OPEN-SOURCE SCRIPT

Actualizado Kaufman's Efficiency Ratio Indicator

Kaufman Efficiency Ratio ("ER")

This ratio was developed by a systematic trader by the name of Perry J. Kaufman.

Formula

The formula is:

= A divided by B,

where:

Under default settings, closing price is used as source data, and the ER value is expressed in +ve/-ve signs (non-absolute), representing whether price had moved upward/downward over the period.

What this script does:

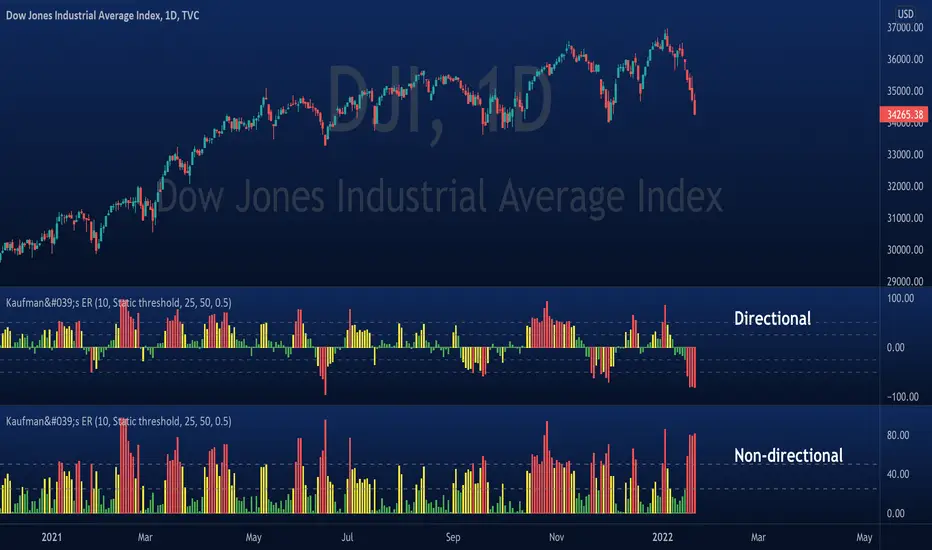

This script plots out ER and fills in the area beneath the curve with colors according to whether ER is classified as low/medium/high. There are two modes:

- Dynamic mode: low/medium/high is determined by ER value relative to it's mean +/- 'multiple' of standard deviation

- Static mode: low/medium/high is based on user defined thresholds

Applications:

- Can be used for identifying bullish moves in instances where price had already gone up steeply, but rests. If speculating that price will continually rise, then can enter during resting phase.

- Can be used to filter out choppy entry signals produced by existing trade strategies. If trying to enter during periods of consolidation, then ER should ideally be low. On the other hand, for mean reversion strategies, ER should be expected high.

This ratio was developed by a systematic trader by the name of Perry J. Kaufman.

Formula

The formula is:

= A divided by B,

where:

- A = Current closing price minus the closing price at the start of the lookback period

- B = Sum of differences between closing prices (in absolute terms) of consecutive bars over the lookback period

Under default settings, closing price is used as source data, and the ER value is expressed in +ve/-ve signs (non-absolute), representing whether price had moved upward/downward over the period.

What this script does:

This script plots out ER and fills in the area beneath the curve with colors according to whether ER is classified as low/medium/high. There are two modes:

- Dynamic mode: low/medium/high is determined by ER value relative to it's mean +/- 'multiple' of standard deviation

- Static mode: low/medium/high is based on user defined thresholds

Applications:

- Can be used for identifying bullish moves in instances where price had already gone up steeply, but rests. If speculating that price will continually rise, then can enter during resting phase.

- Can be used to filter out choppy entry signals produced by existing trade strategies. If trying to enter during periods of consolidation, then ER should ideally be low. On the other hand, for mean reversion strategies, ER should be expected high.

Notas de prensa

Can choose between three color modes: (1) Static, (2) Dynamic, and (3) No colorClarification: In Kaufman's book "Trading Systems and Methods", he compares price movements in a high noise market to the analogy of a "drunken sailor trying to walk a straight line". On the other hand, if a market displays no noise, price should be nicely trending straight. Following is an illustration of what this all means:

Notas de prensa

- switched to using histogram- added horizontal dash lines

Script de código abierto

In true TradingView spirit, the creator of this script has made it open-source, so that traders can review and verify its functionality. Kudos to the author! While you can use it for free, remember that republishing the code is subject to our House Rules.

Read Faster & Learn Anything with Coral AI! getcoralai.com//?ref=dojiemoji

Exención de responsabilidad

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.

Script de código abierto

In true TradingView spirit, the creator of this script has made it open-source, so that traders can review and verify its functionality. Kudos to the author! While you can use it for free, remember that republishing the code is subject to our House Rules.

Read Faster & Learn Anything with Coral AI! getcoralai.com//?ref=dojiemoji

Exención de responsabilidad

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.