MACD Cloud with Moving Average and ATR BandsThe algorithm implements a technical analysis indicator that combines the MACD Cloud, Moving Averages (MA), and volatility bands (ATR) to provide signals on market trends and potential reversal points. It is divided into several sections:

🎨 Color Bars:

Activated based on user input.

Controls bar color display according to price relative to ATR levels and moving average (MA).

Logic:

⚫ Black: Potential bearish reversal (price above the upper ATR band).

🔵 Blue: Potential bullish reversal (price below the lower ATR band).

o

🟢 Green: Bullish trend (price between the MA and upper ATR band).

o

🔴 Red: Bearish trend (price between the lower ATR band and MA).

o

📊 MACD Bars:

Description:

The MACD Bars section is activated by default and can be modified based on user input.

🔴 Red: Indicates a bearish trend, shown when the MACD line is below the Signal line (Signal line is a moving average of MACD).

🔵 Blue: Indicates a bullish trend, shown when the MACD line is above the Signal line.

Matching colors between MACD Bars and MACD Cloud visually confirms trend direction.

MACD Cloud Logic: The MACD Cloud is based on Moving Average Convergence Divergence (MACD), a momentum indicator showing the relationship between two moving averages of price.

MACD and Signal Lines: The cloud visualizes the MACD line relative to the Signal line. If the MACD line is above the Signal line, it indicates a potential bullish trend, while below it suggests a potential bearish trend.

☁️ MA Cloud:

The MA Cloud uses three moving averages to analyze price direction:

Moving Average Relationship: Three MAs of different periods are plotted. The cloud turns green when the shorter MA is above the longer MA, indicating an uptrend, and red when below, suggesting a downtrend.

Trend Visualization: This graphical representation shows the trend direction.

📉 ATR Bands:

The ATR bands calculate overbought and oversold limits using a weighted moving average (WMA) and ATR.

Center (matr): Shows general trend; prices above suggest an uptrend, while below indicate a downtrend.

Up ATR 1: Marks the first overbought level, suggesting a potential bearish reversal if the price moves above this band.

Down ATR 1: Marks the first oversold level, suggesting a possible bullish reversal if the price moves below this band.

Up ATR 2: Extends the overbought range to an extreme, reinforcing the possibility of a bearish reversal at this level.

Down ATR 2: Extends the oversold range to an extreme, indicating a stronger bullish reversal possibility if price reaches here.

Español:

El algoritmo implementa un indicador de análisis técnico que combina la nube MACD, promedios móviles (MA) y bandas de volatilidad (ATR) para proporcionar señales sobre tendencias del mercado y posibles puntos de reversión. Se divide en varias secciones:

🎨 Barras de Color:

- Activado según la entrada del usuario.

- Controla la visualización del color de las barras según el precio en relación con los niveles de ATR y el promedio móvil (MA).

- **Lógica:**

- ⚫ **Negro**: Reversión bajista potencial (precio por encima de la banda superior ATR).

- 🔵 **Azul**: Reversión alcista potencial (precio por debajo de la banda inferior ATR).

- 🟢 **Verde**: Tendencia alcista (precio entre el MA y la banda superior ATR).

- 🔴 **Rojo**: Tendencia bajista (precio entre la banda inferior ATR y el MA).

### 📊 Barras MACD:

- **Descripción**:

- La sección de barras MACD se activa por defecto y puede modificarse según la entrada del usuario.

- 🔴 **Rojo**: Indica una tendencia bajista, cuando la línea MACD está por debajo de la línea de señal (la línea de señal es una media móvil de la MACD).

- 🔵 **Azul**: Indica una tendencia alcista, cuando la línea MACD está por encima de la línea de señal.

- La coincidencia de colores entre las barras MACD y la nube MACD confirma visualmente la dirección de la tendencia.

### 🌥️ Nube MACD:

- **Lógica de la Nube MACD**: Basada en el indicador de convergencia-divergencia de medias móviles (MACD), que muestra la relación entre dos medias móviles del precio.

- **Líneas MACD y de Señal**: La nube visualiza la relación entre la línea MACD y la línea de señal. Si la línea MACD está por encima de la de señal, indica una tendencia alcista potencial; si está por debajo, sugiere una tendencia bajista.

### ☁️ Nube MA:

- **Relación entre Medias Móviles**: Se trazan tres medias móviles de diferentes períodos. La nube se vuelve verde cuando la media más corta está por encima de la más larga, indicando una tendencia alcista, y roja cuando está por debajo, sugiriendo una tendencia bajista.

- **Visualización de Tendencias**: Proporciona una representación gráfica de la dirección de la tendencia.

### 📉 Bandas ATR:

- Las bandas ATR calculan límites de sobrecompra y sobreventa usando una media ponderada y el ATR.

- **Centro (matr)**: Muestra la tendencia general; precios por encima indican tendencia alcista y debajo, bajista.

- **Up ATR 1**: Marca el primer nivel de sobrecompra, sugiriendo una reversión bajista potencial si el precio sube por encima de esta banda.

- **Down ATR 1**: Marca el primer nivel de sobreventa, sugiriendo una reversión alcista potencial si el precio baja por debajo de esta banda.

- **Up ATR 2**: Amplía el rango de sobrecompra a un nivel extremo, reforzando la posibilidad de reversión bajista.

- **Down ATR 2**: Extiende el rango de sobreventa a un nivel extremo, sugiriendo una reversión alcista más fuerte si el precio alcanza esta banda.

Buscar en scripts para "ATR"

Lsma ATR | viResearchLsma ATR | viResearch

Conceptual Foundation and Innovation

The "Lsma ATR" indicator from viResearch combines the power of the Least Squares Moving Average (LSMA) with the Average True Range (ATR) to offer traders a dynamic approach to trend analysis and volatility management. The LSMA is highly regarded for its ability to fit a linear regression line to price data, providing a smooth and precise trend line with minimal lag. When paired with the ATR, which measures market volatility, this indicator not only tracks trend direction but also adapts to changes in volatility. The integration of both elements allows traders to identify potential trend reversals and assess the strength of trends in the context of market volatility. This combination makes the "Lsma ATR" a versatile tool for following trends while managing risk, as it responds quickly to changes in price direction while accounting for shifts in market volatility.

Technical Composition and Calculation

The "Lsma ATR" script consists of two primary components: the Least Squares Moving Average (LSMA) and the Average True Range (ATR). The LSMA is calculated over a user-defined length, providing a smoothed representation of the market trend based on linear regression. The ATR, also user-defined, is used to measure market volatility by calculating the average range between high and low prices over a specified period. By adding and subtracting the ATR from the LSMA, the indicator creates upper and lower boundaries that help define the market's current volatility-adjusted range. The script monitors for price crossovers with these boundaries to generate trend signals. When the price crosses above the upper boundary, it signals a potential upward trend. Conversely, when the price crosses below the lower boundary, it signals a possible downward trend. These boundaries dynamically adjust based on volatility, providing more accurate signals as market conditions change.

Features and User Inputs

The "Lsma ATR" script offers several customizable inputs, allowing traders to fine-tune the indicator to their trading preferences. The LSMA Length controls the lookback period for the LSMA, determining how smooth or responsive the trend line is. The ATR Length defines the period used for calculating the average volatility, affecting the width of the volatility-adjusted range. Additionally, the indicator includes alert conditions that notify traders when a trend shift occurs, either to the upside or downside.

Practical Applications

The "Lsma ATR" indicator is designed for traders who want to follow market trends while accounting for changes in volatility. The LSMA provides a clear, smoothed trend line that helps identify the direction of the market, while the ATR adjusts the boundaries based on the current volatility level. This combination makes the indicator particularly effective for detecting trend reversals, as the LSMA tracks the overall trend direction and price crossovers with the ATR boundaries provide early signals of potential trend changes. It also helps manage risk by understanding market volatility, allowing traders to adjust their strategies based on the strength of price movements. The indicator improves trend-following strategies by combining LSMA’s trend detection with ATR’s volatility adjustment, offering a nuanced approach in various market conditions.

Advantages and Strategic Value

The "Lsma ATR" script offers significant value by integrating the precision of the LSMA with the adaptability of the ATR. This dual approach allows traders to reduce noise in price data while responding to changes in volatility, leading to more accurate trend signals. The volatility-adjusted boundaries provide a dynamic range that helps traders avoid false signals and stay aligned with stronger trends. This makes the "Lsma ATR" an ideal tool for traders seeking to enhance their trend-following strategies while accounting for market volatility.

Alerts and Visual Cues

The script includes alert conditions that notify traders when the price crosses the ATR boundaries, signaling a potential trend change. The "Lsma ATR Long" alert is triggered when the price crosses above the upper boundary, indicating a potential upward trend, while the "Lsma ATR Short" alert signals a possible downward trend when the price crosses below the lower boundary. Visual cues, such as changes in the color of the LSMA line and shaded areas between the ATR boundaries, help traders quickly identify these trend shifts.

Summary and Usage Tips

The "Lsma ATR | viResearch" indicator combines the smoothing benefits of the LSMA with the volatility sensitivity of the ATR, providing traders with a robust tool for trend detection and volatility management. By incorporating this script into your trading strategy, you can improve your ability to detect trend reversals, confirm trend direction, and manage risk by adjusting to market volatility. The "Lsma ATR" offers a reliable and customizable solution for traders looking to enhance their technical analysis in both trending and volatile market environments.

Note: Backtests are based on past results and are not indicative of future performance.

The Flash-Strategy with Minervini Stage Analysis QualifierThe Flash-Strategy (Momentum-RSI, EMA-crossover, ATR) with Minervini Stage Analysis Qualifier

Introduction

Welcome to a comprehensive guide on a cutting-edge trading strategy I've developed, designed for the modern trader seeking an edge in today's dynamic markets. This strategy, which I've honed through my years of experience in the trading arena, stands out for its unique blend of technical analysis and market intuition, tailored specifically for use on the TradingView platform.

As a trader with a deep passion for the financial markets, my journey began several years ago, driven by a relentless pursuit of a trading methodology that is both effective and adaptable. My background in trading spans various market conditions and asset classes, providing me with a rich tapestry of experiences from which to draw. This strategy is the culmination of that journey, embodying the lessons learned and insights gained along the way.

The cornerstone of this strategy lies in its ability to generate precise long signals in a Stage 2 uptrend and equally accurate short signals in a Stage 4 downtrend. This approach is rooted in the principles of trend following and momentum trading, harnessing the power of key indicators such as the Momentum-RSI, EMA Crossover, and Average True Range (ATR). What sets this strategy apart is its meticulous design, which allows it to adapt to the ever-changing market conditions, providing traders with a robust tool for navigating both bullish and bearish scenarios.

This strategy was born out of a desire to create a trading system that is not only highly effective in identifying potential trade setups but also straightforward enough to be implemented by traders of varying skill levels. It's a reflection of my belief that successful trading hinges on clarity, precision, and disciplined execution. Whether you are a seasoned trader or just beginning your journey, this guide aims to provide you with a comprehensive understanding of how to harness the full potential of this strategy in your trading endeavors.

In the following sections, we will delve deeper into the mechanics of the strategy, its implementation, and how to make the most out of its features. Join me as we explore the nuances of a strategy that is designed to elevate your trading to the next level.

Stage-Specific Signal Generation

A distinctive feature of this trading strategy is its focus on generating long signals exclusively during Stage 2 uptrends and short signals during Stage 4 downtrends. This approach is based on the widely recognized market cycle theory, which divides the market into four stages: Stage 1 (accumulation), Stage 2 (uptrend), Stage 3 (distribution), and Stage 4 (downtrend). By aligning the signal generation with these specific stages, the strategy aims to capitalize on the most dynamic and clear-cut market movements, thereby enhancing the potential for profitable trades.

1. Long Signals in Stage 2 Uptrends

• Characteristics of Stage 2: Stage 2 is characterized by a strong uptrend, where prices are consistently rising. This stage typically follows a period of accumulation (Stage 1) and is marked by increased investor interest and bullish sentiment in the market.

• Criteria for Long Signal Generation: Long signals are generated during this stage when the technical indicators align with the characteristics of a Stage 2 uptrend.

• Rationale for Stage-Specific Signals: By focusing on Stage 2 for long trades, the strategy seeks to enter positions during the phase of strong upward momentum, thus riding the wave of rising prices and investor optimism. This stage-specific approach minimizes exposure to less predictable market phases, like the consolidation in Stage 1 or the indecision in Stage 3.

2. Short Signals in Stage 4 Downtrends

• Characteristics of Stage 4: Stage 4 is identified by a pronounced downtrend, with declining prices indicating prevailing bearish sentiment. This stage typically follows the distribution phase (Stage 3) and is characterized by increasing selling pressure.

• Criteria for Short Signal Generation: Short signals are generated in this stage when the indicators reflect a strong bearish trend.

• Rationale for Stage-Specific Signals: Targeting Stage 4 for shorting capitalizes on the market's downward momentum. This tactic aligns with the natural market cycle, allowing traders to exploit the downward price movements effectively. By doing so, the strategy avoids the potential pitfalls of shorting during the early or late stages of the market cycle, where trends are less defined and more susceptible to reversals.

In conclusion, the strategy’s emphasis on stage-specific signal generation is a testament to its sophisticated understanding of market dynamics. By tailoring the long and short signals to Stages 2 and 4, respectively, it leverages the most compelling phases of the market cycle, offering traders a clear and structured approach to aligning their trades with dominant market trends.

Strategy Overview

At the heart of this trading strategy is a philosophy centered around capturing market momentum and trend efficiency. The core objective is to identify and capitalize on clear uptrends and downtrends, thereby allowing traders to position themselves in sync with the market's prevailing direction. This approach is grounded in the belief that aligning trades with these dominant market forces can lead to more consistent and profitable outcomes.

The strategy is built on three foundational components, each playing a critical role in the decision-making process:

1. Momentum-RSI (Relative Strength Index): The Momentum-RSI is a pivotal element of this strategy. It's an enhanced version of the traditional RSI, fine-tuned to better capture the strength and velocity of market trends. By measuring the speed and change of price movements, the Momentum-RSI provides invaluable insights into whether a market is potentially overbought or oversold, suggesting possible entry and exit points. This indicator is especially effective in filtering out noise and focusing on substantial market moves.

2. EMA (Exponential Moving Average) Crossover: The EMA Crossover is a crucial component for trend identification. This strategy employs two EMAs with different timeframes to determine the market trend. When the shorter-term EMA crosses above the longer-term EMA, it signals an emerging uptrend, suggesting a potential long entry. Conversely, a crossover below indicates a possible downtrend, hinting at a short entry opportunity. This simple yet powerful tool is key in confirming trend directions and timing market entries.

3. ATR (Average True Range): The ATR is instrumental in assessing market volatility. This indicator helps in understanding the average range of price movements over a given period, thus providing a sense of how much a market might move on a typical day. In this strategy, the ATR is used to adjust stop-loss levels and to gauge the potential risk and reward of trades. It allows for more informed decisions by aligning trade management techniques with the current volatility conditions.

The synergy of these three components – the Momentum-RSI, EMA Crossover, and ATR – creates a robust framework for this trading strategy. By combining momentum analysis, trend identification, and volatility assessment, the strategy offers a comprehensive approach to navigating the markets. Whether it's capturing a strong trend in its early stages or identifying a potential reversal, this strategy aims to provide traders with the tools and insights needed to make well-informed, strategically sound trading decisions.

Detailed Component Analysis

The efficacy of this trading strategy hinges on the synergistic functioning of its three key components: the Momentum-RSI, EMA Crossover, and Average True Range (ATR). Each component brings a unique perspective to the strategy, contributing to a well-rounded approach to market analysis.

1. Momentum-RSI (Relative Strength Index)

• Definition and Function: The Momentum-RSI is a modified version of the classic Relative Strength Index. While the traditional RSI measures the velocity and magnitude of directional price movements, the Momentum-RSI amplifies aspects that reflect trend strength and momentum.

• Significance in Identifying Trend Strength: This indicator excels in identifying the strength behind a market's move. A high Momentum-RSI value typically indicates strong bullish momentum, suggesting the potential continuation of an uptrend. Conversely, a low Momentum-RSI value signals strong bearish momentum, possibly indicative of an ongoing downtrend.

• Application in Strategy: In this strategy, the Momentum-RSI is used to gauge the underlying strength of market trends. It helps in filtering out minor fluctuations and focusing on significant movements, providing a clearer picture of the market's true momentum.

2. EMA (Exponential Moving Average) Crossover

• Definition and Function: The EMA Crossover component utilizes two exponential moving averages of different timeframes. Unlike simple moving averages, EMAs give more weight to recent prices, making them more responsive to new information.

• Contribution to Market Direction: The interaction between the short-term and long-term EMAs is key to determining market direction. A crossover of the shorter EMA above the longer EMA is an indicator of an emerging uptrend, while a crossover below signals a developing downtrend.

• Application in Strategy: The EMA Crossover serves as a trend confirmation tool. It provides a clear, visual representation of the market's direction, aiding in the decision-making process for entering long or short positions. This component ensures that trades are aligned with the prevailing market trend, a crucial factor for the success of the strategy.

3. ATR (Average True Range)

• Definition and Function: The ATR is an indicator that measures market volatility by calculating the average range between the high and low prices over a specified period.

• Role in Assessing Market Volatility: The ATR provides insights into the typical market movement within a given timeframe, offering a measure of the market's volatility. Higher ATR values indicate increased volatility, while lower values suggest a calmer market environment.

• Application in Strategy: Within this strategy, the ATR is instrumental in tailoring risk management techniques, particularly in setting stop-loss levels. By accounting for the market's volatility, the ATR ensures that stop-loss orders are placed at levels that are neither too tight (risking premature exits) nor too loose (exposing to excessive risk).

In summary, the combination of Momentum-RSI, EMA Crossover, and ATR in this trading strategy provides a comprehensive toolkit for market analysis. The Momentum-RSI identifies the strength of market trends, the EMA Crossover confirms the market direction, and the ATR guides in risk management by assessing volatility. Together, these components form the backbone of a strategy designed to navigate the complexities of the financial markets effectively.

1. Signal Generation Process

• Combining Indicators: The strategy operates by synthesizing signals from the Momentum-RSI, EMA Crossover, and ATR indicators. Each indicator serves a specific purpose: the Momentum-RSI gauges trend momentum, the EMA Crossover identifies the trend direction, and the ATR assesses the market’s volatility.

• Criteria for Signal Validation: For a signal to be considered valid, it must meet specific criteria set by each of the three indicators. This multi-layered approach ensures that signals are not only based on one aspect of market behavior but are a result of a comprehensive analysis.

2. Conditions for Long Positions

• Uptrend Confirmation: A long position signal is generated when the shorter-term EMA crosses above the longer-term EMA, indicating an uptrend.

• Momentum-RSI Alignment: Alongside the EMA crossover, the Momentum-RSI should indicate strong bullish momentum. This is typically represented by the Momentum-RSI being at a high level, confirming the strength of the uptrend.

• ATR Consideration: The ATR is used to fine-tune the entry point and set an appropriate stop-loss level. In a low volatility scenario, as indicated by the ATR, the stop-loss can be set tighter, closer to the entry point.

3. Conditions for Short Positions

• Downtrend Confirmation: Conversely, a short position signal is indicated when the shorter-term EMA crosses below the longer-term EMA, signaling a downtrend.

• Momentum-RSI Confirmation: The Momentum-RSI should reflect strong bearish momentum, usually seen when the Momentum-RSI is at a low level. This confirms the bearish strength of the market.

• ATR Application: The ATR again plays a role in determining the stop-loss level for the short position. Higher volatility, as indicated by a higher ATR, would warrant a wider stop-loss to accommodate larger market swings.

By adhering to these mechanics, the strategy aims to ensure that each trade is entered with a high probability of success, aligning with the market’s current momentum and trend. The integration of these indicators allows for a holistic market analysis, providing traders with clear and actionable signals for both entering and exiting trades.

Customizable Parameters in the Strategy

Flexibility and adaptability are key features of this trading strategy, achieved through a range of customizable parameters. These parameters allow traders to tailor the strategy to their individual trading style, risk tolerance, and specific market conditions. By adjusting these parameters, users can fine-tune the strategy to optimize its performance and align it with their unique trading objectives. Below are the primary parameters that can be customized within the strategy:

1. Momentum-RSI Settings

• Period: The lookback period for the Momentum-RSI can be adjusted. A shorter period makes the indicator more sensitive to recent price changes, while a longer period smoothens the RSI line, offering a broader view of the momentum.

• Overbought/Oversold Thresholds: Users can set their own overbought and oversold levels, which can help in identifying extreme market conditions more precisely according to their trading approach.

2. EMA Crossover Settings

• Timeframes for EMAs: The strategy uses two EMAs with different timeframes. Traders can modify these timeframes, choosing shorter periods for a more responsive approach or longer periods for a more conservative one.

• Source Data: The choice of price data (close, open, high, low) used in calculating the EMAs can be varied depending on the trader’s preference.

3. ATR Settings

• Lookback Period: Adjusting the lookback period for the ATR impacts how the indicator measures volatility. A longer period may provide a more stable but less responsive measure, while a shorter period offers quicker but potentially more erratic readings.

• Multiplier for Stop-Loss Calculation: This parameter allows traders to set how aggressively or conservatively they want their stop-loss to be in relation to the ATR value.

Here are the standard settings:

Time-Decay Liquidity Zones [BackQuant]Time-Decay Liquidity Zones

A dynamic liquidity map that turns single-bar exhaustion events into fading, color-graded zones, so you can see where trapped traders and unfinished business still matter, and when those areas have finally stopped pulling price.

What this is

This indicator detects unusually strong impulsive moves into wicks, converts them into supply or demand “zones,” then lets those zones decay over time. Each zone carries a strength score that fades bar by bar. Zones that stop attracting or rejecting price are gradually de-emphasized and eventually removed, while the most relevant areas stay bright and obvious.

Instead of static rectangles that live forever, you get a living liquidity map where:

Zones are born from objective criteria: volatility, wick size, and optional volume spikes.

Zones “age” using a configurable decay factor and maximum lifetime.

Zone color and opacity reflect current relative strength on a unified clear → green → red gradient.

Zones freeze when broken, so you can distinguish “active reaction areas” from “historical levels that have already given way”.

Conceptual idea

Large wicks with strong volatility often mark areas where aggressive orders met hidden liquidity and got absorbed. Price may revisit these areas to test leftover interest or to relieve trapped positions. However, not every wick matters for long. As time passes and more bars print, the market “forgets” some areas.

Time-Decay Liquidity Zones turns that idea into a rule-based system:

Find bars that likely reflect strong aggressive flows into liquidity.

Mark a zone around the wick using ATR-based thickness.

Assign a strength score of 1.0 at birth.

Each bar, reduce that score by a decay factor and remove zones that fall below a threshold or live too long.

Color all surviving zones from weak to strong using a single gradient scale and a visual legend.

How events are detected

Detection lives in the Event Detection group. The script combines range, wick size, and optional volume filters into simple rules.

Volatility filter

ATR Length — computes a rolling ATR over your chosen window. This is the volatility baseline.

Min range in ATRs — bar range (High–Low) must exceed this multiple of ATR for an event to be considered. This avoids tiny bars triggering zones.

Wick filters

For each bar, the script splits the candle into body and wicks:

Upper wick = High minus the max(Open, Close).

Lower wick = min(Open, Close) minus Low.

Then it tests:

Upper wick condition — upper wick must be larger than Min wick size in ATRs × ATR.

Lower wick condition — lower wick must be larger than Min wick size in ATRs × ATR.

Only bars with a sufficiently long wick relative to volatility qualify as candidate “liquidity events”.

Volume filter

Optionally, the script requires a volume spike:

Use volume filter — if enabled, volume must exceed a rolling volume SMA by a configurable multiplier.

Volume SMA length — period for the volume average.

Volume spike multiplier — how many times above the SMA current volume needs to be.

This lets you focus only on “heavy” tests of liquidity and ignore quiet bars.

Event types

Putting it together:

Upper event (potential supply / long liquidation, etc.)

Occurs when:

Upper wick is large in ATR terms.

Full bar range is large in ATR terms.

Volume is above the spike threshold (if enabled).

Lower event (potential demand / short liquidation, etc.)

Symmetric conditions using the lower wick.

How zones are constructed

Zone geometry lives in Zone Geometry .

When an event is detected, the script builds a rectangular box that anchors to the wick and extends in the appropriate direction by an ATR-based thickness.

For upper (supply-type) zones

Bottom of the zone = event bar high.

Top of the zone = event bar high + Zone thickness in ATRs × ATR.

The zone initially spans only the event bar on the x-axis, but is extended to the right as new bars appear while the zone is active.

For lower (demand-type) zones

Top of the zone = event bar low.

Bottom of the zone = event bar low − Zone thickness in ATRs × ATR.

Same extension logic: box starts on the event bar and grows rightward while alive.

The result is a band around the wick that scales with volatility. On high-ATR charts, zones are thicker. On calm charts, they are narrower and more precise.

Zone lifecycle, decay, and removal

All lifecycle logic is controlled by the Decay & Lifetime group.

Each zone carries:

Score — a floating-point “importance” measure, starting at 1.0 when created.

Direction — +1 for upper zones, −1 for lower zones.

Birth index — bar index at creation time.

Active flag — whether the zone is still considered unbroken and extendable.

1) Active vs broken

Each confirmed bar, the script checks:

For an upper zone , the zone is counted as “broken” when the close moves above the top of the zone.

For a lower zone , the zone is counted as “broken” when the close moves below the bottom of the zone.

When a zone breaks:

Its right edge is frozen at the previous bar (no further extension).

The zone remains on the chart, but is no longer updated by price interaction. It still decays in score until removal.

This lets you see where a major level was overrun, while naturally fading its influence over time.

2) Time decay

At each confirmed bar:

Score := Score × Score decay per bar .

A decay value close to 1.0 means very slow decay and long-lived zones.

Lower values (closer to 0.9) mean faster forgetting and more current-focused zones.

You are controlling how quickly the market “forgets” past events.

3) Age and score-based removal

Zones are removed when either:

Age in bars exceeds Max bars a zone can live .

This is a hard lifetime cap.

Score falls below Minimum score before removal .

This trims zones that have decayed into irrelevance even if their age is still within bounds.

When a zone is removed, its box is deleted and all associated state is freed to keep performance and visuals clean.

Unified gradient and color logic

Color control lives in Gradient & Color . The indicator uses a single continuous gradient for all zones, above and below price, so you can read strength at a glance without guessing what palette means what.

Base colors

You set:

Mid strength color (green) — used for mid-level strength zones and as the “anchor” in the gradient.

High strength color (red) — used for the strongest zones.

Max opacity — the maximum visual opacity for the solid part of the gradient. Lower values here mean more solid; higher values mean more transparent.

The script then defines three internal points:

Clear end — same as mid color, but with a high alpha (close to transparent).

Mid end — mid color at the strongest allowed opacity.

High end — high color at the strongest allowed opacity.

Strength normalization

Within each update:

The script finds the maximum score among all existing zones.

Each zone’s strength is computed as its score divided by this maximum.

Strength is clamped into .

This means a zone with strength 1.0 is currently the strongest zone on the chart. Other zones are colored relative to that.

Piecewise gradient

Color is assigned in two stages:

For strength between 0.0 and 0.5: interpolate from “clear” green to solid green.

Weak zones are barely visible, mid-strength zones appear as solid green.

For strength between 0.5 and 1.0: interpolate from solid green to solid red.

The strongest zones shift toward the red anchor, clearly separating them from everything else.

Strength scale legend

To make the gradient readable, the indicator draws a vertical legend on the right side of the chart:

About 15 cells from top (Strong) to bottom (Weak).

Each cell uses the same gradient function as the zones themselves.

Top cell is labeled “Strong”; bottom cell is labeled “Weak”.

This legend acts as a fixed reference so you can instantly map a zone’s color to its approximate strength rank.

What it plots

At a glance, the indicator produces:

Upper liquidity zones above price, built from large upper wick events.

Lower liquidity zones below price, built from large lower wick events.

All zones colored by relative strength using the same gradient.

Zones that freeze when price breaks them, then fade out via decay and removal.

A strength scale legend on the right to interpret the gradient.

There are no extra lines, labels, or clutter. The focus is the evolving structure of liquidity zones and their visual strength.

How to read the zones

Bright red / bright green zones

These are your current “major” liquidity areas. They have high scores relative to other zones and have not yet decayed. Expect meaningful reactions, absorption attempts, or spillover moves when price interacts with them.

Faded zones

Pale, nearly transparent zones are either old, decayed, or minor. They can still matter, but priority is lower. If these are in the middle of a long consolidation, they often become background noise.

Broken but still visible zones

Zones whose extension has stopped have been overrun by closing price. They show where a key level gave way. You can use them as context for regime shifts or failed attempts.

Absence of zones

A chart with few or no zones means that, under your current thresholds, there have not been strong enough liquidity events recently. Either tighten the filters or accept that recent price action has been relatively balanced.

Use cases

1) Intraday liquidity hunting

Run the indicator on lower timeframes (e.g., 1–15 minute) with moderately fast decay.

Use the upper zones as potential sell reaction areas, the lower zones as potential buy reaction areas.

Combine with order flow, CVD, or footprint tools to see whether price is absorbing or rejecting at each zone.

2) Swing trading context

Increase ATR length and range/wick multipliers to focus only on major spikes.

Set slower decay and higher max lifetime so zones persist across multiple sessions.

Use these zones as swing inflection areas for larger setups, for example anticipating re-tests after breakouts.

3) Stop placement and invalidation

For longs, place invalidation beyond a decaying lower zone rather than in the middle of noise.

For shorts, place invalidation beyond strong upper zones.

If price closes through a strong zone and it freezes, treat that as additional evidence your prior bias may be wrong.

4) Identifying trapped flows

Upper zones formed after violent spikes up that quickly fail can mark trapped longs.

Lower zones formed after violent spikes down that quickly reverse can mark trapped shorts.

Watching how price behaves on the next touch of those zones can hint at whether those participants are being rescued or squeezed.

Settings overview

Event Detection

Use volume filter — enable or disable the volume spike requirement.

Volume SMA length — rolling window for average volume.

Volume spike multiplier — how aggressive the volume spike filter is.

ATR length — period for ATR, used in all size comparisons.

Min wick size in ATRs — minimum wick size threshold.

Min range in ATRs — minimum bar range threshold.

Zone Geometry

Zone thickness in ATRs — vertical size of each liquidity zone, scaled by ATR.

Decay & Lifetime

Score decay per bar — multiplicative decay factor for each zone score per bar.

Max bars a zone can live — hard cap on lifetime.

Minimum score before removal — score cut-off at which zones are deleted.

Gradient & Color

Mid strength color (green) — base color for mid-level zones and the lower half of the gradient.

High strength color (red) — target color for the strongest zones.

Max opacity — controls the most solid end of the gradient (0 = fully solid, 100 = fully invisible).

Tuning guidance

Fast, session-only liquidity

Shorter ATR length (e.g., 20–50).

Higher wick and range multipliers to focus only on extreme events.

Decay per bar closer to 0.95–0.98 and moderate max lifetime.

Volume filter enabled with a decent multiplier (e.g., 1.5–2.0).

Slow, structural zones

Longer ATR length (e.g., 100+).

Moderate wick and range thresholds.

Decay per bar very close to 1.0 for slow fading.

Higher max lifetime and slightly higher min score threshold so only very weak zones disappear.

Noisy, high-volatility instruments

Increase wick and range ATR multipliers to avoid over-triggering.

Consider enabling the volume filter with stronger settings.

Keep decay moderate to avoid the chart getting overloaded with old zones.

Notes

This is a structural and contextual tool, not a complete trading system. It does not account for transaction costs, execution slippage, or your specific strategy rules. Use it to:

Highlight where liquidity has recently been tested hard.

Rank these areas by decaying strength.

Guide your attention when layering in separate entry signals, risk management, and higher-timeframe context.

Time-Decay Liquidity Zones is designed to keep your chart focused on where the market has most recently “cared” about price, and to gradually forget what no longer matters. Adjust the detection, geometry, decay, and gradient to fit your product and timeframe, and let the zones show you which parts of the tape still have unfinished business.

Kalman Adjusted Average True Range [BackQuant]Kalman Adjusted Average True Range

A volatility-aware trend baseline that fuses a Kalman price estimate with ATR “rails” to create a smooth, adaptive guide for entries, exits, and trailing risk.

Built on my original Kalman

This indicator is based on my original Kalman Price Filter:

That core smoother is used here to estimate the “true” price path, then blended with ATR to control step size and react proportionally to market noise.

What it plots

Kalman ATR Line the main baseline that turns up/down with the filtered trend.

Optional Moving Average of the Kalman ATR a secondary line for confluence (SMA/Hull/EMA/WMA/DEMA/RMA/LINREG/ALMA).

Candle Coloring (optional) paint bars by the baseline’s current direction.

Why combine Kalman + ATR?

Kalman reduces measurement noise and produces a stable path without the lag of heavy MAs.

ATR rails scale the baseline’s step to current volatility, so it’s calm in chop and more responsive in expansion.

The result is a single, intelligible line you can trade around: slope-up = constructive; slope-down = caution.

How it works (plain English)

Each bar, the Kalman filter updates an internal state (tunable via Process Noise , Measurement Noise , and Filter Order ) to estimate the underlying price.

An ATR band (Period × Factor) defines the allowed per-bar adjustment. The baseline cannot “jump” beyond those rails in one step.

A direction flip is detected when the baseline’s slope changes sign (upturn/downturn), and alerts are provided for both.

Typical uses

Trend confirmation Trade in the baseline’s direction; avoid fading a firmly rising/falling line.

Pullback timing Look for entries when price mean-reverts toward a rising baseline (or exits on tags of a falling one).

Trailing risk Use the baseline as a dynamic guide; many traders set stops a small buffer beyond it (e.g., a fraction of ATR).

Confluence Enable the MA overlay of the Kalman ATR; alignment (baseline above its MA and rising) supports continuation.

Inputs & what they do

Calculation

Kalman Price Source which price the filter tracks (Close by default).

Process Noise how quickly the filter can adapt. Higher = more responsive (but choppier).

Measurement Noise how much you distrust raw price. Higher = smoother (but slower to turn).

Filter Order (N) depth of the internal state array. Higher = slightly steadier behavior.

Kalman ATR

Period ATR lookback. Shorter = snappier; longer = steadier.

Factor scales the allowed step per bar. Larger factors permit faster drift; smaller factors clamp movement.

Confluence (optional)

MA Type & Period compute an MA on the Kalman ATR line , not on price.

Sigma (ALMA) if ALMA is selected, this input controls the curve’s shape. (Ignored for other MA types.)

Visuals

Plot Kalman ATR toggle the main line.

Paint Candles color bars by up/down slope.

Colors choose long/short hues.

Signals & alerts

Trend Up baseline turns upward (slope crosses above 0).

Alert: “Kalman ATR Trend Up”

Trend Down baseline turns downward (slope crosses below 0).

Alert: “Kalman ATR Trend Down”

These are state flips , not “price crossovers,” so you avoid many one-bar head-fakes.

How to start (fast presets)

Swing (daily/4H) ATR Period 7–14, Factor 0.5–0.8, Process Noise 0.02–0.05, Measurement Noise 2–4, N = 3–5.

Intraday (5–15m) ATR Period 5–7, Factor 0.6–1.0, Process Noise 0.05–0.10, Measurement Noise 2–3, N = 3–5.

Slow assets / FX raise Measurement Noise or ATR Period for calmer lines; drop Factor if the baseline feels too jumpy.

Reading the line

Rising & curving upward momentum building; consider long bias until a clear downturn.

Flat & choppy regime uncertainty; many traders stand aside or tighten risk.

Falling & accelerating distribution lower; short bias until a clean upturn.

Practical playbook

Continuation entries After a Trend Up alert, wait for a minor pullback toward the baseline; enter on evidence the line keeps rising.

Exit/reduce If long and the baseline flattens then turns down, trim or exit; reverse logic for shorts.

Filters Add a higher-timeframe check (e.g., only take longs when the daily Kalman ATR is rising).

Stops Place stops just beyond the baseline (e.g., baseline − x% ATR for longs) to avoid “tag & reverse” noise.

Notes

This is a guide to state and momentum, not a guarantee. Combine with your process (structure, volume, time-of-day) for decisions.

Settings are asset/timeframe dependent; start with the presets and nudge Process/Measurement Noise until the baseline “feels right” for your market.

Summary

Kalman ATR takes the noise-reduction of a Kalman price estimate and couples it with volatility-scaled movement to produce a clean, adaptive baseline. If you liked the original Kalman Price Filter (), this is its trend-trading cousin purpose-built for cleaner state flips, intuitive trailing, and confluence with your existing

Deadband Hysteresis Supertrend [BackQuant]Deadband Hysteresis Supertrend

A two-stage trend tool that first filters price with a deadband baseline, then runs a Supertrend around that baseline with optional flip hysteresis and ATR-based adverse exits.

What this is

A hybrid of two ideas:

Deadband Hysteresis Baseline that only advances when price pulls far enough from the baseline to matter. This suppresses micro noise and gives you a stable centerline.

Supertrend bands wrapped around that baseline instead of raw price. Flips are further gated by an extra margin so side changes are more deliberate.

The goal is fewer whipsaws in chop and clearer regime identification during trends.

How it works (high level)

Deadband step — compute a per-bar “deadband” size from one of four modes: ATR, Percent of price, Ticks, or Points. If price deviates from the baseline by more than this amount, move the baseline forward by a fraction of the excess. If not, hold the line.

Centered Supertrend — build upper and lower bands around the baseline using ATR and a user factor. Track the usual trailing logic that tightens a band while price moves in its favor.

Flip hysteresis — require price to exceed the active band by an extra flip offset × ATR before switching sides. This adds stickiness at the boundary.

Adverse exit — once a side is taken, trigger an exit if price moves against the entry by K × ATR .

If you would like to check out the filter by itself:

What it plots

DBHF baseline (optional) as a smooth centerline.

DBHF Supertrend as the active trailing band.

Candle coloring by trend side for quick read.

Signal markers 𝕃 and 𝕊 at flips plus ✖ on adverse exits.

Inputs that matter

Price Source — series being filtered. Close is typical. HL2 or HLC3 can be steadier.

Deadband mode — ATR, Percent, Ticks, or Points. This defines the “it’s big enough to matter” zone.

ATR Length / Mult (DBHF) — only used when mode = ATR. Larger values widen the do-nothing zone.

Percent / Ticks / Points — alternatives to ATR; pick what fits your market’s convention.

Enter Mult — scales the deadband you must clear before the baseline moves. Increase to filter more noise.

Response — fraction of the excess applied to baseline movement. Higher responds faster; lower is smoother.

Supertrend ATR Period & Factor — traditional band size controls; higher factor widens and flips less often.

Flip Offset ATR — extra ATR buffer required to flip. Useful in choppy regimes.

Adverse Stop K·ATR — per-trade danger brake that forces an exit if price moves K×ATR against entry.

UI — toggle baseline, supertrend, signals, and bar painting; choose long and short colors.

How to read it

Green regime — candles painted long and the Supertrend running below price. Pullbacks toward the baseline that fail to breach the opposite band often resume higher.

Red regime — candles painted short and the Supertrend running above price. Rallies that cannot reclaim the band may roll over.

Frequent side swaps — reduce sensitivity by increasing Enter Mult, using ATR mode, raising the Supertrend factor, or adding Flip Offset ATR.

Use cases

Bias filter — allow entries only in the direction of the current side. Use your preferred triggers inside that bias.

Trailing logic — treat the active band as a dynamic stop. If the side flips or an adverse K·ATR exit prints, reduce or close exposure.

Regime map — on higher timeframes, the combination baseline + band produces a clean up vs down template for allocation decisions.

Tuning guidance

Fast markets — ATR deadband, modest Enter Mult (0.8–1.2), response 0.2–0.35, Supertrend factor 1.7–2.2, small Flip Offset (0.2–0.5 ATR).

Choppy ranges — widen deadband or raise Enter Mult, lower response, and add more Flip Offset so flips require stronger evidence.

Slow trends — longer ATR periods and higher Supertrend factor to keep you on side longer; use a conservative adverse K.

Included alerts

DBHF ST Long — side flips to long.

DBHF ST Short — side flips to short.

Adverse Exit Long / Short — K·ATR stop triggers against the current side.

Strengths

Deadbanded baseline reduces micro whipsaws before Supertrend logic even begins.

Flip hysteresis adds a second layer of confirmation at the boundary.

Optional adverse ATR stop provides a uniform risk cut across assets and regimes.

Clear visuals and minimal parameters to adjust for symbol behavior.

Putting it together

Think of this tool as two decisions layered into one view. The deadband baseline answers “does this move even count,” then the Supertrend wrapped around that baseline answers “if it counts, which side should I be on and where do I flip.” When both parts agree you tend to stay on the correct side of a trend for longer, and when they disagree you get an early warning that conditions are changing.

When the baseline bends and price cannot reclaim the opposite band , momentum is usually continuing. Pullbacks into the baseline that stall before the far band often resolve in trend.

When the baseline flattens and the bands compress , expect indecision. Use the Flip Offset ATR to avoid reacting to the first feint. Wait for a clean band breach with follow through.

When an adverse K·ATR exit prints while the side has not flipped , treat it as a risk event rather than a full regime change. Many users cut size, re-enter only if the side reasserts, and let the next flip confirm a new trend.

Final thoughts

Deadband Hysteresis Supertrend is best read as a regime lens. The baseline defines your tolerance for noise, the bands define your trailing structure, and the flip offset plus adverse ATR stop define how forgiving or strict you want to be at the boundary. On strong trends it helps you hold through shallow shakeouts. In choppy conditions it encourages patience until price does something meaningful. Start with settings that reflect the cadence of your market, observe how often flips occur, then nudge the deadband and flip offset until the tool spends most of its time describing the move you care about rather than the noise in between.

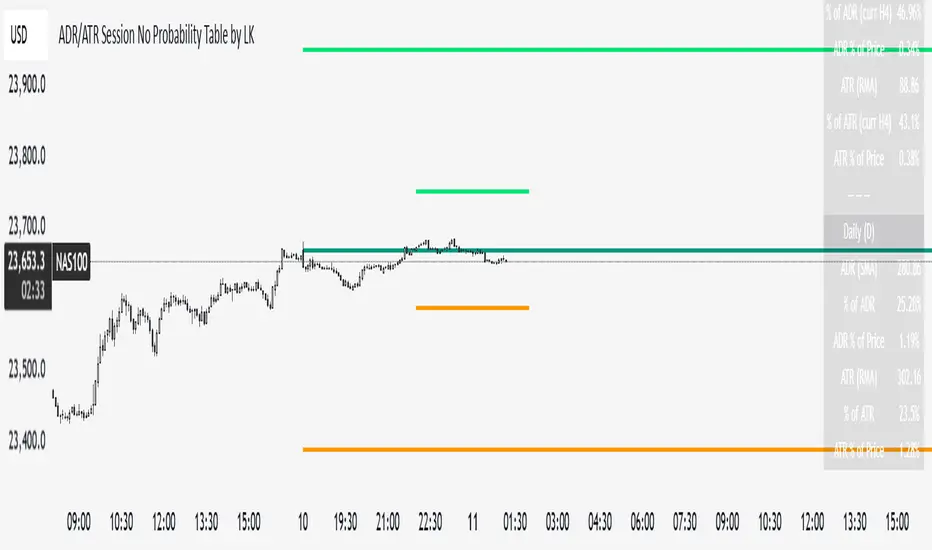

ADR/ATR Session No Probability Table by LKHere you go—clear, English docs you can drop into your script’s description or share with teammates.

ADR/ATR Session by LK — Overview

This indicator summarizes Average Daily Range (ADR) and Average True Range (ATR) for two horizons:

• Session H4 (e.g., 06:00–13:00 on a 4‑hour chart)

• Daily (D)

It shows:

• Current ADR/ATR values (using your chosen smoothing method)

• How much of ADR/ATR today/this bar has already been consumed (% of ADR/ATR)

• ADR/ATR as a percent of price

• Optional probability blocks: likelihood that %ADR will exceed user‑defined thresholds over a lookback window

• Optional on‑chart lines for the current H4 and Daily candles: Open, ADR High, ADR Low

⸻

What the metrics mean

• ADR (H4 / D): Moving average of the bar range (high - low).

• ATR (H4 / D): Moving average of True Range (max(hi-lo, |hi-close |, |lo-close |)).

• % of ADR (curr H4): (H4 range of the current H4 bar) / ADR(H4) × 100. Updates live even if the current time is outside the session.

• % of ADR (Daily): (today’s intra‑day range) / ADR(D) × 100.

• % of ATR (curr H4 / Daily): TR / ATR × 100 for that horizon.

• ADR % of Price / ATR % of Price: ADR or ATR divided by current price × 100 (a quick “volatility vs. price” gauge).

Session logic (H4): ADR/ATR(H4) only update on bars that fall inside the configured session window; outside the window the values hold steady (no recalculation “bleed”).

Daily range tracking: The indicator tracks today’s high/low in real‑time and resets at the day change.

⸻

Inputs (quick reference)

Core

• Length (ADR/ATR): smoothing length for ADR/ATR (default 21).

• Wait for Higher TF Bar Close: if true, updates ADR/ATR only after the higher‑TF bar closes when using request.security.

Timeframes

• Session Timeframe (H4): default 240.

• Daily Timeframe: default D.

Session time

• Session Timezone: “Chart” (default) or a fixed timezone.

• Session Start Hour, End Hour (minutes are fixed to 0 in this version).

Smoothing methods

• H4 ADR Method / H4 ATR Method: SMA/EMA/RMA/WMA.

• Daily ADR Method / Daily ATR Method: SMA/EMA/RMA/WMA.

Table appearance

• Table BG, Table Text, Table Font Size.

Lines (optional)

• Show current H4 segments, Show current Daily segments

• Line colors for Open / ADR High / ADR Low

• Line width

Probability

• H4 Probability Lookback (bars): number of H4 bars to examine (e.g., 300).

• Daily Probability Lookback (days): number of D bars (e.g., 180).

• ADR thresholds (%): CSV list of thresholds (e.g., 25,50,55,60,65,70,75,80,85,90,95,100,125,150).

The table will show the % of lookback bars where %ADR ≥ threshold.

Tip: If you want probabilities only for session H4 bars (not every H4 bar), ask and I can add a toggle to filter by inSess.

⸻

How to read the table

H4 block

• ADR (method) / ATR (method): the session‑aware averages.

• % of ADR (curr H4): live progress of this H4 bar toward the session ADR.

• ADR % of Price: ADR(H4) relative to price.

• % of ATR (curr H4) and ATR % of Price: same idea for ATR.

H4 Probability (lookback N bars)

• Rows like “≥ 80% ADR” show the fraction (in %) of the last N H4 bars that reached at least 80% of ADR(H4).

Daily block

• Mirrors the H4 block, but for Daily.

Daily Probability (lookback M days)

• Rows like “≥ 100% ADR” show the fraction of the last M daily bars whose daily range reached at least 100% of ADR(D).

⸻

Practical usage

• Use % of ADR (curr H4 / Daily) to judge exhaustion or room left in the day/session.

E.g., if Daily %ADR is already 95%, be cautious with momentum continuation trades.

• The probability tables give a quick historical context:

If “≥ 125% ADR” is ~18%, the market rarely stretches that far; your trade sizing/targets can reflect that.

• ADR/ATR % of Price helps normalize volatility between instruments.

⸻

Troubleshooting

• If probability rows are blank: ensure lookback windows are large enough (and that the chart has enough history).

• If ADR/ATR show … (NA): usually you don’t have enough bars for the chosen length/TF yet.

• If line segments are missing: verify you’re on a chart with visible current H4/D bars and the toggles are enabled.

⸻

Notes & customization ideas

• Add a toggle to count only session bars in H4 probability.

• Add separate thresholds for H4 vs Daily.

• Let users pick minutes for session start/end if needed.

• Add alerts when %ADR crosses specified thresholds.

If you want me to bundle any of the “ideas” above into the code, say the word and I’ll ship a clean patch.

WRAMA Channel (Weighted RSI ATR MA)OVERVIEW

The WRAMA Channel (Weighted RSI ATR MA) is an advanced technical analysis tool designed to react more quickly to price movements compared to indicators using conventional moving averages. It combines the Relative Strength Index (RSI), Average True Range (ATR), and a weighted moving average, resulting in the WRAMA. This indicator forms a dynamic price channel based on a weighted average that incorporates both trend strength (via RSI) and market volatility (via ATR). It helps traders identify trends, potential reversals, and breakout signals, while offering broad customization options.

Key Features

WRAMA Price Channel:

Generates a dynamic channel around the weighted moving average (WRAMA), adapting to market volatility and momentum, similar to Bollinger Bands. Users are encouraged to adjust channel width and length according to their strategy.

The upper and lower channel bands are calculated based on a percentage deviation from the baseline line.

The channel fill color changes depending on the price's position relative to the baseline (green above, red below), with an optional gradient for better visualization.

Weighted Moving Average (WRAMA):

WRAMA is a custom weighted moving average (MA1), where closing prices are weighted based on RSI and ATR, allowing it to dynamically adapt to market conditions.

Baseline: The WRAMA line calculated over a user-defined period.

WRAMA Calculation:

RSI Weight: Based on RSI value. When RSI is in extreme zones (below the lower threshold or above the upper threshold), an extreme weight is applied. Otherwise, the weight is based on the squared RSI value divided by 100, raised to a power defined by the rsi_weight_factor.

ATR Weight: Based on the ATR-to-average-ATR ratio. If ATR exceeds a threshold (atr_threshold × avg_atr), an extreme weight is applied. Otherwise, the weight is based on the squared ratio of ATR to average ATR, raised to the power of the atr_weight_factor.

Combined Weight: RSI and ATR weights are combined using a rsi_atr_balance parameter. Final weight = RSI weight × balance + ATR weight × (1 - balance).

WRAMA Calculation: The closing price is multiplied by the combined weight. The result is averaged over the ma_length period and divided by the average of the weights, forming the WRAMA line. For current WRAMA (ma_length = 1), the calculation simplifies to a single weighted price.

Additional Moving Averages:

For additional confirmations, the indicator supports up to five moving averages (MA1–MA5) with various types (SMA, EMA, WMA, HMA, ALMA) and customizable periods.

All additional MAs are calculated based on WRAMA or its baseline, ensuring consistency and enabling deeper analysis within a unified methodology. MA trend directions can be tracked in a built-in signal table.

Trading Signals:

Breakout Signals: Breakouts above/below the channel are optionally marked with triangle shapes (green for bullish, red for bearish).

MA Signals: Price position relative to MAs or their slope generates bullish/bearish signals. These are optionally visualized with default triangles (green up, red down).

A signal table in the top-right corner summarizes the status of each moving average – bullish, bearish, or neutral.

Customization Options

Channel Settings:

MA Period: Length of the WRAMA baseline (default: 100).

Channel Deviation : Percentage offset from the baseline for upper/lower bands (default: 1.5%).

RSI Settings:

RSI Period: Length of the RSI calculation (default: 14).

RSI Upper/Lower Threshold: Overbought/oversold levels (default: 70/30).

RSI Weight Factor: Influence of RSI on weighting (default: 2.0).

ATR Settings:

ATR Period: ATR calculation length (default: 14).

ATR Threshold: Volatility threshold as a multiple of average ATR (default: 1.5).

ATR Weight Factor: Influence of ATR on weighting (default: 2.0).

RSI & ATR Combined:

Extreme Weight: Weight applied in extreme RSI/ATR conditions (default: 3.0).

RSI/ATR Balance: Balance between RSI and ATR influence (default: 0.5).

Signal Settings:

Show Breakout Signals: Enable/disable breakout triangles.

Show MA Signals: Enable/disable MA-based signals.

MA Signal Source: Choose between current WRAMA or baseline.

MA Signal Analysis: Based on price position or slope.

Neutral Threshold : Minimum distance from MA for signal neutrality (default: 0.5%).

Minimum MA Slope : Minimum slope for trend direction signals (default: 0.01%).

Moving Averages (MA1–MA5):

Options to enable/disable, select type (SMA, EMA, WMA, HMA, ALMA), set period length, and choose color.

Style Settings:

Gradient Fill: Enable/disable gradient coloring within the channel.

Show Baseline: Enable/disable WRAMA baseline visibility.

Colors: Customize line, fill, and signal colors.

Use Cases

Trend Identification: The WRAMA channel highlights trend direction and potential reversal zones when price contacts the channel edges.

Breakout Signals: Channel breakouts may indicate trend shifts or momentum surges.

MA Analysis: The signal table provides a clear summary of market direction (bullish, bearish, or neutral) based on selected moving averages.

Trading Strategies: Suitable for trend-following, mean-reversion, and scalping strategies, depending on user preferences and settings.

Notes

The indicator offers a high degree of flexibility, making it adaptable to various trading styles, instruments, and timeframes.

It is recommended to adjust channel length and width to fit your trading strategy.

Backtesting settings on historical data is advised to optimize parameters for a specific strategy and market.

ALEX - ATR Extensions + ADR + TableALEX - ATR Extensions + ADR + Table

Overview

The ALEX ATR Extensions indicator is a comprehensive volatility and momentum analysis tool that combines Average True Range (ATR), Average Daily Range (ADR), and moving average distance calculations in a single, customizable display. This indicator helps traders assess current price action relative to historical volatility and key moving averages, providing crucial context for risk management and trade planning.

Key Features

Multi-Metric Analysis

- ATR Percentage: Current ATR as a percentage of price for volatility assessment

- ADR Percentage: Average Daily Range as a percentage for typical daily movement

- Low of Day Distance: Distance from current price to daily low

- Moving Average Distance: ATR-normalized distance from 21 and 50 period moving averages

Flexible Moving Average Options

- Configurable MA Types: Choose between EMA or SMA for both 21 and 50 period averages

- Customizable Periods: Adjust moving average lengths to suit your trading style

- Daily Timeframe Data: Uses daily moving averages regardless of chart timeframe

ATR Extension Levels

- Dynamic Price Targets: Calculate extension levels based on ATR multiples from moving averages

- Visual Reference Lines: Optional overlay lines showing ATR extension targets

- Customizable Multipliers: Adjust ATR multipliers for different risk/reward scenarios

Smart Visual Alerts

- Color-Coded Distance Metrics: Automatic color changes based on distance thresholds

- Symbol Plotting: Customizable chart symbols when distance thresholds are exceeded

- Threshold-Based Alerts: Visual cues when price reaches significant ATR distances

Comprehensive Data Table

- Real-Time Metrics: Live updating table with all key measurements

- Customizable Display: Toggle individual metrics on/off based on preference

- Professional Styling: Adjustable colors, fonts, and transparency

How to Use

Volatility Assessment

- High ATR%: Indicates elevated volatility, larger position sizing considerations

- Low ATR%: Suggests compressed volatility, potential for expansion

- ADR% Comparison: Compare current day's range to historical average

Moving Average Analysis

- ATR Distance 21/50: Normalized distance showing how extended price is from key levels

- Positive Values: Price above moving average (bullish positioning)

- Negative Values: Price below moving average (bearish positioning)

- Color Changes: Automatic alerts when reaching threshold levels

Extension Target Planning

- ATR Extension Lines: Visual price targets based on volatility-adjusted projections

- Risk/Reward Planning: Use extension levels for profit target placement

- Breakout Confirmation: Extension levels can confirm breakout validity

Symbol Alert System

- Chart Symbols: Automatic plotting when distance thresholds are breached

- Customizable Triggers: Set your own threshold levels for alerts

- Visual Scanning: Quick identification of extended conditions across multiple charts

Settings

Display Controls

- Show ADR%: Toggle average daily range percentage display

- Show ATR%: Toggle average true range percentage display

- Show LoD Distance: Toggle low of day distance calculation

- Show LoD Price: Toggle actual low of day price display

- Show ATR Distance from 21/50 DMA: Toggle moving average distance metrics

- Show 21/50 DMA Price: Toggle actual moving average price display

- Show ATR Extension Levels: Toggle extension target display in table

Moving Average Configuration

- 21/50 DMA Type: Choose between EMA or SMA calculation methods

- 21/50 DMA Period: Customize moving average lengths

- ADR/ATR Length: Adjust calculation periods for range measurements

Color Thresholds

- Threshold Levels: Set distance levels for color changes (default 2.0 and 5.0)

- Custom Colors: Choose colors for different threshold breaches

- Separate 21/50 Settings: Independent color schemes for each moving average

Symbol Settings

- Show Char Symbol: Toggle symbol plotting for each moving average

- Custom Symbols: Choose any character for chart plotting

- Symbol Colors: Customize colors for visual distinction

- Threshold Levels: Set trigger points for symbol appearance

ATR Extension Lines

- Show Extension Lines: Toggle visual extension level lines

- ATR Multipliers: Customize extension distance (default 2.0x)

- Line Colors: Choose colors for extension level visualization

Table Customization

- Background Color: Adjust table transparency and color

- Text Color: Customize default text appearance

- Font Size: Choose from tiny to huge font options

Advanced Applications

Trend Strength Analysis

- Large ATR distances suggest strong trending moves

- Small ATR distances indicate potential consolidation or reversal zones

- Compare current readings to recent historical ranges

Risk Management

- Use ATR% for position sizing calculations

- Extension levels provide natural profit target zones

- Distance metrics help identify overextended conditions

Multi-Timeframe Context

- Apply to different timeframes for comprehensive analysis

- Daily data provides consistency across all chart intervals

- Combine with weekly/monthly analysis for broader context

Market Regime Identification

- High volatility periods: Increased ATR% readings

- Low volatility periods: Compressed ATR% readings

- Trending markets: Sustained high distance readings

- Consolidating markets: Low distance readings with frequent color changes

Best Practices

Volatility-Adjusted Trading

- Increase position sizes during low volatility periods

- Reduce position sizes during high volatility periods

- Use ATR% for stop-loss placement relative to normal market movement

Extension Level Usage

- Primary targets: 1.5-2.0x ATR extensions

- Secondary targets: 2.5-3.0x ATR extensions

- Avoid chasing prices beyond 3x ATR extensions

Threshold Optimization

- Backtest different threshold levels for your trading style

- Consider market conditions when setting alert levels

- Adjust thresholds based on instrument volatility characteristics

Integration Strategies

- Combine with momentum indicators for confirmation

- Use alongside support/resistance levels

- Incorporate into systematic trading approaches

Technical Specifications

- Compatible with Pine Script v6

- Uses daily timeframe data for consistency

- Optimized for real-time performance

- Works on all chart types and timeframes

- Supports all tradeable instruments

Ideal For

- Swing traders using daily charts

- Position traders seeking volatility context

- Day traders needing intraday reference levels

- Risk managers requiring volatility metrics

- Systematic traders building rule-based strategies

Disclaimer

This indicator is for educational and informational purposes only. It should not be used as the sole basis for trading decisions. Always combine with other forms of analysis, proper risk management techniques, and consider your individual trading plan and risk tolerance. Past performance does not guarantee future results.

Compatible with Pine Script v6 | Optimized for daily timeframe analysis | Works across all markets and instruments

Trend CCITrend CCI (TCCI) Indicator

Description:

The Trend CCI (TCCI) indicator is a unique combination of the Commodity Channel Index (CCI) and the Average True Range (ATR), designed to identify trends and market reversals with a refined sensitivity to price volatility. The indicator plots the CCI, adjusted by an ATR filter, and color-codes the trendline to signal uptrends and downtrends.

How It Works:

This indicator uses the CCI to measure price momentum and an ATR-based filter to smooth out market noise, making it easier to detect significant shifts in the market trend. Key parameters such as the ATR Period, ATR Multiplier, and CCI Period have been carefully chosen to optimize the indicator's performance:

1. ATR Period (default: 18)

The ATR Period determines the number of periods used to calculate the **Average True Range**, which reflects market volatility. In this case, an **ATR Period of 18** has been selected for several reasons:

Balance between responsiveness and noise reduction : A period of 18 strikes a balance between being responsive to recent price movements and filtering out minor fluctuations. Shorter ATR periods might be too reactive, creating false signals, while longer periods might miss shorter-term trends.

Adaptable to various market conditions : An 18-period ATR is suitable for both intraday and swing trading strategies, making it versatile across different time frames.

Standard industry practice : Many traders use ATR settings between 14 and 20 periods as a convention for detecting reliable volatility levels.

2. ATR Multiplier (default: 1.5)

The ATR Multiplier is applied to the ATR value to define how sensitive the indicator is to volatility. In this case, a multiplier of 1.5 has been chosen:

Avoiding whipsaws in low volatility markets: By setting the multiplier to 1.5, the indicator filters out smaller, less significant price movements, reducing the likelihood of whipsaw signals (i.e., false trend reversals during periods of low volatility).

Optimizing signal accuracy: A moderate multiplier like 1.5 ensures that the indicator only generates signals when the price moves a significant distance from the average range. Higher multipliers (e.g., 2.0) may ignore valid opportunities, while lower multipliers (e.g., 1.0) might create too many signals.

Enhancing trend clarity : The multiplier’s role in widening the range allows the indicator to respond more clearly during periods of strong trends, reducing signal noise and false positives.

3. CCI Period (default: 63)

The CCI Period defines the number of periods used to calculate the Commodity Channel Index. A 63-period CCI is selected based on the following considerations:

Smoothing the momentum calculation: A longer period, such as 63, is used to smooth out the CCI and reduce the effects of short-term price fluctuations. This period captures longer-term momentum, making it ideal for identifying more significant market trends.

-Filtering out short-term noise: While shorter CCI periods (e.g., 14 or 20) may be more reactive, they tend to produce more signals, some of which may be false. A 63-period CCI focuses on stronger and more sustained price movements, providing fewer but higher-quality signals.

Adapted to intermediate trading: A 63-period CCI aligns well with traders looking for medium-term trend-following strategies, striking a balance between long-term trend identification and responsiveness to significant price shifts.

How to Use:

Green Area: When the trendline turns green, it signals that the CCI is positive, reflecting upward momentum. This can be interpreted as a buy signal, indicating the potential for long positions or continuing bullish trades.

Red Area: When the trendline turns red, it signals that the CCI is negative, reflecting downward momentum. This can be interpreted as a sell signal, indicating potential short positions or bearish trades.

ATR Filter: The ATR helps reduce false signals by ignoring minor price movements. Traders can adjust the ATR Multiplier to make the indicator more or less sensitive based on market conditions. A lower multiplier (e.g., 1.2) may increase signal frequency, while a higher multiplier (e.g., 2.0) reduces it.

Originality:

The Trend CCI (TCCI) stands out due to its combination of the CCI and ATR. While many indicators simply plot raw CCI values, this script enhances the CCI’s effectiveness by incorporating an ATR-based volatility filter. This ensures that only significant trends trigger signals, making it a more reliable tool in volatile markets. The choice of the ATR period, multiplier, and CCI period ensures a refined balance between trend detection and noise reduction, distinguishing it as a powerful trend-following indicator.

Additionally, the visual aspect—using color-coded trendlines that dynamically shift between green and red—simplifies the interpretation of market trends, offering traders a clear and immediate understanding of trend direction and momentum strength.

Final Recommendations:

Use in Trending Markets The TCCI is most effective in trending markets, where its signals align with broader market momentum. In sideways or low-volatility markets, consider adjusting the ATR multiplier or using other complementary indicators to confirm the signals.

Risk Management: Always integrate robust risk management practices, such as using stop-loss orders and position sizing, to protect against sudden market reversals or periods of heightened volatility.

Adjust for Volatility: Consider the volatility of the asset being traded. In highly volatile assets, a higher ATR multiplier (e.g., 2.0) may be necessary to filter out noise, while in more stable assets, a lower multiplier (e.g., 1.2) might generate earlier signals.

By using the Trend CCI (TCCI) indicator with a deeper understanding of its key parameters, traders can better identify trends, reduce noise, and improve their overall decision-making in the markets.

Good Profits!

ATR%指標概要 / Overview

ATR Percentage (MTF):把 ATR 轉為百分比(ATR%)或保留為絕對值,並在該「波動序列」上套用布林帶。支援多週期(MTF)計算:例如在 5 分圖顯示 4H / D1 的 ATR%。內建白色點狀水平線作為固定門檻(預設 1%)。

ATR Percentage (MTF): Converts ATR to a percentage of price (ATR%) or keeps it as absolute ATR, then applies Bollinger Bands on this volatility series. Supports multi-timeframe (MTF) calculation (e.g., show 4H/D1 ATR% on a 5-min chart). Includes a configurable white dotted horizontal threshold line (default 1%).

⸻

設計目的 / Purpose

• 以 ATR% 衡量相對波動,利於跨品種比較。

Use ATR% for relative volatility to compare across markets.

• 以 布林帶 標示「高/低波動區」,觀察擴張與壓縮。

Use Bollinger Bands on volatility to highlight expansion/squeeze.

• 提供 固定閾值(1%) 作為策略濾網或告警門檻。

Provide a fixed threshold (1%) for filters/alerts.

• 以 MTF 方式,讓低週期策略用高週期波動做濾網。

MTF lets lower-TF strategies filter by higher-TF volatility.

⸻

參數說明 / Inputs

• Use ATR as % of Close:切換 ATR(絕對值)/ ATR%(建議)。

Toggle between absolute ATR and ATR% (recommended).

• ATR Periods:ATR 計算長度(預設 22)。

ATR lookback (default 22).

• Show Bollinger Bands / BB Periods / StdDev:布林帶開關、長度與倍數(預設 20 / 2)。

Bollinger Bands on/off, length, and deviation (default 20 / 2).

• Source Timeframe:計算用週期(如 60、240、D、W;留空/Chart = 跟隨圖表)。

Timeframe used for calculations (e.g., 60, 240, D, W; empty/“Chart” = current).

• Threshold Line (%):白色點線門檻,預設 1.0(即 1%)。

White dotted threshold line, default 1.0 (1%).

提醒:當 非 ATR% 模式時,Threshold 值代表「價格單位」而非百分比。

Note: In non-ATR% mode, the threshold is in price units, not percent.

⸻

訊號解讀 / How to Read

• ATR% > 上軌:波動顯著擴張(趨勢啟動或加速常見)。

ATR% above upper band: significant expansion; often trend ignition/acceleration.

• ATR% < 下軌:波動明顯壓縮(常見於突破前)。

ATR% below lower band: volatility squeeze; often precedes breakouts.

• ATR% 穿越 Threshold(1%):達到固定波動標準,可作策略開關或風控分水嶺。

ATR% crossing the 1% threshold: fixed volatility bar for filters/risk gates.

⸻

內建告警 / Built-in Alerts

• Volatility Breakout (MTF):ATR/ATR% 向上穿越上軌。

Triggers when ATR/ATR% crosses above the upper band.

• Volatility Squeeze (MTF):ATR/ATR% 向下穿越下軌。

Triggers when ATR/ATR% crosses below the lower band.

⸻

使用建議 / Suggested Uses

• 當沖濾網:於 1–5 分圖選擇 4H / D1 作為 Source Timeframe;僅在 ATR% > 1% 且位於中線以上時允許趨勢進場。

Intraday filter: on 1–5m charts, set 4H/D1 as source TF; allow trend entries only when ATR% > 1% and above the midline.

• 突破前偵測:ATR% 長時間貼近下軌 → 留意可能的波動擴張。

Pre-breakout scan: prolonged ATR% near lower band can foreshadow expansion.

• 跨品種比較:用 ATR% 統一指數、外匯、商品的波動刻度。