Microstructure Participation & Acceptance Indicator📊 Microstructure Participation & Acceptance Indicator

An advanced participation-based filter combining VWAP distance analysis, volume delta detection, and real-time acceptance/rejection state identification—designed for smaller timeframe trading.

📊 FEATURES

VWAP Distance Normalization

Context-aware fair value measurement:

Automatically resets based on selected anchor (Session/Week/Month)

ATR-normalized distance calculation for universal application

Identifies when price is extended or compressed relative to equilibrium

Configurable extreme distance threshold (default: 1.5 ATR)

Adjustable source input (default: HLC3)

Volume Delta Proxy

Bull vs Bear participation tracking:

Calculates volume imbalance between bullish and bearish candles

EMA smoothing for cleaner signal generation (default: 9 periods)

Delta ratio measurement to identify dominant side

Expansion/compression detection to gauge momentum commitment

Configurable expansion threshold (default: 1.3x)

Acceptance/Rejection State Machine

Real-time market regime identification with six distinct states:

🟢 Accepted Long

Price moving away from VWAP with expanding bullish delta

Distance from VWAP increasing

Volume confirming the move

Indicates real buying pressure—trade WITH the move

🟢 Accepted Short

Price moving away from VWAP with expanding bearish delta

Distance from VWAP increasing

Volume confirming the move

Indicates real selling pressure—trade WITH the move

🟠 Fade Long

Price extended beyond threshold (>1.5 ATR above VWAP)

Delta not supporting the extension

Volume participation absent or diminishing

Potential mean-reversion short setup

🟠 Fade Short

Price extended beyond threshold (>1.5 ATR below VWAP)

Delta not supporting the extension

Volume participation absent or diminishing

Potential mean-reversion long setup

⚪ Chop

Price compressed near VWAP

Bollinger Bands tight (width compressed)

Delta neutral—no clear commitment

NO TRADE ZONE—wait for expansion

⚪ Neutral

Transitional state between regimes

Momentum shifting but not yet confirmed

Monitor for next acceptance signal

Bollinger Bands

Standard volatility measurement with TradingView default styling:

Adjustable period length (default: 20)

Configurable standard deviation multiplier (default: 2.0)

Visual fill between bands for volatility context

Used internally for chop/compression detection

Live Dashboard

Real-time metrics display (top-right corner):

Current market state with color coding

VWAP distance in ATR units

Delta ratio (bull/bear volume balance)

Delta state (Expanding/Compressing)

High-contrast design for instant readability

🎯 HOW TO USE

For Trend Trading:

Accepted Long/Short backgrounds indicate confirmed participation—stay with the trend

Strong moves typically travel 1-1.5 ATR from VWAP with delta support

Use VWAP as dynamic support/resistance

Combine with momentum indicators (MACD, RSI) for confluence

Price above VWAP + Accepted Long state = bullish bias

Price below VWAP + Accepted Short state = bearish bias

For Mean Reversion:

Fade Long/Short states signal overextension without participation

Price beyond 1.5 ATR from VWAP with weak delta = potential reversal

Look for price return to VWAP when extended

Bollinger Band extremes + Fade state = high-probability mean reversion setup

VWAP acts as mean reversion anchor during range-bound sessions

For Risk Management:

Chop state = avoid new entries

Bollinger Band compression + Chop = pre-expansion zone (wait for breakout)

Delta compression after strong move = early exhaustion warning

State transitions (Accepted → Neutral → Fade) = tighten stops

Signal Confirmation:

Strongest setups occur when multiple factors align:

BB breakout + Accepted state + price above/below VWAP

Price rejection at BB bands + Fade state

VWAP support/resistance hold + state transition

Delta expansion + distance increasing + trend direction

⚙️ SETTINGS

All components are fully customizable through organized input groups:

VWAP Distance Group:

VWAP source (default: HLC3)

Anchor period (Session/Week/Month)

ATR length for normalization (default: 14)

Extreme distance threshold in ATR multiples (default: 1.5)

Volume Delta Group:

Delta EMA length (default: 9)

Delta expansion threshold (default: 1.3)

Acceptance Logic Group:

Acceptance lookback period (default: 5)

Chop threshold in VWAP/ATR units (default: 0.3)

Bollinger Bands Group:

BB length (default: 20)

Standard deviation multiplier (default: 2.0)

Display Group:

Toggle state backgrounds

Toggle state change labels

Toggle VWAP line

Toggle Bollinger Bands

💡 EDUCATIONAL VALUE

This indicator teaches important concepts:

How institutional money identifies fair value (VWAP)

The difference between price movement and market acceptance

Why volume participation matters more than price action alone

How to distinguish between noise and committed directional moves

The relationship between volatility compression and expansion cycles

Why distance from equilibrium predicts mean reversion probability

⚠️ IMPORTANT NOTES

This indicator is for educational and informational purposes only

This is a filter, not a standalone trading system

No indicator is perfect—always use proper risk management

Past performance does not guarantee future results

Combine with your own analysis and risk tolerance

Test thoroughly on historical data before live trading

This is not financial advice—use at your own risk

🔧 TECHNICAL DETAILS

Pine Script Version 6

Overlay indicator (displays on price chart)

All calculations use standard, well-documented formulas

No repainting—all signals are confirmed on bar close

Compatible with all timeframes and instruments

Optimized for smaller timeframes (1-5 minute charts)

Minimal computational overhead

📝 CHANGELOG

Version 1.0

Initial release

VWAP distance normalization with ATR scaling

Volume delta proxy system (bull/bear EMA)

6-state acceptance/rejection state machine

Bollinger Bands integration

Real-time dashboard with live metrics

State change labels and background coloring

Full customization options

Developed for traders who need objective participation filters to distinguish high-probability setups from low-quality noise—without cluttering their charts with multiple indicator panels.

Meanreversion

Session ATR Progression Tracker📊 Session ATR Progression Tracker - SIYL Regression Trading Tool

Track how much of your instrument's 7-day Average True Range (ATR) has been covered during the current trading session. This indicator is specifically designed for regression traders who follow the "Stay In Your Lane" (SIYL) methodology, helping you identify when the probability of mean reversion significantly increases. If you are interested in more on that check out Rod Casselli and tradersdevgroup.com.

🎯 Key Features:

• Real-time ATR Coverage Percentage - See at a glance what percentage of the 7-day ATR has been covered in the current session

• SIYL-Optimized Thresholds - See at a glance when the instrument has achieved 80% and 100% ATR coverage, the proven thresholds where mean reversion probability increases (customizable)

• Flexible Session Modes:

- Daily: Resets at calendar day change

- Session: Uses exchange-defined trading sessions

- Custom Session: Set your exact session start/end times (perfect for futures traders and international markets)

• Visual Alerts - Color-coded display (gray → orange → red) and optional background highlighting

• Repositionable Display - Choose from 9 screen positions to avoid chart clutter

• Session Markers - Green triangles mark the start of each new session

• Detailed Stats - View current range, ATR value, session high/low, and session status

💡 Why Use This Indicator?

This tool is built around a proven concept: regression trading becomes significantly more effective once a session has achieved at least 80% of its 7-day ATR. At this threshold, the probability of price reverting to mean increases substantially, creating higher-probability trade setups for SIYL practitioners.

Benefits for regression traders:

- Identify optimal entry points when mean reversion probability is highest (≥80% ATR coverage)

- Avoid premature regression entries before adequate range has been established

- Recognize when daily moves have "earned their range" and are ripe for reversal

- Time fade-the-move and counter-trend strategies with statistical backing

- Improve win rates by trading only after proven probability thresholds are met

⚙️ Setup Instructions:

1. Add the indicator to your chart

2. Select your preferred "Reset Mode" (recommend "Custom Session" for futures/international markets)

3. If using Custom Session, enter your session times in 24-hour format (e.g., 0930-1600 for US stocks, 1700-1600 for CME futures)

4. Adjust alert thresholds if desired (default: 80% and 100% - proven SIYL thresholds)

5. Position the display where it's most visible on your chart

📈 Works Across All Markets:

Stocks • Futures • Forex • Indices • Crypto • Commodities

Perfect for regression traders, mean reversion specialists, and SIYL practitioners who want to trade with probability on their side by entering only after the session has "earned its range."

---

Tip: For futures contracts with overnight sessions that span calendar days (like MES, MNQ, MYM), use "Custom Session" mode with your exchange's official session times for accurate tracking.

Ultimate Reversion BandsURB – The Smart Reversion Tool

URB Final filters out false breakouts using a real retest mechanism that most indicators miss. Instead of chasing wicks that fail immediately, it waits for price to confirm rejection by retesting the inner band—proving sellers/buyers are truly exhausted.

Eliminates fakeouts – The retest filter catches only genuine reversions

Triple confirmation – Wick + retest + optional volume/RSI filters

Clear visuals – Outer bands show extremes, inner bands show retest zones

Works on any timeframe – From scalping to swing trading

Perfect for traders tired of getting stopped out by false breakouts.

Core Construction:

Smart Dynamic Bands:

Basis = Weighted hybrid EMA of HLC3, SMA, and WMA

Outer Bands = Basis ± (ATR × Multiplier)

Inner Bands = Basis ± (ATR × Multiplier × 0.5) → The "retest zone"

The Unique Filter: The Real Retest

Step 1: Identify an extreme wick touching the outer band

Step 2: Wait 1-3 bars for price to return and touch the inner band

Why it works: Most false breakouts never retest. A genuine reversal shows seller/buyer exhaustion by allowing price to come back to the "halfway" level.

Optional Confirmations:

Volume surge filter (default ON)

RSI extremes filter (optional)

Each can be toggled ON/OFF

How to Use:

Watch for extreme wicks touching the red/lime outer bands

Wait for the retest – price must return to touch the inner band (dotted line) within 3 bars

Enter on confirmation with built-in volume/RSI filters

Set stops beyond the extreme wick

Trend Tracer [AlgoAlpha]🟠 OVERVIEW

This tool builds a two-stage trend model that reacts to structure shifts while also showing how strong or weak the move is. It uses a mid-price band (from the highest high and lowest low over a lookback) and applies two Supertrend passes on top of it. The first pass smoothens the basis. The second pass refines that direction and produces the final trail used for signals. A gradient fill between the two trails uses RSI of price-to-trail distance to show when price is stretched or cooling off. The aim is to give traders a simple way to read trend alignment, pressure, and early turns without guessing.

🟠 CONCEPTS

The script starts with a mid-range basis. This is the average of the rolling highest high and lowest low. It acts as a stable structure reference instead of raw close or typical price. From there, two Supertrend layers are applied:

• The first Supertrend uses a shorter ATR period and lower factor. It reacts faster and sets the main regime.

• The second Supertrend uses a slightly longer ATR and higher factor. It filters noise, waits for confirmed continuation, and generates the signal line.

The interaction between these trails matters. The outer Supertrend provides context by defining the broader regime. The inner Supertrend provides timing by flipping earlier and marking possible shifts. The gradient fill uses RSI of (close − supertrend value) to display when price stretches away from the trail. This shows strength, exhaustion, or compression within the trend.

🟠 FEATURES

Bullish and bearish flip markers placed at recent highs/lows

Rejection signals off the trend tracer line

Alerts for bullish and bearish trend changes

🟠 USAGE

Setup : Add the script to your chart. Timeframe is flexible; lower timeframes show more flips while higher ones give cleaner swings. Adjust Length to change how wide the basis range is. Use the two ATR settings and factors to match the volatility of the market you trade.

Read the chart : When the refined trail (stv_) sits above price the regime is bearish; when below, it is bullish. The wide trail (stv) confirms the larger move. Watch the gradient fill: darker colors appear when price is stretched from the trail and lighter colors appear when the move is weakening. Flip markers ▲ or ▼ highlight the first clean shift of the refined trail.

Settings that matter : Increasing the Main Factor slows main-trend flips and filters chop. Increasing the Signal Factor delays the timing trail but reduces noise. Shortening Length makes the basis more reactive. ATR periods change how sensitive each Supertrend pass is to volatility.

Trend Step Channel [BigBeluga]🔵 OVERVIEW

Trend Step Channel identifies directional bias by forming a dynamic volatility-based step channel. It detects trend shifts when candle lows close above the upper band (bullish) or when candle highs drop below the lower band (bearish). A step-style midline tracks the trend evolution, while an integrated dashboard shows price positioning percentages across multiple timeframes.

🔵 CONCEPTS

ATR-Based Channel — The indicator constructs upper and lower channel boundaries using ATR distance around a single adaptive trend line, providing automatic scaling with volatility.

Trend Direction Logic —

• Low above upper band → uptrend confirmation.

• High below lower band → downtrend confirmation.

Step Trend Line — A reactive midline that locks onto price swings, stepping upward or downward as new trend confirmations occur.

Channel Width — Defines the total volatility range around the midline; a wider channel smooths market noise, while a narrower one reacts faster.

Price Position Ratio — Calculates the relative position of the close within the channel, from 0% (bottom) to 100% (top).

🔵 FEATURES

Volatility-Adaptive Channel — Expands and contracts dynamically to match market volatility, maintaining consistent distance scaling.

Configurable MA Source — Choose from SMA, EMA, SMMA, WMA, or VWMA as the base smoothing method.

Color-Coded Step Line —

• Green indicates an uptrend.

• Orange indicates a downtrend.

Channel Fill Visualization — Semi-transparent fills highlight active volatility zones for clear trend identification.

Price Position Label — Displays a “<” marker and percentage at the channel edge showing how far the current close is from the lower or upper band.

Multi-Timeframe Dashboard —

• Displays alignment across 1H–5H charts.

• Each cell shows an arrow (↑ / ↓) with price % positioning.

• Cell background color reflects bullish or bearish bias.

Real-Time Updating — The channel, midline, and dashboard refresh dynamically every bar for continuous feedback.

🔵 HOW TO USE

Trend Confirmation —

• Bullish trend forms when candle low closes above the upper band.

• Bearish trend forms when candle high closes below the lower band.

Trend Continuation — Maintain bias while the step line color remains consistent.

Volatility Breakouts — Sudden candle breaks outside the band suggest new directional strength.

Dashboard Alignment — Confirm trend consistency across multiple timeframes before entering trades.

Entry Planning — In uptrends, consider entries near the lower band; in downtrends, focus on upper-band rejections.

Price Position Insight — Use the % label to judge whether price is extended (near 100%) or compressed (near 0%) within the channel.

🔵 CONCLUSION

Trend Step Channel delivers a precise, volatility-driven view of trend structure using ATR-based boundaries and a step-line framework. The integrated dashboard, color-coded channel, and live positioning metrics give traders a complete picture of market direction, trend strength, and price location within evolving conditions.

SMC Statistical Liquidity Walls [PhenLabs]📊 SMC Statistical Liquidity Walls

Version: PineScript™ v6

📌 Description

The SMC Statistical Liquidity Walls indicator is designed to visualize market volatility and potential reversal zones using advanced statistical modeling. Unlike traditional Bollinger Bands that use simple lines, this script utilizes an “Inverted Sigmoid” opacity function to create a “fog of war” effect. This visualizes the density of liquidity: the further price moves from the equilibrium (mean), the “harder” the liquidity wall becomes.

This tool solves the problem of over-trading in low-probability areas. By automatically mapping “Premium” (Resistance) and “Discount” (Support) zones based on Standard Deviation (SD), traders can instantly see when price is overextended. The result is a clean, intuitive overlay that helps you identify high-probability mean reversion setups without cluttering your chart with manual drawings.

🚀 Points of Innovation

Inverted Sigmoid Logic: A custom mathematical function maps Standard Deviation to opacity, creating a realistic “wall” density effect rather than linear gradients.

Dynamic “Solidity”: The indicator is transparent at the center (Equilibrium) and becomes visually solid at the edges, mimicking physical resistance.

Separated Directional Bias: distinct Red (Premium) and Green (Discount) coding helps SMC traders instantly recognize expensive vs. cheap pricing.

Smart “Safe” Deviation: Includes fallback logic to handle calculation errors if deviation hits zero, ensuring the indicator never crashes during data gaps.

🔧 Core Components

Basis Calculation: Uses a Simple Moving Average (SMA) to determine the market’s equilibrium point.

Standard Deviation Zones: Calculates 1SD, 2SD, and 3SD levels to define the statistical extremes of price action.

Sigmoid Alpha Calculation: Converts the SD distance into a transparency value (0-100) to drive the visual gradient.

🔥 Key Features

Automated Premium/Discount Zones: Red zones indicate overbought (Premium) areas; Green zones indicate oversold (Discount) areas.

Customizable Density: Users can adjust the “Steepness” and “Midpoint” of the sigmoid curve to control how fast the walls become solid.

Integrated Alerts: Built-in alert conditions trigger when price hits the “Solid” wall (2SD or higher), perfect for automated trading or notifications.

Visual Clarity: The center of the chart remains clear (high transparency) to keep focus on price action where it matters most.

🎨 Visualization

Equilibrium Line: A gray line representing the mean price.

Gradient Fills: The space between bands fills with color that increases in opacity as it moves outward.

Premium Wall: Upper zones fade from transparent red to solid red.

Discount Wall: Lower zones fade from transparent green to solid green.

📖 Usage Guidelines

Range Period: Default 20. Controls the lookback period for the SMA and Standard Deviation calculation.

Source: Default Close. The price data used for calculations.

Center Transparency: Default 100 (Clear). Controls how transparent the middle of the chart is.

Edge Transparency: Default 45 (Solid). Controls the opacity of the outermost liquidity wall.

Wall Steepness: Default 2.5. Adjusts how aggressively the gradient transitions from clear to solid.

Wall Start Point: Default 1.5 SD. The deviation level where the gradient shift begins to accelerate.

✅ Best Use Cases

Mean Reversion Trading: Enter trades when price hits the solid 2SD or 3SD wall and shows rejection wicks.

Take Profit Targets: Use the Equilibrium (Gray Line) as a logical first target for reversal trades.

Trend Filtering: Do not initiate new long positions when price is deep inside the Red (Premium) wall.

⚠️ Limitations

Lagging Nature: As a statistical tool based on Moving Averages, the walls react to past price data and may lag during sudden volatility spikes.

Trending Markets: In strong parabolic trends, price can “ride” the bands for extended periods; mean reversion should be used with caution in these conditions.

💡 What Makes This Unique

Physics-Based Visualization: We treat liquidity as a physical barrier that gets denser the deeper you push, rather than just a static line on a chart.

🔬 How It Works

Step 1: The script calculates the mean (SMA) and the Standard Deviation (SD) of the source price.

Step 2: It defines three zones above and below the mean (1SD, 2SD, 3SD).

Step 3: The custom `get_inverted_sigmoid` function calculates an Alpha (transparency) value based on the SD distance.

Step 4: Plot fills are colored dynamically, creating a seamless gradient that hardens at the extremes to visualize the “Liquidity Wall.”

💡 Note

For best results, combine this indicator with Price Action confirmation (such as pin bars or engulfing candles) when price touches the solid walls.

Volatility Signal-to-Noise Ratio🙏🏻 this is VSNR: the most effective and simple volatility regime detector & automatic volatility threshold scaler that somehow no1 ever talks about.

This is simply an inverse of the coefficient of variation of absolute returns, but properly constructed taking into account temporal information, and made online via recursive math with algocomplexity O(1) both in expanding and moving windows modes.

How do the available alternatives differ (while some’re just worse)?

Mainstream quant stat tests like Durbin-Watson, Dickey-Fuller etc: default implementations are ALL not time aware. They measure different kinds of regime, which is less (if at all) relevant for actual trading context. Mix of different math, high algocomplexity.

The closest one is MMI by financialhacker, but his approach is also not time aware, and has a higher algocomplexity anyways. Best alternative to mine, but pls modify it to use a time-weighted median.

Fractal dimension & its derivatives by John Ehlers: again not time aware, very low info gain, relies on bar sizes (high and lows), which don’t always exist unlike changes between datapoints. But it’s a geometric tool in essence, so this is fundamental. Let it watch your back if you already use it.

Hurst exponent: much higher algocomplexity, mix of parametric and non-parametric math inside. An invention, not a math entity. Again, not time aware. Also measures different kinds of regime.

How to set it up:

Given my other tools, I choose length so that it will match the amount of data that your trading method or study uses multiplied by ~ 4-5. E.g if you use some kind of bands to trade volatility and you calculate them over moving window 64, put VSNR on 256.

However it depends mathematically on many things, so for your methods you may instead need multipliers of 1 or ~ 16.

Additionally if you wanna use all data to estimate SNR, put 0 into length input.

How to use for regime detection:

First we define:

MR bias: mean reversion bias meaning volatility shorts would work better, fading levels would work better

Momo bias: momentum bias meaning volatility longs would work better, trading breakouts of levels would work better.

The study plots 3 horizontal thresholds for VSNR, just check its location:

Above upper level: significant Momo bias

Above 1 : Momo bias

Below 1 : MR bias

Below lower level: significant MR bias

Take a look at the screenshots, 2 completely different volatility regimes are spotted by VSNR, while an ADF does not show different regime:

^^ CBOT:ZN1!

^^ INDEX:BTCUSD

How to use as automatic volatility threshold scaler

Copy the code from the script, and use VSNR as a multiplier for your volatility threshold.

E.g you use a regression channel and fade/push upper and lower thresholds which are RMSEs multiples. Inside the code, multiply RMSE by VSNR, now you’re adaptive.

^^ The same logic as when MM bots widen spreads with vola goes wild.

How it works:

Returns follow Laplace distro -> logically abs returns follow exponential distro , cuz laplace = double exponential.

Exponential distro has a natural coefficient of variation = 1 -> signal to noise ratio defined as mean/stdev = 1 as well. The same can be said for Student t distro with parameter v = 4. So 1 is our main threshold.

We can add additional thresholds by discovering SNRs of Student t with v = 3 and v = 5 (+- 1 from baseline v = 4). These have lighter & heavier tails each favoring mean reversion or momentum more. I computed the SNR values you see in the code with mpmath python module, with precision 256 decimals, so you can trust it I put it on my momma.

Then I use exponential smoothing with properly defined alphas (one matches cumulative WMA and another minimizes error with WMA in moving window mode) to estimate SNR of abs returns.

…

Lightweight huh?

∞

Change in State of Delivery CISD [AlgoAlpha]🟠 OVERVIEW

This script tracks how price “changes delivery” after failed attempts to push in one direction. It builds swing levels from pivots, watches for those levels to be wicked, and then checks if price delivers cleanly in the opposite direction. When the pattern meets the script’s tolerance rules, it marks a Change in State of Delivery (CISD). These CISD levels are drawn as origin lines and are used to spot shifts in intent, failed pushes, and continuation attempts. A CISD becomes stronger when it forms after opposing liquidity is swept within a defined lookback.

🟠 CONCEPTS

The script first defines structure using swing highs/lows. These levels act as potential liquidity points. When price wicks through a swing, the script registers a mitigation event. After this, it looks for a reversal-style candle sequence: a failed push, followed by a counter-move strong enough to pass a tolerance ratio. This ratio compares how far price expanded away from the failed attempt versus the counter-move that followed. If the ratio is high enough, this becomes a CISD. The idea is simple: liquidity interaction sets context , and the tolerance logic identifies actual intent . CISD levels and sweep markers combine these two ideas into a clean map of where delivery flipped.

🟠 FEATURES

Liquidity tracking: marks swing highs/lows and updates them until expiry

Liquidity sweep confirmation when CISD aligns with recent mitigations

Alert conditions for all key events: mitigations, CISDs, and strong CISDs

🟠 USAGE

Setup : Add the script to your chart. Use it on any timeframe where swing behavior matters. Set the Swing Period for how wide a pivot must be. Set Noise Filter to control how strict the CISD detection is. Liquidity Lookback defines how recent a wick must be to confirm a sweep.

Read the chart : Origin lines mark where the CISD began. A green line signals bullish intent; a red line signals bearish intent. ▲ and ▼ shapes show CISDs that form after liquidity is swept, these mark strong signals for potential entry. Swing dots show recent swing highs/lows. Candle colors follow the latest CISD trend.

Settings that matter : Increasing Swing Period produces fewer but stronger swings. Raising Noise Filter requires cleaner counter-moves and reduces false CISDs. Liquidity Lookback controls how strict the sweep confirmation is. Expiry Bars decides how long swing levels remain active.

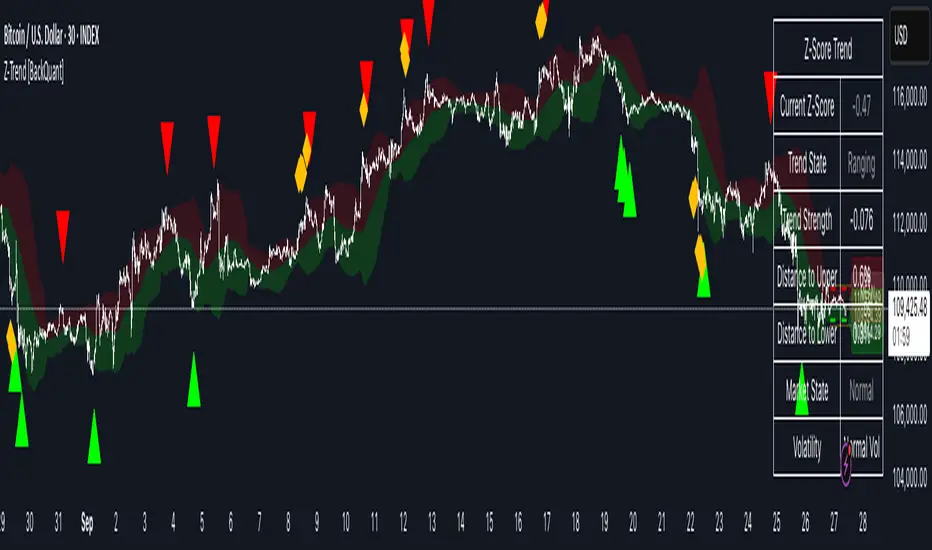

Uptrick: Dynamic Z-Score DivergenceIntroduction

Uptrick: Dynamic Z-Score Divergence is an oscillator that combines multiple momentum sources within a Z-Score framework, allowing for the detection of statistically significant mean-reversion setups, directional shifts, and divergence signals. It integrates a multi-source normalized oscillator, a slope-based signal engine, structured divergence logic, a slope-adaptive EMA with dynamic bands, and a modular bar coloring system. This script is designed to help traders identify statistically stretched conditions, evolving trend dynamics, and classical divergence behavior using a unified statistical approach.

Overview

At its core, this script calculates the Z-Score of three momentum sources—RSI, Stochastic RSI, and MACD—using a user-defined lookback period. These are averaged and smoothed to form the main oscillator line. This normalized oscillator reflects how far short-term momentum deviates from its mean, highlighting statistically extreme areas.

Signals are triggered when the oscillator reverses slope within defined inner zones, indicating a shift in direction while the signal remains in a statistically stretched state. These mean-reversion flips (referred to as TP signals) help identify turning points when price momentum begins to revert from extended zones.

In addition, the script includes a divergence detection engine that compares oscillator pivot points with price pivot points. It confirms regular bullish and bearish divergence by validating spacing between pivots and visualizes both the oscillator-side and chart-side divergences clearly.

A dynamic trend overlay system is included using a Slope Adaptive EMA (SA-EMA). This trend line becomes more responsive when Z-Score deviation increases, allowing the trend line to adapt to market conditions. It is paired with ATR-based bands that are slope-sensitive and selectively visible—offering context for dynamic support and resistance.

The script includes configurable bar coloring logic, allowing users to color candles based on oscillator slope, last confirmed divergence, or the most recent signal of any type. A full alert system is also built-in for key signals.

Originality

The script is based on the well-known concept of Z-Score valuation, which is a standard statistical method for identifying how far a signal deviates from its mean. This foundation—normalizing momentum values such as RSI or MACD to measure relative strength or weakness—is not unique to this script and is widely used in quantitative analysis.

What makes this implementation original is how it expands the Z-Score foundation into a fully featured, signal-producing system. First, it introduces a multi-source composite oscillator by combining three momentum inputs—RSI, Stochastic RSI, and MACD—into a unified Z-Score stream. Second, it builds on that stream with a directional slope logic that identifies turning points inside statistical zones.

The most distinctive additions are the layered features placed on top of this normalized oscillator:

A structured divergence detection engine that compares oscillator pivots with price pivots to validate regular bullish and bearish divergence using precise spacing and timing filters.

A fully integrated slope-adaptive EMA overlay, where the smoothing dynamically adjusts based on real-time Z-Score movement of RSI, allowing the trend line to become more reactive during high-momentum environments and slower during consolidation.

ATR-based dynamic bands that adapt to slope direction and offer real-time visual zones for support and resistance within trend structures.

These features are not typically found in standard Z-Score indicators and collectively provide a unique approach that bridges statistical normalization, structure detection, and adaptive trend modeling within one script.

Features

Z-Score-based oscillator combining RSI, StochRSI, and MACD

Configurable smoothing for stable composite signal output

Buy/Sell TP signals based on slope flips in defined zones

Background highlighting for extreme outer bands

Inner and outer zones with fill logic for statistical context

Pivot-based divergence detection (regular bullish/bearish)

Divergence markers on oscillator and price chart

Slope-Adaptive EMA (SA-EMA) with real-time adaptivity based on RSI Z-Score

ATR-based upper and lower bands around the SA-EMA, visibility tied to slope direction

Configurable bar coloring (oscillator slope, divergence, or most recent signal)

Alerts for TP signals and confirmed divergences

Optional fixed Y-axis scaling for consistent oscillator view

The full setup mode can be seen below:

Input Parameters

General Settings

Full Setup: Enables rendering of the full visual system (lines, bands, signals)

Z-Score Lookback: Lookback period for normalization (mean and standard deviation)

Main Line Smoothing: EMA length applied to the averaged Z-Score

Slope Detection Index: Used to calculate directional flips for signal logic

Enable Background Highlighting: Enables visual region coloring in

overbought/oversold areas

Force Visible Y-Axis Scale: Forces max/min bounds for a consistent oscillator range

Divergence Settings

Enable Divergence Detection: Toggles divergence logic

Pivot Lookback Left / Right: Defines the structure of oscillator pivot points

Minimum / Maximum Bars Between Pivots: Controls the allowed spacing range for divergence validation

Bar Coloring Settings

Bar Coloring Mode:

➜ Line Color: Colors bars based on oscillator slope

➜ Latest Confirmed Signal: Colors bars based on the most recent confirmed divergence

➜ Any Latest Signal: Colors based on the most recent signal (TP or divergence)

SA-EMA Settings

RSI Length: RSI period used to determine adaptivity

Z-Score Length: Lookback for normalizing RSI in adaptive logic

Base EMA Length: Base length for smoothing before adaptivity

Adaptivity Intensity: Scales the smoothing responsiveness based on RSI deviation

Slope Index: Determines slope direction for coloring and band logic

Band ATR Length / Band Multiplier: Controls the width and responsiveness of the trend-following bands

Alerts

The script includes the following alert conditions:

Buy Signal (TP reversal detected in oversold zone)

Sell Signal (TP reversal detected in overbought zone)

Confirmed Bullish Divergence (oscillator HL, price LL)

Confirmed Bearish Divergence (oscillator LH, price HH)

These alerts allow integration into automation systems or signal monitoring setups.

Summary

Uptrick: Dynamic Z-Score Divergence is a statistically grounded trading indicator that merges normalized multi-momentum analysis with real-time slope logic, divergence detection, and adaptive trend overlays. It helps traders identify mean-reversion conditions, divergence structures, and evolving trend zones using a modular system of statistical and structural tools. Its alert system, layered visuals, and flexible input design make it suitable for discretionary traders seeking to combine quantitative momentum logic with structural pattern recognition.

Disclaimer

This script is for educational and informational purposes only. No indicator can guarantee future performance, and trading involves risk. Always use risk management and test strategies in a simulated environment before deploying with live capital.

Baseline Deviation Oscillator [Alpha Extract]A sophisticated normalized oscillator system that measures price deviation from a customizable moving average baseline using ATR-based scaling and dynamic threshold adaptation. Utilizing advanced HL median filtering and multi-timeframe threshold calculations, this indicator delivers institutional-grade overbought/oversold detection with automatic zone adjustment based on recent oscillator extremes. The system's flexible baseline architecture supports six different moving average types while maintaining consistent ATR normalization for reliable signal generation across varying market volatility conditions.

🔶 Advanced Baseline Construction Framework

Implements flexible moving average architecture supporting EMA, RMA, SMA, WMA, HMA, and TEMA calculations with configurable source selection for optimal baseline customization. The system applies HL median filtering to the raw baseline for exceptional smoothing and outlier resistance, creating ultra-stable trend reference levels suitable for precise deviation measurement.

// Flexible Baseline MA System

ma(src, length, type) =>

if type == "EMA"

ta.ema(src, length)

else if type == "TEMA"

ema1 = ta.ema(src, length)

ema2 = ta.ema(ema1, length)

ema3 = ta.ema(ema2, length)

3 * ema1 - 3 * ema2 + ema3

// Baseline with HL Median Smoothing

Baseline_Raw = ma(src, MA_Length, MA_Type)

Baseline = hlMedian(Baseline_Raw, HL_Filter_Length)

🔶 ATR Normalization Engine

Features sophisticated ATR-based scaling methodology that normalizes price deviations relative to current volatility conditions, ensuring consistent oscillator readings across different market regimes. The system calculates ATR bands around the baseline and uses half the band width as the normalization factor for volatility-adjusted deviation measurement.

🔶 Dynamic Threshold Adaptation System

Implements intelligent threshold calculation using rolling window analysis of oscillator extremes with configurable smoothing and expansion parameters. The system identifies peak and trough levels over dynamic windows, applies EMA smoothing, and adds expansion factors to create adaptive overbought/oversold zones that adjust to changing market conditions.

1D

3D

1W

🔶 Multi-Source Configuration Architecture

Provides comprehensive source selection including Close, Open, HL2, HLC3, and OHLC4 options for baseline calculation, enabling traders to optimize oscillator behavior for specific trading styles. The flexible source system allows adaptation to different market characteristics while maintaining consistent ATR normalization methodology.

🔶 Signal Generation Framework

Generates bounce signals when oscillator crosses back through dynamic thresholds and zero-line crossover signals for trend confirmation. The system identifies both standard threshold bounces and extreme zone bounces with distinct alert conditions for comprehensive reversal and continuation pattern detection.

Bull_Bounce = ta.crossover(OSC, -Active_Lower) or

ta.crossover(OSC, -Active_Lower_Extreme)

Bear_Bounce = ta.crossunder(OSC, Active_Upper) or

ta.crossunder(OSC, Active_Upper_Extreme)

// Zero Line Signals

Zero_Cross_Up = ta.crossover(OSC, 0)

Zero_Cross_Down = ta.crossunder(OSC, 0)

🔶 Enhanced Visual Architecture

Provides color-coded oscillator line with bullish/bearish dynamic coloring, signal line overlay for trend confirmation, and optional cloud fills between oscillator and signal. The system includes gradient zone fills for overbought/oversold regions with configurable transparency and threshold level visualization with automatic label generation.

snapshot

🔶 HL Median Filter Integration

Features advanced high-low median filtering identical to DEMA Flow for exceptional baseline smoothing without lag introduction. The system constructs rolling windows of baseline values, performs median extraction for both odd and even window lengths, and eliminates outliers for ultra-clean deviation measurement baseline.

🔶 Comprehensive Alert System

Implements multi-tier alert framework covering bullish bounces from oversold zones, bearish bounces from overbought zones, and zero-line crossovers in both directions. The system provides real-time notifications for critical oscillator events with customizable message templates for automated trading integration.

🔶 Performance Optimization Framework

Utilizes efficient calculation methods with optimized array management for median filtering and minimal computational overhead for real-time oscillator updates. The system includes intelligent null value handling and automatic scale factor protection to prevent division errors during extreme market conditions.

🔶 Why Choose Baseline Deviation Oscillator ?

This indicator delivers sophisticated normalized oscillator analysis through flexible baseline architecture and dynamic threshold adaptation. Unlike traditional oscillators with fixed levels, the BDO automatically adjusts overbought/oversold zones based on recent oscillator behavior while maintaining consistent ATR normalization for reliable cross-market and cross-timeframe comparison. The system's combination of multiple MA type support, HL median filtering, and intelligent zone expansion makes it essential for traders seeking adaptive momentum analysis with reduced false signals and comprehensive reversal detection across cryptocurrency, forex, and equity markets.

INMERELO EMA Reclaim HighlighterOverview

The INMERELO EMA Reclaim indicator highlights intraday candles reclaiming a configurable EMA on any timeframe. It identifies candles based on customizable candle geometry filters and confirms momentum using a custom MACD setup.

Features

Configurable Intraday EMA

Any EMA length and timeframe. Default: 6-period EMA on chart timeframe.

Highlights when price reclaims the EMA after a configurable number of prior closes below it.

Candle Geometry Filters (ORB-Style)

Open Position: Maximum position of open relative to candle range (0–1). Default: 0.40

Close Position: Minimum position of close relative to candle range (0–1). Default: 0.70

Body Fraction: Minimum body size relative to candle range. Default: 0.50

Custom MACD Filter

Fast line above slow line.

Configurable: Fast (default 6), Slow (default 20), Signal (default 9).

Prior Closes Below EMA Filter

Configurable minimum number of prior closes below EMA. Default: 2

Visual Options

Paint candle with configurable color.

Optional arrow display above reclaim candle (toggleable).

Flexible

Works on any intraday timeframe, including 5-minute, 2-minute, 15-minute, etc.

Settings Overview

Setting Default Notes

EMA Length 6 EMA used for reclaim detection

EMA Timeframe Chart TF Can be set to any intraday timeframe

Open ≤ 0.40 ORB-style filter

Close ≥ 0.70 ORB-style filter

Body Fraction 0.50 ORB-style filter

Min Prior Closes Below EMA 2 Minimum closes below EMA before reclaim

MACD Fast 6 Custom MACD fast line

MACD Slow 20 Custom MACD slow line

MACD Signal 9 Custom MACD signal line

Paint Candle True Highlights valid candles

Candle Color Lime Configurable

Show Arrow False Optional visual

Summary:

The INMERELO EMA Reclaim indicator identifies intraday candles reclaiming a configurable EMA, filtered by customizable candle geometry and MACD momentum. Visual options include painted candles and optional arrows, and all settings are fully configurable.

Market Extreme Zones IndexThe Market Extreme Zones Index is a new mean reversion (valuation) tool focused on catching long term oversold/overbought zones. Combining an enhanced RSI with a smoothed Z-score this indicator allows traders to find oppurtunities during highly oversold/overbought zones.

I will separate the explanation into the following parts:

1. How does it work?

2. Methodologies & Concepts

3. Use cases

How does it work?

The indicator attempts to catch highly unprobable events in either direction to capture reversal points over the long term. This is done by calculating the Z-Score of an enhanced RSI.

First we need to calculate the Enhanced RSI:

For this we need to calculate 2 additional lengths:

Length1 = user defined length

Length2 = Length1/2

Length3 = √Length

Now we need to calculate 3 different RSIs:

1st RSI => uses classic user defined source and classic user defined length.

2nd RSI => uses classic user defined source and Length 2.

3rd RSI => uses RSI 2 as source and Length 2

Now calculate the divergence:

RSI_base => 2nd RSI * 3 - 1st RSI - 3rd RSI

After this we need to calculate the median of the RSI_base over √Length and make a divergence of these 2:

RSI => RSI_base*2 - median

All that remains now is the Z-score calculations:

We need:

Average RSI value

Standard Deviation = a measure of how dispersed or spread out a set of data values are from their average

Z-score = (Current Value - Average Value) / Standard Deviation

After this we just smooth the Z-score with a Weighted Moving average with √Length

Methodology & Concepts

Mean Reversion Methodology:

The methodology behind mean reversion is the theory that asset prices will eventually return to their long-term average after deviating significantly, driven by the belief that extreme moves are temporary.

Z-Score Methodology:

A Z-score, or standard score, is a statistical measure that indicates how many standard deviations a data point is from the mean of a dataset. A positive z-score means the value is above the mean, a negative score means it's below, and a score of zero means the value is equal to the mean.

You might already be able to see where I am going with this:

Z-Score could be used for the extreme moves to capture reversal points.

By applying it to the RSI rather than the Price, we get a more accurate measurement that allow us to get a banger indicator.

Use Cases

Capturing reversal points

Trend Direction

- while the main use it for mean reversion, the values can indicate whether we are in an uptrend or a downtrend.

Advantages:

Visualization:

The indicator has many plots to ensure users can easily see what the indicator signals, such as highlighting extreme conditions with background colors.

Versatility:

This indicator works across multiple assets, including the S&P500 and more, so it is not only for crypto.

Final note:

No indicator alone is perfect.

Backtests are not indicative of future performance.

Hope you enjoy Gs!

Good luck!

McMillan Volatility Bands (MVB) – with Entry Logic// McMillan Volatility Bands (MVB) with signal + entry logic

// Author: ChatGPT for OneRyanAlexander

// Notes:

// - Bands are computed using percentage volatility (log returns), per the Black‑Scholes framing.

// - Inner band (default 3σ) and outer band (default 4σ) are configurable.

// - A setup occurs when price closes outside the outer band, then closes back within the inner band.

// The bar that re‑enters is the "signal bar." We then require price to trade beyond the signal bar's

// extreme by a user‑defined cushion (default 0.34 * signal bar range) to confirm entry.

// - Includes alertconditions for both setups and confirmed entries.

Ornstein-Uhlenbeck Trend Channel [BOSWaves]Ornstein-Uhlenbeck Trend Channel - Adaptive Mean Reversion with Dynamic Equilibrium Geometry

Overview

The Ornstein-Uhlenbeck Trend Channel introduces an advanced equilibrium-mapping framework that blends statistical mean reversion with adaptive trend geometry. Traditional channels and regression bands react linearly to volatility, often failing to capture the natural rhythm of price equilibrium. This model evolves that concept through a dynamic reversion engine, where equilibrium adapts continuously to volatility, trend slope, and structural bias - forming a living channel that bends, expands, and contracts in real time.

The result is a smooth, equilibrium-driven representation of market balance - not just trend direction. Instead of static bands or abrupt slope shifts, traders see fluid, volatility-aware motion that mirrors the natural pull-and-release dynamic of market behavior. Each channel visualizes the probabilistic boundaries of fair value, showing where price tends to revert and where it accelerates away from its statistical mean.

Unlike conventional envelopes or Bollinger-type constructs, the Ornstein-Uhlenbeck framework is volatility-reactive and equilibrium-sensitive, providing traders with a contextual map of where price is likely to stabilize, extend, or exhaust.

Theoretical Foundation

The Ornstein-Uhlenbeck Trend Channel is inspired by stochastic mean-reversion processes - mathematical models used to describe systems that oscillate around a drifting equilibrium. While linear regression channels assume constant variance, financial markets operate under variable volatility and shifting equilibrium points. The OU process accounts for this by treating price as a mean-seeking motion governed by volatility and trend persistence.

At its core are three interacting components:

Equilibrium Mean (μ) : Represents the evolving balance point of price, adjusting to directional bias and volatility.

Reversion Rate (θ) : Defines how strongly price is pulled back toward equilibrium after deviation, capturing the self-correcting nature of market structure.

Volatility Coefficient (σ) : Controls how far and how quickly price can diverge from equilibrium before mean reversion pressure increases.

By embedding this stochastic model inside a volatility-adjusted framework, the system accurately scales across different markets and conditions - maintaining meaningful equilibrium geometry across crypto, forex, indices, or commodities. This design gives traders a mathematically grounded yet visually intuitive interpretation of dynamic balance in live market motion.

How It Works

The Ornstein-Uhlenbeck Trend Channel is constructed through a structured multi-stage process that merges stochastic logic with volatility mechanics:

Equilibrium Estimation Core : The indicator begins by identifying the evolving mean using adaptive smoothing influenced by trend direction and volatility. This becomes the live centerline - the statistical anchor around which price naturally oscillates.

Volatility Normalization Layer : ATR or rolling deviation is used to calculate volatility intensity. The output scales the channel width dynamically, ensuring that boundaries reflect current variance rather than static thresholds.

Directional Bias Engine : EMA slope and trend confirmation logic determine whether equilibrium should tilt upward or downward. This creates asymmetrical channel motion that bends with the prevailing trend rather than staying horizontal.

Channel Boundary Construction : Upper and lower bands are plotted at volatility-proportional distances from the mean. These envelopes form the “statistical pressure zones” that indicate where mean reversion or acceleration may occur.

Signal and Lifecycle Control : Channel breaches, mean crossovers, and slope flips mark statistically significant events - exhaustion, continuation, or rebalancing. Older equilibrium zones gradually fade, ensuring a clear, context-aware visual field.

Through these layers, the channel forms a continuously updating equilibrium corridor that adapts in real time - breathing with the market’s volatility and rhythm.

Interpretation

The Ornstein-Uhlenbeck Trend Channel reframes how traders interpret balance and momentum. Instead of viewing price as directional movement alone, it visualizes the constant tension between trending force and equilibrium pull.

Uptrend Phases : The equilibrium mean tilts upward, with price oscillating around or slightly above the midline. Upper band touches signal momentum extension; lower touches reflect healthy reversion.

Downtrend Phases : The mean slopes downward, with upper-band interactions marking resistance zones and lower bands acting as reversion boundaries.

Equilibrium Transitions : Flat mean sections indicate balance or distribution phases. Breaks from these neutral zones often precede directional expansion.

Overextension Events : When price closes beyond an outer boundary, it marks statistically significant disequilibrium - an early warning of exhaustion or volatility reset.

Visually, the OU channel translates volatility and equilibrium into structured geometry, giving traders a statistical lens on trend quality, reversion probability, and volatility stress points.

Strategy Integration

The Ornstein-Uhlenbeck Trend Channel integrates seamlessly into both mean-reversion and trend-continuation systems:

Trend Alignment : Use mean slope direction to confirm higher-timeframe bias before entering continuation setups.

Reversion Entries : Target rejections from outer bands when supported by volume or divergence, capturing snapbacks toward equilibrium.

Volatility Breakout Mapping : Monitor boundary expansions to identify transition from compression to expansion phases.

Liquidity Zone Confirmation : Combine with BOS or order-block indicators to validate structural zones against equilibrium positioning.

Momentum Filtering : Align with oscillators or volume profiles to isolate equilibrium-based pullbacks with statistical context.

Technical Implementation Details

Core Engine : Stochastic Ornstein-Uhlenbeck process for continuous mean recalibration.

Volatility Framework : ATR- and deviation-based scaling for dynamic channel expansion.

Directional Logic : EMA-slope driven bias for adaptive mean tilt.

Channel Composition : Independent upper and lower envelopes with smoothing and transparency control.

Signal Structure : Alerts for mean crossovers and boundary breaches.

Performance Profile : Lightweight, multi-timeframe compatible implementation optimized for real-time responsiveness.

Optimal Application Parameters

Timeframe Guidance:

1 - 5 min : Reactive equilibrium tracking for short-term scalping and microstructure analysis.

15 - 60 min : Medium-range setups for volatility-phase transitions and intraday structure.

4H - Daily : Macro equilibrium mapping for identifying exhaustion, distribution, or reaccumulation zones.

Suggested Configuration:

Mean Length : 20 - 50

Volatility Multiplier : 1.5× - 2.5×

Reversion Sensitivity : 0.4 - 0.8

Smoothing : 2 - 5

Parameter tuning should reflect asset liquidity, volatility, and desired reversion frequency.

Performance Characteristics

High Effectiveness:

Trending environments with cyclical pullbacks and volatility oscillation.

Markets exhibiting consistent equilibrium-return behavior (indices, majors, high-cap crypto).

Reduced Effectiveness:

Low-volatility consolidations with minimal variance.

Random walk markets lacking definable equilibrium anchors.

Integration Guidelines

Confluence Framework : Pair with BOSWaves structural tools or momentum oscillators for context validation.

Directional Control : Follow mean slope alignment for directional conviction before acting on channel extremes.

Risk Calibration : Use outer band violations for controlled contrarian entries or trailing stop management.

Multi-Timeframe Synergy : Derive macro equilibrium zones on higher timeframes and refine entries on lower levels.

Disclaimer

The Ornstein-Uhlenbeck Trend Channel is a professional-grade equilibrium and volatility framework. It is not predictive or profit-assured; performance depends on parameter calibration, volatility regime, and disciplined execution. BOSWaves recommends using it as part of a comprehensive analytical stack combining structure, liquidity, and momentum context.

Multi-Anchor VWAP | Trade Symmetry🧩 Multi-Anchor VWAP

Description:

Dynamic VWAP anchored to Session, Week, Month, Quarter, and Year — all in one view.

Full Description:

This indicator plots multiple VWAPs (Volume-Weighted Average Prices) simultaneously — each anchored to a different time period:

Session, Week, Month, Quarter, and Year.

💡 Ideal for traders who track institutional mean reversion and liquidity zones across multiple timeframes.

Features

✅ Session, Weekly, Monthly, Quarterly, and Yearly Anchored VWAPs

✅ Independent color and visibility controls for each anchor

✅ Adjustable label position and size

✅ Option to hide VWAPs on Daily or higher charts

✅ Clean and efficient performance

This tool helps you visualize volume-weighted mean levels where price often reacts — offering a clear map of bias and equilibrium across all major time horizons.

Volume Sentiment Breakout Channels [AlgoAlpha]🟠 OVERVIEW

This tool visualizes breakout zones based on volume sentiment within dynamic price channels . It identifies high-impact consolidation areas, quantifies buy/sell dominance inside those zones, and then displays real-time shifts in sentiment strength. When the market breaks above or below these sentiment-weighted channels, traders can interpret the event as a change in conviction, not just a technical breakout.

🟠 CONCEPTS

The script builds on two layers of logic:

Channel Detection : A volatility-based algorithm locates price compression areas using normalized highs and lows over a defined lookback. These “boxes” mark accumulation or distribution ranges.

Volume Sentiment Profiling : Each channel is internally divided into small bins, where volume is aggregated and signed by candle direction. This produces a granular sentiment map showing which levels are dominated by buyers or sellers.

When a breakout occurs, the script clears the previous box and forms a new one, letting traders visually track transitions between phases of control. The colored gradients and text updates continuously reflect the internal bias—green for net-buying, red for net-selling—so you can see conviction strength at a glance.

🟠 FEATURES

Volume-weighted sentiment map inside each box, with gradient color intensity proportional to participation.

Dynamic text display of current and overall sentiment within each channel.

Real-time trail lines to show active bullish/bearish trend extensions after breakout.

🟠 USAGE

Setup : Add the script to your chart and enable Strong Closes Only if you prefer cleaner breakouts. Use shorter normalization length (e.g., 50–80) for fast markets; longer (100–200) for smoother transitions.

Read Signals : Transparent boxes mark active sentiment channels. Green gradients show buy-side dominance, red shows sell-side. The middle dashed line is the equilibrium of the channel. “▲” appears when price breaks upward, “▼” when it breaks downward.

Understanding Sentiment : The sentiment profile can be used to show the probability of the price moving up or down at respective price levels.

VWAP Composites📊 VWAP Composite - Advanced Multi-Period Volume Weighted Average Price Indicator

═══════════════════════════════════════════════════════════════════

🎯 OVERVIEW

VWAP Composite is an advanced volume-weighted average price (VWAP) indicator that goes beyond traditional single-period VWAP calculations by offering composite multi-period analysis and unprecedented customization. This indicator solves a common problem traders face: traditional VWAP resets at arbitrary intervals (session start, day, week), but significant price action and volume accumulation often spans multiple periods. VWAP Composite allows you to anchor VWAP calculations to any timeframe—or combine multiple periods into a single composite VWAP—giving you a true representation of average price weighted by volume across the exact periods that matter to your analysis.

═══════════════════════════════════════════════════════════════════

⚙️ HOW IT WORKS - CALCULATION METHODOLOGY

📌 CORE VWAP CALCULATION

The indicator calculates VWAP using the standard volume-weighted formula:

• Typical Price = (High + Low + Close) / 3

• VWAP = Σ(Typical Price × Volume) / Σ(Volume)

This calculation is performed across user-defined time periods, ensuring each bar's contribution to the average is proportional to its trading volume.

📌 STANDARD DEVIATION BANDS

The indicator calculates volume-weighted standard deviation to measure price dispersion around the VWAP:

• Variance = Σ / Σ(Volume)

• Standard Deviation = √Variance

• Upper Band = VWAP + (StdDev × Multiplier)

• Lower Band = VWAP - (StdDev × Multiplier)

These bands help identify overbought/oversold conditions relative to the volume-weighted mean, with high-volume price excursions having greater impact on band width than low-volume moves.

📌 COMPOSITE PERIOD METHODOLOGY (Auto Mode)

Unlike traditional VWAP that resets at fixed intervals, Auto Mode creates composite VWAPs by combining the current period with N previous periods:

• Period Span = 1: Current period only (standard VWAP behavior)

• Period Span = 2: Current period + 1 previous period combined

• Period Span = 3: Current period + 2 previous periods combined

• And so on...

Example: A 3-period Weekly composite VWAP calculates from the start of 2 weeks ago through the current week's end, creating a single VWAP that represents 21 days of continuous price and volume data. This provides context about where price stands relative to the volume-weighted average over multiple weeks, not just the current week.

═══════════════════════════════════════════════════════════════════

🔧 KEY FEATURES & ORIGINALITY

✅ DUAL OPERATING MODES

1️⃣ MANUAL MODE (5 Independent VWAPs)

Define up to 5 separate VWAP calculations with custom start/end times:

• Perfect for anchoring VWAP to specific events (earnings, Fed announcements, major reversals)

• Each VWAP has independent color settings for lines and deviation band backgrounds

• Individual control over calculation extension and visual extension (explained below)

• Useful for tracking multiple institutional accumulation/distribution zones simultaneously

2️⃣ AUTO MODE (Composite Period VWAP)

Automatically calculates VWAP across combined time periods:

• Supported periods: Daily, Weekly, Monthly, Quarterly, Yearly

• Configurable period span (1-20 periods)

• Always up-to-date, recalculates on each new bar

• Ideal for systematic analysis across consistent timeframes

✅ DUAL EXTENSION SYSTEM (Manual Mode Innovation)

Most VWAP indicators only offer "on/off" for extending calculations. This indicator provides two distinct extension options:

🔹 EXTEND CALCULATION TO CURRENT BAR

When enabled, continues including new bars in the VWAP calculation after the defined end time. The VWAP value updates dynamically as new volume enters the market.

Use case: You anchored VWAP to a major low 3 weeks ago. You want the VWAP to continue evolving with new volume data to track ongoing institutional positioning.

🔹 EXTEND VISUAL LINE ONLY

When enabled (and calculation extension is disabled), projects the "frozen" VWAP value forward as a reference line. The VWAP value remains fixed at what it was at the end time, but the line and deviation bands visually extend to current price.

Use case: You want to see how price is behaving relative to the VWAP that existed at a specific point in time (e.g., "Where is price now vs. the 5-day VWAP that existed at last Friday's close?").

This dual system gives you unprecedented control over whether you're tracking a "living" VWAP that incorporates new data or using historical VWAP levels as static reference points.

✅ CUSTOMIZABLE STANDARD DEVIATION BANDS

• Adjustable multiplier (0.1 to 5.0)

• Independent background colors with opacity control for each VWAP

• Dashed band lines for easy visual distinction from main VWAP

• Bands extend when visual extension is enabled, maintaining zone visibility

✅ COMPREHENSIVE LABELING SYSTEM

Each VWAP displays:

• Current VWAP value

• Upper deviation band value (High)

• Lower deviation band value (Low)

• Extension status indicator (Calc Extended / Visual Extended)

• Color-coded for quick identification

═══════════════════════════════════════════════════════════════════

📖 HOW TO USE THIS INDICATOR

🎯 SCENARIO 1: EVENT-ANCHORED VWAP (Manual Mode)

Use case: A stock gaps down 15% on earnings and you want to track where institutions are positioning during the recovery.

Setup:

1. Switch to Manual Mode

2. Enable VWAP 1

3. Set Start Time to the earnings gap bar

4. Set End Time to current time (or leave far in future)

5. Enable "Extend Calculation to Current Bar"

6. Watch how price respects the VWAP as a dynamic support/resistance

Interpretation:

• Price above VWAP = buyers in control since the event

• Price testing VWAP from above = potential support

• Volume-weighted standard deviation bands show normal price range

• Price outside bands = potential exhaustion/mean reversion setup

🎯 SCENARIO 2: MULTI-WEEK INSTITUTIONAL ACCUMULATION ZONE (Auto Mode)

Use case: You trade swing setups and want to identify where institutions have been accumulating over the past 3 weeks.

Setup:

1. Switch to Auto Mode

2. Select "Weekly" period type

3. Set Period Span to 3

4. Enable standard deviation bands

Interpretation:

• 3-week composite VWAP shows the true average institutional entry

• Price bouncing off VWAP repeatedly = strong support (institutions defending their average)

• Price breaking below VWAP on high volume = potential distribution

• Deviation bands contracting = consolidation; expanding = volatility increase

🎯 SCENARIO 3: COMPARING MULTIPLE TIME HORIZONS (Manual Mode)

Use case: You want to see short-term vs medium-term vs long-term VWAP alignments.

Setup:

1. Switch to Manual Mode

2. VWAP 1: Last 5 trading days (blue)

3. VWAP 2: Last 10 trading days (orange)

4. VWAP 3: Last 20 trading days (purple)

5. Enable "Extend Calculation" for all

6. Set different background colors for visual separation

Interpretation:

• All VWAPs aligned upward = strong trend across all timeframes

• Price between VWAPs = finding equilibrium between different trader timeframes

• Short-term VWAP crossing long-term VWAP = momentum shift

• Price rejecting at higher-timeframe VWAP = that timeframe's traders defending their average

🎯 SCENARIO 4: HISTORICAL VWAP REFERENCE LEVELS (Manual Mode)

Use case: You want to see where the 1-month VWAP was at each month-end as static reference levels.

Setup:

1. Switch to Manual Mode

2. VWAP 1: Set to last month's start/end dates

3. VWAP 2: Set to 2 months ago start/end dates

4. VWAP 3: Set to 3 months ago start/end dates

5. Disable "Extend Calculation"

6. Enable "Extend Visual Line Only"

Interpretation:

• Each VWAP represents the volume-weighted average for that complete month

• These become static support/resistance levels

• Price returning to old monthly VWAPs = institutional memory/gap fill behavior

• Useful for identifying longer-term value areas

═══════════════════════════════════════════════════════════════════

🎨 CUSTOMIZATION OPTIONS

GENERAL SETTINGS

• Show/hide labels

• Line style: Solid, Dashed, or Dotted

• Standard deviation multiplier (impacts band width)

• Toggle standard deviation bands on/off

MANUAL MODE (Per VWAP)

• Custom start and end times

• Line color picker

• Background color picker (with transparency control)

• Extend calculation option

• Extend visual option

• Show/hide individual VWAPs

AUTO MODE

• Period type selection (Daily/Weekly/Monthly/Quarterly/Yearly)

• Period span (1-20 periods)

• Line color

• Background color (with transparency control)

═══════════════════════════════════════════════════════════════════

💡 TRADING APPLICATIONS

✓ Mean Reversion: Use deviation bands to identify stretched prices likely to return to VWAP

✓ Trend Confirmation: Price sustained above VWAP = bullish bias; below = bearish bias

✓ Support/Resistance: VWAP often acts as dynamic S/R, especially on higher volume periods

✓ Institutional Positioning: Multi-day/week VWAPs show where large players have established positions

✓ Entry Timing: Wait for pullbacks to VWAP in trending markets

✓ Stop Placement: Use VWAP ± standard deviation as volatility-adjusted stop levels

✓ Breakout Confirmation: Breakouts from consolidation with price reclaiming VWAP = stronger signal

✓ Multi-Timeframe Analysis: Compare short vs long-period VWAPs to gauge momentum alignment

═══════════════════════════════════════════════════════════════════

⚠️ IMPORTANT NOTES

• The indicator redraws on each bar to maintain accurate visual representation (uses `barstate.islast`)

• Maximum lookback is limited to 5000 bars for performance optimization

• Time range calculations work across all timeframes but are most effective on intraday to daily charts

• Standard deviation bands assume volume-weighted distribution; extreme events may violate assumptions

• Auto mode always calculates to current bar; use Manual mode for fixed historical periods

═══════════════════════════════════════════════════════════════════

This indicator is open-source. Feel free to examine the code, learn from it, and adapt it to your needs.

Mean Reversion Oscillator [Alpha Extract]An advanced composite oscillator system specifically designed to identify extreme market conditions and high-probability mean reversion opportunities, combining five proven oscillators into a single, powerful analytical framework.

By integrating multiple momentum and volume-based indicators with sophisticated extreme level detection, this oscillator provides precise entry signals for contrarian trading strategies while filtering out false reversals through momentum confirmation.

🔶 Multi-Oscillator Composite Framework

Utilizes a comprehensive approach that combines Bollinger %B, RSI, Stochastic, Money Flow Index, and Williams %R into a unified composite score. This multi-dimensional analysis ensures robust signal generation by capturing different aspects of market extremes and momentum shifts.

// Weighted composite (equal weights)

normalized_bb = bb_percent

normalized_rsi = rsi

normalized_stoch = stoch_d_val

normalized_mfi = mfi

normalized_williams = williams_r

composite_raw = (normalized_bb + normalized_rsi + normalized_stoch + normalized_mfi + normalized_williams) / 5

composite = ta.sma(composite_raw, composite_smooth)

🔶 Advanced Extreme Level Detection

Features a sophisticated dual-threshold system that distinguishes between moderate and extreme market conditions. This hierarchical approach allows traders to identify varying degrees of mean reversion potential, from moderate oversold/overbought conditions to extreme levels that demand immediate attention.

🔶 Momentum Confirmation System

Incorporates a specialized momentum histogram that confirms mean reversion signals by analyzing the rate of change in the composite oscillator. This prevents premature entries during strong trending conditions while highlighting genuine reversal opportunities.

// Oscillator momentum (rate of change)

osc_momentum = ta.mom(composite, 5)

histogram = osc_momentum

// Momentum confirmation

momentum_bullish = histogram > histogram

momentum_bearish = histogram < histogram

// Confirmed signals

confirmed_bullish = bullish_entry and momentum_bullish

confirmed_bearish = bearish_entry and momentum_bearish

🔶 Dynamic Visual Intelligence

The oscillator line adapts its color intensity based on proximity to extreme levels, providing instant visual feedback about market conditions. Background shading creates clear zones that highlight when markets enter moderate or extreme territories.

🔶 Intelligent Signal Generation

Generates precise entry signals only when the composite oscillator crosses extreme thresholds with momentum confirmation. This dual-confirmation approach significantly reduces false signals while maintaining sensitivity to genuine mean reversion opportunities.

How It Works

🔶 Composite Score Calculation

The indicator simultaneously tracks five different oscillators, each normalized to a 0-100 scale, then combines them into a smoothed composite score. This approach eliminates the noise inherent in single-oscillator analysis while capturing the consensus view of multiple momentum indicators.

// Mean reversion entry signals

bullish_entry = ta.crossover(composite, 100 - extreme_level) and composite < (100 - extreme_level)

bearish_entry = ta.crossunder(composite, extreme_level) and composite > extreme_level

// Bollinger %B calculation

bb_basis = ta.sma(src, bb_length)

bb_dev = bb_mult * ta.stdev(src, bb_length)

bb_percent = (src - bb_lower) / (bb_upper - bb_lower) * 100

🔶 Extreme Zone Identification

The system automatically identifies when markets reach statistically significant extreme levels, both moderate (65/35) and extreme (80/20). These zones represent areas where mean reversion has the highest probability of success based on historical market behavior.

🔶 Momentum Histogram Analysis

A specialized momentum histogram tracks the velocity of oscillator changes, helping traders distinguish between healthy corrections and potential trend reversals. The histogram's color-coded display makes momentum shifts immediately apparent.

🔶 Divergence Detection Framework

Built-in divergence analysis identifies situations where price and oscillator movements diverge, often signaling impending reversals. Diamond-shaped markers highlight these critical divergence patterns for enhanced pattern recognition.

🔶 Real-Time Information Dashboard

An integrated information table provides instant access to current oscillator readings, market status, and individual component values. This dashboard eliminates the need to manually check multiple indicators while trading.

🔶 Individual Component Display

Optional display of individual oscillator components allows traders to understand which specific indicators are driving the composite signal. This transparency enables more informed decision-making and deeper market analysis.

🔶 Adaptive Background Coloring

Intelligent background shading automatically adjusts based on market conditions, creating visual zones that correspond to different levels of mean reversion potential. The subtle color gradations make pattern recognition effortless.

1D

3D

🔶 Comprehensive Alert System

Multi-tier alert system covers confirmed entry signals, divergence patterns, and extreme level breaches. Each alert type provides specific context about the detected condition, enabling traders to respond appropriately to different signal strengths.

🔶 Customizable Threshold Management

Fully adjustable extreme and moderate levels allow traders to fine-tune the indicator's sensitivity to match different market volatilities and trading timeframes. This flexibility ensures optimal performance across various market conditions.

🔶 Why Choose AE - Mean Reversion Oscillator?

This indicator provides the most comprehensive approach to mean reversion trading by combining multiple proven oscillators with advanced confirmation mechanisms. By offering clear visual hierarchies for different extreme levels and requiring momentum confirmation for signals, it empowers traders to identify high-probability contrarian opportunities while avoiding false reversals. The sophisticated composite methodology ensures that signals are both statistically significant and practically actionable, making it an essential tool for traders focused on mean reversion strategies across all market conditions.

Volume Delta [BigBeluga]🔵 OVERVIEW

The Volume Delta indicator visualizes the dominance between buying and selling volume within a given period. It calculates the percentage of bullish (buy) versus bearish (sell) volume, then color-codes the candles and provides a real-time dashboard comparing delta values across multiple currency pairs. This makes it a powerful tool for monitoring order-flow strength and intermarket relationships in real time.

🔵 CONCEPTS

Each bar’s buy volume is counted when the close is higher than the open.

Each bar’s sell volume is counted when the close is lower than the open.

volumeBuy = 0.

volumeSell = 0.

for i = 0 to period

if close > open

volumeBuy += volume

else

volumeSell += volume

The indicator sums both over a chosen period to calculate the ratio of buy-to-sell pressure.

Delta (%) = (Buy Volume ÷ (Buy Volume + Sell Volume)) × 100.

Gradient colors highlight whether buying or selling pressure dominates.

🔵 FEATURES

Calculates real-time Volume Delta for the selected chart or for multiple assets.

Colors candles dynamically based on the delta intensity (green = buy pressure, red = sell pressure).

Displays a dashboard table showing volume delta % for up to five instruments.

The dashboard features visual progress bars for quick intermarket comparison.