Delta Zones Smart Money Concept (SMC) UT Trend Reversal Mul.Sig.🚀 What's New in This Version (V5 Update)

This version is a major overhaul focused on improving trade entry timing and risk management through enhanced UT Bot functionality:

Integrated UT Trailing Stop (ATR-based): The primary trend filter and moving stop-loss mechanism is now fully integrated.

Pre-Warning Line: A revolutionary feature that alerts traders when the price penetrates a specific percentage distance (customizable) from the UT Trailing Stop before the main reversal signal fires.

"Ready" Signal: Plots a "Ready" warning label on the chart and triggers an alert condition (UT Ready Long/Short) for pre-emptive trade preparation.

V5 Compatibility: All code has been optimized for Pine Script version 5, utilizing the modern array and type structures for efficient Order Block and Breaker Block detection.

💡 How to Use This Indicator

This indicator works best when confirming signals across different components:

1. Identify the Trend Bias (UT Trailing Stop)

Uptrend: UT Trailing Stop line is Green (Focus only on Buy/Long opportunities).

Downtrend: UT Trailing Stop line is Red (Focus only on Sell/Short opportunities).

2. Prepare for Entry (Warning Line)

Action: When you see the "Ready" label or the price hits the Pre-Warning Line (Dotted Orange Line), this is your alert to prepare for a trend flip, or to tighten the stop on your current trade.

3. Confirm the Entry (Multi-Signals)

Look for a primary entry signal that aligns with the desired trend:

High-Conviction Entry: Wait for the UT Buy/Sell label (confirmed trend flip) AND a Combined Buy/Sell arrow (confirmed by your selected Oscillator settings).

High-Liquidity Entry: Look for a Delta Zone Box forming near an active Order Block or Breaker Block (SMC zones), and then confirm with a UT or Combined Signal.

4. Manage Risk (Trailing Stop)

Always set your initial Stop Loss (SL) either just outside the opposite Order Block or at the UT Trailing Stop level itself.

If the price closes back across the UT Trailing Stop, exit your position immediately, as the trend bias has officially shifted.

Features & Components

1. Delta Zones (Liquidity/Wick Pressure)

Identifies periods of extreme buying or selling pressure based on wick-to-body ratios and standard deviation analysis.

Plots colored pressure boxes (Buy/Sell) to highlight potential exhaustion points or institutional activity.

2. Smart Money Concepts (SMC)

Automatically detects and plots Order Blocks (OBs) and Breaker Blocks (BBs) based on confirmed Market Structure Breaks (MSBs).

Includes Chop Control logic to remove less reliable Breaker Blocks.

3. UT Bot Trailing Stop & Warning Line

UT Trailing Stop (ATR-based): Plots a dynamic trend line (Green/Red) that acts as a moving stop-loss and primary trend filter.

Ready/Warning Signals: Alerts traders (via the "Ready" label and orange lines) when the price enters a "Pre-Reversal Zone" near the Trailing Stop.

4. Multi-Indicator Confirmation (Filters)

Includes customizable signals based on the crossover/crossunder of RSI, CCI, and Stochastic indicators against configurable Overbought/Oversold levels.

Allows selection of combination signals (e.g., RSI & CCI, All Combined, etc.) for high-conviction entries.

Bandas y canales

Volume Spike & Second Entry (Fast Scalping)this indicator puts volume spikes on your chart which gives a good indicator of a large move

45DS v6.0 FULL FINAL1-5-15-30-60 dakıkalık zaman dlimlerinde sculp indikatörü . Başarısına inanamayacalsınız..

MA200 Parallel ChannelDynamic MA100 Parallel Bands – Precision S/R Levels

This indicator builds a clean, parallel channel around the 100-period moving average using a fixed ±4 offset.

Because the offset mirrors the short-term MA1 fluctuations, the channel reveals highly accurate support and resistance zones that react instantly to market micro-structure.

Unlike Bollinger Bands—which expand with volatility—this tool stays perfectly parallel and trend-aligned, making breakouts and pullbacks incredibly easy to spot.

How it works:

Centerline: 100-period moving average (MA100)

Upper Band: MA100 + 4

Lower Band: MA100 – 4

MA1 used as a sensitivity reference for micro-trend behavior

Parallel structure ensures stable, predictable levels

Why it’s powerful:

The ±4 channel creates extremely precise S/R zones

Price respecting the lower band = dynamic support

Price rejecting the upper band = dynamic resistance

A clean break above or below the bands highlights strong momentum shifts

Perfect for intraday traders needing structure without noise

Perfect for:

Identifying high-probability bounce levels

Spotting early trend continuation

Confirming MA100 breakouts

Filtering weak signals and fake volatility spikes

If you want razor-sharp support & resistance levels that stay consistent across all timeframes, these MA100 parallel bands deliver exceptional clarity.

MA % Deviation ChannelMA % Deviation Channel — an indicator for measuring price deviation from the moving average

MA % Deviation Channel (MA%DC) is a visual analysis tool that shows how far the current price deviates from a selected moving average, expressed in percentages. The indicator builds dynamic channels based on historical percentage deviations, helping traders identify statistical extremes and use them as potential reversal or continuation zones.

How the indicator works

MA%DC calculates the percentage deviation of High and Low from the chosen MA and stores these values in arrays. Based on the average deviation values, the script plots four key levels:

Avg. High Dev. — average deviation of highs from the MA

Avg. Low Dev. — average deviation of lows from the MA

Avg. Extreme High Dev. — extreme (above-average) deviations of highs

Avg. Extreme Low Dev. — extreme (below-average) deviations of lows

The width of the channel automatically adapts to the selected MA period — the longer the period, the deeper the historical analysis.

Purpose and use cases

MA % Deviation Channel helps:

Evaluate volatility relative to the moving average

Identify overbought and oversold zones based on real price behavior

Filter breakouts and false impulses

Build trend-following and counter-trend strategies using statistical deviations

Advantages

Based on percentage deviation rather than fixed distances

Adaptive to changing market conditions

Supports 5 popular types of moving averages

Settings

MA Source — data source for the moving average

MA Type — moving average type (SMA, EMA, WMA, VWMA, RMA)

MA Length — smoothing period

Visual elements

The moving average line

Average deviation channels

Extreme deviation channels

Color fills between levels for improved readability

Vital Wave 20-50Simplicity is almost always the most effective approach, and here I’m giving you a trend-following system that exploits the bullish bias of traditional markets and their trending nature, with very basic rules.

Rules (long entries only)

• Market entry: When the EMA 20 crosses above the EMA 50 (from below)

• Main market exit: When the EMA 20 crosses below the EMA 50 (from above)

• Fixed Stop Loss: Placed at the price level of the Lower Bollinger Band at the moment the trade is entered.

In my strategy, the primary exit is when the EMA 20 crosses below the EMA 50. However, this crossover can sometimes take a while to occur, and in the meantime the price may have already dropped significantly. The Stop Loss based on the Lower Bollinger Band is designed to limit losses in case the market moves sharply against the position without giving the bearish crossover signal in time. Having two exit conditions makes the strategy much more robust in terms of risk management.

Risk Management:

• Initial capital: $10,000

• Position size: 10% of available capital per trade

• Commissions: 0.1% on traded volume

• Stop Loss: Based on the Lower Bollinger Band

• Take Profit / Exit: When EMA 20 crosses below EMA 50

Recommended Markets:

XAUUSD (OANDA) (Daily)

Period: January 3, 1833 – November 23, 2025

Total Profit & Loss: +$6,030.62 USD (+57.57%)

Maximum Drawdown: $541.53 USD (3.83%)

Total Trades: 136

Winning Trades (Win Rate): 36.03% (49/136)

Profit Factor: 2.483

XAUUSD (OANDA) (12-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,209.56 USD (+11.89%)

Maximum Drawdown: $384.58 USD (3.61%)

Total Trades: 97

Winning Trades (Win Rate): 35.05% (34/97)

Profit Factor: 1.676

XAUUSD (OANDA) (8-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,179.36 USD (+11.81%)

Maximum Drawdown: $246.88 USD (2.32%)

Total Trades: 147

Winning Trades (Win Rate): 31.97% (47/147)

Profit Factor: 1.626

Tesla (NASDAQ) (4-hour)

Period: June 29, 2010 – November 23, 2025

Total Profit & Loss (Absolute): +$11,687.90 USD (+116.88%)

Maximum Drawdown: $922.05 USD (6.50%)

Total Trades: 68

Winning Trades (Win Rate): 39.71% (27/68)

Profit Factor: 4.156

Tesla (NASDAQ) (3-hour)

Total Profit & Loss: +$11,522.33 USD (+115.22%)

Maximum Drawdown: $1,247.60 USD (8.80%)

Total Trades: 114

Winning Trades: 33.33% (38/114)

Profit Factor: 2.811

Additional Recommendations

(These assets have shown good trending behavior with the same strategy across multiple timeframes):

• NVDA (15 min, 30 min, 1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• NFLX (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• MA (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• META (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• AAPL (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• SPY (12h, Daily)

About the Code

The user can modify:

• EMA periods (20 and 50 by default)

• Bollinger Bands length (20 periods)

• Standard deviation (2.0)

Visualization

• EMA 20: Blue line

• EMA 50: Red line

• Green background when EMA20 > EMA50 (bullish trend)

• Red background when EMA20 < EMA50 (bearish trend)

Important Note:

We can significantly increase the profit factor and overall profitability by risking a fixed percentage per trade instead of a fixed amount. This would prevent losses from fluctuating with changes in volatility.

This could be implemented by reducing position size or adjusting leverage based on the volatility percentage required for each trade, but I’m not sure if this is fully possible in Pine Script. In my other script, “ Golden Cross 50/200 EMA ,” I go deeper into this topic and provide examples.

I hope you enjoy this contribution. Best regards!

RSI Hybrid + EMA Cloud + Swings(15m/2H)RSI Hybrid + EMA Cloud (15m Trend + 2H Momentum)

A dual-timeframe trading system combining fast 15-minute trend structure with higher-timeframe 2-Hour momentum, volume and structural levels.

🧩 What This Indicator Does

This tool blends:

🔹 15m Trend (EMA Cloud) – 2 Points

EMA 7 vs 21 → Short trend

EMA 30 vs 74 → Long trend

Cloud shading highlights bullish/bearish alignment

Faster, intraday trend sensitivity

🔹 2H Momentum (RSI Hybrid) – 3 Points

RSI > 50

RSI > SMA(4)

RSI > SMA(12)

Gives short / medium / long momentum confirmation from the higher timeframe.

🔹 2H Volume Pressure – 1 Point

Volume vs 20-SMA

Mild / Moderate / Strong Bull/Bear

Confirms true participation behind price moves

⭐ Score System (0–6 Total)

Component Points

15m EMA Trend 2

2H RSI Hybrid 3

2H Volume Power 1

Total 6

Interpretation:

5–6 → High-confluence direction

3–4 → Partial confluence

1–2 → Weak bias

0 → No reliable direction

Designed for discretionary and semi-systematic intraday traders.

📊 15m Structural Levels

Includes:

✔ Last confirmed 15m Swing High / Swing Low

Based on close-price pivots, not highs/lows.

✔ Live Running High since last Swing LOW

Tracks how far price has extended upward.

✔ Live Running Low since last Swing HIGH

Tracks downward extension after a swing high.

✔ ATR(15m)

Volatility reference for SL/TP or risk modeling.

These levels help in timing entries, managing stops, and identifying breakout/breakdown zones.

🖥 On-Chart Info Table

Summarizes:

15m EMA short & long trend

2H RSI short/medium/long momentum

RSI vs 50

2H volume power

Bull & Bear score (with breakdown)

Last 15m swing highs/lows

ATR(15m)

Color-coded for clarity

💡 Why Use This Indicator

High-speed 15m trend detection

Higher-TF 2H momentum & volume confirmation

Multi-layered bias presented in a simple score

Built-in structure for more intelligent entries/exits

Works on indices, stocks, FX, crypto

Ideal for intraday traders who want speed + reliability

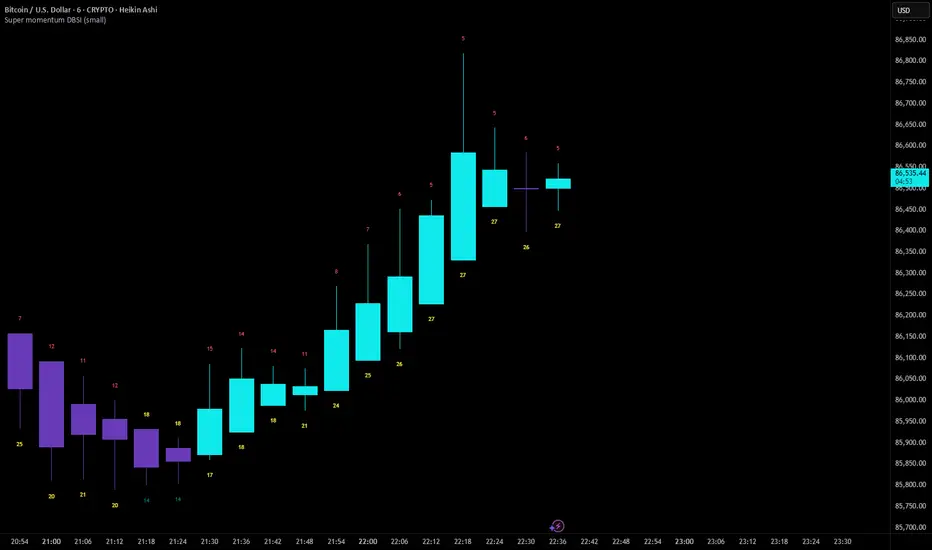

Super momentum DBSISuper momentum DBSI: The Ultimate Guide

1. What is this Indicator?

The Super momentum DBSI is a "Consensus Engine." Instead of relying on a single line (like an RSI) to tell you where the market is going, this tool calculates 33 distinct technical indicators simultaneously for every single candle.

It treats the market like a democracy. It asks 33 mathematical "voters" (Momentum, Trend, Volume, Volatility) if they are Bullish or Bearish.

If 30 out of 33 say "Buy," the score is high (Yellow), and the trend is extremely strong.

If only 15 say "Buy," the score is low (Teal), and the trend is weak or choppy.

2. Visual Guide: How to Read the Numbers

The Scores

Top Number (Bears): Represents Selling Pressure.

Bottom Number (Bulls): Represents Buying Pressure.

The Colors (The Traffic Lights)

The colors are your primary signal. They tell you who is currently winning the war.

🟡 YELLOW (Dominance):

This indicates the Winning Side.

If the Bottom Number is Yellow, Bulls are in control.

If the Top Number is Yellow, Bears are in control.

🔴 RED (Weakness):

This appears on the Top. It means Bears are present but losing.

🔵 TEAL (Weakness):

This appears on the Bottom. It means Bulls are present but losing.

3. Trading Strategy

Scenario A: The "Strong Buy" (Long Entry)

The Setup: You are looking for a shift in momentum where Buyers overwhelm Sellers.

Watch the Bottom Number: Wait for it to turn Yellow.

Confirm Strength: Ensure the score is above 15 and rising (e.g., 12 → 18 → 22).

Check the Top: The Top Number should be Red and low (below 10).

Trigger: Enter on the candle close.

Scenario B: The "Strong Sell" (Short Entry)

The Setup: You are looking for Sellers to crush the Buyers.

Watch the Top Number: Wait for it to turn Yellow.

Confirm Strength: Ensure the score is above 15 and rising.

Check the Bottom: The Bottom Number should be Teal and low.

Trigger: Enter on the candle close.

Scenario C: The "No Trade Zone" (Choppy Market)

The Setup: The market is confused.

Visual: Top is Red, Bottom is Teal.

Meaning: NOBODY IS WINNING. There is no Yellow number.

Action: Do not trade. This usually happens during lunch hours, weekends, or right before big news. This filter alone will save you from many false breakouts.

4. What is Inside? (The 33 Indicators)

To give you confidence in the signals, here is exactly what the script is checking:

Group 1: Momentum (Oscillators)

Detects if price is moving fast.

RSI (Relative Strength Index)

CCI (Commodity Channel Index)

Stochastic

Williams %R

Momentum

Rate of Change (ROC)

Ultimate Oscillator

Awesome Oscillator

True Strength Index (TSI)

Stoch RSI

TRIX

Chande Momentum Oscillator

Group 2: Trend Direction

Detects the general path of the market.

13. MACD

14. Parabolic SAR

15. SuperTrend

16. ALMA (Moving Average)

17. Aroon

18. ADX (Directional Movement)

19. Coppock Curve

20. Ichimoku Conversion Line

21. Hull Moving Average

Group 3: Price Action

Detects where price is relative to averages.

22. Price vs EMA 20

23. Price vs EMA 50

24. Price vs EMA 200

Group 4: Volume & Force

Detects if there is money behind the move.

25. Money Flow Index (MFI)

26. On Balance Volume (OBV)

27. Chaikin Money Flow (CMF)

28. VWAP (Intraday)

29. Elder Force Index

30. Ease of Movement

Group 5: Volatility

Detects if price is pushing the outer limits.

31. Bollinger Bands

32. Keltner Channels

33. Donchian Channels

5. Pro Tips for Success

Don't Catch Knives: If the Bear score (Top) is Yellow and 25+, do not try to buy the dip. Wait for the Yellow score to break.

Exit Early: If you are Long and the Yellow Bull score drops from 28 to 15 in one candle, TAKE PROFIT. The momentum has died.

Use Higher Timeframes: This indicator works best on 15m, 1H, and 4H charts. On the 1m chart, it may be too volatile.

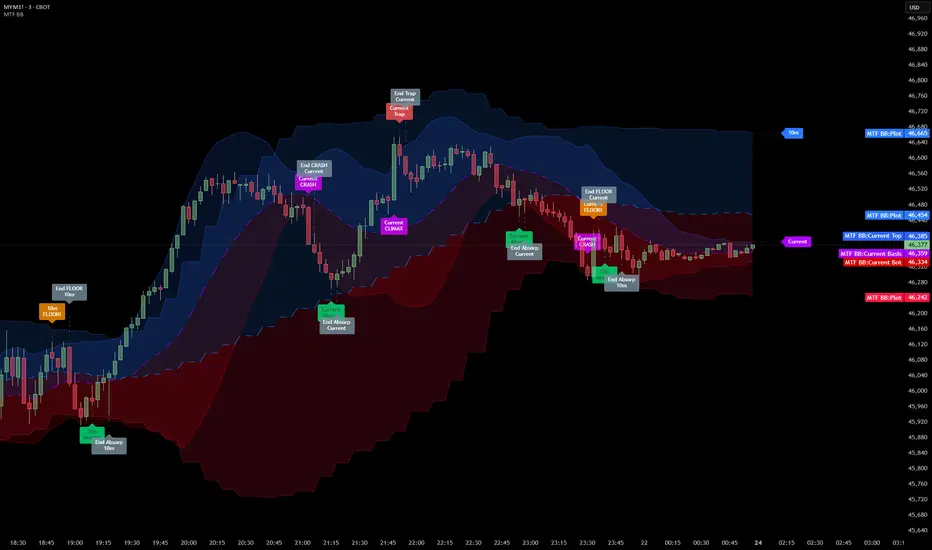

Multi Timeframe Bollinger Bands Spectrum [Ata]Multi-Timeframe Bollinger Bands Spectrum

Technical Overview

This script integrates multi-timeframe volatility analysis with volume-derived order flow estimation. By combining Bollinger Bands (statistical deviation) with internal candle volume logic, the indicator qualifies price movements to differentiate between sustained trends, reversals, and exhaustion events.

The system is designed to provide a structural context for price action, visualizing market regimes through a dual-zone spectrum and filtering signals based on the interaction between price location and specific volume thresholds.

Core Logic & Calculation

1. Volume Decomposition Algorithm

Instead of using total volume, the script estimates Buying Pressure vs. Selling Pressure based on the close position relative to the candle's High/Low range:

- Buying Volume (vb): Increases as the close approaches the High.

- Selling Volume (vs): Increases as the close approaches the Low.

This logic allows the detection of directional flow even within standard volume bars.

2. Statistical Spectrum

The indicator renders deviations from the Basis (SMA) as two distinct zones:

- Bullish Zone (Blue): Price positioning between the Basis and Upper Band.

- Bearish Zone (Red): Price positioning between the Basis and Lower Band.

This structure is applied across multiple timeframes (overlay) to visualize the macro trend context without noise.

3. Non-Repainting Execution

To ensure historical accuracy and reliability for backtesting, all higher-timeframe data is requested using "lookahead_off". Signals are confirmed only upon the closure of the respective timeframe's candle.

Signal Definitions

Signals are generated only when specific Volatility and Volume conditions intersect:

Reversal Setups (Reaction to Liquidity)

- WALL: Triggered when price rejects the Upper Band accompanied by Extreme Selling Volume (vs > Limit). This suggests active limit sell orders absorbing the rally.

- FLOOR: Triggered when price rejects the Lower Band accompanied by Extreme Buying Volume (vb > Limit). This suggests active limit buy orders absorbing the drop.

- ABSORP: Identifies absorption near the lower bands where selling pressure is met with passive buying (indicated by lower wicks and relative buy volume).

Momentum Setups (Trend Continuation)

- POWER: Validates a breakout above the Upper Band only if supported by Dominant Buying Volume and a strong candle body.

- PANIC: Validates a breakdown below the Lower Band only if supported by Dominant Selling Volume.

- TRAP: Marks failed breakouts where price exits the bands but volume analysis contradicts the move (e.g., low directional volume).

Exhaustion Setups (Statistical Extremes)

- CLIMAX/CRASH: Identifies anomalies where price deviates significantly from the mean (Extreme Deviation) or when volume reaches unsustainable levels relative to the average, often preceding a mean reversion.

Input Parameters

- Bollinger Logic: Configuration for Length and Standard Deviation Multiplier.

- Volume Thresholds: Adjustable factors for Minimum Volume (Trend) and Extreme Volume (Reversal/Climax).

- Timeframe Layers: Toggle visibility for up to 5 higher timeframes.

- Theme: Adjusts label contrast for Dark/Light backgrounds.

Disclaimer

This indicator is strictly for analytical purposes. It provides a visualization of past market data based on statistical and volumetric formulas. Users should apply their own risk management protocols.

COT Net Positions OTCCOT Net Positions Indicator Description

This is a TradingView Pine Script indicator that displays Commitment of Traders (COT) data for any trading instrument.

What it does:

Fetches COT Data - Uses the TradingView COT library to retrieve official CFTC (Commodity Futures Trading Commission) data for the current symbol

Calculates Net Positions for three trader categories:

Commercial (Blue) - Large hedging institutions; represents institutional long/short positioning

Non-Commercial (Yellow) - Large speculators and hedge funds; often considered "smart money"

Retail (Red) - Small individual traders; often considered contrarian indicators

Net Position Calculation - For each category:

Takes Long Positions minus Short Positions

Plots the result on a separate panel below the price chart

Special Symbol Handling - Includes custom mappings for specific commodities:

Copper (HG) → CFTC code 085692

Brazilian Real (LBR) → CFTC code 058644

Use Cases:

Market Bias Detection - See if institutions are mostly long or short

Contrarian Trading - When retail traders are extremely positioned one way, often the market reverses

Trend Confirmation - Non-commercial positioning often aligns with established trends

Support/Resistance - Extreme COT positions can signal market turning points

Systemic Net Liquidity (Macro Fuel for Crypto & Stocks)This indicator tracks Systemic Net Liquidity, the single most important macro factor for determining the long-term trend of risk assets like Bitcoin (BTC) and major indices (S&P 500). It measures the amount of actual cash available in the financial system to chase speculative assets, distinguishing between money that is circulating and money that is locked up at the Federal Reserve.

Mechanism (What It Measures)

The script uses direct data from the FRED (Federal Reserve Economic Data) to calculate the true state of market funding:

\text{Net Liquidity} = \text{Fed Assets (WALCL)} - \text{Treasury General Account (TGA)} - \text{Reverse Repo (RRP)}

1. Fed Assets (WALCL): The total balance sheet of the Fed (The overall supply of money).

2. Treasury General Account (TGA): Funds the US Treasury collects via bond issuance. When the TGA rises, liquidity is actively drained from the banking system (A major bearish pressure).

3. Overnight Reverse Repo (RRP): Cash parked by banks and money market funds at the Fed, effectively frozen and not contributing to market activity.

How to Interpret Signals

Treat the Net Liquidity line as the market's "Fuel Gauge":

📈 BULLISH SIGNAL (Liquidity Injection): When the Net Liquidity line is rising, money is flowing back into the system, signalling a tailwind for risk assets.

📉 BEARISH SIGNAL (Liquidity Drain): When the line is falling (often due to high TGA balances), cash is being removed. This signals major friction and pressure on price action.

⚠️ DIVERGENCE WARNING: A strong signal is generated when Price (e.g., BTC) rises, but Net Liquidity falls. This macro divergence strongly suggests a major trend reversal or correction is imminent.

Important Notes

Data Source: Data is directly sourced from FRED and updates daily/weekly. This tool is best used for macro analysis and identifying high-level cycles, not short-term scalping.

Disclaimer: Use this indicator as a confirmation tool within your broader strategy. It is not a standalone trading signal.

Systemic Net Liquidity (Macro Fuel for Crypto & Stocks)This indicator tracks Systemic Net Liquidity, the single most important macro factor for determining the long-term trend of risk assets like Bitcoin (BTC) and major indices (S&P 500). It measures the amount of actual cash available in the financial system to chase speculative assets, distinguishing between money that is circulating and money that is locked up at the Federal Reserve.

Mechanism (What It Measures)

The script uses direct data from the FRED (Federal Reserve Economic Data) to calculate the true state of market funding:

\text{Net Liquidity} = \text{Fed Assets (WALCL)} - \text{Treasury General Account (TGA)} - \text{Reverse Repo (RRP)}

1. Fed Assets (WALCL): The total balance sheet of the Fed (The overall supply of money).

2. Treasury General Account (TGA): Funds the US Treasury collects via bond issuance. When the TGA rises, liquidity is actively drained from the banking system (A major bearish pressure).

3. Overnight Reverse Repo (RRP): Cash parked by banks and money market funds at the Fed, effectively frozen and not contributing to market activity.

How to Interpret Signals

Treat the Net Liquidity line as the market's "Fuel Gauge":

📈 BULLISH SIGNAL (Liquidity Injection): When the Net Liquidity line is rising, money is flowing back into the system, signalling a tailwind for risk assets.

📉 BEARISH SIGNAL (Liquidity Drain): When the line is falling (often due to high TGA balances), cash is being removed. This signals major friction and pressure on price action.

⚠️ DIVERGENCE WARNING: A strong signal is generated when Price (e.g., BTC) rises, but Net Liquidity falls. This macro divergence strongly suggests a major trend reversal or correction is imminent.

Important Notes

Data Source: Data is directly sourced from FRED and updates daily/weekly. This tool is best used for macro analysis and identifying high-level cycles, not short-term scalping.

Disclaimer: Use this indicator as a confirmation tool within your broader strategy. It is not a standalone trading signal.

Coinbase Premium Index (Custom Tickers)📊 Coinbase Premium Index (Auto Symbol Support)

1. Overview

The Coinbase Premium Index is a widely used indicator to gauge the sentiment difference between US institutional investors (Coinbase Pro) and global retail/futures traders (Binance).

This script calculates the percentage difference between the Coinbase (USD pair) price and the Binance (USDT pair) price.

2. Key Features

🔄 Auto Symbol Matching (New): You no longer need to manually change tickers when switching charts.

If you are looking at a SOL/USDT chart, the indicator automatically detects "SOL" and compares COINBASE:SOLUSD vs BINANCE:SOLUSDT.

🛠 Manual Mode: Includes a manual override option if you wish to compare specific fixed tickers (e.g., strictly BTC).

🎨 Dynamic Visuals:

Histogram: Color-coded bars (Green/Red) indicate positive or negative premiums.

Smart Label: Displays the real-time premium value on the chart. The label color adapts to the trend, and hovering over it shows a Tooltip confirming exactly which tickers are being compared.

3. How to Interpret

The premium indicates the flow of funds and buying pressure:

🟢 Positive Premium (Green Bar):

Coinbase Price > Binance Price

Interpretation: Strong buying pressure from US institutions or spot whales. Often considered a Bullish signal.

🔴 Negative Premium (Red Bar):

Coinbase Price < Binance Price

Interpretation: Strong selling from US investors, or overheated buying in the offshore futures market (Binance). Often considered a Bearish or mean-reversion signal.

4. Settings Guide

Ticker Mode:

Auto (Current Chart): Automatically sets the comparison based on your current chart's base currency (Recommended).

Manual (Custom): Uses the specific tickers defined in the manual input fields below.

Manual Inputs: Enter tickers here if using Manual Mode (Default: COINBASE:BTCUSD vs BINANCE:BTCUSDT).

Bar & Label Settings: Customize colors, transparency, and the vertical position (Y-Offset) of the data label to fit your chart layout.

Coin Jin Multi SMA+ BB+ SMA forecast Ver2.02This script provides a complete trend-analysis system based on the

5 / 20 / 60 / 112 / 224 / 448 / 896 SMAs.

It precisely detects bullish/bearish alignment and automatically identifies

12 advanced trend-shift signals (Start, End, and Reversal).

Key Features:

● 9 SMA lines (including custom X1 & X2)

Each SMA supports custom color, width, and style (Line/Step/Circles).

● Bollinger Bands with customizable options

Fully adjustable length, source, width, style, fill transparency, and more.

● SMA Forecast (curved projection)

– Slope computed via linear regression

– Predicts up to 30 future bars

– Forced dotted style ensures visibility at all zoom levels

● 12 Advanced Trend Signals (alertcondition)

Automatically detects:

Start of full alignment (with/without SMA 896)

End of alignment

Bull ↔ Bear transitions

Perfect for momentum trading, trend-following, reversal detection, or automated alert systems.

● Labeling last value of each SMA

Each SMA prints a label such as "5", “20”, “60”, “896”, or custom lengths at the latest bar.

이 스크립트는 5 / 20 / 60 / 112 / 224 / 448 / 896 이동평균선을 기반으로

정배열·역배열 상태를 정밀하게 분석하고,

총 12가지 고급 추세 신호(시작·종료·전환) 를 자동으로 감지하는 통합 추세 분석 도구입니다.

주요 기능:

● 9개의 SMA 표시 (커스텀 X1, X2 포함)

각 SMA는 색상·굵기·형태(Line/Step/Circle)를 개별 설정할 수 있습니다.

● 볼린저밴드 표시 및 채우기 옵션

BB 길이, 소스, 타입, 두께, 투명도 등을 자유롭게 조절 가능.

● SMA Forecast (미래 방향 곡선 예측)

– 기울기 기반 선형회귀 슬로프 계산

– 곡선 형태로 미래 30봉까지 예측

– 점선(Dotted) 강제 적용으로 어떤 배율에서도 선명하게 표시

● 12가지 고급 추세 신호(alertcondition)

정배열·역배열의

Start (처음 완성될 때)

End (깨질 때)

Switch (전환)

을 모두 자동 탐지하여 트레이딩뷰 알림으로 받을 수 있음.

● SMA 마지막 가격 라벨 표시

각 SMA 끝 지점에 “5 / 20 / 60 / ... / 896” 식으로 라벨 표시.

SMA Cross + KC Breakout + ATR StopThis is the same script previously published with the exception of utilizing SMA vs EMA for those who prefer that moving average type.

VOSC+RSI Pro-Trend V22 (Bollinger Integration) [PersianDev]this is an extention of andicator volume osc and rsi

Turtle System 1 (20/10) + N-Stop + MTF Table V7.2🐢 Description: Turtle System 1 (20/10) IndicatorThis indicator implements the original trading signals of the Turtle Trading System 1 based on the classic Donchian Channels. It incorporates a historically correct, volatility-based Trailing Stop (N-Stop) and a Multi-Timeframe (MTF) status dashboard. The script is written in Pine Script v6, optimized for performance and reliability.📊 Core Logic and ParametersThe system is a pure trend-following model, utilizing the more widely known, conservative parameters of the Turtle System 1:FunctionParameterValueDescriptionEntry$\text{Donchian Breakout}$$\mathbf{20}$Buy/Sell upon breaking the 20-day High/Low.Exit (Turtle)$\text{Donchian Breakout}$$\mathbf{10}$Close the position upon breaking the 10-day Low/High.Volatility$\mathbf{N}$ (ATR Period)$\mathbf{20}$Calculation of market volatility using the Average True Range (ATR).Stop-LossMultiplier$\mathbf{2.0} BER:SETS the initial and Trailing Stop at $\mathbf{2N}$.🛠️ Key Technical Features1. Original Turtle Trailing Stop (Section 4)The stop-loss mechanism is implemented with the historically accurate Turtle Trailing Logic. The stop is not aggressively tied to the current candle's low/high, which often causes premature exits. Instead, the stop only trails in the direction of the trend, maximizing the previous stop price against the new calculated $\text{Close} \pm 2N$:$$\text{New Trailing Stop} = \text{max}(\text{Previous Stop}, \text{Close} \pm (2 \times N))$$2. Reliable Multi-Timeframe (MTF) Status (Section 6)The indicator features a robust MTF status table.Purpose: It calculates and persistently stores the Turtle System 1 status (LONG=1, SHORT=-1, FLAT=0) for various timeframes (1H, 4H, 8H, 1D, and 1W).Method: It uses global var int variables combined with request.security(), ensuring the status is accurately maintained and updated across different bars and timeframes, providing a reliable higher-timeframe context.3. VisualizationsChannels: The 20-period (Entry) and 10-period (Exit) Donchian Channels are plotted.Stop Line: The dynamic $\mathbf{2N}$ Trailing Stop is visible as a distinct line.Signals: plotshape markers indicate Entry and Exit.MTF Table: A clean, color-coded status summary is displayed in the upper right corner.