Cipher B divergencies for Crypto (Finandy support)Hello Traders!

In times of high volatility, it is important to follow a market-neutral strategy to protect your hard-earned assets. The simple script employs common buy/sell and/or divergencies signals from the VuManChu Cipher B indicator with fixed stop losses and takes profits. The signals are filtered by a local trend of a coin of interest and the global trend of Bitcoin. These trends-filtered signals demonstrated better performance on most of the back- and forward- tests for USDT cryptocurrency futures. The strategy is based on my real experience, it's a diamond I want to share with you.

In terms of visualization if the background is red and the price is below the yellow line then only a short position can be opened. Conversely, if the price is above the yellow line AND the background is green only a long position can be opened.

Inputs from VuManChu you can find on the top. Frankly, I do not know how they can help you to improve the performance of the strategy. My inputs of the script you can find in "Trend Settings" and "TP/SL Settings" at the bottom.

The checkbox "Only divergencies" lets to broadcast only more reliable buy/sell signals for a cost of rare deals.

The checkbox "Cancel all positions if price crosses local sma?" makes additional trailing stop loss. Usually, this function increases the win rate by "smoothing" the risk/reward ratio, as a usual stop loss does.

You can tune SL/TP based on backtesting.

To connect the script to Finandy just edit "name" and "secret" to connect your webhook (see the bottom of the script).

The rule of thumb for the strategy is "only divergencies" - ON, high reward/risk (TP/SL) ratio, 5 min timeframe on chart help with performance.

Finally, I am looking forward to feedback from you. If you have some cool features for my script in your mind, do not hesitate to leave them in the comments.

Good luck!

Buscar en scripts para "Futures"

SGX Nifty Movement During Indian Market HoursSGX Nifty or Singapore Nifty is a derivative contract of the Nifty 50 index which is the benchmark index of NSE in India. SGX Nifty trades for 21 hours in a day while Nifty 50 trades only for 6 hours and 15 minutes. Traders in India miss out on a lot of price action which happens on the Singapore Nifty. This code which is originally inspired from @Gustavorubi has been modified to track SGX Nifty's movements outside Indian market hours. This will help intraday traders to identify support and resistance levels which are not seen on Nifty 50 futures.

This source code is inspired from GustavoRubi's code on FX Sessions.

Overnight inventoryThe indicator is dedicated for market / volume profile traders. It presents overnight inventory as a yellow number next to the indicator name on your charts. It does not plot anything.

If the number is positive then the inventory is net long and vice versa.

It is calibrated for US indicies, so it makes sense to use it only on US futures.

action zone - ATR stop reverse order strategy v0.1 by 9nckACTION ZONE-ATR MOD v0.1 DOCUMENTATION

Overview

This tradingview pine script strategy is mainly created to enrich my coding skill. It is a combination of “CDC-ACTIONZONE” and my personal studies of trading techniques in various sources e.g.book, course or blog. This strategy purposefully built to connect with my automatic trading bot. However, It will be very useful to aid your trading routine by diminishing mental distraction which possibly leads to bad trades.

How does it work?

This strategy will do a basic simple thing that most traders do by creating entry signals on both sides long/short and also set the stop loss. Furthermore, It will also reverse the order (from long to short and vice versa (if long/short conditions are met). Finally, it will recalculate the stop loss/take profit price in every complete bar to increase the chance of winning and limit our loss.

Entry rules(Long/Short)

If you have no open order, an order will be created when a fast EMA crosses(up(long)/down(short) the slow EMA(It’s as simple as that).

If you have an open order, the current order will be (sold if long, covered if short) and the opposite side order will be created.

Exit and Reverse rules(Long/Short)

If fast EMA cross (DOWN(long), UP(short)), the current order will be closed, THE OPPOSITE SIDE ORDER WILL ALSO BE CREATED.

Risk management

FLEX STOP PRICE : initial value will be set at the bar which order created. It is a fast ema (+/-) MIDDLE ATR value.

If MIDDLE ATR value rises, it will be our new stop price.

If MIDDLE ATR value falls, stop price unchanged

If Price OVERBOUGHT(long)/SOLD(short), LOW of that bar will be a new stop price.

Minimum position hold period

In order to eliminate risk of repeatedly open, close orders in sideway trends. Minimum hold period must be passed to start exit our position. However, It always respects stop loss prices. The value refers to the number of bars.

MUST READ!!!

This strategy uses only MARKET ORDER. If you trade with a bot, make sure you choose only enormous market cap tokens.

This strategy is bi-direction strategy. It will work best in the DERIVATIVE market.

It was initially designed to compete in the cryptocurrency market which has very high volume and volatility.

I only use this strategy in 1HR (acceptable change rate, optimum trade frequency)

How (should) we use it?

Choose crypto future pairs (recommend only top 10-15 market volume pairs in Binance, let’s say 1000M+ trade value)

Choose your time frame (1H is strongly recommended)

Setup your portfolio profile (Setting->Properties) such as Initial cap, order size, commission. DO NOT USE CAL ON EVERY TICK IT WILL CAUSE REPAINTING AND YOUR CAPITAL IS BLEEDING !!!

BACKTEST FIRST!! Back test is a combination of art, math and statis(and a bit of luck). You can apply to train and test methods or whatever you are familiar with. In my opinion, your test period should include UPTREND, SIDEWAY, DOWNTREND. Fine tune fast, slow ema first(my best ema length of 1H timeframe around 7-10, 17-22). Try to eliminate fault breakout trade and use other options only necessary. Hopefully we can use automatic optimization on Pine Script soon.

Don’t forget to turn off using a specific backtest date option to start your strategy.A

THIS IS NOT A PERFECT (OR EVEN PROFITABLE) STRATEGY. USE AT YOUR OWN RISK AND TRADE RESPONSIBLY. DYOR DUDE.

ADX and DI LevelsADX:

ADX is used to quantify trend strength. ADX calculations are based on a moving average of price range expansion over a given period of time. The default setting is 14 bars, although other time periods can be used.1

ADX can be used on any trading vehicle such as stocks, mutual funds, exchange-traded funds and futures.

DI (+/-):

The directional movement index (DMI) is an indicator developed by J. Welles Wilder in 1978 that identifies in which direction the price of an asset is moving. The indicator does this by comparing prior highs and lows and drawing two lines: a positive directional movement line (+DI) and a negative directional movement line (-DI). An optional third line, called the average directional index (ADX), can also be used to gauge the strength of the uptrend or downtrend.

This indicator has the length changed from 14 to 9 so you can have more updated price calculation

I also add the 4 levels I use for day trading; the 10, 20, 30, 40-50 are the levels I like to see the Di to break over.

A lot of traders use different levels, but these I have and found most useful. You can set alerts when any Di crosses over the 40 for true trend breakout!

Baekdoo multi OverSold OverBuy colored CandleHi forks,

I'm trader Baekdoosan who trading Equity from South Korea. This Baekdoo multi OverSold OverBuy colored candle will give you the idea of

multiple indicators in one shot with colored candle. Those indicators tell us that oversold or overbuy statistically. For the color, you can freely change

based on your comfort. For me, in Korea white candle has red color and black candle has blue color. So somewhat confusing for you. Anyway you can

easily modify color in the script. Please refer this line.

barcolor(open<close and result_pos == 4 ? color.new(color.red, 0) : open<close and result_pos == 3 ? color.new(color.red, 25) : open<close and result_pos == 2 ? color.new(color.red, 50) : open<close and result_pos == 1? color.new(color.red, 75) : na)

you can see I put different transparency at color.new() function with color code. Let me divide and conquer to explain for up candle

white candle and black candle.

1. White candle

with 4 oversold signal case with white candle tells us it is almost reached real bottom and try to rebound. In this case, I put vivid color (no transparency) on the candle. And all 4 signal case, I put text on "OverSold". It will not happen frequently. Then 2 approaches can be made.

(a) short term approach

You can buy on this time. and you set stop loss with open price. This is mainly aimed for technical rebound.

(b) long term approach

You can accumulate based on your budget with 5 times dividing. At that day might not be the very bottom but those period will most probably real bottom. You can put more weight on latter buy. Let say, 1 : 1.25 : 1.5 : 1.75 : 2.5. So for example, if you have $8,000 to investigate then, buy $1,000 and then $1,250, $1,500, accordingly. If price rebound then don't adding weight on accumulation but with the first amount that you buy(i.e., $1,000 with above example). With this approach, you will not have much stress and you will get profit well. If this is grand bottom case, then you can HODL this long term. What you needs is stick to the plan. :)

with 3 signals the color is less vivid, 2 signals is much less vivid, accordingly.

2. Black candle

The approaches are opposite to above. The signal will tells us for 4 overBuy signals, then vivid blue candle will be shown. Our strategy is distribute to sell. Please do not sell in one shot. As Newton said, "I can calculate the motions of the heavenly bodies, but not the madness of the people". Strong buy phase, we don't know how far will it go. But indicators will tell us it is quite overSold situation. So what I can suggest you is sell it 10% to 20% on resistance price, and put 50% of lower than certain support price. Remember, accumulation and distribution will always better than one shot trading if you want to survive long time on this war field.

Hope this will help your trading on equity as well as crypto. I didn't try it on futures. Best of luck all of you. Gazua~!

Baekdoo ANGNHi forks,

I'm trader Baekdoosan who trading Equity from South Korea. This Baekdoo ANGN indicator plot volume when large volume trading happened.

Assume that the large volume means higher than 1% of its marketcap amount. And adding ANGN (An-Na-Gan-Ni?, means "are you still there? in Korean")

line for upgrade version of On Balance Volume (OBV).

OBV is very good indicator but when it has long tail and short body, it can have wrong indication of buying or selling from big whales. So ANGN with large volume indicator combination would gives you better idea for the big brothers buying or selling tracker.

hope this will help your trading on equity as well as crypto. I didn't try it on futures. Best of luck all of you. Gazua~!

Baekdoo baselineHi forks,

I'm trader Baekdoosan who trading Equity from South Korea. This Baekdoo baseline will give you the idea of big whale's approximate average price. The idea behind this indicator is to combine volume and price. Here's one of the equation.

...

HT4=highest(volume, 250)

NewH4=valuewhen(volume>HT4 , (open+close+low+high+close)/5, 1)

result4=ema(NewH4, 20)

...

As you can see it will update when highest volume is updated by certain period of time. At that update will be the price of the close weighted price. and I put shift value of 20 (offset of input value) due to putting time theorem of Ichimoku Balance Table. 20 days means for 1 month of market day.

Why this idea work? It is mainly for the support / resistance. Resistance is made for lots of individual's buy. When the price goes down, they are tend to hold. As time goes by price getting high to their average price, then they are selling it with small profit or the same price or with small loss. So resistance is made by lots of individuals. And supports are made by small number of big whales. If we see the volume only, then we cannot differentiate easily for lots of individuals and small number of big whales. But lower price's large volume will most probably be the whale where higher price's large volume will most probably tons of individuals.

hope this will help your trading on equity as well as crypto. I didn't try it on futures. Best of luck all of you. Gazua~!

Customizable Gap FinderThis is a fully customizable gap finder. You can change the color of just about anything, on top of hiding filled/old gaps. This is so you can spot those tiny gaps on something such as futures. Be sure to play around with the settings.

RSI Classic Strategy (by Coinrule)One of the questions hobbyist traders more often ask is: what is the perfect trading indicator?

Every indicator is just a tool, so its efficiency is proportional to your ability to read its signals and translate them into an actionable trading strategy. The RSI is likely the most flexible and easy to use among the technical indicators.

This trading strategy tries to catch short-term swings on the coins of your choice with a simple yet profitable setup.

Buy when the RSI is lower than 30 (you can adjust it to 35 in times of steep uptrend).

Sell when the RSI is greater than 65 (the target may range between 60 and 75 depending on the volatility of the coin).

Note that the buy signal comes when the indicator crosses below 30 and not when it crosses above 30 as it happens on the built-in RSI strategy on Tradingview.

The present script overperforms the built-in strategy, even adding trading fees and using a lower amount of capital for each trade (30%). That means that the system can deliver higher net-profits with lower risk levels.

A typical example of market conditions where this strategy works perfectly is as follows.

The first initial breakout indicates that a new leg up in the trend may start. Bitcoin starts to trade within a range which you can identify when it reaches the point 3. That is the perfect time to start the rule because

- trading within a channel anticipates possible swings up and down

- the trend is on the upside, providing low downside risk in buying the dips.

This strategy works well with selected coins of your choice, and it's a great fit on leverage exchanges like Binance Futures.

If you prefer to run it across all available coins on the market, instead, you may choose an optimized version.

Normalized Volatility IndicatorFrom an article by Rajesh Kayakkal:

"Early bear phase signals can help you get out of the market before it turns down. This indicator tells you how.

There are many ways to identify the trend of a financial market, the most common being the 200-day exponential moving average (Ema). When price is trending down below the 200-day Ema, the market is believed to be in a bear phase. If the market is trending up above the 200-day Ema, it is considered to be in a bull phase.

Since every indicator fails at times, I wanted to find other indicators to confirm a trend. In my quest for another indicator to determine the trend for the financial markets, I found the Cboe Volatility Index (Vix) to be a good indicator of the market direction. The Vix is calculated from the weighted average of the implied volatilities of various options on the Standard & Poor’s 500 index futures.

J. Welles Wilder’s average true range can also give an indication of the financial market trends; that is, when the market is in a bull phase, the average true range narrows, and when it is in a bear phase, the average true range expands. The normalized volatility indicator (Nvi) is based on this behavior.

Normalized volatility indicator (Nvi)

Average true range (Atr) varies depending on time. But how do we determine the phase of the financial market with Atr? Perhaps some type of ratio could give us a clue. A ratio presents a relationship of a quantity with respect to another. I did some research based on a ratio of the 64-day average true range and the end-of-day value of equity indexes such as the Standard & Poor’s 500 (Spx). I selected the 64-day period since it is close to the average number of trading days in a quarter. The ratio of the 64-day average true range and closing price does discount seasonal variations in the average true range and gives a single number that can be used to compare volatility of an instrument across many decades. I call this ratio the normalized volatility indicator.

I found an interesting correlation between Nvi and cycles of major equity market indexes. The formula for the Nvi is:

Nvi = 64 - Day average true range/End-of-day price * 100

The NVI gave advanced signals before the cyclical bear phase of SPX commenced in October 2000 and was almost on the spot with the bull phase that began in 2003 and the current secular bear market cycle, which started in November 2007."

Includes options to show inverse NVI and change the ATR length and smoothing.

Equity Index Overnight FakeoutThis script highlights when price violates the highest high or lowest low within the user's selected lookback period, with the caveat that it occurs during the GLOBEX session. The script is designed to work exclusively with the trading hours for CME and CBOT Equity Index futures. I'm planning to make a more customizable version down the line.

My reasoning behind this very simple script is that the low liquidity and participation of the overnight session creates a tendency for moves at extremes to mean revert. Let me know what you think.

Relative Strength Index of EU and US Stock Index Trends quality//Relative Strength Index of European and US Stock Index Trends quality

//This indicator reveals the relative strength of European and US stock index futures.

//take Bull trend as an example , the current closed price>EMA20 value and the current closed price >20th previous bar closed price( deduction price),

//it's defined as a lower level bull trend .If the current price EMA20>EMA60, it's defined as a higher level bull trend .If the EMA20>EMA60>EMA120,it's defined as the highest level bull trend.

//You can choose to draw the curve with the deviation rate of the original major indexes to 20EMA, or draw the deviation rate with the average value (default value is 5 bars).

//In addition, a more technical method is added to analyze the deviation changes of the major indexes.The deviation rate changing velocity value, parameter tan (abbreviated by t) of 1, 2, 5, 10 is introduced.

//You can have the option of calculate the tan using average value of 5 candlesticks or original value.

//Taking tan1 as an example, it indicates how much the deviation rate between the current price and the previous candlestick has changed.

//The indicator of the index color and the description of the trend quality color can be switched off in option.

//In addition, this code color scheme is only suitable for black background (the code color needs to be changed by yourself if you use white background).

Turtle N NormalizedSimple script that calculates the normalized value of N. Rules taken from an online PDF containing the original Turtle system:

"The Turtles used a volatility-based constant percentage risk position sizing algorithm. The Turtles used a concept that Richard Dennis and Bill Eckhardt called N to represent the underlying volatility of a particular market.

N is simply the 20-day exponential moving average of the True Range, which is now more commonly known as the ATR. Conceptually, N represents the average range in price movement that a particular market makes in a single day, accounting for opening gaps. N was measured in the same points as the underlying contract.

The Turtles built positions in pieces which we called Units. Units were sized so that 1 N represented 1% of the account equity. Thus, a unit for a given market or commodity can be calculated using the following formula:

Unit = 1% of Account/(N x Dollars per Point)"

To normalize the Unit formula, this script instead takes the value of (close/N). Dollars per point = 1 for stocks and crypto, but will change depending on the contract specifications for individual futures.

"Since the Turtles used the Unit as the base measure for position size, and since those units were volatility risk adjusted, the Unit was a measure of both the risk of a position, and of the entire portfolio of positions."

When the value of N is high, volatility is low and you should be more risk-on.

When the value of N is low, volatility is high and you should be more risk-off.

Donchian Channel Strategy [for free bot]

I present to you a script for testing the Donchian channel breakout strategy for the Binance_exchange.

This strategy is trending, and is especially effective for trading cryptocurrency futures.

This strategy is very flexible, and you can configure virtually all possible parameters, moreover, separately for longs and separately for shorts.

In the script, you can configure the parameters of the channel for entry and exit, the exit method, enable or disable purchases / sales, specify take profit and stop loss, and more.

On the example of optimization, only 20% of the deposit is used. This is done for diversification, since there are 37 contracts on binance_futures (at the time of writing the script description). That is, by optimizing the parameters for different currencies, you can very well reduce risks.

Представляю Вам скрипт для тестирования стратегии пробоя канала Дончиана для биржи Бинанс.

Данная стратегия относится к трендовым, и особенно эффективная на торговли криптовалютных фьючерсов.

Данная стратегия очень гибкая, и можно настроить фактически все возможные параметры, при чем, отдельно для покупок и отдельно для продаж.

В скрипте можно настроить параметры канала на вход и на выход, метод выхода, разрешить или запретить покупки/проаджи, указать тейк-профит и стоп-лосс и другое.

На примере оптимизации используется всего 20% от депозита. Это сделано для диверсификации, так как на фьючерсах бинансе присутсвует 37 контрактов (на момент написания описания скрипта). Т.е., оптимизировав параметры под разные валюты, можно очень хорошо снизить риски.

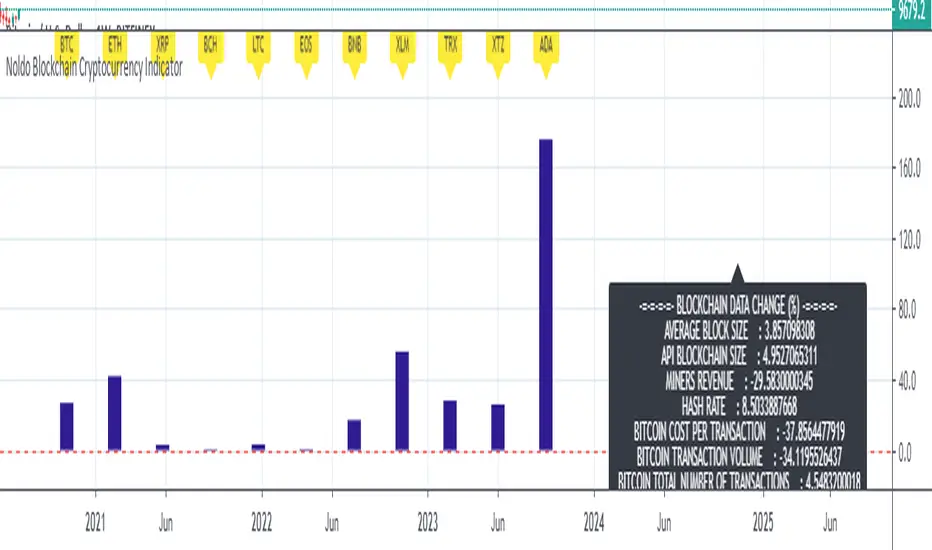

Noldo Blockchain Cryptocurrency Indicator

Hello, this script has the same logic as Noldo CFTC COT Forex Indicator :

And Noldo CFTC COT Commodities Indicator :

*

Script briefly calculates the period length between two signals of Pivot Reversal Strategy when new signal arrives and allows us to see relative Blockchain data and price changes of Major Cryptocurrencies over that automatic length.

This saves us from the hassle and time wasting of searching for a reference point.

Usage

This script works only on all Bitcoin / U.S Dollar pairs and futures.

It only works on 1W graphics.

ICOT data are pulled via Quandl

NOTE :

Since blockchain data is very votalile, 7-day ema values are adjusted to take into account.

Regards.

[Bitcoin] Lastbattle's nose pickerI've been working on a top and bottom picker script over the past couple of weeks, based on RSI of multiple timeframe closing price. It've been a pretty good trading system that's tested over the last meteoric rise from 220~270 and back down to 230 right now, and I think it should be released to the community.

Sure, I'm not worried about this strategy not working anymore after it is being used by the majority. Everyone have a different view of the market, and this is more towards psychology. It'll likely to hold for as long as there are still humans trading Bitcoins. Bitcoin market is full of emotions, you'll never run out of it.

So why does it work?

If you take a look at the live charts offered by Bitcoinwisdom and Cryptowatch, they only offer 1, 3, 5, and 15 minute timeframe by default with no other option to switch.

Naturally more traders will look at these levels for oversold and overbought condition.

The same indicator does not work for the broader commodities market such as Gold and Silver.

How does it work?

As long as the RSI levels of 1, 3, 5, and 15 minute fulfills the oversold/overbought level, a signal will be given.

The overbought/oversold level gets compensated the higher volatility the market is in.

Note: **

-This is only for exit strategy. If you're on long, consider reducing or exiting your position when it displays a red. On the other hand if you're short, consider reducing or covering your shorts if it shows a green.

-It may give false signal in a trending market, use your trading experience and judgement to filter them out. (eg: uptrend usually have more than 1 legs AND after a long consolidation, RSI gets to oversold/overbought easily... the market will tend to test the support/resistance again.)

-This is tuned for the 15m interval, the script won't work beyond this. I use it for scalping futures. Feel free to change or remove this line 'plot(interval == 15 and '

-Even if it shows a signal, it may not be the true top/bottom. Sometimes there may be a weak diverged leg aka 'last fart', so that's one reason I dont use this for entry until more confirmation is given via other indicators.

** If your chart is zooming all the way down to 0, right click on the price at the right and select 'Scale price only'

Go ahead and try this out with willy, etc and see what works better :D

Credits:

-LazyBear for the volatility switcher script

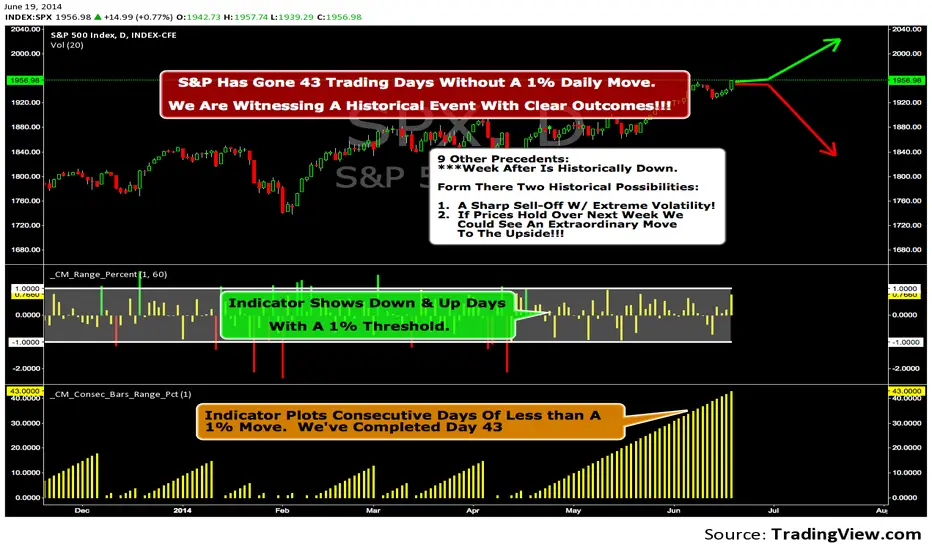

We Are Witnessing A Historical Event With A Clear Outcome!!!"Full Disclosure: I came across this information from www.SentimenTrader.com

I have no financial affiliation…They provide incredible statistical facts on

The General Market, Currencies, and Futures. They offer a two week free trial.

I Highly Recommend.

The S&P 500 has gone 43 trading days without a 1% daily move, up or down.

which is the equivalent of two months and one day in trading days.

During this stretch, the S&P has gained more than 4%,

and it has notched a 52-week high recently as well.

Since 1952, there were nine other precedents. All of

these went 42 trading days without a 1% move, all of

them saw the S&P gain at least 4% during their streaks,

and all of them saw the S&P close at a 52-week highs.

***There was consistent weakness a week later, with only three

gainers, and all below +0.5%.

***After that, stocks did better, often continuing an Extraordinary move higher.

Charts can sometimes give us a better nuance than

numbers from a table, and from the charts we can see a

general pattern -

***if stocks held up well in the following

weeks, then they tended to do extremely well in the

months ahead.

***If stocks started to stumble after this two-

month period of calm, however, then the following months

tended to show a lot more volatility.

We already know we're seeing an exceptional market

environment at the moment, going against a large number

of precedents that argued for weakness here, instead of

the rally we've seen. If we continue to head higher in

spite of everything, these precedents would suggest that

we're in the midst of something that could be TRULY EXTRAORDINARY.

Gold Timing Composite (EURUSD + DXY + US02Y)Here's the publication-ready description for TradingView:

Gold Timing Composite Indicator - 3-Component Model

Overview

A precision-engineered multi-component oscillator designed specifically for intraday gold trading. This indicator synthesizes three critical market drivers—EUR/USD dynamics, broad US Dollar strength, and Treasury yield movements—to isolate genuine gold price catalysts from market noise, delivering high-probability timing signals through triple-layer confirmation.

Components & Methodology

The indicator employs z-score normalization (default 20-period lookback) to harmonize three distinct but correlated market signals into a unified composite reading:

Fast Price Discovery Signal (40%):

EURUSD (40%) - EUR/USD captures rapid USD repricing with the deepest FX liquidity globally

Broad USD Strength Confirmation (35%):

-DXY (35%) - Inverted US Dollar Index measures comprehensive USD strength across six major currencies (EUR 57%, JPY 14%, GBP 12%, CAD 9%, SEK 4%, CHF 4%)

Real Yield Proxy (25%):

-US02Y (25%) - Inverted 2-Year Treasury yield captures Fed policy expectations and real rate dynamics

Key Features

✅ Dual USD Validation - EURUSD (speed) + DXY (breadth) filter EUR-specific moves from true USD weakness

✅ Real Yield Sensitivity - US02Y isolates rate-driven gold moves from pure currency effects

✅ Triple Confirmation System - Visual alignment dots when all three components agree simultaneously

✅ Mean-Reversion Zones - Overbought/oversold thresholds at ±1.5 standard deviations

✅ Clean Visualization - Candle-based display (no wicks) for rapid pattern recognition

✅ EUR/USD Divergence Detection - Identifies when EURUSD moves are EUR-specific vs broad USD moves

How to Use

Basic Signals:

Green candles = Bullish gold pressure (USD weakening / yields falling)

Red candles = Bearish gold pressure (USD strengthening / yields rising)

Above +1.5 = Overbought zone → look for mean-reversion shorts

Below -1.5 = Oversold zone → look for mean-reversion longs

High-Confidence Setups (Alignment Dots):

Lime dot at top = All 3 components bullish → maximum gold long confidence

Magenta dot at bottom = All 3 components bearish → maximum gold short confidence

No dots = Components diverging → reduce position size or wait for clarity

Divergence Trading:

Gold makes new high but composite doesn't confirm → potential reversal down

Gold makes new low but composite doesn't confirm → potential reversal up

Understanding Component Interactions

Normal Correlation (High Confidence):

EURUSD ↑ + DXY ↓ + US02Y ↓ → Broad USD weakness + falling yields → Strong gold bull signal

EURUSD ↓ + DXY ↑ + US02Y ↑ → Broad USD strength + rising yields → Strong gold bear signal

EURUSD/DXY Divergence (Critical Filter):

EURUSD ↑ but DXY flat/up → EUR-specific strength (ECB, Eurozone news) → Weak gold signal

DXY flat = USD not actually weak, just EUR strong → Gold may not follow EURUSD

EURUSD flat but DXY ↓ → Broad USD weakness (JPY, GBP, CAD all strong) → Strong gold signal

True USD weakness beyond just EUR → High-probability gold long

FX vs Yields Divergence:

EURUSD ↑ + DXY ↓ but US02Y ↑ → USD weak in FX but yields rising → Mixed signal

Hawkish Fed repricing vs currency weakness → Medium confidence, smaller size

EURUSD ↓ + DXY ↑ but US02Y ↓ → USD strong but yields falling → Conflicting drivers

Could be risk-off (safe haven bid to Treasuries) → Analyze broader market context

Best Practices

Timeframes: 5-minute to 15-minute charts for intraday trading

Session Focus: London fix (10:30 AM GMT) and New York open (8:20 AM EST) for peak gold liquidity

Pair With:

Key gold technical levels (round numbers, previous highs/lows)

COMEX gold futures volume profile

Real yield charts (when available)

VIX for risk sentiment context

Risk Management:

Full position: When alignment dots appear (all 3 components agree)

Half position: When 2 of 3 components align

Wait/reduce: When all three components diverge

Weight Adjustments:

Fed announcement days (FOMC, CPI, NFP): Increase US02Y to 35%, reduce EURUSD to 35%

ECB policy days: Monitor EURUSD/DXY divergence closely (EUR-specific moves may not affect gold)

Geopolitical events: DXY and yields may diverge (safe-haven flows) → Focus on DXY + yields, reduce EURUSD weight

Asian session: EURUSD less reliable (lower liquidity), consider increasing DXY weight to 45%

Technical Details

Calculation Method: Z-score normalization with configurable lookback period

Default Weights: EURUSD 40% | -DXY 35% | -US02Y 25%

Extreme Threshold: ±1.5 standard deviations (adjustable)

Alignment Trigger: All 3 components in unanimous agreement

Customizable Parameters:

Z-score lookback period (default: 20)

15-20: Faster, more sensitive (intraday focus)

30-50: Slower, smoother (swing trade context)

Individual component weights

Extreme threshold levels (1.3 for more signals, 1.8 for extremes only)

Alignment indicator toggle

Advantages Over Simple Indicators

Unlike single-instrument or DXY-only indicators, this composite:

Filters EUR-specific noise - When EURUSD moves but DXY doesn't confirm, gold often doesn't follow

Combines speed + breadth - EURUSD for fast entries, DXY for broad confirmation

Isolates real yield drivers - US02Y separates rate-driven moves from pure FX effects

Identifies regime shifts - When FX and yields diverge, signals changing market dynamics

Adaptable weighting - Adjust for different sessions, events, or market regimes

Real-World Signal Examples

Example 1: High-Confidence Long (All Aligned)

Fed dovish surprise → US02Y falls sharply

USD sells off → EURUSD rises + DXY falls

Composite surges, lime dot appears

Action: Full position gold long

Example 2: False Signal (EUR-Specific)

ECB hawkish statement → EURUSD rallies

But DXY unchanged (JPY, GBP, CAD not moving)

US02Y also unchanged

Composite rises but no alignment dot

Action: Small/no gold position (move is EUR-specific, not USD weakness)

Example 3: Mixed Signal (FX vs Yields)

Strong US jobs data → US02Y spikes (bearish gold)

But USD sells off in FX → EURUSD up + DXY down (bullish gold)

Composite shows divergence, no dots

Action: Wait for clarity or trade with tight stops

Example 4: Divergence Entry

Gold makes new intraday high

But composite fails to confirm (makes lower high)

Bearish divergence forms

Action: Short gold on next pullback

Suggested Complementary Analysis

Fundamental:

Fed vs ECB policy divergence and forward guidance

Real yield trends (10Y TIPS when available)

Inflation expectations (breakevens)

Central bank balance sheet changes

Geopolitical risk premium

Technical:

Gold futures COT (Commitment of Traders) positioning

COMEX gold open interest

Gold/Silver ratio

Mining stock performance (GDX, GDXJ)

Intermarket:

US equity market performance (risk-on/risk-off context)

Crude oil (inflation proxy)

Copper (growth expectations)

Bitcoin correlation (alternative store of value narrative)

Limitations & Considerations

When the Indicator Struggles:

Flash crashes or circuit breakers - Extreme events can break normal correlations temporarily

Asian session gaps - Lower EURUSD liquidity can cause false signals

Central bank interventions - SNB or BOJ FX intervention distorts DXY temporarily

Geopolitical shocks - Gold can decouple from USD/yields during wars, crises (safe-haven bid)

Quarter-end flows - Rebalancing can create temporary USD moves unrelated to fundamentals

Best Used When:

Normal market conditions (liquid sessions, no major shocks)

Clear trending or mean-reverting environment

Components showing consistent correlations

Combined with price action and volume confirmation

Performance Optimization Tips

Backtest your timeframe - Test 15-25 lookback periods to find optimal sensitivity

Session-specific weights - Use different weight profiles for London vs New York vs Asia

Combine with price action - Don't trade composites alone; wait for gold to confirm with candle patterns

Monitor component correlations - If EURUSD/DXY correlation breaks down, reduce both weights temporarily

Use with stop-loss discipline - Composite extremes suggest mean-reversion, but trends can extend

Disclaimer

This indicator is a technical analysis tool and does not guarantee profitable trades. Gold markets are influenced by numerous factors including geopolitics, central bank policy, inflation, and market sentiment that cannot be fully captured by any indicator. Always employ proper risk management, position sizing, and stop-losses. Backtest thoroughly before live implementation. Past performance is not indicative of future results.

Credits

Developed for intraday precious metals traders seeking multi-factor confirmation for gold timing decisions. Built on intermarket analysis principles combining currency dynamics, interest rate differentials, and statistical normalization for robust signal generation. Designed to filter EUR-specific noise and isolate true USD weakness—the primary driver of gold price movements.

Version: 1.0

Pine Script Version: 6

Asset Class: Precious Metals (Gold, Silver)

Category: Oscillators, Multi-Timeframe Analysis, Intermarket Analysis

Use Case: Intraday mean-reversion and momentum timing for gold (XAUUSD, GC futures)

Trading gold with this indicator? Share your results, questions, or improvement suggestions in the comments!

BTC Fundamental Value Hypothesis [OmegaTools]BTC Fundamental Value Hypothesis is a macro-valuation and regime-detection model designed to contextualize Bitcoin’s price through relative market-cap comparisons against major capital reservoirs: Gold, Silver, the Altcoin market, and large-cap equities. Instead of relying on traditional on-chain metrics or purely technical signals, this tool frames BTC as an asset competing for global liquidity and “store-of-value mindshare”, then estimates an implied fair value based on how BTC historically coexists (or diverges) from these benchmark universes.

Core concept: relative market-cap anchoring

The indicator builds a reference-based fair price by translating external market capitalizations into implied BTC valuation using a dominance framework. In practice, you choose one or more reference universes (Gold, Silver, Altcoins, Stocks). For each selected universe, the script computes how large BTC “should be” relative to that universe (dominance ratio), and converts that into an implied BTC price. The final fair price is the average of the implied prices from the enabled universes.

Two dominance modes: automatic vs manual

1. Automatic Dominance % (default)

When enabled, the model estimates dominance ratios dynamically using a 252-period simple moving average of BTC market cap divided by each reference market cap. This produces an adaptive baseline that follows structural changes over time and reduces sensitivity to short-term spikes.

2. Manual Dominance %

If you prefer a discretionary macro thesis, you can directly input dominance parameters for each reference universe. This is useful when you want to stress-test scenarios (e.g., “BTC should converge toward X% of Gold’s market cap”) or align the model with a specific long-term adoption narrative.

Reference universes and data construction

- BTC market cap: pulled from CRYPTOCAP:BTC.

- Gold and Silver market caps: derived from the corresponding futures symbols (GC1!, SI1!) multiplied by an assumed total above-ground quantity (constant tonnage converted to troy ounces). This provides a practical and tradable proxy for spot valuation context.

- Altcoin market cap: pulled from CRYPTOCAP:TOTAL2 (total crypto market excluding BTC).

- Stocks market cap proxy (Σ3): a deliberately conservative equity benchmark built from three mega-cap stocks (AAPL, MSFT, AMZN) using total shares outstanding (request.financial) multiplied by price. This avoids index licensing complexity while still tracking a meaningful slice of global equity beta/liquidity.

Valuation output: overvalued vs undervalued (log-based)

The valuation readout is expressed as a percentage derived from the logarithmic distance between BTC price and the model’s fair price. This choice makes valuation comparable across long time horizons and reduces distortion during exponential growth phases. A positive valuation indicates BTC trading below the model’s implied value (undervalued), while a negative valuation indicates trading above it (overvalued).

Oscillator: relative momentum and regime confirmation

In addition to fair value, the indicator includes a momentum differential oscillator built from RSI(50):

- BTC RSI is compared to the average RSI of the selected reference universes.

- The oscillator highlights when BTC strength is leading or lagging the broader macro benchmarks.

- Color is rendered through a gradient to provide immediate regime readability (risk-on vs risk-off behavior, expansion vs contraction phases).

Visualization and UI components

- Fair Price overlay: the computed fair price is plotted directly on the BTC chart for immediate comparison with spot price action.

- Valuation shading: the area between price and fair price is filled to visually emphasize dislocation and potential mean-reversion zones.

- Oscillator panel: a zero-centered oscillator with filled bands helps you identify persistent trend regimes versus transitional conditions.

- Summary table: a right-side table displays the current valuation (over/under) and, when Automatic mode is enabled, the live dominance ratios used in the model (BTC/GOLD, BTC/SILVER, BTC/ALTC, BTC/STOCKS).

How to use it (practical workflows)

- Macro valuation context: use fair price as a structural anchor to assess whether BTC is trading at a premium or discount relative to external liquidity baselines.

- Regime filtering: combine valuation with the oscillator to distinguish “cheap but weak” from “cheap and strengthening” (and the inverse for tops).

- Mean-reversion mapping: large, persistent deviations from fair value often highlight speculative extremes or capitulation zones; this can support systematic entries/exits, position sizing, or hedging decisions.

- Scenario analysis: switch to Manual Dominance % to model adoption outcomes, policy-driven shifts, or multi-year re-rating assumptions.

Important notes and limitations (read before use)

- This is a hypothesis-driven macro model, not a literal intrinsic value calculation. Results depend on dominance assumptions, proxies, and data availability.

- Gold/Silver market caps are approximations based on futures pricing and fixed supply constants; real-world supply dynamics, above-ground estimates, and spot/futures basis can differ.

- The Stocks (Σ3) benchmark is a proxy and intentionally not “the whole market”. It is designed to represent a large-cap liquidity reference, not total equity capitalization.

- Always validate signals with additional context (market structure, volatility regime, risk management rules). This indicator is best used as a macro layer in a broader decision framework.

Designed for clarity, macro discipline, and repeatability

BTC Fundamental Value Hypothesis by OmegaTools is built for traders and investors who want a clean, data-driven way to interpret BTC through the lens of competing asset classes and capital flows. It is particularly effective on higher timeframes (Daily/Weekly) where macro relationships are more stable and valuation signals are less noisy.

© OmegaTools, Eros

Weekly High/Low Day StatisticsThis indicator analyzes historical price data to determine which day of the week (Monday through Friday) most frequently hosts the weekly high and low prices. It provides overall counts, percentages, and the total number of weeks analyzed. Ideal for traders studying seasonal or day-of-week patterns in markets like futures (e.g., ES1!, NQ1!) or stocks (e.g., SPY).

Key Features:

Overall Statistics: Aggregates data across all available history, including the current partial week if applicable.

High/Low Tracking: Counts how many times each day was the weekly high or low, with percentages calculated over the total weeks.

Tie Handling: Uses the first occurrence in case of price ties (e.g., if multiple days hit the same high, the earliest day is credited).

Futures-Friendly: Utilizes time_tradingday for accurate day-of-week detection on continuous contracts like ES1!, accounting for session timings in UTC.

Table Display: Results are presented in a clean, semi-transparent table in the top-right corner, with columns for counts, percentages, and a total weeks summary.

Dynamic Updates: Processes all available historical bars on daily (1D) charts, supporting deep history (e.g., back to 2001 for ES1!). Note: On intraday timeframes, historical depth may be limited by TradingView's bar constraints.

How It Works:

The script iterates through daily bars, identifying the start of each new week via ta.change(time("W")). It tracks the highest and lowest prices within each week and assigns them to the corresponding trading day. At the end of each complete week, it tallies the results. The current incomplete week is included for real-time relevance.

Percentages are calculated as: (Count / Total Weeks) * 100, rounded to one decimal place.

Usage Tips:

Recommended Timeframe: Daily (1D) for maximum historical analysis. Works on intraday charts but with shallower data.

Symbols: Best for markets trading Monday-Friday, like indices, futures, or equities. Sunday/Saturday data is ignored as it's typically non-trading.

Customization: If ties should favor the last day instead, modify the comparison operators from >/< to >=/<= in the update logic.

Performance: Efficient for large datasets; no max_bars_back needed as it avoids deep historical references.

This tool can help uncover patterns, such as whether Fridays tend to be highs in bullish markets or Mondays lows during volatility. Use it alongside other indicators for comprehensive strategy building. Feedback welcome—feel free to suggest improvements!

Daily Inputs - The Prometheus InitiativeDaily ES inputs from the Prometheus Initiative is a clean, customizable overlay indicator designed specifically for ES (S&P 500 E-mini futures) day traders who rely on manually selected key price levels each session.

Instead of spending time manually drawing horizontal lines every day, this tool lets you quickly input the daily price levels directly in the settings and instantly see them plotted as horizontal lines across your chart.

Key Features:

• 15 fully editable price inputs with customizable settings.

Why this indicator was created:

Manually drawing 10–15 lines each morning is time-consuming. This indicator was developed to eliminate that friction — allowing fast, accurate plotting of levels so you can focus on execution rather than drawing tools. The largest benefit is that you can toggle the indicator on/off to keep a clean chart as to not interfere with your existing visual levels.

Perfect for:

- ES / NQ futures traders

- Anyone who wants a clean, no-nonsense way to visualize custom horizontal levels

How to use:

1. Add to your chart

2. Open Settings → Enter the daily levels provided

3. Watch price interact with the levels!

Note: This is a manual input tool. Levels do NOT auto-calculate. It's meant to reflect the exact levels posted each day.

Happy trading! 📈

Feel free to leave feedback or suggestions in the comments.

Disclaimer: This indicator is for educational/visual purposes only. Trading futures involves substantial risk of loss and is not suitable for all investors.