Williams Alligator Spread Oscillator (WASO)Short description (About box)

Williams Alligator Spread Oscillator (WASO) converts Bill Williams’ Alligator into a 0–100 oscillator that measures the average distance between Lips/Teeth/Jaw relative to ATR. High = expansion/trend (default), low = compression/range — making sideways markets easier to spot. Includes adaptive normalization, configurable thresholds, background shading, and alerts.

Full description (Description field)

What it does

The Williams Alligator Spread Oscillator (WASO) transforms Bill Williams’ Alligator into a single, adaptive 0–100 scale. It computes the average pairwise distance among the Alligator lines (Lips/Teeth/Jaw), normalizes it by ATR and a rolling min–max window, and smooths the result. This makes the signal robust across symbols and timeframes and explicitly improves detection of sideways (ranging) conditions by highlighting compression regimes.

Why it helps

Sideways detection made easier: Low WASO marks compressed regimes that commonly align with consolidation/range phases, helping you identify chop and plan breakout strategies.

Trend/expansion clarity: High WASO indicates the Alligator lines are widening relative to volatility, pointing to trending or expanding conditions.

You can flip the direction if you prefer “High = Range.”

How it is calculated (plain English)

Smooth price with RMA (SMMA-like) to get Jaw, Teeth, Lips.

Compute the average pairwise distance between these three lines.

Divide by ATR to remove price-scale effects.

Normalize with a rolling min–max window to map values to 0–100.

Optionally apply EMA smoothing to the oscillator.

Key settings

Jaw/Teeth/Lips Lengths: Alligator periods (SMMA-like via ta.rma).

ATR Length: Volatility benchmark for scaling.

Normalization Lookback: Longer = steadier; shorter = more responsive.

Smoothing (EMA): Evens out noise.

High Value = Large Spread (Trend): Toggle to invert semantics.

Upper/Lower Thresholds: 70/30 are practical starting points.

Signals / interpretation

Sideways / Compression (easier to spot):

Default direction: WASO below Lower Threshold (e.g., <30).

With inverted direction OFF: WASO above Upper Threshold (e.g., >70).

Trend / Expansion:

Default direction: WASO above Upper Threshold (e.g., >70).

With inverted direction OFF: WASO below Lower Threshold (e.g., <30).

Midline (50): Neutral zone; flips around 50 can hint at regime shifts.

Alerts included

Range Start (sideways/compression)

Trend Start (expansion/trend)

Notes & limitations

This implementation omits the classic forward shift of Alligator lines to keep signals usable on live bars.

If market behavior shifts (very quiet or very volatile), tune Lookback and ATR Length.

Combine WASO with breakout levels or momentum filters for entries/exits.

Credits & disclaimer

Inspired by Bill Williams’ Alligator.

For educational purposes only. Not financial advice.

Release Notes (v1.0):

Initial release of Williams-Alligator Spread Oscillator (WASO) with ATR-based scaling and adaptive 0–100 normalization.

Direction toggle (High = Trend by default), adjustable thresholds, background shading, and two alert conditions.

Buscar en scripts para "纳斯达克指数期货cfd"

Two-Part Supply & Demand Zones with Role ReversalWill show demand and supply with boxes

Once a zone is used it will be removed to keep the chart clean

4H + 15m Sell Signals It shows sell positions on the 15 min based on 4 hour ,imbalance, order block and swing high and low frameworks.

MTF TR HelperThe “MTF TR Helper” is a TradingView indicator that displays TC888’s Time Rotation (TR) slots for the London and New York sessions. It’s designed for intraday traders who want precise timing references based on TC888’s method.

It marks expert-level (orange) and sweetspot (green) TR timings directly on the chart using small visual cues. These slots help identify potential points of interest during active market hours. The script is optimized for lower timeframes and automatically filters out markers on higher timeframes to reduce clutter.

Key Features:

• 🔶 Orange lines = Expert TR slots (per TC888)

• 🟢 Green lines = Sweetspot TR slots (per TC888)

• ⚪ Dots = Hourly rotation points, including new 4-hour bars

• 📈 Works best on 1m and 5m charts; adapts visibility based on timeframe

• 🕒 Built on London and New York time zone references

This tool follows the timing logic of TC888, offering a clean and practical way to stay aligned with key session-based rotations.

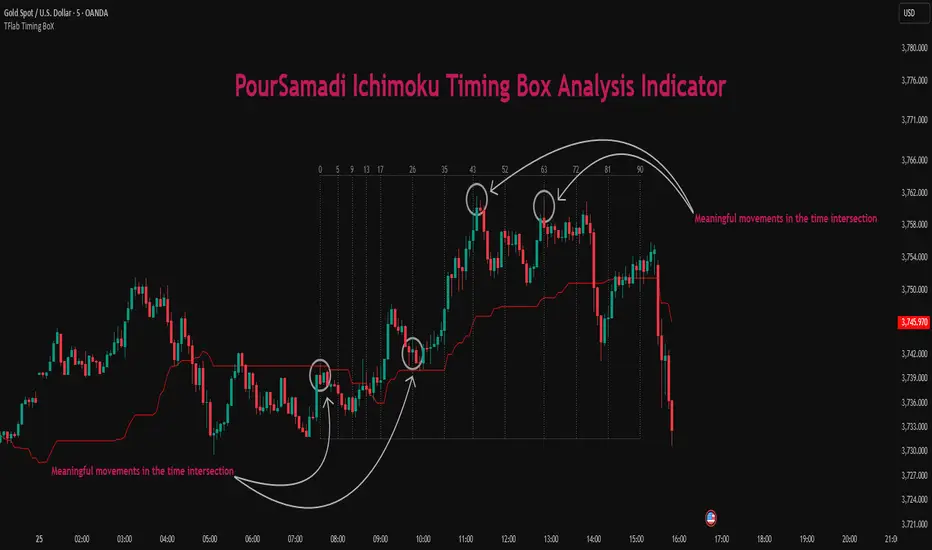

Ichimoku PourSamadi Signal [TradingFinder] KijunSen Magic Number🔵 Introduction

The Ichimoku Kinko Hyo system is one of the most comprehensive market analysis tools ever created. Developed by Goichi Hosoda, a Japanese journalist in the 1930s, its purpose was to allow traders to recognize the balance between price, time, and momentum at a single glance. (In Japanese, Ichimoku literally means “one look.”)

At the core of the system lie five key components: Tenkan-sen (Conversion Line), Kijun-sen (Baseline), Chikou Span (Lagging Line), and the two leading spans, Senkou Span A and Senkou Span B, which together form the well-known Kumo or cloud representing both temporal structure and equilibrium zones in the market.

Although Ichimoku is commonly used to identify trends and support/resistance levels, a deeper layer of time philosophy exists within it. Ichimoku was not designed solely for price analysis but equally for time analysis.

In the classical model, the numerical cycles 9, 26, 52 reflect the natural rhythm of the market originally based on the Tokyo Stock Exchange’s trading schedule in the 1930s.

These values repeat across the system’s calculations, forming the foundation of Ichimoku’s time symmetry where price and time ultimately seek equilibrium.

In recent years, modern analysts have explored new approaches to extract time-based turning points from Ichimoku’s structure. One such approach is the analysis of flat segments on the Kijun-sen and Senkou B lines.

Whenever one of these lines remains flat for a period, it signals temporary balance between buyers and sellers; when the flat breaks, the market exits equilibrium and a new cycle begins.

This indicator is built precisely upon that philosophy. Following the timing methodology introduced by M.A. Poursamadi, the focus shifts away from price signals and line crossovers toward identifying flat periods on Kijun-sen (period 52) as time anchors.

From the first candle that changes the line’s slope, the tool begins a temporal count using a fixed sequence of key numbers: 5, 9, 13, 17, 26, 35, 43, 52, 63, 72, 81, 90.

Derived from both classical Ichimoku cycles and empirical testing, these numbers mark potential timing nodes where a market wave may end, a correction may begin, or a new leg may form.

Thus, this method serves not merely as another Ichimoku tool but as a temporal metronome for market structure a way to visualize moments when the market is ready to change rhythm, often before candles reveal it.

🔵 How to Use

The Kijun Timing BoX is built entirely on Ichimoku’s concept of time analysis.

Its core idea is that within every flat segment of the Kijun-sen, the market enters a temporary balance between opposing forces.

When that flat breaks, a new time cycle begins. From that first breakout candle, the indicator starts counting forward through the predefined time sequence(5, 9, 13, 17, 26, 35, 43, 52, 63, 72, 81, 90).

This counting framework creates a temporal map of market behavior, where each number represents an area where meaningful price fluctuations often occur.

A “meaningful fluctuation” does not necessarily imply reversal or continuation; rather, it marks a moment when the market’s internal energy balance shifts, typically visible as noticeable reactions on lower timeframes.

🟣 Identifying the Anchor Point

The first step is recognizing a valid flat zone on the Kijun-sen.

When this line remains flat for several candles and then changes slope, the indicator marks that bar as the Anchor, initiating the time count.

From that point onward, vertical gray lines appear at each interval in the key-number sequence, visualizing the time nodes ahead.

🟣 Reading the Timing Lines

Each numbered line represents a timing node a temporal point where a change in price rhythm is statistically more likely to occur.

At these nodes, the market may :

Enter a consolidation or minor correction phase.

Develop range-bound movement.

Or simply alter the speed and intensity of its move.

These behaviors do not imply a specific direction; they only highlight zones where time-based activity tends to cluster, giving traders a clearer view of cyclical rhythm.

🟣 Applying Time Analysis

The indicator’s primary use is to observe temporal order, not to predict price direction.

By tracking the distance between Anchors and the reactions that appear near major timing lines, traders can empirically identify each market’s characteristic rhythm—its own time DNA.

For example, one asset may consistently show significant fluctuations around the 13- and 26-bar marks,while another might react closer to 9 or 52. Recognizing such patterns helps traders understand how long typical cycles last before new phases of volatility emerge.

🟣 Combining with Other Tools

The indicator does not generate buy/sell signals on its own.

Its best use is in combination with price- or structure-based methods, to see whether meaningful price reactions occur around the same timing nodes.

In practice, it helps distinguish structured time-based fluctuations from random, noise-driven moves an insight often overlooked in conventional market analysis.

🔵 Settings

🟣 Logical Settings

KijunSen Period : Defines the baseline period used for timing analysis. Default = 52. It is the main line for detecting flats and generating time anchors.

Flat Event Filter : Controls how flat segments are validated before triggering a new timing event.

All : Every flat triggers a new Timing Box.

Automatic : Only flats longer than the historical average are used (recommended).

Custom : User manually defines the minimum flat length via Custom Count.

Update Timing Analysis BoX Per Event : If enabled, a new Timing Box is drawn each time a new flat event occurs. If disabled, the box completes its 90-bar window before refreshing.

🟣 Ichimoku Settings

TenkanSen Period : Defines the period for the Conversion Line (Tenkan-sen). Default = 9.

KijunSen Period : Sets the standard Ichimoku baseline (not the timing line). Default = 26.

Span B Period : Defines the period for Senkou Span B, the slower cloud boundary. Default = 52.

Shift Lines : Offsets cloud projection into the future. Default = 26.

🟣 Display Settings

Users can show or hide all Ichimoku lines Tenkan-sen, Kijun-sen, Chikou Span, Span A, and Span B as well as the Ichimoku Cloud.

They can also customize the color of each element to match personal chart preferences and improve visibility.

🔵 Conclusion

This analytical approach transforms Ichimoku’s time philosophy into a visual and measurable framework. A flat Kijun-sen represents a moment of market equilibrium; when its slope shifts, a new temporal cycle begins.

The purpose is not to forecast price direction but to highlight periods when meaningful fluctuations are more likely to develop.

Through this perspective, traders can observe the hidden rhythm of market time and expand their analysis beyond price into a broader time-cycle dimension.

Ultimately, the method revives Ichimoku’s original principle: the market can only be truly understood through the simultaneous harmony of price, time, and balance.

Ngo Gia Minh Quy 30Indicator xin vai ca lon a. Dung indicator nay trade thua nua thi nghi me no di. hahahahaha

Ngo Gia Minh Quy 50Indicator xin vai ca lon a. Dung indicator nay trade thua nua thi nghi me no di. hahahahaha

No Supply (Low-Volume Down Bars) — IdoThis indicator flags classic Wyckoff/VSA “No Supply (NS)” events—down bars that print on unusually low volume, suggesting a lack of sellers rather than strong selling pressure. NS often appears near support, LPS, or within re-accumulation ranges as a test before continuation higher.

Signal definition (configurable):

Down bar: choose Close < PrevClose or Close < Open.

Low volume: Volume < SMA(Volume, len) × threshold (e.g., 0.7).

Optional volume lower than the prior two bars (reduces noise).

Optional narrow spread: range (H–L) below its average.

Optional close position: close in the upper half of the bar.

Optional trend filter: only mark NS above or below an EMA (or any).

Optional wide-bar exclusion: skip unusually wide bars.

Visuals & outputs

Blue dot below each NS bar (optional bar tint).

Separate pane showing Relative Volume (vol / volSMA) to gauge effort.

Built-in alertcondition to trigger notifications when NS prints.

Inputs (high level)

lenVol: Volume SMA length.

ratioVol: Volume threshold vs. average (e.g., 0.7 = 70%).

usePrev2: Require volume below each of the prior two bars.

useNarrow + lenRange + ratioRange: Narrow-bar filter.

useClosePos + minClosePos: Close in upper portion of the bar.

downBarMode: Define “down bar” logic.

trendFiltOn, trendLen, trendSide: EMA trend filter.

useWideFilter, lenRangeWide, wideThreshold: Skip wide bars.

How to use (Wyckoff/VSA context)

Treat NS as a test of supply: price dips, but volume is light and close holds up.

Stronger when it prints near support/LPS within a re-accumulation structure.

Confirmation (recommended): within 1–3 bars, see demand—e.g., break above the NS high with expanding volume (above average or above the prior two bars). Many traders place a buy-stop just above the NS high; common stops are below the NS low or the most recent swing low.

Scanning tip

TradingView’s stock screener can’t consume Pine directly.

Use a Watchlist Custom Column that reports “bars since NS” to sort symbols (0 = NS on the latest bar). A companion column script is provided separately.

Notes & limitations

Works on any timeframe (intraday/daily/weekly), but context matters.

Expect false positives around news, gaps, or illiquid symbols—combine with structure (trend, S/R, phases) and risk management.

© moshel — Educational use only; not financial advice.

Multi-Timeframe MA - TCMasterThis indicator displays up to four moving averages from different timeframes on a single chart.

It’s designed for traders who want to track higher-timeframe trends while analyzing price action on lower timeframes — a key technique in multi-timeframe confluence trading.

You can freely customize the type, length, timeframe, and color for each moving average line.

⚙️ Features

4 configurable Moving Averages (each with its own type, length, and timeframe).

Supported types:

SMA, EMA, WMA, RMA, HMA, VWMA, DEMA, TEMA.

Real-time values are fetched from higher timeframes using request.security() (no repaint).

Individual visibility toggle and line width for each MA.

Dynamic info label shows current distance between price and each MA.

Built with Pine Script v6, ensuring optimal performance and flexibility.

📊 Typical Use Cases

Identify trend direction across multiple timeframes.

Confirm entries/exits using higher timeframe trend alignment.

Spot potential reversal or continuation zones when short-term price interacts with long-term MAs.

Build confluence setups for swing, scalp, or intraday strategies.

🧠 Example Setup

MA Type Length Timeframe Purpose

MA #1 SMA 200 1m Micro trend

MA #2 EMA 200 5m Short-term trend

MA #3 EMA 200 15m Medium trend

MA #4 SMA 200 30m Macro trend

🔔 Tips

Combine with oscillators (e.g., RSI, Stoch, MACD) for stronger confluence.

Use color coding to distinguish short vs long timeframe trends.

Consider adding alerts when price crosses any MA (can be extended easily in code).

⚠️ Notes

All higher-timeframe data is handled safely using lookahead=barmerge.lookahead_off to prevent repainting.

Label updates only on the latest bar for efficiency.

VWMA, DEMA, TEMA, and HMA are computed via internal formulas for compatibility with Pine Script v6.

🏁 Summary

Multi-Timeframe MA is a powerful tool for traders who want to merge the clarity of moving averages with the precision of multi-timeframe analysis.

It helps you see the bigger picture without switching charts — perfect for intraday, swing, and trend-following strategies.

Multi-Timeframe MA - TCMaster🧩 Overview

This indicator displays up to four moving averages from different timeframes on a single chart.

It’s designed for traders who want to track higher-timeframe trends while analyzing price action on lower timeframes — a key technique in multi-timeframe confluence trading.

You can freely customize the type, length, timeframe, and color for each moving average line.

⚙️ Features

4 configurable Moving Averages (each with its own type, length, and timeframe).

Supported types:

SMA, EMA, WMA, RMA, HMA, VWMA, DEMA, TEMA.

Real-time values are fetched from higher timeframes using request.security() (no repaint).

Individual visibility toggle and line width for each MA.

Dynamic info label shows current distance between price and each MA.

Built with Pine Script v6, ensuring optimal performance and flexibility.

📊 Typical Use Cases

Identify trend direction across multiple timeframes.

Confirm entries/exits using higher timeframe trend alignment.

Spot potential reversal or continuation zones when short-term price interacts with long-term MAs.

Build confluence setups for swing, scalp, or intraday strategies.

🧠 Example Setup

MA Type Length Timeframe Purpose

MA #1 SMA 200 1m Micro trend

MA #2 EMA 200 5m Short-term trend

MA #3 EMA 200 15m Medium trend

MA #4 SMA 200 30m Macro trend

🔔 Tips

Combine with oscillators (e.g., RSI, Stoch, MACD) for stronger confluence.

Use color coding to distinguish short vs long timeframe trends.

Consider adding alerts when price crosses any MA (can be extended easily in code).

⚠️ Notes

All higher-timeframe data is handled safely using lookahead=barmerge.lookahead_off to prevent repainting.

Label updates only on the latest bar for efficiency.

VWMA, DEMA, TEMA, and HMA are computed via internal formulas for compatibility with Pine Script v6.

🏁 Summary

Multi-Timeframe MA is a powerful tool for traders who want to merge the clarity of moving averages with the precision of multi-timeframe analysis.

It helps you see the bigger picture without switching charts — perfect for intraday, swing, and trend-following strategies.

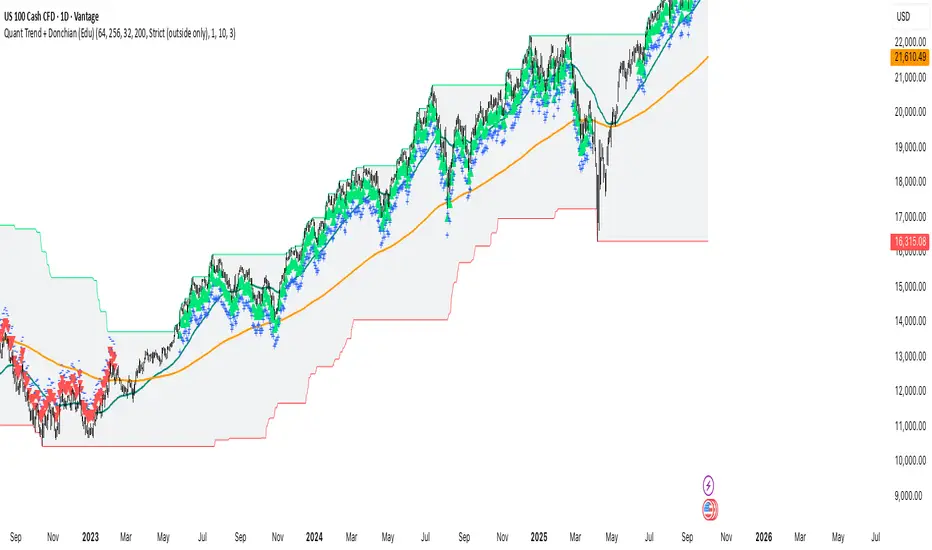

Quant Trend + Donchian (Educational, Public-Safe)What this does

Educational, public-safe visualization of a quant regime model:

• Trend : EMA(64) vs EMA(256) (EWMAC proxy)

• Breakout : Donchian channel (200)

• Volatility-awareness : internal z-scores (not plotted) for concept clarity

Why it’s useful

• Shows when trend & breakout align (clean regimes) vs conflict (chop)

• Helps explain why volatility-aware systems size up in smooth trends and scale down in noise

How to read it

• EMA64 above EMA256 with price near/above Donchian high → trend-following alignment

• EMA64 below EMA256 with price near/below Donchian low → bearish alignment

• Inside channel with EMAs tangled → range/chop risk

Notes

• Indicator is educational only (no orders).

• Built entirely with TradingView built-ins.

• For consistent visuals: enable “Indicator values on price scale” and disable “Scale price chart only” in Settings → Scales .

HTF Candle Overlay (Boxes + Wicks) 1hr / SolalDescription:

This indicator lets you visualize higher time frame (HTF) candles directly on a lower time frame chart.

It draws each HTF candle as a transparent box (the body) with wicks extending to the high and low. The boxes automatically update as each higher time frame candle forms and remain fixed once the candle closes.

You can choose any higher time frame (e.g., 1H, 4H, 1D) while trading on lower intervals (like 1m, 5m, 15m) to see key market structure and price zones.

Features:

Display candles from any higher time frame on your current chart.

Customizable colors for bullish and bearish candles.

Adjustable transparency, border and wick thickness.

History depth setting to control how many past HTF candles are displayed.

No repainting — candles stay fixed once closed.

Use case:

Ideal for traders who want to monitor higher time frame price action (support/resistance, trend direction) without switching chart time frames.

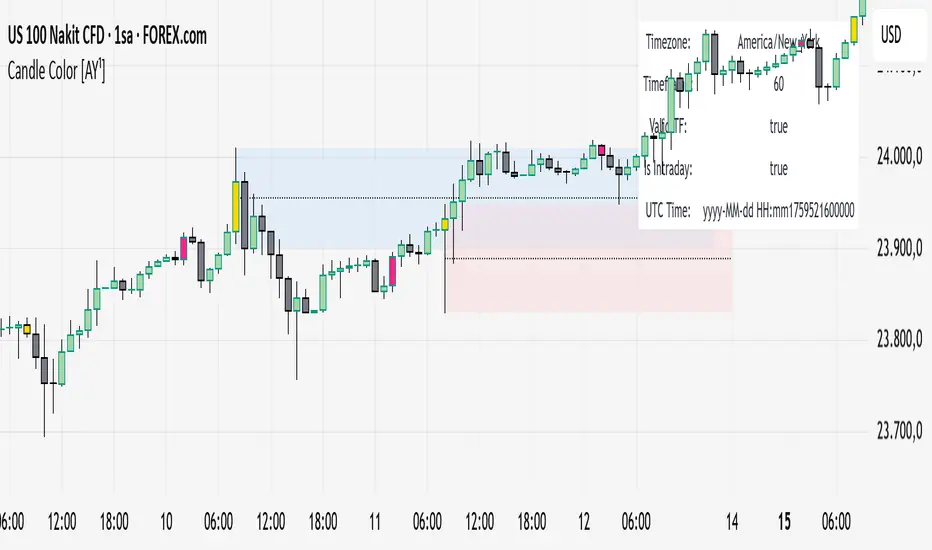

Candle Color [AY¹]Visually highlight specific time periods with custom colors on intraday charts.

Ideal for session-based traders who want to emphasize New York, London or any custom trading hours. Developed by AY¹

Candle Color Highlighter

A simple yet powerful intraday visualization tool that colors candles or chart background during your chosen trading sessions.

Perfect for traders who rely on time-based confluences — such as ICT, SMC, or session scalping frameworks.

🔧 Key Features

✅ Highlight up to four custom time periods (e.g. London Open, NY Open, Lunch Hour, etc.)

✅ Supports multiple highlight styles:

• Bar Color only

• Background only

• Both

✅ Full timezone control (Exchange, UTC, New York, London, Tokyo, or custom UTC+3)

✅ Works on all intraday timeframes or only those you select (1m–4h).

✅ Optional labels marking session starts.

✅ Integrated alerts when any period becomes active.

✅ Informative status table showing timezone, timeframe, and active period.

🕒 Use Cases

Highlight New York Killzone (07:30–09:30) or London Open (02:00–03:00)

Separate different liquidity windows

Emphasize your backtest periods

Combine with volume, displacement, or structure indicators for time-based confluence setups

🎨 Customization

Each of the four configurable periods allows you to choose:

Start/End time

Custom color and transparency

Session label visibility

Highlight style preference

💡 Example Setup

Period Session Time Color Notes

Period 1 02:00–03:00 Magenta London Killzone

Period 2 07:30–08:30 Yellow NY Pre-market

Period 3 08:30–09:30 Blue NY Open

Period 4 09:30–10:00 Green Initial Balance

BFM Yen Carry to Risk Ratio (Dynamic Rates)Shows risk of yen carry trade unwinding. Based on cost to borrow from Japan to buy us stocks compared to interest rate in USA.

Bar Count Custom Start TimeThis simple bar count script lets you configure when you want to start your count in case you have the globex charts in use for your assets.

Example NYSE:

Set start hour to: 8

Set start minute to: 30

Example DAX:

Set start hour to: 2

Set start minute to: 0

The indicator is based on the "Bar Count" indicator from GYH9 - many thanks!

Can be found here:

Multi-TF FVG Kerze Break AlertHere's a breakdown of the key files:

App.tsx: This is the main component that orchestrates the entire user interface. It manages the application's state, including the input Pine Script, the selected target language, the resulting converted code, and the loading/error states.

services/geminiService.ts: This file handles all communication with the Google Gemini API. It takes the Pine Script and the target language, constructs a detailed prompt instructing the AI on how to perform the conversion, sends the request, and processes the response.

components/CodeEditor.tsx: A reusable UI component that provides a styled for both displaying the input Pine Script and the read-only output.

constants.ts: This file centralizes static data. It contains the list of target languages for the dropdown menu and the default Pine Script code that loads when the application first starts.

index.html & index.tsx: These are the standard entry points for the React application, responsible for setting up the web page and mounting the main App component.

In essence, the application provides a user-friendly interface for developers to convert financial trading algorithms written in TradingView's Pine Script into other popular programming languages, leveraging the power of the Gemini AI model to perform the translation.

US Government Shutdowns – Full History (with durations)이 지표는 1976년 이후 실제로 정부 기능이 중단된 모든 미국 정부 셧다운 기간을 시각화합니다.

S&P500 또는 지정한 심볼 차트 위에 각 셧다운 구간을 세로선과 음영 박스로 표시하고,

각 기간의 지속일수(일) 라벨을 함께 제공합니다.

데이터 출처: 미국 하원 공식 기록 (U.S. House History – Funding Gaps and Shutdowns in the Federal Government)

기능

• 모든 셧다운 구간 자동 표시

• 음영/세로선/라벨 개별 On-Off 가능

• 진행 중인 셧다운은 자동으로 ‘현재 시점까지’ 확장 표시

시장 변동성 분석, 정책 이벤트 리스크 평가, 장기 매크로 백테스트 등에 유용합니다.

This indicator visualizes all official US government shutdown periods since 1976 directly on any selected chart (default: S&P 500).

Each shutdown period is shown with vertical lines and shaded boxes, along with labels indicating the duration in days.

Data Source: U.S. House History – Funding Gaps and Shutdowns in the Federal Government

Features:

• Displays every historical shutdown automatically

• Optional shading, lines, and duration labels

• Ongoing shutdowns dynamically extend to the current date

Useful for analyzing volatility around fiscal policy events and long-term macro correlations.

MACD cu RSI 7 Fibonacci color levelsMACD with RSI info

The RSI is display as value with changing color as Fibonacci levels.

MACD with RSI color 7 Fibonacci levelsMACD that contain RSI info

The color of RSI is change accordingly with Fibonacci levels, from red till green

EMA Dual with SL/TP ATR basedDouble EMA with cross and direction display.

Calculate stop loss / take profit based on ATR

If entering is not in the recognize direction also SL/TP is display (inversed values)

SL is 2xATR and TP is 4xAT by default - can be change

Also, SL/TP can be calculated at cross or at actual - see the table.