Exposure Oscillator (Cumulative 0 to ±100%)

Exposure Oscillator (Cumulative 0 to ±100%)

This Pine Script indicator plots an "Exposure Oscillator" on the chart, which tracks the cumulative market exposure from a range of technical buy and sell signals. The exposure is measured on a scale from -100% (maximum short exposure) to +100% (maximum long exposure), helping traders assess the strength of their position in the market. It provides an intuitive visual cue to aid decision-making for trend-following strategies.

Buy Signals (Increase Exposure Score by +10%)

Buy Signal 1 (Cross Above 21 EMA):

This signal is triggered when the price crosses above the 21-period Exponential Moving Average (EMA), where the current bar closes above the EMA21, and the previous bar closed below the EMA21. This indicates a potential upward price movement as the market shifts into a bullish trend.

buySignal1 = ta.crossover(close, ema21)

Buy Signal 2 (Trending Above 21 EMA):

This signal is triggered when the price closes above the 21-period EMA for each of the last 5 bars, indicating a sustained bullish trend. It confirms that the price is consistently above the EMA21 for a significant period.

buySignal2 = ta.barssince(close <= ema21) > 5

Buy Signal 3 (Living Above 21 EMA):

This signal is triggered when the price has closed above the 21-period EMA for each of the last 15 bars, demonstrating a strong, prolonged uptrend.

buySignal3 = ta.barssince(close <= ema21) > 15

Buy Signal 4 (Cross Above 50 SMA):

This signal is triggered when the price crosses above the 50-period Simple Moving Average (SMA), where the current bar closes above the 50 SMA, and the previous bar closed below it. It indicates a shift toward bullish momentum.

buySignal4 = ta.crossover(close, sma50)

Buy Signal 5 (Cross Above 200 SMA):

This signal is triggered when the price crosses above the 200-period Simple Moving Average (SMA), where the current bar closes above the 200 SMA, and the previous bar closed below it. This suggests a long-term bullish trend.

buySignal5 = ta.crossover(close, sma200)

Buy Signal 6 (Low Above 50 SMA):

This signal is true when the lowest price of the current bar is above the 50-period SMA, indicating strong bullish pressure as the price maintains itself above the moving average.

buySignal6 = low > sma50

Buy Signal 7 (Accumulation Day):

An accumulation day occurs when the closing price is in the upper half of the daily range (greater than 50%) and the volume is larger than the previous bar's volume, suggesting buying pressure and accumulation.

buySignal7 = (close - low) / (high - low) > 0.5 and volume > volume

Buy Signal 8 (Higher High):

This signal occurs when the current bar’s high exceeds the highest high of the previous 14 bars, indicating a breakout or strong upward momentum.

buySignal8 = high > ta.highest(high, 14)

Buy Signal 9 (Key Reversal Bar):

This signal is generated when the stock opens below the low of the previous bar but rallies to close above the previous bar’s high, signaling a potential reversal from bearish to bullish.

buySignal9 = open < low and close > high

Buy Signal 10 (Distribution Day Fall Off):

This signal is triggered when a distribution day (a day with high volume and a close near the low of the range) "falls off" the rolling 25-bar period, indicating the end of a bearish trend or selling pressure.

buySignal10 = ta.barssince(close < sma50 and close < sma50) > 25

Sell Signals (Decrease Exposure Score by -10%)

Sell Signal 1 (Cross Below 21 EMA):

This signal is triggered when the price crosses below the 21-period Exponential Moving Average (EMA), where the current bar closes below the EMA21, and the previous bar closed above it. It suggests that the market may be shifting from a bullish trend to a bearish trend.

sellSignal1 = ta.crossunder(close, ema21)

Sell Signal 2 (Trending Below 21 EMA):

This signal is triggered when the price closes below the 21-period EMA for each of the last 5 bars, indicating a sustained bearish trend.

sellSignal2 = ta.barssince(close >= ema21) > 5

Sell Signal 3 (Living Below 21 EMA):

This signal is triggered when the price has closed below the 21-period EMA for each of the last 15 bars, suggesting a strong downtrend.

sellSignal3 = ta.barssince(close >= ema21) > 15

Sell Signal 4 (Cross Below 50 SMA):

This signal is triggered when the price crosses below the 50-period Simple Moving Average (SMA), where the current bar closes below the 50 SMA, and the previous bar closed above it. It indicates the start of a bearish trend.

sellSignal4 = ta.crossunder(close, sma50)

Sell Signal 5 (Cross Below 200 SMA):

This signal is triggered when the price crosses below the 200-period Simple Moving Average (SMA), where the current bar closes below the 200 SMA, and the previous bar closed above it. It indicates a long-term bearish trend.

sellSignal5 = ta.crossunder(close, sma200)

Sell Signal 6 (High Below 50 SMA):

This signal is true when the highest price of the current bar is below the 50-period SMA, indicating weak bullishness or a potential bearish reversal.

sellSignal6 = high < sma50

Sell Signal 7 (Distribution Day):

A distribution day is identified when the closing range of a bar is less than 50% and the volume is larger than the previous bar's volume, suggesting that selling pressure is increasing.

sellSignal7 = (close - low) / (high - low) < 0.5 and volume > volume

Sell Signal 8 (Lower Low):

This signal occurs when the current bar's low is less than the lowest low of the previous 14 bars, indicating a breakdown or strong downward momentum.

sellSignal8 = low < ta.lowest(low, 14)

Sell Signal 9 (Downside Reversal Bar):

A downside reversal bar occurs when the stock opens above the previous bar's high but falls to close below the previous bar’s low, signaling a reversal from bullish to bearish.

sellSignal9 = open > high and close < low

Sell Signal 10 (Distribution Cluster):

This signal is triggered when a distribution day occurs three times in the rolling 7-bar period, indicating significant selling pressure.

sellSignal10 = ta.valuewhen((close < low) and volume > volume , 1, 7) >= 3

Theme Mode:

Users can select the theme mode (Auto, Dark, or Light) to match the chart's background or to manually choose a light or dark theme for the oscillator's appearance.

Exposure Score Calculation: The script calculates a cumulative exposure score based on a series of buy and sell signals.

Buy signals increase the exposure score, while sell signals decrease it. Each signal impacts the score by ±10%.

Signal Conditions: The buy and sell signals are derived from multiple conditions, including crossovers with moving averages (EMA21, SMA50, SMA200), trend behavior, and price/volume analysis.

Oscillator Visualization: The exposure score is visualized as a line on the chart, changing color based on whether the exposure is positive (long position) or negative (short position). It is limited to the range of -100% to +100%.

Position Type: The indicator also indicates the position type based on the exposure score, labeling it as "Long," "Short," or "Neutral."

Horizontal Lines: Reference lines at 0%, 100%, and -100% visually mark neutral, increasing long, and increasing short exposure levels.

Exposure Table: A table displays the current exposure level (in percentage) and position type ("Long," "Short," or "Neutral"), updated dynamically based on the oscillator’s value.

Inputs:

Theme Mode: Choose "Auto" to use the default chart theme, or manually select "Dark" or "Light."

Usage:

This oscillator is designed to help traders track market sentiment, gauge exposure levels, and manage risk. It can be used for long-term trend-following strategies or short-term trades based on moving average crossovers and volume analysis.

The oscillator operates in conjunction with the chart’s price action and provides a visual representation of the market’s current trend strength and exposure.

Important Considerations:

Risk Management: While the exposure score provides valuable insight, it should be combined with other risk management tools and analysis for optimal trading decisions.

Signal Sensitivity: The accuracy and effectiveness of the signals depend on market conditions and may require adjustments based on the user’s trading strategy or timeframe.

Disclaimer:

This script is for educational purposes only. Trading involves significant risk, and users should carefully evaluate all market conditions and apply appropriate risk management strategies before using this tool in live trading environments.

Buscar en scripts para "accumulation"

Buy/Sell Volume Totals for PeriodThis indicator can be used to help you tell the difference between Wyckoff Accumulation and Distribution.

The idea is to add up all the Buy Volume and all the Sell Volume separately from the beginning of the Trading Range (TR) for each candle. You can define the Start and End dates in the settings of the indicator.

The indicator will show you 3 numbers of interest:

GREEN = Total Buy Volume from beginning of date range

RED = Total Sell Volume from beginning of date range

YELLOW = Ratio of Total Buy / Total Sell Volume from beginning of date range

When the Total Buy Volume exceeds the Total Sell Volume in the TR, the indicator will color the background in GREEN color, to indicate possible accumulation. Otherwise the background will be RED, to indicate possible distribution.

You can float your cursor over any candle to see the current Volume Totals at that candle from the beginning of the TR (set by you in settings to a specific date).

Here's a few examples of the indicator in action:

1) Accumulation

2) Distribution

3) Possible Re-distribution

Please note that this indicator is meant to be used in combination with other analysis techniques from the Wyckoff Methodology!

Apex Wallet - Bitcoin Halving Cycle & Profit ProjectionOverview The Apex Wallet Bitcoin Halving Cycle Profit is a strategic macro-analysis tool designed for Bitcoin investors and long-term holders. It provides a visual framework of Bitcoin's 4-year cycles by identifying past halving dates and projecting future ones automatically. The script highlights key accumulation and profit-taking windows based on historical cycle performance.

Dynamic Cycle Intelligence

Halving Milestones: Automatically detects and marks all major halving events (2012, 2016, 2020, 2024) with precise timestamps.

Predictive Projections: Using an estimated 1,460-day cycle, the script projects up to 30 future halving events to help plan long-term investment horizons.

Timeframe Optimization: Built specifically for Weekly (W) and Monthly (M) charts to provide a clean, high-level perspective of market structure.

Key Strategy Visuals

Profit Windows: Visualizes "Start" and "End" profit zones with automated vertical lines and color-coded labels based on user-defined offsets from the halving.

DCA Chain Signals: Identifies strategic Dollar Cost Averaging (DCA) points throughout the cycle to assist in disciplined accumulation.

Heatmap Shading: Features dynamic background shading that intensifies as the cycle progresses toward historical peak performance periods.

How to Use:

Switch to a Weekly or Monthly Bitcoin chart.

Use the Green Labels (Profit START) to identify early cycle strength.

Monitor the Red Labels (Profit END) for historical cycle exhaustion zones.

Scalp Breakout Predictor Pro - by Herman Sangivera (Papua)Scalp Breakout Predictor Pro by Herman Sangivera ( Papuan Trader )

Overview

The Scalp Breakout Predictor Pro is a high-performance technical indicator designed for scalpers and day traders who thrive on market volatility. This tool specializes in identifying "Squeeze" phases—periods where the market is consolidating sideways—and predicts the likely direction of the upcoming breakout using underlying momentum accumulation.

How It Works

The indicator combines three core mathematical concepts to ensure "Safe but Fast" entries:

Squeeze Detection (BB vs. KC): It monitors the relationship between Bollinger Bands and Keltner Channels. When Bollinger Bands contract inside the Keltner Channels, the market is in a "Squeeze" (represented by the gray background). This indicates that energy is being coiled for a massive move.

Momentum Accumulation (Pre-Signal): While the price is still moving sideways, the script analyzes linear regression momentum.

PRE-BULL: Momentum is building upwards despite price being flat.

PRE-BEAR: Momentum is fading downwards despite price being flat.

Breakout Confirmation: An entry signal is only triggered when the Squeeze "fires" (the price breaks out of the bands), ensuring you don't get stuck in a dead market for too long.

Key Features

Real-time Prediction Labels: Get early warnings (PRE-BULL / PRE-BEAR) to prepare for the trade before it happens.

Dynamic TP/SL Lines: Automatically calculates Take Profit and Stop Loss levels based on the Average True Range (ATR), adapting to the current market's "breath."

On-Screen Dashboard: A sleek table in the top-right corner displays the current market phase (Squeeze vs. Volatile), the predicted next move, and the current ATR value.

Pine Script V6 Optimized: Built using the latest version of TradingView’s coding language for maximum speed and compatibility.

Trading Rules

Preparation: When you see a Gray Background, the market is sideways. Watch the Dashboard for the "Potential" direction.

Anticipation: If a PRE-BULL or PRE-BEAR label appears, get ready to enter.

Execution: Enter the trade when the ENTRY BUY (Lime Triangle) or ENTRY SELL (Red Triangle) signal appears.

Exit: Follow the Green Line for Take Profit and the Red Line for Stop Loss.

Technical Settings

HMA Length: Adjusts the sensitivity of the trend filter (Hull Moving Average).

TP/SL Multipliers: Allows you to customize your Risk:Reward ratio based on ATR volatility.

Squeeze Length: Determines the lookback period for consolidation detection.

Disclaimer: Scalping involves high risk. Always test this indicator on a demo account before using it with live capital.

ETH Dynamic Risk Strategy# ETH Dynamic Risk Strategy - Publication Description

## Overview

The ETH Dynamic Risk Strategy is a systematic approach to accumulating Ethereum during bear markets and distributing during bull markets. It combines multiple risk indicators into a single composite metric (0-1 scale) that identifies optimal buying and selling zones based on market conditions.

## Key Features

• **Multi-Component Risk Metric**: Combines 4 weighted indicators to assess market conditions

• **Tiered Buy/Sell System**: 3 levels of buy signals (L1, L2, L3) and 3 levels of sell signals based on risk thresholds

• **Configurable Filters**: Optional buy filters to reduce signal frequency by 30-50%

• **Visual Risk Zones**: Color-coded risk metric plot with clear threshold lines

• **Comprehensive Dashboard**: Real-time statistics including position size, P/L, and component scores

## How It Works

### Risk Components (Configurable Weights)

1. **Log Return from ATH** (Default: 35%)

- Tracks drawdown from all-time high over lookback period

- Deep drawdowns (-70% to -90%) = low risk / buying opportunity

- Near ATH (0% to -20%) = high risk / selling opportunity

2. **ETH/BTC Ratio** (Default: 25%)

- Measures ETH strength relative to Bitcoin

- Below historical average = ETH undervalued = low risk

- Above historical average = ETH overvalued = high risk

3. **Volatility Regime** (Default: 20%)

- Compares current volatility to long-term average

- Compressed volatility at lows = opportunity

- Expanded volatility at highs = danger

4. **Trend Strength** (Default: 20%)

- Uses multiple EMA alignment and slope analysis

- Strong downtrends = low risk scores

- Strong uptrends = high risk scores

### Trading Logic

**Buy Signals:**

- L1: Risk ≤ 0.30 → Buy $100 (default)

- L2: Risk ≤ 0.20 → Buy $250 total

- L3: Risk ≤ 0.10 → Buy $450 total

**Sell Signals (Sequential):**

- L1: Risk ≥ 0.75 → Sell 25% of position

- L2: Risk ≥ 0.85 → Sell 35% of remaining

- L3: Risk ≥ 0.95 → Sell 40% of remaining

**Buy Filters (Optional):**

- Minimum days between buys (prevents clustering)

- Minimum risk drop required (ensures falling risk)

- Toggle on/off to compare performance

## Settings Guide

### Risk Components

Toggle individual components on/off and adjust their weights. Total weight is automatically normalized. Experiment with different combinations to match your market view.

### Advanced Settings

- ATH Lookback: How far back to look for all-time highs (500-2000 recommended)

- Volatility Period: Window for volatility calculations (40-100 recommended)

- ETH/BTC MA Period: Moving average for ratio comparison (100-300 recommended)

- Trend Period: Base period for trend calculations (50-150 recommended)

### Trading Thresholds

Customize buy/sell trigger points and position sizes. Lower buy thresholds = more aggressive accumulation. Higher sell thresholds = holding longer into bull markets.

### Buy Filters

- Enable/disable filtering system

- Min Days Between Buys: Spacing between purchases (1-3 recommended)

- Min Risk Drop: How much risk must fall (-0.001 to -0.01 range)

## Best Practices

• **Timeframe**: Works best on daily (1D) and 3-day (3D) charts

• **Initial Capital**: Set based on your DCA budget (default $10,000)

• **Backtest First**: Test different parameter combinations on historical data

• **Position Sizing**: Adjust buy amounts to match your risk tolerance

• **Monitor Filters**: Check "Filtered Buys" stat to ensure filter isn't too strict

## Use Cases

- Long-term ETH accumulation strategy

- Systematic DCA with market-adaptive buying

- Risk-based portfolio rebalancing

- Educational tool for understanding crypto market cycles

## Disclaimer

This strategy is for educational purposes only. Past performance does not guarantee future results. Cryptocurrency trading involves substantial risk. The strategy uses historical price action and technical indicators which may not predict future movements. Always do your own research and never invest more than you can afford to lose.

## Credits

Strategy concept and development by nakphanan with assistance from Claude AI (Anthropic). Built using Pine Script v5....Mostly from Claude AI!!!

## Version History

v7.0 - Initial release with 4-component risk metric, tiered trading system, and optional buy filters

BTC - BEAM: Adaptive Multiple (Open-Source)Title: BTC - BEAM: Adaptive Multiple Cycle Oscillator | RM

Overview & Philosophy

The BTC - BEAM (Bitcoin Economics Adaptive Multiple) is a premier macro-valuation tool designed to identify the "Logarithmic Pulse" of Bitcoin's 4-year cycles. Unlike standard oscillators that lose relevance as the network grows, BEAM uses an adaptive baseline that tracks Bitcoin’s fundamental growth curve with precision.

It identifies the harmonic distance between the current price and its multi-year mean, helping you spot the rare windows of deep capitulation and terminal euphoria.

Methodology

This edition is a hardened, gap-proof and Open-Source implementation of the canonical BEAM model.

1. The 1400-Day Anchor (200 Weeks):

The model is anchored to a 1400-day Simple Moving Average. On the Weekly chart, this aligns with the legendary 200-week moving average—the historical "floor" of the Bitcoin network. It represents one full halving cycle of data.

2. Daily-Lock Architecture:

Even when viewed on the 1W chart, the script performs its calculations using Daily data. This ensures that the oscillator captures the exact peak day of a cycle, providing a "high-resolution" signal within a "low-noise" weekly environment.

3. Logarithmic Normalization:

We calculate the natural logarithm of the price-to-mean relationship, scaled by a factor of 2.5: Score = ln(Price / 1400d MA) / 2.5 This creates a standardized "Multiple" that remains comparable across all Bitcoin eras.

How to Read the Chart (1W Context)

🟧 The BEAM Line (Orange): Tracks the "macro heat" of the market. On the 1W chart, look for the slope of this line to identify cycle acceleration.

🔴 The Cycle Ceiling (Score > 1.0): Historical Cycle Tops. When the weekly candle sustains in this zone, the market has reached a state of unsustainable mania. Every major blow-off top has been captured in this red corridor.

🟢 The Cycle Floor (Score < 0.1): Generational Accumulation. On the 1W chart, these zones appear as extended "green troughs." These are the only times in history where Bitcoin is fundamentally "too cheap" relative to its 4-year trend.

The Status Dashboard

The bottom-right monitor provides immediate cycle classification:

• BEAM Score: The exact logarithmic multiple.

• Cycle Regime: ACCUMULATION , NEUTRAL , or OVERHEATED .

Credits

BitcoinEcon: For the original concept of the BEAM adaptive model.

⚠️ RECOMMENDATION: While this indicator captures daily data, it is strongly recommended to be viewed on the Weekly (1W) Timeframe. The 1W chart filters market noise and perfectly reveals the long-term "Cycle Narrative."

Disclaimer

This script is for research and educational purposes only. Macro indicators provide structural context; they are not crystal balls. Always manage your risk according to your personal financial plan.

Tags

bitcoin, btc, beam, macro, cycle, halving, log-growth, valuation, on-chain, Rob Maths

WAD : Whale Activity Detector🐋 WAD: Whale Activity Detector

WAD (Whale Activity Detector) automatically detects periods of abnormally high trading volume compared to the average, identifying potential whale (institutional) buy or sell activity and visualizing it directly on the chart.

🔍 How It Works

1. Buy/Sell Volume Separation

Each candle’s trading volume is categorized based on its direction:

Bullish candle → Buy volume

Bearish candle → Sell volume

This separation helps distinguish the actual strength of buying vs. selling pressure, rather than looking at total volume alone.

2. Average Volume Calculation

Over a user-defined lookback period (default: 34 bars), the indicator calculates the moving average of both buy and sell volumes, establishing a baseline for what constitutes “normal” activity.

3. Whale Activity Detection

When the current volume exceeds n times the average volume (default: 4×), the indicator flags it as a Whale Zone — a potential sign of large player involvement.

Volume surge on a bullish candle → Whale Buy

Volume surge on a bearish candle → Whale Sell

4. Visual Display

🟢 Green bars: Whale buy activity

🔴 Red bars: Whale sell activity

BUY/SELL labels: Appear above the chart when an anomaly is detected

Average line toggle: Users can turn the average volume lines on or off for clarity

5. Alerts

Whenever whale buy/sell signals are detected, real-time alerts are triggered.

Example: 🐋 Whale Buy – NVDA! 🟢

⚙️ Indicator Meaning

Rather than showing raw volume, WAD tracks “abnormal volume relative to the average.”

It filters out noise and highlights the moments where large entities begin to move.

Essentially, it visualizes intentional and impactful trades hidden within standard volume activity.

🚀 Example Use Cases

Whale accumulation tracking – Repeated strong buy signals may indicate sustained institutional accumulation.

Short-term breakout confirmation – Price often rallies shortly after whale buy signals appear.

Support/resistance analysis – Whale sell zones frequently align with short-term resistance areas.

In short:

WAD identifies when trading volume exceeds its historical norm to highlight where big money enters or exits the market.

===============================================================================

🐋 WAD : 세력 매매거래 추적기

WAD(Whale Activity Detector) 는 특정 종목의 거래량 패턴 속에서

‘평균 대비 비정상적으로 큰 거래량이 발생한 구간’을 자동으로 감지해

세력(Whale)의 매수·매도 활동을 시각화하는 지표입니다.

🔍 작동 원리

매수·매도 거래량 분리

각 캔들이 양봉인지, 음봉인지에 따라 거래량을 분리합니다.

양봉 시 발생한 거래량 → 매수 거래량(buy volume)

음봉 시 발생한 거래량 → 매도 거래량(sell volume)

이렇게 분리함으로써 단순 거래량이 아닌,

실제 매수세/매도세의 힘을 구분할 수 있습니다.

평균 거래량 계산

사용자가 지정한 기간(기본 34봉)을 기준으로

매수·매도 거래량의 이동평균선을 각각 계산합니다.

이는 ‘정상적인 거래량 수준’을 판단하는 기준선으로 활용됩니다.

이상치 탐지 (Whale Activity Detection)

현재 거래량이 평균 거래량의 n배(기본 4배)를 초과할 경우,

그 구간을 세력 개입 구간(Whale Zone) 으로 판단합니다.

양봉에서 급증 → 세력 매수 (Whale Buy)

음봉에서 급증 → 세력 매도 (Whale Sell)

시각적 표시

초록색 기둥 : 세력 매수 거래량

빨간색 기둥 : 세력 매도 거래량

라벨 표시 (BUY / SELL) : 이상치 발생 시 차트 상단에 표시

평균선 표시 옵션 : 사용자가 원할 때 평균선을 켜거나 끌 수 있음

알림(Alerts)

세력의 매수·매도 신호가 감지되면,

알림 메시지를 통해 실시간으로 통보받을 수 있습니다.

(예: 🐋 Whale Buy - NVDA! 🟢)

⚙️ 지표의 의미

단순 거래량이 아니라, ‘평균 대비 비정상적 거래량’ 을 추적합니다.

즉, “세력이 본격적으로 움직이기 시작한 구간” 만 걸러내는 지표입니다.

노이즈가 많은 거래량 차트 속에서 의도 있는 거래의 흔적을 포착할 수 있습니다.

🚀 활용 예시

세력 매집 구간 포착 : 큰 매수 시그널이 반복적으로 발생하는 구간은 세력의 누적 매집 가능성을 의미함

단기 급등 신호 확인 : 매수 이상치가 발생한 직후 가격이 급등하는 경우가 많음

지지/저항 분석과 병행 활용 : 세력 매도 구간은 단기 저항으로 작용하는 경향이 있음

copyright @invest_hedgeway

Cyclical Phases of the Market🧭 Overview

“Cyclical Phases of the Market” automatically detects major market cycles by connecting swing lows and measuring the average number of bars between them.

Once it learns the rhythm of past cycles, it projects the next expected cycle (in time and price) using a dashed orange line and a forecast label.

In simple terms:

The indicator shows where the next potential low is statistically expected to occur, based on the timing and depth of previous cycles.

⚙️ Core Logic – Step by Step

1️⃣ Pivot Detection

The script uses the built-in ta.pivotlow() and ta.pivothigh() functions to find local turning points:

pivotLow marks a local swing low, defined by pivotLeft and pivotRight bars on each side.

Only confirmed lows are used to define the major cycle points.

Each new pivot low is stored in two arrays:

cycleLows → price level of the low

cycleBars → bar index where the low occurred

2️⃣ Cycle Identification and Drawing

Every time two consecutive swing lows are found, the indicator:

Calculates the number of bars between them (cycle length).

If that distance is greater than or equal to minCycleBars, it draws a teal line connecting the two lows — visually representing one complete cycle.

These teal lines form the historical cycle structure of the market.

3️⃣ Average Cycle Length

Once there are at least three completed cycles, the script calculates the average duration (mean number of bars between lows).

This value — avgCycleLength — represents the dominant periodicity or cycle rhythm of the market.

4️⃣ Forecasting the Next Cycle

When a valid average cycle length exists, the model projects the next expected cycle:

Time projection:

Adds avgCycleLength to the last cycle’s ending bar index to find where the next low should occur.

Price projection:

Estimates the vertical amplitude by taking the difference between the last two cycle lows (priceDiff).

Adds this same difference to the last low price to forecast the next probable low level.

The result is drawn as an orange dashed line extending into the future, representing the Next Expected Cycle.

5️⃣ Forecast Label

An orange label 🔮 appears at the projected future point showing:

Text:

🔮 Upcoming Cycle Forecast

Price:

The label marks the probable area and timing of the next cyclical low.

(Note: the date/time calculation currently multiplies bar count by 7 days, so it’s designed mainly for daily charts. On other timeframes, that conversion can be adapted.)

📊 How to Read It on the Chart

Visual Element Meaning Interpretation

Teal lines Completed historical cycles (low to low) Show actual periodic rhythm of the market

Orange dashed line Projection of the next expected cycle Anticipated path toward the next cyclical low

Orange label 🔮 Upcoming Cycle Forecast Displays expected price and bar location

Average cycle length Internal variable (bars between lows) Represents the dominant cycle period

📈 Interpretation

When teal segments show consistent spacing, the market is following a stable rhythm → cycles are predictable.

When cycle spacing shortens, the market is accelerating (volatility rising).

When it widens, the market is slowing down or entering accumulation.

The orange dashed line represents the next expected low zone:

If the market drops near this line → cyclical pattern confirmed.

If the market breaks well below → cycle amplitude has increased (trend weakening).

If the market rises above and delays → a new longer cycle may be forming.

🧠 Practical Use

Combine with oscillators (e.g., RSI or TSI) to confirm momentum alignment near projected lows.

Use in conjunction with volume to identify accumulation or exhaustion near the expected turning point.

Compare across timeframes: weekly cycles confirm long-term rhythm; daily cycles refine short-term entries.

⚡ Summary

Aspect Description

Purpose Detect and forecast recurring market cycles

Cycle basis Low-to-Low pivot analysis

Visuals Teal historical cycles + Orange forecast line

Forecast Next expected low (price and time)

Ideal timeframe Daily

Main outputs Average cycle length, next projected cycle, visual cycle map

Nightrangers IndicatorDescription

This indicator combines three EMA's, Ichimoku Cloud, RSI and MACD. By combining and modifying their use case this turns into an extremely powerful and accessible indicator for finding long and short position entries, below is a description of how to use this indicator, and what makes it different.

Primary Use case

The three EMA's would be the initial indicators you would be looking at, they are based on the 7d, 25d and 200d MA - Used on their own, they would be worthless, and this is where the Ichimoku Cloud comes into it, I have removed all other aspects of the Ichimoku Cloud and only kept the baseline, combine this with the three MA's and we have a very powerful indicator for finding Long entries, that is used uniquely in a way to which the Ichimoku Cloud is not originally meant to be used for.

An early indication of a LONG entry would be when the 7d MA crosses above the Ichimoku Baseline, through this early indicator, you are able to watch and monitor the chart, you would be waiting to see if the 25d MA then also crosses above the Ichimoku Baseline, This would be the second important indication of a long entry. The 200d MA helps here when making decisions on where to set your own personal take profits - If the Ichimoku baseline, and the MA's are below the 200d MA, you would be expecting a bounce point here, or heavy resistance so the long entry could be over a shorter period, than that if it was above the 200d MA, which is why it is included here, to help make a better informed choice.

The latter is reversed for finding short positions, and entries. This indicator is completely reliant on each other to find the best possible entry/exit by complementing each other, and by using the Ichimoku Baseline on it's own, and not as the Ichimoku Cloud is intended.

Just using these though, is not enough, which is why the RSI and MACD are also combined, once the conditions are met above, You may find that there can be false positives for entries, and this is where the RSI has multiple use cases within this script.

Firstly the backdrop colour will change based on whether the chart is in an uptrend or downtrend, This is a visual indicator provided to work simultaneaously on the chart itself to help identification of entries/exits easier to identify in conjunction with the above.

Secondly, It is used to display in the top right, The current Trend in a text format, as well as if the current chart is in one of three phases, these are Overbrought, Oversold and accumulation.

And finally it will display the current RSI Value on the last candle in a clear to see blue Label, This helps with the visual accessible side, to help you make a more informed choice depending on your own personal tolerance.

This ties into the above Indicators, by combining the information, you would not be looking to take a long, if for example, the RSI showed it was over-brought, and in a downtrend, even if the MA's had crossed above the Baseline, as this would most likely be a fakeout.

However if the Indicators above, showed a potential long, and the backdrop had flipped green, indicating an uptrend, and it was in an accumulation phase, you would consider this position. and this is where the MACD comes into play.

You would use the MACD to see whether or not the Signal line has crossed over the MACD line, and vice versa - However this script uses it to simplify and portray current market sentiment, and visually display by reducing clutter on screen, and making it more accessible.

It is designed to portray an easy to read and understand visual indicator by displaying in the top right simply as Bullish or Bearish, with markers above the candles ( "M" and "MX" ).

The M indicator is to show where the MACD Crosses above the Signal, and if aligned with all the other indicators within the script, shows a very strong confirmation for a buying opportunity, and vice versa for the "MX" indicator if aligned with the other indicators in reverse, provides a very strong confirmation for opening a short position or for selling.

Secondary Use case

By combining the indicators above, the secondary conditions you would be looking for, If you opened a LONG position, would be knowing when to sell, On top of what has been described above already regarding this, you would be looking to start taking profits, when the 7d MA crosses above or across the candles, and looking to close the position, when the 25d MA also crosses above the candles, and respectively, in reverse for closing short positions. This is shown across the charts to be extremely useful, however, combine this with the other indicators, portrayed in an easy to use and understand visual representation, you are now able to make more informed decisions, on whether to close a position or not.

How is it different and not just a mash up

I have combined these indicators to make the world of trading more accessible for everyone regardless of circumstances, by creating an easy to understand visual representation, keeping colours vibrant and easy to stand out, with clear and simple to read text indications. So whether you are a seasoned trader, or just starting out, you can make more informed choices, without the need of learning how to use multiple different indicators, and learning how to combine them all, or if you have difficulties learning, this indicator also simplifies a lot of the more technical intricacies, by still allowing you to make a more informed choice.

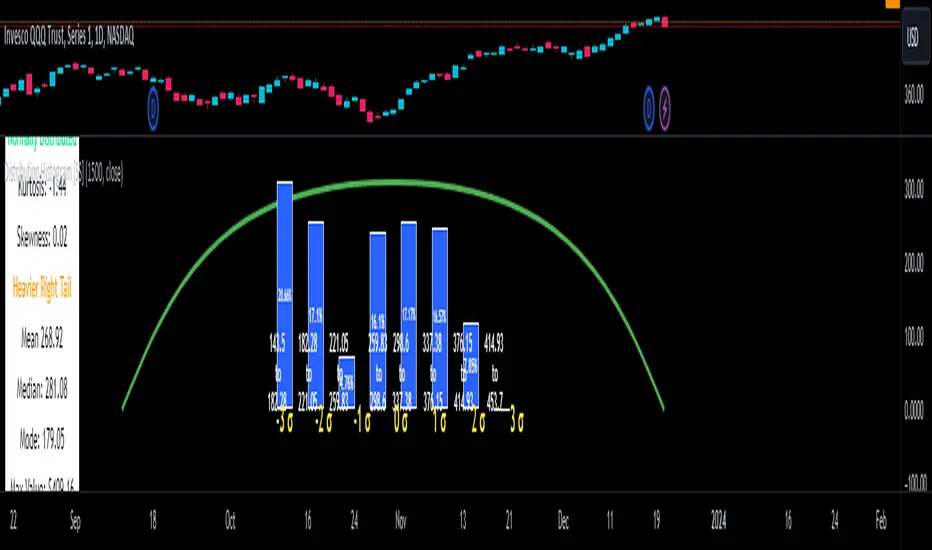

Distribution Histogram [SS]This is the frequency histogram indicator. It does just that—creates a frequency histogram distribution based on your desired lookback period. It then uses Pine's new Polyline function to plot a normal curve of the expected results for a normal distribution. This allows you to see quite a few things:

🎯 Firstly, it allows you to see where the accumulation rests in terms of a bell curve. The histogram represents a bell curve, and you can visually observe what the curve would look like.

🎯 Secondly, it will assess the normal distribution and the degree of skewness based on the curve itself. The indicator imports the SPTS statistics library to assess the distribution using Kurtosis and Skewness. However, it also adds functionality in this regard by making a qualitative assessment of the data. For example, if there are heavy left tails or heavier right tails present in the histogram, the indicator will alert you that a heavier left or right tail has been observed.

🎯 Thirdly, it provides you with the kurtosis and skewness of the dataset.

🎯 Fourthly, it provides the mean, median, and mode of the dataset, as well as the maximum and minimum values within the dataset.

🎯 Lastly, it provides you with the ability to toggle on tips/explanations of the curve itself. Simply toggle on "Show Distribution Explanation" in the settings menu:

How is the indicator helpful for trading?

If you are a mean reversion trader, this helps you identify the areas and price ranges of high and low accumulation. It also allows you to ascertain the probability by looking at the standard deviation of the bell curve. Remember, the majority of values should fall between -1 and 1 standard deviation of the mean (68%).

If it is revealed that the distribution has a heavier right or left tail, you will know that the stock is more likely to experience sudden drops and shifts in the curve in one direction or the other. Heavier left tails will tend to shift to the values on the far left, and vice versa for right tails.

Customization

You can turn off and on the following:

👉 The normal curve,

👉 The standard deviation levels, and

👉 The distribution explanations and tips.

Conclusion: And that is the indicator! Hope you enjoy it!

Chips MasterChips Master, a way to tell potential chips accumulation.

There are a couple of situation where Chips Master's Yellow Bars will show up.

Firstly,

When an uptrend trend completed Dow's 12345 waves, moving into ABC waves, yellow bars will show up between MA21 and MA60

if we refer to Granville rules, it is in the vicinity of buy point number 4.

Secondly,

During a down trend, when new low is created, potentially, yellow bars will show up, an indication of chips accumulation at low price.

Feel free to provide inputs to further improve the accuracy to benefit users.

Disclaimer : Purely for Technical Analysis study. No suggestion on buy/sell.

Average Volume at Time (AVAT)Calculation of average volume at current time for a number of previous sessions, known as Average Volume at Time (AVAT).

Inputs:

* period to use for accumulation. "D" is the default value, useful to view data for each session.

* number of previous sessions to average

TODO: more intelligent accumulation of number of bars in a session, since there may be sessions with different values

TODO: interpolate volume according to current time, inside of the last bar

Advanced Chaikin Money Flow (CMF)TL;DR: change the aggregation to EMA to achieve similar results to Twiggs Money Flow. Play with the rest of parameters to get the desired results.

This script allows customization of CMF. It also includes all the improvements made by Twiggs Money flow.

Regular CMF does not take price gaps into account as you can see in the chart below. True range fixes this issue, as done in Twiggs Money flow (TMF).

More info here: www.incrediblecharts.com

Customization Options:

- You can change the effect of volume by setting volume exponent. 0 to 10 reduces the effect and 10+ increases it. In exchanges with too much wash trading, you may want to reduce volume effect.

- You can factor in price in CMF. It gives you a slightly different results. See my Volume x price (VxP) indicator for why it might be useful.

- The range can be changed to percentage (similar to RSI)

PS: I do not recommend using CMF in today's Crypto markets. Chaikin uses the same multiplier in CMF and Accumulation/Distribution Line (ADL). ADL is a totally broken indicator for BTC. If you look at the period after ATH (chart below), you will notice that ADL keeps increasing implying accumulation. While it is clear that there was distribution going on. The reason might be the artificially inflated prices in Crypto that is achieved by the help of bots and having "certain" exchanges as a price reference. So, my reasoning is that if ADL is a broken indicator, so should be CMF. CMF diverges from BTC price frequently. This is a double edged sword IMO. Still CMF is a much better indicator than ADL because it works relative to prior periods which covers some of its flaws.

Note for super nerds: Twiggs Money Flow includes true range and Welles Wilder's Moving Average (WWMA). I have seen some other scripts using their own calculations for WWMA which is not efficient. WWMA is equal to built-in RMA/SMMA which is equal to EMA with length 2x-1.

Edufx's Power of ThreeIndicator Overview

Name: Edufx's Power of Three

Purpose:

To highlight the high and low price ranges of specific hourly candles on a chart.

To visualize these ranges using rectangles.

Features

Visibility Toggle:

Users can enable or disable the visibility of the rectangles highlighting the high and low price ranges of the specified candles.

Customizable Rectangle Length:

Users can adjust the length of the rectangles that extend from the specified candle's high and low prices.

Price Range Tracking:

The high and low prices of the specified candles are tracked and stored.

Rectangle Drawing:

Rectangles are drawn from 5 bars before the end of the specified hour, highlighting the high and low price ranges.

How It Works

Price Range Tracking:

During each specified hour, the high and low prices are updated with the highest and lowest prices observed.

Rectangle Drawing:

At the end of each specified hour, the high and low prices are used to draw rectangles extending 5 bars backward from the end of the hour.

Rectangles are color-coded (red, green, and blue) for easy identification.

Usage

This indicator is useful for traders who want to monitor and react to key price levels at specific times of the day.

The visual rectangles help in identifying potential trading opportunities based on price action relative to these key levels.

Example

If the price moves above the high of the specified candle but fails to close above it, a visual rectangle will highlight this price range.

Similarly, if the price moves below the low of the specified candle but fails to close below it, the rectangle will indicate this range.

This indicator provides visual aids to assist traders in making informed decisions based on the behavior of price at specific key levels.

Dynamic Support and Resistance with Trend LinesDynamic Support and Resistance with Trend Lines (DSRTL)

1. Introduction & Methodology

The DSRTL indicator is designed to provide a multidimensional analysis of market structure. Unlike traditional tools that rely solely on price pivots, this script combines Static Volume-based Zones with Dynamic Trend Lines to evaluate the price's position relative to critical market components.

The S/R Identification Technique

Instead of standard pivot points, DSRTL utilizes Volume Analysis to highlight areas of significant trader participation:

- Strategy A:

Matrix Climax: Identifies candles within the lookback period that are near price extremes (Highs/Lows) and coincide with significant buying or selling volume.

- Strategy B:

Volume Extremes: Detects candles with the absolute highest buy/sell volumes within the selected lookback window, creating extreme volume-based S/R zones.

- Result:

This creates Support/Resistance (S/R) zones that are validated by actual market activity, not just price geometry.

Dynamic Trend Lines

To complement the static zones, the indicator employs two adaptive channel methods:

- Pivot Span: Connects recent significant pivots for a fast, reactive trend corridor.

- 5-Point Channel: Segments the lookback period into 5 parts to perform a linear regression analysis, creating a stable and statistically significant channel.

2. Volume Calculation Methodology

Accurate S/R detection requires distinguishing Buy Volume from Sell Volume. DSRTL offers two calculation modes:

- Geometry (Source File): Estimates buy/sell volume based on the Close price's position relative to the High/Low of the candle.

Note: This is an approximation that works on all plan types as it does not require intrabar data.

- Intrabar (Precise): Analyzes historical lower-timeframe data (e.g., 15S) to calculate intrabar-based volume deltas with higher precision compared to the geometric method.

Note: This offers superior accuracy. It requires access to historical intrabar data (depending on your plan limits). For the best analytical results, use this mode if available.

3. The Smart Matrix Engine (3D Analysis)

The core of DSRTL is its dashboard, powered by the "Smart Matrix Engine." This engine evaluates the current price in a multi-layer market structure context (Static Volume Zones + Dynamic Channels + Volume Metrics).:

A. S-State (Static): Where is the price relative to the Volume S/R zones?

B. D-State (Dynamic): Where is the price relative to the Trend Channels?

How to read the Matrix Map:

The dashboard displays a 5x5 grid representing 25 possible market scenarios.

- Rows (S1-S5): Represent the Static State (S1=Breakout, S3=Mid-Range, S5=Breakdown).

- Columns (D1-D5): Represent the Dynamic State (D1=Overextended Up, D3=Neutral, D5=Overextended Down).

- Active Cell: Marked with a dot, indicating the specific intersection of price action and market structure.

4. Matrix Interpretations (The 25 Scenarios)

Below is the detailed logic for every possible state displayed on the dashboard, explaining the Title, Bias, and actionable Signal.

Section I: S1 - Static Breakout (Price > Static Resistance)

The price has cleared the static volume resistance zone.

- S1 / D1: HYPER EXTENSION

Bias: Extreme Bullish

Signal: Caution: Exhaustion Risk. Trail stops tight.

- S1 / D2: RESISTANCE CLASH

Bias: Bullish

Signal: Breakout confirmed but facing immediate dynamic resistance.

- S1 / D3: CHANNEL BREAKOUT

Bias: Strong Bullish

Signal: Ideal Trend Continuation. Look to buy dips.

- S1 / D4: SMART PULLBACK

Bias: Bullish (Pullback)

Signal: A pullback occurring after a breakout. Strong buy opportunity.

- S1 / D5: CONFLICT (DIV)

Bias: Conflict/Reversal

Signal: Major Divergence. Static breakout is failing against dynamic structure. High Risk.

Section II: S2 - Inside Static Resistance

The price is currently testing the overhead resistance zone.

- S2 / D1: WEAK SPIKE

Bias: Neutral/Bullish

Signal: Testing resistance, but short-term overextended.

- S2 / D2: IRON FORTRESS (R)

Bias: Rejection Risk

Signal: Double Resistance (Static + Dynamic). High probability of rejection.

- S2 / D3: TESTING RES

Bias: Neutral

Signal: Consolidating at resistance. Wait for a clear break or rejection.

- S2 / D4: COMPRESSION (UP)

Bias: Conflict (Squeeze)

Signal: Squeezed between Static Resistance and Dynamic Support. Volatility imminent.

- S2 / D5: RES vs DOWN-TREND

Bias: Bearish

Signal: Strong downtrend meeting static resistance. Potential Short entry.

Section III: S3 - Mid-Range

The price is floating between significant Static Support and Resistance.

- S3 / D1: OVERBOUGHT RANGE

Bias: Rejection Risk (OB)

Signal: Overextended within the range. Potential fade (short).

- S3 / D2: RANGE HIGH LIMIT

Bias: Neutral/Bearish

Signal: At the top of the dynamic channel. Look for rejection signs.

- S3 / D3: NEUTRAL / CHOPPY

Bias: Neutral

Signal: Dead Center. Low probability environment. Avoid trading.

- S3 / D4: RANGE DIP BUY

Bias: Neutral/Bullish

Signal: At the bottom of the dynamic channel. Look for bounce signs.

- S3 / D5: WEAK RANGE (OS)

Bias: Bounce Risk (OS)

Signal: Oversold within the range. Potential fade (long).

Section IV: S4 - Inside Static Support

The price is currently testing the floor support zone.

- S4 / D1: SUP vs UP-TREND

Bias: Bullish

Signal: Strong uptrend meeting static support. Potential Long entry.

- S4 / D2: COMPRESSION (DN)

Bias: Conflict (Squeeze)

Signal: Squeezed between Static Support and Dynamic Resistance. Volatility imminent.

- S4 / D3: TESTING SUPPORT

Bias: Neutral

Signal: Consolidating at support. Wait for a bounce or breakdown.

- S4 / D4: IRON FLOOR (S)

Bias: Bounce Risk

Signal: Double Support (Static + Dynamic). High probability of a bounce.

- S4 / D5: WEAK DIP

Bias: Neutral/Bearish

Signal: Testing support, but short-term oversold.

Section V: S5 - Static Breakdown (Price < Static Support)

The price has dropped below the static volume support zone.

- S5 / D1: CONFLICT (DIV)

Bias: Conflict/Reversal

Signal: Major Divergence. Static breakdown is failing. High Risk.

- S5 / D2: BEAR PULLBACK

Bias: Bearish (Pullback)

Signal: A pullback occurring after a breakdown. Strong selling opportunity.

- S5 / D3: CHANNEL BREAKDOWN

Bias: Strong Bearish

Signal: Ideal Trend Continuation (Down). Sell rallies.

- S5 / D4: SUPPORT CLASH

Bias: Bearish

Signal: Breakdown confirmed but facing immediate dynamic support.

- S5 / D5: HYPER DROP (VOID)

Bias: Extreme Bearish

Signal: Caution: Climax risk. Trail stops for shorts.

DISCLAIMER & EDUCATIONAL PURPOSE

This indicator is strictly an educational tool designed to visualize complex market structure concepts. Its primary purpose is to help traders "bridge the gap" between academic theory and real-time market behavior by providing a visual representation of support, resistance, and volume dynamics.

Please Note:

1. Not a Trading Strategy: This script is an analytical assistant, not a standalone "Black Box" trading system. It does not generate buy or sell signals that should be followed blindly.

2. No Financial Advice: The data provided by this tool is for informational purposes only. It is not a recommendation to buy or sell any asset.

3. Risk Warning: Trading involves significant risk. Always use your own judgment, perform your own technical analysis, and use proper risk management. Do not use this tool as the sole basis for your trading decisions.

4. Data Precision & Platform Limits: The "Intrabar (Precise)" calculation mode relies on high-resolution historical data to provide exact results. Access to this specific data depth depends entirely on your platform's subscription capabilities. If your plan does not support this level of historical intrabar data, the Precise mode may have limited coverage. In that case, you should switch to "Geometry" mode for a fully populated view.

FluidFlow OscillatorFluidFlow Oscillator: Study Material for Traders

Overview

The FluidFlow Oscillator is a custom technical indicator designed to measure price momentum and market flow dynamics by simulating fluid motion concepts such as velocity, viscosity, and turbulence. It helps traders identify potential buy and sell signals along with trend strength, momentum direction, and volatility conditions.

This study explains the underlying calculation concepts, signal logic, visual cues, and how to interpret the professional dashboard table that summarizes key indicator readings.

________________________________________

How the FluidFlow Oscillator Works

Core Mechanisms

1. Price Flow Velocity

o Measures the rate of change of price over a specified flow length (default 40 bars).

o Calculated as a percentage change of closing price: roc=close−closelen_flowcloselen_flow×100\text{roc} = \frac{\text{close} - \text{close}_{len\_flow}}{\text{close}_{len\_flow}} \times 100roc=closelen_flowclose−closelen_flow×100

o Smoothed by an EMA (Exponential Moving Average) to reduce noise, generating a "flow velocity" value.

2. Viscosity Factor

o Analogous to fluid viscosity, it adjusts the flow velocity based on recent price volatility.

o Volatility is computed as the standard deviation of close prices over the flow length.

o The viscosity acts as a damping factor to slow down the flow velocity in highly volatile conditions.

o This results in a "flow with viscosity" value, that smooths out the velocity considering market turbulence.

3. Turbulence Burst

o Captures sudden changes or bursts in the flow by measuring changes between successive viscosity-adjusted flows.

o The turbulence value is a smoothed absolute change in flow.

o A burst boost factor is added to the oscillator to incorporate this rapid change component, amplifying signals during sudden shifts.

4. Oscillator Calculation

o The raw oscillator value is the sum of flow with viscosity plus burst boost, scaled by 10.

o Clamped between -100 and +100 to limit extremes.

o Finally, smoothed again by EMA for cleaner visualization.

________________________________________

Signal Logic

The oscillator works with complementary components to produce actionable signals:

• Signal Line: An EMA-smoothed version of the oscillator for generating crossover-based signals.

• Momentum: The rate of change of the oscillator itself, smoothed by EMA.

• Trend: Uses fast (21-period EMA) and slow (50-period EMA) moving averages of price to identify market trend direction (uptrend, downtrend, or sideways).

Signal Conditions

• Bullish Signal (Buy): Oscillator crosses above the oversold threshold with positive momentum.

• Bearish Signal (Sell): Oscillator crosses below the overbought threshold with negative momentum.

Statuses

The oscillator provides descriptive market states based on level and momentum:

• Overbought

• Oversold

• Buy Signal

• Sell Signal

• Bullish / Bearish (momentum-driven)

• Neutral (no clear trend)

________________________________________

Color System and Visualization

The oscillator uses a sophisticated HSV color model adapting hues according to:

• Oscillator value magnitude and sign (positive or negative)

• Acceleration of oscillator changes

• Smooth color gradients to facilitate intuitive understanding of trend strength and momentum shifts

Background colors highlight overbought (red tint) and oversold (green tint) zones with transparency.

________________________________________

How to Understand the Professional Dashboard Table

The FluidFlow Oscillator offers an integrated table at the bottom center of the chart. This dashboard summarizes critical indicator readings in 8 columns across 3 rows:

Column Description

SIGNAL Current signal status (e.g., Buy, Sell, Overbought) with color coding

OSCILLATOR Current oscillator value (-100 to +100) with color reflecting intensity and direction

MOMENTUM Momentum bias indicating strength/direction of oscillator changes (Strong Up, Up, Sideways, Down, Strong Down)

TREND Current trend status based on EMAs (Strong Uptrend, Uptrend, Sideways, Downtrend, Strong Downtrend)

VOLATILITY Volatility percentage relative to average, indicating market activity level

FLOW Flow velocity value describing price momentum magnitude and direction

TURBULENCE Turbulence level indicating sudden bursts or spikes in price movement

PROGRESS Oscillator's position mapped as a percentage (0% to 100%) showing proximity to extreme levels

Rows Explained

• Row 1 (Header): Labels for each metric.

• Row 2 (Values): Current numerical or descriptive values color-coded along a professional scheme:

o Green or lime tones indicate positive or bullish conditions.

o Red or orange tones indicate caution, sell signals, or bearish conditions.

o Blue tones indicate neutral or stable conditions.

• Row 3 (Status Indicators): Emoji-like icons and bars provide a quick visual gauge of each metric's intensity or signal strength:

o For example, "🟢🟢🟢" suggests very strong bullish momentum, while "🔴🔴🔴" suggests strong bearish momentum.

o Progress bar visually demonstrates oscillator movement toward oversold or overbought extremes.

________________________________________

Practical Interpretation Tips

• A Buy signal with green colors and strong momentum usually precedes upward price moves.

• An Overbought status with red background and red table colors warns of potential price corrections or reversals.

• Watch the Turbulence to gauge market instability; spikes may precede price shocks or volatility bursts.

• Confirm signals with the Trend and Momentum columns to avoid false entries.

• Use the Progress bar to anticipate oscillations approaching key threshold levels for timing trades.

________________________________________

Alerts

The oscillator supports alerts for:

• Buy and sell signals based on oscillator crossovers.

• Overbought and oversold levels reached.

These help traders automate awareness of important market conditions.

________________________________________

Disclaimer

The FluidFlow Oscillator and its signals are for educational and informational purposes only. They do not guarantee profits and should not be considered as financial advice. Always conduct your own research and use proper risk management when trading. Past performance is not indicative of future results.

________________________________________

This detailed explanation should help you understand the workings of the FluidFlow Oscillator, its components, signal logic, and how to analyze its professional dashboard for informed trading decisions.

Daily 6 AM & 8 AM CST Linesit help so you can figure out 6am and 8am on cst time in americas very fast.

CVDD Z-ScoreCumulative Value Days Destroyed (CVDD) - The CVDD was created by Willy Woo and is the ratio of the cumulative value of Coin Days Destroyed in USD and the market age (in days). While this indicator is used to detect bottoms normally, an extension is used to allow detection of BTC tops. When the BTC price goes above the CVDD extension, BTC is generally considered to be overvalued. Because the "strength" of the BTC tops has decreased over the cycles, a logarithmic function for the extension was created by fitting past cycles as log extension = slope * time + intercept. This indicator is triggered for a top when the BTC price is above the CVDD extension. For the bottoms, the CVDD is shifted upwards at a default value of 120%. The slope, intercept, and CVDD bottom shift can all be modified in the script.

Now with the automatic Z-Score calculation for ease of classification of Bitcoin's valuation according to this metric.

Created for TRW.

Previous Day Liquidity ZonesThis indicator is designed for intraday liquidity-based trading strategies and helps traders identify high-probability reversal or breakout zones based on smart money concepts.

It automatically plots the:

🟥 Previous Day High Zone – potential buy-side liquidity trap

🟩 Previous Day Low Zone – potential sell-side liquidity trap

🟧 Previous Day Close Zone – potential rebalancing or indecision zone

These levels are critical areas where institutional stop-hunting, reversals, and fake breakouts often occur.

🎯 How to Use

Use this indicator on 1-minute or 5-minute charts for stocks, indices (like NIFTY, BANKNIFTY), or forex.

Watch for price entering these zones during live market hours.

Combine with price action confirmation:

Rejection wicks

Engulfing candles

Change of character (CHoCH) or BOS

Fair Value Gaps (FVG)

First 5-minute candle (9:15 AM in Indian market) is highlighted for breakout setups.

🧠 Smart Money Logic

These zones mimic the logic used by institutions to:

Trigger retail stop-losses

Reverse market direction near liquidity pools

Trap breakout traders around session extremes

⚙️ Features

Configurable zone width (%)

Visual fill zones with subtle shading

Support for all assets and timeframes

Highlights first candle of day to assist with pre-trade bias

✅ Ideal For:

Smart money traders

ICT / Wyckoff / SMC followers

Breakout trap or reversal strategy users

Anyone who trades key session levels

⚠️ Disclaimer

This is an informational tool. Always use confirmation and sound risk management before executing any trade.

[Teyo69] T1 Wyckoff Aggressive A/D Setup📘 Overview

The T1 Wyckoff Aggressive A/D Setup is a dual-mode indicator that detects bullish accumulations and bearish distributions using core principles from the Wyckoff Method. It identifies price/volume behavior during Selling/Buying Climaxes, ARs, SOS/SOW, and triggers based on trend structure.

🔍 Features

✅ Automatic detection of:

Automatic Rally (AR)

Automatic Reaction (AR)

Sign of Strength (SOS) or Sign of Weakness (SOW)

🧠 Trend-sensitive logic with linear regression slope filters

⚙️ Configurable options for Reversal vs Trend Following mode

🎯 Smart structure timing filters using barssince() logic

🔊 Volume spike and wide-range candle detection

📊 Visual cues for bullish (green) and bearish (red) backgrounds

🛠 How to Use

Reversal Mode

Triggers early signals after a Climax + AR

Ideal for catching turning points during consolidations

Trend Following Mode

Requires Climax, AR, and confirmation (SOS or SOW)

Waits for structure confirmation before signaling

Use this when you want higher probability trades

⚙️ Configuration

Volume MA Length - Determines baseline volume to detect spikes

Wick % of Candle - Filters candles with long tails for SC/BC

Close Near Threshold - Ensures candles close near high/low

Breakout Lookback - Sets structure breakout level

Structure Threshold - Controls timing window for setups

Signal Option - Switch between Reversal or Trend Following mode

⚠️ Limitations

Doesn't confirm macro structure like full Wyckoff phase labeling (A–E)

May repaint on lower timeframes during volatile candles

Works best when combined with visual range recognition and market context

🧠 Advanced Tips

Use in confluence with:

Volume Profile ranges

Trendlines and supply/demand areas

Ideal timeframes: 8H to 1D for crypto and forex markets

Combine this with LPS/UTAD patterns for refined entries

📝 Notes

SC/AR/SOS = Bullish

BC/AR/SOW = Bearish

Trend coloring adapts background (green = rising slope, red = falling slope)

🛡️ Disclaimer

This tool is a market structure guide, not financial advice. Past behavior does not guarantee future performance. Always use proper risk management.

ICT Dealing RangeICT Dealing Range

This indicator identifies and plots ICT (Inner Circle Trader) Dealing Ranges - key institutional areas where smart money accumulates or distributes positions before significant moves.

What is a Dealing Range?

A Dealing Range is a significant price area where institutional traders accumulate or distribute their positions. These ranges form through a specific sequence of price movements that indicate institutional order flow:

Bullish Dealing Range Sequence:

1. Initial High (H)

2. Initial Low (L)

3. Higher High (HH)

4. Lower Low (LL)

5. Break above HH (confirmation)

Bearish Dealing Range Sequence:

1. Initial Low (L)

2. Initial High (H)

3. Lower Low (LL)

4. Higher High (HH)

5. Break below LL (confirmation)

My Trading Strategy

Entry Methods:

1. Range Extreme Retests:

- After range formation, wait for price to return to either extreme

- Long entries at range bottom with stops below

- Short entries at range top with stops above

2. Mid-Line Strategy:

- Use the mid-line as a pivot point for reversals

- Long entries on mid-line bounce with stops below

- Short entries on mid-line rejection with stops above

Stop Loss Placement:

- When entering at extremes: Place stops beyond the mid

- When entering at mid-line: Place stops beyond the opposing extreme

- Always respect the structure's boundaries

Take Profit Targets:

- Minimum 2:1 Risk-Reward ratio

- For extreme entries: Target the opposite extreme

- For mid-line entries: Target the nearest extreme

Risk Management

- Never enter without a clear invalidation point

- Maintain minimum 2:1 RR ratio

- Consider market structure and higher timeframe context

Indicator Features

- Auto-detection of dealing range patterns

- Color-coded boxes (green for bullish, red for bearish)

- Optional mid-line display

- Customizable colors and styles

- Adjustable pivot lookback periods

Notes

This tool is based on ICT concepts but should be used in conjunction with other forms of analysis. The dealing range provides a framework for understanding institutional order flow, but proper risk management and market context are essential for successful trading.

Remember: The best trades often come from clean retests of these ranges after their initial formation. Patience in waiting for proper setups is key to successful implementation.

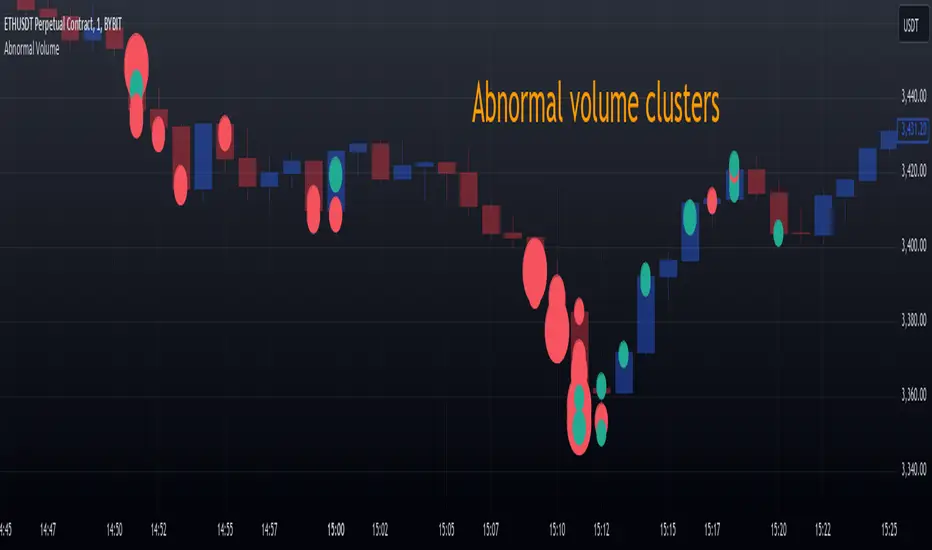

Abnormal volume [VG]🪙 INTRODUCTION

This technical indicator helps identify and highlight large volume clusters on the chart.

Abnormal volume refers to unusually large accumulations of volume over short time intervals. Such clusters appear when the amount of assets bought or sold significantly exceeds typical volumes for a specific asset over a given period. These patterns can indicate significant events or intentions of market participants.

Reasons for abnormal volume clusters:

Institutional investments :

Large investment funds and banks may buy or sell significant volumes of assets to rebalance their portfolios.

Impact of news and events :

Important news (e.g., mergers, bankruptcies, management changes) can trigger large-scale buying or selling of assets.

Market manipulation :

Big players may execute large trades to artificially create demand or supply for an asset, affecting its price in the short term.

Insider trading :

Abnormal volumes may signal that someone with insider information has started buying or selling assets in anticipation of future events that could impact the price.

What do abnormal volume clusters mean for traders?

A signal of potential price changes :

High trading volumes are often accompanied by sharp price movements. An increase in volume during price growth might indicate rising interest in the asset, while an increase during a decline could signal a sell-off.

Potential entry or exit points :

For short-term traders, abnormal trades can serve as signals to enter or exit positions. For example, a large volume growth accompanied by a breakout of a key level might be seen as a buy signal.

Caution due to potential manipulation :

Abnormal trades don’t always lead to expected outcomes. Sometimes, they are part of a price manipulation strategy, so it’s essential to consider the broader context and confirm with other signals.

🪙 USAGE

This indicator doesn’t provide trading signals, entry points, or actionable recommendations.

Instead, it simplifies tracking market dynamics and highlights unusual activity worth considering during analysis.

After adding the indicator to the chart, you only need to configure two parameters: the threshold value that determines what constitutes a significant volume cluster and the period over which volumes are aggregated for comparison against the threshold.

It’s recommended to use the shortest available period, as this helps more precisely identify the prevailing volume direction (since this depends on price changes, not trade direction).

The threshold value can be fine-tuned by switching the chart’s timeframe to match the selected period, observing of the significant volume increase on the classic volume histogram, and noting the corresponding market reactions. This allows for selecting a threshold that highlights early signs of impactful trading events on higher timeframes.

Let’s look at an example in the screenshot:

Once the parameters are set, you can also enable an alert to trigger whenever a new volume cluster appears, simplifying event tracking.

Note: in the current version of the indicator, the alert will be triggered only once per bar on the chart at the first detected cluster of abnormal volume.

🪙 IMPLEMENTATION

Technically, the script retrieves volume data from a lower timeframe and estimates whether the volume was primarily generated by buyers or sellers based on price movements.

The lower resolution timeframe is determined as follows:

if the settings base period is less than 1 minute, then the data timeframe will be equal to 1 second

if the settings base period is equals 1 minute or more, then the data timeframe will be equal to 1 minute

The algorithm checks whether the price increased or decreased at each point. If the price rose, the volume is presumed to be driven by buyers and marked as buy volume; otherwise, it’s marked as sell volume.

The total volume at each point is then checked against the user-defined threshold. If the volume exceeds the threshold, a corresponding circle is drawn on the chart, and an alert is generated if created.

The size of the visual representation is proportional to the most recent maximum volume and follows the rules below:

Percentage of max volume -> Volume cluster size

less than 25% -> Tiny

25% to 50% -> Small

50% to 75% -> Normal

75% to 100% -> Large

100% or more -> Huge

🪙 SETTINGS

The indicator is designed to be as simple and minimalist as possible, making configuration effortless. There are only two core parameters, with additional options to customize the colors of volume clusters based on their type.

Trade volume threshold

Defines the volume level above which a cluster is considered significant and displayed on the chart as a circle. The size of the circle depends on the proportion of the current volume relative to the most recent maximum over the chosen period.

Trades base period

Specifies the period for aggregating trade volumes to determine whether they qualify as abnormal. The significance level is set using the Trade volume threshold parameter.

Buy/Sell trades

Allows you to set the colors for abnormal volume circles based on the price direction during cluster formation.

🪙 CONCLUSION

Abnormal volume clusters are always a critical indicator requiring attention and analysis, but they are not a guaranteed predictor of trend changes.

ADMAThe ADMA indicator is a technical analysis tool designed to identify trends and potential reversal points in a financial market. The indicator is based on the cumulative difference between the closing price and the high and low points of a candle. Two moving averages (MAs) are used to smooth the trend dynamics and generate clear signals.

Calculation:

The indicator calculates the trend as the cumulative difference between the current closing price and the maximum (or minimum) value of the current and previous candle, depending on market development.

The ADMA indicator is particularly useful for recognizing market dynamics and making trading decisions based on them. By using double smoothing, false signals are reduced, and the signals generated by the indicator are clear and easy to interpret. It is a flexible tool that can be adapted to different trading strategies.