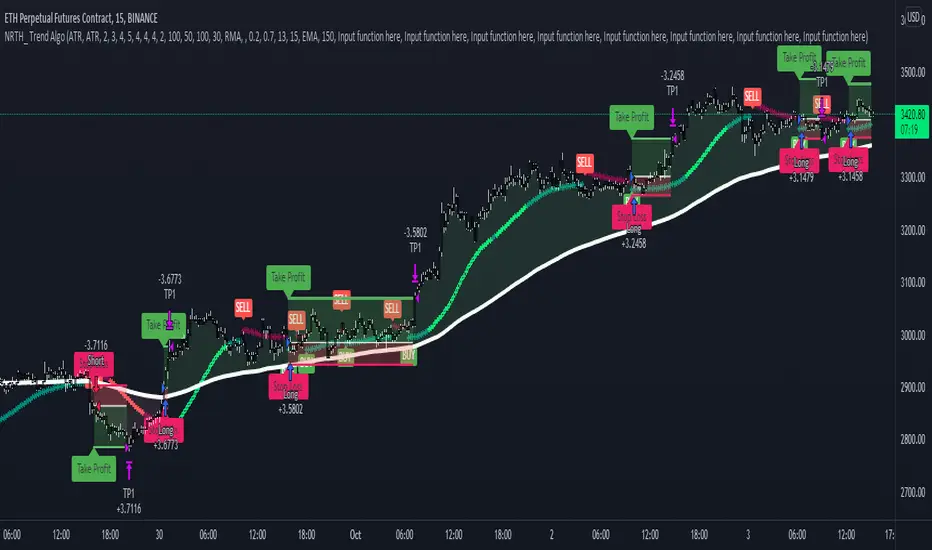

Trend AlgoA NRTH_ Premium Momentum Based Strategy

Comes included with the Premium Package.

Indicator features

Built-In Alerts

Visual Risk Management

Customizable Entry Rules

Usage Tips

This strategy works on timeframes as low as 5m, great for scalping or day trading.

The algo identifies price momentum with strict entry signal settings (can be made more or less sensitive).

Works for all markets with the ability to customize to your liking.

Backtesting Results Info

Period 1/1/2021-1/10/2021

Entry value at $1000 with 10x leverage

Binance standard taker fee rate (0.04%)

ATR Exits : 1:2 RR

-------------------------------------------

Disclaimer

Copyright NRTH_ Indicators 2021.

NRTH_ and all affiliated parties are not registered as financial advisors. The products & services NRTH_ offers are for educational purposes only and should not be construed as financial advice. You must be aware of the risks and be willing to bear any level of risk to invest in financial markets. Past performance is not necessarily indicative of future results. NRTH_ and all individuals associated assume no responsibility for your trading results or investments.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Buscar en scripts para "algo"

Pullback AlgoFlagship NRTH_ Premium Strategy

Comes included with the Essentials or Premium Package.

Indicator features

Built-In Alerts

Visual Risk Management

Customizable Entry Rules

Usage Tips

This strategy is designed for Swing Trading and Intra-Day timeframes (1hr+)

The algo targets pullbacks in an up or down-trending scenario allowing for multiple entries in a strong trending market.

Works for all markets with the ability to customize to your liking.

Backtesting Results Info

Period 1/1/2021-1/10/2021

Entry value at $1000 with 10x leverage

Binance standard taker fee rate (0.04%)

ATR Exits : 1:2 RR

-------------------------------------------

Disclaimer

Copyright NRTH_ Indicators 2021.

NRTH_ and all affiliated parties are not registered as financial advisors. The products & services NRTH_ offers are for educational purposes only and should not be construed as financial advice. You must be aware of the risks and be willing to bear any level of risk to invest in financial markets. Past performance is not necessarily indicative of future results. NRTH_ and all individuals associated assume no responsibility for your trading results or investments.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

BKN: Thick Cut StrategyThick Cut is the juiciest BKN yet. This indicator is created to take a profitable trading strategy and turn it into an automated system. We've built in several pieces that professional traders use every day and turned it into an algo that produces on timeframes as low as 1, 3, and 5 minutes!

Limit Order Entries: When criteria is met, an alert is signaled that will send a value to enter a position at a limit price.

Built in Stop Loss: A stop is built in and the value can be sent to your bot using the {{plot}} function or you can rely on a TradingView alert when the stop is hit.

Built in Take Profits: We've built in two separate take profits and the ability to move your stop loss to breakeven after the first take profit is hit. Even if you take 50% profit at 1R and move your stop loss, you already have a profitable trade. Test results show 50% profits at 2R and the remainder at higher returns result in exceptional results.

Position Sizing: We've built in a position size based on your own predetermined risk. Want to risk $100 per trade? Great, put in 100 in the inputs and reference a quantity of {{plot("Position Size")}} in your alert to send a position size to the bot. You can also reference {{plot("Partial Close")}} to pull 50% of the position size closing 50% at TP1 and 50% at TP2.

Backtest results shown are very short term since we are viewing a 15m chart. This can be a profitable strategy on many timeframes, but lower timeframes will maximize results.

A unique script with incredible results. Further forward testing is live.

***IMPORTANT***

For access, please do not comment below. Comments here will not be replied to. Please send a DM here or on my linked Twitter. At this time, this strategy is considered a Beta release as we continue to fine tune settings and more. Expecting 2 weeks of beta with official release around June 6.

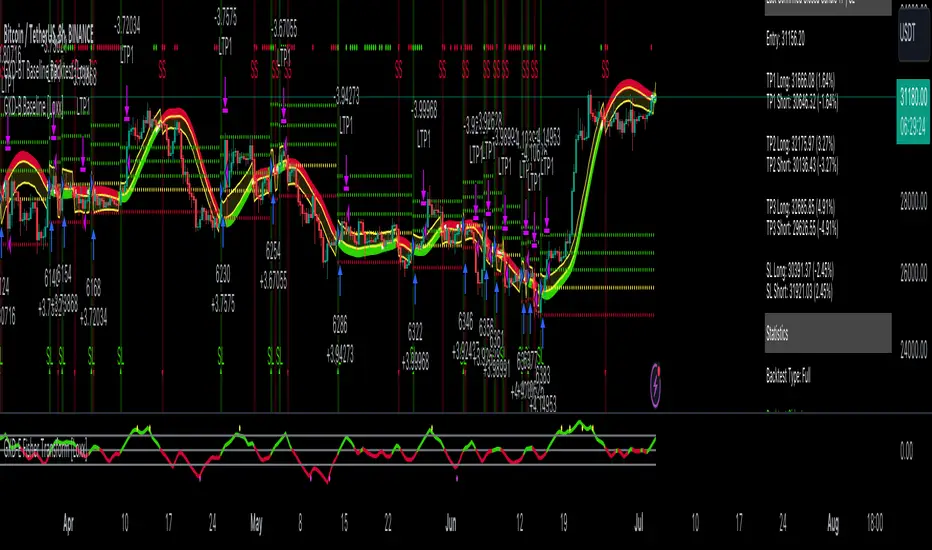

BKN: MapleThis strategy is tied to the BKN: Maple indicator which is an automation ready algo for entering/exiting trades. The script comes prepared with a stop loss and trailing stop loss so that you don't have to host your stop on the exchange and can also optimize trade entries and exits.

We've released optimizations for Forex and Crypto on multiple timeframes, but the script shines on the one and four hour charts.

***IMPORTANT***

For access, please do not comment below. Access requests in the comments will not be responded to.

Instead, please send a DM or reach out to my linked Twitter account.

BlackPika XBTUSD Algo StrategyThis is a strategy script to the "BlackPika XBTUSD Algo" with Take Profit and Stop Loss features.

Easy to backtest. Enjoy

AK_ TREND ID AS A STRATEGY : FOR EDUCATIONAL PURPOSES ONLYJust converted the AK_ TREND ID into a strategy , to show the efficiency of this simple indicator. I used SPX in this example, to display that the indicator has been accurate for a long time.

ALGO 3h, 1h, 2hThis script tracks the crossing of the 10EMA on the 3h timeframe and the 200EMA on the 1h timeframe to open LONGS and SHORTS. Whether those LONGS or SHORTS actually trigger is based on the first 2 EMA's position in relation to a 3rd "controller" EMA.

Guided144Algorithm conditions suggested by a friend, works best on daily tf for bitcoin.

simple cycle trading of buy and sell..

A great guide for trading those complicated moves.

Reversal Point Dynamics - Machine Learning⇋ Reversal Point Dynamics - Machine Learning

RPD Machine Learning: Self-Adaptive Multi-Armed Bandit Trading System

RPD Machine Learning is an advanced algorithmic trading system that implements genuine machine learning through contextual multi-armed bandits, reinforcement learning, and online adaptation. Unlike traditional indicators that use fixed rules, RPD learns from every trade outcome , automatically discovers which strategies work in current market conditions, and continuously adapts without manual intervention .

Core Innovation: The system deploys six distinct trading policies (ranging from aggressive trend-following to conservative range-bound strategies) and uses LinUCB contextual bandit algorithms with Random Fourier Features to learn which policy performs best in each market regime. After the initial learning phase (50-100 trades), the system achieves autonomous adaptation , automatically shifting between policies as market conditions evolve.

Target Users: Quantitative traders, algorithmic trading developers, systematic traders, and data-driven investors who want a system that adapts over time . Suitable for stocks, futures, forex, and cryptocurrency on any liquid instrument with >100k daily volume.

The Problem This System Solves

Traditional Technical Analysis Limitations

Most trading systems suffer from three fundamental challenges :

Fixed Parameters: Static settings (like "buy when RSI < 30") work well in backtests but may struggle when markets change character. What worked in low-volatility environments may not work in high-volatility regimes.

Strategy Degradation: Manual optimization (curve-fitting) produces systems that perform well on historical data but may underperform in live trading. The system never adapts to new market conditions.

Cognitive Overload: Running multiple strategies simultaneously forces traders to manually decide which one to trust. This leads to hesitation, late entries, and inconsistent execution.

How RPD Machine Learning Addresses These Challenges

Automated Strategy Selection: Instead of requiring you to choose between trend-following and mean-reversion strategies, RPD runs all six policies simultaneously and uses machine learning to automatically select the best one for current conditions. The decision happens algorithmically, removing human hesitation.

Continuous Learning: After every trade, the system updates its understanding of which policies are working. If the market shifts from trending to ranging, RPD automatically detects this through changing performance patterns and adjusts selection accordingly.

Context-Aware Decisions: Unlike simple voting systems that treat all conditions equally, RPD analyzes market context (ADX regime, entropy levels, volatility state, volume patterns, time of day, historical performance) and learns which combinations of context features correlate with policy success.

Machine Learning Architecture: What Makes This "Real" ML

Component 1: Contextual Multi-Armed Bandits (LinUCB)

What Is a Multi-Armed Bandit Problem?

Imagine facing six slot machines, each with unknown payout rates. The exploration-exploitation dilemma asks: Should you keep pulling the machine that's worked well (exploitation) or try others that might be better (exploration)? RPD solves this for trading policies.

Academic Foundation:

RPD implements Linear Upper Confidence Bound (LinUCB) from the research paper "A Contextual-Bandit Approach to Personalized News Article Recommendation" (Li et al., 2010, WWW Conference). This algorithm is used in content recommendation and ad placement systems.

How It Works:

Each policy (AggressiveTrend, ConservativeRange, VolatilityBreakout, etc.) is treated as an "arm." The system maintains:

Reward History: Tracks wins/losses for each policy

Contextual Features: Current market state (8-10 features including ADX, entropy, volatility, volume)

Uncertainty Estimates: Confidence in each policy's performance

UCB Formula: predicted_reward + α × uncertainty

The system selects the policy with highest UCB score , balancing proven performance (predicted_reward) with potential for discovery (uncertainty bonus). Initially, all policies have high uncertainty, so the system explores broadly. After 50-100 trades, uncertainty decreases, and the system focuses on known-performing policies.

Why This Matters:

Traditional systems pick strategies based on historical backtests or user preference. RPD learns from actual outcomes in your specific market, on your timeframe, with your execution characteristics.

Component 2: Random Fourier Features (RFF)

The Non-Linearity Challenge:

Market relationships are often non-linear. High ADX may indicate favorable conditions when volatility is normal, but unfavorable when volatility spikes. Simple linear models struggle to capture these interactions.

Academic Foundation:

RPD implements Random Fourier Features from "Random Features for Large-Scale Kernel Machines" (Rahimi & Recht, 2007, NIPS). This technique approximates kernel methods (like Support Vector Machines) while maintaining computational efficiency for real-time trading.

How It Works:

The system transforms base features (ADX, entropy, volatility, etc.) into a higher-dimensional space using random projections and cosine transformations:

Input: 8 base features

Projection: Through random Gaussian weights

Transformation: cos(W×features + b)

Output: 16 RFF dimensions

This allows the bandit to learn non-linear relationships between market context and policy success. For example: "AggressiveTrend performs well when ADX >25 AND entropy <0.6 AND hour >9" becomes naturally encoded in the RFF space.

Why This Matters:

Without RFF, the system could only learn "this policy has X% historical performance." With RFF, it learns "this policy performs differently in these specific contexts" - enabling more nuanced selection.

Component 3: Reinforcement Learning Stack

Beyond bandits, RPD implements a complete RL framework :

Q-Learning: Value-based RL that learns state-action values. Maps 54 discrete market states (trend×volatility×RSI×volume combinations) to 5 actions (4 policies + no-trade). Updates via Bellman equation after each trade. Converges toward optimal policy after 100-200 trades.

TD(λ) with Eligibility Traces: Extension of Q-Learning that propagates credit backwards through time . When a trade produces an outcome, TD(λ) updates not just the final state-action but all states visited during the trade, weighted by eligibility decay (λ=0.90). This accelerates learning from multi-bar trades.

Policy Gradient (REINFORCE): Learns a stochastic policy directly from 12 continuous market features without discretization. Uses gradient ascent to increase probability of actions that led to positive outcomes. Includes baseline (average reward) for variance reduction.

Meta-Learning: The system learns how to learn by adapting its own learning rates based on feature stability and correlation with outcomes. If a feature (like volume ratio) consistently correlates with success, its learning rate increases. If unstable, rate decreases.

Why This Matters:

Q-Learning provides fast discrete decisions. Policy Gradient handles continuous features. TD(λ) accelerates learning. Meta-learning optimizes the optimization. Together, they create a robust, multi-approach learning system that adapts more quickly than any single algorithm.

Component 4: Policy Momentum Tracking (v2 Feature)

The Recency Challenge:

Standard bandits treat all historical data equally. If a policy performed well historically but struggles in current conditions due to regime shift, the system may be slow to adapt because historical success outweighs recent underperformance.

RPD's Solution:

Each policy maintains a ring buffer of the last 10 outcomes. The system calculates:

Momentum: recent_win_rate - global_win_rate (range: -1 to +1)

Confidence: consistency of recent results (1 - variance)

Policies with positive momentum (recent outperformance) get an exploration bonus. Policies with negative momentum and high confidence (consistent recent underperformance) receive a selection penalty.

Effect: When markets shift, the system detects the shift more quickly through momentum tracking, enabling faster adaptation than standard bandits.

Signal Generation: The Core Algorithm

Multi-Timeframe Fractal Detection

RPD identifies reversal points using three complementary methods :

1. Quantum State Analysis:

Divides price range into discrete states (default: 6 levels)

Peak signals require price in top states (≥ state 5)

Valley signals require price in bottom states (≤ state 1)

Prevents mid-range signals that may struggle in strong trends

2. Fractal Geometry:

Identifies swing highs/lows using configurable fractal strength

Confirms local extremum with neighboring bars

Validates reversal only if price crosses prior extreme

3. Multi-Timeframe Confirmation:

Analyzes higher timeframe (4× default) for alignment

MTF confirmation adds probability bonus

Designed to reduce false signals while preserving valid setups

Probability Scoring System

Each signal receives a dynamic probability score (40-99%) based on:

Base Components:

Trend Strength: EMA(velocity) / ATR × 30 points

Entropy Quality: (1 - entropy) × 10 points

Starting baseline: 40 points

Enhancement Bonuses:

Divergence Detection: +20 points (price/momentum divergence)

RSI Extremes: +8 points (RSI >65 for peaks, <40 for valleys)

Volume Confirmation: +5 points (volume >1.2× average)

Adaptive Momentum: +10 points (strong directional velocity)

MTF Alignment: +12 points (higher timeframe confirms)

Range Factor: (high-low)/ATR × 3 - 1.5 points (volatility adjustment)

Regime Bonus: +8 points (trending ADX >25 with directional agreement)

Penalties:

High Entropy: -5 points (entropy >0.85, chaotic price action)

Consolidation Regime: -10 points (ADX <20, no directional conviction)

Final Score: Clamped to 40-99% range, classified as ELITE (>85%), STRONG (75-85%), GOOD (65-75%), or FAIR (<65%)

Entropy-Based Quality Filter

What Is Entropy?

Entropy measures randomness in price changes . Low entropy indicates orderly, directional moves. High entropy indicates chaotic, unpredictable conditions.

Calculation:

Count up/down price changes over adaptive period

Calculate probability: p = ups / total_changes

Shannon entropy: -p×log(p) - (1-p)×log(1-p)

Normalized to 0-1 range

Application:

Entropy <0.5: Highly ordered (ELITE signals possible)

Entropy 0.5-0.75: Mixed (GOOD signals)

Entropy >0.85: Chaotic (signals blocked or heavily penalized)

Why This Matters:

Prevents trading during choppy, news-driven conditions where technical patterns may be less reliable. Automatically raises quality bar when market is unpredictable.

Regime Detection & Market Microstructure - ADX-Based Regime Classification

RPD uses Wilder's Average Directional Index to classify markets:

Bull Trend: ADX >25, +DI > -DI (directional conviction bullish)

Bear Trend: ADX >25, +DI < -DI (directional conviction bearish)

Consolidation: ADX <20 (no directional conviction)

Transitional: ADX 20-25 (forming direction, ambiguous)

Filter Logic:

Blocks all signals during Transitional regime (avoids trading during uncertain conditions)

Blocks Consolidation signals unless ADX ≥ Min Trend Strength

Adds probability bonus during strong trends (ADX >30)

Effect: Designed to reduce signal frequency while focusing on higher-quality setups.

Divergence Detection

Bearish Divergence:

Price makes higher high

Velocity (price momentum) makes lower high

Indicates weakening upward pressure → SHORT signal quality boost

Bullish Divergence:

Price makes lower low

Velocity makes higher low

Indicates weakening downward pressure → LONG signal quality boost

Bonus: Adds probability points and additional acceleration factor. Divergence signals have historically shown higher success rates in testing.

Hierarchical Policy System - The Six Trading Policies

1. AggressiveTrend (Policy 0):

Probability Threshold: 60% (trades more frequently)

Entropy Threshold: 0.70 (tolerates moderate chaos)

Stop Multiplier: 2.5× ATR (wider stops for trends)

Target Multiplier: 5.0R (larger targets)

Entry Mode: Pyramid (scales into winners)

Best For: Strong trending markets, breakouts, momentum continuation

2. ConservativeRange (Policy 1):

Probability Threshold: 75% (more selective)

Entropy Threshold: 0.60 (requires order)

Stop Multiplier: 1.8× ATR (tighter stops)

Target Multiplier: 3.0R (modest targets)

Entry Mode: Single (one-shot entries)

Best For: Range-bound markets, low volatility, mean reversion

3. VolatilityBreakout (Policy 2):

Probability Threshold: 65% (moderate)

Entropy Threshold: 0.80 (accepts high entropy)

Stop Multiplier: 3.0× ATR (wider stops)

Target Multiplier: 6.0R (larger targets)

Entry Mode: Tiered (splits entry)

Best For: Compression breakouts, post-consolidation moves, gap opens

4. EntropyScalp (Policy 3):

Probability Threshold: 80% (very selective)

Entropy Threshold: 0.40 (requires extreme order)

Stop Multiplier: 1.5× ATR (tightest stops)

Target Multiplier: 2.5R (quick targets)

Entry Mode: Single

Best For: Low-volatility grinding moves, tight ranges, highly predictable patterns

5. DivergenceHunter (Policy 4):

Probability Threshold: 70% (quality-focused)

Entropy Threshold: 0.65 (balanced)

Stop Multiplier: 2.2× ATR (moderate stops)

Target Multiplier: 4.5R (balanced targets)

Entry Mode: Tiered

Best For: Divergence-confirmed reversals, exhaustion moves, trend climax

6. AdaptiveBlend (Policy 5):

Probability Threshold: 68% (balanced)

Entropy Threshold: 0.75 (balanced)

Stop Multiplier: 2.0× ATR (standard)

Target Multiplier: 4.0R (standard)

Entry Mode: Single

Best For: Mixed conditions, general trading, fallback when no clear regime

Policy Clustering (Advanced/Extreme Modes)

Policies are grouped into three clusters based on regime affinity:

Cluster 1 (Trending): AggressiveTrend, DivergenceHunter

High regime affinity (0.8): Performs well when ADX >25

Moderate vol affinity (0.6): Works in various volatility

Cluster 2 (Ranging): ConservativeRange, AdaptiveBlend

Low regime affinity (0.3): Better suited for ADX <20

Low vol affinity (0.4): Optimized for calm markets

Cluster 3 (Breakout): VolatilityBreakout

Moderate regime affinity (0.6): Works in multiple regimes

High vol affinity (0.9): Requires high volatility for optimal characteristics

Hierarchical Selection Process:

Calculate cluster scores based on current regime and volatility

Select best-matching cluster

Run UCB selection within chosen cluster

Apply momentum boost/penalty

This two-stage process reduces learning time - instead of choosing among 6 policies from scratch, system first narrows to 1-2 policies per cluster, then optimizes within cluster.

Risk Management & Position Sizing

Dynamic Kelly Criterion Sizing (Optional)

Traditional Fixed Sizing Challenge:

Using the same position size for all signal probabilities may be suboptimal. Higher-probability signals could justify larger positions, lower-probability signals smaller positions.

Kelly Formula:

f = (p × b - q) / b

Where:

p = win probability (from signal score)

q = loss probability (1 - p)

b = win/loss ratio (average_win / average_loss)

f = fraction of capital to risk

RPD Implementation:

Uses Fractional Kelly (1/4 Kelly default) for safety. Full Kelly is theoretically optimal but can recommend large position sizes. Fractional Kelly reduces volatility while maintaining adaptive sizing benefits.

Enhancements:

Probability Bonus: Normalize(prob, 65, 95) × 0.5 multiplier

Divergence Bonus: Additional sizing on divergence signals

Regime Bonus: Additional sizing during strong trends (ADX >30)

Momentum Adjustment: Hot policies receive sizing boost, cold policies receive reduction

Safety Rails:

Minimum: 1 contract (floor)

Maximum: User-defined cap (default 10 contracts)

Portfolio Heat: Max total risk across all positions (default 4% equity)

Multi-Mode Stop Loss System

ATR Mode (Default):

Stop = entry ± (ATR × base_mult × policy_mult)

Consistent risk sizing

Ignores market structure

Best for: Futures, forex, algorithmic trading

Structural Mode:

Finds swing low (long) or high (short) over last 20 bars

Identifies fractal pivots within lookback

Places stop below/above structure + buffer (0.1× ATR)

Best for: Stocks, instruments that respect structure

Hybrid Mode (Intelligent):

Attempts structural stop first

Falls back to ATR if:

Structural level is invalid (beyond entry)

Structural stop >2× ATR away (too wide)

Best for: Mixed instruments, adaptability

Dynamic Adjustments:

Breakeven: Move stop to entry + 1 tick after 1.0R profit

Trailing: Trail stop 0.8R behind price after 1.5R profit

Timeout: Force close after 30 bars (optional)

Tiered Entry System

Challenge: Equal sizing on all signals may not optimize capital allocation relative to signal quality.

Solution:

Tier 1 (40% of size): Enters immediately on all signals

Tier 2 (60% of size): Enters only if probability ≥ Tier 2 trigger (default 75%)

Example:

Calculated optimal size: 10 contracts

Signal probability: 72%

Tier 2 trigger: 75%

Result: Enter 4 contracts only (Tier 1)

Same signal at 80% probability

Result: Enter 10 contracts (4 Tier 1 + 6 Tier 2)

Effect: Automatically scales size to signal quality, optimizing capital allocation.

Performance Optimization & Learning Curve

Warmup Phase (First 50 Trades)

Purpose: Ensure all policies get tested before system focuses on preferred strategies.

Modifications During Warmup:

Probability thresholds reduced 20% (65% becomes 52%)

Entropy thresholds increased 20% (more permissive)

Exploration rate stays high (30%)

Confidence width (α) doubled (more exploration)

Why This Matters:

Without warmup, system might commit to early-performing policy without testing alternatives. Warmup forces thorough exploration before focusing on best-performing strategies.

Curriculum Learning

Phase 1 (Trades 1-50): Exploration

Warmup active

All policies tested

High exploration (30%)

Learning fundamental patterns

Phase 2 (Trades 50-100): Refinement

Warmup ended, thresholds normalize

Exploration decaying (30% → 15%)

Policy preferences emerging

Meta-learning optimizing

Phase 3 (Trades 100-200): Specialization

Exploration low (15% → 8%)

Clear policy preferences established

Momentum tracking fully active

System focusing on learned patterns

Phase 4 (Trades 200+): Maturity

Exploration minimal (8% → 5%)

Regime-policy relationships learned

Auto-adaptation to market shifts

Stable performance expected

Convergence Indicators

System is learning well when:

Policy switch rate decreasing over time (initially ~50%, should drop to <20%)

Exploration rate decaying smoothly (30% → 5%)

One or two policies emerge with >50% selection frequency

Performance metrics stabilizing over time

Consistent behavior in similar market conditions

System may need adjustment when:

Policy switch rate >40% after 100 trades (excessive exploration)

Exploration rate not decaying (parameter issue)

All policies showing similar selection (not differentiating)

Performance declining despite relaxed thresholds (underlying signal issue)

Highly erratic behavior after learning phase

Advanced Features

Attention Mechanism (Extreme Mode)

Challenge: Not all features are equally important. Trading hour might matter more than price-volume correlation, but standard approaches treat them equally.

Solution:

Each RFF dimension has an importance weight . After each trade:

Calculate correlation: sign(feature - 0.5) × sign(reward)

Update importance: importance += correlation × 0.01

Clamp to range

Effect: Important features get amplified in RFF transformation, less important features get suppressed. System learns which features correlate with successful outcomes.

Temporal Context (Extreme Mode)

Challenge: Current market state alone may be incomplete. Historical context (was volatility rising or falling?) provides additional information.

Solution:

Includes 3-period historical context with exponential decay (0.85):

Current features (weight 1.0)

1 bar ago (weight 0.85)

2 bars ago (weight 0.72)

Effect: Captures momentum and acceleration of market features. System learns patterns like "rising volatility with falling entropy" that may precede significant moves.

Transfer Learning via Episodic Memory

Short-Term Memory (STM):

Last 20 trades

Fast adaptation to immediate regime

High learning rate

Long-Term Memory (LTM):

Condensed historical patterns

Preserved knowledge from past regimes

Low learning rate

Transfer Mechanism:

When STM fills (20 trades), patterns consolidated into LTM . When similar regime recurs later, LTM provides faster adaptation than starting from scratch.

Practical Implementation Guide - Recommended Settings by Instrument

Futures (ES, NQ, CL):

Adaptive Period: 20-25

ML Mode: Advanced

RFF Dimensions: 16

Policies: 6

Base Risk: 1.5%

Stop Mode: ATR or Hybrid

Timeframe: 5-15 min

Forex Majors (EURUSD, GBPUSD):

Adaptive Period: 25-30

ML Mode: Advanced

RFF Dimensions: 16

Policies: 6

Base Risk: 1.0-1.5%

Stop Mode: ATR

Timeframe: 5-30 min

Cryptocurrency (BTC, ETH):

Adaptive Period: 20-25

ML Mode: Extreme (handles non-stationarity)

RFF Dimensions: 32 (captures complexity)

Policies: 6

Base Risk: 1.0% (volatility consideration)

Stop Mode: Hybrid

Timeframe: 15 min - 4 hr

Stocks (Large Cap):

Adaptive Period: 25-30

ML Mode: Advanced

RFF Dimensions: 16

Policies: 5-6

Base Risk: 1.5-2.0%

Stop Mode: Structural or Hybrid

Timeframe: 15 min - Daily

Scaling Strategy

Phase 1 (Testing - First 50 Trades):

Max Contracts: 1-2

Goal: Validate system on your instrument

Monitor: Performance stabilization, learning progress

Phase 2 (Validation - Trades 50-100):

Max Contracts: 2-3

Goal: Confirm learning convergence

Monitor: Policy stability, exploration decay

Phase 3 (Scaling - Trades 100-200):

Max Contracts: 3-5

Enable: Kelly sizing (1/4 Kelly)

Goal: Optimize capital efficiency

Monitor: Risk-adjusted returns

Phase 4 (Full Deployment - Trades 200+):

Max Contracts: 5-10

Enable: Full momentum tracking

Goal: Sustained consistent performance

Monitor: Ongoing adaptation quality

Limitations & Disclaimers

Statistical Limitations

Learning Sample Size: System requires minimum 50-100 trades for basic convergence, 200+ trades for robust learning. Early performance (first 50 trades) may not reflect mature system behavior.

Non-Stationarity Risk: Markets change over time. A system trained on one market regime may need time to adapt when conditions shift (typically 30-50 trades for adjustment).

Overfitting Possibility: With 16-32 RFF dimensions and 6 policies, system has substantial parameter space. Small sample sizes (<200 trades) increase overfitting risk. Mitigated by regularization (λ) and fractional Kelly sizing.

Technical Limitations

Computational Complexity: Extreme mode with 32 RFF dimensions, 6 policies, and full RL stack requires significant computation. May perform slowly on lower-end systems or with many other indicators loaded.

Pine Script Constraints:

No true matrix inversion (uses diagonal approximation for LinUCB)

No cryptographic RNG (uses market data as entropy)

No proper random number generation for RFF (uses deterministic pseudo-random)

These approximations reduce mathematical precision compared to academic implementations but remain functional for trading applications.

Data Requirements: Needs clean OHLCV data. Missing bars, gaps, or low liquidity (<100k daily volume) can degrade signal quality.

Forward-Looking Bias Disclaimer

Reward Calculation Uses Future Data: The RL system evaluates trades using an 8-bar forward-looking window. This means when a position enters at bar 100, the reward calculation considers price movement through bar 108.

Why This is Disclosed:

Entry signals do NOT look ahead - decisions use only data up to entry bar

Forward data used for learning only, not signal generation

In live trading, system learns identically as bars unfold in real-time

Simulates natural learning process (outcomes are only known after trades complete)

Implication: Backtested metrics reflect this 8-bar evaluation window. Live performance may vary if:

- Positions held longer than 8 bars

- Slippage/commissions differ from backtest settings

- Market microstructure changes (wider spreads, different execution quality)

Risk Warnings

No Guarantee of Profit: All trading involves substantial risk of loss. Machine learning systems can fail if market structure fundamentally changes or during unprecedented events.

Maximum Drawdown: With 1.5% base risk and 4% max total risk, expect potential drawdowns. Historical drawdowns do not predict future drawdowns. Extreme market conditions can exceed expectations.

Black Swan Events: System has not been tested under: flash crashes, trading halts, circuit breakers, major geopolitical shocks, or other extreme events. Such events can exceed stop losses and cause significant losses.

Leverage Risk: Futures and forex involve leverage. Adverse moves combined with leverage can result in losses exceeding initial investment. Use appropriate position sizing for your risk tolerance.

System Failures: Code bugs, broker API failures, internet outages, or exchange issues can prevent proper execution. Always monitor automated systems and maintain appropriate safeguards.

Appropriate Use

This System Is:

✅ A machine learning framework for adaptive strategy selection

✅ A signal generation system with probabilistic scoring

✅ A risk management system with dynamic sizing

✅ A learning system designed to adapt over time

This System Is NOT:

❌ A price prediction system (does not forecast exact prices)

❌ A guarantee of profits (can and will experience losses)

❌ A replacement for due diligence (requires monitoring and understanding)

❌ Suitable for complete beginners (requires understanding of ML concepts, risk management, and trading fundamentals)

Recommended Use:

Paper trade for 100 signals before risking capital

Start with minimal position sizing (1-2 contracts) regardless of calculated size

Monitor learning progress via dashboard

Scale gradually over several months only after consistent results

Combine with fundamental analysis and broader market context

Set account-level risk limits (e.g., maximum drawdown threshold)

Never risk more than you can afford to lose

What Makes This System Different

RPD implements academically-derived machine learning algorithms rather than simple mathematical calculations or optimization:

✅ LinUCB Contextual Bandits - Algorithm from WWW 2010 conference (Li et al.)

✅ Random Fourier Features - Kernel approximation from NIPS 2007 (Rahimi & Recht)

✅ Q-Learning, TD(λ), REINFORCE - Standard RL algorithms from Sutton & Barto textbook

✅ Meta-Learning - Learning rate adaptation based on feature correlation

✅ Online Learning - Real-time updates from streaming data

✅ Hierarchical Policies - Two-stage selection with clustering

✅ Momentum Tracking - Recent performance analysis for faster adaptation

✅ Attention Mechanism - Feature importance weighting

✅ Transfer Learning - Episodic memory consolidation

Key Differentiators:

Actually learns from trade outcomes (not just parameter optimization)

Updates model parameters in real-time (true online learning)

Adapts to changing market regimes (not static rules)

Improves over time through reinforcement learning

Implements published ML algorithms with proper citations

Conclusion

RPD Machine Learning represents a different approach from traditional technical analysis to adaptive, self-learning systems . Instead of manually optimizing parameters (which can overfit to historical data), RPD learns behavior patterns from actual trading outcomes in your specific market.

The combination of contextual bandits, reinforcement learning, random fourier features, hierarchical policy selection, and momentum tracking creates a multi-algorithm learning system designed to handle non-stationary markets better than static approaches.

After the initial learning phase (50-100 trades), the system achieves autonomous adaptation - automatically discovering which strategies work in current conditions and shifting allocation without human intervention. This represents an approach where systems adapt over time rather than remaining static.

Use responsibly. Paper trade extensively. Scale gradually. Understand that past performance does not guarantee future results and all trading involves risk of loss.

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

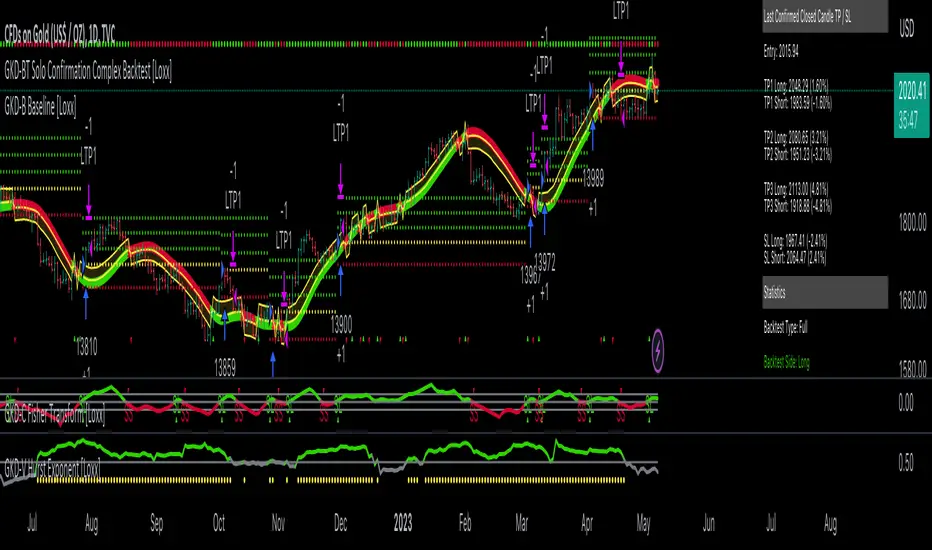

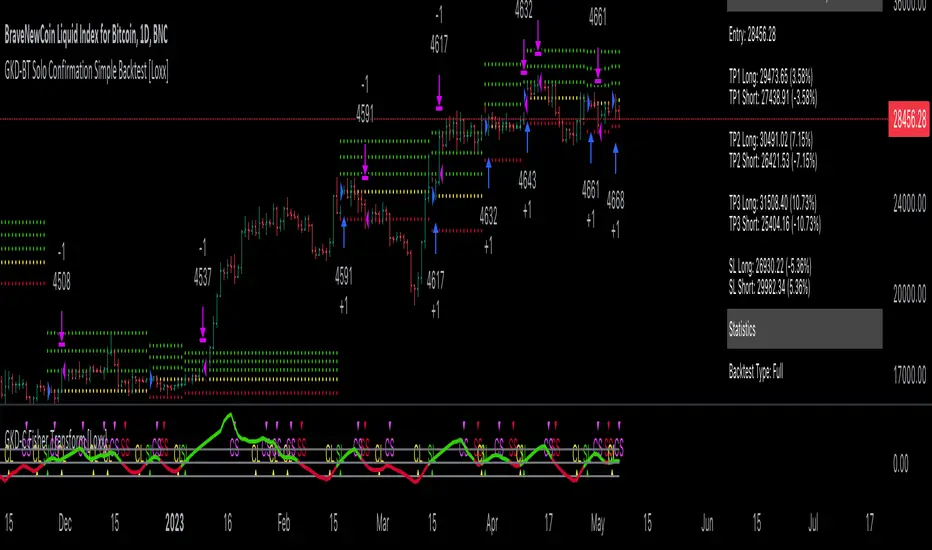

GKD-BT Baseline Backtest [Loxx]The Giga Kaleidoscope GKD-BT Baseline Backtest is a backtesting module included in Loxx's "Giga Kaleidoscope Modularized Trading System."

█ GKD-BT Baseline Backtest

The GKD-BT Baseline Backtest allows traders to backtest the Regular and Stepped baselines used in the GKD trading system. This module includes 65+ moving averages and 15+ types of volatility to choose from.

Additionally, this backtest module provides the option to test the GKD-B indicator with 1 to 3 take profits and 1 stop loss. The Trading backtest allows for the use of 1 to 3 take profits, while the Full backtest is limited to 1 take profit. The Trading backtest also offers the capability to apply a trailing take profit.

In terms of the percentage of trade removed at each take profit, this backtest module has the following hardcoded values:

Take profit 1: 50% of the trade is removed

Take profit 2: 25% of the trade is removed

Take profit 3: 25% of the trade is removed

Stop loss: 100% of the trade is removed

After each take profit is achieved, the stop loss level is adjusted. When take profit 1 is reached, the stop loss is moved to the entry point. Similarly, when take profit 2 is reached, the stop loss is shifted to take profit 1. The trailing take profit feature comes into play after take profit 2 or take profit 3, depending on the number of take profits selected in the settings. The trailing take profit is always activated on the final take profit when 2 or more take profits are chosen.

The backtest also offers the capability to restrict by a specific date range, allowing for simulated forward testing based on past data. Additionally, users have the option to display or hide a trading panel that provides relevant information about the backtest, statistics, and the current trade. It is also possible to activate alerts and toggle sections of the trading panel on or off. On the chart, historical take profit and stop loss levels are represented by horizontal lines overlaid for reference.

This backtest also includes an optional GKD-E Exit indicator that can be used to test early exits.

The GKD system utilizes volatility-based take profits and stop losses. Each take profit and stop loss is calculated as a multiple of volatility. You can change the values of the multipliers in the settings as well.

To utilize this strategy, follow these steps:

1. (Required) Import the value "Input into NEW GKD-BT Backtest" from the GKD-B Baseline indicator into the GKD-BT Baseline Backtest field "Import GKD-B Baseline"

2. (Optional) Import the value "Input into NEW GKD-BT Backtest" from the GKD-E Exit indicator into the GKD-BT Baseline Backtest field "Import GKD-E Exit". You can toggle the Exit on or off using the "Activate GKD-E Exit" option.

Baselines that are compatible with this backtest module:

GKD-B Baseline

GKD-B Stepped Baseline

Volatility Types Included

17 types of volatility are included in this indicator

Close-to-Close

Parkinson

Garman-Klass

Rogers-Satchell

Yang-Zhang

Garman-Klass-Yang-Zhang

Exponential Weighted Moving Average

Standard Deviation of Log Returns

Pseudo GARCH(2,2)

Average True Range

True Range Double

Standard Deviation

Adaptive Deviation

Median Absolute Deviation

Efficiency-Ratio Adaptive ATR

Mean Absolute Deviation

Static Percent

█ Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

8. Metamorphosis - a technical indicator that produces a compound signal from the combination of other GKD indicators*

*(not part of the NNFX algorithm)

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?

Volume indicators, such as the On Balance Volume (OBV), the Chaikin Money Flow (CMF), or the Volume Price Trend (VPT), are used to measure the amount of buying and selling activity in a market. They are based on the trading volume of the market, and can provide information about the strength of the trend. In the NNFX system, volume indicators are used to confirm trading signals generated by the Moving Average and the Relative Strength Index. Volatility indicators include Average Direction Index, Waddah Attar, and Volatility Ratio. In the NNFX trading system, volatility is a proxy for volume and vice versa.

By using volume indicators as confirmation tools, the NNFX trading system aims to reduce the risk of false signals and improve the overall profitability of trades. These indicators can provide additional information about the market that is not captured by the primary indicators, and can help traders to make more informed trading decisions. In addition, volume indicators can be used to identify potential changes in market trends and to confirm the strength of price movements.

What is an Exit indicator?

The exit indicator is used in conjunction with other indicators in the system, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR), to provide a comprehensive trading strategy.

The exit indicator in the NNFX system can be any technical indicator that is deemed effective at identifying optimal exit points. Examples of exit indicators that are commonly used include the Parabolic SAR, the Average Directional Index (ADX), and the Chandelier Exit.

The purpose of the exit indicator is to identify when a trend is likely to reverse or when the market conditions have changed, signaling the need to exit a trade. By using an exit indicator, traders can manage their risk and prevent significant losses.

In the NNFX system, the exit indicator is used in conjunction with a stop loss and a take profit order to maximize profits and minimize losses. The stop loss order is used to limit the amount of loss that can be incurred if the trade goes against the trader, while the take profit order is used to lock in profits when the trade is moving in the trader's favor.

Overall, the use of an exit indicator in the NNFX trading system is an important component of a comprehensive trading strategy. It allows traders to manage their risk effectively and improve the profitability of their trades by exiting at the right time.

What is an Metamorphosis indicator?

The concept of a metamorphosis indicator involves the integration of two or more GKD indicators to generate a compound signal. This is achieved by evaluating the accuracy of each indicator and selecting the signal from the indicator with the highest accuracy. As an illustration, let's consider a scenario where we calculate the accuracy of 10 indicators and choose the signal from the indicator that demonstrates the highest accuracy.

The resulting output from the metamorphosis indicator can then be utilized in a GKD-BT backtest by occupying a slot that aligns with the purpose of the metamorphosis indicator. The slot can be a GKD-B, GKD-C, or GKD-E slot, depending on the specific requirements and objectives of the indicator. This allows for seamless integration and utilization of the compound signal within the GKD-BT framework.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v2.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

6. GKD-M - Metamorphosis module (Metamorphosis, Number 8 in the NNFX algorithm, but not part of the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data to A backtest module wherein the various components of the GKD system are combined to create a trading signal.

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: GKD-BT Baseline Backtest as shown on the chart above

Baseline: Hull Moving Average as shown on the chart above

Volatility/Volume: Hurst Exponent

Confirmation 1: Sherif's HiLo

Confirmation 2: uf2018

Continuation: Coppock Curve

Exit: Fisher Transform as shown on the chart above

Metamorphosis: Baseline Optimizer

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, GKD-M, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD system.

█ Giga Kaleidoscope Modularized Trading System Signals

Standard Entry

1. GKD-C Confirmation gives signal

2. Baseline agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

1-Candle Standard Entry

1a. GKD-C Confirmation gives signal

2a. Baseline agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Baseline Entry

1. GKD-B Baseline gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

7. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

1-Candle Baseline Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Volatility/Volume Entry

1. GKD-V Volatility/Volume gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Volatility/Volume Entry

1a. GKD-V Volatility/Volume gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSVVC Bars Back' prior

Next Candle

1b. Price retraced

2b. Volatility/Volume agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Baseline agrees

Confirmation 2 Entry

1. GKD-C Confirmation 2 gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Volatility/Volume agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Confirmation 2 Entry

1a. GKD-C Confirmation 2 gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSC2C Bars Back' prior

Next Candle

1b. Price retraced

2b. Confirmation 2 agrees

3b. Confirmation 1 agrees

4b. Volatility/Volume agrees

5b. Baseline agrees

PullBack Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price is beyond 1.0x Volatility of Baseline

Next Candle

1b. Price inside Goldie Locks Zone Minimum

2b. Price inside Goldie Locks Zone Maximum

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Continuation Entry

1. Standard Entry, 1-Candle Standard Entry, Baseline Entry, 1-Candle Baseline Entry, Volatility/Volume Entry, 1-Candle Volatility/Volume Entry, Confirmation 2 Entry, 1-Candle Confirmation 2 Entry, or Pullback entry triggered previously

2. Baseline hasn't crossed since entry signal trigger

4. Confirmation 1 agrees

5. Baseline agrees

6. Confirmation 2 agrees

SMC Pro [Stansbooth]

🔮 SMC × Fibonacci Confluence Engine — The Hidden Algorithm of the Markets

Welcome to a level of chart analysis where mathematics , market psychology , and institutional logic merge into one ultra-intelligent system.

This indicator decodes the true structure of price delivery by combining Smart Money Concepts with the timeless precision of Fibonacci ratios , revealing what retail traders can’t see — *the algorithmic heartbeat of the market*.

✨ What Makes This Indicator Different

Instead of drawing random lines or reacting to late signals, this tool **anticipates** market behavior by reading the footprints left behind by institutional algorithms. Every element is placed with purpose — every zone, every shift, every fib level — all forming a seamless narrative that explains *why* price moves the way it does.

🔥 Core Intelligence Features

Advanced BOS/CHOCH Auto-Detection — Spot structure shifts before momentum even forms.

Institutional Liquidity Mapping

— Identify liquidity pools, engineered sweeps, equal highs/lows, and trap zones designed by smart money.

Fibonacci-Aligned Precision Zones

— Auto-generated fib grids synced with SMC levels for pinpoint reversal and continuation setups.

Imbalance Engine

— FVGs, displacement, inefficiencies, and mitigation blocks displayed with crystal clarity.

Premium/Discount Algorithm

— Understand instantly whether price is in a zone of accumulation or distribution.

🚀 Designed for Traders Who Want an Edge

Whether you're scalping fast moves, capturing intraday swings, or holding higher-timeframe plays, this indicator provides a professional lens into the market. It turns complex price action into a structured, predictable system where every move has logic and every entry has confluence.

You don’t just see the chart —

you see the intention behind every push, pull, manipulation, and reversal.

💎 Why It Feels Like a Cheat Code

Because it mirrors the way institutions analyze the market:

— Identify liquidity

— Seek equilibrium

— Deliver price

— Create inefficiency

— Mitigate

— Continue the narrative

Using SMC and Fibonacci together unlocks the “algorithmic geometry” behind price movement, giving you clarity where others see chaos.

⚡ Trade With Confidence, Confluence & Control

This indicator isn’t just a tool.

It’s a complete trading framework — structured, intelligent, and deadly accurate.

Master the markets.

Decode the algorithm.

Trade like smart money .

Optimized Grid with KNN_2.0Strategy Overview

This strategy, named "Optimized Grid with KNN_2.0," is designed to optimize trading decisions using a combination of grid trading, K-Nearest Neighbors (KNN) algorithm, and a greedy algorithm. The strategy aims to maximize profits by dynamically adjusting entry and exit thresholds based on market conditions and historical data.

Key Components

Grid Trading:

The strategy uses a grid-based approach to place buy and sell orders at predefined price levels. This helps in capturing profits from market fluctuations.

K-Nearest Neighbors (KNN) Algorithm:

The KNN algorithm is used to optimize entry and exit points based on historical price data. It identifies the nearest neighbors (similar price movements) and adjusts the thresholds accordingly.

Greedy Algorithm:

The greedy algorithm is employed to dynamically adjust the stop-loss and take-profit levels. It ensures that the strategy captures maximum profits by adjusting thresholds based on recent price changes.

Detailed Explanation

Grid Trading:

The strategy defines a grid of price levels where buy and sell orders are placed. The openTh and closeTh parameters determine the thresholds for opening and closing positions.

The t3_fast and t3_slow indicators are used to generate trading signals based on the crossover and crossunder of these indicators.

KNN Algorithm:

The KNN algorithm is used to find the nearest neighbors (similar price movements) in the historical data. It calculates the distance between the current price and historical prices to identify the most similar price movements.

The algorithm then adjusts the entry and exit thresholds based on the average change in price of the nearest neighbors.

Greedy Algorithm:

The greedy algorithm dynamically adjusts the stop-loss and take-profit levels based on recent price changes. It ensures that the strategy captures maximum profits by adjusting thresholds in real-time.

The algorithm uses the average_change variable to calculate the average price change of the nearest neighbors and adjusts the thresholds accordingly.

GKD-BT Giga Confirmation Stack Backtest [Loxx]Giga Kaleidoscope GKD-BT Giga Confirmation Stack Backtest is a Backtesting module included in Loxx's "Giga Kaleidoscope Modularized Trading System".

█ GKD-BT Giga Confirmation Stack Backtest

The Giga Confirmation Stack Backtest module allows users to perform backtesting on Long and Short signals from the confluence between GKD-C Confirmation 1 and GKD-C Confirmation 2 indicators. This module encompasses two types of backtests: Trading and Full. The Trading backtest permits users to evaluate individual trades, whether Long or Short, one at a time. Conversely, the Full backtest allows users to analyze either Longs or Shorts separately by toggling between them in the settings, enabling the examination of results for each signal type. The Trading backtest emulates actual trading conditions, while the Full backtest assesses all signals, regardless of being Long or Short.

Additionally, this backtest module provides the option to test using indicators with 1 to 3 take profits and 1 stop loss. The Trading backtest allows for the use of 1 to 3 take profits, while the Full backtest is limited to 1 take profit. The Trading backtest also offers the capability to apply a trailing take profit.

In terms of the percentage of trade removed at each take profit, this backtest module has the following hardcoded values:

Take profit 1: 50% of the trade is removed.

Take profit 2: 25% of the trade is removed.

Take profit 3: 25% of the trade is removed.

Stop loss: 100% of the trade is removed.

After each take profit is achieved, the stop loss level is adjusted. When take profit 1 is reached, the stop loss is moved to the entry point. Similarly, when take profit 2 is reached, the stop loss is shifted to take profit 1. The trailing take profit feature comes into play after take profit 2 or take profit 3, depending on the number of take profits selected in the settings. The trailing take profit is always activated on the final take profit when 2 or more take profits are chosen.

The backtest module also offers the capability to restrict by a specific date range, allowing for simulated forward testing based on past data. Additionally, users have the option to display or hide a trading panel that provides relevant information about the backtest, statistics, and the current trade. It is also possible to activate alerts and toggle sections of the trading panel on or off. On the chart, historical take profit and stop loss levels are represented by horizontal lines overlaid for reference.

To utilize this strategy, follow these steps:

1. Adjust the "Confirmation Type" in the GKD-C Confirmation 1 Indicator to "GKD New."

2. GKD-C Confirmation 1 Import: Import the value "Input into NEW GKD-BT Backtest" from the GKD-C Confirmation 1 module into the GKD-BT Giga Confirmation Stack Backtest module setting named "Import GKD-C Confirmation 1."

3. Adjust the "Confirmation Type" in the GKD-C Confirmation 2 Indicator to "GKD New."

4. GKD-C Confirmation 2 Import: Import the value "Input into NEW GKD-BT Backtest" from the GKD-C Confirmation 2 module into the GKD-BT Giga Confirmation Stack Backtest module setting named "Import GKD-C Confirmation 2."

█ Giga Confirmation Stack Backtest Entries

Entries are generated from the confluence of a GKD-C Confirmation 1 and GKD-C Confirmation 2 indicators. The Confirmation 1 gives the signal and the Confirmation 2 indicator filters or "approves" the the Confirmation 1 signal. If Confirmation 1 gives a long signal and Confirmation 2 shows a downtrend, then the long signal is rejected. If Confirmation 1 gives a long signal and Confirmation 2 shows an uptrend, then the long signal is approved and sent to the backtest execution engine.

█ Volatility Types Included

The GKD system utilizes volatility-based take profits and stop losses. Each take profit and stop loss is calculated as a multiple of volatility. Users can also adjust the multiplier values in the settings.

This module includes 17 types of volatility:

Close-to-Close

Parkinson

Garman-Klass

Rogers-Satchell

Yang-Zhang

Garman-Klass-Yang-Zhang

Exponential Weighted Moving Average

Standard Deviation of Log Returns

Pseudo GARCH(2,2)

Average True Range

True Range Double

Standard Deviation

Adaptive Deviation

Median Absolute Deviation

Efficiency-Ratio Adaptive ATR

Mean Absolute Deviation

Static Percent

Close-to-Close

Close-to-Close volatility is a classic and widely used volatility measure, sometimes referred to as historical volatility.

Volatility is an indicator of the speed of a stock price change. A stock with high volatility is one where the price changes rapidly and with a larger amplitude. The more volatile a stock is, the riskier it is.

Close-to-close historical volatility is calculated using only a stock's closing prices. It is the simplest volatility estimator. However, in many cases, it is not precise enough. Stock prices could jump significantly during a trading session and return to the opening value at the end. That means that a considerable amount of price information is not taken into account by close-to-close volatility.

Despite its drawbacks, Close-to-Close volatility is still useful in cases where the instrument doesn't have intraday prices. For example, mutual funds calculate their net asset values daily or weekly, and thus their prices are not suitable for more sophisticated volatility estimators.

Parkinson

Parkinson volatility is a volatility measure that uses the stock’s high and low price of the day.

The main difference between regular volatility and Parkinson volatility is that the latter uses high and low prices for a day, rather than only the closing price. This is useful as close-to-close prices could show little difference while large price movements could have occurred during the day. Thus, Parkinson's volatility is considered more precise and requires less data for calculation than close-to-close volatility.

One drawback of this estimator is that it doesn't take into account price movements after the market closes. Hence, it systematically undervalues volatility. This drawback is addressed in the Garman-Klass volatility estimator.

Garman-Klass

Garman-Klass is a volatility estimator that incorporates open, low, high, and close prices of a security.

Garman-Klass volatility extends Parkinson's volatility by taking into account the opening and closing prices. As markets are most active during the opening and closing of a trading session, it makes volatility estimation more accurate.

Garman and Klass also assumed that the process of price change follows a continuous diffusion process (Geometric Brownian motion). However, this assumption has several drawbacks. The method is not robust for opening jumps in price and trend movements.

Despite its drawbacks, the Garman-Klass estimator is still more effective than the basic formula since it takes into account not only the price at the beginning and end of the time interval but also intraday price extremes.

Researchers Rogers and Satchell have proposed a more efficient method for assessing historical volatility that takes into account price trends. See Rogers-Satchell Volatility for more detail.

Rogers-Satchell

Rogers-Satchell is an estimator for measuring the volatility of securities with an average return not equal to zero.

Unlike Parkinson and Garman-Klass estimators, Rogers-Satchell incorporates a drift term (mean return not equal to zero). As a result, it provides better volatility estimation when the underlying is trending.

The main disadvantage of this method is that it does not take into account price movements between trading sessions. This leads to an underestimation of volatility since price jumps periodically occur in the market precisely at the moments between sessions.

A more comprehensive estimator that also considers the gaps between sessions was developed based on the Rogers-Satchel formula in the 2000s by Yang-Zhang. See Yang Zhang Volatility for more detail.

Yang-Zhang

Yang Zhang is a historical volatility estimator that handles both opening jumps and the drift and has a minimum estimation error.

Yang-Zhang volatility can be thought of as a combination of the overnight (close-to-open volatility) and a weighted average of the Rogers-Satchell volatility and the day’s open-to-close volatility. It is considered to be 14 times more efficient than the close-to-close estimator.

Garman-Klass-Yang-Zhang

Garman-Klass-Yang-Zhang (GKYZ) volatility estimator incorporates the returns of open, high, low, and closing prices in its calculation.

GKYZ volatility estimator takes into account overnight jumps but not the trend, i.e., it assumes that the underlying asset follows a Geometric Brownian Motion (GBM) process with zero drift. Therefore, the GKYZ volatility estimator tends to overestimate the volatility when the drift is different from zero. However, for a GBM process, this estimator is eight times more efficient than the close-to-close volatility estimator.

Exponential Weighted Moving Average

The Exponentially Weighted Moving Average (EWMA) is a quantitative or statistical measure used to model or describe a time series. The EWMA is widely used in finance, with the main applications being technical analysis and volatility modeling.

The moving average is designed such that older observations are given lower weights. The weights decrease exponentially as the data point gets older – hence the name exponentially weighted.

The only decision a user of the EWMA must make is the parameter lambda. The parameter decides how important the current observation is in the calculation of the EWMA. The higher the value of lambda, the more closely the EWMA tracks the original time series.

Standard Deviation of Log Returns

This is the simplest calculation of volatility. It's the standard deviation of ln(close/close(1)).

Pseudo GARCH(2,2)

This is calculated using a short- and long-run mean of variance multiplied by ?.

?avg(var;M) + (1 ? ?) avg(var;N) = 2?var/(M+1-(M-1)L) + 2(1-?)var/(M+1-(M-1)L)

Solving for ? can be done by minimizing the mean squared error of estimation; that is, regressing L^-1var - avg(var; N) against avg(var; M) - avg(var; N) and using the resulting beta estimate as ?.

Average True Range

The average true range (ATR) is a technical analysis indicator, introduced by market technician J. Welles Wilder Jr. in his book New Concepts in Technical Trading Systems, that measures market volatility by decomposing the entire range of an asset price for that period.

The true range indicator is taken as the greatest of the following: current high less the current low; the absolute value of the current high less the previous close; and the absolute value of the current low less the previous close. The ATR is then a moving average, generally using 14 days, of the true ranges.

True Range Double

A special case of ATR that attempts to correct for volatility skew.

Standard Deviation

Standard deviation is a statistic that measures the dispersion of a dataset relative to its mean and is calculated as the square root of the variance. The standard deviation is calculated as the square root of variance by determining each data point's deviation relative to the mean. If the data points are further from the mean, there is a higher deviation within the data set; thus, the more spread out the data, the higher the standard deviation.

Adaptive Deviation

By definition, the Standard Deviation (STD, also represented by the Greek letter sigma ? or the Latin letter s) is a measure that is used to quantify the amount of variation or dispersion of a set of data values. In technical analysis, we usually use it to measure the level of current volatility.

Standard Deviation is based on Simple Moving Average calculation for mean value. This version of standard deviation uses the properties of EMA to calculate what can be called a new type of deviation, and since it is based on EMA, we can call it EMA deviation. Additionally, Perry Kaufman's efficiency ratio is used to make it adaptive (since all EMA type calculations are nearly perfect for adapting).

The difference when compared to the standard is significant--not just because of EMA usage, but the efficiency ratio makes it a "bit more logical" in very volatile market conditions.

Median Absolute Deviation

The median absolute deviation is a measure of statistical dispersion. Moreover, the MAD is a robust statistic, being more resilient to outliers in a data set than the standard deviation. In the standard deviation, the distances from the mean are squared, so large deviations are weighted more heavily, and thus outliers can heavily influence it. In the MAD, the deviations of a small number of outliers are irrelevant.

Because the MAD is a more robust estimator of scale than the sample variance or standard deviation, it works better with distributions without a mean or variance, such as the Cauchy distribution.

Efficiency-Ratio Adaptive ATR

Average True Range (ATR) is a widely used indicator for many occasions in technical analysis. It is calculated as the RMA of the true range. This version adds a "twist": it uses Perry Kaufman's Efficiency Ratio to calculate adaptive true range.

Mean Absolute Deviation

The mean absolute deviation (MAD) is a measure of variability that indicates the average distance between observations and their mean. MAD uses the original units of the data, which simplifies interpretation. Larger values signify that the data points spread out further from the average. Conversely, lower values correspond to data points bunching closer to it. The mean absolute deviation is also known as the mean deviation and average absolute deviation.

This definition of the mean absolute deviation sounds similar to the standard deviation (SD). While both measure variability, they have different calculations. In recent years, some proponents of MAD have suggested that it replace the SD as the primary measure because it is a simpler concept that better fits real life.

Static Percent

Static Percent allows the user to insert their own constant percent that will then be used to create take profits and stoploss

█ Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.