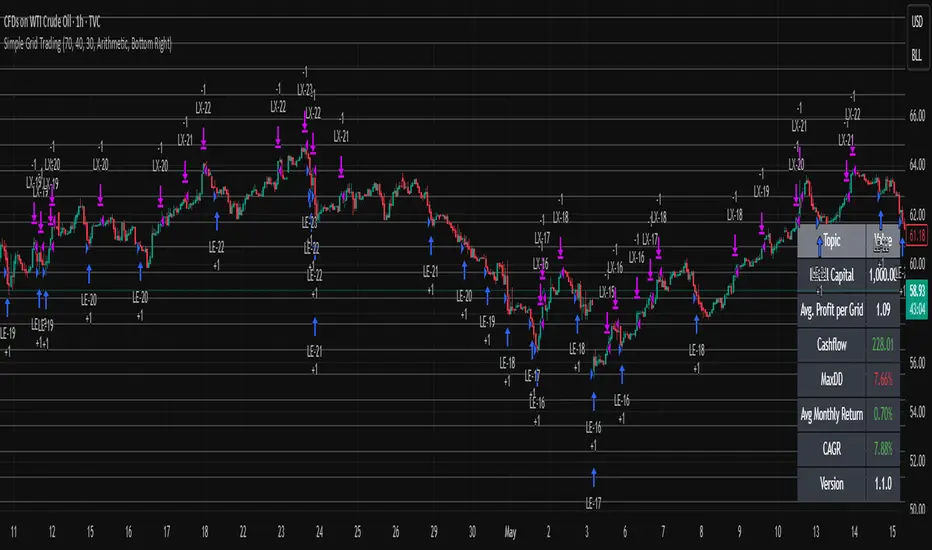

Simple Grid Trading v1.0 [PUCHON]Simple Grid Trading v1.0

Overview

This is a Long-Only Grid Trading Strategy developed in Pine Script v6 for TradingView. It is designed to profit from market volatility by placing a series of Buy Limit orders at predefined price levels. As the price drops, the strategy accumulates positions. As the price rises, it sells these positions at a profit.

Features

Grid Types : Supports both Arithmetic (equal price spacing) and Geometric (equal percentage spacing) grids.

Flexible Order Management : Uses strategy.order for precise control and prevents duplicate orders at the same level.

Performance Dashboard : A real-time table displaying key metrics like Capital, Cashflow, and Drawdown.

Advanced Metrics : Includes Max Drawdown (MaxDD) , Avg Monthly Return , and CAGR calculations.

Customizable : Fully adjustable price range, grid lines, and lot size.

Dashboard Metrics

The dashboard (default: Bottom Right) provides a quick snapshot of the strategy's performance:

Initial Capital : The starting capital defined in the strategy settings.

Lot Size : The fixed quantity of assets purchased per grid level.

Avg. Profit per Grid : The average realized profit for each closed trade.

Cashflow : The total realized net profit (closed trades only).

MaxDD : Maximum Drawdown . The largest percentage drop in equity (realized + unrealized) from a peak.

Avg Monthly Return : The average percentage return generated per month.

CAGR : Compound Annual Growth Rate . The mean annual growth rate of the investment over the specified time period.

Strategy Settings (Inputs)

Grid Settings

Upper Price : The highest price level for the grid.

Lower Price : The lowest price level for the grid.

Number of Grid Lines : The total number of levels (lines) in the grid.

Grid Type :

Arithmetic: Distance between lines is fixed in price terms (e.g., $10, $20, $30).

Geometric: Distance between lines is fixed in percentage terms (e.g., 1%, 2%, 3%).

Lot Size : The fixed amount of the asset to buy at each level.

Dashboard Settings

Show Dashboard : Toggle to hide/show the performance table.

Position : Choose where the dashboard appears on the chart (e.g., Bottom Right, Top Left).

How It Works

Initialization : On the first bar, the script calculates the price levels based on your Upper/Lower price and Grid Type.

Entry Logic :

The strategy places Buy Limit orders at every grid level below the current price.

It checks if a position already exists at a specific level to avoid "stacking" multiple orders on the same line.

Exit Logic :

For every Buy order, a corresponding Sell Limit (Take Profit) order is placed at the next higher grid level.

MaxDD Calculation :

The script continuously tracks the highest equity peak.

It calculates the drawdown on every bar (including intra-bar movements) to ensure accuracy.

Displayed as a percentage (e.g., 5.25%).

Disclaimer

This script is for educational and backtesting purposes only. Grid trading involves significant risk, especially in strong trending markets where the price may move outside your grid range. Always use proper risk management.

GRID

EMA Grid + Martingale Strategy (Long-Only) with CooldownTitle:

EMA Grid + Martingale Strategy (Long-Only) with Cooldown

Short Summary:

A long-only strategy combining EMA trend filters, grid-based entries, optional martingale sizing, and a cooldown feature to manage position timing and exits.

Full Description:

This strategy uses a 4-EMA trend confirmation system to detect bullish momentum, then deploys a grid-style entry method with optional martingale position sizing. It includes a cooldown mechanism to prevent reentry too soon after a completed trade cycle.

How It Works

1. Trend Confirmation: Two EMA groups (fast/slow) determine whether market conditions are bullish.

2. Initial Entry: A new position is entered when both EMA groups confirm an uptrend and no position is currently active.

3. Grid Entries: Additional long entries are placed when price drops by a defined pip distance from the last entry, respecting the maximum number of entries.

4. Martingale Sizing (Optional): Grid orders can increase in size with each level using a customizable multiplier.

5. Weighted-Average Exit: All positions close once price reaches or exceeds the average entry price plus a buffer.

6. Cooldown Timer: After closing a position set, the strategy waits a defined number of bars before opening a new grid.

Key Features

• 4 customizable EMAs for trend confirmation.

• Dynamic grid-style long entries based on pip intervals.

• Optional martingale-style position sizing.

• Weighted-average price exit logic with buffer control.

• Cooldown bar period to limit overtrading.

• Suitable for optimization and backtesting with full control over inputs.

Use Cases

• Designed for trending markets where pullbacks present entry opportunities.

• Helps manage staged entries while avoiding premature reentry.

• Ideal for testing martingale and grid-based strategies with exit precision.

Note: This strategy is for testing and educational purposes only. It does not guarantee profits and is not financial advice.

Grid TLong V1The “Grid TLong V1” strategy is based on the classic Grid strategy, but in the mode of buying and selling in favor of the trend and only on Long. This allows to take advantage of large uptrend movements to maximize profits in bull markets. For this reason, excessively sideways or bearish markets may not be very conducive to this strategy.

Like our Grid strategies in favor of the trend, you can enter and exit with the balance with controlled risk, as the distance between each grid functions as a natural and adaptable stop loss and take profit. What differentiates it from bidirectional strategies is that Short uses a minimum amount of follow-through, so that the percentage distance between the grids is maintained.

In this version of the script the entries and exits can be chosen at market or limit , and are based on the profit or loss of the current position, not on the percentage change in price.

The user may also notice that the strategy setup is risk-controlled, because it risks 5% on each trade, has a fairly standard commission and modest initial capital, all in order to protect the strategy user from unrealistic results.

As with all strategies, it is strongly recommended to optimize the parameters for the strategy to be effective for each asset and for each time frame.

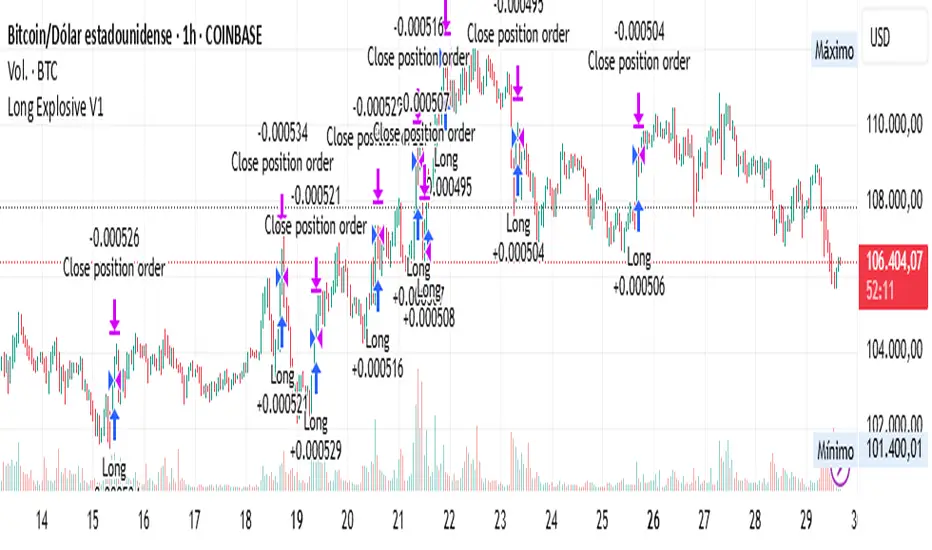

Long Explosive V1The “Long Explosive V1” strategy calculates the percentage change in price from the last closing price of the candlestick, so that if it increases by a certain percentage it goes long, but if it decreases by another percentage it sends an exit order, so that the percentage limits above and below the current price function as inherent stop loss and take profit, with the benefit of taking advantage of the volatility of the bull market.

Entries and exits are always at the market and based on percentage changes in the price. Of course, the default configuration of the strategy considers a position with a 5% risk control, modest initial capital and standard commissions, which helps to obtain realistic results and protect the user from unexpectedly controlled potential losses.

It is again emphasized that it is always advisable to adjust the parameters of the strategy well, so that the risk-reward is well controlled.

Grid Tendence V1The “Grid Tendence V1” strategy is based on the classic Grid strategy, only in this case the entries and exits are made in favor of the trend, which allows to take advantage of large movements to maximize profits, since it is also possible to enter and exit with the balance with a controlled risk, because precisely the distance between each Grid works as a natural and adaptable stop loss and take profit. This fact helps to avoid overlapping entries and exits that would result from using stop loss and take profit as limit orders.

In this version of the script the entries and exits are always at market, and based on the percentage change of the price, not on the profit or loss of the current position.

The user will notice that the strategy setup is based on a controlled risk, risking 5% on each trade, a fairly standard commission and a modest initial capital, all this in order to protect the user of the strategy from unexpected or unrealistic results.

However, it is always recommended to optimize the parameters so that the strategy is effective for each asset and for each time frame.

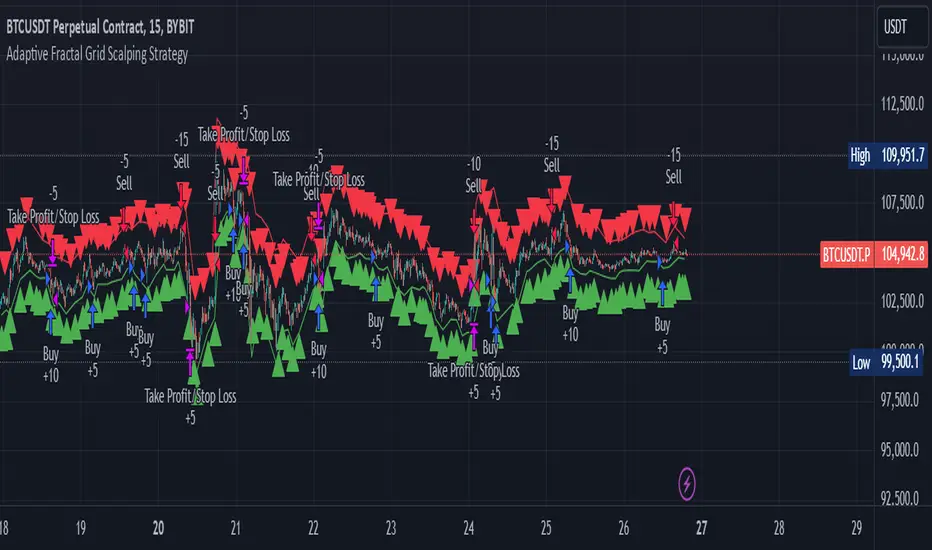

Adaptive Fractal Grid Scalping StrategyThis Pine Script v6 component implements an "Adaptive Fractal Grid Scalping Strategy" with an added volatility threshold feature.

Here's how it works:

Fractal Break Detection: Uses ta.pivothigh and ta.pivotlow to identify local highs and lows.

Volatility Clustering: Measures volatility using the Average True Range (ATR).

Adaptive Grid Levels: Dynamically adjusts grid levels based on ATR and user-defined multipliers.

Directional Bias Filter: Uses a Simple Moving Average (SMA) to determine trend direction.

Volatility Threshold: Introduces a new input to specify a minimum ATR value required to activate the strategy.

Trade Execution Logic: Places limit orders at grid levels based on trend direction and fractal levels, but only when ATR exceeds the volatility threshold.

Profit-Taking and Stop-Loss: Implements profit-taking at grid levels and a trailing stop-loss based on ATR.

How to Use

Inputs: Customize the ATR length, SMA length, grid multipliers, trailing stop multiplier, and volatility threshold through the input settings.

Visuals: The script plots fractal points and grid levels on the chart for easy visualization.

Trade Signals: The strategy automatically places buy/sell orders based on the detected fractals, trend direction, and volatility threshold.

Profit and Risk Management: The script includes logic for taking profits and setting stop-loss levels to manage trades effectively.

This strategy is designed to capitalize on micro-movements during high volatility and avoid overtrading during low-volatility trends. Adjust the input parameters to suit your trading style and market conditions.

FreedX Grid Backtest█ FreedX Grid Backtest is an open-source tool that offers accurate GRID calculations for GRID trading strategies. This advanced tool allows users to backtest GRID trading parameters with precision, accurately reflecting exchange functionalities. We are committed to enhancing trading strategies through precise backtesting solutions and address the issue of unreliable backtesting practices observed on GRID trading strategies. FreedX Grid Backtest is designed for optimal calculation speed and plotting efficiency, ensuring users to achieve fastest calculations during their analysis.

█ GRID TRADING STRATEGY SETTINGS

The core of the FreedX Grid Backtest tool lies in its ability to simulate grid trading strategies. Grid trading involves placing orders at regular intervals within a predefined price range, creating a grid of orders that capitalize on market volatility.

Features:

⚙️ Backtest Range:

→ Purpose: Allows users to specify the backtesting range of GRID strategy. Closes all positions at the end of this range.

→ How to Use: Drag the dates to fit the desired backtesting range.

⚙️ Investment & Compounding:

→ Purpose: Allows users to specify the total investment amount and select between fixed and compound investment strategies. Compounding adjusts trade quantities based on performance, enhancing the grid strategy's adaptability to market changes.

→ How to Use: Set the desired investment amount and choose between "Fixed" or "Compound" for the investment method.

⚙️ Leverage & Grid Levels:

→ Purpose: Leverage amplifies the investment amount, increasing potential returns (and risks). Users can define the number of grid levels, which determines how the investment is distributed across the grid.

→ How to Use: Input the desired leverage and number of grids. The tool automatically calculates the distribution of funds across each grid level.

⚙️ Distribution Type & Mode:

→ Purpose: Users can select the distribution type (Arithmetic or Geometric) to set how grid levels are determined. The mode (Neutral, Long, Short) dictates the direction of trades within the grid.

→ How to Use: Choose the distribution type and mode based on the desired trading strategy and market outlook.

⚙️ Enable LONG/SHORT Grids exclusively:

█ MANUAL LEVELS AND STOP TRIGGERS

Beyond automated settings, the tool offers manual adjustments for traders seeking finer control over their grid strategies.

Features:

⚙️ Manual Level Adjustment:

→ Purpose: Enables traders to manually set the top, reference, and bottom levels of the grid, offering precision control over the trading range.

→ How to Use: Activate manual levels and adjust the top, reference, and bottom levels as needed to define the grid's scope.

⚙️ Stop Triggers:

→ Purpose: Provides an option to set upper and lower price limits, acting as stop triggers to close or terminate trades. This feature safeguards investments against significant market movements outside the anticipated range.

→ How to Use: Enable stop triggers and specify the upper and lower limits. The tool will automatically manage positions based on these parameters.

---

This guide gives you a quick and clear overview of the FreedX Grid Backtest tool, explaining how you can use this cutting-edge tool to improve your trading strategies.

Grid Bot BacktestingBinance, Bybit, Bitget, and other cross-exchange (grid) trading bot backtesting.

Auto bound: Automatically setting upper and lower price bounds.

Manual: Setting upper and lower price bounds manually.

The graph below represents the overall asset changes (initial investment amount + current position profit + grid profit).

Try using backtesting when setting up a grid bot on the exchange!

바이낸스, 바이비트, 비트겟 등 교차거래(그리드) 봇 백테스팅

Auto bound : 자동으로 상,하단 가격 설정

Manual : 직접 상,하단 가격 설정

아래 그래프는 총 자산 변화입니다.(초기투자금액 + 현재 포지션 수익 + 그리드 수익)

거래소에서 그리드 봇 설정할 때 백테스팅 유용하게 써보세요!

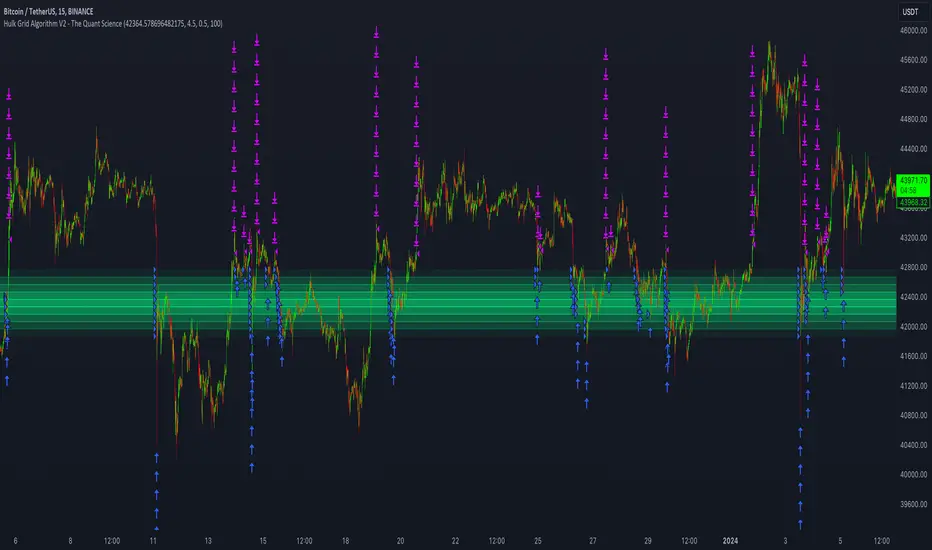

Hulk Grid Algorithm V2 - The Quant ScienceIt's the latest proprietary grid algorithm developed by our team. This software represents a clearer and more comprehensive modernization of the deprecated Hulk Grid Algorithm. In this new release, we have optimized the source code architecture and investment logic, which we will describe in detail below.

Overview

Hulk Grid Algorithm V2 is designed to optimize returns in sideways market conditions. In this scenario, the algorithm divides purchases with long orders at each level of the grid. Unlike a typical grid algorithm, this version applies an anti-martingale model to mitigate volatility and optimize the average entry price. Starting from the lower level, the purchase quantity is increased at each new subsequent level until reaching the upper level. The initial quantity of the first order is fixed at 0.50% of the initial capital. With each new order, the initial quantity is multiplied by a value equal to the current grid level (where 1 is the lower level and 10 is the upper level).

Example: Let's say we have an initial capital of $10,000. The initial capital for the first order would be $50 * 1 = $50, for the second order $50 * 2 = $100, for the third order $50 * 3 = $150, and so on until reaching the upper level.

All previously opened orders are closed using a percentage-based stop-loss and take-profit, calculated based on the extremes of the grid.

Set Up

As mentioned earlier, the user's goal is to analyze this strategy in markets with a lack of trend, also known as sideways markets. After identifying a price range within which the asset tends to move, the user can choose to create the grid by placing the starting price at the center of the range. This way, they can consider trading the asset, if the backtesting generates a return greater than the Buy & Hold return.

Grid Configuration

To create the grid, it's sufficient to choose the starting price during the launch phase. This level will be the center of the grid from which the upper and lower levels will be calculated. The grid levels are computed using an arithmetic method, adding and subtracting a configurable fixed amount from the user interface (Grid Step $).

Example: Let's imagine choosing 1000 as the starting price and 50 as the Grid Step ($). The upper levels will be 1000, 1050, 1100, 1150, 1200. The lower levels will be 950, 900, 850, 800, and 750.

Markets

This software can be used in all markets: stocks, indices, commodities, cryptocurrencies, ETFs, Forex, etc.

Application

With this backtesting software, is possible to analyze the strategy and search for markets where it can generate better performance than Buy & Hold returns. There are no alerts or automatic investment mechanisms, and currently, the strategy can only be executed manually.

Design

Is possible to modify the grid style and customize colors by accessing the Properties section of the user interface.

RSI Box Strategy (pseudo- Grid Bot)This is a strategy intended primarily for algorithmic traders. It's a pseudo-grid bot that uses a dynamic, volume-weighted grid that only updates when the RSI meets certain conditions. It's also a breakout strategy, whereas normal grid bots are not (typical grid bots sell when a higher grid is reached, whereas this strategy sells when a lower grid is breached under specific conditions). This strategy also sells 100% of pyramiding orders on close.

In a nutshell, the strategy updates its grid to the volume-weighted highest/lowest values of your given source ("src" in the settings) each time that there is a RSI crossunder/crossover. From this range it produces an evenly-spaced grid of five lines, and uses the current source to determine which grid line is closest to the source. Then, if the source crosses over the line directly above the current line, it enters a buy order. If the source crosses under the line directly below the current line, it enters a sell order.

You can configure shorts, source, RSI length, and overbought/oversold levels in the settings.

For the strategy results below: fees are at 0.1% per trade, with order size 1% of equity and a max pyramiding value of 33. For a greater R/R profile, you can increase the order size, which will increase drawdown but potentially yield better results.

Grid Spot Trading Algorithm V2 - The Quant ScienceGrid Spot Trading Algorithm V2 is the last grid trading algorithm made by our developer team.

Grid Spot Trading Algorithm V2 is a fixed 10-level grid trading algorithm. The grid is divided into an accumulation area (red) and a selling area (green).

In the accumulation area, the algorithm will place new buy orders, selling the long positions on the top of the grid.

BUYING AND SELLING LOGIC

The algorithm places up to 5 limit orders on the accumulation section of the grid, each time the price cross through the middle grid. Each single order uses 20% of the equity.

Positions are closed at the top of the grid by default, with the algorithm closing all orders at the first sell level. The exit level can be adjusted using the user interface, from the first level up to the fifth level above.

CONFIGURING THE ALGORITHM

1) Add it to the chart: Add the script to the current chart that you want to analyze.

2) Select the top of the grid: Confirm a price level with the mouse on which to fix the top of the grid.

3) Select the bottom of the grid: Confirm a price level with the mouse on which to fix the bottom of the grid.

4) Wait for the automatic creation of the grid.

USING THE ALGORITHM

Once the grid configuration process is completed, the algorithm will generate automatic backtesting.

You can add a stop loss that destroys the grid by setting the destruction price and activating the feature from the user interface. When the stop loss is activated, you can view it on the chart.

AUTOMATIC GRID BOT STRATEGY [ilovealgotrading]

OVERVIEW:

This Grid trading strategy can help you maximize your profit in a ranging sideways market with no clear direction.

INDICATOR:

We can get some money by taking advantage of the movement of the price between the range we have determined.

Short positions are opened while the price is rising, long positions are opened while the price is falling.

Therefore, there is no need to predict the trend direction.

What is different in this indicator:

I want to say thank you to © thequantscience. His GRID SPOT TRADING ALGORITHM - GRID BOT TRADING strategy helped me when I was writing my indicator.

I want to explain what I have improved:

1- Grid strategy is a type of strategy that can be traded in very short time frames and users can trade this strategy algorithmically by connecting this strategy to their own accounts with the help of API systems. For this reason, I have developed a software that can give us signals by dynamically changing the long and short messages when users are trading.

2- We can change the start and end dates of our grid bot as we want. It is necessary to use this setting when setting up automatic bots, so that previously opened transactions are not taken into account.

3 - Lot or quantity size should not be excessively small when users are taking automatic trades because exchanges have limitations, to avoid this problem, I have prevented this error by automatically rounding up to the nearest quantity size inside the software.

4 - Users can avoid excessive losses by using stop loss on this grid bot if they wish.

5 - When our price is over the range high or below the range low, our open positions are closed, if the stop button is active. We can also change which close price time frame we take as a basis from the settings.

6 -Users can set how many dollars they can enter per transaction while performing their transactions automatically.

IMPLEMENTATION DETAILS – SETTINGS:

This script allows the user to choose the highs and lows leves of our range. Our bot trades in the specified range.

1. This strategy allows us to set start and end backtest dates.

2. We can change range high and range low leves of our bot

3. IF people want to trade algorithmically with the help of this bot, there are 6 different input systems that will receive the Json codes as an alarm

4. IF the price closes above the upper line or below the lower line, all transactions will be closed. We can determine in which time frame our transactions will be stopped if the price closes outside these levels.We can adjust how our bot works by activating or turning off the Stop Loss button.

5. In this strategy, you can determine your dollar cost for per position.

6. The user can also divide the interval we have determined into 10 parts or 20 equal parts.

7. The grid is divided and colored at the interval we set. At the same time, if we don't want we can turn off colored channels.

Notes:

If you're going to connect this bot to an automatic Long and Short direction,

Don’t forget! you need to Webhook URL,

Don’t miss paste this code to your message window {{strategy.order.alert_message}}

ALSO:

Set your range below the support zones and above the resistance zones.

Don't be afraid to take a wide range, it doesn't matter if you make a little money, the important thing is that you don't lose money.

If you have any ideas what to add to my work to add more sources or make calculations cooler, suggest in DM .

GRID SPOT TRADING ALGORITHM - GRID BOT TRADING STRATEGYGRID SPOT TRADING ALGORITHM : LONG ONLY STRATEGY OPEN SOURCE

This is a long only strategy for spot assets.

HOW IT WORKS

Grid trading is a trading strategy where an investor creates a so-called "price grid". The basic idea of the strategy is to repeatedly buy at the pre-specified price and then wait for the price to rise above that level and then sell the position (and vice versa with shorting or hedging).

FEATURES

Grids: This algorithm has a total of 10 grids.

Take profit: The trader can increase or decrease the distance between the grids from the User Interface panel, the distance between one grid and another represents the take profit.

Management: The algorithm buys 10% of the capital every time the price breaks down a grid and sells during a rise to the next higher grid. The initial capital is invested in 10 sizes which represent 10% of the capital per trade.

Stop Loss: The algorithm knows no stop loss as long as it is not activated from the User Interface panel. By activating the stop loss from the User Interface panel the algorithm will insert a close condition on all trades which will be calculated from the last lower grid.

Trades: Trades are opened only if the price is within the grid. If the market leaves the grid the algorithm will not buy new positions or sell new positions.

Optimal market conditions: The favorable market for this algorithm is the sideways market.

LIMITATIONS OF THE MODEL

The trader must take into account that this is a static model. It only works perfectly well if the market is in a sideways phase and incurs heavy losses if the market takes a downward trend. The model is unusable for an uptrend. The trader must therefore carefully analyze the market where he intends to use this strategy, making sure that the price is in a sideways phase.

USES

Indispensable research and backtesting tool for those using bots for their investments. The algorithm produces a backtesting of the strategy for past history. It is used by professional traders to understand if this strategy has been profitable on a market and what parameters to use for bots using this strategy (Kucoin, Binance etc.).

If you would like to develop your own algorithm with customized conditions based on a grid strategy, please contact us.

If you need help in using this tool, please contact us without hesitation.

Intraday Grid trading exampleHello everyone,

This was a grid trading example for intraday trading.

Please be advised that every commodity have diferent kind of reaction and rate of change between periods therefore the percentages need to be adjusted acording to the commodities change %.

In order to specify the adjustment rate we add the Zig Zag in the script.

For Example ;

Last 3 days zigzag high points are %25 , %13 and %8 , the average %is about %9 therefore you have to put the adjustment ratios something like;

Z%1 = %3

Z%2 = %6

Z%3 = %9

Feel free to use the script with caution( it was not a investment advice), this was only a example of grid trading strategy on our trading platform.

Regards.

7-RSI strategyHello, I've only been trying to learn PineScript for two months on my own, here I am posting a version of the strategy for a grid bot with 20 orders, order size 5%, earlier I tried to find something similar, but could not. Perhaps others, those who, like me, are just starting to learn PineScript, will find something useful. In the process of using grid bots, I noticed that the RSI indicator is sufficient, so the strategy uses 7 RSI indicators on different timeframes, but it is not necessary to use all 7, usually 3 is enough, therefore, by default, the RSI values are set to limit so that there is no effect on the settings of others. The step between bot orders is set in the settings. The code can of course be simplified, but it's better for understanding, I think.

(IK) Grid ScriptThis is my take on a grid trading strategy. From Investopedia:

"Grid trading is most commonly associated with the foreign exchange market. Overall the technique seeks to capitalize on normal price volatility in an asset by placing buy and sell orders at certain regular intervals above and below a predefined base price."

This strategy is best used on sideways markets, without a definitive up or down major trend. Because it doesn't rely on huge vertical movement, this strategy is great for small timeframes. It only goes long. I've set initial_capital to 100 USD. default_qty_value should be your initial capital divided by your amount of grid lines. I'm also assuming a 0.1% commission per trade.

Here's the basic algorithm:

- Create a grid based on an upper-bound (strong resistance) and a lower-bound (strong support)

- Grid lines are spaced evenly between these two bounds. (I recommend anywhere between 5-10 grid lines, but this script lets you use up to 15. More gridlines = more/smaller trades)

- Identify nearest gridline above and below current price (ignoring the very closest grid line)

- If price crosses under a near gridline, buy and recalculate near gridlines

- If price crosses over a near gridline, sell and recalculate near gridlines

- Trades are entered and exited based on a FIFO system. So if price falls 3 grid lines (buy-1, buy-2, buy-3), and subsequently crosses above one grid line, only the first trade will exit (sell-1). If it falls again, it will enter a new trade (buy-4), and if it crosses above again it will sell the original second trade (sell-2). The amount of trades you can be in at once are based on the amount of grid lines you have.

This strategy has no built-in stop loss! This is not a 'set-it-and-forget-it" script. Make sure that price remains within the bounds of your grid. If prices exits above the grid, you're in the money, but you won't be making any more trades. If price exits below the grid, you're 100% staked in whatever you happen to be trading.

This script is more complicated than my last one, but should be more user friendly. Make sure to correctly set your lower-bound and upper-bound based on strong support and resistance (the default values for these are probably going to be meaningless). If you change your "Grid Quantity" (amount of grid lines) make sure to also change your 'Order Size' property under settings for proper test results (or default_qty_value in the strategy() declaration).

Grid System With Fake MartingaleThe proposed strategy is based on a grid system with a money management that tries to replicate the effect of a martingale without having to double your position size after each loss, hence the name "fake martingale". Note that a balance using this strategy is still subject to exponential decay, the risk is not minimized, as such, it would be dangerous to use this strategy.

For more information on the martingale and grid systems see:

Strategy Settings

Point determines the "grid" size and should be adjusted accordingly to the scale of the security you are applying the strategy to. Higher value would require larger price movements in order to trigger a trade, generating fewer trades as a result.

The order size determines the number of contracts/shares to purchase.

The martingale multiplier determines the factor by which the position size is multiplied after a loss, using values higher to 2 will "squarify" your balance, while a value of 1 would use a constant position sizing.

Finally, the anti-martingale parameter determines whether the strategy uses a reverse martingale or not, if set to true then the position size is multiplied after each win.

How It Works

Let's illustrate how we replicate a martingale without doubling our exposure with a simple casino example. Imagine you are playing roulette, and that you are betting on colors (black/red), your payout is 1 to 1, in the case you win, you will have your initial stake back plus a profit equal to your initial stake.

If your strategy is to recover any previous losses, you can double your stake each time you lose, once you win you will get back the previous losses plus a profit equal to your original stake, this is the martingale system. So how can we win back previous losses without having to double our stake? We could do that by doubling the payout ratio after a loss, so after a loss, we must use a payout ratio of 2:1, if we lose once again we must use a payout of 4:1...etc, our payout ratio would be subject to exponential growth instead of our stake.

Of course, the payout ratio is fixed with casino games, but in trading, we can manipulate the position of our take profit in order to replicate such effect, this is what this strategy is doing. So after a loss, we place our take profit such that a win recover our losses back plus generate a profit.

Advantages

The advantage of this approach is that unlike the martingale we don't double our position size, which instead can remain constant, this is a huge advantage as a martingale will require a significant capital in order to tank a series of losses.

Disadvantages

The main disadvantage of this method is that the price might never reach our take profit after a long losing streak, our balance would remain in the red and we couldn't do anything about it except reset the strategy.

Frictional costs are still a disadvantage, as such, we would need to place our take profits in order to account for them, while this is still better than purchasing additional shares, it minimizes the chances of the price reaching the take profit.

Conclusions

An alternative money management system replicating the effect of a martingale as been presented, we can see that such a system is far from being perfect, and it would be foolish to use it, however, it stills offer a convenient alternative to less aggressive progressive position sizing systems.

I have been receiving some messages from users criticizing me for exposing the martingale money management system, and I understand why but I can't agree, talking about it allow me to warn users against it, the grid-martingale methodology is will create more harm than anything else, the reward is only one side of the story and should always be compared against the risk, so always take a look at all the statics in a backtest.

Thanks for reading!

Shout-Out

This post was made possible thanks to my patrons:

@Happymono, @AmariMars, @kkhaial, @Nugehe, @LucF, @Nosmok, @iflostio, @DankBeans, @ecletv, @Neverstorm, @alex.crown.jr, @uk503, @xkingshotss, @vsov, @jbelka, @yatrader2, @hughza, @ganh

Grid Like StrategyIt is possible to use progressive position sizing in order to recover from past losses, a well-known position sizing system being the "martingale", which consists of doubling your position size after a loss, this allows you to recover any previous losses in a losing streak + winning an extra. This system has seen a lot of attention from the trading community (mostly from beginners), and many strategies have been designed around the martingale, one of them being "grid trading strategies".

While such strategies often shows promising results on paper, they are often subjects to many frictions during live trading that makes them totally unusable and dangerous to the trader. The motivations behind posting such a strategy isn't to glorify such systems, but rather to present the problems behind them, many users come to me with their ideas and glorious ways to make money, sometimes they present strategies using the martingale, and it is important to present the flaws of this methodology rather than blindly saying "you shouldn't use it".

Strategy Settings

Point determines the "grid" size and should be adjusted accordingly to the scale of the symbol you are applying the strategy to. Higher value would require larger price movements in order to trigger a trade, as such higher values will generate fewer trades.

The order size determines the number of contracts/shares to purchase.

The martingale multiplier determines the factor by which the position size is multiplied after a loss, using values higher to 2 will "squarify" your balance, while a value of 1 would use a constant position sizing.

Finally, the anti-martingale parameter determines whether the strategy uses a reverse martingale or not, if set to true then the position size is multiplied after any wins.

The Grid

Grid strategies are commons and do not present huge problems until we use certain position sizing methods such as the martingale. A martingale is extremely sensitive to any kind of friction (frictional costs, slippage...etc), the grid strategy aims to provide a stable and simple environment where a martingale might possibly behave well.

The goal of a simple grid strategy is to go long once the price crossover a certain level, a take profit is set at the level above the current one and stop loss is placed at the level below the current one, in a winning scenario the price reach the take profit, the position is closed and a new one is opened with the same setup. In a losing scenario, the price reaches the stop loss level, the position is closed and a short one is opened, the take profit is set at the level below the current one, and a stop loss is set at the level above the current one. Note that all levels are equally spaced.

It follows from this strategy that wins and losses should be constant over time, as such our balance would evolve in a linear fashion. This is a great setup for a martingale, as we are theoretically assured to recover all the looses in a losing streak.

Martingale - Exponential Decays - Risk/Reward

By using a martingale we double our position size (exposure) each time we lose a trade, if we look at our balance when using a martingale we see significant drawdowns, with our balance peaking down significantly. The martingale sequence is subject to exponential growth, as such using a martingale makes our balance exposed to exponential decays, that's really bad, we could basically lose all the initially invested capital in a short amount of time, it follows from this that the theoretical success of a martingale is determined by what is the maximum losing streak you can endure

Now consider how a martingale affects our risk-reward ratio, assuming unity position sizing our martingale sequence can be described by 2^(x-1) , using this formula we would get the amount of shares/contracts we need to purchase at the x trade of a losing streak, we would need to purchase 256 contracts in order to recover from a losing streak of size 9, this is enormous when you take into account that your wins are way smaller, the risk-reward ratio is totally unfair.

Of course, some users might think that a losing streak of size 9 is pretty unlikely, if the probability of winning and losing are both equal to 0.5, then the probability of 9 consecutive losses is equal to 0.5^9 , there are approximately 0.2% of chance of having such large losing streak, note however that under a ranging market such case scenario could happen, but we will see later that the length of a losing streak is not the only problem.

Other Problems

Having a capital large enough to tank 9any number of consecutive losses is not the only thing one should focus on, as we have to take into account market prices and trading dynamics, that's where the ugly part start.

Our first problem is frictional costs, one example being the spread, but this is a common problem for any strategy, however here a martingale is extra sensitive to it, if the strategy does not account for it then we will still double our positions costs but we might not recover all the losses of a losing streak, instead we would be recovering only a proportion of it, under such scenario you would be certain to lose over time.

Another problem are gaps, market price might open under a stop-loss without triggering it, and this is a big no-no.

Equity of the strategy on AMD, in a desired scenario the equity at the second arrow should have been at a higher position than the equity at the first arrow.

In order for the strategy to be more effective, we would need to trade a market that does not close, such as the cryptocurrency market. Finally, we might be affected by slippage, altho only extreme values might drastically affect our balance.

The Anti Martingale

The strategy lets you use an anti-martingale, which double the position size after a win instead of a loss, the goal here is not to recover from a losing strike but instead to profit from a potential winning streak.

Here we are exposing your balance to exponential gross but you might also lose a trade at the end a winning streak, you will generally want to reinitialize your position size after a few wins instead of waiting for the end of a streak.

Alternative

You can use other-kind of progressions for position sizing, such as a linear one, increasing your position size by a constant number each time you lose. More gentle progressions will recover a proportion of your losses in a losing streak.

You can also simulate the effect of a martingale without doubling your position size by doubling your target profit, if for example you have a 10$ profit-target/stop-loss and lose a trade, you can use a 20$ profit target to recover from the lost trade + gain a profit of 10$. While this approach does not introduce exponential decay in your balance, you are betting on the market reaching your take profits, considering the fact that you are doubling their size you are expecting market volatility to increase drastically over time, as such this approach would not be extremely effective for high losing streak.

Conclusion

You will see a lot of auto-trading strategies that are based on a grid approach, they might even use a martingale. While the backtests will look appealing, you should think twice before using such kind of strategy, remember that frictional costs will be a huge challenge for the strategy, and that it assumes that the trader has an important initial capital. We have also seen that the risk/reward ratio is theoretically the worst you can have on a strategy, having a low reward and a high risk. This does not mean that progressive position sizing is bad, but it should not be pushed to the extreme.

It is nice to note that the martingale is originally a betting system designed for casino games, which unlike trading are not subject to frictional costs, but even casino players don't use it, so why would you?

Thx for reading

CoGrid ManagementThis strategy uses grid levels determined by pivot points based on the selected time period.

It's useful for swing trading without leverage, spot trading or for Hold management.

If the price goes down we buy and if it continues to go down we keep buying improving the average price.

When the price rises above the average entry price, we sell and if it continues to rise, we continue to sell.

It works for any pair as long as Buys and Sells quantities are adjusted correctly.

In these times of great economic change, good luck to everyone 🍀