[RS]Experimental - Excess Combined Intraday VolumeEXPERIMENTAL:

Use at your discretion.

A different way to look at volume information from a time flowing perspective.

Experimental

[RS]Swing Charts V0 Trend Counter V0EXPERIMENTAL:

wave counting using swing charts, use at your own discretion.

[RS]3 Level ZigZag Semafor V0EXPERIMENTAL:

request for CharanTejaM

zigzag may be adjusted to use other methods.

zigzag repaints, use at your own discretion.

[RS]Volatility Explosive Measure V0EXPERIMENTAL:

Measures the volatility range of current price range, can help detect squeezes as well explosive moves

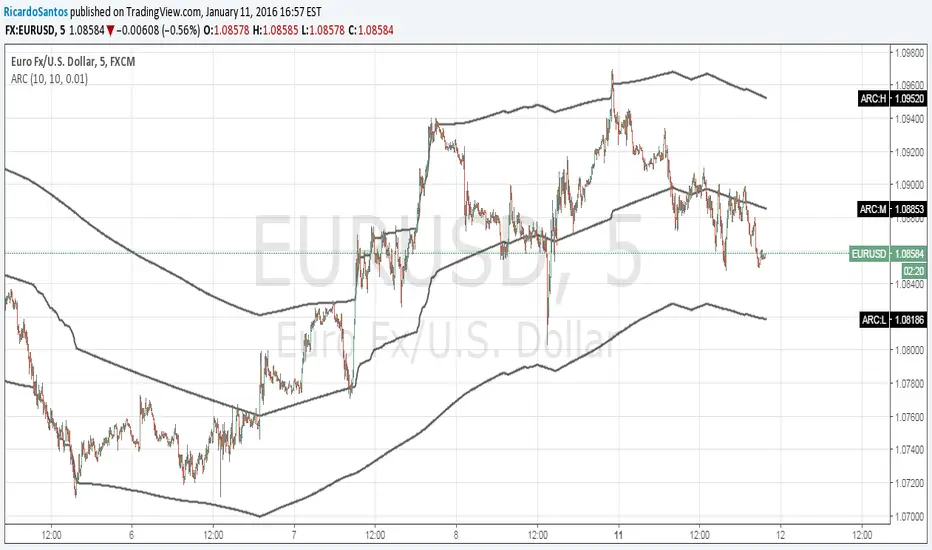

[RS]Time Based Thermal Support and Resistance V0EXPERIMENTAL:

theres a bug where certain dates dont work for the loop, returning a out of index error, please review..

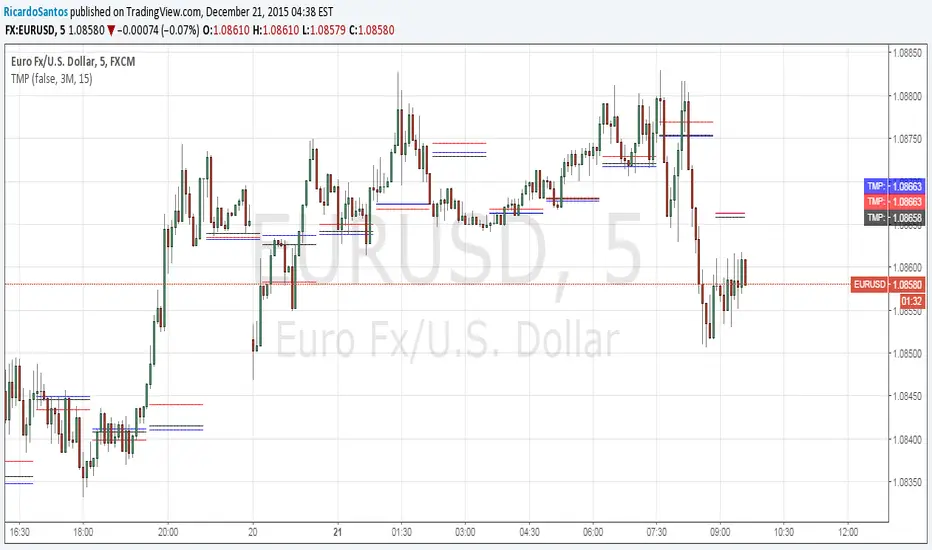

[RS]Temporal Median Price V1EXPERIMENTAL: previous custom time window median price and current time window open price in a neat package :p

(JeanLouisHardy) added option for bar count system, also added a donchian average.

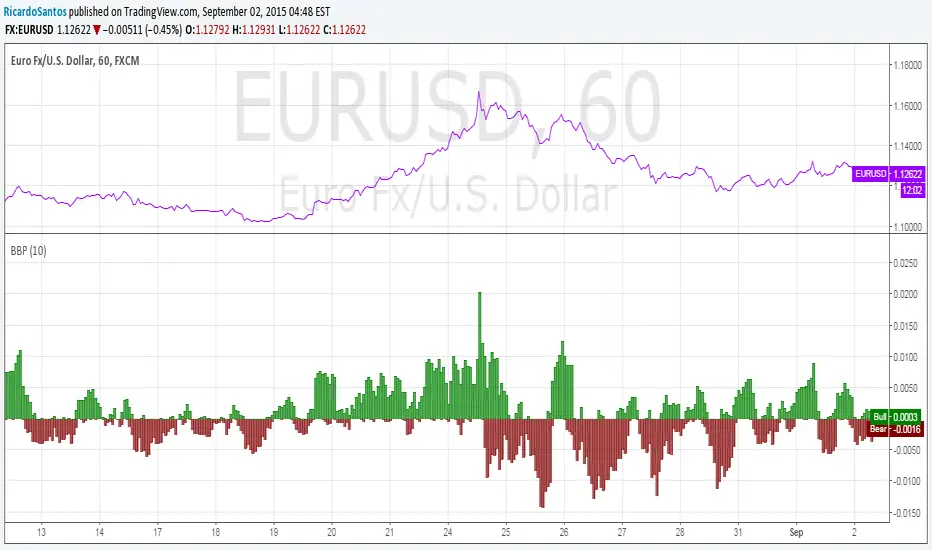

[RS]Linear Regression Bull and Bear Power Accumulation V1EXPERIMENTAL:

Bull and Bear power based on linear regression (this is a non lagging oscillator, the parameter are for the lookup window for the donchian extremes)

this indicator can also be used for convergence/divergence.

(accidentjev2) added multi timeframe support (indicator may repaint values)

[RS]Power Correlation Oscillator (EURO) V1EXPERIMENTAL:

Added Smoother avg for a better visualization of the trending strength.

[RS]Market Fractility Flow Oscillator V0EXPERIMENTAL:

same as MTF-BIAS. but slightly more practical, reads market fractality flow into a oscillator.

[RS]Linear Regression Bands V2EXPERIMENTAL:

added titles to inputs and plots for better understanding what is what(DCC)

M = middle, T = top, B = bottom, S = signal.

[RS]Linear Regression Bull and Bear Power V0EXPERIMENTAL:

Bull and Bear power based on linear regression (this is a non lagging oscillator, the parameter are for the lookup window for the donchian extremes)

this indicator can also be used for convergence/divergence.

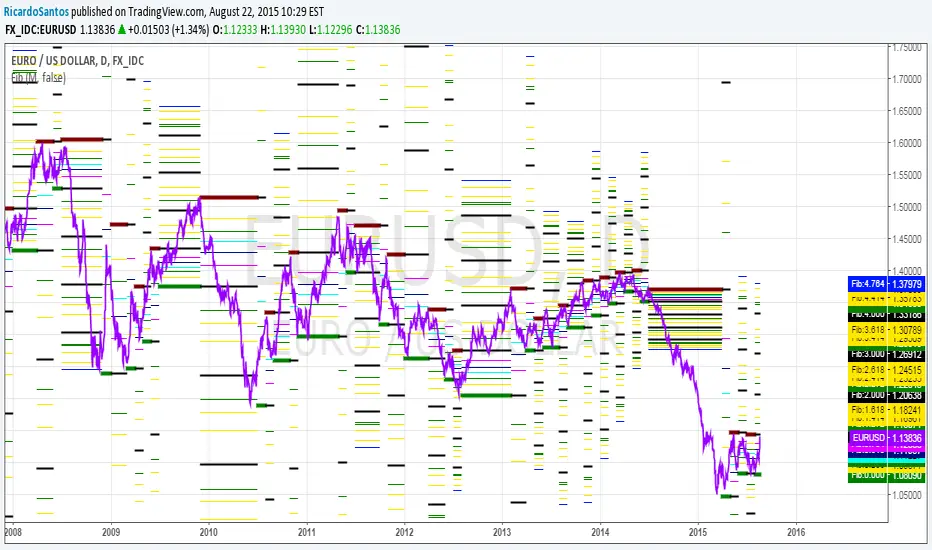

[RS]MTF Fibonacci Cycles V0EXPERIMENTAL:

Fibonacci rate levels based on price advance/decline, can be used to make visualizations of fib clusters or for cycles.

[RS]Timed Percentual Change V0EXPERIMENTAL: time based percentual change.

note: each series uses it self as base reference so there's a bit a divergence.

[RS]Neo Wave V0EXPERIMENTAL: Request for IvanLabrie.

Method for reading Neo Wave's.

note: some issues arent possible to work around/fix due to limitations in pinescript.