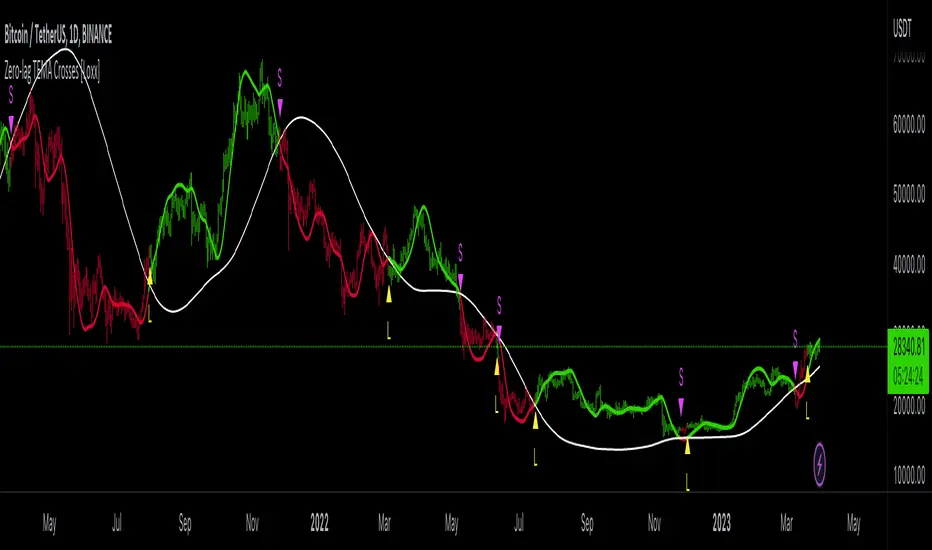

Zero-lag TEMA Crosses [Loxx]Zero-lag TEMA Crosses is a spinoff of a the Zero-lag MA as described by David Stendahl in the April 2000 issue of the journal "Technical Analysis of Stocks and Commodities". This indicator uses TEMA calculation mode in order to make the lag lesser compared to the original Zero-lag MA, and that makes this version even faster than the Zero-lag DEMA too. This indicator is the difference between a Fast and Slow Zero-lag TEMA. This indicator is very useful for lower timeframe scalping.

What is the Zero-lag MA?

The Zero-lag MA (Zero-Lag Moving Average) is a technical indicator that was introduced in the April 2000 issue of the journal "Technical Analysis of Stocks and Commodities" by David Stendahl.

The Zero-lag MA is a type of moving average (MA) that is designed to reduce or eliminate the lag that is typically associated with traditional moving averages. Moving averages are a widely used technical analysis tool that helps traders to identify trends and potential trading opportunities. They work by calculating the average price of a security over a given period of time, and then plotting that average on a chart. The most commonly used moving averages are simple moving averages (SMAs) and exponential moving averages (EMAs).

The problem with traditional moving averages is that they can be slow to respond to changes in market conditions. This lag can cause traders to miss out on potential trading opportunities, or to enter or exit trades at the wrong time. The Zero-lag MA was developed as a solution to this problem.

The Zero-lag MA is calculated using a combination of two EMAs and a subtraction formula. The first step in calculating the Zero-lag MA is to calculate two exponential moving averages: a fast EMA and a slow EMA. The fast EMA is calculated over a shorter period of time than the slow EMA. The exact period lengths will depend on the trader's preferences and the security being analyzed.

Once the two EMAs have been calculated, the next step is to take the difference between them. This difference represents the current market trend, with a positive value indicating an uptrend and a negative value indicating a downtrend. However, this difference alone is not enough to create a useful indicator, as it can still suffer from lag.

To further reduce lag, the difference between the two EMAs is multiplied by a factor derived from a third, slower EMA. This slower EMA acts as a smoothing factor, helping to reduce noise and make the indicator more accurate. The exact period length of the slower EMA will depend on the trader's preferences and the security being analyzed.

The final step in calculating the Zero-lag MA is to add the result of the multiplication to the fast EMA. This produces a final value that represents the current market trend with reduced lag. The Zero-lag MA can be plotted on a chart like any other moving average, and can be used to identify trends, potential trading opportunities, and support and resistance levels.

Overall, the Zero-lag MA is designed to provide traders with a more accurate representation of current market conditions by reducing the lag time between price changes and the moving average. By doing so, it can help traders to make more informed trading decisions and improve their overall profitability.

What is the TEMA?

The triple exponential moving average (TEMA) is a technical analysis indicator that was developed to reduce the lag of traditional moving averages, such as the simple moving average (SMA) or the exponential moving average (EMA). The TEMA was first introduced by Patrick Mulloy in the January 1994 issue of the "Technical Analysis of Stocks and Commodities" magazine.

The TEMA is a type of moving average that is calculated by applying multiple exponential smoothing techniques to price data. Unlike traditional moving averages, which apply a single smoothing factor to price data, the TEMA applies three smoothing factors to produce a more responsive and accurate indicator.

To calculate the TEMA, the following steps are taken:

Calculate the single exponential moving average (SMA) of the price data over a given period.

Calculate the double exponential moving average (DEMA) of the SMA over the same period.

Calculate the triple exponential moving average (TEMA) of the DEMA over the same period.

The formula for calculating the TEMA is:

TEMA = 3 * EMA(SMA) - 3 * EMA(EMA(SMA)) + EMA(EMA(EMA(SMA)))

where EMA is the exponential moving average and SMA is the simple moving average.

The TEMA is designed to reduce the lag associated with traditional moving averages by applying multiple smoothing factors to the price data. This helps to filter out short-term price fluctuations and provide a smoother indicator of the underlying trend. The TEMA is also less susceptible to whipsaws, which occur when a security's price moves in one direction and then quickly reverses, causing false trading signals.

The TEMA can be used in a variety of ways in technical analysis. It can be used to identify trends, determine support and resistance levels, and generate trading signals. When the TEMA is rising, it is generally interpreted as a bullish signal, indicating that the price is trending higher. When the TEMA is falling, it is generally interpreted as a bearish signal, indicating that the price is trending lower.

In summary, the TEMA is a more responsive and accurate indicator than traditional moving averages, designed to reduce lag and provide a smoother representation of the underlying trend. It is a useful tool for technical analysts and traders looking to identify trends, support and resistance levels, and potential trading opportunities.

Extras

Alerts

Bar coloring

Signals

Loxx's Expanded Source Types, see here:

Buscar en scripts para "2000元+股票投资+最低门槛"

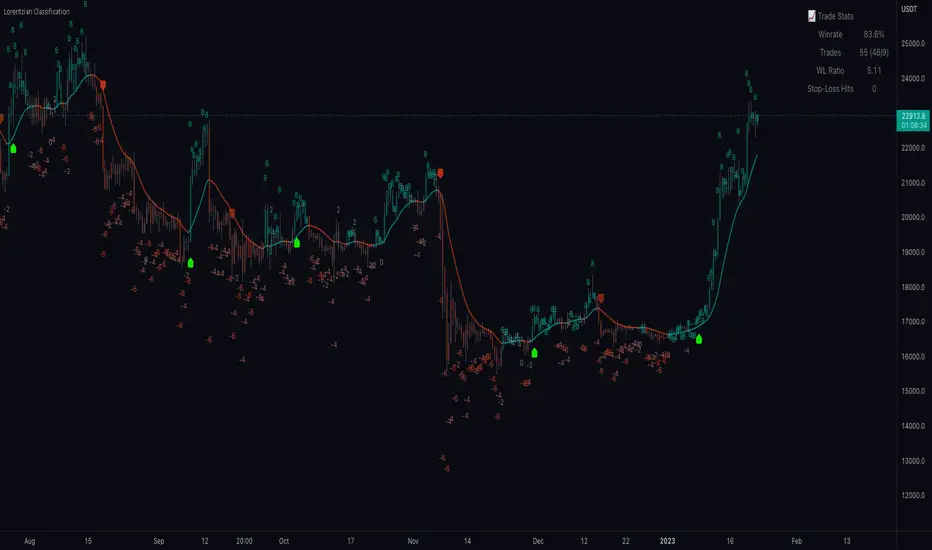

Machine Learning: Lorentzian Classification█ OVERVIEW

A Lorentzian Distance Classifier (LDC) is a Machine Learning classification algorithm capable of categorizing historical data from a multi-dimensional feature space. This indicator demonstrates how Lorentzian Classification can also be used to predict the direction of future price movements when used as the distance metric for a novel implementation of an Approximate Nearest Neighbors (ANN) algorithm.

█ BACKGROUND

In physics, Lorentzian space is perhaps best known for its role in describing the curvature of space-time in Einstein's theory of General Relativity (2). Interestingly, however, this abstract concept from theoretical physics also has tangible real-world applications in trading.

Recently, it was hypothesized that Lorentzian space was also well-suited for analyzing time-series data (4), (5). This hypothesis has been supported by several empirical studies that demonstrate that Lorentzian distance is more robust to outliers and noise than the more commonly used Euclidean distance (1), (3), (6). Furthermore, Lorentzian distance was also shown to outperform dozens of other highly regarded distance metrics, including Manhattan distance, Bhattacharyya similarity, and Cosine similarity (1), (3). Outside of Dynamic Time Warping based approaches, which are unfortunately too computationally intensive for PineScript at this time, the Lorentzian Distance metric consistently scores the highest mean accuracy over a wide variety of time series data sets (1).

Euclidean distance is commonly used as the default distance metric for NN-based search algorithms, but it may not always be the best choice when dealing with financial market data. This is because financial market data can be significantly impacted by proximity to major world events such as FOMC Meetings and Black Swan events. This event-based distortion of market data can be framed as similar to the gravitational warping caused by a massive object on the space-time continuum. For financial markets, the analogous continuum that experiences warping can be referred to as "price-time".

Below is a side-by-side comparison of how neighborhoods of similar historical points appear in three-dimensional Euclidean Space and Lorentzian Space:

This figure demonstrates how Lorentzian space can better accommodate the warping of price-time since the Lorentzian distance function compresses the Euclidean neighborhood in such a way that the new neighborhood distribution in Lorentzian space tends to cluster around each of the major feature axes in addition to the origin itself. This means that, even though some nearest neighbors will be the same regardless of the distance metric used, Lorentzian space will also allow for the consideration of historical points that would otherwise never be considered with a Euclidean distance metric.

Intuitively, the advantage inherent in the Lorentzian distance metric makes sense. For example, it is logical that the price action that occurs in the hours after Chairman Powell finishes delivering a speech would resemble at least some of the previous times when he finished delivering a speech. This may be true regardless of other factors, such as whether or not the market was overbought or oversold at the time or if the macro conditions were more bullish or bearish overall. These historical reference points are extremely valuable for predictive models, yet the Euclidean distance metric would miss these neighbors entirely, often in favor of irrelevant data points from the day before the event. By using Lorentzian distance as a metric, the ML model is instead able to consider the warping of price-time caused by the event and, ultimately, transcend the temporal bias imposed on it by the time series.

For more information on the implementation details of the Approximate Nearest Neighbors (ANN) algorithm used in this indicator, please refer to the detailed comments in the source code.

█ HOW TO USE

Below is an explanatory breakdown of the different parts of this indicator as it appears in the interface:

Below is an explanation of the different settings for this indicator:

General Settings:

Source - This has a default value of "hlc3" and is used to control the input data source.

Neighbors Count - This has a default value of 8, a minimum value of 1, a maximum value of 100, and a step of 1. It is used to control the number of neighbors to consider.

Max Bars Back - This has a default value of 2000.

Feature Count - This has a default value of 5, a minimum value of 2, and a maximum value of 5. It controls the number of features to use for ML predictions.

Color Compression - This has a default value of 1, a minimum value of 1, and a maximum value of 10. It is used to control the compression factor for adjusting the intensity of the color scale.

Show Exits - This has a default value of false. It controls whether to show the exit threshold on the chart.

Use Dynamic Exits - This has a default value of false. It is used to control whether to attempt to let profits ride by dynamically adjusting the exit threshold based on kernel regression.

Feature Engineering Settings:

Note: The Feature Engineering section is for fine-tuning the features used for ML predictions. The default values are optimized for the 4H to 12H timeframes for most charts, but they should also work reasonably well for other timeframes. By default, the model can support features that accept two parameters (Parameter A and Parameter B, respectively). Even though there are only 4 features provided by default, the same feature with different settings counts as two separate features. If the feature only accepts one parameter, then the second parameter will default to EMA-based smoothing with a default value of 1. These features represent the most effective combination I have encountered in my testing, but additional features may be added as additional options in the future.

Feature 1 - This has a default value of "RSI" and options are: "RSI", "WT", "CCI", "ADX".

Feature 2 - This has a default value of "WT" and options are: "RSI", "WT", "CCI", "ADX".

Feature 3 - This has a default value of "CCI" and options are: "RSI", "WT", "CCI", "ADX".

Feature 4 - This has a default value of "ADX" and options are: "RSI", "WT", "CCI", "ADX".

Feature 5 - This has a default value of "RSI" and options are: "RSI", "WT", "CCI", "ADX".

Filters Settings:

Use Volatility Filter - This has a default value of true. It is used to control whether to use the volatility filter.

Use Regime Filter - This has a default value of true. It is used to control whether to use the trend detection filter.

Use ADX Filter - This has a default value of false. It is used to control whether to use the ADX filter.

Regime Threshold - This has a default value of -0.1, a minimum value of -10, a maximum value of 10, and a step of 0.1. It is used to control the Regime Detection filter for detecting Trending/Ranging markets.

ADX Threshold - This has a default value of 20, a minimum value of 0, a maximum value of 100, and a step of 1. It is used to control the threshold for detecting Trending/Ranging markets.

Kernel Regression Settings:

Trade with Kernel - This has a default value of true. It is used to control whether to trade with the kernel.

Show Kernel Estimate - This has a default value of true. It is used to control whether to show the kernel estimate.

Lookback Window - This has a default value of 8 and a minimum value of 3. It is used to control the number of bars used for the estimation. Recommended range: 3-50

Relative Weighting - This has a default value of 8 and a step size of 0.25. It is used to control the relative weighting of time frames. Recommended range: 0.25-25

Start Regression at Bar - This has a default value of 25. It is used to control the bar index on which to start regression. Recommended range: 0-25

Display Settings:

Show Bar Colors - This has a default value of true. It is used to control whether to show the bar colors.

Show Bar Prediction Values - This has a default value of true. It controls whether to show the ML model's evaluation of each bar as an integer.

Use ATR Offset - This has a default value of false. It controls whether to use the ATR offset instead of the bar prediction offset.

Bar Prediction Offset - This has a default value of 0 and a minimum value of 0. It is used to control the offset of the bar predictions as a percentage from the bar high or close.

Backtesting Settings:

Show Backtest Results - This has a default value of true. It is used to control whether to display the win rate of the given configuration.

█ WORKS CITED

(1) R. Giusti and G. E. A. P. A. Batista, "An Empirical Comparison of Dissimilarity Measures for Time Series Classification," 2013 Brazilian Conference on Intelligent Systems, Oct. 2013, DOI: 10.1109/bracis.2013.22.

(2) Y. Kerimbekov, H. Ş. Bilge, and H. H. Uğurlu, "The use of Lorentzian distance metric in classification problems," Pattern Recognition Letters, vol. 84, 170–176, Dec. 2016, DOI: 10.1016/j.patrec.2016.09.006.

(3) A. Bagnall, A. Bostrom, J. Large, and J. Lines, "The Great Time Series Classification Bake Off: An Experimental Evaluation of Recently Proposed Algorithms." ResearchGate, Feb. 04, 2016.

(4) H. Ş. Bilge, Yerzhan Kerimbekov, and Hasan Hüseyin Uğurlu, "A new classification method by using Lorentzian distance metric," ResearchGate, Sep. 02, 2015.

(5) Y. Kerimbekov and H. Şakir Bilge, "Lorentzian Distance Classifier for Multiple Features," Proceedings of the 6th International Conference on Pattern Recognition Applications and Methods, 2017, DOI: 10.5220/0006197004930501.

(6) V. Surya Prasath et al., "Effects of Distance Measure Choice on KNN Classifier Performance - A Review." .

█ ACKNOWLEDGEMENTS

@veryfid - For many invaluable insights, discussions, and advice that helped to shape this project.

@capissimo - For open sourcing his interesting ideas regarding various KNN implementations in PineScript, several of which helped inspire my original undertaking of this project.

@RikkiTavi - For many invaluable physics-related conversations and for his helping me develop a mechanism for visualizing various distance algorithms in 3D using JavaScript

@jlaurel - For invaluable literature recommendations that helped me to understand the underlying subject matter of this project.

@annutara - For help in beta-testing this indicator and for sharing many helpful ideas and insights early on in its development.

@jasontaylor7 - For helping to beta-test this indicator and for many helpful conversations that helped to shape my backtesting workflow

@meddymarkusvanhala - For helping to beta-test this indicator

@dlbnext - For incredibly detailed backtesting testing of this indicator and for sharing numerous ideas on how the user experience could be improved.

I11L - Meanreverter 4h---Overview---

The system buys fear and sells greed.

Its relies on a Relative Strength Index (RSI) and moving averages (MA) to find oversold and overbought states.

It seems to work best in market conditions where the Bond market has a negative Beta to Stocks.

Backtests in a longer Timeframe will clearly show this.

---Parameter---

Frequency: Smothens the RSI curve, helps to "remember" recent highs better.

RsiFrequency: A Frequency of 40 implies a RSI over the last 40 Bars.

BuyZoneDistance: Spacing between the different zones. A wider spacing reduces the amount of signals and icnreases the holding duration. Should be finetuned with tradingcosts in mind.

AvgDownATRSum: The multiple of the Average ATR over 20 Bars * amount of opentrades for your average down. I choose the ATR over a fixed percent loss to find more signals in low volatility environments and less in high volatility environments.

---Some of my thoughts---

Be very careful about the good backtesting performance in many US-Stocks because the System had a favourable environment since 1970.

Be careful about the survivorship bias as well.

52% of stocks from the S&P500 were removed since 2000.

I discount my Annual Results by 5% because of this fact.

You will find yourself quite often with very few signals because of the high market correlation.

My testing suggests that there is no expected total performance difference between a signal from a bad and a signal from a good market condition but a higher volatility.

I am sharing this strategy because i am currently not able to implement it as i want to and i think that meanreversion is starting to be taken more serious by traders.

The challange in implementing this strategy is that you need to be invested 100% of the time to retrieve the expected annual performance and to reduce the fat tail risk by market crashes.

ChillLax Percent Up and Down

Show the days that the stock is up 5% (default) or down 5%, from the previous close.

Useful to spot a cluster of those days. It indicates violent, choppy environment. It's better to keep your boat docked in choppy waters. Eg: see QQQ in 2008, 2000.

Entanglement Penscript name: Entanglement Pen

For left traders, how to accurately find the bottom and top is very important, and there are various methods. I have shared the bottom type script composed of three bars before, but this type of bottom type is effective in a small range. So, this script is sharing " Entanglement Pen ", which can help us determine bottoms and tops on a global scale.

However, this script uses an approximate reduction method rather than the orthodox solution of entanglement.

After roughly finding the bottom and top, how to determine that these are the bottom and top that meet the definition of entanglement theory?

The main 2 methods of "approximate reduction" are:

(1) The price difference between the top and the bottom is large enough, that is: the lowest price at the top > the highest price at the bottom.

(2) The stock price before the top has continued to rise, that is: both the highest point and the lowest point are rising. In the same way, the stock price before the bottom has a continuous decline, that is: both the high and the low point are falling.

A big disadvantage of this script is that it needs to use future data. This is because:

When multiple bars meet the top definition in a short period of time, only the last bar is used, which is defined as a big top. So, when you see a top appear, you don't know it's not a real top, because it might be followed by a bar that also matches the definition of the top.

When displayed on the graph, bars that meet the top definition have a gray label, which is the small top. Each small top is a big top (with a blue label) at the beginning, and when another small top appears after it, it becomes a gray small top.

Regarding the limit on the number of bars by TradingView:

The logic of calculating the small top and the small bottom is relatively simple, it does not need to use future data, and the amount of calculation is small, so it is the default TradingView limit. (The limit is 2000 in the script, but in practice TradingView won't let us use such many bars)

The calculation logic of the big top and the big bottom is more complicated, and it needs to use future data. The calculation amount is very large, and only the most recent 150 bars can be calculated. The user can try to enter a larger value, but TradingView may report an error. If an error occurs, please enter a lower value. When loading for the first time, it takes a long time, which is indeed not common in general TradingView scripts, but please be patient.

The next version may add the alert function, that is: when the top and bottom appear, the alert function is called. But this only applies to small tops and bottoms, because when the alert is sent,, none of us know what data will be in the future.

Introduction in Chinese:

脚本名称:缠论笔

对于左侧交易者来说,如何准确地找到底部和顶部是非常重要的,方法也是多样的,之前已经分享了三根bar组成的底分型脚本,但这种底分型生效的范围较小,缺乏全局视野。所以,这次的脚本分享的是“缠论笔”,它能帮我们在全局尺度内确定底部和顶部。

不过,此脚本使用的是近似还原的方法,而非缠论的正统解法。

粗略找到底和顶之后,如何确定这就是符合缠论定义的底和顶呢?

“近似还原”的主要2个方法是:

(1)顶部与底部的价差足够大,即:顶部的最低价>底部的最高价。

(2)顶部之前的股价有持续的上涨,即:最高点和最低点都在上涨。同理,底部之前的股价有持续的下跌,即:最高点和最低点都在下跌。

这个脚本的一大缺点是:需要使用将来的数据。这是因为:

当短期内有多个bar都符合顶部定义时,只使用最后一个bar,定义为大顶。所以,当你看到一个顶部出现时,你不知道这不是真的顶部,因为它之后可能还会出现符合顶部定义的bar。

在图上显示时,符合顶部定义的bar有灰色的label,这是小顶。每一个小顶,刚开始时都是大顶(有蓝色的label),直到它之后又有小顶出现时,它就变成了灰色的小顶。

关于TradingView对bar数的限制:

计算小顶和小底的逻辑比较简单,不需要使用将来的数据,计算量较小,所以是默认的TradingView限制。(脚本中限制为2000,但实际上TradingView不会让我们使用那么多bar)

大顶和大底的计算逻辑比较复杂,需要使用将来的数据,计算量非常大,大约只能计算最近150根bar。用户可以尝试输入更大的数值,但TradingView可能会报错。若遇报错,则请输入更低的数值。初次加载时,需要等待较长时间,这确实在一般的TradingView脚本中并不常见,但还是请多些耐心。

下一版可能会增加alert功能,即:当顶部和底部出现时,调用alert函数。但这只适用于小顶和小底,因为警报发出时,我们谁也不知道将来的数据。

Webhook Starter Kit [HullBuster]

Introduction

This is an open source strategy which provides a framework for webhook enabled projects. It is designed to work out-of-the-box on any instrument triggering on an intraday bar interval. This is a full featured script with an emphasis on actual trading at a brokerage through the TradingView alert mechanism and without requiring browser plugins.

The source code is written in a self documenting style with clearly defined sections. The sections “communicate” with each other through state variables making it easy for the strategy to evolve and improve. This is an excellent place for Pine Language beginners to start their strategy building journey. The script exhibits many Pine Language features which will certainly ad power to your script building abilities.

This script employs a basic trend follow strategy utilizing a forward pyramiding technique. Trend detection is implemented through the use of two higher time frame series. The market entry setup is a Simple Moving Average crossover. Positions exit by passing through conditional take profit logic. The script creates ten indicators including a Zscore oscillator to measure support and resistance levels. The indicator parameters are exposed through 47 strategy inputs segregated into seven sections. All of the inputs are equipped with detailed tool tips to help you get started.

To improve the transition from simulation to execution, strategy.entry and strategy.exit calls show enhanced message text with embedded keywords that are combined with the TradingView placeholders at alert time. Thereby, enabling a single JSON message to generate multiple execution events. This is genius stuff from the Pine Language development team. Really excellent work!

This document provides a sample alert message that can be applied to this script with relatively little modification. Without altering the code, the strategy inputs can alter the behavior to generate thousands of orders or simply a few dozen. It can be applied to crypto, stocks or forex instruments. A good way to look at this script is as a webhook lab that can aid in the development of your own endpoint processor, impress your co-workers and have hours of fun.

By no means is a webhook required or even necessary to benefit from this script. The setups, exits, trend detection, pyramids and DCA algorithms can be easily replaced with more sophisticated versions. The modular design of the script logic allows you to incrementally learn and advance this script into a functional trading system that you can be proud of.

Design

This is a trend following strategy that enters long above the trend line and short below. There are five trend lines that are visible by default but can be turned off in Section 7. Identified, in frequency order, as follows:

1. - EMA in the chart time frame. Intended to track price pressure. Configured in Section 3.

2. - ALMA in the higher time frame specified in Section 2 Signal Line Period.

3. - Linear Regression in the higher time frame specified in Section 2 Signal Line Period.

4. - Linear Regression in the higher time frame specified in Section 2 Signal Line Period.

5. - DEMA in the higher time frame specified in Section 2 Trend Line Period.

The Blue, Green and Orange lines are signal lines are on the same time frame. The time frame selected should be at least five times greater than the chart time frame. The Purple line represents the trend line for which prices above the line suggest a rising market and prices below a falling market. The time frame selected for the trend should be at least five times greater than the signal lines.

Three oscillators are created as follows:

1. Stochastic - In the chart time frame. Used to enter forward pyramids.

2. Stochastic - In the Trend period. Used to detect exit conditions.

3. Zscore - In the Signal period. Used to detect exit conditions.

The Stochastics are configured identically other than the time frame. The period is set in Section 2.

Two Simple Moving Averages provide the trade entry conditions in the form of a crossover. Crossing up is a long entry and down is a short. This is in fact the same setup you get when you select a basic strategy from the Pine editor. The crossovers are configured in Section 3. You can see where the crosses are occurring by enabling Show Entry Regions in Section 7.

The script has the capacity for pyramids and DCA. Forward pyramids are enabled by setting the Pyramid properties tab with a non zero value. In this case add on trades will enter the market on dips above the position open price. This process will continue until the trade exits. Downward pyramids are available in Crypto and Range mode only. In this case add on trades are placed below the entry price in the drawdown space until the stop is hit. To enable downward pyramids set the Pyramid Minimum Span In Section 1 to a non zero value.

This implementation of Dollar Cost Averaging (DCA) triggers off consecutive losses. Each loss in a run increments a sequence number. The position size is increased as a multiple of this sequence. When the position eventually closes at a profit the sequence is reset. DCA is enabled by setting the Maximum DCA Increments In Section 1 to a non zero value.

It should be noted that the pyramid and DCA features are implemented using a rudimentary design and as such do not perform with the precision of my invite only scripts. They are intended as a feature to stress test your webhook endpoint. As is, you will need to buttress the logic for it to be part of an automated trading system. It is for this reason that I did not apply a Martingale algorithm to this pyramid implementation. But, hey, it’s an open source script so there is plenty of room for learning and your own experimentation.

How does it work

The overall behavior of the script is governed by the Trading Mode selection in Section 1. It is the very first input so you should think about what behavior you intend for this strategy at the onset of the configuration. As previously discussed, this script is designed to be a trend follower. The trend being defined as where the purple line is predominately heading. In BiDir mode, SMA crossovers above the purple line will open long positions and crosses below the line will open short. If pyramiding is enabled add on trades will accumulate on dips above the entry price. The value applied to the Minimum Profit input in Section 1 establishes the threshold for a profitable exit. This is not a hard number exit. The conditional exit logic must be satisfied in order to permit the trade to close. This is where the effort put into the indicator calibration is realized. There are four ways the trade can exit at a profit:

1. Natural exit. When the blue line crosses the green line the trade will close. For a long position the blue line must cross under the green line (downward). For a short the blue must cross over the green (upward).

2. Alma / Linear Regression event. The distance the blue line is from the green and the relative speed the cross is experiencing determines this event. The activation thresholds are set in Section 6 and relies on the period and length set in Section 2. A long position will exit on an upward thrust which exceeds the activation threshold. A short will exit on a downward thrust.

3. Exponential event. The distance the yellow line is from the blue and the relative speed the cross is experiencing determines this event. The activation thresholds are set in Section 3 and relies on the period and length set in the same section.

4. Stochastic event. The purple line stochastic is used to measure overbought and over sold levels with regard to position exits. Signal line positions combined with a reading over 80 signals a long profit exit. Similarly, readings below 20 signal a short profit exit.

Another, optional, way to exit a position is by Bale Out. You can enable this feature in Section 1. This is a handy way to reduce the risk when carrying a large pyramid stack. Instead of waiting for the entire position to recover we exit early (bale out) as soon as the profit value has doubled.

There are lots of ways to implement a bale out but the method I used here provides a succinct example. Feel free to improve on it if you like. To see where the Bale Outs occur, enable Show Bale Outs in Section 7. Red labels are rendered below each exit point on the chart.

There are seven selectable Trading Modes available from the drop down in Section 1:

1. Long - Uses the strategy.risk.allow_entry_in to execute long only trades. You will still see shorts on the chart.

2. Short - Uses the strategy.risk.allow_entry_in to execute short only trades. You will still see long trades on the chart.

3. BiDir - This mode is for margin trading with a stop. If a long position was initiated above the trend line and the price has now fallen below the trend, the position will be reversed after the stop is hit. Forward pyramiding is available in this mode if you set the Pyramiding value in the Properties tab. DCA can also be activated.

4. Flip Flop - This is a bidirectional trading mode that automatically reverses on a trend line crossover. This is distinctively different from BiDir since you will get a reversal even without a stop which is advantageous in non-margin trading.

5. Crypto - This mode is for crypto trading where you are buying the coins outright. In this case you likely want to accumulate coins on a crash. Especially, when all the news outlets are talking about the end of Bitcoin and you see nice deep valleys on the chart. Certainly, under these conditions, the market will be well below the purple line. No margin so you can’t go short. Downward pyramids are enabled for Crypto mode when two conditions are met. First the Pyramiding value in the Properties tab must be non zero. Second the Pyramid Minimum Span in Section 1 must be non zero.

6. Range - This is a counter trend trading mode. Longs are entered below the purple trend line and shorts above. Useful when you want to test your webhook in a market where the trend line is bisecting the signal line series. Remember that this strategy is a trend follower. It’s going to get chopped out in a range bound market. By turning on the Range mode you will at least see profitable trades while stuck in the range. However, when the market eventually picks a direction, this mode will sustain losses. This range trading mode is a rudimentary implementation that will need a lot of improvement if you want to create a reliable switch hitter (trend/range combo).

7. No Trade. Useful when setting up the trend lines and the entry and exit is not important.

Once in the trade, long or short, the script tests the exit condition on every bar. If not a profitable exit then it checks if a pyramid is required. As mentioned earlier, the entry setups are quite primitive. Although they can easily be replaced by more sophisticated algorithms, what I really wanted to show is the diminished role of the position entry in the overall life of the trade. Professional traders spend much more time on the management of the trade beyond the market entry. While your trade entry is important, you can get in almost anywhere and still land a profitable exit.

If DCA is enabled, the size of the position will increase in response to consecutive losses. The number of times the position can increase is limited by the number set in Maximum DCA Increments of Section 1. Once the position breaks the losing streak the trade size will return the default quantity set in the Properties tab. It should be noted that the Initial Capital amount set in the Properties tab does not affect the simulation in the same way as a real account. In reality, running out of money will certainly halt trading. In fact, your account would be frozen long before the last penny was committed to a trade. On the other hand, TradingView will keep running the simulation until the current bar even if your funds have been technically depleted.

Entry and exit use the strategy.entry and strategy.exit calls respectfully. The alert_message parameter has special keywords that the endpoint expects to properly calculate position size and message sequence. The alert message will embed these keywords in the JSON object through the {{strategy.order.alert_message}} placeholder. You should use whatever keywords are expected from the endpoint you intend to webhook in to.

Webhook Integration

The TradingView alerts dialog provides a way to connect your script to an external system which could actually execute your trade. This is a fantastic feature that enables you to separate the data feed and technical analysis from the execution and reporting systems. Using this feature it is possible to create a fully automated trading system entirely on the cloud. Of course, there is some work to get it all going in a reliable fashion. Being a strategy type script place holders such as {{strategy.position_size}} can be embedded in the alert message text. There are more than 10 variables which can write internal script values into the message for delivery to the specified endpoint.

Entry and exit use the strategy.entry and strategy.exit calls respectfully. The alert_message parameter has special keywords that my endpoint expects to properly calculate position size and message sequence. The alert message will embed these keywords in the JSON object through the {{strategy.order.alert_message}} placeholder. You should use whatever keywords are expected from the endpoint you intend to webhook in to.

Here is an excerpt of the fields I use in my webhook signal:

"broker_id": "kraken",

"account_id": "XXX XXXX XXXX XXXX",

"symbol_id": "XMRUSD",

"action": "{{strategy.order.action}}",

"strategy": "{{strategy.order.id}}",

"lots": "{{strategy.order.contracts}}",

"price": "{{strategy.order.price}}",

"comment": "{{strategy.order.alert_message}}",

"timestamp": "{{time}}"

Though TradingView does a great job in dispatching your alert this feature does come with a few idiosyncrasies. Namely, a single transaction call in your script may cause multiple transmissions to the endpoint. If you are using placeholders each message describes part of the transaction sequence. A good example is closing a pyramid stack. Although the script makes a single strategy.close() call, the endpoint actually receives a close message for each pyramid trade. The broker, on the other hand, only requires a single close. The incongruity of this situation is exacerbated by the possibility of messages being received out of sequence. Depending on the type of order designated in the message, a close or a reversal. This could have a disastrous effect on your live account. This broker simulator has no idea what is actually going on at your real account. Its just doing the job of running the simulation and sending out the computed results. If your TradingView simulation falls out of alignment with the actual trading account lots of really bad things could happen. Like your script thinks your are currently long but the account is actually short. Reversals from this point forward will always be wrong with no one the wiser. Human intervention will be required to restore congruence. But how does anyone find out this is occurring? In closed systems engineering this is known as entropy. In practice your webhook logic should be robust enough to detect these conditions. Be generous with the placeholder usage and give the webhook code plenty of information to compare states. Both issuer and receiver. Don’t blindly commit incoming signals without verifying system integrity.

Setup

The following steps provide a very brief set of instructions that will get you started on your first configuration. After you’ve gone through the process a couple of times, you won’t need these anymore. It’s really a simple script after all. I have several example configurations that I used to create the performance charts shown. I can share them with you if you like. Of course, if you’ve modified the code then these steps are probably obsolete.

There are 47 inputs divided into seven sections. For the most part, the configuration process is designed to flow from top to bottom. Handy, tool tips are available on every field to help get you through the initial setup.

Step 1. Input the Base Currency and Order Size in the Properties tab. Set the Pyramiding value to zero.

Step 2. Select the Trading Mode you intend to test with from the drop down in Section 1. I usually select No Trade until I’ve setup all of the trend lines, profit and stop levels.

Step 3. Put in your Minimum Profit and Stop Loss in the first section. This is in pips or currency basis points (chart right side scale). Remember that the profit is taken as a conditional exit not a fixed limit. The actual profit taken will almost always be greater than the amount specified. The stop loss, on the other hand, is indeed a hard number which is executed by the TradingView broker simulator when the threshold is breached.

Step 4. Apply the appropriate value to the Tick Scalar field in Section 1. This value is used to remove the pipette from the price. You can enable the Summary Report in Section 7 to see the TradingView minimum tick size of the current chart.

Step 5. Apply the appropriate Price Normalizer value in Section 1. This value is used to normalize the instrument price for differential calculations. Basically, we want to increase the magnitude to significant digits to make the numbers more meaningful in comparisons. Though I have used many normalization techniques, I have always found this method to provide a simple and lightweight solution for less demanding applications. Most of the time the default value will be sufficient. The Tick Scalar and Price Normalizer value work together within a single calculation so changing either will affect all delta result values.

Step 6. Turn on the trend line plots in Section 7. Then configure Section 2. Try to get the plots to show you what’s really happening not what you want to happen. The most important is the purple trend line. Select an interval and length that seem to identify where prices tend to go during non-consolidation periods. Remember that a natural exit is when the blue crosses the green line.

Step 7. Enable Show Event Regions in Section 7. Then adjust Section 6. Blue background fills are spikes and red fills are plunging prices. These measurements should be hard to come by so you should see relatively few fills on the chart if you’ve set this up as intended. Section 6 includes the Zscore oscillator the state of which combines with the signal lines to detect statistically significant price movement. The Zscore is a zero based calculation with positive and negative magnitude readings. You want to input a reasonably large number slightly below the maximum amplitude seen on the chart. Both rise and fall inputs are entered as a positive real number. You can easily use my code to create a separate indicator if you want to see it in action. The default value is sufficient for most configurations.

Step 8. Turn off Show Event Regions and enable Show Entry Regions in Section 7. Then adjust Section 3. This section contains two parts. The entry setup crossovers and EMA events. Adjust the crossovers first. That is the Fast Cross Length and Slow Cross Length. The frequency of your trades will be shown as blue and red fills. There should be a lot. Then turn off Show Event Regions and enable Display EMA Peaks. Adjust all the fields that have the word EMA. This is actually the yellow line on the chart. The blue and red fills should show much less than the crossovers but more than event fills shown in Step 7.

Step 9. Change the Trading Mode to BiDir if you selected No Trades previously. Look on the chart and see where the trades are occurring. Make adjustments to the Minimum Profit and Stop Offset in Section 1 if necessary. Wider profits and stops reduce the trade frequency.

Step 10. Go to Section 4 and 5 and make fine tuning adjustments to the long and short side.

Example Settings

To reproduce the performance shown on the chart please use the following configuration: (Bitcoin on the Kraken exchange)

1. Select XBTUSD Kraken as the chart symbol.

2. On the properties tab set the Order Size to: 0.01 Bitcoin

3. On the properties tab set the Pyramiding to: 12

4. In Section 1: Select “Crypto” for the Trading Model

5. In Section 1: Input 2000 for the Minimum Profit

6. In Section 1: Input 0 for the Stop Offset (No Stop)

7. In Section 1: Input 10 for the Tick Scalar

8. In Section 1: Input 1000 for the Price Normalizer

9. In Section 1: Input 2000 for the Pyramid Minimum Span

10. In Section 1: Check mark the Position Bale Out

11. In Section 2: Input 60 for the Signal Line Period

12. In Section 2: Input 1440 for the Trend Line Period

13. In Section 2: Input 5 for the Fast Alma Length

14. In Section 2: Input 22 for the Fast LinReg Length

15. In Section 2: Input 100 for the Slow LinReg Length

16. In Section 2: Input 90 for the Trend Line Length

17. In Section 2: Input 14 Stochastic Length

18. In Section 3: Input 9 Fast Cross Length

19. In Section 3: Input 24 Slow Cross Length

20. In Section 3: Input 8 Fast EMA Length

21. In Section 3: Input 10 Fast EMA Rise NetChg

22. In Section 3: Input 1 Fast EMA Rise ROC

23. In Section 3: Input 10 Fast EMA Fall NetChg

24. In Section 3: Input 1 Fast EMA Fall ROC

25. In Section 4: Check mark the Long Natural Exit

26. In Section 4: Check mark the Long Signal Exit

27. In Section 4: Check mark the Long Price Event Exit

28. In Section 4: Check mark the Long Stochastic Exit

29. In Section 5: Check mark the Short Natural Exit

30. In Section 5: Check mark the Short Signal Exit

31. In Section 5: Check mark the Short Price Event Exit

32. In Section 5: Check mark the Short Stochastic Exit

33. In Section 6: Input 120 Rise Event NetChg

34. In Section 6: Input 1 Rise Event ROC

35. In Section 6: Input 5 Min Above Zero ZScore

36. In Section 6: Input 120 Fall Event NetChg

37. In Section 6: Input 1 Fall Event ROC

38. In Section 6: Input 5 Min Below Zero ZScore

In this configuration we are trading in long only mode and have enabled downward pyramiding. The purple trend line is based on the day (1440) period. The length is set at 90 days so it’s going to take a while for the trend line to alter course should this symbol decide to node dive for a prolonged amount of time. Your trades will still go long under those circumstances. Since downward accumulation is enabled, your position size will grow on the way down.

The performance example is Bitcoin so we assume the trader is buying coins outright. That being the case we don’t need a stop since we will never receive a margin call. New buy signals will be generated when the price exceeds the magnitude and speed defined by the Event Net Change and Rate of Change.

Feel free to PM me with any questions related to this script. Thank you and happy trading!

CFTC RULE 4.41

These results are based on simulated or hypothetical performance results that have certain inherent limitations. Unlike the results shown in an actual performance record, these results do not represent actual trading. Also, because these trades have not actually been executed, these results may have under-or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated or hypothetical trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to these being shown.

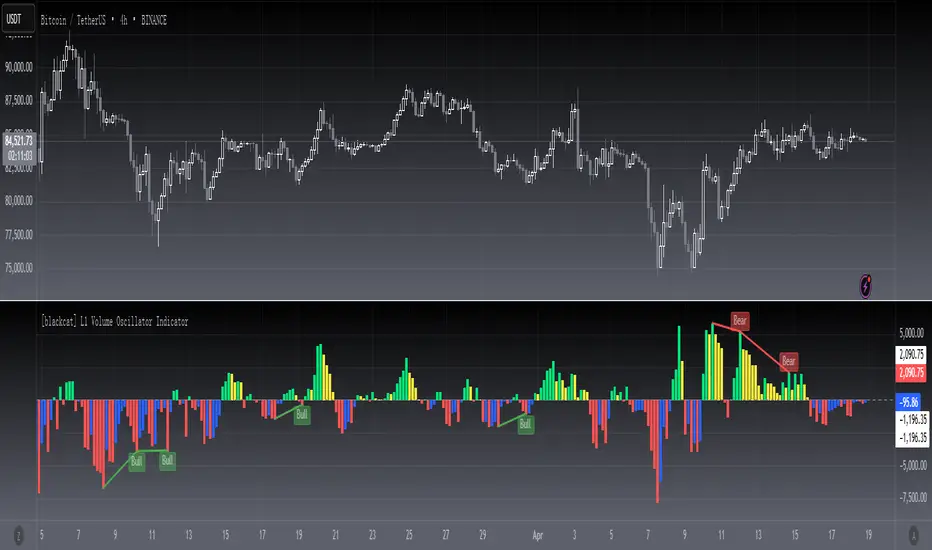

[blackcat] L1 volume Oscillator IndicatorLevel: 1

Background

Omega Research proposed volume oscillator indicator in June 2000.

Function

This is actually a volume-price indicator. With columns greater than zero line, which indicates a up trend. Otherwise, it is a down trend. Green columns indicate up trend pump; yellow columns indicate up trend retracements; red columns indicate down trend dump; blue columns indicate down trend re-bounce.

Key Signal

VolOsc --> volume osillator indicator.

Remarks

This is a Level 1 free and open source indicator.

Feedbacks are appreciated.

[blackcat] L1 Tether LineLevel: 1

Background

Omega Research proposed Tether line in June 2000. I utilized it in fast-slow line form to follow trend.

Function

Due it can provides good support and resistance, using it as "moving average" fast-slow line form can provide very stable golden cross and dead cross signal.

You can adjust parameters to fit for your trading pair and use it and compare it with Supertrend indicator.

Key Signal

Tether_fast --> Tether Fast Line.

Tether_slow --> Tether Slow Line.

Remarks

This is a Level 1 free and open source indicator.

Feedbacks are appreciated.

Random Entries Work!" tHe MaRkEtS aRe RaNdOm ", say moron academics.

The purpose of this study is to show that most markets are NOT random! Most markets show a clear bias where we can make such easy money, that a random number generator can do it.

=== HOW THE INDICATOR WORKS ===

The study will randomly enter the market

The study will randomly exit the market if in a trade

You can choose a Long Only, Short Only, or Bidirectional strategy

=== DEFAULT VALUES AND THEIR LOGIC ===

Percent Chance to Enter Per Bar: 10%

Percent Chance to Exit Per Bar: 3%

Direction: Long Only

Commission: 0

Each bar has a 10% chance to enter the market. Each bar has a 3% to exit the market . It will only enter long.

I included zero commission for simplification. It's a good exercise to include a commission/slippage to see just how much trading fees take from you.

=== TIPS ===

Increasing "Percent Chance to Exit" will shorten the time in a trade. You can see the "Avg # Bars In Trade" go down as you increase. If "Percent Chance to Exit" is too high, the study won't be in the market long enough to catch any movement, possibly exiting on the same bar most of the time.

If you're getting the red screen, that means the strategy lost so much money it went broke. Try reducing the percent equity on the Properties tab.

Switch the start year to avoid/minimize black swan events like the covid drop in 2020.

=== FINDINGS ===

Most markets lose money with a "Random" direction strategy.

Most markets lose ALL money with a "Short Only" strategy.

Most markets make money with a "Long Only" strategy.

Try this strategy on: Bitcoin (BTCUSD) and the NASDAQ (QQQ).

There are two popular memes right now: "Bitcoin to the moon" and "Stocks only go up". Both are seemingly true. Bitcoin was the best performing asset of the 2010's, gaining several billion percent in gains. The stock market is on a 100 year long uptrend. Why? BECAUSE FIAT CURRENCIES ALWAYS GO DOWN! This is inflation. If we measure the market in terms of others assets instead of fiat, the Long Only strategy doesn't work anymore (or works less well).

Try this strategy on: Bitcoin/GLD (BTCUSD/GLD), the Eurodollar (EURUSD), and the S&P 500 measured in gold (SPY/GLD).

Bitcoin measured in gold (BTCUSD/GLD) still works with a Long Only strategy because Bitcoin increased in value over both USD and gold.

The Eurodollar (EURUSD) generally loses money no matter what, especially if you add any commission. This makes sense as they are both fiat currencies with similar inflation schedules.

Gold and the S&P 500 have gained roughly the same amount since ~2000. Some years will show better results for a long strategy, while others will favor a short strategy. Now look at just SPY or GLD (which are both measured in USD by default!) and you'll see the same trend again: a Long Only strategy crushes even when entering and exiting randomly.

=== " JUST TELL ME WHAT TO DO, YOU NERD! " ===

Bulls always win and Bears always lose because fiat currencies go to zero.

You're not underperforming a random number generator, are you?

[blackcat] L1 Joe Sharp More Responsive Moving Average (MMA)Level: 1

Background

Joe Sharp propsed a "More Responsive Moving Averages (MMA)" in Jan, 2000. He describes a modified moving average that greatly diminishes the lag that is typically associated with moving averages. With the formula described in the article, the moving average line is more responsive to changes in the price action.

Function

An MMA indicator to plot the modified moving average is created in this script for application on a chart with fastline and slowline to produce golden crosses and dead crosses. In the pine script below, the calculation for the modified moving average is created in a function called ModifiedMA. This function basically takes care of all the necessary calculations for the modified moving average line. By putting the entire calculation into a function, the modified moving average calculation can be easily referenced by any analysis technique.

Key Signal

ModifiedMA (Price, FastLength) --> ModifiedMA Fast Line.

ModifiedMA (Price, SlowLength) --> ModifiedMA Slow Line.

Remarks

This is a Level 1 free and open source indicator.

Feedbacks are appreciated.

Average True Range NormalizedThis is a modified version of ATR. Instead of having volatility reading as unit price, we have percentage of the current price. Let say currently ATR is at 200 and the current close is 2000. Then this ATR will output 10.0 (10.0% volatility reading).

AVG position priceThis is a simple script that can show the average price of your position.

You can use up to 5 levels of averaging.

Use sum or amount setting - default - amount - you must enter price and amount - for example, your first purchase was - 0.1 bitcoin at 47000, second one - 0.2 btc at 45000 , so you must use this numbers.

Or you can choose "sum" - For example, you want to see what the average price of your position will be if you buy bitcoin for $ 1000 at the level of 47000 and later buy in addition for 2000 at the level of 46000 and another 2000 at the level of 43000.

__________________________________

Скрипт, показывающий среднюю точку входа в позицию.

В настройках необходимо выбрать:

- "amount" если вы знаете точное количество приобретаемого актива - например покупаете 0.1 биткоина на уровне 47000, далее докупаете 0.2 биткоина на 45к итд.

- "sum" если расчет идет исходя из суммы покупки - например взяли на 1к по 47000, дальше на 2к по 45к и еще на 2к по 40000

[blackcat] L2 Ehlers Squelch IndicatorLevel: 2

Background

John F. Ehlers introuced the squelch indicator in Sep, 2000.

Function

This the squelch indicator code is identical to the Hilbert period code , with the addition of the squelch threshold and the display being implemented as a paintbar -- that is, a bar on the chart being colored, depending on the squelch threshold value.

The Pine v4 code for displaying the squelch control as a paintbar for John Ehlers's article, "Squelch Those Whipsaws," can be reproduced in Tradingview by breaking the steps into separate functions. For example, functions can be written to calculate the "InPhase" and "Quadrature" variables, which can then be used in the calculation of the "Phase," "DeltaPhase," and "InstPeriod."

Although paintbars are not a feature of Tradingview, a similar effect can be displayed in a chart by writing a function to determine whether the period is less than 20. This function can then be displayed in main chart to highlight whether the price is in a trend mode or a cycle mode. The squelch period should also prove useful as an input for neural network predictions.

Key Signal

Plot1--> Highlight Period smaller than Squelch Threshold

Plot2--> Highlight Period smaller than Squelch Threshold

Pros and Cons

100% John F. Ehlers definition translation, even variable names are the same. This help readers who would like to use pine to read his book.

Remarks

The 65th script for Blackcat1402 John F. Ehlers Week publication.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

Breakout Trend Trading Strategy - V2This is an alternate version of Breakout Trend Trading Strategy - V1

Only difference is, this strategy places stop orders based on calculated targets whereas V1 waits for price to close target levels and then places market orders. Hence, you will receive the target prices before trade executes in strategy.

Parameters are same as that of Breakout Trend Trading Strategy - V1

There is one additional parameter on Trade Type - which permits user to allow only breakout, pullback or reverse trading or combination of all.

Backtesting parameters remain same :

Capital and position sizing : Capital and position sizing parameters are set to test investing 2000 wholly on certain stock without compounding.

Initial Capital : 2000

Order Size : 100% of equity

Pyramiding : 1

Test cases remain same :

Positive : AAPL , AMZN , TSLA , RUN, VRT , ASX:APT

Negative Test Cases: WPL , WHC , NHC , WOW, COL, NAB (All ASX stocks)

Special test case: WDI

Negative test cases still show losses in back-testing. I have attempted including many conditions to eliminate or reduce the loss. But, further efforts has resulted in reduction in profits in positive cases as well. Still experimenting. Will update whenever I find improvements. Comments and suggestions welcome :)

Breakout Trend Trading Strategy - V1Strategy in nutshell:

This strategy is made to be used in daily time-frames. Works better on trending instruments where volume is available. Hence, this is more suitable for trending shares rather than currencies, commodities and indexes where volume data is either not present or not reliable.

Breakout signifies the continuation of trend. Hence, trade in the direction of breakouts. Breakouts are calculated based on high volume and price movement in a day. This will be combined with few other conditions to generate buy and sell signals along with stop and compound targets. Supertrend is used for trend bias. Our buy and sell targets do not directly depend on the bias. But, entry criteria in opposite trend is made much difficult than that of trend direction. Further explanation of method and input parameters are explained below.

Backtesting parameters :

Capital and position sizing : Capital and position sizing parameters are set to test investing 2000 wholly on certain stock without compounding.

Initial Capital : 2000

Order Size : 100% of equity

Pyramiding : 1

ExitOnSignal : If unchecked exit is triggered solely on trailing stop

Trade Direction : Long, Short or All. Short condition is riskier than long conditions and often results in losses as per my observation. On most of the stocks trending up, strategy will not generate any short signals. This is achieved by comparing yearly high lows to previous two years to decide whether to allow short or long entries.

allowImmediateCompound : Applicable only if compounding/pyramiding is enabled in trade. If checked allows to place compounding orders immediately. If unchecked, it waits for stopline to cross order price before placing next compound.

Display Mode :

Targets : Whenever breakout happens, show marker for upTarget and downTarget

TargetChannel : Show up target and downtarget as a channel

Target With Stop : Along with targets, show also stop levels for breakouts

Up Channel : Channel created from UpTarget and respective stops

Down Channel : Channel created from DownTarget and respective stops

ShowTrailingStop : Shows trailing stop and compound lines when there is a trading position.

ShowTargetLevels : Shows Buy Sell target levels along with stop and compound lines. Trades are done as market orders. Hence, target levels are displayed after strategy makes the trade. Since only one order allowed per side without compounding, target, stop and compound levels are shown sometimes even without trade being made. These can be considered as entry levels if there is no existing position.

ShowPreviousLevels : Shows previous buy/sell target levels. When enabled, layout can look messy.

StopMultiplyer: To Set trailing stop loss.

BacktestYears: Number of years to include in backtest

So far my test cases are:

Positive : AAPL, AMZN, TSLA, RUN, VRT, ASX:APT

Negative Test Cases: WPL, WHC, NHC, WOW, COL, NAB (All ASX stocks)

Special test case: WDI

Negative test cases still show losses in backtesting. I have attempted including many conditions to eliminate or reduce the loss. But, further efforts has resulted in reduction in profits in positive cases as well. Still experimenting. Will update whenever I find improvements. Comments and suggestions welcome :)

StonkBTC - autoswitch secondary series for scalpersSince the drop in March of 2020, the U.S. ETF , SPY, has been correlated with bitcoin's moves, especially during the NY session.

This tool is meant to help traders who want to take advantage of that without having to switch the secondary series between BTCUSD and (generally) SPY when changing the ticker they are viewing.

How this works:

The indicator will automatically switch between bitcoin or equity index depending on what ticker your current chart is. Ideally this tool would be very simple to use.

Options:

Show/hide a 'track price' line

Index choice of SP500, Nasdaq 100, and Russell 2000. Further selection by ETF, futures, and CFD

Varied bitcoin price sources

Notes:

You will need a separate subscription to TradingView to view realtime CME futures data (if not, it will be delayed by 10 minutes). Because of this, the default option chosen is the CFD for the most complete chart when viewing bitcoin.

NY Core Trading Session: 9:30 a.m. to 4:00 p.m. ET

www.nyse.com

Donato Trend Stength IndexThis indicator is a basic way to look at longer periods of time and look for exhaustion based on closes above or below RSI50. The first output is RSI14 the second is a rolling 100 day aggregate of closes where 50 acts as 0. As of now it appears totals of 1200+ /-1200- could be considered overbought / oversold, respectively. Totals near or above / below 2000 / -2000 (respectively) could be great indicators of extreme trend exhaustion and impending reversal.

Open Interest Rank-BuschiEnglish:

One part of the "Commitment of Traders-Report" is the Open Interest which is shown in this indicator (source: Quandl database).

Unlike my also published indicator "Open Interest-Buschi", the values here are not absolute but in a ranking system from 0 to 100 with individual time frames-

The following futures are included:

30-year Bonds (ZB)

10-year Notes ( ZN )

Soybeans (ZS)

Soybean Meal (ZM)

Soybean Oil (ZL)

Corn ( ZC )

Soft Red Winter Wheat (ZW)

Hard Red Winter Wheat (KE)

Lean Hogs (HE)

Live Cattle ( LE )

Gold ( GC )

Silver (SI)

Copper (HG)

Crude Oil ( CL )

Heating Oil (HO)

RBOB Gasoline ( RB )

Natural Gas ( NG )

Australian Dollar (A6)

British Pound (B6)

Canadian Dollar (D6)

Euro (E6)

Japanese Yen (J6)

Swiss Franc (S6)

Sugar ( SB )

Coffee (KC)

Cocoa ( CC )

Cotton ( CT )

S&P 500 E-Mini (ES)

Russell 2000 E-Mini (RTY)

Dow Jones Industrial Mini (YM)

Nasdaq 100 E-Mini (NQ)

Platin (PL)

Palladium (PA)

Aluminium (AUP)

Steel ( HRC )

Ethanol (AEZ)

Brent Crude Oil (J26)

Rice (ZR)

Oat (ZO)

Milk (DL)

Orange Juice (JO)

Lumber (LS)

Feeder Cattle (GF)

S&P 500 ( SP )

Dow Jones Industrial Average Index (DJIA)

New Zealand Dollar (N6)

Deutsch:

Ein Bestandteil des "Commitment of Traders-Report" ist das Open Interest, das in diesem Indikator dargestellt wird (Quelle: Quandl Datenbank).

Anders als in meinem ebenfalls veröffentlichten Indikator "Open Interest-Buschi" werden hier nicht die absoluten Werte dargestellt, sondern in einem Ranking-System von 0 bis 100 mit individuellen Zeitrahmen.

Folgende Futures sind enthalten:

30-jährige US-Staatsanleihen (ZB)

10-jährige US-Staatsanleihen ( ZN )

Sojabohnen(ZS)

Sojabohnen-Mehl (ZM)

Sojabohnen-Öl (ZL)

Mais( ZC )

Soft Red Winter-Weizen (ZW)

Hard Red Winter-Weizen (KE)

Magerschweine (HE)

Lebendrinder ( LE )

Gold ( GC )

Silber (SI)

Kupfer(HG)

Rohöl ( CL )

Heizöl (HO)

Benzin ( RB )

Erdgas ( NG )

Australischer Dollar (A6)

Britisches Pfund (B6)

Kanadischer Dollar (D6)

Euro (E6)

Japanischer Yen (J6)

Schweizer Franken (S6)

Zucker ( SB )

Kaffee (KC)

Kakao ( CC )

Baumwolle ( CT )

S&P 500 E-Mini (ES)

Russell 2000 E-Mini (RTY)

Dow Jones Industrial Mini (YM)

Nasdaq 100 E-Mini (NQ)

Platin (PL)

Palladium (PA)

Aluminium (AUP)

Stahl ( HRC )

Ethanol (AEZ)

Brent Rohöl (J26)

Reis (ZR)

Hafer (ZO)

Milch (DL)

Orangensaft (JO)

Holz (LS)

Mastrinder (GF)

S&P 500 ( SP )

Dow Jones Industrial Average Index (DJIA)

Neuseeland Dollar (N6)

Open Interest-Buschi

English:

One part of the "Commitment of Traders-Report" is the Open Interest which is shown in this indicator (source: Quandl database).

The following futures are included:

30-year Bonds (ZB)

10-year Notes (ZN)

Soybeans (ZS)

Soybean Meal (ZM)

Soybean Oil (ZL)

Corn (ZC)

Soft Red Winter Wheat (ZW)

Hard Red Winter Wheat(KE)

Lean Hogs (HE)

Live Cattle (LE)

Gold (GC)

Silver (SI)

Copper (HG)

Crude Oil (CL)

Heating Oil (HO)

RBOB Gasoline (RB)

Natural Gas (NG)

Australian Dollar (A6)

British Pound (B6)

Canadian Dollar (D6)

Euro (E6)

Japanese Yen (J6)

Swiss Franc (S6)

Sugar (SB)

Coffee (KC)

Cocoa (CC)

Cotton (CT)

S&P 500 E-Mini (ES)

Russell 2000 E-Mini (RTY)

Dow Jones Industrial Mini (YM)

Nasdaq 100 E-Mini (NQ)

Platin (PL)

Palladium (PA)

Aluminium (AUP)

Steel (HRC)

Ethanol (AEZ)

Brent Crude Oil (J26)

Rice (ZR)

Oat (ZO)

Milk (DL)

Orange Juice (JO)

Lumber (LS)

Feeder Cattle (GF)

S&P 500 (SP)

Dow Jones Industrial Average Index (DJIA)

New Zealand Dollar (N6)

Deutsch:

Ein Bestandteil des "Commitment of Traders-Report" ist das Open Interest, das in diesem Indikator dargestellt wird (Quelle: Quandl Datenbank).

Folgende Futures sind enthalten:

30-jährige US-Staatsanleihen (ZB)

10-jährige US-Staatsanleihen (ZN)

Sojabohnen(ZS)

Sojabohnen-Mehl (ZM)

Sojabohnen-Öl (ZL)

Mais(ZC)

Soft Red Winter-Weizen (ZW)

Hard Red Winter-Weizen (KE)

Magerschweine (HE)

Lebendrinder (LE)

Gold (GC)

Silber (SI)

Kupfer(HG)

Rohöl (CL)

Heizöl (HO)

Benzin (RB)

Erdgas (NG)

Australischer Dollar (A6)

Britisches Pfund (B6)

Kanadischer Dollar (D6)

Euro (E6)

Japanischer Yen (J6)

Schweizer Franken (S6)

Zucker (SB)

Kaffee (KC)

Kakao (CC)

Baumwolle (CT)

S&P 500 E-Mini (ES)

Russell 2000 E-Mini (RTY)

Dow Jones Industrial Mini (YM)

Nasdaq 100 E-Mini (NQ)

Platin (PL)

Palladium (PA)

Aluminium (AUP)

Stahl (HRC)

Ethanol (AEZ)

Brent Rohöl (J26)

Reis (ZR)

Hafer (ZO)

Milch (DL)

Orangensaft (JO)

Holz (LS)

Mastrinder (GF)

S&P 500 (SP)

Dow Jones Industrial Average Index (DJIA)

Neuseeland Dollar (N6)

Drawdown and Max Drawdown

I needed to see what the max Drawdown was for a specific security, and so I wrote this script. Maybe others might also find it useful. Here I apply it to the Russel 2000 index. The Russel 2000 index has been gone down quite consistently recently. So someone might wonder how weird is that, and from this index you can see that we are still a long way before the bottom.

Everyday 0002 _ MAC 1st Trading Hour WalkoverThis is the second strategy for my Everyday project.

Like I wrote the last time - my goal is to create a new strategy everyday

for the rest of 2016 and post it here on TradingView.

I'm a complete beginner so this is my way of learning about coding strategies.

I'll give myself between 15 minutes and 2 hours to complete each creation.

This is basically a repetition of the first strategy I wrote - a Moving Average Crossover,

but I added a tiny thing.

I read that "Statistics have proven that the daily high or low is established within the first hour of trading on more than 70% of the time."

(source: )

My first Moving Average Crossover strategy, tested on VOLVB daily, got stoped out by the volatility

and because of this missed one nice bull run and a very nice bear run.

So I added this single line: if time("60", "1000-1600") regarding when to take exits:

if time("60", "1000-1600")

strategy.exit("Close Long", "Long", profit=2000, loss=500)

strategy.exit("Close Short", "Short", profit=2000, loss=500)

Sweden is UTC+2 so I guess UTC 1000 equals 12.00 in Stockholm. Not sure if this is correct, actually.

Anyway, I hope this means the strategy will only take exits based on price action which occur in the afternoon, when there is a higher probability of a lower volatility.

When I ran the new modified strategy on the same VOLVB daily it didn't get stoped out so easily.

On the other hand I'll have to test this on various stocks .

Reading and learning about how to properly test strategies is on my todo list - all tips on youtube videos or blogs

to read on this topic is very welcome!

Like I said the last time, I'm posting these strategies hoping to learn from the community - so any feedback, advice, or corrections is very much welcome and appreciated!

/pbergden

Currency Index Indicator The currency index represents the change in one currency by reference to all other

foreign currencies. The index is calculated by taking the average of the variations

in one currency by reference to the others. Represented in graphical form, it allows

for easy visualization of the individual trends in each currency.

The index of the currencies is a simple arithmetic average of the variation in each pair.

For each index, to have fixed the value 100 on 1 January 2000.

2nd 3rd 4th Order PivotsThis indicator calculates pivots of 2nd, 3rd and 4th order in the current timeframe.

The idea is borrowed from the book "The Art and Science of Technical Trading" by Adam Grimes:

"A pivot high is a bar that has a higher high than the bar that came before it and the bar that comes after it"

"Second-order pivot highs are first-order pivot highs that are preceded and followed by lower first-order pivot highs.

The type of picot calculation can be found as well in script "Higher Order Pivots" by rumpypumpydumpy. However, this script is different in the following ways:

1. Shows pivots of order 2, 3 and 4

2. The chart timeframe can be different than the pivot timeframe, allowing e.g. to map daily pivots to intraday charts via lines

3. Labels and/or lines can be used to show pivot points

4. Use of extended session data can be enabled/disabled, independently from the current chart settings

5. To disable older pivots, a starting time for the pivot calculation can be set

Please consider following limitations:

1. Maximum of 500 drawing objects per chart. Use Notification option to keep track of when running out of chart objects.

2. Lookback history: The max lookback history is limited by the currently selected timeframe. E.g. on a 5min timeframe, 20000 bars (Premium Plan) result in approx. 5 months of lookback period, meaning you may want to verify with a 30 min or higher chart to get a complete picture of pivots.