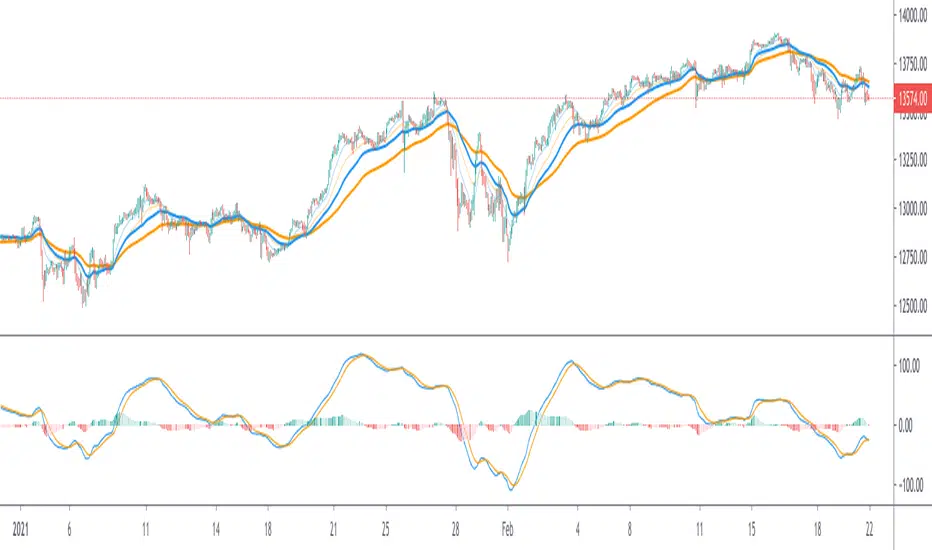

Automatic Moving AverageAutomatic moving average removes the need to set the moving average length manually. The indicator progressively finds a suitable length that minimizes the number of candle body touches and maximizes the number of wick touches.

Indicador Pine Script®