with both row and column headers

mxS.autotable(mxF

, Ypos = "middle", Xpos = "center"

, arRowHeaders = arRowHeaders

, arColHeaders = arColHeaders

, cornerBgClr = #707070, cornerTitle = "Corner\ncell", cornerTxtClr = #ffdc13

, bgcolor = color.gray, text_color = #86f62a

)

Draws this:

█ FUNCTIONS

One main function is autotable() which has only one required argument mxValS, a string matrix.

Please see below the description of all of the function parameters:

The table:

tbl (table) (Optional) If supplied, this table will be deleted.

The data:

mxValS (matrix ) (Required) Cell text values

mxValF (matrix) (Optional) Numerical part of cell text values. Is concatenated to the mxValS values via `string_float_separator` string (default "\n")

Table properties, have same effect as in table.new() :

defaultBgColor (color) (Optional) bgcolor to be used if mxBgColor is not supplied

Ypos (string) (Optional) "top", "bottom" or "center"

Xpos (string) (Optional) "left", "right", or "center"

frame_color (color) (Optional) frame_color like in table.new()

frame_width (int) (Optional) frame_width like in table.new()

border_color (color) (Optional) border_color like in table.new()

border_width (int) (Optional) border_width like in table.new()

force_overlay (simple bool) (Optional) If true draws table on main pane.

Cell parameters, have same effect as in table.cell() ):

mxBgColor (matrix) (Optional) like bgcolor argument in table.cell()

mxTextColor (matrix) (Optional) like text_color argument in table.cell()

mxTt (matrix) (Optional) like tooltip argument in table.cell()

mxWidth (matrix) (Optional) like width argument in table.cell()

mxHeight (matrix) (Optional) like height argument in table.cell()

mxHalign (matrix) (Optional) like text_halign argument in table.cell()

mxValign (matrix) (Optional) like text_valign argument in table.cell()

mxTextSize (matrix) (Optional) like text_size argument in table.cell()

mxFontFamily (matrix) (Optional) like text_font_family argument in table.cell()

Other table properties:

tableWidth (float) (Optional) Overrides table width if cell widths are non zero. E.g. if there are four columns and cell widths are 20 (either as set via cellW or via mxWidth) then if tableWidth is set to e.g. 50 then cell widths will be 50 * (20 / 80), where 80 is 20*4 = total width of all cells. Works simialar for widths set via mxWidth - determines max sum of widths across all cloumns of mxWidth and adjusts cell widths proportionally to it. If cell widths are 0 (i.e. auto-adjust) tableWidth has no effect.

tableHeight (float) (Optional) Overrides table height if cell heights are non zero. E.g. if there are four rows and cell heights are 20 (either as set via cellH or via mxHeight) then if tableHeigh is set to e.g. 50 then cell heights will be 50 * (20 / 80), where 80 is 20*4 = total height of all cells. Works simialar for heights set via mxHeight - determines max sum of heights across all cloumns of mxHeight and adjusts cell heights proportionally to it. If cell heights are 0 (i.e. auto-adjust) tableHeight has no effect.

defaultTxtColor (color) (Optional) text_color to be used if mxTextColor is not supplied

text_size (string) (Optional) text_size to be used if mxTextSize is not supplied

font_family (string) (Optional) cell text_font_family value to be used if a value in mxFontFamily is no supplied

cellW (float) (Optional) cell width to be used if a value in mxWidth is no supplied

cellH (float) (Optional) cell height to be used if a value in mxHeight is no supplied

halign (string) (Optional) cell text_halign value to be used if a value in mxHalign is no supplied

valign (string) (Optional) cell text_valign value to be used if a value in mxValign is no supplied

Headers parameters:

arColTitles (array) (Optional) Array of column titles. If not na a header row is added.

arRowTitles (array) (Optional) Array of row titles. If not na a header column is added.

cornerTitle (string) (Optional) If both row and column titles are supplied allows to set the value of the corner cell.

colTitlesBgColor (color) (Optional) bgcolor for header row

colTitlesTxtColor (color) (Optional) text_color for header row

rowTitlesBgColor (color) (Optional) bgcolor for header column

rowTitlesTxtColor (color) (Optional) text_color for header column

cornerBgClr (color) (Optional) bgcolor for the corner cell

cornerTxtClr (color) (Optional) text_color for the corner cell

Cell merge parameters: