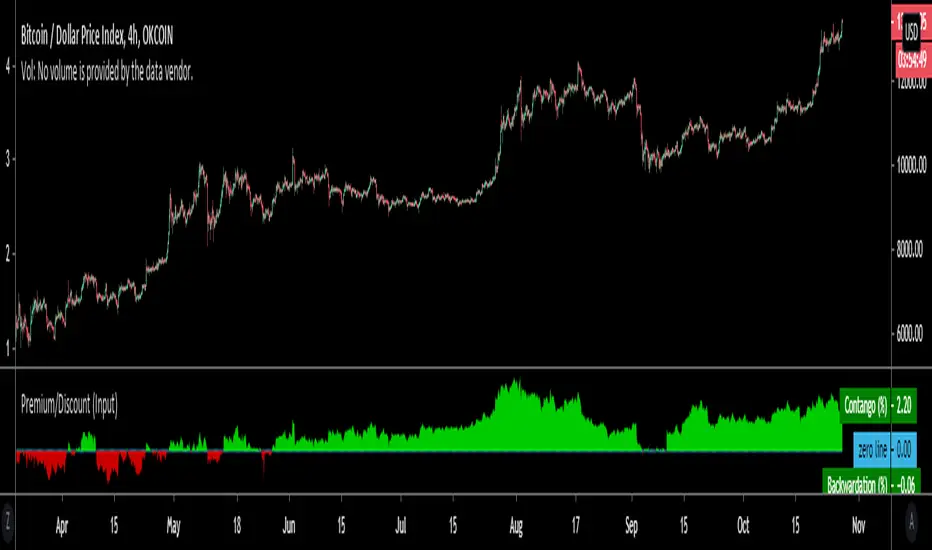

Premium/Discount (Input)Used to show Contango or Backwardation in futures contracts vs spot price. You can input your own tickers so can technically can be used to compare anything.

* In this example I'm showing Okex Quarterly contract vs Okex spot index price because it showcases it better.

* If you are using this after 2019 the default setting will not work because I set it to Bitmex which does not currently have a "current contract in front" ticker available.

It should be fairly self explanatory, but just ask below if you have any questions.

Buscar en scripts para "西班牙人VS奥萨苏纳"

Volume Profile Free Ultra SLI (100 Levels Value Area VWAP) - RRBVolume Profile Free Ultra SLI by RagingRocketBull 2019

Version 1.0

This indicator calculates Volume Profile for a given range and shows it as a histogram consisting of 100 horizontal bars.

This is basically the MAX SLI version with +50 more Pinescript v4 line objects added as levels.

It can also show Point of Control (POC), Developing POC, Value Area/VWAP StdDev High/Low as dynamically moving levels.

Free accounts can't access Standard TradingView Volume Profile, hence this indicator.

There are several versions: Free Pro, Free MAX SLI, Free Ultra SLI, Free History. This is the Free Ultra SLI version. The Differences are listed below:

- Free Pro: 25 levels, +Developing POC, Value Area/VWAP High/Low Levels, Above/Below Area Dimming

- Free MAX SLI: 50 levels, 2x SLI modes for Buy/Sell or even higher res 150 levels

- Free Ultra SLI: 100 levels, packed to the limit, 2x SLI modes for Buy/Sell or even higher res 300 levels

- Free History: auto highest/lowest, historic poc/va levels for each session

Features:

- High-Res Volume Profile with up to 100 levels (line implementation)

- 2x SLI modes for even higher res: 300 levels with 3x vertical SLI, 100 buy/sell levels with 2x horiz SLI

- Calculate Volume Profile on full history

- POC, Developing POC Levels

- Buy/Sell/Total volume modes

- Side Cover

- Value Area, VAH/VAL dynamic levels

- VWAP High/Low dynamic levels with Source, Length, StdDev as params

- Show/Hide all levels

- Dim Non Value Area Zones

- Custom Range with Highlighting

- 3 Anchor points for Volume Profile

- Flip Levels Horizontally

- Adjustable width, offset and spacing of levels

- Custom Color for POC/VA/VWAP levels, Transparency for buy/sell levels

WARNING:

- Compilation Time: 1 min 20 sec

Usage:

- specify max_level/min_level/spacing (required)

- select range (start_bar, range length), confirm with range highlighting

- select volume type: Buy/Sell/Total

- select mode Value Area/VWAP to show corresponding levels

- flip/select anchor point to position the buy/sell levels

- use Horiz Buy/Sell SLI mode with 100 or Vertical SLI with 300 levels if needed

- use POC/Developing POC/VA/VWAP High/Low as S/R levels. Usually daily values from 1-3 days back are used as levels for the current day.

SLI:

use SLI modes to extend the functionality of the indicator:

- Horiz Buy/Sell 2x SLI lets you view 100 Buy/Sell Levels at the same time

- Vertical Max_Vol 3x SLI lets you increase the resolution to 300 levels

- you need at least 2 instances of the indicator attached to the same chart for SLI to work

1) Enable Horiz SLI:

- attach 2 indicator instances to the chart

- make sure all instances have the same min_level/max_level/range/spacing settings

- select volume type for each instance: you can have a buy/sell or buy/total or sell/total SLI. Make sure your buy volume instance is the last attached to be displayed on top of sell/total instances without overlapping.

- set buy_sell_sli_mode to true for indicator instances with volume_type = buy/sell, for type total this is optional.

- this basically tells the script to calculate % lengths based on total volume instead of individual buy/sell volumes and use ext offset for sell levels

- Sell Offset is calculated relative to Buy Offset to stack/extend sell after buy. Buy Offset = Zero - Buy Length. Sell Offset = Buy Offset - Sell Length = Zero - Buy Length - Sell Length

- there are no master/slave instances in this mode, all indicators are equal, poc/va levels are not affected and can work independently, i.e. one instance can show va levels, another - vwap.

2) Enable Vertical SLI:

- attach the first instance and evaluate the full range to roughly determine where is the highest max_vol/poc level i.e. 0..20000, poc is in the bottom half (third, middle etc) or

- add more instances and split the full vertical range between them, i.e. set min_level/max_level of each corresponding instance to 0..10000, 10000..20000 etc

- make sure all instances have the same range/spacing settings

- an instance with a subrange containing the poc level of the full range is now your master instance (bottom half). All other instances are slaves, their levels will be calculated based on the max_vol/poc of the master instance instead of local values

- set show_max_vol_sli to true for the master instance. for slave instances this is optional and can be used to check if master/slave max_vol values match and slave can read the master's value. This simply plots the max_vol value

- you can also attach all instances and set show_max_vol_sli to true in all of them - the instance with the largest max_vol should become the master

Auto/Manual Ext Max_Vol Modes:

- for auto vertical max_vol SLI mode set max_vol_sli_src in all slave instances to the max_vol of the master indicator: "VolumeProfileFree_MAX_RRB: Max Volume for Vertical SLI Mode". It can be tricky with 2+ instances

- in case auto SLI mode doesn't work - assign max_vol_sli_ext in all slave instances the max_vol value of the master indicator manually and repeat on each change

- manual override max_vol_sli_ext has higher priority than auto max_vol_sli_src when both values are assigned, when they are 0 and close respectively - SLI is disabled

- master/slave max_vol values must match on each bar at all times to maintain proper level scale, otherwise slave's levels will look larger than they should relative to the master's levels.

- Max_vol (red) is the last param in the long list of indicator outputs

- the only true max_vol/poc in this SLI mode is the master's max_vol/poc. All poc/va levels in slaves will be irrelevant and are disabled automatically. Slaves can only show VWAP levels.

- VA Levels of the master instance in this SLI mode are calculated based on the subrange, not the whole range and may be inaccurate. Cross check with the full range.

WARNING!

- auto mode max_vol_sli_src is experimental and may not work as expected

- you can only assign auto mode max_vol_sli_src = max_vol once due to some bug with unhandled exception/buffer overflow in Tradingview. Seems that you can clear the value only by removing the indicator instance

- sometimes you may see a "study in error state" error when attempting to set it back to close. Remove indicator/Reload chart and start from scratch

- volume profile may not finish to redraw and freeze in an ugly shape after an UI parameter change when max_vol_sli_src is assigned a max_vol value. Assign it to close - VP should redraw properly, but it may not clear the assigned max_vol value

- you can't seem to be able to assign a proper auto max_vol value to the 3rd slave instance

- 2x Vertical SLI works and tested in both auto/manual, 3x SLI - only manual seems to work (you can have a mixed mode: 2nd instance - auto, 3rd - manual)

Notes:

- This code uses Pinescript v3 compatibility framework

- This code is 20x-30x faster (main for cycle is removed) especially on lower tfs with long history - only 4-5 sec load/redraw time vs 30-60 sec of the old Pro versions

- Instead of repeatedly calculating the total sum of volumes for the whole range on each bar, vol sums are now increased on each bar and passed to the next in the range making it a per range vs per bar calculation that reduces time dramatically

- 100 levels consist of 50 main plot levels and 50 line objects used as alternate levels, differences are:

- line objects are always shown on top of other objects, such as plot levels, zero line and side cover, it's not possible to cover/move them below.

- all line objects have variable lengths, use actual x,y coords and don't need side cover, while all plot levels have a fixed length of 100 bars, use offset and require cover.

- all key properties of line objects, such as x,y coords, color can be modified, objects can be moved/deleted, while this is not possible for static plot levels.

- large width values cause line objects to expand only up/down from center while their length remains the same and stays within the level's start/end points similar to an area style.

- large width values make plot levels expand in all directions (both h/v), beyond level start/end points, sometimes overlapping zero line, making them an inaccurate % length representation, as opposed to line objects/plot levels with area style.

- large width values translate into different widths on screen for line objects and plot levels.

- you can't compensate for this unwanted horiz width expansion of plot levels because width uses its own units, that don't translate into bars/pixels.

- line objects are visible only when num_levels > 50, plot levels are used otherwise

- Since line objects are lines, plot levels also use style line because other style implementations will break the symmetry/spacing between levels.

- if you don't see a volume profile check range settings: min_level/max_level and spacing, set spacing to 0 (or adjust accordingly based on the symbol's precision, i.e. 0.00001)

- you can view either of Buy/Sell/Total volumes, but you can't display Buy/Sell levels at the same time using a single instance (this would 2x reduce the number of levels). Use 2 indicator instances in horiz buy/sell sli mode for that.

- Volume Profile/Value Area are calculated for a given range and updated on each bar. Each level has a fixed length. Offsets control visible level parts. Side Cover hides the invisible parts.

- Custom Color for POC/VA/VWAP levels - UI Style color/transparency can only change shape's color and doesn't affect textcolor, hence this additional option

- Custom Width - UI Style supports only width <= 4, hence this additional option

- POC is visible in both modes. In VWAP mode Developing POC becomes VWAP, VA High and Low => VWAP High and Low correspondingly to minimize the number of plot outputs

- You can't change buy/sell level colors from input (only transparency) - this requires 2x plot outputs => 2x reduces the number of levels to fit the max 64 limit. That's why 2 additional plots are used to dim the non Value Area zones

- You can change level transparency of line objects. Due to Pinescript limitations, only discrete values are supported.

- Inverse transp correlation creates the necessary illusion of "covered" line objects, although they are shown on top of the cover all the time

- If custom lines_transp is set the illusion will break because transp range can't be skewed easily (i.e. transp 0..100 is always mapped to 100..0 and can't be mapped to 50..0)

- transparency can applied to lines dynamically but nva top zone can't be completely removed because plot/mixed type of levels are still used when num_levels < 50 and require cover

- transparency can't be applied to plot levels dynamically from script this can be done only once from UI, and you can't change plot color for the past length bars

- All buy/sell volume lengths are calculated as % of a fixed base width = 100 bars (100%). You can't set show_last from input to change it

- Range selection/Anchoring is not accurate on charts with time gaps since you can only anchor from a point in the future and measure distance in time periods, not actual bars, and there's no way of knowing the number of future gaps in advance.

- Adjust Width for Log Scale mode now also works on high precision charts with small prices (i.e. 0.00001)

- in Adjust Width for Log Scale mode Level1 width extremes can be capped using max deviation (when level1 = 0, shift = 0 width becomes infinite)

- There's no such thing as buy/sell volume, there's just volume, but for the purposes of the Volume Profile method, assume: bull candle = buy volume, bear candle = sell volume

P.S. I am your grandfather, Luke! Now, join the Dark Side in your father's steps or be destroyed! Once more the Sith will rule the Galaxy, and we shall have peace...

Hull MA and Candle crossHull MA vs price cossover . not 2 Hull MA's crossing, and also a price vs previous price crossover :

current price higher than previous = buy

current price lower than previous = sell

Price value set to OPEN to avoid repaint during candle

Volume Profile Free MAX SLI (50 Levels Value Area VWAP) by RRBVolume Profile Free MAX SLI by RagingRocketBull 2019

Version 1.0

All available Volume Profile Free MAX SLI versions are listed below (They are very similar and I don't want to publish them as separate indicators):

ver 1.0: style columns implementation

ver 2.0: style histogram implementation

ver 3.0: style line implementation

This indicator calculates Volume Profile for a given range and shows it as a histogram consisting of 50 horizontal bars.

It can also show Point of Control (POC), Developing POC, Value Area/VWAP StdDev High/Low as dynamically moving levels.

Free accounts can't access Standard TradingView Volume Profile, hence this indicator.

There are several versions: Free Pro, Free MAX SLI, Free History. This is the Free MAX SLI version. The Differences are listed below:

- Free Pro: 25 levels, +Developing POC, Value Area/VWAP High/Low Levels, Above/Below Area Dimming

- Free MAX SLI: 50 levels, packed to the limit, 2x SLI modes for Buy/Sell or even higher res 150 levels

- Free History: auto highest/lowest, historic poc/va levels for each session

Features:

- High-Res Volume Profile with up to 50 levels (3 implementations)

- 20-30x faster than the old Pro versions especially on lower tfs with long history

- 2x SLI modes for even higher res: 150 levels with 3x vertical SLI, 50 buy/sell levels with 2x horiz SLI

- Calculate Volume Profile on full history

- POC, Developing POC Levels

- Buy/Sell/Total volume modes

- Side Cover

- Value Area, VAH/VAL dynamic levels

- VWAP High/Low dynamic levels with Source, Length, StdDev as params

- Show/Hide all levels

- Dim Non Value Area Zones

- Custom Range with Highlighting

- 3 Anchor points for Volume Profile

- Flip Levels Horizontally

- Adjustable width, offset and spacing of levels

- Custom Color for POC/VA/VWAP levels and Transparency for buy/sell levels

Usage:

- specify max_level/min_level/spacing (required)

- select range (start_bar, range length), confirm with range highlighting

- select volume type: Buy/Sell/Total

- select mode Value Area/VWAP to show corresponding levels

- flip/select anchor point to position the buy/sell levels

- use Horiz SLI mode for 50 Buy/Sell or Vertical SLI for 150 levels if needed

- use POC/Developing POC/VA/VWAP High/Low as S/R levels. Usually daily values from 1-3 days back are used as levels for the current day.

SLI:

- use SLI modes to extend the functionality of the indicator:

- Horiz Buy/Sell 2x SLI lets you view 50 Buy/Sell Levels at the same time

- Vertical Max_Vol 3x SLI lets you increase the resolution to 150 levels

- you need at least 2 instances of the indicator attached to the same chart for SLI to work

1) Enable Horiz SLI:

- attach 2 indicator instances to the chart

- make sure all instances have the same min_level/max_level/range/spacing settings

- select volume type for each instance: you can have a buy/sell or buy/total or sell/total SLI. Make sure your buy volume instance is the last attached to be displayed on top of sell/total instances without overlapping.

- set buy_sell_sli_mode to true for indicator instances with volume_type = buy/sell, for type total this is optional.

- this basically tells the script to calculate % lengths based on total volume instead of individual buy/sell volumes and use ext offset for sell levels

- Sell Offset is calculated relative to Buy Offset to stack/extend sell after buy. Buy Offset = Zero - Buy Length. Sell Offset = Buy Offset - Sell Length = Zero - Buy Length - Sell Length

- there are no master/slave instances in this mode, all indicators are equal, poc/va levels are not affected and can work independently, i.e. one instance can show va levels, another - vwap.

2) Enable Vertical SLI:

- attach the first instance and evaluate the full range to roughly determine where is the highest max_vol/poc level i.e. 0..20000, poc is in the bottom half (third, middle etc) or

- add more instances and split the full vertical range between them, i.e. set min_level/max_level of each corresponding instance to 0..10000, 10000..20000 etc

- make sure all instances have the same range/spacing settings

- an instance with a subrange containing the poc level of the full range is now your master instance (bottom half). All other instances are slaves, their levels will be calculated based on the max_vol/poc of the master instance instead of local values

- set show_max_vol_sli to true for the master instance. for slave instances this is optional and can be used to check if master/slave max_vol values match and slave can read the master's value. This simply plots the max_vol value

- you can also attach all instances and set show_max_vol_sli to true in all of them - the instance with the largest max_vol should become the master

Auto/Manual Ext Max_Vol Modes:

- for auto vertical max_vol SLI mode set max_vol_sli_src in all slave instances to the max_vol of the master indicator: "VolumeProfileFree_MAX_RRB: Max Volume for Vertical SLI Mode". It can be tricky with 2+ instances

- in case auto SLI mode doesn't work - assign max_vol_sli_ext in all slave instances the max_vol value of the master indicator manually and repeat on each change

- manual override max_vol_sli_ext has higher priority than auto max_vol_sli_src when both values are assigned, when they are 0 and close respectively - SLI is disabled

- master/slave max_vol values must match on each bar at all times to maintain proper level scale, otherwise slave's levels will look larger than they should relative to the master's levels.

- Max_vol (red) is the last param in the long list of indicator outputs

- the only true max_vol/poc in this SLI mode is the master's max_vol/poc. All poc/va levels in slaves will be irrelevant and are disabled automatically. Slaves can only show VWAP levels.

- VA Levels of the master instance in this SLI mode are calculated based on the subrange, not the whole range. Cross check with the full range.

WARNING!

- auto mode max_vol_sli_src is experimental and may not work as expected

- you can only assign auto mode max_vol_sli_src = max_vol once due to some bug with unhandled exception/buffer overflow in Tradingview. Seems that you can clear the value only by removing the indicator instance

- sometimes you may see a "study in error state" error when attempting to set it back to close. Remove indicator/Reload chart and start from scratch

- volume profile may not finish to redraw and freeze in an ugly shape after an UI parameter change when max_vol_sli_src is assigned a max_vol value. Assign it to close - VP should redraw properly, but it may not clear the assigned max_vol value

- you can't seem to be able to assign a proper auto max_vol value to the 3rd slave instance

- 2x Vertical SLI works and tested in both auto/manual, 3x SLI - only manual seems to work

Notes:

- This code is 20x-30x faster (main for cycle is removed) especially on lower tfs with long history - only 2-3 sec load/redraw time vs 30-60 sec of the old Pro versions

- Instead of repeatedly calculating the total sum of volumes for the whole range on each bar, vol sums are now increased on each bar and passed to the next in the range making it a per range vs per bar calculation that reduces time dramatically

- hist_base for levels still results is ugly redraw

- if you don't see a volume profile check range settings: min_level/max_level and spacing, set spacing to 0 (or adjust accordingly based on the symbol's precision, i.e. 0.00001)

- you can view either of Buy/Sell/Total volumes, but you can't display Buy/Sell levels at the same time using a single instance (this would 2x reduce the number of levels). Use 2 indicator instances in horiz buy/sell sli mode for that.

- Volume Profile/Value Area are calculated for a given range and updated on each bar. Each level has a fixed length. Offsets control visible level parts. Side Cover hides the invisible parts.

- Custom Color for POC/VA/VWAP levels - UI Style color/transparency can only change shape's color and doesn't affect textcolor, hence this additional option

- Custom Width - UI Style supports only width <= 4, hence this additional option

- POC is visible in both modes. In VWAP mode Developing POC becomes VWAP, VA High and Low => VWAP High and Low correspondingly to minimize the number of plot outputs

- You can't change buy/sell level colors from input (only plot transparency) - this requires 2x plot outputs => 2x reduces the number of levels to fit the max 64 limit. That's why 2 additional plots are used to dim the non Value Area zones

- All buy/sell volume lengths are calculated as % of a fixed base width = 100 bars (100%). You can't set show_last from input to change it

- There's no such thing as buy/sell volume, there's just volume, but for the purposes of the Volume Profile method, assume: bull candle = buy volume, bear candle = sell volume

P.S. Gravitonium Levels Are Increasing. Unobtainium is nowhere to be found!

Links on Volume Profile and Value Area calculation and usage:

www.tradingview.com

stockcharts.com

onlinelibrary.wiley.com

Bitfinex Margin ComparisonDisplays the RSI of Longs vs Shorts from Bitfinex for most majors ( BTC , ETH, LTC, XRP, EOS, NEO).

Displays RSI of both longs and shorts to gauge the short term momentum of both while also showing the ratio of Longs vs Shorts as the background.

Premium ComparisonScript to display futures premium/discount vs basis; uses Bitmex XBTUSD 10.99% as basis vs XBTM18 and XBTU18 futures , but these are configurable.

ST_Trend_ReversalSTRONG TREND REVERSAL INDICATOR

The code is the percentage difference between the spot price of a given financial asset and its 200-day MA of that period. My standard setup is Daily, and I think it's got very good predictive power at that timeframe.

It can be read in two ways:

1. Values extremely above or below the 200-period MA present chances of buying/selling agains the prevailing trend.

2. Values closely above or below the 200-period MA are make-or-break market periods, where a medium-term trend becomes evident. Breaks above or below the MA are associated with strong chances of directional movements. But it's not fool-proof as false breaks have become commonplace nowadays.

Other way to use it is as confirmation of breakdowns: For example, an asset that loses its 200-day MA and then can't rally above it becomes exposed to steep losses afterwards.

It's also helpful to use in volatility trading: the closer the asset goes to its MA, the lower goes implied vol, and thus better opportiunities to be long volatility on those occasions where direction is hard to predict.

STRI = close/(200dMA)

Values over 100 indicate percentage premiums of spot vs its moving average.

Values below indicate percentage discounts of spot vs its moving average.

Ersoy-intersection(Kesisme)-Update-1website: www.ersoytoptas.com

Newspaper : tr.investing.com

hi , Friends

i wanna be someone who wants to help everyone

updated my script he published some time ago.

What happened?

* intersection When ever Bar Color Yellow Be

* Alarms to be more comprehensible

* Short and Long Days Choosing a Opportunities

* Source Opportunities

All Charts Usable( Example ;15,30,60 ... vs) and ALL MARKETS ( Stocks , forex , ... vs)

i strive to improve further

Easy to get

Triple 9 Bias filter Triple 9 Bias – Precision Multi-Timeframe Directional Filter

Technical Overview

The Triple 9 Bias is a precision multi-timeframe directional filter built exclusively for 5-minute (and lower) trading.

It stacks three EMA-9 trend directions (4H + 1H + 15m) as Primary confluence and uses only the 4H RSI-14 as Secondary confirmation.

Integrity Check: Zero repaint · Zero lookahead · Works identically on any chart timeframe.

The Trading Rule (Simple)

Long Trades: Only trade longs when all three EMA-9s are UP + 4H RSI > 50

Short Trades: Only trade shorts when all three EMA-9s are DOWN + 4H RSI < 50

Otherwise — stand aside.

Display Components

A. Plotted Higher-Timeframe EMAs (No Repainting)

All values are pulled from closed higher-timeframe bars.

4H EMA 9 (Red step-line)

1H EMA 9 (Purple step-line)

15m EMA 9 (Orange step-line)

B. Locked Dashboard (Bottom-Right)

Clean table split into Primary and Secondary sections for instant bias reading.

Colour Logic:

🟢 Lime = UP / BUY

🔴 Red = DOWN / SELL

Background Logic:

Full Green: Only when all three EMA-9s are UP

Full Red: Only when all three EMA-9s are DOWN

Gray: Otherwise = no trade

Indicator Breakdown

3.1. Primary Confluence – EMA 9 Slope

4H EMA 9 direction (compared 10 bars back)

1H EMA 9 direction (compared 6 bars back)

15m EMA 9 direction (compared 6 bars back)

3.2. Secondary Confluence

4H RSI-14 vs 50 level (BUY if >50, SELL if <50)

High-Probability Signal: When Primary = all three “UP” and Secondary = “BUY” → highest-probability bullish bias (and vice-versa for bearish).

Distância Preço vs VWAPIt calculates the distance from the price to the VWAP. The idea is to make it easier to observe when the price might return to the VWAP.

XAUUSD Multi-Timeframe Bias Scanner🎯 Purpose & Overview

This is a sophisticated trading indicator that analyzes XAUUSD (Gold) across 5 different timeframes simultaneously to determine market bias and trend direction.

⚙️ Core Components

2. Bias Calculation Engine

The heart of the indicator uses 5 technical factors to score each timeframe:

Technical Factors (Weighted):

Moving Average Alignment (30 points)

Bullish: EMA(9) > EMA(21) > EMA(50)

Bearish: EMA(9) < EMA(21) < EMA(50)

Price vs MA Position (20 points)

Score increases when price above MAs

Score decreases when price below MAs

RSI Momentum (20 points)

Bullish: RSI > 60 or > 50

Bearish: RSI < 40 or < 50

MACD Signals (15 points)

Bullish: MACD line > Signal line AND > 0

Bearish: MACD line < Signal line AND < 0

Volume Confirmation (15 points)

Volume spikes with price movement add confirmation

📊 Timeframe Analysis

Five Timeframes Monitored:

5-minute - Short-term noise (10% weight)

15-minute - Intraday direction (15% weight)

1-hour - Key intraday bias (25% weight)

4-hour - Primary directional bias (30% weight)

1-day - Overall trend context (20% weight)

Bias Scoring System:

0-100 Scale (50 = Neutral)

STRONG BULLISH: ≥70 (Green)

BULLISH: 55-69 (Lime)

NEUTRAL: 46-54 (Gray)

BEARISH: 31-45 (Orange)

STRONG BEARISH: ≤30 (Red)

🎨 Visual Features

1. Comprehensive Table Display

pinescript

var table biasTable = table.new(position.top_right, 3, 7, ...)

Shows a color-coded table with:

Timeframe name

Numerical bias score (0-100)

Strength description with color coding

2. Chart Visual Indicators

Background coloring based on overall bias

Label markers for strong bullish/bearish conditions

Real-time label showing all timeframe scores

3. Alert System

Triggers when overall bias crosses 70 (bullish) or 30 (bearish)

Configurable with sound options

🔄 How It Processes Data

Data Flow:

Requests security data for each timeframe using request.security()

Calculates technical indicators for each TF separately

Scores each TF based on 5 technical factors

Computes weighted overall bias

Updates visual displays and checks alert conditions

💡 Trading Applications

Bullish Scenarios:

Multiple timeframes show bullish alignment

Higher timeframe bias supports lower timeframe direction

Overall score > 70 indicates strong bullish conviction

Bearish Scenarios:

Multiple timeframes show bearish alignment

Higher timeframe bias confirms lower timeframe moves

Overall score < 30 indicates strong bearish conviction

Conflict Detection:

When timeframes show conflicting biases

Caution required - market may be consolidating

Wait for alignment before taking trades

🎚️ Customization Options

Users can modify:

Timeframe weights

Technical indicator parameters

Alert thresholds

Visual display preferences

Scoring sensitivity

📈 XAUUSD Specific Optimizations

The indicator considers Gold's unique characteristics:

High volatility periods

ATR-based volatility adjustments

Volume confirmation for breakouts

Multiple timeframe confirmation for trend reliability

This creates a powerful tool for identifying high-probability trade setups in XAUUSD by ensuring traders have a complete multi-timeframe perspective before entering positions.

Scaling_mastery:Free TrendlinesScaling_mastery Trendlines is a clean, trading-ready smart trendline tool built for the Scaling_mastery community.

It automatically finds swing highs/lows and draws dynamic trendlines or channels that stay locked to price, on any symbol and any timeframe.

🔧 Modes

Trendline type

Wicks – classic trendlines anchored on candle wicks (high/low).

Bodies – trendlines anchored on candle bodies (open/close), great for closing structure.

Channel – 3-line channel:

outer lines form a band around price

middle line runs through the centre of the channel

thickness is adjustable (Small / Medium / Large).

Trend strength

Controls how strong the pivots must be to form a line.

Weak → more lines, reacts faster.

Medium → balanced, good for most pairs.

Strong → only the cleanest swings, higher-probability trendlines.

🎨 Visual controls

Max support / resistance lines – cap how many lines are kept on chart.

Show broken lines – hide broken trendlines or keep them for structure history.

Extend lines – None / Right / Both.

Support / Resistance colors – separate colors for active vs broken.

Channel thickness – Small / Medium / Large (0.5% / 1% / 2% of price).

Channel outer lines – color for channel edges.

Channel middle line – color + style (dotted / dashed / solid).

Broken lines are automatically faded + dotted, so you can instantly see what’s still respected and what’s already been taken out.

🧠 How to use

Add the indicator to any chart.

Start with:

Trendline type: Wicks

Trend strength: Strong

Max lines: 1–2 for both support & resistance

Once you like the behavior, experiment with:

Switching between Wicks / Bodies / Channel

Adjusting Channel thickness and Trend strength

Use the lines as a visual confluence tool with your own strategy:

HTF trend direction

LTF entries / retests

Liquidity grabs around broken lines

This script doesn’t generate entries or risk management – it’s designed to give you clean, reliable structure so you can execute your own edge.

⚠️ Disclaimer

This tool is for educational and visual purposes only and is not financial advice.

Always do your own research and manage risk.

BTC GOD — DEFINITIVE BTC MULTI INDICATORBTC GOD — The Ultimate Bitcoin Cycle Indicator (2025 Edition)

The one indicator every serious BTC holder and trader has been waiting for.

A single script that perfectly combines the 5 most powerful and accurate Bitcoin indicators ever created — all 100 % official versions:

- Official Pi Cycle Top (LookIntoBitcoin) → in 2013, 2017 & 2021 (3/3 hits)

- Official MVRV Z-Score (Glassnode / LookIntoBitcoin) → every major bottom (2015, 2018–19, 2022)

- Dynamic Bull/Bear background (red bear-market when price drops X % from cycle ATH + monthly RSI filter)

- Monthly Golden/Death Cross (50-month EMA vs 200-week EMA) → huge, unmistakable signals

- SuperTrend + 200-week EMA + 50-month EMA

- Cycle ATH/ATL tracking with flashing alert in the table when new highs/lows are made

- Exact days to/from the next halving + optimal accumulation zone (200–750 days post-halving)

- Fully customizable inputs for experienced traders

Zero repainting. Zero errors. Works on every timeframe.

This is the indicator used by people who truly understand Bitcoin’s 4-year cycles.

If you could only keep ONE Bitcoin indicator for the rest of your life… this would be it.

Save it, test it, and you’ll instantly see why it’s called BTC GOD.

Built with love and obsession for Bitcoin cycles.

Last update: November 2025

Average True Range % infoATR% is a modified version of the classic Average True Range indicator that displays price volatility as a percentage of the instrument's value, rather than in absolute values. This allows you to easily compare the volatility of different assets (e.g., Bitcoin vs Tesla stock) regardless of their price.

Main Features

1. ATR% Chart

The red line shows the average volatility from the last N candles (default 14), expressed as a percentage. For example:

ATR% = 2.5% means that the average daily move is approximately 2.5% of the asset's value

Higher values = greater volatility (higher profit potential, but also greater risk)

Lower values = lower volatility (calmer market)

2. Volatility Trend Analysis

The indicator automatically detects whether volatility is rising, falling, or stable:

Up arrow (↑) - volatility is rising (price becomes more "nervous")

Down arrow (↓) - volatility is falling (market is calming down)

Horizontal arrow (⮆) - volatility is stable (within ±3% of the moving average)

3. Information Table

In the upper right corner of the chart you will see Current ATR% value and Trend arrow with color coding:

- Green = rising volatility

- Red = falling volatility

- Gray = stable volatility

Parameters to Configure

Indicator Length (default: 14) - How many candles back to include in calculations:

Lower values (5-10): more sensitive to sudden changes, reacts faster

Higher values (20-30): more smoothed, shows long-term volatility picture

Trend Length (default: 10) - Period to analyze whether volatility is rising/falling:

Lower values: faster trend change signals

Higher values: more reliable, but slower signals

Sample Interpretations

ATR% Volatility Asset Type/Situation

< 1% Very low Stable blue-chip stocks, calm market

1-3% Low-medium Typical stocks, normal conditions

3-5% Medium-high Volatile stocks, cryptocurrencies at rest

5-10% High Cryptocurrencies, penny stocks

> 10% Extremely high Market panic, crash, pump & dump

Đại Ka 3 ATR BandsĐại Ka 3 ATR Bands – The ultimate single-slot indicator that replaces three separate ATR plots.

Designed specifically for ICT/SMC traders in 2025:

• Light red band (±0.5 ATR) → fake moves, Judas Swing, Turtle Soup zone

• Gray band (±1.0 ATR) → normal price action

• Light green band (±2.0 ATR) → real displacement zone → Silver Bullet, SFT, high-probability entries

How to use:

– Price stuck inside red band → expect reversal/fakeout

– Price breaks and closes outside green band + volume spike → enter aggressively in that direction (85%+ win-rate inside Killzones)

Default ATR(14), subtle fills for instant visual filtering of real vs fake moves.

Perfect companion for Order Blocks, FVG, Breaker Blocks and NY/London Killzones.

Free forever – coded with love by Đại Ka & Vietnamese ICT crew.

Static K-means Clustering | InvestorUnknownStatic K-Means Clustering is a machine-learning-driven market regime classifier designed for traders who want a data-driven structure instead of subjective indicators or manually drawn zones.

This script performs offline (static) K-means training on your chosen historical window. Using four engineered features:

RSI (Momentum)

CCI (Price deviation / Mean reversion)

CMF (Money flow / Strength)

MACD Histogram (Trend acceleration)

It groups past market conditions into K distinct clusters (regimes). After training, every new bar is assigned to the nearest cluster via Euclidean distance in 4-dimensional standardized feature space.

This allows you to create models like:

Regime-based long/short filters

Volatility phase detectors

Trend vs. chop separation

Mean-reversion vs. breakout classification

Volume-enhanced money-flow regime shifts

Full machine-learning trading systems based solely on regimes

Note:

This script is not a universal ML strategy out of the box.

The user must engineer the feature set to match their trading style and target market.

K-means is a tool, not a ready made system, this script provides the framework.

Core Idea

K-means clustering takes raw, unlabeled market observations and attempts to discover structure by grouping similar bars together.

// STEP 1 — DATA POINTS ON A COORDINATE PLANE

// We start with raw, unlabeled data scattered in 2D space (x/y).

// At this point, nothing is grouped—these are just observations.

// K-means will try to discover structure by grouping nearby points.

//

// y ↑

// |

// 12 | •

// | •

// 10 | •

// | •

// 8 | • •

// |

// 6 | •

// |

// 4 | •

// |

// 2 |______________________________________________→ x

// 2 4 6 8 10 12 14

//

//

//

// STEP 2 — RANDOMLY PLACE INITIAL CENTROIDS

// The algorithm begins by placing K centroids at random positions.

// These centroids act as the temporary “representatives” of clusters.

// Their starting positions heavily influence the first assignment step.

//

// y ↑

// |

// 12 | •

// | •

// 10 | • C2 ×

// | •

// 8 | • •

// |

// 6 | C1 × •

// |

// 4 | •

// |

// 2 |______________________________________________→ x

// 2 4 6 8 10 12 14

//

//

//

// STEP 3 — ASSIGN POINTS TO NEAREST CENTROID

// Each point is compared to all centroids.

// Using simple Euclidean distance, each point joins the cluster

// of the centroid it is closest to.

// This creates a temporary grouping of the data.

//

// (Coloring concept shown using labels)

//

// - Points closer to C1 → Cluster 1

// - Points closer to C2 → Cluster 2

//

// y ↑

// |

// 12 | 2

// | 1

// 10 | 1 C2 ×

// | 2

// 8 | 1 2

// |

// 6 | C1 × 2

// |

// 4 | 1

// |

// 2 |______________________________________________→ x

// 2 4 6 8 10 12 14

//

// (1 = assigned to Cluster 1, 2 = assigned to Cluster 2)

// At this stage, clusters are formed purely by distance.

Your chosen historical window becomes the static training dataset , and after fitting, the centroids never change again.

This makes the model:

Predictable

Repeatable

Consistent across backtests

Fast for live use (no recalculation of centroids every bar)

Static Training Window

You select a period with:

Training Start

Training End

Only bars inside this range are used to fit the K-means model. This window defines:

the market regime examples

the statistical distributions (means/std) for each feature

how the centroids will be positioned post-trainin

Bars before training = fully transparent

Training bars = gray

Post-training bars = full colored regimes

Feature Engineering (4D Input Vector)

Every bar during training becomes a 4-dimensional point:

This combination balances: momentum, volatility, mean-reversion, trend acceleration giving the algorithm a richer "market fingerprint" per bar.

Standardization

To prevent any feature from dominating due to scale differences (e.g., CMF near zero vs CCI ±200), all features are standardized:

standardize(value, mean, std) =>

(value - mean) / std

Centroid Initialization

Centroids start at diverse coordinates using various curves:

linear

sinusoidal

sign-preserving quadratic

tanh compression

init_centroids() =>

// Spread centroids across using different shapes per feature

for c = 0 to k_clusters - 1

frac = k_clusters == 1 ? 0.0 : c / (k_clusters - 1.0) // 0 → 1

v = frac * 2 - 1 // -1 → +1

array.set(cent_rsi, c, v) // linear

array.set(cent_cci, c, math.sin(v)) // sinusoidal

array.set(cent_cmf, c, v * v * (v < 0 ? -1 : 1)) // quadratic sign-preserving

array.set(cent_mac, c, tanh(v)) // compressed

This makes initial cluster spread “random” even though true randomness is hardly achieved in pinescript.

K-Means Iterative Refinement

The algorithm repeats these steps:

(A) Assignment Step, Each bar is assigned to the nearest centroid via Euclidean distance in 4D:

distance = sqrt(dx² + dy² + dz² + dw²)

(B) Update Step, Centroids update to the mean of points assigned to them. This repeats iterations times (configurable).

LIVE REGIME CLASSIFICATION

After training, each new bar is:

Standardized using the training mean/std

Compared to all centroids

Assigned to the nearest cluster

Bar color updates based on cluster

No re-training occurs. This ensures:

No lookahead bias

Clean historical testing

Stable regimes over time

CLUSTER BEHAVIOR & TRADING LOGIC

Clusters (0, 1, 2, 3…) hold no inherent meaning. The user defines what each cluster does.

Example of custom actions:

Cluster 0 → Cash

Cluster 1 → Long

Cluster 2 → Short

Cluster 3+ → Cash (noise regime)

This flexibility means:

One trader might have cluster 0 as consolidation.

Another might repurpose it as a breakout-loading zone.

A third might ignore 3 clusters entirely.

Example on ETHUSD

Important Note:

Any change of parameters or chart timeframe or ticker can cause the “order” of clusters to change

The script does NOT assume any cluster equals any actionable bias, user decides.

PERFORMANCE METRICS & ROC TABLE

The indicator computes average 1-bar ROC for each cluster in:

Training set

Test (live) set

This helps measure:

Cluster profitability consistency

Regime forward predictability

Whether a regime is noise, trend, or reversion-biased

EQUITY SIMULATION & FEES

Designed for close-to-close realistic backtesting.

Position = cluster of previous bar

Fees applied only on regime switches. Meaning:

Staying long → no fee

Switching long→short → fee applied

Switching any→cash → fee applied

Fee input is percentage, but script already converts internally.

Disclaimers

⚠️ This indicator uses machine-learning but does not predict the future. It classifies similarity to past regimes, nothing more.

⚠️ Backtest results are not indicative of future performance.

⚠️ Clusters have no inherent “bullish” or “bearish” meaning. You must interpret them based on your testing and your own feature engineering.

Chop Meter + Trade Filter 1H/30M/15M (Ace PROFILE CLEAN v2)What this indicator does

Name: Chop Meter + Trade Filter 1H/30M/15M (Ace PROFILE CLEAN v2)

This is not an entry signal indicator. It’s a market condition filter:

It checks how compressed or expanded price is on

1H, 30M, and 15M.

It labels each TF as CHOP or NORMAL.

If 2 or more of those are in CHOP, it prints NO TRADE.

If 0 or 1 are in CHOP, it prints TRADE.

You use it to answer one question:

“Is this a session I should be pushing the button,

or is this a day to sit on my hands?”

How it works (simple version)

For each timeframe (1H, 30M, 15M), the script:

Looks back N bars (ATR length).

Measures:

ATR over N bars

Price range over N bars (highest high − lowest low)

Computes a compression value:

compression = ATR / range.

Then it compares that to the Threshold:

If compression > threshold → CHOP (market boxed / compressed)

If compression ≤ threshold → NORMAL (market expanded / trending)

Finally:

It counts how many TFs are CHOP.

If 2 or 3 TFs are CHOP → NO TRADE.

If 0 or 1 TFs are CHOP → TRADE.

Inputs / Profiles

At the top you see:

Profile

Overnight 4/0.40 – for Asia / London / overnight sessions

NYO 5/0.45 – for New York Open profile (default)

Custom – lets you type your own values

When Custom is selected, you can set:

ATR Length (Custom) – how many bars to use in the compression calc

Chop Threshold (ATR ÷ Range) (Custom) – where you cut between CHOP vs NORMAL

Higher threshold → more bars counted as NORMAL, less CHOP

Lower threshold → more bars counted as CHOP, fewer TRADE environments

For NYO, you normally keep:

Profile = NYO 5/0.45

(ATR over 5 bars, threshold 0.45)

What you see on the chart

A single line panel at the bottom-right, like:

1H: NORMAL | 30M: CHOP | 15M: NORMAL | TRADE | NYO 5/0.45

Meaning:

1H: NORMAL → the last 1H window is expanded enough (not boxed).

30M: CHOP → 30M is compressed (inside a tighter range).

15M: NORMAL → 15M has opened up.

TRADE → Only 1 TF is CHOP, so the majority says OK to trade.

NYO 5/0.45 → just a tag to remind which profile you’re using.

If instead you see:

1H: CHOP | 30M: CHOP | 15M: NORMAL | NO TRADE | NYO 5/0.45

That means:

1H and 30M are boxed

15M opened a bit, but 2 TFs are CHOP

Final verdict: NO TRADE environment

How to use it in your trading

1. As a gatekeeper before any entry model

No matter what entry you use (MSS + FVG, OB, purge setups, etc.):

If the panel says NO TRADE →

You do not open new positions.

You’re in “observe only” mode.

You can still study price, mark levels, and journal, but you’re not pressing the button.

If the panel says TRADE →

The environment is acceptable.

Now you can look for your entry model (e.g. MSS + FVG retest, SMT, OB, etc.).

Think of it as your first filter every session:

“Panel says NO TRADE? I don’t care how good the candle looks – I’m waiting.”

2. Reading each timeframe

1H: CHOP → Day is still boxed on the higher frame; big expansion hasn’t kicked in.

30M: CHOP → Classic 30M dealing range; many fake breaks and wicks likely.

15M: CHOP → Intraday still coiling; scalping environment at best.

When 2 or 3 say CHOP, expect:

Whipsaw

MSS both ways

Failed FVGs

News spikes that die in the box

Perfect time to protect your psychology and capital.

When 2 or 3 say NORMAL, expect:

Cleaner swings

Better follow-through after MSS / FVG

Easier to hold for targets

3. How it pairs with your MSS/FVG indicator

With your Chop + MSS/FVG Retest indicator:

Chop meter = environment filter

MSS/FVG indicator = entry trigger

Your process becomes:

Check chop meter:

If NO TRADE → hands off.

If TRADE → go to step 2.

On your chart, wait for:

Purge / SMT at the edges

MSS in the right direction

FVG + retest

Only take L/S when both:

Chop meter = TRADE, and

Entry model = L/S signal in the right area (premium/discount).

That way, you’re not just trading every L/S the MSS script spits out—you’re trading L/S only when the higher-timeframe environment is worth it.

Daily vs Intraday Candle Match Strategy고죠 훈의 차트공부방

Gojo Hoon’s Trading Room

전일 종가 대비 현재 일봉 방향과 시간봉 방향이 일치할 때 진입

Trade when current daily direction (vs. previous close) matches the hourly/15-minute candle direction.

Multi Time Frame EMA & MA IndicatorThis indicator automatically applies prime-number EMAs and MAs based on the current chart timeframe, using faster cool-tone EMAs and slower warm-tone MAs to clearly distinguish momentum vs trend.

It adapts dynamically for 1m, 5m, 15m, 1H, 4H, and 1D charts, and uses a visual hierarchy where thinner lines represent faster averages and thicker lines represent slower ones, ensuring clarity in both light and dark themes.

An on-chart label displays which EMA and MA lengths are active for the selected timeframe.

Time-Decay Liquidity Zones [BackQuant]Time-Decay Liquidity Zones

A dynamic liquidity map that turns single-bar exhaustion events into fading, color-graded zones, so you can see where trapped traders and unfinished business still matter, and when those areas have finally stopped pulling price.

What this is

This indicator detects unusually strong impulsive moves into wicks, converts them into supply or demand “zones,” then lets those zones decay over time. Each zone carries a strength score that fades bar by bar. Zones that stop attracting or rejecting price are gradually de-emphasized and eventually removed, while the most relevant areas stay bright and obvious.

Instead of static rectangles that live forever, you get a living liquidity map where:

Zones are born from objective criteria: volatility, wick size, and optional volume spikes.

Zones “age” using a configurable decay factor and maximum lifetime.

Zone color and opacity reflect current relative strength on a unified clear → green → red gradient.

Zones freeze when broken, so you can distinguish “active reaction areas” from “historical levels that have already given way”.

Conceptual idea

Large wicks with strong volatility often mark areas where aggressive orders met hidden liquidity and got absorbed. Price may revisit these areas to test leftover interest or to relieve trapped positions. However, not every wick matters for long. As time passes and more bars print, the market “forgets” some areas.

Time-Decay Liquidity Zones turns that idea into a rule-based system:

Find bars that likely reflect strong aggressive flows into liquidity.

Mark a zone around the wick using ATR-based thickness.

Assign a strength score of 1.0 at birth.

Each bar, reduce that score by a decay factor and remove zones that fall below a threshold or live too long.

Color all surviving zones from weak to strong using a single gradient scale and a visual legend.

How events are detected

Detection lives in the Event Detection group. The script combines range, wick size, and optional volume filters into simple rules.

Volatility filter

ATR Length — computes a rolling ATR over your chosen window. This is the volatility baseline.

Min range in ATRs — bar range (High–Low) must exceed this multiple of ATR for an event to be considered. This avoids tiny bars triggering zones.

Wick filters

For each bar, the script splits the candle into body and wicks:

Upper wick = High minus the max(Open, Close).

Lower wick = min(Open, Close) minus Low.

Then it tests:

Upper wick condition — upper wick must be larger than Min wick size in ATRs × ATR.

Lower wick condition — lower wick must be larger than Min wick size in ATRs × ATR.

Only bars with a sufficiently long wick relative to volatility qualify as candidate “liquidity events”.

Volume filter

Optionally, the script requires a volume spike:

Use volume filter — if enabled, volume must exceed a rolling volume SMA by a configurable multiplier.

Volume SMA length — period for the volume average.

Volume spike multiplier — how many times above the SMA current volume needs to be.

This lets you focus only on “heavy” tests of liquidity and ignore quiet bars.

Event types

Putting it together:

Upper event (potential supply / long liquidation, etc.)

Occurs when:

Upper wick is large in ATR terms.

Full bar range is large in ATR terms.

Volume is above the spike threshold (if enabled).

Lower event (potential demand / short liquidation, etc.)

Symmetric conditions using the lower wick.

How zones are constructed

Zone geometry lives in Zone Geometry .

When an event is detected, the script builds a rectangular box that anchors to the wick and extends in the appropriate direction by an ATR-based thickness.

For upper (supply-type) zones

Bottom of the zone = event bar high.

Top of the zone = event bar high + Zone thickness in ATRs × ATR.

The zone initially spans only the event bar on the x-axis, but is extended to the right as new bars appear while the zone is active.

For lower (demand-type) zones

Top of the zone = event bar low.

Bottom of the zone = event bar low − Zone thickness in ATRs × ATR.

Same extension logic: box starts on the event bar and grows rightward while alive.

The result is a band around the wick that scales with volatility. On high-ATR charts, zones are thicker. On calm charts, they are narrower and more precise.

Zone lifecycle, decay, and removal

All lifecycle logic is controlled by the Decay & Lifetime group.

Each zone carries:

Score — a floating-point “importance” measure, starting at 1.0 when created.

Direction — +1 for upper zones, −1 for lower zones.

Birth index — bar index at creation time.

Active flag — whether the zone is still considered unbroken and extendable.

1) Active vs broken

Each confirmed bar, the script checks:

For an upper zone , the zone is counted as “broken” when the close moves above the top of the zone.

For a lower zone , the zone is counted as “broken” when the close moves below the bottom of the zone.

When a zone breaks:

Its right edge is frozen at the previous bar (no further extension).

The zone remains on the chart, but is no longer updated by price interaction. It still decays in score until removal.

This lets you see where a major level was overrun, while naturally fading its influence over time.

2) Time decay

At each confirmed bar:

Score := Score × Score decay per bar .

A decay value close to 1.0 means very slow decay and long-lived zones.

Lower values (closer to 0.9) mean faster forgetting and more current-focused zones.

You are controlling how quickly the market “forgets” past events.

3) Age and score-based removal

Zones are removed when either:

Age in bars exceeds Max bars a zone can live .

This is a hard lifetime cap.

Score falls below Minimum score before removal .

This trims zones that have decayed into irrelevance even if their age is still within bounds.

When a zone is removed, its box is deleted and all associated state is freed to keep performance and visuals clean.

Unified gradient and color logic

Color control lives in Gradient & Color . The indicator uses a single continuous gradient for all zones, above and below price, so you can read strength at a glance without guessing what palette means what.

Base colors

You set:

Mid strength color (green) — used for mid-level strength zones and as the “anchor” in the gradient.

High strength color (red) — used for the strongest zones.

Max opacity — the maximum visual opacity for the solid part of the gradient. Lower values here mean more solid; higher values mean more transparent.

The script then defines three internal points:

Clear end — same as mid color, but with a high alpha (close to transparent).

Mid end — mid color at the strongest allowed opacity.

High end — high color at the strongest allowed opacity.

Strength normalization

Within each update:

The script finds the maximum score among all existing zones.

Each zone’s strength is computed as its score divided by this maximum.

Strength is clamped into .

This means a zone with strength 1.0 is currently the strongest zone on the chart. Other zones are colored relative to that.

Piecewise gradient

Color is assigned in two stages:

For strength between 0.0 and 0.5: interpolate from “clear” green to solid green.

Weak zones are barely visible, mid-strength zones appear as solid green.

For strength between 0.5 and 1.0: interpolate from solid green to solid red.

The strongest zones shift toward the red anchor, clearly separating them from everything else.

Strength scale legend

To make the gradient readable, the indicator draws a vertical legend on the right side of the chart:

About 15 cells from top (Strong) to bottom (Weak).

Each cell uses the same gradient function as the zones themselves.

Top cell is labeled “Strong”; bottom cell is labeled “Weak”.

This legend acts as a fixed reference so you can instantly map a zone’s color to its approximate strength rank.

What it plots

At a glance, the indicator produces:

Upper liquidity zones above price, built from large upper wick events.

Lower liquidity zones below price, built from large lower wick events.

All zones colored by relative strength using the same gradient.

Zones that freeze when price breaks them, then fade out via decay and removal.

A strength scale legend on the right to interpret the gradient.

There are no extra lines, labels, or clutter. The focus is the evolving structure of liquidity zones and their visual strength.

How to read the zones

Bright red / bright green zones

These are your current “major” liquidity areas. They have high scores relative to other zones and have not yet decayed. Expect meaningful reactions, absorption attempts, or spillover moves when price interacts with them.

Faded zones

Pale, nearly transparent zones are either old, decayed, or minor. They can still matter, but priority is lower. If these are in the middle of a long consolidation, they often become background noise.

Broken but still visible zones

Zones whose extension has stopped have been overrun by closing price. They show where a key level gave way. You can use them as context for regime shifts or failed attempts.

Absence of zones

A chart with few or no zones means that, under your current thresholds, there have not been strong enough liquidity events recently. Either tighten the filters or accept that recent price action has been relatively balanced.

Use cases

1) Intraday liquidity hunting

Run the indicator on lower timeframes (e.g., 1–15 minute) with moderately fast decay.

Use the upper zones as potential sell reaction areas, the lower zones as potential buy reaction areas.

Combine with order flow, CVD, or footprint tools to see whether price is absorbing or rejecting at each zone.

2) Swing trading context

Increase ATR length and range/wick multipliers to focus only on major spikes.

Set slower decay and higher max lifetime so zones persist across multiple sessions.

Use these zones as swing inflection areas for larger setups, for example anticipating re-tests after breakouts.

3) Stop placement and invalidation

For longs, place invalidation beyond a decaying lower zone rather than in the middle of noise.

For shorts, place invalidation beyond strong upper zones.

If price closes through a strong zone and it freezes, treat that as additional evidence your prior bias may be wrong.

4) Identifying trapped flows

Upper zones formed after violent spikes up that quickly fail can mark trapped longs.

Lower zones formed after violent spikes down that quickly reverse can mark trapped shorts.

Watching how price behaves on the next touch of those zones can hint at whether those participants are being rescued or squeezed.

Settings overview

Event Detection

Use volume filter — enable or disable the volume spike requirement.

Volume SMA length — rolling window for average volume.

Volume spike multiplier — how aggressive the volume spike filter is.

ATR length — period for ATR, used in all size comparisons.

Min wick size in ATRs — minimum wick size threshold.

Min range in ATRs — minimum bar range threshold.

Zone Geometry

Zone thickness in ATRs — vertical size of each liquidity zone, scaled by ATR.

Decay & Lifetime

Score decay per bar — multiplicative decay factor for each zone score per bar.

Max bars a zone can live — hard cap on lifetime.

Minimum score before removal — score cut-off at which zones are deleted.

Gradient & Color

Mid strength color (green) — base color for mid-level zones and the lower half of the gradient.

High strength color (red) — target color for the strongest zones.

Max opacity — controls the most solid end of the gradient (0 = fully solid, 100 = fully invisible).

Tuning guidance

Fast, session-only liquidity

Shorter ATR length (e.g., 20–50).

Higher wick and range multipliers to focus only on extreme events.

Decay per bar closer to 0.95–0.98 and moderate max lifetime.

Volume filter enabled with a decent multiplier (e.g., 1.5–2.0).

Slow, structural zones

Longer ATR length (e.g., 100+).

Moderate wick and range thresholds.

Decay per bar very close to 1.0 for slow fading.

Higher max lifetime and slightly higher min score threshold so only very weak zones disappear.

Noisy, high-volatility instruments

Increase wick and range ATR multipliers to avoid over-triggering.

Consider enabling the volume filter with stronger settings.

Keep decay moderate to avoid the chart getting overloaded with old zones.

Notes

This is a structural and contextual tool, not a complete trading system. It does not account for transaction costs, execution slippage, or your specific strategy rules. Use it to:

Highlight where liquidity has recently been tested hard.

Rank these areas by decaying strength.

Guide your attention when layering in separate entry signals, risk management, and higher-timeframe context.

Time-Decay Liquidity Zones is designed to keep your chart focused on where the market has most recently “cared” about price, and to gradually forget what no longer matters. Adjust the detection, geometry, decay, and gradient to fit your product and timeframe, and let the zones show you which parts of the tape still have unfinished business.

Relative Performance vs XAO (Histogram)RSC Relative Strength Comparison is used to compare performance of a Sector Index or Stock against a Benchmark (Index). The Benchmark used is the Australian All Ordinaries Index with a look back period of 63 days (3 months). Both the benchmark and look back period may be changed in the code to suit.

SMA Cross + KC Breakout + ATR StopThis is the same script previously published with the exception of utilizing SMA vs EMA for those who prefer that moving average type.