RSI + Elder Bull-Bear pressure RSI + Bull/Bear (Elder-Ray enhanced RSI)

What it is

An extended RSI that overlays Elder-Ray Bull/Bear Power on the same, zero-centered scale. You get classic RSI regime cues plus a live read of buy/sell pressure, with optional smoothing, bands, and right-edge value labels.

Key features

RSI with bands – default bands 30 / 50 / 70 (editable).

Bull/Bear Power (Elder) – ATR-normalized; optional EMA/SMA/RMA/HMA smoothing.

One-pane overlay – RSI and Bull/Bear share a common midline (RSI-50 ↔ panel 0).

Right-edge labels – always visible at the chart’s right margin with adjustable offsets.

How to read it

Cyan line = RSI (normalized)

Above the mid band = bullish regime; below = bearish regime.

Green = Bull Power, Red = Bear Power

Columns/lines above 0 show buy pressure; below 0 show sell pressure.

Smoothing reduces noise; zero-line remains your key reference.

Trade logic (simple playbook)

Entry

BUY (primary):

RSI crosses up through 50 (regime turns bullish), and

Bull (green) crosses up through 0 (buy pressure confirms).

SELL (primary):

RSI crosses down through 50, and

Bear (red) crosses down through 0 (sell pressure confirms).

Alternative momentum entries

Aggressive BUY: Bull (green) pushes above RSI-80 band (strong upside impulse).

Aggressive SELL: Bear (red) pushes below RSI-30 band (strong downside impulse).

Exits / trade management

In a long: consider exiting or tightening stops if Bear (red) dips below the 0 line (rising sell pressure) or RSI loses 50.

In a short: consider exiting or tightening if Bull (green) rises above 0 or RSI reclaims 50.

Tip: “0” on the panel is your pressure zero-line (maps to RSI-50). Most whipsaws happen near this line; smoothing (e.g., EMA 21) helps.

Defaults (on first load)

RSI bands: 30 / 50 / 70 with subtle fills.

Labels: tiny, pushed far right (large offsets).

Bull/Bear smoothing: EMA(21), smoothed line plot mode.

RSI plotted normalized so it overlaps the pressure lines cleanly.

Tighten or loosen the Bull/Bear thresholds (e.g., Bull ≥ +0.5 ATR, Bear ≤ −0.5 ATR) to demand stronger confirmation.

Settings that matter

Smoothing length/type – balances responsiveness vs. noise.

Power/RSI Gain – visual scaling only (doesn’t change logic).

Band placement – keep raw 30/50/80 or switch to “distance from 50” if you prefer symmetric spacing.

Label offsets – move values clear of the last bar/scale clutter.

Good practices

Combine with structure/ATR stops (e.g., 1–1.5× ATR, swing high/low).

In trends, hold while RSI stays above/below 50 and the opposite pressure line doesn’t dominate.

In ranges, favor signals occurring near the mid band and take profits at the opposite band.

Disclaimer: This is a research/visual tool, not financial advice at any kind. Test your rules on multiple markets/timeframes and size positions responsibly.

Buscar en scripts para "30年国债收益率"

Dow Jones Trading System with PivotsThis TradingView indicator, tailored for the 30-minute Dow Jones (^DJI) chart, supports DIA options trading with a trend-following approach. It features a 30-period SMA (blue) and a 60-period SMA (red), with an optional 90-period SMA (orange) drawn from rauItrades' Dow SMA outfit. A bullish crossover (30 SMA > 60 SMA) displays a green "BUY" triangle below the bar for potential DIA longs, while a bearish crossunder (30 SMA < 60 SMA) shows a red "SELL" triangle above for shorts or exits. The background turns green (bullish) or red (bearish) to indicate trend bias. Pivot points highlight recent highs (orange circles) and lows (purple circles) for support/resistance, using a 5-bar lookback. Alerts notify for crossovers.

CHOCH + FVG Signals [30m Optimized]CHOCH + FVG Signals

🎯 What It Does:

This script automatically scans your chart for high-probability Smart Money Concepts (SMC) setups based on two key institutional trading principles:

Change of Character (CHOCH) – A shift in market structure signaling potential reversal

Fair Value Gap (FVG) – An imbalance zone where price moved too fast, often acting as support/resistance

When both conditions align, the script plots clear Buy (▲) and Sell (▼) signals directly on your chart — ideal for intraday trading on the 30-minute timeframe (but works on any timeframe).

✅ Key Features:

🔹 Visual Fair Value Gaps

Green shaded zones = Bullish FVGs (potential support)

Red shaded zones = Bearish FVGs (potential resistance)

Toggle on/off in settings

🔹 Smart CHOCH Detection

Detects breaks of recent swing highs/lows with proper context

Avoids false signals by confirming prior price structure

🔹 Clear Trade Signals

Green ▲ below bar = Buy signal (Bullish CHOCH + FVG confluence)

Red ▼ above bar = Sell signal (Bearish CHOCH + FVG confluence)

🔹 Customizable Filters

Option to require FVG for a signal (recommended for higher accuracy)

Adjust sensitivity via swing detection settings (default optimized for 30m)

🔹 Alert-Ready

Built-in alert conditions for instant notifications on TradingView mobile/desktop

⚙️ How to Use:

Apply to a 30-minute chart (e.g., EURUSD, Gold, NAS100, BTC)

Wait for at least 50–100 bars to load (so swing points appear)

Look for:

A green triangle (▲) → consider long entry near FVG support

A red triangle (▼) → consider short entry near FVG resistance

Confirm with price action: Wait for a strong candle close or rejection at the FVG zone

Use stop-loss below/above the FVG and target recent liquidity pools

💡 Pro Tip: Best used during high-volume sessions (e.g., London Open 7–10 AM UTC, NY Open 12:30–3:30 PM UTC).

🛠️ Settings (Inputs):

Show Fair Value Gaps

✅ Enabled

Visualize FVG zones

Max FVG History

100 bars

Prevent chart clutter

Require FVG for Signal?

✅ Enabled

Higher-quality setups (disable to test CHOCH-only)

⚠️ Important Notes:

This is a signal generator, not financial advice. Always manage risk.

Works best in trending or breaking markets — avoid during low-volatility ranges.

FVGs may get filled (tested) before price continues — patience improves results.

Backtest on historical data before live trading.

📣 Ideal For:

Retail traders learning Smart Money Concepts (SMC)

Price action traders seeking institutional-level confluence

Intraday scalpers & swing traders on 30m–1H timeframes

ICT HTF Volume Candles (Based on HTF Candles by Fadi)# ICT HTF Volume Candles - Multi-Timeframe Volume Analysis

## Overview

This indicator provides multi-timeframe volume visualization designed to complement price action analysis. It displays volume data from up to 6 higher timeframes simultaneously in a separate panel, allowing traders to identify volume spikes, divergences, and institutional activity without switching between timeframes.

**Original Concept Credits:** This indicator builds upon the HTF Candles framework by Fadi, adapting it specifically for volume analysis with enhanced features including gap-filling for extended hours, multiple scaling methods, and advanced synchronization.

## What Makes This Script Original

### Key Innovations:

1. **Three Volume Scaling Methods:**

- **Per-HTF Auto Scale:** Each timeframe scales independently for detailed comparison

- **Global Auto Scale:** All timeframes use unified scale for relative volume comparison

- **Manual Scale:** User-defined maximum for consistent analysis across sessions

2. **Bullish/Bearish Volume Differentiation:**

- Volume bars colored based on price movement (close vs open)

- Separate styling for bullish (green) and bearish (red) volume periods

- Helps identify whether volume supports price direction

3. **Advanced Time Synchronization:**

- Custom daily candle open times (Midnight, 8:30 AM, 9:30 AM ET)

- Timezone-aware calculations for New York trading hours

- Real-time countdown timers for each timeframe

- **Gap-filling technology** for continuous display during extended hours and weekends

4. **Flexible Display Options:**

- Configurable spacing and positioning

- Label placement (top, bottom, or both)

- Day-of-week or time interval labels on candles

- Works reliably in backtesting and live trading

## How It Works

### Volume Calculation

The indicator uses `request.security()` with optimized parameters to fetch volume data from higher timeframes:

- **Volume Open/High/Low/Close (OHLC):** Tracks volume changes within each HTF candle

- **Color Logic:** Compares HTF close vs open prices to determine bullish/bearish classification

- **Alignment:** All volume bars share a common baseline for easy visual comparison

- **Gap Handling:** Uses `gaps=barmerge.gaps_off` to maintain continuity during non-trading hours

### Technical Implementation

```

1. Monitors HTF timeframe changes using request.security() with lookahead

2. Creates new VolumeCandle object when HTF bar opens

3. Updates current candle's volume H/L/C on each chart bar

4. Applies selected scaling method to normalize display height

5. Repositions all candles and labels on each bar update

6. Fills gaps automatically during extended hours for consistent display

```

### Scaling Methods Explained

**Method 1 - Auto Scale per HTF:**

Each timeframe displays volume relative to its own maximum. Best for identifying patterns within each individual timeframe.

**Method 2 - Global Auto Scale:**

All timeframes share the same scale based on the highest volume across all HTFs. Best for comparing relative volume strength between timeframes.

**Method 3 - Manual Scale:**

User sets maximum volume value. Best for maintaining consistent scale across different trading sessions or instruments.

## How to Use This Indicator

### Setup

1. Add indicator to your chart (it appears in a separate panel below price)

2. Configure up to 6 higher timeframes (default: 5m, 15m, 1H, 4H, 1D, 1W)

3. Set number of candles to display for each timeframe

4. Choose volume scaling method based on your analysis needs

5. Enable "Fix gaps in non-trading hours" for extended hours trading (enabled by default)

### Interpretation

**Volume Spikes:**

- Sudden increase in volume height indicates institutional activity or strong conviction

- Compare volume between timeframes to identify where the real money is moving

- Look for volume spikes that appear across multiple timeframes simultaneously

**Bullish vs Bearish Volume:**

- **Green volume bars:** Price closed higher (buying pressure)

- **Red volume bars:** Price closed lower (selling pressure)

- High green volume during uptrend = confirmation of strength

- High red volume during downtrend = confirmation of weakness

- High volume opposite to trend = potential reversal warning

**Multi-Timeframe Context:**

- **5m/15m:** Scalping and day trading activity

- **1H/4H:** Swing trading and intraday institutional flows

- **Daily/Weekly:** Major position building and long-term trends

**Divergences:**

- Price making new highs but volume declining = weakening trend

- Volume increasing while price consolidates = potential breakout brewing

- Price breaks level but volume doesn't confirm = likely false breakout

### Practical Examples

**Example 1 - Institutional Confirmation:**

Price breaks above resistance. Check volume across timeframes:

- 5m shows spike = retail interest

- 15m + 1H + 4H all show spikes = institutional confirmation

- **Trade confidence: HIGH**

**Example 2 - False Breakout Detection:**

Price breaks resistance with:

- High volume on 5m only

- Normal/low volume on 1H and 4H

- **Interpretation:** Likely retail trap, institutions not participating

- **Action:** Wait for pullback or avoid

**Example 3 - Accumulation Phase:**

Price ranges sideways but:

- Daily volume gradually increasing

- Weekly volume above average

- **Interpretation:** Smart money accumulating

- **Action:** Prepare for breakout in direction of volume

**Example 4 - Volume Divergence:**

Price makes new high:

- Current high has lower volume than previous high across all timeframes

- **Interpretation:** Weakening momentum

- **Action:** Consider profit-taking or reversal trade

## Configuration Parameters

### Timeframe Settings

- **HTF 1-6:** Select timeframes (must be higher than chart timeframe)

- **Max Display:** Number of candles to show per timeframe (1-50)

- **Limit to Next HTFs:** Display only first N enabled timeframes (1-6)

### Styling

- **Bull/Bear Colors:** Separate colors for body, border, and wick

- **Padding from current candles:** Distance offset from live price action

- **Space between candles:** Gap between individual volume bars

- **Space between Higher Timeframes:** Gap between different timeframe groups

- **Candle Width:** Thickness of volume bars (1-4, multiplied by 2)

### Volume Settings

- **Volume Scale Method:** Choose 1, 2, or 3

- 1 = Auto Scale per HTF (each TF independent)

- 2 = Global Auto Scale (all TF unified)

- 3 = Manual Scale (user-defined max)

- **Auto Scale Volume:** Enable/disable automatic scaling

- **Manual Scale Max Volume:** Set maximum when using Method 3

### Label Settings

- **HTF Label:** Show/hide timeframe names with color and size options

- **Label Positions:** Display at Top, Bottom, or Both

- **Label Alignment:** Align centered or Follow Candles

- **Remaining Time:** Show countdown timer until next HTF candle

- **Interval Value:** Display day-of-week or time on each candle

### Custom Daily Candle

- **Enable Custom Daily:** Override default daily candle timing

- **Open Time Options:**

- **Midnight:** Standard 00:00 ET daily open

- **8:30 AM:** Align with economic data releases

- **9:30 AM:** Align with NYSE market open

- Useful for specific trading strategies or market alignment

### Advanced Settings

- **Fix gaps in non-trading hours:** Maintains alignment during extended hours and weekends (recommended: ON)

- Prevents visual gaps during forex weekend closures

- Ensures consistent display during crypto 24/7 trading

- Improves backtesting reliability

## Best Practices

1. **Pair with Price Action:** Use alongside HTF price candles indicator for complete picture

2. **Start Simple:** Enable 2-3 timeframes initially (e.g., 15m, 1H, 4H), add more as needed

3. **Match Settings:** Use same candle width/spacing as companion price indicator for visual alignment

4. **Scale Appropriately:**

- Use **Global scale** (Method 2) when comparing timeframes

- Use **Per-HTF scale** (Method 1) for pattern analysis within each timeframe

- Use **Manual scale** (Method 3) for consistent day-to-day comparison

5. **Watch for Volume Clusters:** High volume appearing simultaneously across multiple HTFs signals significant market events

6. **Confirm Breakouts:** Always check if volume supports the price movement across higher timeframes

7. **Extended Hours:** Keep "Fix gaps" enabled for 24/7 markets (Forex, Crypto) and weekend analysis

## Technical Notes

- **Timezone:** All calculations use America/New_York timezone for consistency

- **Real-time Updates:** Volume and timers update on each tick during market hours

- **Performance:** Optimized with max_bars_back=5000 for extensive historical analysis

- **Compatibility:** Works on all instruments with volume data (Stocks, Forex, Crypto, Futures)

- **Gap Handling:** Uses `barmerge.gaps_off` to fill data gaps during non-trading periods

- **Backtesting:** Uses `lookahead=barmerge.lookahead_on` for stable historical data without repainting

- **Data Continuity:** Automatically handles market closures, weekends, and extended hours

## Updates & Improvements

**Version 2.0 (Current):**

- ✅ Fixed alignment issues during extended hours and weekends

- ✅ Eliminated repainting in backtesting

- ✅ Added gap-filling technology for continuous display

- ✅ Improved data synchronization across all timeframes

- ✅ Enhanced NA value handling for data integrity

- ✅ Added advanced settings group for user control

## Support

For questions, suggestions, or feedback, please comment on the publication or message the author.

---

**Disclaimer:** This indicator is for educational and informational purposes only. It does not constitute financial advice. Past performance is not indicative of future results. Always perform your own analysis and implement proper risk management before making trading decisions.

RSI Donchian Channel [DCAUT]█ RSI Donchian Channel

📊 ORIGINALITY & INNOVATION

The RSI Donchian Channel represents an important synthesis of two complementary analytical frameworks: momentum oscillators and breakout detection systems. This indicator addresses a common limitation in traditional RSI analysis by replacing fixed overbought/oversold thresholds with adaptive zones derived from historical RSI extremes.

Key Enhancement:

Traditional RSI analysis relies on static threshold levels (typically 30/70), which may not adequately reflect changing market volatility regimes. This indicator adapts the reference zones dynamically based on the actual RSI behavior over the lookback period, helping traders identify meaningful momentum extremes relative to recent price action rather than arbitrary fixed levels.

The implementation combines the proven momentum measurement capabilities of RSI with Donchian Channel's breakout detection methodology, creating a framework that identifies both momentum exhaustion points and potential continuation signals through the same analytical lens.

📐 MATHEMATICAL FOUNDATION

Core Calculation Process:

Step 1: RSI Calculation

The Relative Strength Index measures momentum by comparing the magnitude of recent gains to recent losses:

Calculate price changes between consecutive periods

Separate positive changes (gains) from negative changes (losses)

Apply selected smoothing method (RMA standard, also supports SMA, EMA, WMA) to both gain and loss series

Compute Relative Strength (RS) as the ratio of smoothed gains to smoothed losses

Transform RS into bounded 0-100 scale using the formula: RSI = 100 - (100 / (1 + RS))

Step 2: Donchian Channel Application

The Donchian Channel identifies the highest and lowest RSI values within the specified lookback period:

Upper Channel: Highest RSI value over the lookback period, represents the recent momentum peak

Lower Channel: Lowest RSI value over the lookback period, represents the recent momentum trough

Middle Channel (Basis): Average of upper and lower channels, serves as equilibrium reference

Channel Width Dynamics:

The distance between upper and lower channels reflects RSI volatility. Wide channels indicate high momentum variability, while narrow channels suggest momentum consolidation and potential breakout preparation. The indicator monitors channel width over a 100-period window to identify squeeze conditions that often precede significant momentum shifts.

📊 COMPREHENSIVE SIGNAL ANALYSIS

Primary Signal Categories:

Breakout Signals:

Upper Breakout: RSI crosses above the upper channel, indicates momentum reaching new relative highs and potential trend continuation, particularly significant when accompanied by price confirmation

Lower Breakout: RSI crosses below the lower channel, suggests momentum reaching new relative lows and potential trend exhaustion or reversal setup

Breakout strength is enhanced when the channel is narrow prior to the breakout, indicating a transition from consolidation to directional movement

Mean Reversion Signals:

Upper Touch Without Breakout: RSI reaches the upper channel but fails to break through, may indicate momentum exhaustion and potential reversal opportunity

Lower Touch Without Breakout: RSI reaches the lower channel without breakdown, suggests potential bounce as momentum reaches oversold extremes

Return to Basis: RSI moving back toward the middle channel after touching extremes signals momentum normalization

Trend Strength Assessment:

Sustained Upper Channel Riding: RSI consistently remains near or above the upper channel during strong uptrends, indicates persistent bullish momentum

Sustained Lower Channel Riding: RSI stays near or below the lower channel during strong downtrends, reflects persistent bearish pressure

Basis Line Position: RSI position relative to the middle channel helps identify the prevailing momentum bias

Channel Compression Patterns:

Squeeze Detection: Channel width narrowing to 100-period lows indicates momentum consolidation, often precedes significant directional moves

Expansion Phase: Channel widening after a squeeze confirms the initiation of a new momentum regime

Persistent Narrow Channels: Extended periods of tight channels suggest market indecision and accumulation/distribution phases

🎯 STRATEGIC APPLICATIONS

Trend Continuation Strategy:

This approach focuses on identifying and trading momentum breakouts that confirm established trends:

Identify the prevailing price trend using higher timeframe analysis or trend-following indicators

Wait for RSI to break above the upper channel in uptrends (or below the lower channel in downtrends)

Enter positions in the direction of the breakout when price action confirms the momentum shift

Place protective stops below the recent swing low (long positions) or above swing high (short positions)

Target profit levels based on prior swing extremes or use trailing stops to capture extended moves

Exit when RSI crosses back through the basis line in the opposite direction

Mean Reversion Strategy:

This method capitalizes on momentum extremes and subsequent corrections toward equilibrium:

Monitor for RSI reaching the upper or lower channel boundaries

Look for rejection signals (price reversal patterns, volume divergence) when RSI touches the channels

Enter counter-trend positions when RSI begins moving back toward the basis line

Use the basis line as the initial profit target for mean reversion trades

Implement tight stops beyond the channel extremes to limit risk on failed reversals

Scale out of positions as RSI approaches the basis line and closes the position when RSI crosses the basis

Breakout Preparation Strategy:

This approach positions traders ahead of potential volatility expansion from consolidation phases:

Identify squeeze conditions when channel width reaches 100-period lows

Monitor price action for consolidation patterns (triangles, rectangles, flags) during the squeeze

Prepare conditional orders for breakouts in both directions from the consolidation

Enter positions when RSI breaks out of the narrow channel with expanding width

Use the channel width expansion as a confirmation signal for the breakout's validity

Manage risk with stops just inside the opposite channel boundary

Multi-Timeframe Confluence Strategy:

Combining RSI Donchian Channel analysis across multiple timeframes can improve signal reliability:

Identify the primary trend direction using a higher timeframe RSI Donchian Channel (e.g., daily or weekly)

Use a lower timeframe (e.g., 4-hour or hourly) to time precise entry points

Enter long positions when both timeframes show RSI above their respective basis lines

Enter short positions when both timeframes show RSI below their respective basis lines

Avoid trades when timeframes provide conflicting signals (e.g., higher timeframe below basis, lower timeframe above)

Exit when the higher timeframe RSI crosses its basis line in the opposite direction

Risk Management Guidelines:

Effective risk management is essential for all RSI Donchian Channel strategies:

Position Sizing: Calculate position sizes based on the distance between entry point and stop loss, limiting risk to 1-2% of capital per trade

Stop Loss Placement: For breakout trades, place stops just inside the opposite channel boundary; for mean reversion trades, use stops beyond the channel extremes

Profit Targets: Use the basis line as a minimum target for mean reversion trades; for trend trades, target prior swing extremes or use trailing stops

Channel Width Context: Increase position sizes during narrow channels (lower volatility) and reduce sizes during wide channels (higher volatility)

Correlation Awareness: Monitor correlations between traded instruments to avoid over-concentration in similar setups

📋 DETAILED PARAMETER CONFIGURATION

RSI Source:

Defines the price data series used for RSI calculation:

Close (Default): Standard choice providing end-of-period momentum assessment, suitable for most trading styles and timeframes

High-Low Average (HL2): Reduces the impact of closing auction dynamics, useful for markets with significant end-of-day volatility

High-Low-Close Average (HLC3): Provides a more balanced view incorporating the entire period's range

Open-High-Low-Close Average (OHLC4): Offers the most comprehensive price representation, helpful for identifying overall period sentiment

Strategy Consideration: Use Close for end-of-period signals, HL2 or HLC3 for intraday volatility reduction, OHLC4 for capturing full period dynamics

RSI Length:

Controls the number of periods used for RSI calculation:

Short Periods (5-9): Highly responsive to recent price changes, produces more frequent signals with increased false signal risk, suitable for short-term trading and volatile markets

Standard Period (14): Widely accepted default balancing responsiveness with stability, appropriate for swing trading and intermediate-term analysis

Long Periods (21-28): Produces smoother RSI with fewer signals but more reliable trend identification, better for position trading and reducing noise in choppy markets

Optimization Approach: Test different lengths against historical data for your specific market and timeframe, consider using longer periods in ranging markets and shorter periods in trending markets

RSI MA Type:

Determines the smoothing method applied to price changes in RSI calculation:

RMA (Relative Moving Average - Default): Wilder's original smoothing method providing stable momentum measurement with gradual response to changes, maintains consistency with classical RSI interpretation

SMA (Simple Moving Average): Treats all periods equally, responds more quickly to changes than RMA but may produce more whipsaws in volatile conditions

EMA (Exponential Moving Average): Weights recent periods more heavily, increases responsiveness at the cost of potential noise, suitable for traders prioritizing early signal generation

WMA (Weighted Moving Average): Applies linear weighting favoring recent data, offers a middle ground between SMA and EMA responsiveness

Selection Guidance: Maintain RMA for consistency with traditional RSI analysis, use EMA or WMA for more responsive signals in fast-moving markets, apply SMA for maximum simplicity and transparency

DC Length:

Specifies the lookback period for Donchian Channel calculation on RSI values:

Short Periods (10-14): Creates tight channels that adapt quickly to changing momentum conditions, generates more frequent trading signals but increases sensitivity to short-term RSI fluctuations

Standard Period (20): Balances channel responsiveness with stability, aligns with traditional Bollinger Bands and moving average periods, suitable for most trading styles

Long Periods (30-50): Produces wider, more stable channels that better represent sustained momentum extremes, reduces signal frequency while improving reliability, appropriate for position traders and higher timeframes

Calibration Strategy: Match DC length to your trading timeframe (shorter for day trading, longer for swing trading), test channel width behavior during different market regimes, consider using adaptive periods that adjust to volatility conditions

Market Adaptation: Use shorter DC lengths in trending markets to capture momentum shifts earlier, apply longer periods in ranging markets to filter noise and focus on significant extremes

Parameter Combination Recommendations:

Scalping/Day Trading: RSI Length 5-9, DC Length 10-14, EMA or WMA smoothing for maximum responsiveness

Swing Trading: RSI Length 14, DC Length 20, RMA smoothing for balanced analysis (default configuration)

Position Trading: RSI Length 21-28, DC Length 30-50, RMA or SMA smoothing for stable signals

High Volatility Markets: Longer RSI periods (21+) with standard DC length (20) to reduce noise

Low Volatility Markets: Standard RSI length (14) with shorter DC length (10-14) to capture subtle momentum shifts

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Adaptive Threshold Mechanism:

Unlike traditional RSI analysis with fixed 30/70 thresholds, this indicator's Donchian Channel approach provides several improvements:

Context-Aware Extremes: Overbought/oversold levels adjust automatically based on recent momentum behavior rather than arbitrary fixed values

Volatility Adaptation: In low volatility periods, channels narrow to reflect tighter momentum ranges; in high volatility, channels widen appropriately

Market Regime Recognition: The indicator implicitly adapts to different market conditions without manual threshold adjustments

False Signal Reduction: Adaptive channels help reduce premature reversal signals that often occur with fixed thresholds during strong trends

Signal Quality Characteristics:

The indicator's dual-purpose design provides distinct advantages for different trading objectives:

Breakout Trading: Channel boundaries offer clear, objective breakout levels that update dynamically, eliminating the ambiguity of when momentum becomes "too high" or "too low"

Mean Reversion: The basis line provides a natural profit target for reversion trades, representing the midpoint of recent momentum extremes

Trend Strength: Persistent channel boundary riding offers an objective measure of trend strength without additional indicators

Consolidation Detection: Channel width analysis provides early warning of potential volatility expansion from compression phases

Comparative Analysis:

When compared to traditional RSI implementations and other momentum frameworks:

vs. Fixed Threshold RSI: Provides market-adaptive reference levels rather than static values, helping to reduce false signals during trending markets where RSI can remain "overbought" or "oversold" for extended periods

vs. RSI Bollinger Bands: Offers clearer breakout signals and more intuitive extreme identification through actual high/low boundaries rather than statistical standard deviations

vs. Stochastic Oscillator: Maintains RSI's momentum measurement advantages (unbounded calculation avoiding scale compression) while adding the breakout detection capabilities of Donchian Channels

vs. Standard Donchian Channels: Applies breakout methodology to momentum space rather than price, providing earlier signals of potential trend changes before price breakouts occur

Performance Characteristics:

The indicator exhibits specific behavioral patterns across different market conditions:

Trending Markets: Excels at identifying momentum continuation through channel breakouts, RSI tends to ride one channel boundary during strong trends, providing trend confirmation

Ranging Markets: Channel width narrows during consolidation, offering early preparation signals for potential breakout trading opportunities

High Volatility: Channels widen to reflect increased momentum variability, automatically adjusting signal sensitivity to match market conditions

Low Volatility: Channels contract, making the indicator more sensitive to subtle momentum shifts that may be significant in calm market environments

Transition Periods: Channel squeezes often precede major trend changes, offering advance warning of potential regime shifts

Limitations and Considerations:

Users should be aware of certain operational characteristics:

Lookback Dependency: Channel boundaries depend entirely on the lookback period, meaning the indicator has no predictive element beyond identifying current momentum relative to recent history

Lag Characteristics: As with all moving average-based indicators, RSI calculation introduces lag, and channel boundaries update only as new extremes occur within the lookback window

Range-Bound Sensitivity: In extremely tight ranges, channels may become very narrow, potentially generating excessive signals from minor momentum fluctuations

Trending Persistence: During very strong trends, RSI may remain at channel extremes for extended periods, requiring patience for mean reversion setups or commitment to trend-following approaches

No Absolute Levels: Unlike traditional RSI, this indicator provides no fixed reference points (like 50), making it less suitable for strategies that depend on absolute momentum readings

USAGE NOTES

This indicator is designed for technical analysis and educational purposes to help traders understand momentum dynamics and identify potential trading opportunities. The RSI Donchian Channel has limitations and should not be used as the sole basis for trading decisions.

Important considerations:

Performance varies significantly across different market conditions, timeframes, and instruments

Historical signal patterns do not guarantee future results, as market behavior continuously evolves

Effective use requires understanding of both RSI momentum principles and Donchian Channel breakout concepts

Risk management practices (stop losses, position sizing, diversification) are essential for any trading application

Consider combining with additional analytical tools such as volume analysis, price action patterns, or trend indicators for confirmation

Backtest thoroughly on your specific instruments and timeframes before live trading implementation

Be aware that optimization on historical data may lead to curve-fitting and poor forward performance

The indicator performs best when used as part of a comprehensive trading methodology that incorporates multiple forms of market analysis, sound risk management, and realistic expectations about win rates and drawdowns.

Extreme Pressure Zones Indicator (EPZ) [BullByte]Extreme Pressure Zones Indicator(EPZ)

The Extreme Pressure Zones (EPZ) Indicator is a proprietary market analysis tool designed to highlight potential overbought and oversold "pressure zones" in any financial chart. It does this by combining several unique measurements of price action and volume into a single, bounded oscillator (0–100). Unlike simple momentum or volatility indicators, EPZ captures multiple facets of market pressure: price rejection, trend momentum, supply/demand imbalance, and institutional (smart money) flow. This is not a random mashup of generic indicators; each component was chosen and weighted to reveal extreme market conditions that often precede reversals or strong continuations.

What it is?

EPZ estimates buying/selling pressure and highlights potential extreme zones with a single, bounded 0–100 oscillator built from four normalized components. Context-aware weighting adapts to volatility, trendiness, and relative volume. Visual tools include adaptive thresholds, confirmed-on-close extremes, divergence, an MTF dashboard, and optional gradient candles.

Purpose and originality (not a mashup)

Purpose: Identify when pressure is building or reaching potential extremes while filtering noise across regimes and symbols.

Originality: EPZ integrates price rejection, momentum cascade, pressure distribution, and smart money flow into one bounded scale with context-aware weighting. It is not a cosmetic mashup of public indicators.

Why a trader might use EPZ

EPZ provides a multi-dimensional gauge of market extremes that standalone indicators may miss. Traders might use it to:

Spot Reversals: When EPZ enters an "Extreme High" zone (high red), it implies selling pressure might soon dominate. This can hint at a topside reversal or at least a pause in rallies. Conversely, "Extreme Low" (green) can highlight bottom-fish opportunities. The indicator's divergence module (optional) also finds hidden bullish/bearish divergences between price and EPZ, a clue that price momentum is weakening.

Measure Momentum Shifts: Because EPZ blends momentum and volume, it reacts faster than many single metrics. A rising MPO indicates building bullish pressure, while a falling MPO shows increasing bearish pressure. Traders can use this like a refined RSI: above 50 means bullish bias, below 50 means bearish bias, but with context provided by the thresholds.

Filter Trades: In trend-following systems, one could require EPZ to be in the bullish (green) zone before taking longs, or avoid new trades when EPZ is extreme. In mean-reversion systems, one might specifically look to fade extremes flagged by EPZ.

Multi-Timeframe Confirmation: The dashboard can fetch a higher timeframe EPZ value. For example, you might trade a 15-minute chart only when the 60-minute EPZ agrees on pressure direction.

Components and how they're combined

Rejection (PRV) – Captures price rejection based on candle wicks and volume (see Price Rejection Volume).

Momentum Cascade (MCD) – Blends multiple momentum periods (3,5,8,13) into a normalized momentum score.

Pressure Distribution (PDI) – Measures net buy/sell pressure by comparing volume on up vs down candles.

Smart Money Flow (SMF) – An adaptation of money flow index that emphasizes unusual volume spikes.

Each of these components produces a 0–100 value (higher means more bullish pressure). They are then weighted and averaged into the final Market Pressure Oscillator (MPO), which is smoothed and scaled. By combining these four views, EPZ stands out as a comprehensive pressure gauge – the whole is greater than the sum of parts

Context-aware weighting:

Higher volatility → more PRV weight

Trendiness up (RSI of ATR > 25) → more MCD weight

Relative volume > 1.2x → more PDI weight

SMF holds a stable weight

The weighted average is smoothed and scaled into MPO ∈ with 50 as the neutral midline.

What makes EPZ stand out

Four orthogonal inputs (price action, momentum, pressure, flow) unified in a single bounded oscillator with consistent thresholds.

Adaptive thresholds (optional) plus robust extreme detection that also triggers on crossovers, so static thresholds work reliably too.

Confirm Extremes on Bar Close (default ON): dots/arrows/labels/alerts print on closed bars to avoid repaint confusion.

Clean dashboard, divergence tools, pre-alerts, and optional on-price gradients. Visual 3D layering uses offsets for depth only,no lookahead.

Recommended markets and timeframes

Best: liquid symbols (index futures, large-cap equities, major FX, BTC/ETH).

Timeframes: 5–15m (more signals; consider higher thresholds), 1H–4H (balanced), 1D (clear regimes).

Use caution on illiquid or very low TFs where wick/volume geometry is erratic.

Logic and thresholds

MPO ∈ ; 50 = neutral. Above 50 = bullish pressure; below 50 = bearish.

Static thresholds (defaults): thrHigh = 70, thrLow = 30; warning bands 5 pts inside extremes (65/35).

Adaptive thresholds (optional):

thrHigh = min(BaseHigh + 5, mean(MPO,100) + stdev(MPO,100) × ExtremeSensitivity)

thrLow = max(BaseLow − 5, mean(MPO,100) − stdev(MPO,100) × ExtremeSensitivity)

Extreme detection

High: MPO ≥ thrHigh with peak/slope or crossover filter.

Low: MPO ≤ thrLow with trough/slope or crossover filter.

Cooldown: 5 bars (default). A new extreme will not print until the cooldown elapses, even if MPO re-enters the zone.

Confirmation

"Confirm Extremes on Bar Close" (default ON) gates extreme markers, pre-alerts, and alerts to closed bars (non-repainting).

Divergences

Pivot-based bullish/bearish divergence; tags appear only after left/right bars elapse (lookbackPivot).

MTF

HTF MPO retrieved with lookahead_off; values can update intrabar and finalize at HTF close. This is disclosed and expected.

Inputs and defaults (key ones)

Core: Sensitivity=1.0; Analysis Period=14; Smoothing=3; Adaptive Thresholds=OFF.

Extremes: Base High=70, Base Low=30; Extreme Sensitivity=1.5; Confirm Extremes on Bar Close=ON; Cooldown=5; Dot size Small/Tiny.

Visuals: Heatmap ON; 3D depth optional; Strength bars ON; Pre-alerts OFF; Divergences ON with tags ON; Gradient candles OFF; Glow ON.

Dashboard: ON; Position=Top Right; Size=Normal; MTF ON; HTF=60m; compact overlay table on price chart.

Advanced caps: Max Oscillator Labels=80; Max Extreme Guide Lines=80; Divergence objects=60.

Dashboard: what each element means

Header: EPZ ANALYSIS.

Large readout: Current MPO; color reflects state (extreme, approaching, or neutral).

Status badge: "Extreme High/Low", "Approaching High/Low", "Bullish/Neutral/Bearish".

HTF cell (when MTF ON): Higher-timeframe MPO, color-coded vs extremes; updates intrabar, settles at HTF close.

Predicted (when MTF OFF): Simple MPO extrapolation using momentum/acceleration—illustrative only.

Thresholds: Current thrHigh/thrLow (static or adaptive).

Components: ASCII bars + values for PRV, MCD, PDI, SMF.

Market metrics: Volume Ratio (x) and ATR% of price.

Strength: Bar indicator of |MPO − 50| × 2.

Confidence: Heuristic gauge (100 in extremes, 70 in warnings, 50 with divergence, else |MPO − 50|). Convenience only, not probability.

How to read the oscillator

MPO Value (0–100): A reading of 50 is neutral. Values above ~55 are increasingly bullish (green), while below ~45 are increasingly bearish (red). Think of these as "market pressure".

Extreme Zones: When MPO climbs into the bright orange/red area (above the base-high line, default 70), the chart will display a dot and downward arrow marking that extreme. Traders often treat this as a sign to tighten stops or look for shorts. Similarly, a bright green dot/up-arrow appears when MPO falls below the base-low (30), hinting at a bullish setup.

Heatmap/Candles: If "Pressure Heatmap" is enabled, the background of the oscillator pane will fade green or red depending on MPO. Users can optionally color the price candles by MPO value (gradient candles) to see these extremes on the main chart.

Prediction Zone(optional): A dashed projection line extends the MPO forward by a small number of bars (prediction_bars) using current MPO momentum and acceleration. This is a heuristic extrapolation best used for short horizons (1–5 bars) to anticipate whether MPO may touch a warning or extreme zone. It is provisional and becomes less reliable with longer projection lengths — always confirm predicted moves with bar-close MPO and HTF context before acting.

Divergences: When price makes a higher high but EPZ makes a lower high (bearish divergence), the indicator can draw dotted lines and a "Bear Div" tag. The opposite (lower low price, higher EPZ) gives "Bull Div". These signals confirm waning momentum at extremes.

Zones: Warning bands near extremes; Extreme zones beyond thresholds.

Crossovers: MPO rising through 35 suggests easing downside pressure; falling through 65 suggests waning upside pressure.

Dots/arrows: Extreme markers appear on closed bars when confirmation is ON and respect the 5-bar cooldown.

Pre-alert dots (optional): Proximity cues in warning zones; also gated to bar close when confirmation is ON.

Histogram: Distance from neutral (50); highlights strengthening or weakening pressure.

Divergence tags: "Bear Div" = higher price high with lower MPO high; "Bull Div" = lower price low with higher MPO low.

Pressure Heatmap : Layered gradient background that visually highlights pressure strength across the MPO scale; adjustable intensity and optional zone overlays (warning / extreme) for quick visual scanning.

A typical reading: If the oscillator is rising from neutral towards the high zone (green→orange→red), the chart may see strong buying culminating in a stall. If it then turns down from the extreme, that peak EPZ dot signals sell pressure.

Alerts

EPZ: Extreme Context — fires on confirmed extremes (respects cooldown).

EPZ: Approaching Threshold — fires in warning zones if no extreme.

EPZ: Divergence — fires on confirmed pivot divergences.

Tip: Set alerts to "Once per bar close" to align with confirmation and avoid intrabar repaint.

Practical usage ideas

Trend continuation: In positive regimes (MPO > 50 and rising), pullbacks holding above 50 often precede continuation; mirror for bearish regimes.

Exhaustion caution: E High/E Low can mark exhaustion risk; many wait for MPO rollover or divergence to time fades or partial exits.

Adaptive thresholds: Useful on assets with shifting volatility regimes to maintain meaningful "extreme" levels.

MTF alignment: Prefer setups that agree with the HTF MPO to reduce countertrend noise.

Examples

Screenshots captured in TradingView Replay to freeze the bar at close so values don't fluctuate intrabar. These examples use default settings and are reproducible on the same bars; they are for illustration, not cherry-picking or performance claims.

Example 1 — BTCUSDT, 1h — E Low

MPO closed at 26.6 (below the 30 extreme), printing a confirmed E Low. HTF MPO is 26.6, so higher-timeframe pressure remains bearish. Components are subdued (Momentum/Pressure/Smart$ ≈ 29–37), with Vol Ratio ≈ 1.19x and ATR% ≈ 0.37%. A prior Bear Div flagged weakening impulse into the drop. With cooldown set to 5 bars, new extremes are rate-limited. Many traders wait for MPO to curl up and reclaim 35 or for a fresh Bull Div before considering countertrend ideas; if MPO cannot reclaim 35 and HTF stays weak, treat bounces cautiously. Educational illustration only.

Example 2 — ETHUSD, 30m — E High

A strong impulse pushed MPO into the extreme zone (≥ 70), printing a confirmed E High on close. Shortly after, MPO cooled to ~61.5 while a Bear Div appeared, showing momentum lag as price pushed a higher high. Volume and volatility were elevated (≈ 1.79x / 1.25%). With a 5-bar cooldown, additional extremes won't print immediately. Some treat E High as exhaustion risk—either waiting for MPO rollover under 65/50 to fade, or for a pullback that holds above 50 to re-join the trend if higher-timeframe pressure remains constructive. Educational illustration only.

Known limitations and caveats

The MPO line itself can change intrabar; extreme markers/alerts do not repaint when "Confirm Extremes on Bar Close" is ON.

HTF values settle at the close of the HTF bar.

Illiquid symbols or very low TFs can be noisy; consider higher thresholds or longer smoothing.

Prediction line (when enabled) is a visual extrapolation only.

For coders

Pine v6. MTF via request.security with lookahead_off.

Extremes include crossover triggers so static thresholds also yield E High/E Low.

Extreme markers and pre-alerts are gated by barstate.isconfirmed when confirmation is ON.

Arrays prune oldest objects to respect resource limits; defaults (80/80/60) are conservative for low TFs.

3D layering uses negative offsets purely for drawing depth (no lookahead).

Screenshot methodology:

To make labels legible and to demonstrate non-repainting behavior, the examples were captured in TradingView Replay with "Confirm Extremes on Bar Close" enabled. Replay is used only to freeze the bar at close so plots don't change intrabar. The examples use default settings, include both Extreme Low and Extreme High cases, and can be reproduced by scrolling to the same bars outside Replay. This is an educational illustration, not a performance claim.

Disclaimer

This script is for educational purposes only and does not constitute financial advice. Markets involve risk; past behavior does not guarantee future results. You are responsible for your own testing, risk management, and decisions.

Dr.Yazdani V063 Session OR + A-Lines

**ACD Indicator: Mark Fisher's Opening Range Breakout Strategy**

**Overview**

The ACD system, developed by legendary trader Mark Fisher in his book *The Logical Trader*, is a powerful methodology for identifying high-probability trade setups based on the market's opening range (OR). This indicator automates Layers 1 and 2 of the ACD strategy, helping you spot breakout opportunities, trend direction, and key support/resistance levels. Perfect for day traders, scalpers, and swing traders in forex, stocks, futures, or crypto.

**How It Works**

1. **Opening Range (OR)**: Calculated from the high/low of the first X minutes (default: 30-60 min) of major sessions (e.g., Tokyo, London, New York).

2. **A Levels**: Drawn at a percentage (default: 0.5% of OR range or ATR-based) above/below the OR. A breakout above A-Up signals a bullish setup; below A-Down signals bearish.

3. **C Levels**: Wider levels (default: 1-2% or ATR multiplier) for stronger confirmation. Breakouts here confirm trend strength and filter fakeouts.

4. **Pivot Ranges**: Includes daily and N-day pivots to gauge overall market bias (above pivots = bullish; below = bearish).

**Key Features**

- **Customizable Sessions**: Tokyo (00:00-01:00 GMT), London (08:00-09:00 GMT), New York (13:30-14:30 GMT) – adjustable.

- **ATR Integration**: Uses Average True Range for dynamic A/C levels (period: 14 by default).

- **Visual Alerts**: Color-coded lines (green for bullish, red for bearish) + optional labels for breakouts.

- **Pivot Display**: Show/hide daily or multi-day pivots with customizable colors.

- **Risk Management**: Built-in stop-loss suggestions based on OR width.

**Trading Rules**

- **Bullish Setup**: Price breaks and holds above A-Up → Enter long at C-Up confirmation. Target: Next pivot or 1:2 risk-reward.

- **Bearish Setup**: Price breaks below A-Down → Enter short at C-Down.

- **Avoid Fakeouts**: Wait for stabilization (e.g., close above/below level).

- **Trend Filter**: Combine with PMA (Pivot Moving Average) for Layer 3 confirmation (search "ACD PMA" in TradingView).

**Settings Guide**

- **OR Timeframe**: Session start time and duration (e.g., 30 min).

- **A Multiplier (%)**: Distance for A levels (default: 0.5).

- **C Multiplier (%)**: Distance for C levels (default: 1.0).

- **ATR Period**: For volatility-based levels (default: 14).

- **Show Pivots**: Toggle daily/N-day ranges.

This indicator balances supply/demand by analyzing volume and price action within the opening range. Backtest on your favorite pairs (e.g., EURUSD, BTCUSD) and adjust for your style. Not financial advice – always use proper risk management!

**Inspired by**: Mark Fisher's ACD Methodology. Open-source for community review. Questions? Comment below!

#ACD #OpeningRange #Breakout #DayTrading #FisherStrategy

Tape Speed Pulse (Pace + Direction) [v6 + Climax]Tape Speed Pulse (Pace + Direction)

One-liner:

A lightweight “tape pulse” that turns intraday bursts of buying/selling into an easy-to-read histogram, with surge, slowdown, and climax (exhaustion) markers for fast decision-making. Use on sec and min charts.

What it measures

Pace (RVOL): current bar volume vs the recent average (smoothed).

Direction proxy: uptick/downtick by comparing close to close .

Pulse (histogram): direction × pace, so you see who’s pushing and how fast.

Colors

- Lime = Buy surge (pace ≥ threshold & upticking)

- Red = Sell surge (pace ≥ threshold & downticking)

- Teal = Buy pressure, sub-threshold

- Orange = Sell pressure, sub-threshold

- Faded/gray = Near-neutral pace (below the Neutral Band)

Lines (toggleable)

-White = Pace (RVOL)

- Yellow = Slowdown line = a drop of X% from the last 30-bar peak pace

Background tint mirrors the current state so you can glance risk: greenish for buy pressure, reddish for sell pressure.

Signals & alerts

- BUY surge – fires when pace crosses above the surge threshold with uptick direction (optional acceleration & uptick streak filters; cooldown prevents spam).

- SELL surge – mirror logic to downside.

- Slowdown – fires when pace crosses below the yellow slowdown line while direction ≤ 0 (early fade warning).

Climax (exhaustion)

- Buy Climax: previous bar was a buy surge with a large upper wick; current bar slows (below slowdown line) and direction ≤ 0.

- Sell Climax: mirror (large lower wick → slowdown → direction ≥ 0).

- Great for trimming/tight stops or fade setups at obvious spikes.

- Create alerts via Add alert → Condition: this indicator → choose the specific alert (BUY surge, SELL surge, Slowdown, Buy Climax, Sell Climax).

How to use it (playbook)

- Longs (e.g., VWAP reclaim / micro pullback)

- Only take entries when the pulse is teal→lime (buy pressure to buy surge).

- Into prior highs/VWAP bands, take partials on lime spikes.

- If you get a Slowdown dot and bars turn orange/red, tighten or exit.

Shorts (failed reclaim / lower-high)

- Look for teal→orange→red with rising pace at a level.

- Add confidence if a Buy Climax printed right before (exhaustion).

- Risk above the spike; don’t fight true ignitions out of bases.

Simple guardrails

- Avoid new longs when the histogram is orange/red; avoid new shorts when teal/lime.

- Use with VWAP + 9/20 EMA or your levels. The pulse is confirmation, not the whole thesis.

Inputs (what they do & when to tweak)

- Pace lookback (bars) – window for average volume. Lower = faster; higher = steadier.

Too jumpy? raise it. Missing quick bursts? lower it.

- Smoothing EMA (bars) – smooths pace. Higher = calmer.

Use 4–6 during the open; 3–4 midday.

- Surge threshold (× RVOL) – how fast counts as a surge.

Too many surges? raise it. Too late? lower it slightly.

- Slowdown drop from 30-bar max (%) – how far below the recent peak pace to call a slowdown.

Higher % = later slowdown; lower % = earlier warning.

- Neutral band (× RVOL) – paces below this fade to gray.

Raise to clean up noise; lower to see subtle pressure.

- Min seconds between signals – cooldown to prevent spam.

Increase in chop; reduce if you want more pings.

- BUY/SELL: min consecutive upticks/downticks – tiny streak filter.

Raise to avoid wiggles; lower for earlier signals.

Require pace accelerating into signal – ON = avoid stall breakouts; OFF = earlier pings.

Climax options: wick % threshold & “require slowdown cross”.

Raise wick% / require cross to be stricter; lower to catch more fades.

Quick presets

- Low-float runner, 5–10s chart

- Lookback 20, Smoothing 3–4, Surge 2.2–2.8, Slowdown 35–45, Neutral 1.0–1.2, Cooldown 15–25s, Streaks 2–3, Accel ON.

- Thick large-cap, 1-min

- Lookback 20–30, Smoothing 5–7, Surge 1.5–1.9, Slowdown 25–35, Neutral 0.8–1.0, Cooldown 30–60s, Streaks 2, Accel ON.

- Open vs Midday vs Power Hour

- Open: higher Surge, more Smoothing, longer Cooldown.

- Midday: lower Surge, less Smoothing to catch subtler pushes.

- Power hour: moderate Surge; keep Slowdown on for exits.

Reading common patterns

- Ignition (likely continuation): lime spike out of a base that holds above a level while pace stays above yellow.

- Exhaustion (likely fade): lime spike late in a run with upper wick → Slowdown → orange/red. The Buy Climax diamond is your tell.

Limits / notes

This is an OHLCV-based proxy (TradingView Pine can’t read raw tape/DOM). It won’t match Bookmap/Jigsaw tick-for-tick, but it’s fast and objective.

Use with levels and a risk plan. Past performance ≠ future results. Educational only.

Weinstein Stage Analyzer — Table Only (more padding)What it does

This indicator applies Stan Weinstein’s Stage Analysis (Stages 1–4) and presents the result in a clean, compact table only—no lines, labels, or overlays. It shows:

• Previous Stage

• Current Stage (with Early / Mature / Late tag)

• Duration (how long price has been in the current stage, in HTF bars)

• Sentiment (Bullish / Bearish / Balanced / Cautious, derived from stage & maturity)

Timeframe-aware logic

• Weekly charts: classic 30-period MA (Weinstein’s original 30-week concept).

• Daily & Intraday: computed on Daily 150 as a practical daily translation of the 30-week idea.

• Monthly: ~7-period MA (~30 weeks ≈ 7 months).

The stage classification itself is evaluated on this HTF context and then displayed on your active chart.

EMA/SMA toggle

Choose EMA (default) or SMA for the trend line used in stage detection.

How stages are decided (practical rules)

• Stage 2 (Advance): MA rising with price above an upper band.

• Stage 4 (Decline): MA falling with price below a lower band.

• Flat MA zones become Stage 1 (Base) or Stage 3 (Top) depending on the prior trend.

“Maturity” tags (Early/Mature/Late) come from run length and extension beyond the band.

Inputs you can tweak

• MA Type: EMA / SMA

• Price Band (±%) and Slope Threshold to tighten/loosen stage flips

• Maturity thresholds: min/max bars & late-extension %

Notes

• Duration is for the entire current stage (e.g., total time in Stage 4), not just the maturity slice.

• A Top Padding Rows input is included to nudge the table lower if it overlaps your OHLC readout.

Disclaimer

For educational use only. Not financial advice. Always confirm with your own analysis, risk management, and market context.

Premarket Hi/Lo + Prior Day O/C LevelsPremarket Hi/Lo + Prior Day O/C (today only) shows four clear reference levels for the current regular trading session: the Premarket High and Premarket Low (taken from a user-defined premarket window, 04:00–09:30 by default) and Yesterday’s 09:30 Open and 15:59 Close (sourced from the 1-minute feed for accuracy). The premarket levels “lock” at the opening bell so they don’t move for the rest of the day. All four lines are displayed only during today’s regular hours to keep the chart focused. Small right-edge labels and an optional top-right mini-table show the exact values at a glance.

This indicator is designed to give immediate context without technical jargon. The premarket high/low summarize where price traveled before the bell; the prior-day open/close summarize where the last session began and ended. Checking whether price is above or below these markers helps you quickly judge strength or weakness and anticipate where price may pause, bounce, or break. Typical uses include watching for a clean break and hold above Premarket High (often bullish), a break and hold below Premarket Low (often bearish), drift back toward Prior Day Close after a gap (a common “magnet”), and flips around Prior Day Open that can lead to continuation.

Setup: Turn on Extended Hours in TradingView so premarket bars are visible (Chart Settings → Symbol → Extended Hours). Apply the indicator to any intraday timeframe. In Inputs, you can change the premarket window to match your market, adjust colors and line widths, and toggle the floating labels and the mini-table. Times use the chart’s exchange time (for US stocks, Eastern Time).

Notes and limits: Lines show only for today’s session (default 09:30–16:00). The script looks at the previous calendar day for “prior day,” so values may be empty after weekends or holidays when markets were closed. If your instrument uses different regular hours or you trade futures/crypto, adjust the premarket session in Inputs and—if needed—edit the regular-hours window in code to match. If your data source does not include premarket, the premarket lines will be blank.

Best practice: The first 15–30 minutes after the open are where these levels have the most impact. Reactions are more meaningful when a line aligns with another tool you use (e.g., VWAP or your opening range). If price does not react clearly at a line, avoid forcing a trade.

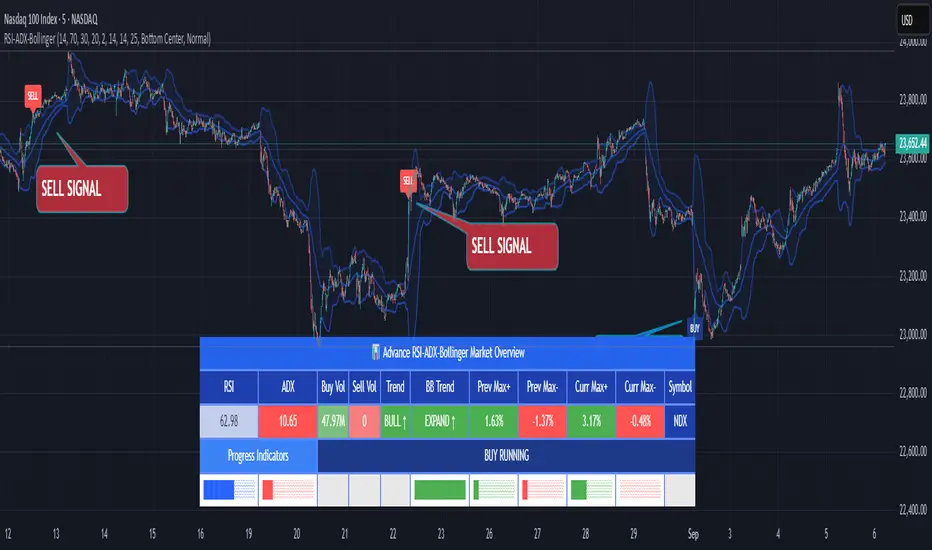

RSI ADX Bollinger Analysis High-level purpose and design philosophy

This indicator — RSI-ADX-Bollinger Analysis — is a compact, educational market-analysis toolkit that blends momentum (RSI), trend strength (ADX), volatility structure (Bollinger Bands) and simple volumetrics to provide traders a snapshot of market condition and trade idea quality. The design philosophy is explicit and layered: use each component to answer a different question about price action (momentum, conviction, volatility, participation), then combine answers to form a more robust, explainable signal. The mashup is intended for analysis and learning, not automatic execution: it surfaces the why behind signals so traders can test, learn and apply rules with risk management.

________________________________________

What each indicator contributes (component-by-component)

RSI (Relative Strength Index) — role and behavior: RSI measures short-term momentum by comparing recent gains to recent losses. A high RSI (near or above the overbought threshold) indicates strong recent buying pressure and potential exhaustion if price is extended. A low RSI (near or below the oversold threshold) indicates strong recent selling pressure and potential exhaustion or a value area for mean-reversion. In this dashboard RSI is used as the primary momentum trigger: it helps identify whether price is locally over-extended on the buy or sell side.

ADX (Average Directional Index) — role and behavior: ADX measures trend strength independently of direction. When ADX rises above a chosen threshold (e.g., 25), it signals that the market is trending with conviction; ADX below the threshold suggests range or weak trend. Because patterns and momentum signals perform differently in trending vs. ranging markets, ADX is used here as a filter: only when ADX indicates sufficient directional strength does the system treat RSI+BB breakouts as meaningful trade candidates.

Bollinger Bands — role and behavior: Bollinger Bands (20-period basis ± N standard deviations) show volatility envelope and relative price position vs. a volatility-adjusted mean. Price outside the upper band suggests pronounced extension relative to recent volatility; price outside the lower band suggests extended weakness. A band expansion (increasing width) signals volatility breakout potential; contraction signals range-bound conditions and potential squeeze. In this dashboard, Bollinger Bands provide the volatility/structural context: RSI extremes plus price beyond the band imply a stronger, volatility-backed move.

Volume split & basic MA trend — role and behavior: Buy-like and sell-like volume (simple heuristic using close>open or closeopen) or sell-like (close1.2 for validation and compare win rate and expectancy.

4. TF alignment: Accept signals only when higher timeframe (e.g., 4h) trend agrees — compare results.

5. Parameter sensitivity: Vary RSI threshold (70/30 vs 80/20), Bollinger stddev (2 vs 2.5), and ADX threshold (25 vs 30) and measure stability of results.

These exercises teach both statistical thinking and the specific failure modes of the mashup.

________________________________________

Limitations, failure modes and caveats (explicit & teachable)

• ADX and Bollinger measures lag during fast-moving news events — signals can be late or wrong during earnings, macro shocks, or illiquid sessions.

• Volume classification by open/close is a heuristic; it does not equal TAPEDATA, footprint or signed volume. Use it as supportive evidence, not definitive proof.

• RSI can remain overbought or oversold for extended stretches in persistent trends — relying solely on RSI extremes without ADX or BB context invites large drawdowns.

• Small-cap or low-liquidity instruments yield noisy band behavior and unreliable volume ratios.

Being explicit about these limitations is a strong point in a TradingView description — it demonstrates transparency and educational intent.

________________________________________

Originality & mashup justification (text you can paste)

This script intentionally combines classical momentum (RSI), volatility envelope (Bollinger Bands) and trend-strength (ADX) because each indicator answers a different and complementary question: RSI answers is price locally extreme?, Bollinger answers is price outside normal volatility?, and ADX answers is the market moving with conviction?. Volume participation then acts as a practical check for real market involvement. This combination is not a simple “indicator mashup”; it is a designed ensemble where each element reduces the others’ failure modes and together produce a teachable, testable signal framework. The script’s purpose is educational and analytical — to show traders how to interpret the interplay of momentum, volatility, and trend strength.

________________________________________

TradingView publication guidance & compliance checklist

To satisfy TradingView rules about mashups and descriptions, include the following items in your script description (without exposing source code):

1. Purpose statement: One or two lines describing the script’s objective (educational multi-indicator market overview and idea filter).

2. Component list: Name the major modules (RSI, Bollinger Bands, ADX, volume heuristic, SMA trend checks, signal tracking) and one-sentence reason for each.

3. How they interact: A succinct non-code explanation: “RSI finds momentum extremes; Bollinger confirms volatility expansion; ADX confirms trend strength; all three must align for a BUY/SELL.”

4. Inputs: List adjustable inputs (RSI length and thresholds, BB length & stddev, ADX threshold & smoothing, volume MA, table position/size).

5. Usage instructions: Short workflow (check TF alignment → confirm participation → define stop & R:R → backtest).

6. Limitations & assumptions: Explicitly state volume is approximated, ADX has lag, and avoid promising guaranteed profits.

7. Non-promotional language: No external contact info, ads, claims of exclusivity or guaranteed outcomes.

8. Trademark clause: If you used trademark symbols, remove or provide registration proof.

9. Risk disclaimer: Add the copy-ready disclaimer below.

This matches TradingView’s request for meaningful descriptions that explain originality and inter-component reasoning.

________________________________________

Copy-ready short publication description (paste into TradingView)

Advanced RSI-ADX-Bollinger Market Overview — educational multi-indicator dashboard. This script combines RSI (momentum extremes), Bollinger Bands (volatility envelope and band expansion), ADX (trend strength), simple SMA trend bias and a basic buy/sell volume heuristic to surface high-quality idea candidates. Signals require alignment of momentum, volatility expansion and rising ADX; volume participation is displayed to support signal confidence. Inputs are configurable (RSI length/levels, BB length/stddev, ADX length/threshold, volume MA, display options). This tool is intended for analysis and learning — not for automated execution. Users should back test and apply robust risk management. Limitations: volume classification here is a heuristic (close>open), ADX and BB measures lag in fast news events, and results vary by instrument liquidity.

________________________________________

Copy-ready risk & misuse disclaimer (paste into description or help file)

This script is provided for educational and analytical purposes only and does not constitute financial or investment advice. It does not guarantee profits. Indicators are heuristics and may give false or late signals; always back test and paper-trade before using real capital. The author is not responsible for trading losses resulting from the use or misuse of this indicator. Use proper position sizing and risk controls.

________________________________________

Risk Disclaimer: This tool is provided for education and analysis only. It is not financial advice and does not guarantee returns. Users assume all risk for trades made based on this script. Back test thoroughly and use proper risk management.

Smart Money Precision Structure [BullByte]Smart Money Precision Structure

Advanced Market Structure Analysis Using Institutional Order Flow Concepts

---

OVERVIEW

Smart Money Precision Structure (SMPS) is a comprehensive market analysis indicator that combines six analytical frameworks to identify high-probability market structure patterns. The indicator uses multi-dimensional scoring algorithms to evaluate market conditions through institutional order flow concepts, providing traders with professional-grade market analysis.

---

PURPOSE AND ORIGINALITY

Why This Indicator Was Developed

• Addresses the gap between retail and institutional analysis methods

• Consolidates multiple analysis techniques that professionals use separately

• Automates complex market structure evaluation into actionable insights

• Eliminates the need for multiple indicators by providing comprehensive analysis

What Makes SMPS Original

• Six-Layer Confluence System - Unique combination of market regime, structure, volume flow, momentum, price action, and adaptive filtering

• Institutional Pattern Recognition - Identifies smart money accumulation and distribution patterns

• Adaptive Intelligence - Parameters automatically adjust based on detected market conditions

• Real-Time Market Scoring - Proprietary algorithm rates market quality from 0-100%

• Structure Break Detection - Advanced pivot analysis identifies trend reversals early

---

HOW IT WORKS - TECHNICAL METHODOLOGY

1. Market Regime Analysis Engine

The indicator evaluates five core market dimensions:

• Volatility Score - Measures current volatility against 50-period historical baseline

• Trend Score - Analyzes alignment between 8, 21, and 50-period EMAs

• Momentum Score - Combines RSI divergence with MACD signal alignment

• Structure Score - Evaluates pivot point formation clarity

• Efficiency Score - Calculates directional movement efficiency ratio

These scores combine to classify markets into five regimes:

• TRENDING - Strong directional movement with aligned indicators

• RANGING - Sideways movement with mixed directional signals

• VOLATILE - Elevated volatility with unpredictable price swings

• QUIET - Low volatility consolidation periods

• TRANSITIONAL - Market shifting between different regimes

2. Market Structure Analysis

Advanced pivot point analysis identifies:

• Higher Highs and Higher Lows for bullish structure

• Lower Highs and Lower Lows for bearish structure

• Structure breaks when established patterns fail

• Dynamic support and resistance from recent pivot points

• Key level proximity detection using ATR-based buffers

3. Volume Flow Decoding

Institutional activity detection through:

• Volume surge identification when volume exceeds 2x average

• Buy versus sell pressure analysis using price-volume correlation

• Flow strength measurement through directional volume consistency

• Divergence detection between volume and price movements

• Institutional threshold alerts when unusual volume patterns emerge

4. Multi-Period Momentum Synthesis

Weighted momentum calculation across four timeframes:

• 1-period momentum weighted at 40%

• 3-period momentum weighted at 30%

• 5-period momentum weighted at 20%

• 8-period momentum weighted at 10%

Result smoothed with 6-period EMA for noise reduction.

5. Price Action Quality Assessment

Each bar evaluated for:

• Range quality relative to 20-period average

• Body-to-range ratio for directional conviction

• Wick analysis for rejection pattern identification

• Pattern recognition including engulfing and hammer formations

• Sequential price movement analysis

6. Adaptive Parameter System

Parameters automatically adjust based on detected regime:

• Trending markets reduce sensitivity and confirmation requirements

• Volatile markets increase filtering and require additional confirmations

• Ranging markets maintain neutral settings

• Transitional markets use moderate adjustments

---

COMPLETE SETTINGS GUIDE

Section 1: Core Analysis Settings

Analysis Sensitivity (0.3-2.0)

• Default: 1.0

• Lower values require stronger price movements

• Higher values detect more subtle patterns

• Scalpers use 0.8-1.2, swing traders use 1.5-2.0

Noise Reduction Level (2-7)

• Default: 4

• Controls filtering of false patterns

• Higher values reduce pattern frequency

• Increase in volatile markets

Minimum Move % (0.05-0.50)

• Default: 0.15%

• Sets minimum price movement threshold

• Adjust based on instrument volatility

• Forex: 0.05-0.10%, Stocks: 0.15-0.25%, Crypto: 0.20-0.50%

High Confirmation Mode

• Default: True (Enabled)

• Requires all technical conditions to align

• Reduces frequency but increases reliability

• Disable for more aggressive pattern detection

Section 2: Market Regime Detection

Enable Regime Analysis

• Default: True (Enabled)

• Activates market environment evaluation

• Essential for adaptive features

• Keep enabled for best results

Regime Analysis Period (20-100)

• Default: 50 bars

• Determines regime calculation lookback

• Shorter for responsive, longer for stable

• Scalping: 20-30, Swing: 75-100

Minimum Market Clarity (0.2-0.8)

• Default: 0.4

• Quality threshold for pattern generation

• Higher values require clearer conditions

• Lower for more patterns, higher for quality

Adaptive Parameter Adjustment

• Default: True (Enabled)

• Enables automatic parameter optimization

• Adjusts based on market regime

• Highly recommended to keep enabled

Section 3: Market Structure Analysis

Enable Structure Validation

• Default: True (Enabled)

• Validates patterns against support/resistance

• Confirms trend structure alignment

• Essential for reliability

Structure Analysis Period (15-50)

• Default: 30 bars

• Period for structure pattern analysis

• Affects support/resistance calculation

• Match to your trading timeframe

Minimum Structure Alignment (0.3-0.8)

• Default: 0.5

• Required structure score for valid patterns

• Higher values need stronger structure

• Balance with desired frequency

Section 4: Analysis Configuration

Minimum Strength Level (3-5)

• Default: 4

• Minimum confirmations for pattern display

• 5 = Maximum reliability, 3 = More patterns

• Beginners should use 4-5

Required Technical Confirmations (4-6)

• Default: 5

• Number of aligned technical factors

• Higher = fewer but better patterns

• Works with High Confirmation Mode

Pattern Separation (3-20 bars)

• Default: 8 bars

• Minimum bars between patterns

• Prevents clustering and overtrading

• Increase for cleaner charts

Section 5: Technical Filters

Momentum Validation

• Default: True (Enabled)

• Requires momentum alignment

• Filters counter-trend patterns

• Essential for trend following

Volume Confluence Analysis

• Default: True (Enabled)

• Requires volume confirmation

• Identifies institutional participation

• Critical for reliability

Trend Direction Filter

• Default: True (Enabled)

• Only shows patterns with trend

• Reduces counter-trend signals

• Disable for reversal hunting

Section 6: Volume Flow Analysis

Institutional Activity Threshold (1.2-3.5)

• Default: 2.0

• Multiplier for unusual volume detection

• Lower finds more institutional activity

• Stock: 2.0-2.5, Forex: 1.5-2.0, Crypto: 2.5-3.5

Volume Surge Multiplier (1.8-4.5)

• Default: 2.5

• Defines significant volume increases

• Adjust per instrument characteristics

• Higher for stocks, lower for forex

Volume Flow Period (12-35)

• Default: 18 bars

• Smoothing for volume analysis

• Shorter = responsive, longer = smooth

• Match to timeframe used

Section 7: Analysis Frequency Control

Maximum Analysis Points Per Hour (1-5)

• Default: 3

• Limits pattern frequency

• Prevents overtrading

• Scalpers: 4-5, Swing traders: 1-2

Section 8: Target Level Configuration

Target Calculation Method

• Default: Market Adaptive

• Three modes available:

- Fixed: Uses set point distances

- Dynamic: ATR-based calculations

- Market Adaptive: Structure-based levels

Minimum Target/Risk Ratio (1.0-3.0)

• Default: 1.5

• Minimum acceptable reward vs risk

• Higher filters lower probability setups

• Professional standard: 1.5-2.0

Fixed Mode Settings:

• Fixed Target Distance: 50 points default

• Fixed Invalidation Distance: 30 points default

• Use for consistent instruments

Dynamic Mode Settings: